BTEC Unit 5: Management Accounting Report for Prime Furniture Analysis

VerifiedAdded on 2022/12/28

|13

|3204

|33

Report

AI Summary

This report, prepared for Prime Furniture, a UK-based furniture manufacturer and seller, delves into the core concepts and practical applications of management accounting. The report begins with an introduction to management accounting, emphasizing its importance in enhancing profitability and sustainability through internal decision-making processes such as cost analysis, budgeting, and forecasting. It then explores various costing techniques, including absorption costing and variable costing, providing detailed calculations and income statements for both methods. The report further examines the use of standard costing, marginal costing, statistical techniques, ratio analysis, and financial statement analysis as essential tools. It also addresses budgetary control, outlining its merits and demerits, and describes planning tools like production planning, economic order, and scheduling. Finally, the report compares how companies can use management accounting to respond to financial problems, offering insights into decision-making processes and financial planning strategies. The assignment meets the requirements of a BTEC Level 4 Higher National Certificate in Business Unit 5: Management Accounting.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

P3 Costing Techniques................................................................................................................3

Planning tools used by company to combat financial problems..................................................7

P4 Budgetary Control and merits and Demerits..........................................................................8

P5 Comparison of companies to financial problems...................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

P3 Costing Techniques................................................................................................................3

Planning tools used by company to combat financial problems..................................................7

P4 Budgetary Control and merits and Demerits..........................................................................8

P5 Comparison of companies to financial problems...................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES................................................................................................................................1

INTRODUCTION

Management accounting is all about preparing reports and budgets for improving future

performance in terms of profitability and sustainability. It is a matter of internal management

where the accountant is concerned about improving processes that is internal to the organization.

Such accounting system is meant for managerial decision-making which includes, cost analysis,

budgeting, forecasting and obtaining break-even point. The present report is based on the

concept and usefulness of management accounting. The report will highlight the utility of

management accounting for Prime furniture, which is UK based organization making and selling

furnitures. This report will indicate how Prime Furniture has integrated management accounting

in their operations to improve their performance and ensure sustainability for long term. The

systems under management accounting are very useful in addressing various financial issues to

lead on the path of success.

P3 Costing Techniques

Cost: It refers to the amount paid by an organization towards obtaining raw materials for

initiating production activities, payment for machinery and technology, expenses incurred for

selling and administration activities, etc. Cost analysis is an important aspect of management

accounting as a minor variation in cost leads to a greater impact on profitability of a concern. By

obtaining cost data, managers can decide upon the requirement of external borrowings and

arranges the same in advance at the best possible terms. Costs under management accounting are

defined under the following heads:

Absorption costing: Under the method of absorption costing, all cost related to the production of

a particular product are accounted for ascertaining the cost per unit of product manufactured. The

main purpose of adopting this technique of costing is to facilitate inventory valuation. It is also

called as full costing method. It takes into consideration both direct cost of manufacturing and

fixed and variable overhead costs (Oyewo and AJIBOLADE, 2019).

Variable costing: This particular method of costing provide useful insight to management

accountant regarding the changes occurred in the profit figures due to the small changes in the

level of output. This technique bifurcates the total cost associated with the production into fixed

and variable cost. Fixed cost remains constant at different level of output while the variable cost

goes on increasing and decreasing continuously with the corresponding increasing and

Management accounting is all about preparing reports and budgets for improving future

performance in terms of profitability and sustainability. It is a matter of internal management

where the accountant is concerned about improving processes that is internal to the organization.

Such accounting system is meant for managerial decision-making which includes, cost analysis,

budgeting, forecasting and obtaining break-even point. The present report is based on the

concept and usefulness of management accounting. The report will highlight the utility of

management accounting for Prime furniture, which is UK based organization making and selling

furnitures. This report will indicate how Prime Furniture has integrated management accounting

in their operations to improve their performance and ensure sustainability for long term. The

systems under management accounting are very useful in addressing various financial issues to

lead on the path of success.

P3 Costing Techniques

Cost: It refers to the amount paid by an organization towards obtaining raw materials for

initiating production activities, payment for machinery and technology, expenses incurred for

selling and administration activities, etc. Cost analysis is an important aspect of management

accounting as a minor variation in cost leads to a greater impact on profitability of a concern. By

obtaining cost data, managers can decide upon the requirement of external borrowings and

arranges the same in advance at the best possible terms. Costs under management accounting are

defined under the following heads:

Absorption costing: Under the method of absorption costing, all cost related to the production of

a particular product are accounted for ascertaining the cost per unit of product manufactured. The

main purpose of adopting this technique of costing is to facilitate inventory valuation. It is also

called as full costing method. It takes into consideration both direct cost of manufacturing and

fixed and variable overhead costs (Oyewo and AJIBOLADE, 2019).

Variable costing: This particular method of costing provide useful insight to management

accountant regarding the changes occurred in the profit figures due to the small changes in the

level of output. This technique bifurcates the total cost associated with the production into fixed

and variable cost. Fixed cost remains constant at different level of output while the variable cost

goes on increasing and decreasing continuously with the corresponding increasing and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

decreasing of output level. There exist direct relationship between variable cost and volume of

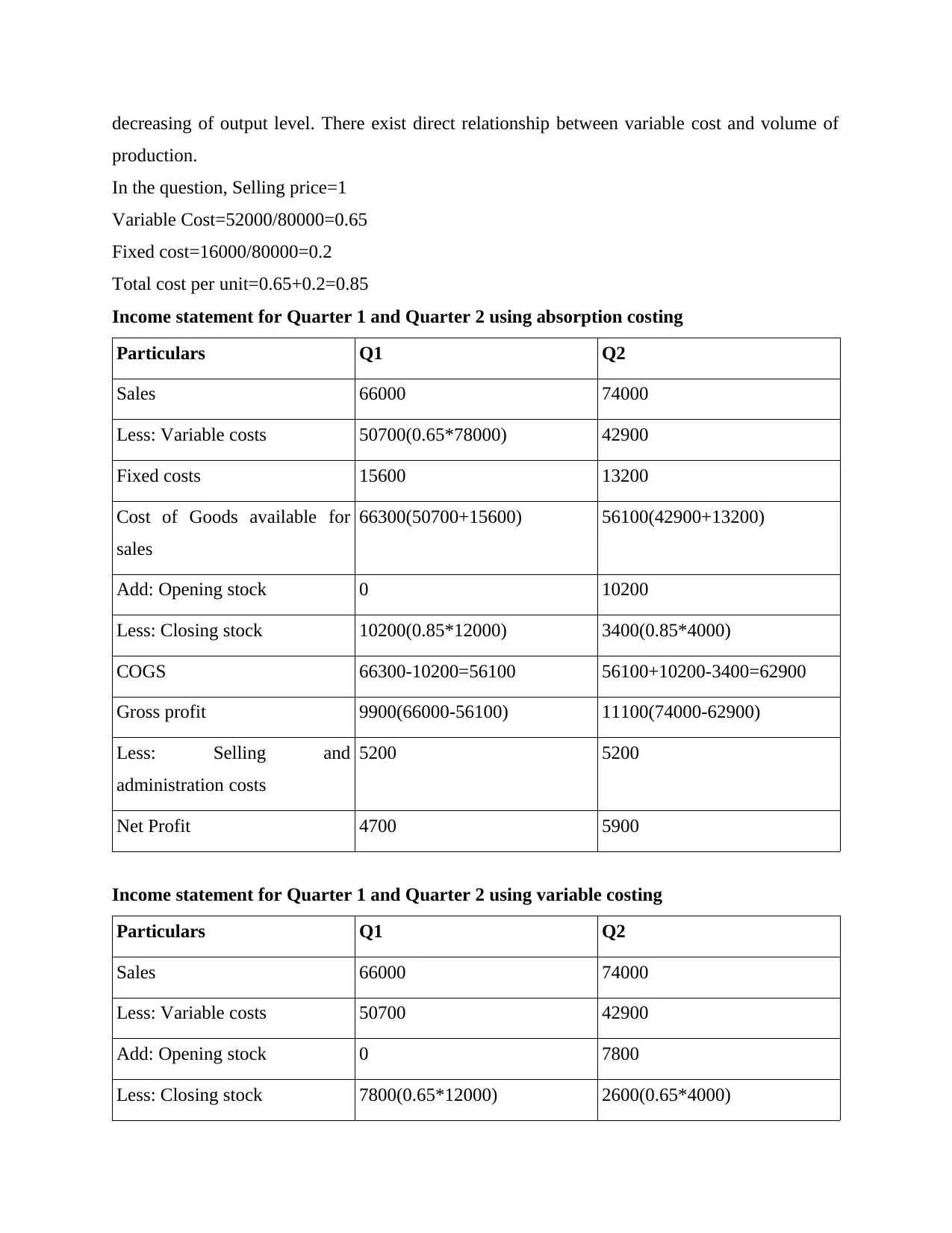

production.

In the question, Selling price=1

Variable Cost=52000/80000=0.65

Fixed cost=16000/80000=0.2

Total cost per unit=0.65+0.2=0.85

Income statement for Quarter 1 and Quarter 2 using absorption costing

Particulars Q1 Q2

Sales 66000 74000

Less: Variable costs 50700(0.65*78000) 42900

Fixed costs 15600 13200

Cost of Goods available for

sales

66300(50700+15600) 56100(42900+13200)

Add: Opening stock 0 10200

Less: Closing stock 10200(0.85*12000) 3400(0.85*4000)

COGS 66300-10200=56100 56100+10200-3400=62900

Gross profit 9900(66000-56100) 11100(74000-62900)

Less: Selling and

administration costs

5200 5200

Net Profit 4700 5900

Income statement for Quarter 1 and Quarter 2 using variable costing

Particulars Q1 Q2

Sales 66000 74000

Less: Variable costs 50700 42900

Add: Opening stock 0 7800

Less: Closing stock 7800(0.65*12000) 2600(0.65*4000)

production.

In the question, Selling price=1

Variable Cost=52000/80000=0.65

Fixed cost=16000/80000=0.2

Total cost per unit=0.65+0.2=0.85

Income statement for Quarter 1 and Quarter 2 using absorption costing

Particulars Q1 Q2

Sales 66000 74000

Less: Variable costs 50700(0.65*78000) 42900

Fixed costs 15600 13200

Cost of Goods available for

sales

66300(50700+15600) 56100(42900+13200)

Add: Opening stock 0 10200

Less: Closing stock 10200(0.85*12000) 3400(0.85*4000)

COGS 66300-10200=56100 56100+10200-3400=62900

Gross profit 9900(66000-56100) 11100(74000-62900)

Less: Selling and

administration costs

5200 5200

Net Profit 4700 5900

Income statement for Quarter 1 and Quarter 2 using variable costing

Particulars Q1 Q2

Sales 66000 74000

Less: Variable costs 50700 42900

Add: Opening stock 0 7800

Less: Closing stock 7800(0.65*12000) 2600(0.65*4000)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

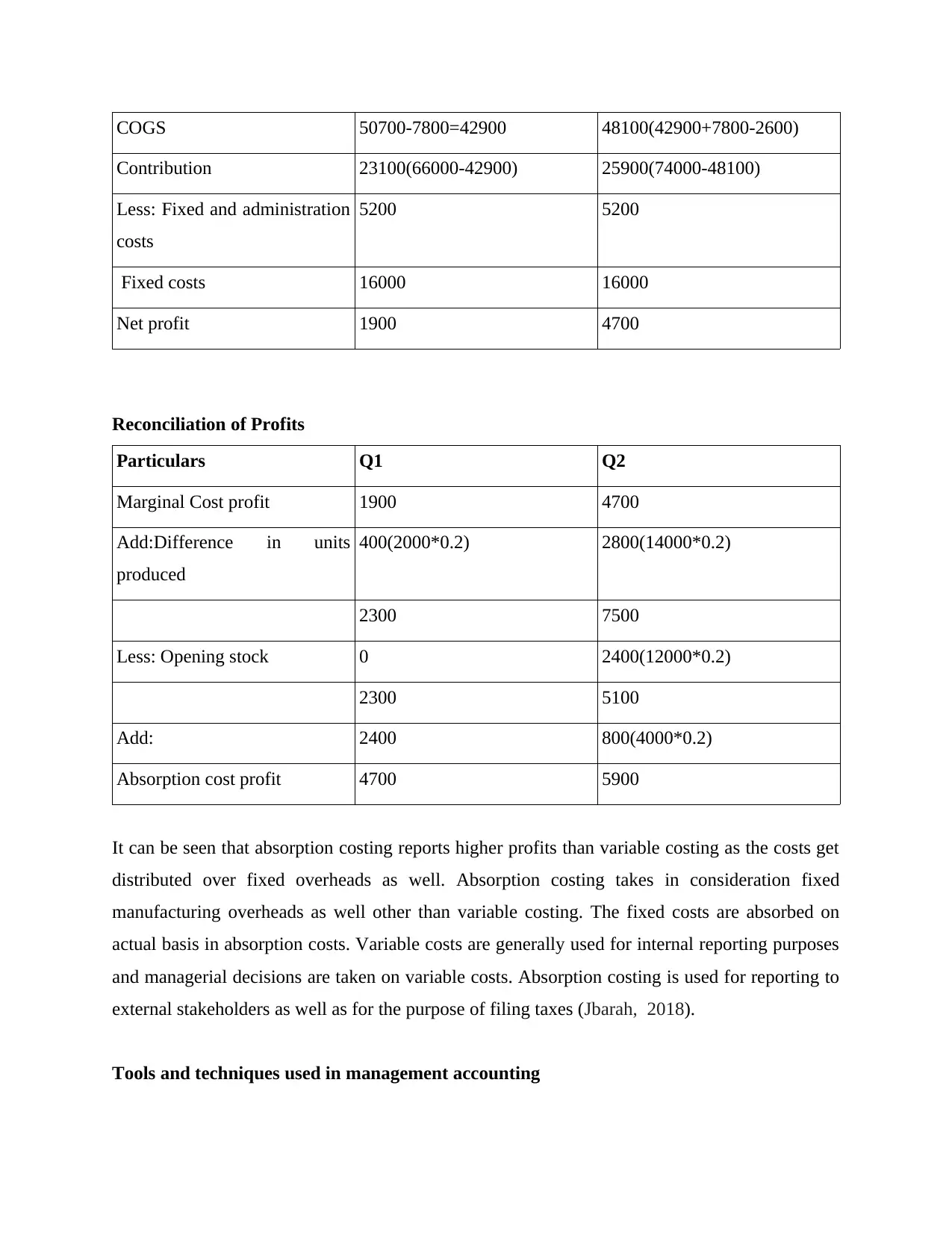

COGS 50700-7800=42900 48100(42900+7800-2600)

Contribution 23100(66000-42900) 25900(74000-48100)

Less: Fixed and administration

costs

5200 5200

Fixed costs 16000 16000

Net profit 1900 4700

Reconciliation of Profits

Particulars Q1 Q2

Marginal Cost profit 1900 4700

Add:Difference in units

produced

400(2000*0.2) 2800(14000*0.2)

2300 7500

Less: Opening stock 0 2400(12000*0.2)

2300 5100

Add: 2400 800(4000*0.2)

Absorption cost profit 4700 5900

It can be seen that absorption costing reports higher profits than variable costing as the costs get

distributed over fixed overheads as well. Absorption costing takes in consideration fixed

manufacturing overheads as well other than variable costing. The fixed costs are absorbed on

actual basis in absorption costs. Variable costs are generally used for internal reporting purposes

and managerial decisions are taken on variable costs. Absorption costing is used for reporting to

external stakeholders as well as for the purpose of filing taxes (Jbarah, 2018).

Tools and techniques used in management accounting

Contribution 23100(66000-42900) 25900(74000-48100)

Less: Fixed and administration

costs

5200 5200

Fixed costs 16000 16000

Net profit 1900 4700

Reconciliation of Profits

Particulars Q1 Q2

Marginal Cost profit 1900 4700

Add:Difference in units

produced

400(2000*0.2) 2800(14000*0.2)

2300 7500

Less: Opening stock 0 2400(12000*0.2)

2300 5100

Add: 2400 800(4000*0.2)

Absorption cost profit 4700 5900

It can be seen that absorption costing reports higher profits than variable costing as the costs get

distributed over fixed overheads as well. Absorption costing takes in consideration fixed

manufacturing overheads as well other than variable costing. The fixed costs are absorbed on

actual basis in absorption costs. Variable costs are generally used for internal reporting purposes

and managerial decisions are taken on variable costs. Absorption costing is used for reporting to

external stakeholders as well as for the purpose of filing taxes (Jbarah, 2018).

Tools and techniques used in management accounting

Standard costing: It being a predetermined cost helps Prime furniture in determining a yard

stick for measuring actual performance. Reasons for deviations are found out which managers

assess how to reduce them.

Marginal costing: Prime furniture uses the technique to fix the selling price, selection of sales

mix, best use of raw materials, to take a make or buy decision, acceptance of a bulk order by

suppliers. This is based on fixed cost, variable cost and contribution received. It has helped the

company to fix pricing over a batch of production after reaching break even on a category of

products. Overall it has helped company in realising the profits (Abdusalomova, 2019).

Statistical techniques: Prime furniture has used techniques like least square, regression and

quality control in removing the management problems. This technique has helped the company

in removal of errors and provide base for the company to look at how much progress has been

made in which section and which section requires improvement.

Ratio Analysis: It has helped management in helping out in functions like forecasting, planning,

coordination, communication and control. The physical and monetary targets which paves the

way for control of business operations have been undertaken (Usenko and et.al., 2018).

Financial Statement Analysis: The Profit and loss and Balance Sheet are the two important

financial statements which are assessed by the investors. The statements are analysed for

different period and analysis is done to know the strong and weak points of the company. It helps

to know whether the company's operational expenses are high or low,it helps to know the

company's amount of debt and receivables, lays light on variable expenses and fixed assets and

the most important the net profit for the company which is used by shareholders and investors.

Prime furniture being a new company in business lays emphasis on the financials to have clarity

for assessment purposes (Ameen, Ahmed and Abd Hafez, 2018).

Cost analysis: There are a number of costs going in production with respect to direct and

indirect costs which involve raw material, labour, and other expenses which are variable.

Through costing techniques company is able to find out the total cost of production and divide it

stick for measuring actual performance. Reasons for deviations are found out which managers

assess how to reduce them.

Marginal costing: Prime furniture uses the technique to fix the selling price, selection of sales

mix, best use of raw materials, to take a make or buy decision, acceptance of a bulk order by

suppliers. This is based on fixed cost, variable cost and contribution received. It has helped the

company to fix pricing over a batch of production after reaching break even on a category of

products. Overall it has helped company in realising the profits (Abdusalomova, 2019).

Statistical techniques: Prime furniture has used techniques like least square, regression and

quality control in removing the management problems. This technique has helped the company

in removal of errors and provide base for the company to look at how much progress has been

made in which section and which section requires improvement.

Ratio Analysis: It has helped management in helping out in functions like forecasting, planning,

coordination, communication and control. The physical and monetary targets which paves the

way for control of business operations have been undertaken (Usenko and et.al., 2018).

Financial Statement Analysis: The Profit and loss and Balance Sheet are the two important

financial statements which are assessed by the investors. The statements are analysed for

different period and analysis is done to know the strong and weak points of the company. It helps

to know whether the company's operational expenses are high or low,it helps to know the

company's amount of debt and receivables, lays light on variable expenses and fixed assets and

the most important the net profit for the company which is used by shareholders and investors.

Prime furniture being a new company in business lays emphasis on the financials to have clarity

for assessment purposes (Ameen, Ahmed and Abd Hafez, 2018).

Cost analysis: There are a number of costs going in production with respect to direct and

indirect costs which involve raw material, labour, and other expenses which are variable.

Through costing techniques company is able to find out the total cost of production and divide it

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

by the total number of units produced. It helps in ascertaining the cost per unit of production and

also the pricing is then decided per unit. This has helped Prime Furniture to also assess on the

costs which can be reduced like switching to a low cost tender supplier which is providing same

quality of raw material.

Budgetary Control

The management uses budgetary tool for controlling and planning of allotment of resources

which control the activities of business. It is an important technique of directing business

operations in which the business is able to receive a return on investment. This is also an exercise

which helps improve communication between different sections of the organisation and help

achieve a common goal (Rikhardsson and Yigitbasioglu, 2018).

Decision making: Prime Furniture gets help in evaluating business decisions which may involve

big investment costs. Techniques like NPV and IRR have helped the company in choosing

between projects as to which project will be giving better returns considering the time value of

money aspect in mind. The company has also benefited through the management accounting

techniques while making purchase for the company in terms of raw material from suppliers and

purchase of fixed assets as to what type of financing company should take; whether it should be

done through company's own capital or using leverage methods like debt. The balance of equity

and debt is also reflected in management accounting as to recommending a fixed proportion of

debt and equity to be maintained.

Planning tools used by company to combat financial problems

In today's technical era, companies are taking help of software to help record payments, bills,

salaries. Prime furniture uses technology to record its payments and receivables. The planning

which company does is:

a) Production Planning: Company is taking help in this area with advanced software which

aids in production planning and control. Managers and Planners use pertinent data from

any of the stages in manufacturing process, machine capacity and availability, worker

skill sets and orders received.

also the pricing is then decided per unit. This has helped Prime Furniture to also assess on the

costs which can be reduced like switching to a low cost tender supplier which is providing same

quality of raw material.

Budgetary Control

The management uses budgetary tool for controlling and planning of allotment of resources

which control the activities of business. It is an important technique of directing business

operations in which the business is able to receive a return on investment. This is also an exercise

which helps improve communication between different sections of the organisation and help

achieve a common goal (Rikhardsson and Yigitbasioglu, 2018).

Decision making: Prime Furniture gets help in evaluating business decisions which may involve

big investment costs. Techniques like NPV and IRR have helped the company in choosing

between projects as to which project will be giving better returns considering the time value of

money aspect in mind. The company has also benefited through the management accounting

techniques while making purchase for the company in terms of raw material from suppliers and

purchase of fixed assets as to what type of financing company should take; whether it should be

done through company's own capital or using leverage methods like debt. The balance of equity

and debt is also reflected in management accounting as to recommending a fixed proportion of

debt and equity to be maintained.

Planning tools used by company to combat financial problems

In today's technical era, companies are taking help of software to help record payments, bills,

salaries. Prime furniture uses technology to record its payments and receivables. The planning

which company does is:

a) Production Planning: Company is taking help in this area with advanced software which

aids in production planning and control. Managers and Planners use pertinent data from

any of the stages in manufacturing process, machine capacity and availability, worker

skill sets and orders received.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

b) Economic Order: Company gets help in inventory management through management

accounting methods and is able to order the exact quantity required without any wastage

of ordering more or getting less in stock (Jbarah, 2018).

c) Scheduling: With help of scheduling system company is able to build a lean process.

Managers are able to input data as and when required and assess improvement with input

of new data. This way they are also able to balance demand with supply.

P4 Budgetary Control and merits and Demerits

The budgetary control is an exercise of allotting capital for operations and it is done on

estimates of previous years capital allotment in various sections of the organization. The budget

allocation done based on previous financial may suit the system and sometimes, it may go wrong

considering changes in organization structure and market factors.

Budgetary control begin from preparation of budgets for the future, and after doing so the

management accountant on completing their objective as planned accordingly carry out the

report in order to identify what are the major deviations in performance. Such control through

preparing budget leads to minimization of major deviations in performance and helps in

matching actual performance with that of planned performance. The budgets help in achieving

objectives with a greater ease. A possible control system can be established within organization

to control variations and eliminating wasteful activities. Each individual within organization

know what is expected from them and what are the standards against which their performance

are going to be compared (Vakhrushina and et.al., 2018).

The advantages of budgetary control are:

Provide plan: It provides the plans for achieving organizational objectives. It helps in deciding

early on what is to be done and checking on the expenses and estimating the sources of funds.

accounting methods and is able to order the exact quantity required without any wastage

of ordering more or getting less in stock (Jbarah, 2018).

c) Scheduling: With help of scheduling system company is able to build a lean process.

Managers are able to input data as and when required and assess improvement with input

of new data. This way they are also able to balance demand with supply.

P4 Budgetary Control and merits and Demerits

The budgetary control is an exercise of allotting capital for operations and it is done on

estimates of previous years capital allotment in various sections of the organization. The budget

allocation done based on previous financial may suit the system and sometimes, it may go wrong

considering changes in organization structure and market factors.

Budgetary control begin from preparation of budgets for the future, and after doing so the

management accountant on completing their objective as planned accordingly carry out the

report in order to identify what are the major deviations in performance. Such control through

preparing budget leads to minimization of major deviations in performance and helps in

matching actual performance with that of planned performance. The budgets help in achieving

objectives with a greater ease. A possible control system can be established within organization

to control variations and eliminating wasteful activities. Each individual within organization

know what is expected from them and what are the standards against which their performance

are going to be compared (Vakhrushina and et.al., 2018).

The advantages of budgetary control are:

Provide plan: It provides the plans for achieving organizational objectives. It helps in deciding

early on what is to be done and checking on the expenses and estimating the sources of funds.

Coordination: It focuses on having coordination with departments or divisions of a business

organization. The committee decides roles and responsibilities for departments and

communicates with them.

Variance analysis: It helps in knowing which departments have been able to follow the budget

constraints and which departments have exceeded them. This helps in knowing which

departments have performed optimally and for whom measures need to be taken (O’Grady,

Akroyd and Scott, 2017).

Measures performance: It helps in measuring the performance of various departments by

providing comparison tools. It finds out the factors which are deviating the budget standards set.

Cost control: A planning done with budgeting helps in controlling the costs which can go

unnecessary if not made with a planned budget. All divisions are accordingly instructed to make

expenditure go within the planned budget.

Maximization of profit: It aims at enhancing the efficiency of the organisation resources with

elimination of additional costs. By monitoring the performance of all divisions necessary steps

are taken to increase the productivity.

Disadvantages of Budgetary Control

The disadvantages are as follows:

Inaccuracies in Estimates: The budgets are framed for future events which require calculations.

It may also happen that due to changing market factors, the estimates may go wrong. The

requirements may go high than set for various divisions (Vakhrushina and et.al., 2018).

Expensive process: It is expensive to make the budget as each division is to be kept in

consideration with various categories to be evaluated. In doing research and forecasting it

requires heavy expenditure.

organization. The committee decides roles and responsibilities for departments and

communicates with them.

Variance analysis: It helps in knowing which departments have been able to follow the budget

constraints and which departments have exceeded them. This helps in knowing which

departments have performed optimally and for whom measures need to be taken (O’Grady,

Akroyd and Scott, 2017).

Measures performance: It helps in measuring the performance of various departments by

providing comparison tools. It finds out the factors which are deviating the budget standards set.

Cost control: A planning done with budgeting helps in controlling the costs which can go

unnecessary if not made with a planned budget. All divisions are accordingly instructed to make

expenditure go within the planned budget.

Maximization of profit: It aims at enhancing the efficiency of the organisation resources with

elimination of additional costs. By monitoring the performance of all divisions necessary steps

are taken to increase the productivity.

Disadvantages of Budgetary Control

The disadvantages are as follows:

Inaccuracies in Estimates: The budgets are framed for future events which require calculations.

It may also happen that due to changing market factors, the estimates may go wrong. The

requirements may go high than set for various divisions (Vakhrushina and et.al., 2018).

Expensive process: It is expensive to make the budget as each division is to be kept in

consideration with various categories to be evaluated. In doing research and forecasting it

requires heavy expenditure.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Revision at times: It requires revision of the budget made in between as per the changing

circumstances faced by the organisation. It thus requires attention regularly and takes time out of

the daily routine (O’Grady, Akroyd and Scott, 2017).

Time consuming: Budget requires time to make and minute details have to be given to make it

accurate and precise. The ongoing demand for various departments have to be taken in

consideration and have to take various product categories in consideration. Thus it is time

consuming process.

P5 Comparison of companies to financial problems

Costing analysis

Capital Joinery has used costing techniques to find out its overall cost of production. There are a

lot of direct and indirect costs involved like procurement of raw materials, labor and other. All

these costs are computed per unit and then a profit margin is set up on products. The costing thus

helps company in calculation of costs as well as ways to reduce variable costs and realize profit

margin.

Prime furniture has a wide variety of products and thus has several variable costs

attached. Costing analysis helps in computation of costs and of cost cutting measures to realize a

different alternative for process (Usenko and et.al., 2018).

Financial Planning

Prime furniture has been able to plan financially for its sub departments and got help in allotting

of budget with help of tools like variance analysis etc. It helps in determining the short term and

long term obligations of the company. It has helped the company in developing financial policies

and procedures to achieve those objectives.

Capital Joinery has benefited from financial planning in terms of maximizing return on

capital employed. It has helped in managing the sources of funds, help in determination and

distribution of income to shareholders in the form of dividends.

Financial Analysis

Prime furniture has been able to judge its future earnings, ability to pay interest on securities and

solvency of the firm in period of crisis. The company has been able to judge its account

circumstances faced by the organisation. It thus requires attention regularly and takes time out of

the daily routine (O’Grady, Akroyd and Scott, 2017).

Time consuming: Budget requires time to make and minute details have to be given to make it

accurate and precise. The ongoing demand for various departments have to be taken in

consideration and have to take various product categories in consideration. Thus it is time

consuming process.

P5 Comparison of companies to financial problems

Costing analysis

Capital Joinery has used costing techniques to find out its overall cost of production. There are a

lot of direct and indirect costs involved like procurement of raw materials, labor and other. All

these costs are computed per unit and then a profit margin is set up on products. The costing thus

helps company in calculation of costs as well as ways to reduce variable costs and realize profit

margin.

Prime furniture has a wide variety of products and thus has several variable costs

attached. Costing analysis helps in computation of costs and of cost cutting measures to realize a

different alternative for process (Usenko and et.al., 2018).

Financial Planning

Prime furniture has been able to plan financially for its sub departments and got help in allotting

of budget with help of tools like variance analysis etc. It helps in determining the short term and

long term obligations of the company. It has helped the company in developing financial policies

and procedures to achieve those objectives.

Capital Joinery has benefited from financial planning in terms of maximizing return on

capital employed. It has helped in managing the sources of funds, help in determination and

distribution of income to shareholders in the form of dividends.

Financial Analysis

Prime furniture has been able to judge its future earnings, ability to pay interest on securities and

solvency of the firm in period of crisis. The company has been able to judge its account

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

receivables and accordingly work on its credit policy. The analysis helps company know which

ratios to work on to bring further investment.

Capital Joinery has made use of financial ratios like activity ratios to judge its working

capital efficiency and accordingly plan an increase in current assets. It has made company aware

of future credit risks and do a forecast in earnings to announce dividend policy (Sedevich-Fons,

2018).

Funds flow and cash flow analysis

Prime furniture uses techniques of funds flow in order to analyse the changes in the financial

position between two terms. It has helped identify for the company sources of funds and which

funds can be increased through use of fixed assets.

Capital Joinery deals with many suppliers and creditors. The analysis has helped the

company estimate cash flows in its future projects showing the profitability aspect in the jobs

undertaken. Cash expenditures thus have been able to channelise by the company and save costs.

CONCLUSION

It can be concluded that management accounting is a very important aspect for planning and

decision-making. It helps not only in saving costs for the company but also in realising profits

and doing investment analysis for the company. Management accounting helps managers in

allotment of finance and use surplus wherever necessary in operations.

ratios to work on to bring further investment.

Capital Joinery has made use of financial ratios like activity ratios to judge its working

capital efficiency and accordingly plan an increase in current assets. It has made company aware

of future credit risks and do a forecast in earnings to announce dividend policy (Sedevich-Fons,

2018).

Funds flow and cash flow analysis

Prime furniture uses techniques of funds flow in order to analyse the changes in the financial

position between two terms. It has helped identify for the company sources of funds and which

funds can be increased through use of fixed assets.

Capital Joinery deals with many suppliers and creditors. The analysis has helped the

company estimate cash flows in its future projects showing the profitability aspect in the jobs

undertaken. Cash expenditures thus have been able to channelise by the company and save costs.

CONCLUSION

It can be concluded that management accounting is a very important aspect for planning and

decision-making. It helps not only in saving costs for the company but also in realising profits

and doing investment analysis for the company. Management accounting helps managers in

allotment of finance and use surplus wherever necessary in operations.

REFERENCES

Books and journals

Abdusalomova, N., 2019. PROBLEMS OF MANAGEMENT ACCOUNTING AND WAYS TO

SOLVE THEM. International Finance and Accounting. 2019(3).p.2.

Ameen, A.M., Ahmed, M.F. and Abd Hafez, M.A., 2018. The Impact of Management

Accounting and How It Can Be Implemented into the Organizational Culture. Dutch

Journal of Finance and Management. 2(1). p.02.

Rikhardsson, P. and Yigitbasioglu, O., 2018. Business intelligence & analytics in management

accounting research: Status and future focus. International Journal of Accounting

Information Systems. 29. pp.37-58.

Oyewo, B. and AJIBOLADE, S., 2019. Does the use of strategic management accounting

techniques creates and sustains competitive advantage? Some empirical

evidence. Annals of Spiru Haret University. Economic Series. 19(2). pp.61-91.

Jbarah, S.S., 2018. The impact of strategic management accounting techniques in taking

investment decisions in the jordanian industrial companies. International Business

Research. 11(1). pp.145-156.

Rasyid, A., Sugiarto, E. and Kosasih, W., 2017. Management accounting techniques and

corporate performance of manufacturing industries. Risk Governance & Control:

Financial Markets & Institutions. 7 (2). pp.116-122.

Vakhrushina, M.A. and et.al., 2018. Integrated management accounting in the financial

management system. Research Journal of Pharmaceutical, Biological and Chemical

Sciences. 9(3). pp.808-813.

O’Grady, W., Akroyd, C. and Scott, I., 2017. Beyond budgeting: distinguishing modes of

adaptive performance management. In Advances in management accounting. Emerald

Publishing Limited.

Usenko, L.N. and et.al., 2018. Formation of an integrated accounting and analytical management

system for value analysis purposes.

Sedevich-Fons, L., 2018. Linking strategic management accounting and quality management

systems. Business Process Management Journal.

1

Books and journals

Abdusalomova, N., 2019. PROBLEMS OF MANAGEMENT ACCOUNTING AND WAYS TO

SOLVE THEM. International Finance and Accounting. 2019(3).p.2.

Ameen, A.M., Ahmed, M.F. and Abd Hafez, M.A., 2018. The Impact of Management

Accounting and How It Can Be Implemented into the Organizational Culture. Dutch

Journal of Finance and Management. 2(1). p.02.

Rikhardsson, P. and Yigitbasioglu, O., 2018. Business intelligence & analytics in management

accounting research: Status and future focus. International Journal of Accounting

Information Systems. 29. pp.37-58.

Oyewo, B. and AJIBOLADE, S., 2019. Does the use of strategic management accounting

techniques creates and sustains competitive advantage? Some empirical

evidence. Annals of Spiru Haret University. Economic Series. 19(2). pp.61-91.

Jbarah, S.S., 2018. The impact of strategic management accounting techniques in taking

investment decisions in the jordanian industrial companies. International Business

Research. 11(1). pp.145-156.

Rasyid, A., Sugiarto, E. and Kosasih, W., 2017. Management accounting techniques and

corporate performance of manufacturing industries. Risk Governance & Control:

Financial Markets & Institutions. 7 (2). pp.116-122.

Vakhrushina, M.A. and et.al., 2018. Integrated management accounting in the financial

management system. Research Journal of Pharmaceutical, Biological and Chemical

Sciences. 9(3). pp.808-813.

O’Grady, W., Akroyd, C. and Scott, I., 2017. Beyond budgeting: distinguishing modes of

adaptive performance management. In Advances in management accounting. Emerald

Publishing Limited.

Usenko, L.N. and et.al., 2018. Formation of an integrated accounting and analytical management

system for value analysis purposes.

Sedevich-Fons, L., 2018. Linking strategic management accounting and quality management

systems. Business Process Management Journal.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.