Management Accounting: Systems, Costs, and Financial Problems Report

VerifiedAdded on 2020/11/12

|13

|3498

|176

Report

AI Summary

This report provides a comprehensive overview of management accounting, exploring its fundamentals, various systems, and reporting methods. It delves into cost accounting systems, inventory management, and job-costing systems, highlighting their significance in financial planning and decision-...

MANAGEMENT

ACCOUNTING

1

ACCOUNTING

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

LO 1.................................................................................................................................................3

P.1. Management Accounting and Different types of Management accounting Systems...........3

P2. Methods used for Management Accounting Reporting.........................................................4

LO.2.................................................................................................................................................5

P.3. Prepare an income statement using marginal and absorption costs.....................................5

LO.3.................................................................................................................................................7

P.4.Advantages and Disadvantages of different types of planning tools used for budgetary

control..........................................................................................................................................7

P.5.Management Accounting Systems helps to respond to Financial Problems.........................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

Books and Journals....................................................................................................................12

2

INTRODUCTION...........................................................................................................................3

LO 1.................................................................................................................................................3

P.1. Management Accounting and Different types of Management accounting Systems...........3

P2. Methods used for Management Accounting Reporting.........................................................4

LO.2.................................................................................................................................................5

P.3. Prepare an income statement using marginal and absorption costs.....................................5

LO.3.................................................................................................................................................7

P.4.Advantages and Disadvantages of different types of planning tools used for budgetary

control..........................................................................................................................................7

P.5.Management Accounting Systems helps to respond to Financial Problems.........................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

Books and Journals....................................................................................................................12

2

INTRODUCTION

Management accounting is the system which helps managers in making plans, policies

and strategies; it aids in decision-making process. This practice of management is applied to a

wider organisational context. It is a vast concept that includes important accounting practice

within it which guides and directs the managers. In this report we will discuss about the

importance and fundamentals of management accounting, different tools and techniques,

common costing systems like, job costing, absorption cost and the way managers resolve

financial issues with the use of management accounting system.

LO 1

P.1. Management Accounting and Different types of Management accounting Systems

The accounting system which analyse the cost incurred in business and prepare financial

reports that aids managers with the relevant information. It assists in planning and formulation of

business strategies which enables to achieve goals and objectives of organisation. The origin of

management accounting system helps the managers to forecast about future and enables in

understanding performance variances. There are no set principles, but according to role it plays

here are few accepted principles. These are, Management by exception, utilisation of resources

of company and Integration. These principles help in decision making process, internal

management, maintain customer value, etc, that are needed to be fulfilled objectives of

organisation.

Management accounting is a vast concept that differs from financial accounting system.

Information provided is used by internal management, which may not be audited and focus on

future trends. Whereas, the financial accounting focuses over past data and follows generally

accepted principles as well as information is audited (Chiwamit, Modell and Scapens, 2017).

Types of Management Accounting Systems Cost-accounting systems: It refers to system which tracks down the inventory as it goes

down various stages of production within organisation. It is generally meant for

manufactures. This system helps management to maintain required inventory and thus,

reduce the cost of warehouse and security.

3

Management accounting is the system which helps managers in making plans, policies

and strategies; it aids in decision-making process. This practice of management is applied to a

wider organisational context. It is a vast concept that includes important accounting practice

within it which guides and directs the managers. In this report we will discuss about the

importance and fundamentals of management accounting, different tools and techniques,

common costing systems like, job costing, absorption cost and the way managers resolve

financial issues with the use of management accounting system.

LO 1

P.1. Management Accounting and Different types of Management accounting Systems

The accounting system which analyse the cost incurred in business and prepare financial

reports that aids managers with the relevant information. It assists in planning and formulation of

business strategies which enables to achieve goals and objectives of organisation. The origin of

management accounting system helps the managers to forecast about future and enables in

understanding performance variances. There are no set principles, but according to role it plays

here are few accepted principles. These are, Management by exception, utilisation of resources

of company and Integration. These principles help in decision making process, internal

management, maintain customer value, etc, that are needed to be fulfilled objectives of

organisation.

Management accounting is a vast concept that differs from financial accounting system.

Information provided is used by internal management, which may not be audited and focus on

future trends. Whereas, the financial accounting focuses over past data and follows generally

accepted principles as well as information is audited (Chiwamit, Modell and Scapens, 2017).

Types of Management Accounting Systems Cost-accounting systems: It refers to system which tracks down the inventory as it goes

down various stages of production within organisation. It is generally meant for

manufactures. This system helps management to maintain required inventory and thus,

reduce the cost of warehouse and security.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory management systems: In this system, the goods or inventory manage business

operations to the entire supply chains. It varies from business to enterprise and depends upon

the size and nature of business. It helps managers to make effective decision and investment. Job-costing systems: The managers can calculate cost of each job within organisation. Job-

costing system helps managers to know the amount of cost incurred on each job. This is a

relevant costing system that helps in maintaining data which is useful for business operations.

It is useful in construction business while making a particular batch of products (Goddard

and Simm, 2017).

Price optimising systems: It is used to determine the reaction of consumers in relation to

different prices of products/services provided by company through different channels. This

enables managers to choose the price that will meet all its objectives.

Difference between management accounting and financial accounting

Management accounting Financial accounting

It helps in providing key information within

the organization.

It helps in providing information to people

outside the organization, particularly

stakeholders.

It is an optional aspect that can be initiated

based on will of the management.

It is mandatory for the organization to present

its financial accounting reports

It generally focus on future regulations It generally focuses on past transactions

P2. Methods used for Management Accounting Reporting

There are various types of reports prepared by management to know about the internal

issues and to get relevant information about them. They are: Performance report: The report is meant to understand overall performance of company.

It focuses over each employee within organisation. These are relevant reports as they help

management to make strategic decision and provide deep insight in working of company. Budget: They are prepared by every organisation whether it is a small business or large.

Department wise budgets are made in big companies. These budgets help to measure the

actual performance with set standards.

4

operations to the entire supply chains. It varies from business to enterprise and depends upon

the size and nature of business. It helps managers to make effective decision and investment. Job-costing systems: The managers can calculate cost of each job within organisation. Job-

costing system helps managers to know the amount of cost incurred on each job. This is a

relevant costing system that helps in maintaining data which is useful for business operations.

It is useful in construction business while making a particular batch of products (Goddard

and Simm, 2017).

Price optimising systems: It is used to determine the reaction of consumers in relation to

different prices of products/services provided by company through different channels. This

enables managers to choose the price that will meet all its objectives.

Difference between management accounting and financial accounting

Management accounting Financial accounting

It helps in providing key information within

the organization.

It helps in providing information to people

outside the organization, particularly

stakeholders.

It is an optional aspect that can be initiated

based on will of the management.

It is mandatory for the organization to present

its financial accounting reports

It generally focus on future regulations It generally focuses on past transactions

P2. Methods used for Management Accounting Reporting

There are various types of reports prepared by management to know about the internal

issues and to get relevant information about them. They are: Performance report: The report is meant to understand overall performance of company.

It focuses over each employee within organisation. These are relevant reports as they help

management to make strategic decision and provide deep insight in working of company. Budget: They are prepared by every organisation whether it is a small business or large.

Department wise budgets are made in big companies. These budgets help to measure the

actual performance with set standards.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sales Report: This report helps to know the revenue earned from sales by company. It

shows which avenues has generated more profit and which avenues are in loses, it helps

mangers to know which salesperson has contributed more to the sales of product/services.

Cost Reports: In this report, the managers calculated the cost that incurred in production

of an item or product. It includes material, labour, overhead and wages and other factors

that are affects the cost of production (Jermias, 2017).

The information mentioned in these reports is utilised by the managers to make various

decision in relation to employees, products/services, etc. They act as the guidelines to managers.

Reports show the relevant information about overall business operations. Thus, the accuracy and

reliability should be there. If reports are not up to date then they hamper the performance of an

organisation. accurate reports make managers to take faster decision, formulate polices and plan

according to trends and changes, provide rewards to the hard-working employees and motivate

them to work for achievement of goals. To make a proper investment, produce goods in a cost

effective manner, all these activities of management can be achieved only when the information

in reports prepared are reliable. As the management operates in dynamic environment that keeps

on changing if the data provided is old and not up to date, this makes company to be stagnant in

its operations. Thus, above mentioned management report should be reliable, accurate and up to

date (Srinivasa, Kaura and Gilman, 2017).

The understandability of report means that it must be understandable by the people or the

one who are using it, a user must have certain basic knowledge of business activities. If given

data is not provided in a proper form then it may not be able to deliver the required information.

As mangers use them to make decision, formulate policies and marketing strategies, guides

employees, manages inventory, etc.; all these tasks would not be fulfilled if the information

provided is not understandable.

LO.2.

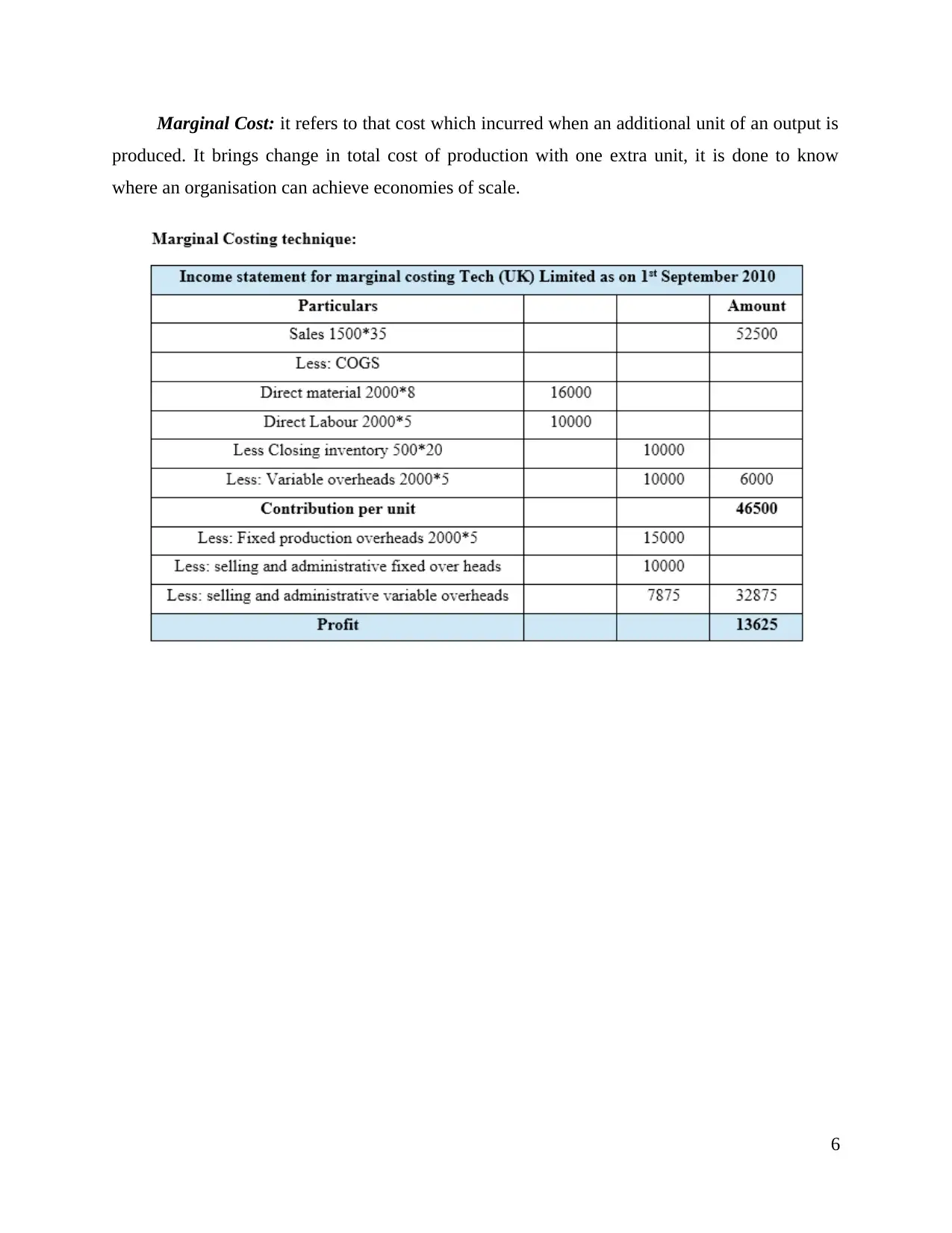

P.3. Prepare an income statement using marginal and absorption costs

Cost is an amount that is paid or given in order to get something gain return. It is usually a

monetary valuation of material, efforts resources, risks, time and utilities consumed and

opportunity that has been foregone for production. There are basically two types of cost in case

of company. These are fixed cost, variable cost and overhead cost. However, product costing can

be initiated in the form of absorption costing and marginal costing.

5

shows which avenues has generated more profit and which avenues are in loses, it helps

mangers to know which salesperson has contributed more to the sales of product/services.

Cost Reports: In this report, the managers calculated the cost that incurred in production

of an item or product. It includes material, labour, overhead and wages and other factors

that are affects the cost of production (Jermias, 2017).

The information mentioned in these reports is utilised by the managers to make various

decision in relation to employees, products/services, etc. They act as the guidelines to managers.

Reports show the relevant information about overall business operations. Thus, the accuracy and

reliability should be there. If reports are not up to date then they hamper the performance of an

organisation. accurate reports make managers to take faster decision, formulate polices and plan

according to trends and changes, provide rewards to the hard-working employees and motivate

them to work for achievement of goals. To make a proper investment, produce goods in a cost

effective manner, all these activities of management can be achieved only when the information

in reports prepared are reliable. As the management operates in dynamic environment that keeps

on changing if the data provided is old and not up to date, this makes company to be stagnant in

its operations. Thus, above mentioned management report should be reliable, accurate and up to

date (Srinivasa, Kaura and Gilman, 2017).

The understandability of report means that it must be understandable by the people or the

one who are using it, a user must have certain basic knowledge of business activities. If given

data is not provided in a proper form then it may not be able to deliver the required information.

As mangers use them to make decision, formulate policies and marketing strategies, guides

employees, manages inventory, etc.; all these tasks would not be fulfilled if the information

provided is not understandable.

LO.2.

P.3. Prepare an income statement using marginal and absorption costs

Cost is an amount that is paid or given in order to get something gain return. It is usually a

monetary valuation of material, efforts resources, risks, time and utilities consumed and

opportunity that has been foregone for production. There are basically two types of cost in case

of company. These are fixed cost, variable cost and overhead cost. However, product costing can

be initiated in the form of absorption costing and marginal costing.

5

Marginal Cost: it refers to that cost which incurred when an additional unit of an output is

produced. It brings change in total cost of production with one extra unit, it is done to know

where an organisation can achieve economies of scale.

6

produced. It brings change in total cost of production with one extra unit, it is done to know

where an organisation can achieve economies of scale.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

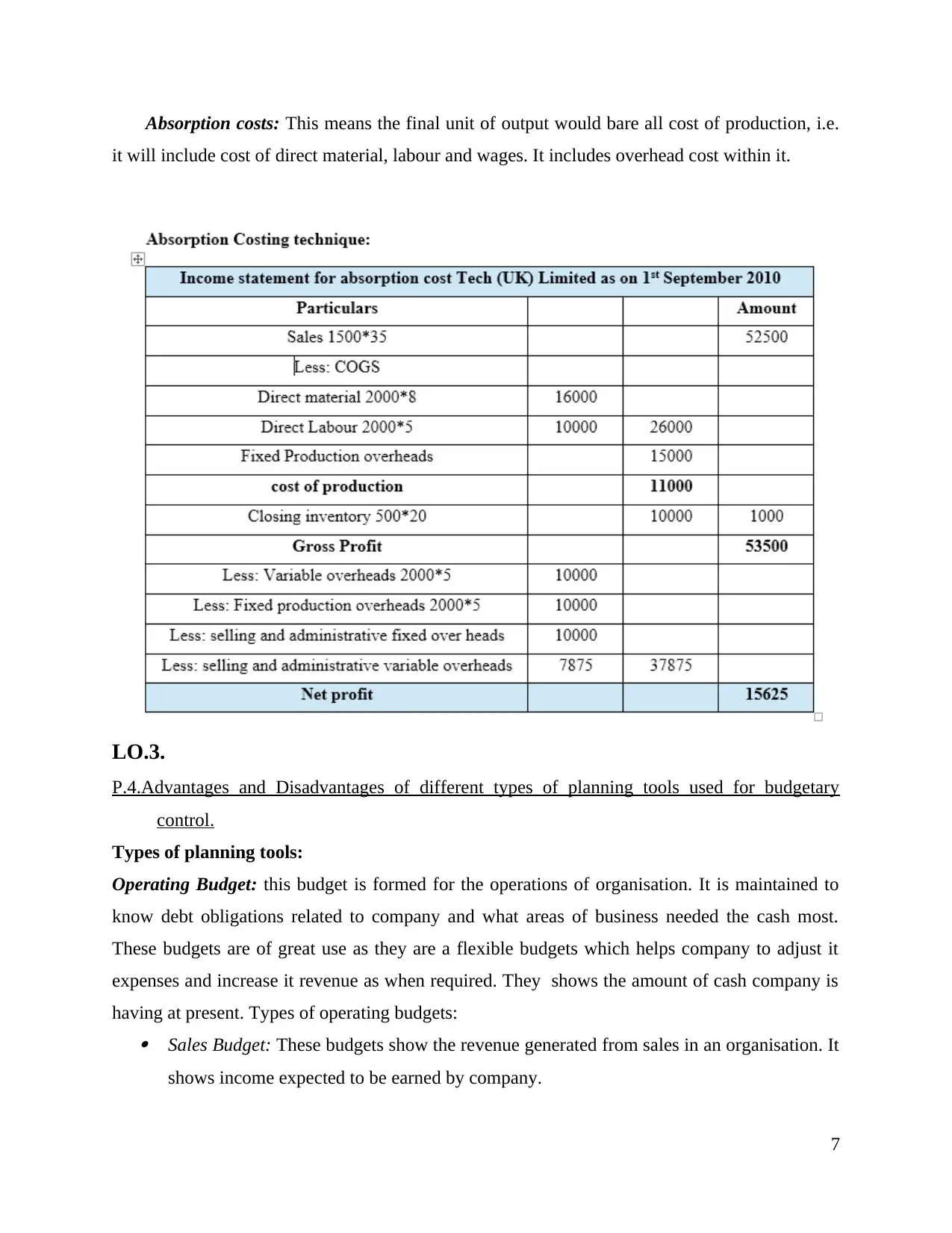

Absorption costs: This means the final unit of output would bare all cost of production, i.e.

it will include cost of direct material, labour and wages. It includes overhead cost within it.

LO.3.

P.4.Advantages and Disadvantages of different types of planning tools used for budgetary

control.

Types of planning tools:

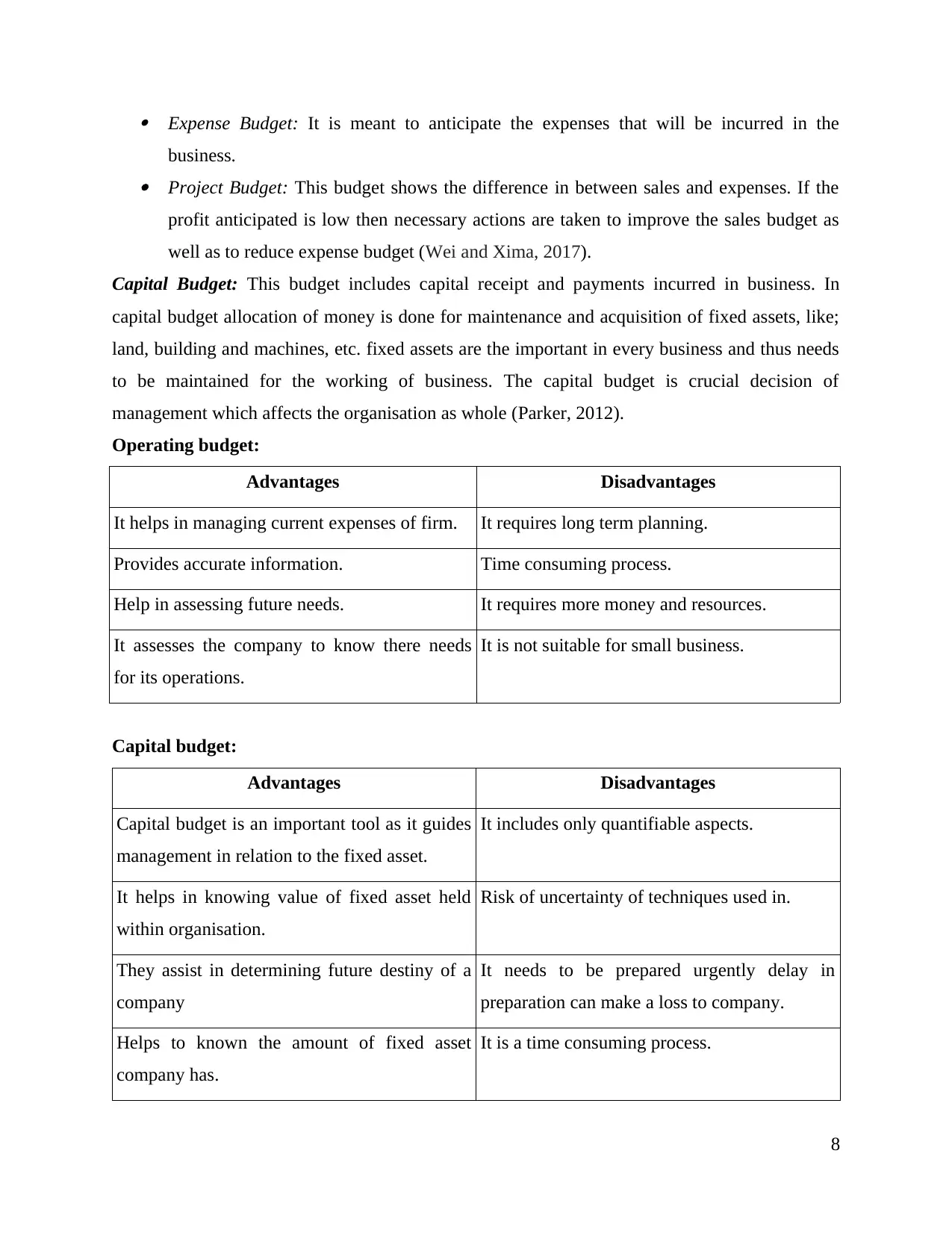

Operating Budget: this budget is formed for the operations of organisation. It is maintained to

know debt obligations related to company and what areas of business needed the cash most.

These budgets are of great use as they are a flexible budgets which helps company to adjust it

expenses and increase it revenue as when required. They shows the amount of cash company is

having at present. Types of operating budgets: Sales Budget: These budgets show the revenue generated from sales in an organisation. It

shows income expected to be earned by company.

7

it will include cost of direct material, labour and wages. It includes overhead cost within it.

LO.3.

P.4.Advantages and Disadvantages of different types of planning tools used for budgetary

control.

Types of planning tools:

Operating Budget: this budget is formed for the operations of organisation. It is maintained to

know debt obligations related to company and what areas of business needed the cash most.

These budgets are of great use as they are a flexible budgets which helps company to adjust it

expenses and increase it revenue as when required. They shows the amount of cash company is

having at present. Types of operating budgets: Sales Budget: These budgets show the revenue generated from sales in an organisation. It

shows income expected to be earned by company.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Expense Budget: It is meant to anticipate the expenses that will be incurred in the

business. Project Budget: This budget shows the difference in between sales and expenses. If the

profit anticipated is low then necessary actions are taken to improve the sales budget as

well as to reduce expense budget (Wei and Xima, 2017).

Capital Budget: This budget includes capital receipt and payments incurred in business. In

capital budget allocation of money is done for maintenance and acquisition of fixed assets, like;

land, building and machines, etc. fixed assets are the important in every business and thus needs

to be maintained for the working of business. The capital budget is crucial decision of

management which affects the organisation as whole (Parker, 2012).

Operating budget:

Advantages Disadvantages

It helps in managing current expenses of firm. It requires long term planning.

Provides accurate information. Time consuming process.

Help in assessing future needs. It requires more money and resources.

It assesses the company to know there needs

for its operations.

It is not suitable for small business.

Capital budget:

Advantages Disadvantages

Capital budget is an important tool as it guides

management in relation to the fixed asset.

It includes only quantifiable aspects.

It helps in knowing value of fixed asset held

within organisation.

Risk of uncertainty of techniques used in.

They assist in determining future destiny of a

company

It needs to be prepared urgently delay in

preparation can make a loss to company.

Helps to known the amount of fixed asset

company has.

It is a time consuming process.

8

business. Project Budget: This budget shows the difference in between sales and expenses. If the

profit anticipated is low then necessary actions are taken to improve the sales budget as

well as to reduce expense budget (Wei and Xima, 2017).

Capital Budget: This budget includes capital receipt and payments incurred in business. In

capital budget allocation of money is done for maintenance and acquisition of fixed assets, like;

land, building and machines, etc. fixed assets are the important in every business and thus needs

to be maintained for the working of business. The capital budget is crucial decision of

management which affects the organisation as whole (Parker, 2012).

Operating budget:

Advantages Disadvantages

It helps in managing current expenses of firm. It requires long term planning.

Provides accurate information. Time consuming process.

Help in assessing future needs. It requires more money and resources.

It assesses the company to know there needs

for its operations.

It is not suitable for small business.

Capital budget:

Advantages Disadvantages

Capital budget is an important tool as it guides

management in relation to the fixed asset.

It includes only quantifiable aspects.

It helps in knowing value of fixed asset held

within organisation.

Risk of uncertainty of techniques used in.

They assist in determining future destiny of a

company

It needs to be prepared urgently delay in

preparation can make a loss to company.

Helps to known the amount of fixed asset

company has.

It is a time consuming process.

8

There can be difference in pricing at which the products are actually offered by different

competitors. They tend to determine their prices based on cost of production that has actually

being incurred by them. Supply and demand is another factor that ios generally being considered

by them while determining prices. In this scenario, consumers play an important role in it.

P.5.Management Accounting Systems helps to respond to Financial Problems.

Every company needs money for its operations. The role of finance in business is crucial

as every aspects of business neds a proper funding to operate. But, at times there are financial

problems arises that hampers the growth of business. These problems are common in all type of

organisation. Examples; Increasing amount of debt over company: They are bad indicators as company growth is

been stopped with increasing amount of debts. High amount of unpaid loans and

increasing limits of credit cards raises companies monthly expenses. At a certain point

where company fails to repay or the amount of it debts and loans exceeds it revenues then

it leads to bankruptcy of company. Lack of strong financial Management: if company dose not have a sound financial

management then it will note be able to sustain in market. The firm which overspend

there financial resources and underestimates the competitors, suffers from improper

financial management (Bodie, 2013).

Not enough cash flow: Cash flows are important for company to run it business. If cash

flow of company shows negative balance then it will not be able to expand it business

and lastly it has to depend over borrowing of debt from outside parties.

To solve the above mentioned problems following methods can be used. Benchmarks: These refers to sets of standards which firm/company uses to check it

quality and to improve it performance in comparison to the other companies within the

industry. Benchmarks can be established by company itself or it can use the

predetermined standards that exist within environment. Organisation can set standards to

make effective use of financial resources, in order to avoid the wastage and duplication of

them. Further, management should set a benchmark to measure it performance. Key performance Indicators: These indicators shows the key operational areas of

organisation which it needs to be focused in order to achieve the objectives. They are the

9

competitors. They tend to determine their prices based on cost of production that has actually

being incurred by them. Supply and demand is another factor that ios generally being considered

by them while determining prices. In this scenario, consumers play an important role in it.

P.5.Management Accounting Systems helps to respond to Financial Problems.

Every company needs money for its operations. The role of finance in business is crucial

as every aspects of business neds a proper funding to operate. But, at times there are financial

problems arises that hampers the growth of business. These problems are common in all type of

organisation. Examples; Increasing amount of debt over company: They are bad indicators as company growth is

been stopped with increasing amount of debts. High amount of unpaid loans and

increasing limits of credit cards raises companies monthly expenses. At a certain point

where company fails to repay or the amount of it debts and loans exceeds it revenues then

it leads to bankruptcy of company. Lack of strong financial Management: if company dose not have a sound financial

management then it will note be able to sustain in market. The firm which overspend

there financial resources and underestimates the competitors, suffers from improper

financial management (Bodie, 2013).

Not enough cash flow: Cash flows are important for company to run it business. If cash

flow of company shows negative balance then it will not be able to expand it business

and lastly it has to depend over borrowing of debt from outside parties.

To solve the above mentioned problems following methods can be used. Benchmarks: These refers to sets of standards which firm/company uses to check it

quality and to improve it performance in comparison to the other companies within the

industry. Benchmarks can be established by company itself or it can use the

predetermined standards that exist within environment. Organisation can set standards to

make effective use of financial resources, in order to avoid the wastage and duplication of

them. Further, management should set a benchmark to measure it performance. Key performance Indicators: These indicators shows the key operational areas of

organisation which it needs to be focused in order to achieve the objectives. They are the

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

indicators that shows how effectively it is achieving the goals. They vary from business

to business depending on the priorities every firm has. The KPI for financial problems is

to see how much revenue is been generated by company. Budgetary Targets: The budget targets refers to a set amount of target which company

wants to achieved within a specific period, for example; if a company wants to increase it

sales by 1000 units by end of the current accounting period, this would be refereed to as

the budget target of company (Pondeville, Swaen and De Rongé, 2013).

Financial Governance: The predetermined rules that is been issued to provide governance or

protection to financial resources by there regulators (Kaplan and Atkinson, 2015). These set

standards or rules issued by the finance governance helps to regulate and check over financial

resources of company. It helps in preventing problems in many ways:

Improved companies reputation by controlling and checking over the financial assets of

company.

Reduces burden of debts and loans from organisation as resources are properly

maintained and guided.

Makes companies image stronger in the market.

Resolve the issue of cash flow from business.

Decreases conflicts from organisation and helps to reduce duplications and frauds.

Characteristics of an effective management accountant: Flexibility : The management should be adjustable and flexible, he should be able to

adapt to the changes within environment/ organisation. He should accepts the challenges

and take advantages of opportunities. Good Communication Skill: The communication skill of managers should be excellent,

he must be able to communicate the relevant information to there employees, collogues

and client. This will strength relationship between the employees and managers. Time Management skill: Managers are to take into consideration various issues of

organisation. They make strategic decision, thus they are lined up with various task in

line, so it becomes important for managers to effectively managed it time skills. Creativity: They deal within dynamic environment that keeps on changing, a manager

with a creative mind can easily adapt to these changes. Further, to resolve some issues

they need a creative approach rather than textbooks solutions.

10

to business depending on the priorities every firm has. The KPI for financial problems is

to see how much revenue is been generated by company. Budgetary Targets: The budget targets refers to a set amount of target which company

wants to achieved within a specific period, for example; if a company wants to increase it

sales by 1000 units by end of the current accounting period, this would be refereed to as

the budget target of company (Pondeville, Swaen and De Rongé, 2013).

Financial Governance: The predetermined rules that is been issued to provide governance or

protection to financial resources by there regulators (Kaplan and Atkinson, 2015). These set

standards or rules issued by the finance governance helps to regulate and check over financial

resources of company. It helps in preventing problems in many ways:

Improved companies reputation by controlling and checking over the financial assets of

company.

Reduces burden of debts and loans from organisation as resources are properly

maintained and guided.

Makes companies image stronger in the market.

Resolve the issue of cash flow from business.

Decreases conflicts from organisation and helps to reduce duplications and frauds.

Characteristics of an effective management accountant: Flexibility : The management should be adjustable and flexible, he should be able to

adapt to the changes within environment/ organisation. He should accepts the challenges

and take advantages of opportunities. Good Communication Skill: The communication skill of managers should be excellent,

he must be able to communicate the relevant information to there employees, collogues

and client. This will strength relationship between the employees and managers. Time Management skill: Managers are to take into consideration various issues of

organisation. They make strategic decision, thus they are lined up with various task in

line, so it becomes important for managers to effectively managed it time skills. Creativity: They deal within dynamic environment that keeps on changing, a manager

with a creative mind can easily adapt to these changes. Further, to resolve some issues

they need a creative approach rather than textbooks solutions.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Effective Organisation: He should be able to organise the company in an effective

manner. It must have all the required information, reports and data to the related issues.

This will help him find a quick solution to the problems.

Apply these skills of management to solve financial problems:

The skills of management like effective communication, this will help to generate

management information it required, also when subordinates provides proper and timely

information this would help managers to solve any issues if arises.

Creativity of managers help it to get over any untimely or contingent liabilities arises in

an organisation or outside environment. Further, the creative approach of him towards

problems will able to get a better solution in a cost effective manner.

The managing of organisation as whole is key aspects that resolves the issues of financial

problems as mangers will be able to effectively control over the financial assets of

company. This will reduce the need and dependency of firm over debts and loans.

Effective management of time will generate more revenue. When a manger will be able

to effectively manages it given time, he can focus over core issues of business that affects

company performances. Also, he will be able to make effective and timely decision for

arrived issues and control environment from getting worsen (Klychova and et.al., 2015).

The strategies of management accounting helps to combat the problems of financial

management. Financial statements of company is of great significance to each parties whether it

be outside or inside of organisation. The financial statements help management to know it

positions and progress in an accounting year (Nixon and Burns, 2012), Similarly these

statements attracts potential investors and enable the existing ones to know that there

investments are in safe place and generates good rate of return. Creditors finds the state of there

money through the financial statements it builds there faith and trust over companies'. Further,

government can formulate taxation policies for the a particular industry by knowing there

financial positions. Thus, it becomes important aspects of an organisation to provide a reliable,

accurate and up to date information in there financial statements so the outside parties can rely to

them.

CONCLUSION.

Management accounting is evolutionary subject, that plays an important role in managing

and assessing the organisation. It helps mangers to get necessary and timely information as and

11

manner. It must have all the required information, reports and data to the related issues.

This will help him find a quick solution to the problems.

Apply these skills of management to solve financial problems:

The skills of management like effective communication, this will help to generate

management information it required, also when subordinates provides proper and timely

information this would help managers to solve any issues if arises.

Creativity of managers help it to get over any untimely or contingent liabilities arises in

an organisation or outside environment. Further, the creative approach of him towards

problems will able to get a better solution in a cost effective manner.

The managing of organisation as whole is key aspects that resolves the issues of financial

problems as mangers will be able to effectively control over the financial assets of

company. This will reduce the need and dependency of firm over debts and loans.

Effective management of time will generate more revenue. When a manger will be able

to effectively manages it given time, he can focus over core issues of business that affects

company performances. Also, he will be able to make effective and timely decision for

arrived issues and control environment from getting worsen (Klychova and et.al., 2015).

The strategies of management accounting helps to combat the problems of financial

management. Financial statements of company is of great significance to each parties whether it

be outside or inside of organisation. The financial statements help management to know it

positions and progress in an accounting year (Nixon and Burns, 2012), Similarly these

statements attracts potential investors and enable the existing ones to know that there

investments are in safe place and generates good rate of return. Creditors finds the state of there

money through the financial statements it builds there faith and trust over companies'. Further,

government can formulate taxation policies for the a particular industry by knowing there

financial positions. Thus, it becomes important aspects of an organisation to provide a reliable,

accurate and up to date information in there financial statements so the outside parties can rely to

them.

CONCLUSION.

Management accounting is evolutionary subject, that plays an important role in managing

and assessing the organisation. It helps mangers to get necessary and timely information as and

11

when required. Various types of system of management accounting like; cost accounting, job

costing, etc. helps mangers to know about the cost incurred in production and the cost of various

jobs within business. The reports prepared by management helps to address about the progress of

organisation and enables to measure there actual performance with set standard. Further, there

are various ways in which management accounting principles can be used to solve the financial

problems.

12

costing, etc. helps mangers to know about the cost incurred in production and the cost of various

jobs within business. The reports prepared by management helps to address about the progress of

organisation and enables to measure there actual performance with set standard. Further, there

are various ways in which management accounting principles can be used to solve the financial

problems.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES.

Books and Journals.

Bodie, Z., 2013. Investments. McGraw-Hill.

Chiwamit, P., Modell, S. and Scapens, R. W., 2017. Regulation and adaptation of management

accounting innovations: The case of economic value added in Thai state-owned

enterprises. Management Accounting Research. 37. pp.30-48.

Goddard, A. and Simm, A., 2017. Management accounting, performance measurement and

strategy in English local authorities. Public Money & Management. 37(4). pp.261-268.

Jermias, J., 2017. Development of management accounting practices in Indonesia. The

Routledge Handbook of Accounting in Asia, p.104.

Kaplan, R. S. and Atkinson, A. A., 2015. Advanced management accounting. PHI Learning.

Klychova, G. S. and et.al., 2015. Management aspects of production cost accounting in horse

breeding. Asian Social Science. 11(11). pp.308.

Nixon, B. and Burns, J., 2012. The paradox of strategic management accounting. Management

Accounting Research. 23(4). pp.229-244.

Parker, L. D., 2012. Qualitative management accounting research: Assessing deliverables and

relevance. Critical perspectives on accounting. 23(1). pp.54-70.

Pondeville, S., Swaen, V. and De Rongé, Y., 2013. Environmental management control systems:

The role of contextual and strategic factors.Management accounting research. 24(4).

pp.317-332.

Srinivasa, D., Kaura, A. and Gilman, R., 2017. A Systematic Review and Variance Analysis:

Does Plane of Dissection Affect Nerve Injury Complication Rates in Various

Rhytidectomy Techniques?. Plastic and Reconstructive Surgery Global Open. 5(9 Suppl).

Wei, W. E. I. and Xima, Y. U. E., 2017. Research on Accunting Development Cost Per Graduate

Student in University. Canadian Social Science. 13(1). pp.11-15.

13

Books and Journals.

Bodie, Z., 2013. Investments. McGraw-Hill.

Chiwamit, P., Modell, S. and Scapens, R. W., 2017. Regulation and adaptation of management

accounting innovations: The case of economic value added in Thai state-owned

enterprises. Management Accounting Research. 37. pp.30-48.

Goddard, A. and Simm, A., 2017. Management accounting, performance measurement and

strategy in English local authorities. Public Money & Management. 37(4). pp.261-268.

Jermias, J., 2017. Development of management accounting practices in Indonesia. The

Routledge Handbook of Accounting in Asia, p.104.

Kaplan, R. S. and Atkinson, A. A., 2015. Advanced management accounting. PHI Learning.

Klychova, G. S. and et.al., 2015. Management aspects of production cost accounting in horse

breeding. Asian Social Science. 11(11). pp.308.

Nixon, B. and Burns, J., 2012. The paradox of strategic management accounting. Management

Accounting Research. 23(4). pp.229-244.

Parker, L. D., 2012. Qualitative management accounting research: Assessing deliverables and

relevance. Critical perspectives on accounting. 23(1). pp.54-70.

Pondeville, S., Swaen, V. and De Rongé, Y., 2013. Environmental management control systems:

The role of contextual and strategic factors.Management accounting research. 24(4).

pp.317-332.

Srinivasa, D., Kaura, A. and Gilman, R., 2017. A Systematic Review and Variance Analysis:

Does Plane of Dissection Affect Nerve Injury Complication Rates in Various

Rhytidectomy Techniques?. Plastic and Reconstructive Surgery Global Open. 5(9 Suppl).

Wei, W. E. I. and Xima, Y. U. E., 2017. Research on Accunting Development Cost Per Graduate

Student in University. Canadian Social Science. 13(1). pp.11-15.

13

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.