Analyzing the Role of Management Accounting in Organizational Strategy

VerifiedAdded on 2020/06/03

|22

|5573

|26

AI Summary

Management accounting serves as a pivotal tool for businesses aiming to enhance their performance through informed strategic decisions and efficient resource allocation. This essay explores the significance of management accounting practices such as activity-based and zero-based budgeting in driving business success. By analyzing these techniques, the paper highlights how they contribute to cost control, improved financial decision-making, and overall organizational effectiveness. The discussion is supported by insights from various academic sources, providing a comprehensive understanding of management accounting's role in fostering sustainable business growth.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and its types..................................................................................1

P2. Explaining methods used in management accounting reporting..........................................6

M1. Application and advantages, disadvatages of Management accounting system.................8

D1. Integrating management accounting system within organisation........................................9

TASK 2..........................................................................................................................................10

P3. Income statement using different costing techniques.........................................................10

M2. Applying various management accounting techniques.....................................................11

D2. Interpreting financial reports..............................................................................................12

TASK 3..........................................................................................................................................12

P4. Advantages and disadvantages of budgetary control tools.................................................12

M3. Uses of different planning tools in forecasting budgets....................................................14

D3. Planning tools for solving financial problems...................................................................15

TASK 4..........................................................................................................................................16

P5 Use of management accounting system for responding financial problems........................16

M4. Sustainable organisation through responding financial problems.....................................18

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and its types..................................................................................1

P2. Explaining methods used in management accounting reporting..........................................6

M1. Application and advantages, disadvatages of Management accounting system.................8

D1. Integrating management accounting system within organisation........................................9

TASK 2..........................................................................................................................................10

P3. Income statement using different costing techniques.........................................................10

M2. Applying various management accounting techniques.....................................................11

D2. Interpreting financial reports..............................................................................................12

TASK 3..........................................................................................................................................12

P4. Advantages and disadvantages of budgetary control tools.................................................12

M3. Uses of different planning tools in forecasting budgets....................................................14

D3. Planning tools for solving financial problems...................................................................15

TASK 4..........................................................................................................................................16

P5 Use of management accounting system for responding financial problems........................16

M4. Sustainable organisation through responding financial problems.....................................18

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

INTRODUCTION

Management accounting is an essential part of accounting process in any organisation or

business concern. It is also known as managerial accounting. It is a tool for managers to analyse,

assess and evaluate various aspects of managerial accounting within an organisation. Various

techniques and methods used management accounting system facilitates financial information for

financial reporting and also helps in assessing performance of organisation as a whole and its

individual functions. In the present report different types of management accounting systems and

reports are explained along with their uses in the context of Unicorn Grocery store. It is a small

business of retail store based in UK with less than 50 employees. Main purpose of this report is

to explain how different methods, systems and techniques provides aid to managers and small

business owners in achieving their target objectives and goals along with helping them in making

future economic decisions. In order to fulfil purpose of this report, various topics and discussions

comes under its scope such as advantages of management accounting systems and how the

system can be integrated within an organisation. Further, financial statement has been prepared

for cited firm using two different techniques along with explaining difference between both.

Different planning tools that helps managers in forecasting future events that ultimately

facilitates sustainable growth of business are also explained bvelow.

TASK 1

P1. Management accounting and its types

Following are some types of management accounting system that can be used by Unicorn

Store for improving efficiency of its business operations.

Management accounting is an essential part of accounting process in any organisation or

business concern. It is also known as managerial accounting. It is a tool for managers to analyse,

assess and evaluate various aspects of managerial accounting within an organisation. Various

techniques and methods used management accounting system facilitates financial information for

financial reporting and also helps in assessing performance of organisation as a whole and its

individual functions. In the present report different types of management accounting systems and

reports are explained along with their uses in the context of Unicorn Grocery store. It is a small

business of retail store based in UK with less than 50 employees. Main purpose of this report is

to explain how different methods, systems and techniques provides aid to managers and small

business owners in achieving their target objectives and goals along with helping them in making

future economic decisions. In order to fulfil purpose of this report, various topics and discussions

comes under its scope such as advantages of management accounting systems and how the

system can be integrated within an organisation. Further, financial statement has been prepared

for cited firm using two different techniques along with explaining difference between both.

Different planning tools that helps managers in forecasting future events that ultimately

facilitates sustainable growth of business are also explained bvelow.

TASK 1

P1. Management accounting and its types

Following are some types of management accounting system that can be used by Unicorn

Store for improving efficiency of its business operations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

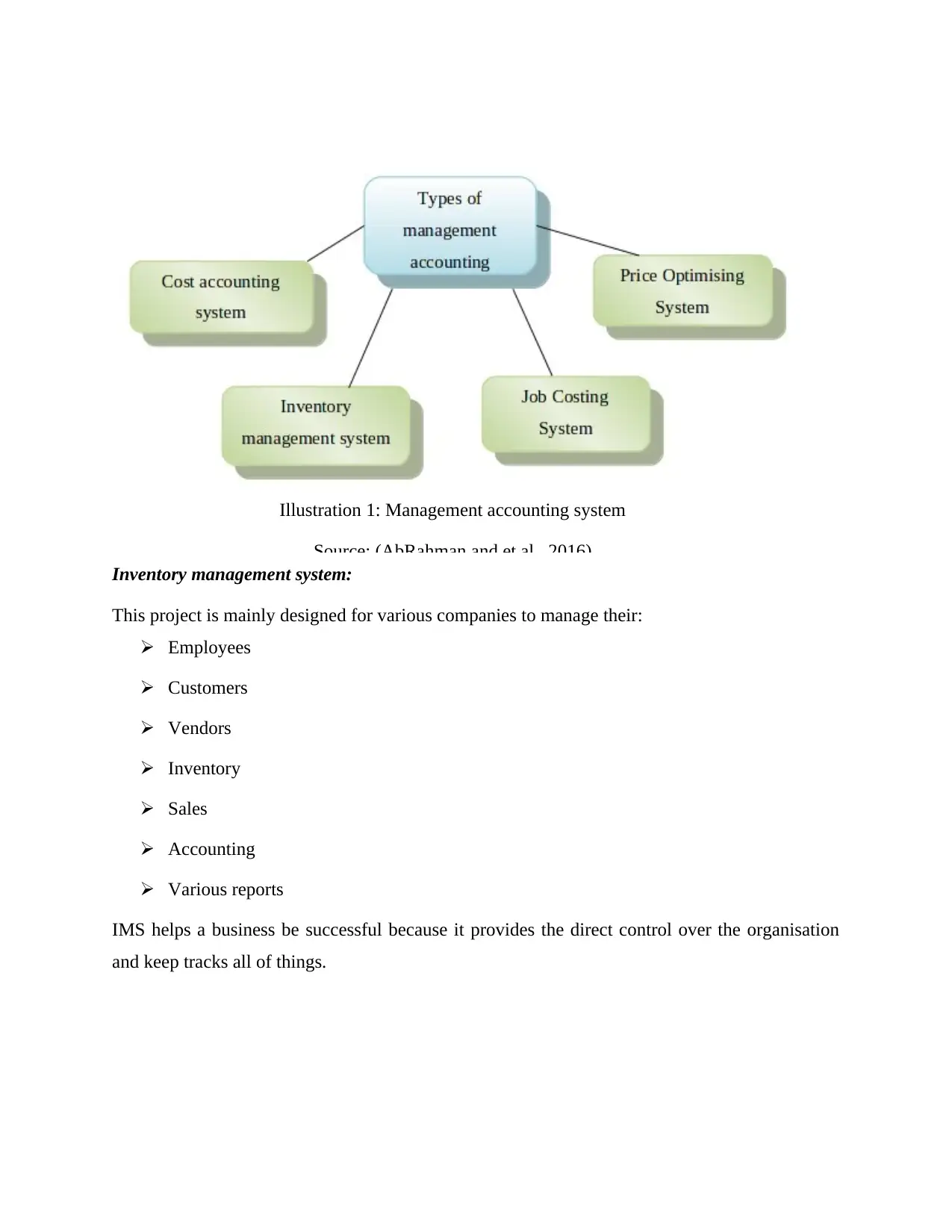

Illustration 1: Management accounting system

Source: (AbRahman and et.al., 2016)

Inventory management system:

This project is mainly designed for various companies to manage their:

Employees

Customers

Vendors

Inventory

Sales

Accounting

Various reports

IMS helps a business be successful because it provides the direct control over the organisation

and keep tracks all of things.

Source: (AbRahman and et.al., 2016)

Inventory management system:

This project is mainly designed for various companies to manage their:

Employees

Customers

Vendors

Inventory

Sales

Accounting

Various reports

IMS helps a business be successful because it provides the direct control over the organisation

and keep tracks all of things.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The project scope provide the user with a platform in which user will be to an update exactly

how much inventory is required to avoid shortage and wastage of products to get the better

turnover from the inventory (AbRahman and et.al., 2016). With the in company can:

Provide employee efficiency

Have accurate planning of keeping right amount of products.

Manages the vendors. Which plays a key role in the business

Keeps sales records, slips and manages the invoices.

Manages the accounts of company Will manage all amount of reports like invoice or history of customers, vendors and

inventory also.

Cost accounting system

Concepts of cost

Cost is the amount of resource which is given up in exchange of goods and services. The

resource given up is money expressed in monetary terms.

The charted institute of management accountants, London also defines cost as“the amount of

expenditure incurred on to specified thing or activity.

These kinds of activity involves expenditure under various heads, eg material, labour, other

expenses etc. Manufacturing organisation interested in ascertaining cost per unit of product

manufacture while an organisation who is rendering services eg, transport, canteen, electricity

company, municipality etc is interested in ascertain the cost of the services it renders. In simple

form it means the cost per unit is arrived by dividing the total expenditure incurred by the total

units produced (Bertz and Quinn, 2014). If the manufacture produces more than one product it

becomes imperative to split up the total expenditure between the various products so that the cost

of each product can be ascertained separately. For consumer cost means PRICE. For

management cost means EXPENDITURE. The process of ascertaining the cost is known as

costing.

how much inventory is required to avoid shortage and wastage of products to get the better

turnover from the inventory (AbRahman and et.al., 2016). With the in company can:

Provide employee efficiency

Have accurate planning of keeping right amount of products.

Manages the vendors. Which plays a key role in the business

Keeps sales records, slips and manages the invoices.

Manages the accounts of company Will manage all amount of reports like invoice or history of customers, vendors and

inventory also.

Cost accounting system

Concepts of cost

Cost is the amount of resource which is given up in exchange of goods and services. The

resource given up is money expressed in monetary terms.

The charted institute of management accountants, London also defines cost as“the amount of

expenditure incurred on to specified thing or activity.

These kinds of activity involves expenditure under various heads, eg material, labour, other

expenses etc. Manufacturing organisation interested in ascertaining cost per unit of product

manufacture while an organisation who is rendering services eg, transport, canteen, electricity

company, municipality etc is interested in ascertain the cost of the services it renders. In simple

form it means the cost per unit is arrived by dividing the total expenditure incurred by the total

units produced (Bertz and Quinn, 2014). If the manufacture produces more than one product it

becomes imperative to split up the total expenditure between the various products so that the cost

of each product can be ascertained separately. For consumer cost means PRICE. For

management cost means EXPENDITURE. The process of ascertaining the cost is known as

costing.

It is necessary to specify the exact meaning of cost. When the term is used specifically it is

modified with terms as prime cost, fixed cost, sunk cost etc. To ascertaining these there are three

basic objectives namely- cost ascertainment, cost control and cost presentation.

General principles of cost accounting:

1. A cost should be related to its cause.

2. A cost should be charged only after it has been incurred.

3. The convention of prudence should be ignored (Bryer, 2013).

4. Abnormal cost should be excluded from cost accounts.

5. Past cost not to be charged to future period.

6. Principles of double entry should be applied wherever necessary.

Objectives of cost accounting

To analyse all expenditure with reference to the cost products.

To arrive at the cost of production every unit, job, operations should be analysed

To provide data’s for profit and loss accounts and balance sheets at regular intervals such

as weekly, monthly, yearly.

To provide actual cost and figures for estimations the price fixing policy should be

checked.

To present comparative cost data for different periods. This is also helpful in budgetary

control (Chan, 2015).

Last but not least, all information should be provided to the management to make the

short term decisions at various level like quotation of prices or make or buy decisions etc.

Importance of costing

Cost accounting helps in periods of trade depressions and trade competition

Cost accounting helps in price fixation

Cost accounting helps in making estimates

Cost accounting makes comparisons possible

modified with terms as prime cost, fixed cost, sunk cost etc. To ascertaining these there are three

basic objectives namely- cost ascertainment, cost control and cost presentation.

General principles of cost accounting:

1. A cost should be related to its cause.

2. A cost should be charged only after it has been incurred.

3. The convention of prudence should be ignored (Bryer, 2013).

4. Abnormal cost should be excluded from cost accounts.

5. Past cost not to be charged to future period.

6. Principles of double entry should be applied wherever necessary.

Objectives of cost accounting

To analyse all expenditure with reference to the cost products.

To arrive at the cost of production every unit, job, operations should be analysed

To provide data’s for profit and loss accounts and balance sheets at regular intervals such

as weekly, monthly, yearly.

To provide actual cost and figures for estimations the price fixing policy should be

checked.

To present comparative cost data for different periods. This is also helpful in budgetary

control (Chan, 2015).

Last but not least, all information should be provided to the management to make the

short term decisions at various level like quotation of prices or make or buy decisions etc.

Importance of costing

Cost accounting helps in periods of trade depressions and trade competition

Cost accounting helps in price fixation

Cost accounting helps in making estimates

Cost accounting makes comparisons possible

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost accounting eliminates wastages.

Cost accounting helps in inventory control

Cost accounting helps in enhancing efficiency

Cost accounting helps in channelizing production in right areas.

Job-Costing system

Job costing is that form of costing which applies where work is under taken to customers

special requirement in short duration (Groot and Selto, 2013). These kinds of works are generally

carried out in a factory or workshops. Eg, construction jobs, Engineering jobs, printing, furniture

making, fabrication jobs etc.

Features

It is a specific order costing.

The job is carried out or product is produced to meet the specific requirements of order.

It is concerned with the cost of individual job or batch, but normally short duration of

time.

Cost is collected at the end of its completion.

Cost of job ia ascertained by adding material, labour and overheads.

Work in progress may or may not exist in the end of the accounting year.

Advantages

The profit or loss can be easily measured.

It generates data cost which is useful for analysis and management control.

It shows whether the job is profitable or not (Joshi and Li, 2016).

Job costing enables comparison with other jobs so that inefficiencies identified and after

that rectified.

Disadvantages

Time consuming process.

Cost accounting helps in inventory control

Cost accounting helps in enhancing efficiency

Cost accounting helps in channelizing production in right areas.

Job-Costing system

Job costing is that form of costing which applies where work is under taken to customers

special requirement in short duration (Groot and Selto, 2013). These kinds of works are generally

carried out in a factory or workshops. Eg, construction jobs, Engineering jobs, printing, furniture

making, fabrication jobs etc.

Features

It is a specific order costing.

The job is carried out or product is produced to meet the specific requirements of order.

It is concerned with the cost of individual job or batch, but normally short duration of

time.

Cost is collected at the end of its completion.

Cost of job ia ascertained by adding material, labour and overheads.

Work in progress may or may not exist in the end of the accounting year.

Advantages

The profit or loss can be easily measured.

It generates data cost which is useful for analysis and management control.

It shows whether the job is profitable or not (Joshi and Li, 2016).

Job costing enables comparison with other jobs so that inefficiencies identified and after

that rectified.

Disadvantages

Time consuming process.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Expensive

P2. Explaining methods used in management accounting reporting

Illustration 2: Management accounting reports

Source: (Khodzytska and Ivchenko, 2014)

Management accounting reports are also known as cost accounting reports. Which are

basically designed to offer internal information to organisation or companies through financial

accounting? The main purpose of management accounting reports is to help is to planning,

monitoring, determining decision. Management accountants depends upon standard financial

reports such as

Balance sheet

Income reports

Cash reports

Other management accounting reports

P2. Explaining methods used in management accounting reporting

Illustration 2: Management accounting reports

Source: (Khodzytska and Ivchenko, 2014)

Management accounting reports are also known as cost accounting reports. Which are

basically designed to offer internal information to organisation or companies through financial

accounting? The main purpose of management accounting reports is to help is to planning,

monitoring, determining decision. Management accountants depends upon standard financial

reports such as

Balance sheet

Income reports

Cash reports

Other management accounting reports

Management accountants use information not only financial but accounting as well as

management skills (Khodzytska and Ivchenko, 2014). Few of the above mentioned reports are

explained as below that can be used by Unicorn Store:

Cost reports

Cost reports help management accountant to calculate cost of items that are produced

through to unprocessed data. Such data includes:

Cost of products

Overheads

Labour cost etc

Cost reports are also called management accounting reports which are used for the purpose of

planning and profit margins.

Budget reports

With many types of management accounting reports, the budget reports are also an

important report. The main purpose of budget report is to create budget from previous years data

to make future predictions (Klemstine and Maher, 2014). Supply of revenues and expenses must

be in the budget reports and company must work within the amount that has been calculated in

the budget.

Budget reports help small company owners to analyse their performance. If there is big

company owners managers should analyse departments control cost. If small business owners

were over budget in the previous year and can’t trim their cost, the budget for future years needs

to be increased to a more accurate level. Owners and managers use budget reports to give

incentives to their employees, as well as for giving bonus also for meeting their specific goals.

Performance report

Another type of management accounting report is performance report. These kinds of

reports are used by management accountants to analyse expenditures and revenues to amounts

that have been allocated. These inequalities are computed to help in deciding new budget. These

management skills (Khodzytska and Ivchenko, 2014). Few of the above mentioned reports are

explained as below that can be used by Unicorn Store:

Cost reports

Cost reports help management accountant to calculate cost of items that are produced

through to unprocessed data. Such data includes:

Cost of products

Overheads

Labour cost etc

Cost reports are also called management accounting reports which are used for the purpose of

planning and profit margins.

Budget reports

With many types of management accounting reports, the budget reports are also an

important report. The main purpose of budget report is to create budget from previous years data

to make future predictions (Klemstine and Maher, 2014). Supply of revenues and expenses must

be in the budget reports and company must work within the amount that has been calculated in

the budget.

Budget reports help small company owners to analyse their performance. If there is big

company owners managers should analyse departments control cost. If small business owners

were over budget in the previous year and can’t trim their cost, the budget for future years needs

to be increased to a more accurate level. Owners and managers use budget reports to give

incentives to their employees, as well as for giving bonus also for meeting their specific goals.

Performance report

Another type of management accounting report is performance report. These kinds of

reports are used by management accountants to analyse expenditures and revenues to amounts

that have been allocated. These inequalities are computed to help in deciding new budget. These

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

reports are computed annually although there are many companies who compute monthly or

quarterly reports (McLellan and Sherine, 2013). These reports are compiled with the data from

economic accounting. Accounting reports are one of the necessities for planned management

economy.

Accounting reports are submitted to higher authority of ministry to credit and financing

institution of HSBC and Bank of England to central statistical administration and local bodies.

Accounting reports which are submitted to higher authority are signed by head and the chief

accountant of the organisation. Copies should be send to all addresses are certified by the chief

accountant. Periodic accounting reports should be submitted not later than 15th of the month. And

annual accounting report should be submitted not later than 25thjanuary of the following year

under review. Higher organisation considers and approves accounting reports within 15 days of

the day reports are received.

M1. Application and advantages, disadvatages of Management accounting system

As discussed above various types of management accounting system and the types of

report, these can benefit unicorn grocery in number of ways:

This will help the management of Unicorn in estimating the cost of their products and

services and also that segment of products that are most profitable (Nørreklit, 2014).

Use of management accounting system will help in forecasting the future trends through

management can prepare various policies accordingly.

Management accounting system will help the management in making various future

economic decisions regarding the activities that need to be closed down and those that

need to be started.

Forecasting of future cash inflow and outflow is possible to determine and the impact of

the same to business unit.

This also helps in identifying the areas for future business expansions.

quarterly reports (McLellan and Sherine, 2013). These reports are compiled with the data from

economic accounting. Accounting reports are one of the necessities for planned management

economy.

Accounting reports are submitted to higher authority of ministry to credit and financing

institution of HSBC and Bank of England to central statistical administration and local bodies.

Accounting reports which are submitted to higher authority are signed by head and the chief

accountant of the organisation. Copies should be send to all addresses are certified by the chief

accountant. Periodic accounting reports should be submitted not later than 15th of the month. And

annual accounting report should be submitted not later than 25thjanuary of the following year

under review. Higher organisation considers and approves accounting reports within 15 days of

the day reports are received.

M1. Application and advantages, disadvatages of Management accounting system

As discussed above various types of management accounting system and the types of

report, these can benefit unicorn grocery in number of ways:

This will help the management of Unicorn in estimating the cost of their products and

services and also that segment of products that are most profitable (Nørreklit, 2014).

Use of management accounting system will help in forecasting the future trends through

management can prepare various policies accordingly.

Management accounting system will help the management in making various future

economic decisions regarding the activities that need to be closed down and those that

need to be started.

Forecasting of future cash inflow and outflow is possible to determine and the impact of

the same to business unit.

This also helps in identifying the areas for future business expansions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Through this management can also determine the variations in forecasted budgets of cost

and sales and actual amount of expenses and sales volume.

However, these techniques will be helpful for the business in terms of making the

adequate improvement in the operational or financial performance. Therefore, such techniques

will increase the productivity as well as make the adequate increment in efficiency of firm.

D1. Integrating management accounting system within organisation

As the need of management accounting has been discussed in the above report. The need

of its integration within the organisation also increases (Fullerton, Kennedy and Widener, 2013).

Before integrating management accounting management should identify the key areas that

require integration System of management accounting can be integrated in Unicorn grocery by:

Setting the prices of different segments of products and services.

By providing cost centres of goods and services.

Preparation of budgets for various activities in different departments.

Preparing centralised budget for the company as a whole.

Developing budgets for staff development.

By conducting personal meetings and interview with key personnel of the organisation.

Identifying best practices that are required by the organisation.

Explaining purpose of integrating management system to the employees.

In terms with making the improvements in the operational activities of the business there

can be need to analyse the requirements of funds, efforts in any business tasks. The managers of

Unicorn must concentrate over utilisation resources in consideration with the market needs and

wants.

and sales and actual amount of expenses and sales volume.

However, these techniques will be helpful for the business in terms of making the

adequate improvement in the operational or financial performance. Therefore, such techniques

will increase the productivity as well as make the adequate increment in efficiency of firm.

D1. Integrating management accounting system within organisation

As the need of management accounting has been discussed in the above report. The need

of its integration within the organisation also increases (Fullerton, Kennedy and Widener, 2013).

Before integrating management accounting management should identify the key areas that

require integration System of management accounting can be integrated in Unicorn grocery by:

Setting the prices of different segments of products and services.

By providing cost centres of goods and services.

Preparation of budgets for various activities in different departments.

Preparing centralised budget for the company as a whole.

Developing budgets for staff development.

By conducting personal meetings and interview with key personnel of the organisation.

Identifying best practices that are required by the organisation.

Explaining purpose of integrating management system to the employees.

In terms with making the improvements in the operational activities of the business there

can be need to analyse the requirements of funds, efforts in any business tasks. The managers of

Unicorn must concentrate over utilisation resources in consideration with the market needs and

wants.

TASK 2

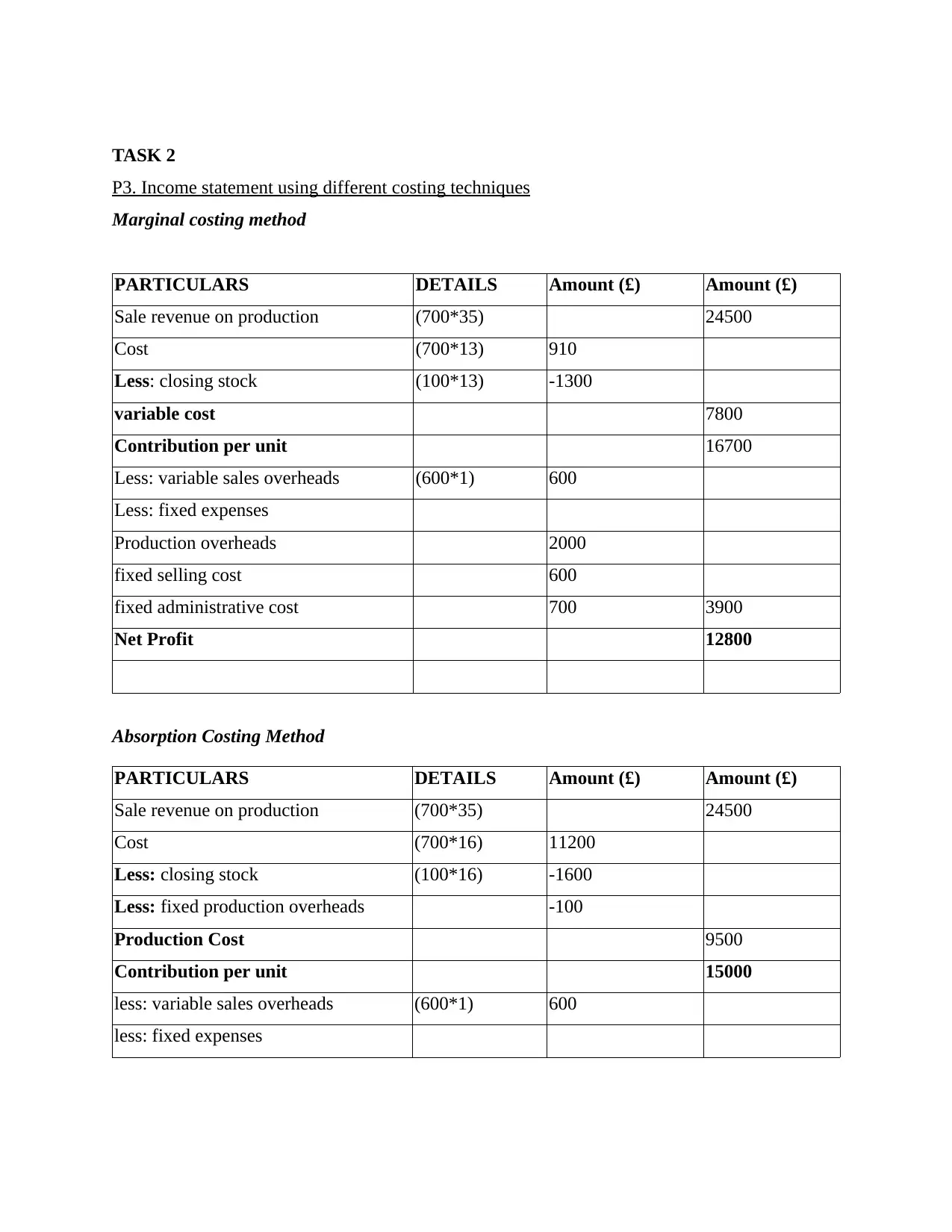

P3. Income statement using different costing techniques

Marginal costing method

PARTICULARS DETAILS Amount (£) Amount (£)

Sale revenue on production (700*35) 24500

Cost (700*13) 910

Less: closing stock (100*13) -1300

variable cost 7800

Contribution per unit 16700

Less: variable sales overheads (600*1) 600

Less: fixed expenses

Production overheads 2000

fixed selling cost 600

fixed administrative cost 700 3900

Net Profit 12800

Absorption Costing Method

PARTICULARS DETAILS Amount (£) Amount (£)

Sale revenue on production (700*35) 24500

Cost (700*16) 11200

Less: closing stock (100*16) -1600

Less: fixed production overheads -100

Production Cost 9500

Contribution per unit 15000

less: variable sales overheads (600*1) 600

less: fixed expenses

P3. Income statement using different costing techniques

Marginal costing method

PARTICULARS DETAILS Amount (£) Amount (£)

Sale revenue on production (700*35) 24500

Cost (700*13) 910

Less: closing stock (100*13) -1300

variable cost 7800

Contribution per unit 16700

Less: variable sales overheads (600*1) 600

Less: fixed expenses

Production overheads 2000

fixed selling cost 600

fixed administrative cost 700 3900

Net Profit 12800

Absorption Costing Method

PARTICULARS DETAILS Amount (£) Amount (£)

Sale revenue on production (700*35) 24500

Cost (700*16) 11200

Less: closing stock (100*16) -1600

Less: fixed production overheads -100

Production Cost 9500

Contribution per unit 15000

less: variable sales overheads (600*1) 600

less: fixed expenses

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.