Management Accounting Report: Analysis of Innocent Drinks' Strategies

VerifiedAdded on 2023/01/07

|16

|5087

|42

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices, focusing on Innocent Drinks as a case study. It begins by defining management accounting and exploring various management accounting systems such as inventory management, job costing, cost accounting, and price costing systems, and their applications within Innocent Drinks. The report then delves into different methods of management accounting reporting, including cost accounting reports, performance reports, and accounts receivable reporting. The benefits of these systems and their application for Innocent Drinks are thoroughly examined. The core of the report centers on cost analysis, using marginal costing and absorption costing to prepare income statements. Detailed calculations and comparisons are provided to illustrate the impact of each method. Furthermore, the report explores planning tools used in budgetary control, discussing their benefits and drawbacks, and analyzes their application within the context of Innocent Drinks. The report concludes with a comparison of organizations and how they adapt management accounting systems to address financial problems, providing a holistic view of management accounting's role in business decision-making and performance enhancement.

Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Management accounting and management accounting systems......................................3

P2 Explaining various methods of MA reporting...................................................................5

M1 Benefits of MA systems and their application for Innocent drinks.................................6

TASK 2............................................................................................................................................6

P3. Calculation of costs using best method of cost analysis to make an income statement...6

M2 Range of management accounting techniques...............................................................10

TASK 3..........................................................................................................................................11

P4. Explanation of various planning tools used in budgetary control with proper benefits and

drawbacks.............................................................................................................................11

M3 Analyse of planning tools and their application............................................................12

TASK 4..........................................................................................................................................13

P5. Comparison of organisations for adapting MAS to defect to financial problems.........13

M4.........................................................................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Management accounting and management accounting systems......................................3

P2 Explaining various methods of MA reporting...................................................................5

M1 Benefits of MA systems and their application for Innocent drinks.................................6

TASK 2............................................................................................................................................6

P3. Calculation of costs using best method of cost analysis to make an income statement...6

M2 Range of management accounting techniques...............................................................10

TASK 3..........................................................................................................................................11

P4. Explanation of various planning tools used in budgetary control with proper benefits and

drawbacks.............................................................................................................................11

M3 Analyse of planning tools and their application............................................................12

TASK 4..........................................................................................................................................13

P5. Comparison of organisations for adapting MAS to defect to financial problems.........13

M4.........................................................................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting defined as the financial reporting whereby all monetary and non-

monetary data are integrated to include effective and efficient decision-making tools. This is an

important instrument for planning, decision-making as well as creating an efficient financial

statement because standard costing is the central component in the method of cost determination

as well as price-setting (Wagenhofer, 2016). The management accounting definition and method

varies from financial accounting, as MA includes both financial and nonfinancial considerations.

The key purpose of the production of this study is to pass through performance of the second

task effectively.

This really uses a wide variety of managerial accounting documents to promote the

performance assessment procedure, as well as several budgeting process strategies enable proper

knowledge about the business employee's success. Various strategies and their effect are

addressed as a central objective of this review and they are analysed from a separate angle.

Moreover, methodologies used during MA offer a good picture in the context of company to

make better results.

TASK 1

P1. Management accounting and management accounting systems

Management accounting functions include formulating market objectives like

understanding the financial impact of corporate decision making, tracking spending, and

maximizing profit. MA theory includes the design of gathering financial information,

documents as well as assumptions, outstanding management, extra cost of absorption, as well as

reference of accounting discipline. MA Systems aim to create cost accounting records for

managers' organizational use in order to enhance the effective decision making process and

better operate the company (Epstein and Lee, 2015). Some of the useful system of MA that can

be used by Innocent Drinks in making proper decision is discussed underneath:

Inventory management system: This system helps a company to retain an optimal

amount of inventory such that it can access as it is needed and thus does not get to deal with

surplus product problem or in appropriate product. This system is managed by

implementing different algorithms, with some of the more efficient methods being FIFO, LIFO,

ABC Analysis, JIT etc. (Botes and Sharma, 2017).

Management accounting defined as the financial reporting whereby all monetary and non-

monetary data are integrated to include effective and efficient decision-making tools. This is an

important instrument for planning, decision-making as well as creating an efficient financial

statement because standard costing is the central component in the method of cost determination

as well as price-setting (Wagenhofer, 2016). The management accounting definition and method

varies from financial accounting, as MA includes both financial and nonfinancial considerations.

The key purpose of the production of this study is to pass through performance of the second

task effectively.

This really uses a wide variety of managerial accounting documents to promote the

performance assessment procedure, as well as several budgeting process strategies enable proper

knowledge about the business employee's success. Various strategies and their effect are

addressed as a central objective of this review and they are analysed from a separate angle.

Moreover, methodologies used during MA offer a good picture in the context of company to

make better results.

TASK 1

P1. Management accounting and management accounting systems

Management accounting functions include formulating market objectives like

understanding the financial impact of corporate decision making, tracking spending, and

maximizing profit. MA theory includes the design of gathering financial information,

documents as well as assumptions, outstanding management, extra cost of absorption, as well as

reference of accounting discipline. MA Systems aim to create cost accounting records for

managers' organizational use in order to enhance the effective decision making process and

better operate the company (Epstein and Lee, 2015). Some of the useful system of MA that can

be used by Innocent Drinks in making proper decision is discussed underneath:

Inventory management system: This system helps a company to retain an optimal

amount of inventory such that it can access as it is needed and thus does not get to deal with

surplus product problem or in appropriate product. This system is managed by

implementing different algorithms, with some of the more efficient methods being FIFO, LIFO,

ABC Analysis, JIT etc. (Botes and Sharma, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In context of Innocent Drinks the inventory management system have an important part

in managing the organization's holding costs and price levels. Manager can use a standardizing

supply chain management system to create storage stocks and product inventories.

Company items are typically the home pieces that are cumbersome to bring to sell as they are

sold by a list in stores and these pieces are shipped from the factory as they are ordered. This

inventory management program is basically needed by this organization as this program helps

reduce the expense of the keeping and able to promote goods rapidly and efficiently.

Job costing system: This MA system is a program which deals with the expenses

involved among each work a company conducts (Drury, 2013). This work costing system is done

in a sequence of steps; initial costing of every work including small or big is reported and then,

at the conclusion of the evaluation process, all costs are split into separate cost object that can be

valuation, output, distribution of materials and much more. In order to monitor and manage the

organization's budget, each expense pool is then evaluated to determine the amount of expenses

involved within them.

This MA system is needed at Innocent drinks because it allows this manager to track the

expenditures related to jobs like packaging and distribution. Company also uses cost-per-touch

methodology associated with this method to track its expenditures.

Cost accounting system: This system is a mechanism that companies use to measure the

expenses associated in their goods being made and marketed. The cost of this assessment covers

all the expense pools including cost of production, cost of marketing and much more. This

framework aims to define expenses paid with each organisation's commodity.

This accounting parameter is helpful for Innocent drink management because it can

determine which goods are more cost-involved and so it can evaluate if they really are worth

investing a massive proportion or whether they're able to achieve a large market share. Company

also uses this method to measure the prices of its goods and to select its product line which is

more profitable and demanding in the market.

Price costing system: This management method depends on a methodology focused on

economics rather than scientific and machinery. Through this method, a company should

determine the price of each of the goods so that it can lead in their consumers becoming

extremely successful and happy (Hiebl and Richter, 2018).

in managing the organization's holding costs and price levels. Manager can use a standardizing

supply chain management system to create storage stocks and product inventories.

Company items are typically the home pieces that are cumbersome to bring to sell as they are

sold by a list in stores and these pieces are shipped from the factory as they are ordered. This

inventory management program is basically needed by this organization as this program helps

reduce the expense of the keeping and able to promote goods rapidly and efficiently.

Job costing system: This MA system is a program which deals with the expenses

involved among each work a company conducts (Drury, 2013). This work costing system is done

in a sequence of steps; initial costing of every work including small or big is reported and then,

at the conclusion of the evaluation process, all costs are split into separate cost object that can be

valuation, output, distribution of materials and much more. In order to monitor and manage the

organization's budget, each expense pool is then evaluated to determine the amount of expenses

involved within them.

This MA system is needed at Innocent drinks because it allows this manager to track the

expenditures related to jobs like packaging and distribution. Company also uses cost-per-touch

methodology associated with this method to track its expenditures.

Cost accounting system: This system is a mechanism that companies use to measure the

expenses associated in their goods being made and marketed. The cost of this assessment covers

all the expense pools including cost of production, cost of marketing and much more. This

framework aims to define expenses paid with each organisation's commodity.

This accounting parameter is helpful for Innocent drink management because it can

determine which goods are more cost-involved and so it can evaluate if they really are worth

investing a massive proportion or whether they're able to achieve a large market share. Company

also uses this method to measure the prices of its goods and to select its product line which is

more profitable and demanding in the market.

Price costing system: This management method depends on a methodology focused on

economics rather than scientific and machinery. Through this method, a company should

determine the price of each of the goods so that it can lead in their consumers becoming

extremely successful and happy (Hiebl and Richter, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This program is strongly needed by Innocent drinks because by doing this, manager sets

the values on all of its goods in such a manner that it will result in high profitability on

company and could also be a commodity with the maximum priority for its quality, so that might

also obtain customer loyalty.

All of the above-mentioned management accounting framework is basically necessary at

innocent drinks and lets this business sustain and monitor its organizational and financial

performance.

P2 Explaining various methods of MA reporting

MA reports are the records that are generated by providing financial and organizational

information in these reports so that administrators can justify their plans and decisions as

confirmation of policy development in these reports. Various reports are published under

MA and others can be designed by innocent drinks. Such reports serve as tools for accounting

managerial accounting, although these documents are the means to execute accounting system

successfully. Here are some of those approaches explained:

Cost accounting report: This process of cost financial reports assists an enterprise to

carry out its audit task smoothly as this study is produced under a cost system where all the

prices of all the organization's products are reported (Jermias, Gani and Juliana, 2018). This

study provides prices of all of the company's purchased goods and splits all of the other products

through variable, semi-variable, as well as fixed operating costs to aid in decision-making.

Innocent drinks manager can produces such a study to assess the amount of the fixed costs they

are paying on each commodity.

Performance report: This is among the most relevant MA report that is not associated

with numerical revenues or spending problems but is associated with increasing employee's

success in an enterprise. This study is produced by an organisation's HR department and reports

on the workers' 360-degree success evaluations. Innocent drinks manager finds their staff

member as the most important asset by which they create this study to define their staff

performance standards. This study aims to improve the efficiency of the workers and of the

whole company effectively.

Reporting of accounts receivable: This report is deemed acceptable for large-scale

companies or entities which is involved in numerous money transaction obtained per day

(Kaplan and Atkinson, 2015). This account receivables summary contains an organization's

the values on all of its goods in such a manner that it will result in high profitability on

company and could also be a commodity with the maximum priority for its quality, so that might

also obtain customer loyalty.

All of the above-mentioned management accounting framework is basically necessary at

innocent drinks and lets this business sustain and monitor its organizational and financial

performance.

P2 Explaining various methods of MA reporting

MA reports are the records that are generated by providing financial and organizational

information in these reports so that administrators can justify their plans and decisions as

confirmation of policy development in these reports. Various reports are published under

MA and others can be designed by innocent drinks. Such reports serve as tools for accounting

managerial accounting, although these documents are the means to execute accounting system

successfully. Here are some of those approaches explained:

Cost accounting report: This process of cost financial reports assists an enterprise to

carry out its audit task smoothly as this study is produced under a cost system where all the

prices of all the organization's products are reported (Jermias, Gani and Juliana, 2018). This

study provides prices of all of the company's purchased goods and splits all of the other products

through variable, semi-variable, as well as fixed operating costs to aid in decision-making.

Innocent drinks manager can produces such a study to assess the amount of the fixed costs they

are paying on each commodity.

Performance report: This is among the most relevant MA report that is not associated

with numerical revenues or spending problems but is associated with increasing employee's

success in an enterprise. This study is produced by an organisation's HR department and reports

on the workers' 360-degree success evaluations. Innocent drinks manager finds their staff

member as the most important asset by which they create this study to define their staff

performance standards. This study aims to improve the efficiency of the workers and of the

whole company effectively.

Reporting of accounts receivable: This report is deemed acceptable for large-scale

companies or entities which is involved in numerous money transaction obtained per day

(Kaplan and Atkinson, 2015). This account receivables summary contains an organization's

inflow cash transfers to keep a list of the money that the company routinely collects toward their

activities. Both these inflow assets contribute to a company income. Innocent drinks finance

team is accountable for devising such a database, taking into consideration the company's

transaction flow, it could be said organization is creating an automated account receivables

system to efficiently monitor the flow of cash in its business but instead keep making effective

strategies.

All of these MA reports analysed above ensure that an organization such

as Innocent drinks can effectively manage all its internal process and operation to make better

performance every year.

M1 Benefits of MA systems and their application for Innocent drinks.

Inventory management system: This system is effective for respective organization to record

the total inventory and support to determine the exact level as well as time of reordering (Leotta,

Rizza and Ruggeri, 2017). Innocent drinks use this to standardize its inventory by administering

a completely separate storage facility with several of its stores.

Job costing system: The additional benefit of such a system is to identify expenses

involved among each job. Innocent drinks uses this approach to enhance different cost streams

and afterwards incorporate cost reduction strategies related to every cost in order to increase the

overall profit.

Cost accounting system: This is very beneficial system as it aims to identify costs

involved by the organization for each manufactured product. Innocent drinks use this method to

track their price per unit and afterwards keep making actions to minimize a certain cost by re-

analysing their variable and fixed costs.

Price optimization system: This specific system is beneficial to business organization as

this support to find the specific price for its products sold to customers. Innocent drinks can use

this specific system to fix an affordable price for all of its products which can result in

trustworthy affordable customer costs and make company profit.

TASK 2

P3. Calculation of costs using best method of cost analysis to make an income statement.

The cost may be described as the monetary interest a corporation has expended on

inventing content, so this decided to donate a certain number of money a company has used to

activities. Both these inflow assets contribute to a company income. Innocent drinks finance

team is accountable for devising such a database, taking into consideration the company's

transaction flow, it could be said organization is creating an automated account receivables

system to efficiently monitor the flow of cash in its business but instead keep making effective

strategies.

All of these MA reports analysed above ensure that an organization such

as Innocent drinks can effectively manage all its internal process and operation to make better

performance every year.

M1 Benefits of MA systems and their application for Innocent drinks.

Inventory management system: This system is effective for respective organization to record

the total inventory and support to determine the exact level as well as time of reordering (Leotta,

Rizza and Ruggeri, 2017). Innocent drinks use this to standardize its inventory by administering

a completely separate storage facility with several of its stores.

Job costing system: The additional benefit of such a system is to identify expenses

involved among each job. Innocent drinks uses this approach to enhance different cost streams

and afterwards incorporate cost reduction strategies related to every cost in order to increase the

overall profit.

Cost accounting system: This is very beneficial system as it aims to identify costs

involved by the organization for each manufactured product. Innocent drinks use this method to

track their price per unit and afterwards keep making actions to minimize a certain cost by re-

analysing their variable and fixed costs.

Price optimization system: This specific system is beneficial to business organization as

this support to find the specific price for its products sold to customers. Innocent drinks can use

this specific system to fix an affordable price for all of its products which can result in

trustworthy affordable customer costs and make company profit.

TASK 2

P3. Calculation of costs using best method of cost analysis to make an income statement.

The cost may be described as the monetary interest a corporation has expended on

inventing content, so this decided to donate a certain number of money a company has used to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

manufacture or generate products and services. Some of the common method of costing used by

innocent drinks in order to prepare income statement so that net profit can be determined is

discussed underneath:

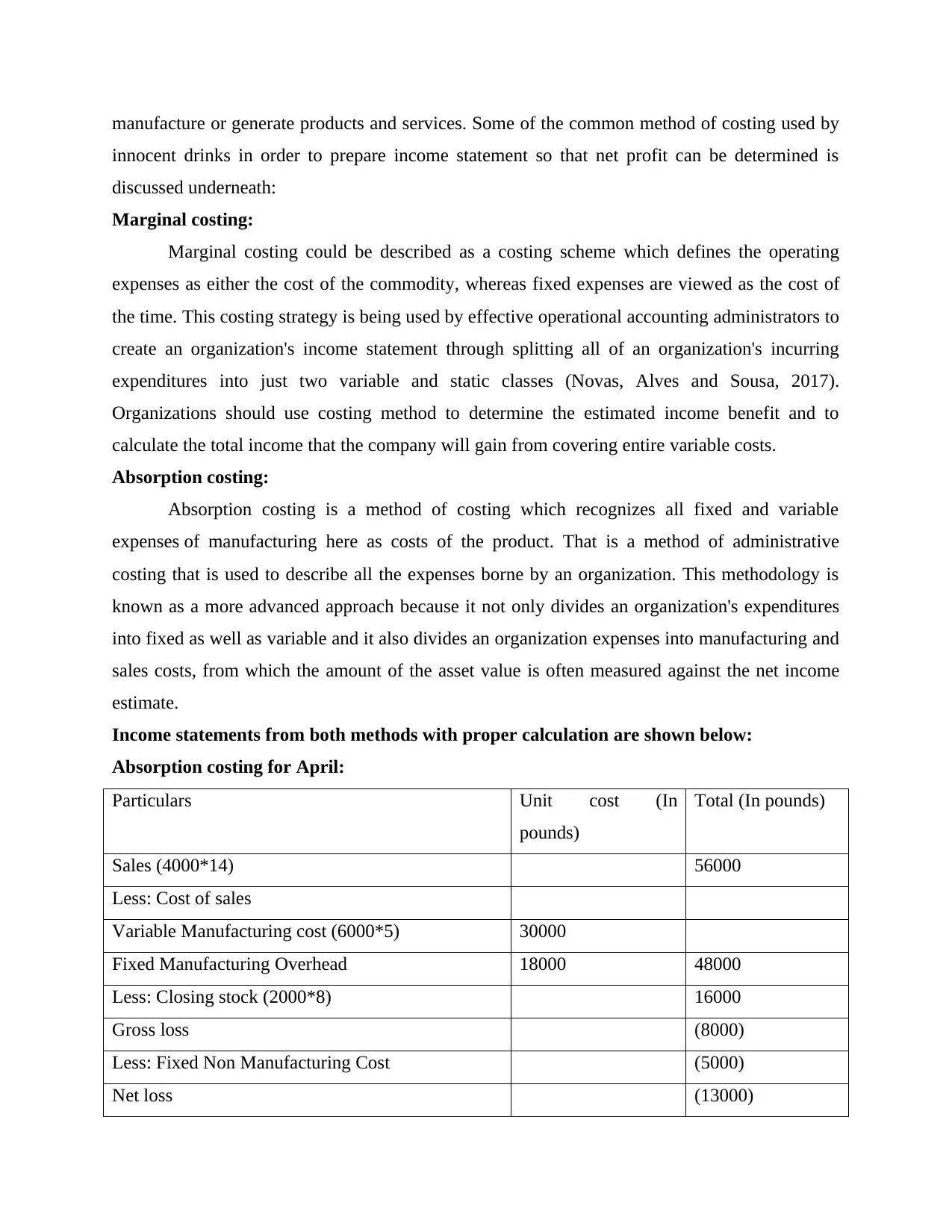

Marginal costing:

Marginal costing could be described as a costing scheme which defines the operating

expenses as either the cost of the commodity, whereas fixed expenses are viewed as the cost of

the time. This costing strategy is being used by effective operational accounting administrators to

create an organization's income statement through splitting all of an organization's incurring

expenditures into just two variable and static classes (Novas, Alves and Sousa, 2017).

Organizations should use costing method to determine the estimated income benefit and to

calculate the total income that the company will gain from covering entire variable costs.

Absorption costing:

Absorption costing is a method of costing which recognizes all fixed and variable

expenses of manufacturing here as costs of the product. That is a method of administrative

costing that is used to describe all the expenses borne by an organization. This methodology is

known as a more advanced approach because it not only divides an organization's expenditures

into fixed as well as variable and it also divides an organization expenses into manufacturing and

sales costs, from which the amount of the asset value is often measured against the net income

estimate.

Income statements from both methods with proper calculation are shown below:

Absorption costing for April:

Particulars Unit cost (In

pounds)

Total (In pounds)

Sales (4000*14) 56000

Less: Cost of sales

Variable Manufacturing cost (6000*5) 30000

Fixed Manufacturing Overhead 18000 48000

Less: Closing stock (2000*8) 16000

Gross loss (8000)

Less: Fixed Non Manufacturing Cost (5000)

Net loss (13000)

innocent drinks in order to prepare income statement so that net profit can be determined is

discussed underneath:

Marginal costing:

Marginal costing could be described as a costing scheme which defines the operating

expenses as either the cost of the commodity, whereas fixed expenses are viewed as the cost of

the time. This costing strategy is being used by effective operational accounting administrators to

create an organization's income statement through splitting all of an organization's incurring

expenditures into just two variable and static classes (Novas, Alves and Sousa, 2017).

Organizations should use costing method to determine the estimated income benefit and to

calculate the total income that the company will gain from covering entire variable costs.

Absorption costing:

Absorption costing is a method of costing which recognizes all fixed and variable

expenses of manufacturing here as costs of the product. That is a method of administrative

costing that is used to describe all the expenses borne by an organization. This methodology is

known as a more advanced approach because it not only divides an organization's expenditures

into fixed as well as variable and it also divides an organization expenses into manufacturing and

sales costs, from which the amount of the asset value is often measured against the net income

estimate.

Income statements from both methods with proper calculation are shown below:

Absorption costing for April:

Particulars Unit cost (In

pounds)

Total (In pounds)

Sales (4000*14) 56000

Less: Cost of sales

Variable Manufacturing cost (6000*5) 30000

Fixed Manufacturing Overhead 18000 48000

Less: Closing stock (2000*8) 16000

Gross loss (8000)

Less: Fixed Non Manufacturing Cost (5000)

Net loss (13000)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

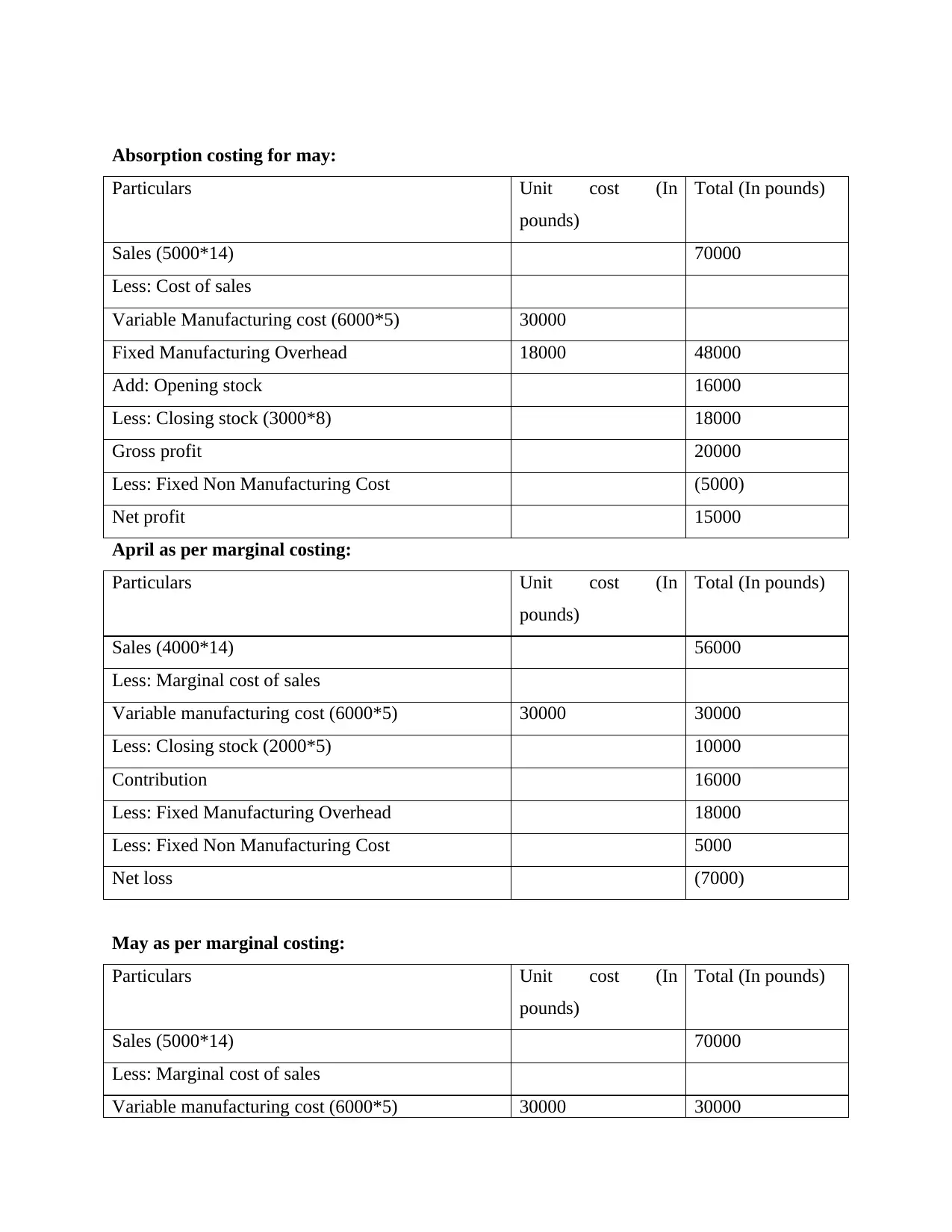

Absorption costing for may:

Particulars Unit cost (In

pounds)

Total (In pounds)

Sales (5000*14) 70000

Less: Cost of sales

Variable Manufacturing cost (6000*5) 30000

Fixed Manufacturing Overhead 18000 48000

Add: Opening stock 16000

Less: Closing stock (3000*8) 18000

Gross profit 20000

Less: Fixed Non Manufacturing Cost (5000)

Net profit 15000

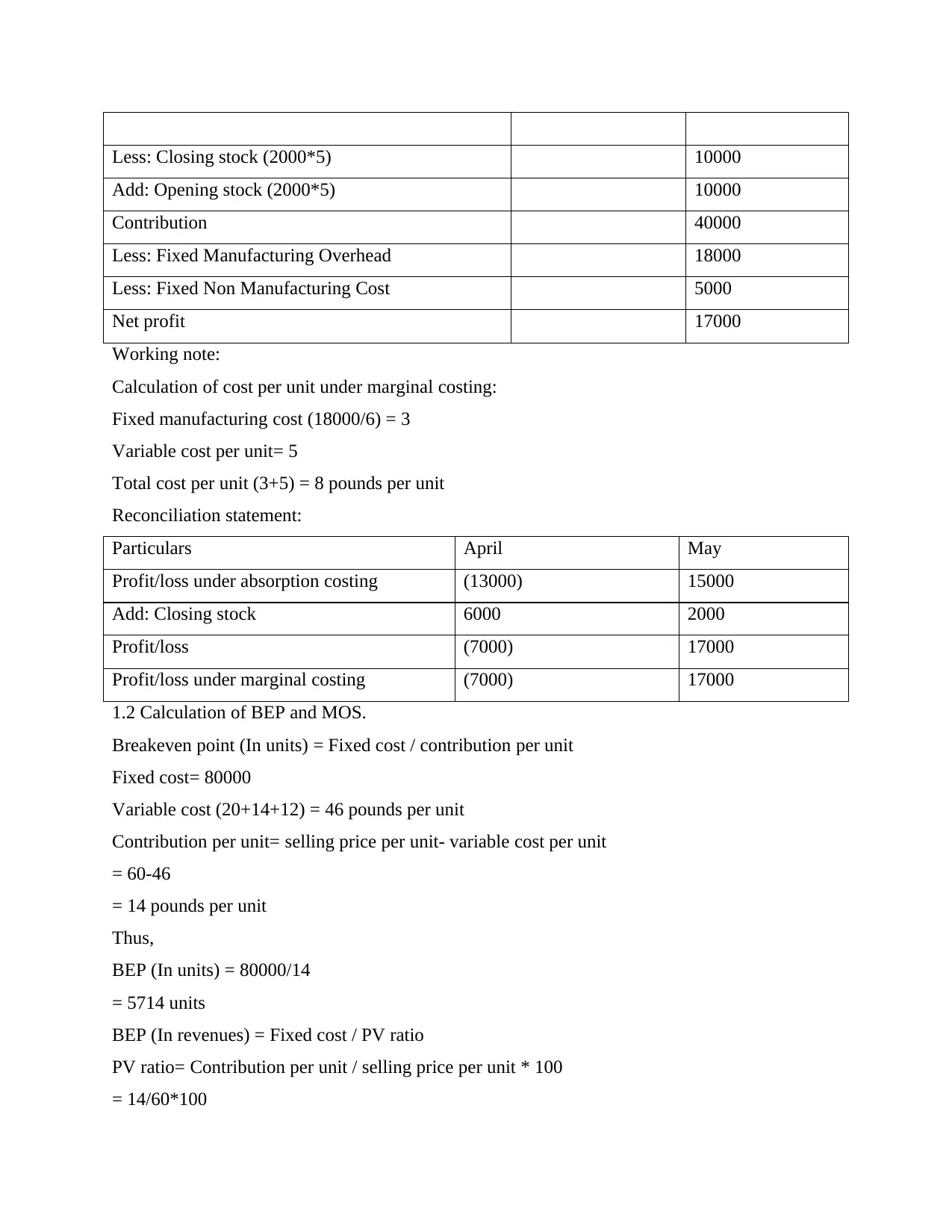

April as per marginal costing:

Particulars Unit cost (In

pounds)

Total (In pounds)

Sales (4000*14) 56000

Less: Marginal cost of sales

Variable manufacturing cost (6000*5) 30000 30000

Less: Closing stock (2000*5) 10000

Contribution 16000

Less: Fixed Manufacturing Overhead 18000

Less: Fixed Non Manufacturing Cost 5000

Net loss (7000)

May as per marginal costing:

Particulars Unit cost (In

pounds)

Total (In pounds)

Sales (5000*14) 70000

Less: Marginal cost of sales

Variable manufacturing cost (6000*5) 30000 30000

Particulars Unit cost (In

pounds)

Total (In pounds)

Sales (5000*14) 70000

Less: Cost of sales

Variable Manufacturing cost (6000*5) 30000

Fixed Manufacturing Overhead 18000 48000

Add: Opening stock 16000

Less: Closing stock (3000*8) 18000

Gross profit 20000

Less: Fixed Non Manufacturing Cost (5000)

Net profit 15000

April as per marginal costing:

Particulars Unit cost (In

pounds)

Total (In pounds)

Sales (4000*14) 56000

Less: Marginal cost of sales

Variable manufacturing cost (6000*5) 30000 30000

Less: Closing stock (2000*5) 10000

Contribution 16000

Less: Fixed Manufacturing Overhead 18000

Less: Fixed Non Manufacturing Cost 5000

Net loss (7000)

May as per marginal costing:

Particulars Unit cost (In

pounds)

Total (In pounds)

Sales (5000*14) 70000

Less: Marginal cost of sales

Variable manufacturing cost (6000*5) 30000 30000

Less: Closing stock (2000*5) 10000

Add: Opening stock (2000*5) 10000

Contribution 40000

Less: Fixed Manufacturing Overhead 18000

Less: Fixed Non Manufacturing Cost 5000

Net profit 17000

Working note:

Calculation of cost per unit under marginal costing:

Fixed manufacturing cost (18000/6) = 3

Variable cost per unit= 5

Total cost per unit (3+5) = 8 pounds per unit

Reconciliation statement:

Particulars April May

Profit/loss under absorption costing (13000) 15000

Add: Closing stock 6000 2000

Profit/loss (7000) 17000

Profit/loss under marginal costing (7000) 17000

1.2 Calculation of BEP and MOS.

Breakeven point (In units) = Fixed cost / contribution per unit

Fixed cost= 80000

Variable cost (20+14+12) = 46 pounds per unit

Contribution per unit= selling price per unit- variable cost per unit

= 60-46

= 14 pounds per unit

Thus,

BEP (In units) = 80000/14

= 5714 units

BEP (In revenues) = Fixed cost / PV ratio

PV ratio= Contribution per unit / selling price per unit * 100

= 14/60*100

Add: Opening stock (2000*5) 10000

Contribution 40000

Less: Fixed Manufacturing Overhead 18000

Less: Fixed Non Manufacturing Cost 5000

Net profit 17000

Working note:

Calculation of cost per unit under marginal costing:

Fixed manufacturing cost (18000/6) = 3

Variable cost per unit= 5

Total cost per unit (3+5) = 8 pounds per unit

Reconciliation statement:

Particulars April May

Profit/loss under absorption costing (13000) 15000

Add: Closing stock 6000 2000

Profit/loss (7000) 17000

Profit/loss under marginal costing (7000) 17000

1.2 Calculation of BEP and MOS.

Breakeven point (In units) = Fixed cost / contribution per unit

Fixed cost= 80000

Variable cost (20+14+12) = 46 pounds per unit

Contribution per unit= selling price per unit- variable cost per unit

= 60-46

= 14 pounds per unit

Thus,

BEP (In units) = 80000/14

= 5714 units

BEP (In revenues) = Fixed cost / PV ratio

PV ratio= Contribution per unit / selling price per unit * 100

= 14/60*100

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

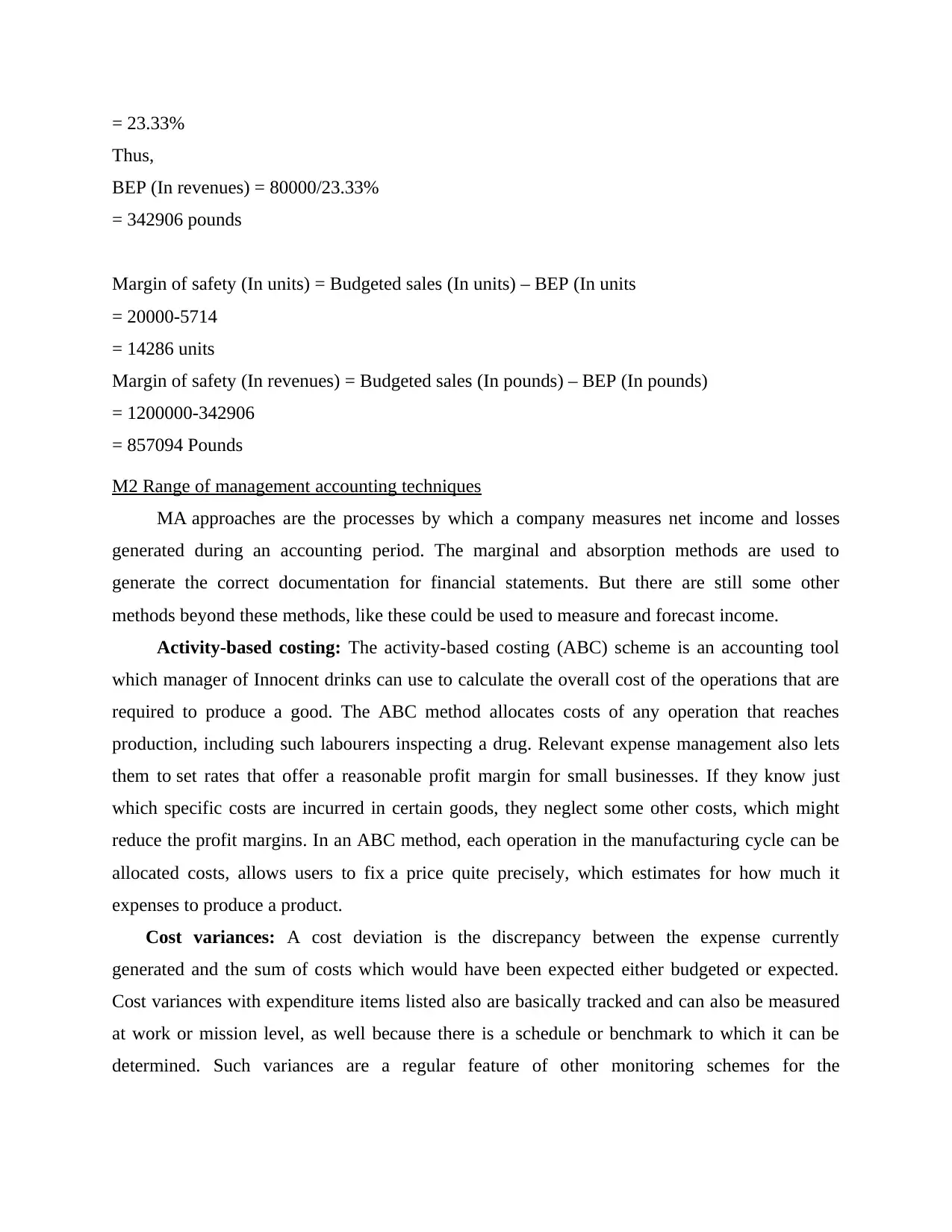

= 23.33%

Thus,

BEP (In revenues) = 80000/23.33%

= 342906 pounds

Margin of safety (In units) = Budgeted sales (In units) – BEP (In units

= 20000-5714

= 14286 units

Margin of safety (In revenues) = Budgeted sales (In pounds) – BEP (In pounds)

= 1200000-342906

= 857094 Pounds

M2 Range of management accounting techniques

MA approaches are the processes by which a company measures net income and losses

generated during an accounting period. The marginal and absorption methods are used to

generate the correct documentation for financial statements. But there are still some other

methods beyond these methods, like these could be used to measure and forecast income.

Activity-based costing: The activity-based costing (ABC) scheme is an accounting tool

which manager of Innocent drinks can use to calculate the overall cost of the operations that are

required to produce a good. The ABC method allocates costs of any operation that reaches

production, including such labourers inspecting a drug. Relevant expense management also lets

them to set rates that offer a reasonable profit margin for small businesses. If they know just

which specific costs are incurred in certain goods, they neglect some other costs, which might

reduce the profit margins. In an ABC method, each operation in the manufacturing cycle can be

allocated costs, allows users to fix a price quite precisely, which estimates for how much it

expenses to produce a product.

Cost variances: A cost deviation is the discrepancy between the expense currently

generated and the sum of costs which would have been expected either budgeted or expected.

Cost variances with expenditure items listed also are basically tracked and can also be measured

at work or mission level, as well because there is a schedule or benchmark to which it can be

determined. Such variances are a regular feature of other monitoring schemes for the

Thus,

BEP (In revenues) = 80000/23.33%

= 342906 pounds

Margin of safety (In units) = Budgeted sales (In units) – BEP (In units

= 20000-5714

= 14286 units

Margin of safety (In revenues) = Budgeted sales (In pounds) – BEP (In pounds)

= 1200000-342906

= 857094 Pounds

M2 Range of management accounting techniques

MA approaches are the processes by which a company measures net income and losses

generated during an accounting period. The marginal and absorption methods are used to

generate the correct documentation for financial statements. But there are still some other

methods beyond these methods, like these could be used to measure and forecast income.

Activity-based costing: The activity-based costing (ABC) scheme is an accounting tool

which manager of Innocent drinks can use to calculate the overall cost of the operations that are

required to produce a good. The ABC method allocates costs of any operation that reaches

production, including such labourers inspecting a drug. Relevant expense management also lets

them to set rates that offer a reasonable profit margin for small businesses. If they know just

which specific costs are incurred in certain goods, they neglect some other costs, which might

reduce the profit margins. In an ABC method, each operation in the manufacturing cycle can be

allocated costs, allows users to fix a price quite precisely, which estimates for how much it

expenses to produce a product.

Cost variances: A cost deviation is the discrepancy between the expense currently

generated and the sum of costs which would have been expected either budgeted or expected.

Cost variances with expenditure items listed also are basically tracked and can also be measured

at work or mission level, as well because there is a schedule or benchmark to which it can be

determined. Such variances are a regular feature of other monitoring schemes for the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

management of Innocent drinks. Any variances of prices are formally established into uniform

equations.

TASK 3

P4. Explanation of various planning tools used in budgetary control with proper benefits and

drawbacks.

A budget might be described as an estimate of income and expenses throughout a given

period, which is calculated which calculated on a timely manner. Budgetary monitoring is a

management control mechanism in which the real revenue and cost estimates are measured and

correlated with the expected cost and profits, so that the uncertainty and divergence can be

detected and appropriate steps need to be taken to increase productivity. Budgetary management

has various functions in which it can monitor the organisation, such as providing a robust system

of measures, conducting fund reviews, keeping the funds available, and tracking real budget

expenditures (Sims and Smith, 2016). Planning methods are the devices a company uses to plan

the budgets for the future. These techniques are used to manage a company's spending plans;

some of these techniques and their benefits and limitations are discussed below in the context of

Innocent drinks:

Production schedule: This forecasting method helps a company like Innocent drinks

to prepare for its potential growth by tracking its currently projected development costs and the

expected production units. Developing such production expenditure is used in an enterprise as a

conventional forecasting method for budgetary management.

The advantage of such a budget would be that it enables to quantify independently the

various manufacturing expenses like direct inventory costs, direct labour costs as well as other

operating costs from which Innocent drinks can use this budget to determine the cause of the

issue owing whereby the budget has also been overflowed. It also helps to determine the

production process which is increasing costs for company so that steps are made to remove such

operations. The disadvantage of this method is that separating any cost into a group is

complicated, because it is often hard to classify the type of the expenditure.

Master budget: This preparation mechanism is indeed a conventional budget built to

simplify the tasks of an organization's organizational managers (Soderstrom, Soderstrom and

equations.

TASK 3

P4. Explanation of various planning tools used in budgetary control with proper benefits and

drawbacks.

A budget might be described as an estimate of income and expenses throughout a given

period, which is calculated which calculated on a timely manner. Budgetary monitoring is a

management control mechanism in which the real revenue and cost estimates are measured and

correlated with the expected cost and profits, so that the uncertainty and divergence can be

detected and appropriate steps need to be taken to increase productivity. Budgetary management

has various functions in which it can monitor the organisation, such as providing a robust system

of measures, conducting fund reviews, keeping the funds available, and tracking real budget

expenditures (Sims and Smith, 2016). Planning methods are the devices a company uses to plan

the budgets for the future. These techniques are used to manage a company's spending plans;

some of these techniques and their benefits and limitations are discussed below in the context of

Innocent drinks:

Production schedule: This forecasting method helps a company like Innocent drinks

to prepare for its potential growth by tracking its currently projected development costs and the

expected production units. Developing such production expenditure is used in an enterprise as a

conventional forecasting method for budgetary management.

The advantage of such a budget would be that it enables to quantify independently the

various manufacturing expenses like direct inventory costs, direct labour costs as well as other

operating costs from which Innocent drinks can use this budget to determine the cause of the

issue owing whereby the budget has also been overflowed. It also helps to determine the

production process which is increasing costs for company so that steps are made to remove such

operations. The disadvantage of this method is that separating any cost into a group is

complicated, because it is often hard to classify the type of the expenditure.

Master budget: This preparation mechanism is indeed a conventional budget built to

simplify the tasks of an organization's organizational managers (Soderstrom, Soderstrom and

Stewart, 2017). Both expenditures are integrated in one framework so that when companies like

Innocent drinks manager can decide to compare their various budgets, money will be saved.

Considering the aforementioned review, it can be assumed that the advantages of master

budget is that it help to save time and providing a detailed summary of each operation within

company. As every other method, this budget does have its demerits that are absence

of specific information due to which there is greater room for uncertainty. It also require

professional person for understanding and estimating the figures for future due to which job cost

increase for company.

Zero-based budgeting: This planning method is a new and innovative form of budgetary

management where all spending for every year is explained and not by following the old pattern

for specific years. This budget contains features that apply mainly to a particular future time and

which make it more suited for project budgeting rather than whole organizations.

In the context of innocent drinks benefit of this method is that it provides the reason behind

all costs which protects the company from every economic recession. It also supports to maintain

a new budget for every new task or product which is added within company for the very first

time so that actual profitability can be analysed. The drawbacks of this technique are it also

supports in short term preparation so this involves the production of high expertise, time and

resources (Yalcin, 2012).

M3 Analyse of planning tools and their application.

Budgeting Forecasting

Budget means a structured financial estimate

for a given duration of revenue and spending.

It is a schedule for the money available to

accomplish the tasks, which needs to be

implemented, in order to meet the desired goal.

Budgeting details how the total program will

be implemented month by month, usually

including income and spending forecasts and

projected working capital including debt

reduction. At the start of a fiscal year,

businesses sometimes set their targets and

Forecasts are a straightforward prediction of

the possible course of events or patterns. It's a

forward-looking operation that involves

prediction. Prediction can be interpreted as the

estimation and understanding of the

circumstances that are expected to continue in

the near future, including regard to the

company's activities. Forecasts leverage

cumulative past evidence and business

dynamics to forecast upcoming years or

decades of financial results. The predictions

Innocent drinks manager can decide to compare their various budgets, money will be saved.

Considering the aforementioned review, it can be assumed that the advantages of master

budget is that it help to save time and providing a detailed summary of each operation within

company. As every other method, this budget does have its demerits that are absence

of specific information due to which there is greater room for uncertainty. It also require

professional person for understanding and estimating the figures for future due to which job cost

increase for company.

Zero-based budgeting: This planning method is a new and innovative form of budgetary

management where all spending for every year is explained and not by following the old pattern

for specific years. This budget contains features that apply mainly to a particular future time and

which make it more suited for project budgeting rather than whole organizations.

In the context of innocent drinks benefit of this method is that it provides the reason behind

all costs which protects the company from every economic recession. It also supports to maintain

a new budget for every new task or product which is added within company for the very first

time so that actual profitability can be analysed. The drawbacks of this technique are it also

supports in short term preparation so this involves the production of high expertise, time and

resources (Yalcin, 2012).

M3 Analyse of planning tools and their application.

Budgeting Forecasting

Budget means a structured financial estimate

for a given duration of revenue and spending.

It is a schedule for the money available to

accomplish the tasks, which needs to be

implemented, in order to meet the desired goal.

Budgeting details how the total program will

be implemented month by month, usually

including income and spending forecasts and

projected working capital including debt

reduction. At the start of a fiscal year,

businesses sometimes set their targets and

Forecasts are a straightforward prediction of

the possible course of events or patterns. It's a

forward-looking operation that involves

prediction. Prediction can be interpreted as the

estimation and understanding of the

circumstances that are expected to continue in

the near future, including regard to the

company's activities. Forecasts leverage

cumulative past evidence and business

dynamics to forecast upcoming years or

decades of financial results. The predictions

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.