Management Accounting Concept - Zylla

Added on 2020-10-22

17 Pages5204 Words450 Views

Management Accounting1

Table of ContentsINTRODUCTION..............................................................................................................................3P1. Management accounting concept and its requirements...........................................................4P2. Various methods applied for management accounting reporting............................................5M1 Evaluate the benefits of management accounting systems.....................................................7D1 Critical evaluation of how management accounting systems..................................................7P3) Cost analysis to prepare an income statement using marginal and absorption cost ...............8M2 Range of accounting techniques..............................................................................................9M2 Preparing financial Report.....................................................................................................10P4 Advantages and disadvantages of different types of planning tools used in budgetary control......................................................................................................................................................10M3 Use of different planning tools..............................................................................................12P5 Adoption of management accounting system to solve problems...........................................12M4 Management accounting can lead organisations to sustainable success...............................14D3 Evaluation of planning tools for accounting respond appropriately to solving financialproblems ......................................................................................................................................14CONCLUSION:...............................................................................................................................14REFERENCES:................................................................................................................................152

INTRODUCTIONManagement accounting is a provision of accounting information which is used bymanagers for better information for their firm so that decisions could be taken in a systematicmanner to assist performance and management of business. It requires accuracy and perfection ininternal activities of a firm. In this report, Zylla has shown different management accountingtechniques for deciding costs and ways to respond towards financial problems. Here, requirementof management and its crucial evaluation is also done (Arkorful and Abaidoo, 2015). Zylla makesuse of management accounting in decision making, devising planning and giving expertise infinancial reporting. Its areas are extended to strategic management, risk pln and performance isneed to be measured. Its tools assist in improvement of better cost mechanism as well as inoperational ability. Current report will illustrate costing system, different budgetary techniques,reporting methods and techniques of appraisal which help in internal administration. It focuses ondetailed information on operations, tasks and other divisions.P1. Management accounting concept and its requirementsManagement accounting is required to examine data collected so that its basic needs aredetermined for business purpose. It is a type of mathematical tool which sets data in assistivemanner in terms of planning and decision making for managerial professionals to forecast budgetsfor different operational departments. Such techniques target goals in a managerial form and witheffectiveness so that firm can achieve its objectives in a prominent way. It plays a crucial role indelivering information to the people of management. It is an integration of non-financial andfinancial statements to give information so that impressive decisions can be taken for organisation.Proper techniques are used in the application of processing data and establishing plans so thatrational decisions will be taken with a view to move towards objectives (Ceulemans, Molderez andVan Liedekerke, 2015). It underlines various phases of the management. Different accountingtechniques are as follows: Job Costing: Costs incurred in every operational activity of business are determined by transactionactivities. Therefore, all types of satisfactory records are made in accounting systems like labour,direct material and other relevant costs. Thus, these costs are required in every department toillustrate cost requirement of it.Management of inventory: It helps in keeping export-import record of business. This is dependenton managing the level of inventories. So, production department should be cautious regarding3

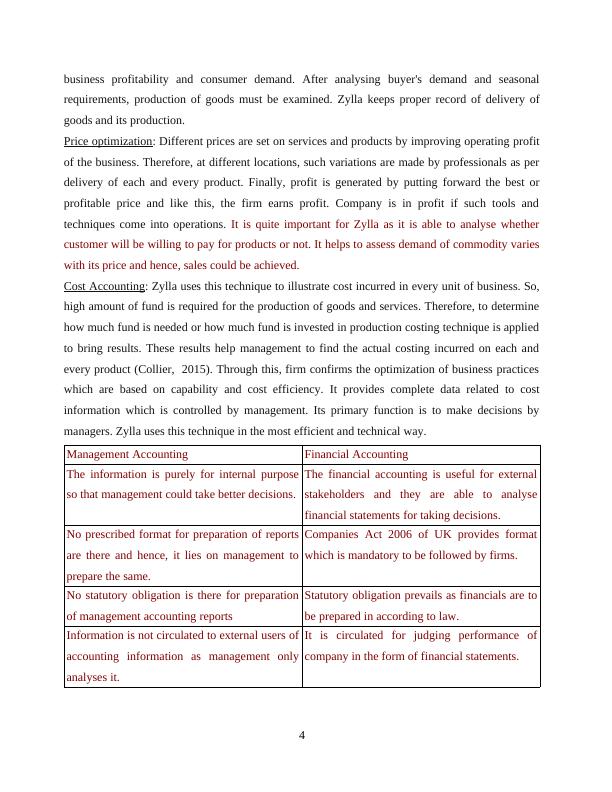

business profitability and consumer demand. After analysing buyer's demand and seasonalrequirements, production of goods must be examined. Zylla keeps proper record of delivery ofgoods and its production.Price optimization: Different prices are set on services and products by improving operating profitof the business. Therefore, at different locations, such variations are made by professionals as perdelivery of each and every product. Finally, profit is generated by putting forward the best orprofitable price and like this, the firm earns profit. Company is in profit if such tools andtechniques come into operations. It is quite important for Zylla as it is able to analyse whethercustomer will be willing to pay for products or not. It helps to assess demand of commodity varieswith its price and hence, sales could be achieved. Cost Accounting: Zylla uses this technique to illustrate cost incurred in every unit of business. So,high amount of fund is required for the production of goods and services. Therefore, to determinehow much fund is needed or how much fund is invested in production costing technique is appliedto bring results. These results help management to find the actual costing incurred on each andevery product (Collier, 2015). Through this, firm confirms the optimization of business practiceswhich are based on capability and cost efficiency. It provides complete data related to costinformation which is controlled by management. Its primary function is to make decisions bymanagers. Zylla uses this technique in the most efficient and technical way.Management AccountingFinancial AccountingThe information is purely for internal purposeso that management could take better decisions.The financial accounting is useful for externalstakeholders and they are able to analysefinancial statements for taking decisions.No prescribed format for preparation of reportsare there and hence, it lies on management toprepare the same.Companies Act 2006 of UK provides formatwhich is mandatory to be followed by firms.No statutory obligation is there for preparationof management accounting reportsStatutory obligation prevails as financials are tobe prepared in according to law.Information is not circulated to external users ofaccounting information as management onlyanalyses it.It is circulated for judging performance ofcompany in the form of financial statements.4

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Management Accounting Conceptslg...

|13

|3941

|341

Introduction to the Management Accounting Systemlg...

|15

|5016

|36

Management Accounting Techniques Reportlg...

|13

|3548

|62

Management Accounting of Zylla Companylg...

|16

|3933

|89

Management Accounting Assignment - Zylla companylg...

|15

|5245

|237

Management Accounting Systems and Techniqueslg...

|15

|4691

|20