Management Accounting

VerifiedAdded on 2023/01/18

|14

|1852

|50

AI Summary

Find comprehensive study material and solved assignments on Management Accounting at Desklib. Get essays, dissertations, and more for your management courses.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT ACCOUNTING 1

MANAGEMENT

ACCOUNTING

MANAGEMENT

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MANAGEMENT ACCOUNTING 2

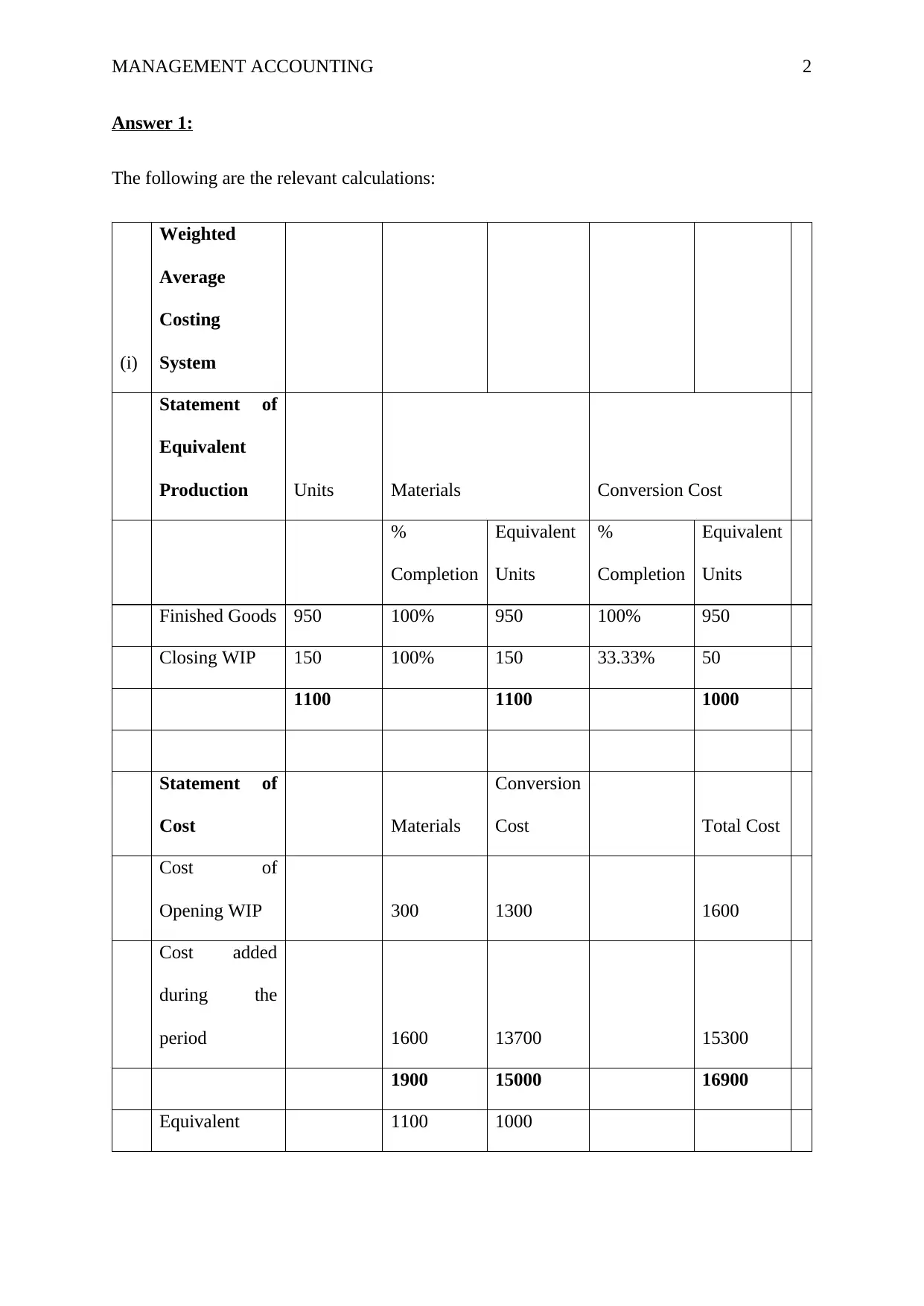

Answer 1:

The following are the relevant calculations:

(i)

Weighted

Average

Costing

System

Statement of

Equivalent

Production Units Materials Conversion Cost

%

Completion

Equivalent

Units

%

Completion

Equivalent

Units

Finished Goods 950 100% 950 100% 950

Closing WIP 150 100% 150 33.33% 50

1100 1100 1000

Statement of

Cost Materials

Conversion

Cost Total Cost

Cost of

Opening WIP 300 1300 1600

Cost added

during the

period 1600 13700 15300

1900 15000 16900

Equivalent 1100 1000

Answer 1:

The following are the relevant calculations:

(i)

Weighted

Average

Costing

System

Statement of

Equivalent

Production Units Materials Conversion Cost

%

Completion

Equivalent

Units

%

Completion

Equivalent

Units

Finished Goods 950 100% 950 100% 950

Closing WIP 150 100% 150 33.33% 50

1100 1100 1000

Statement of

Cost Materials

Conversion

Cost Total Cost

Cost of

Opening WIP 300 1300 1600

Cost added

during the

period 1600 13700 15300

1900 15000 16900

Equivalent 1100 1000

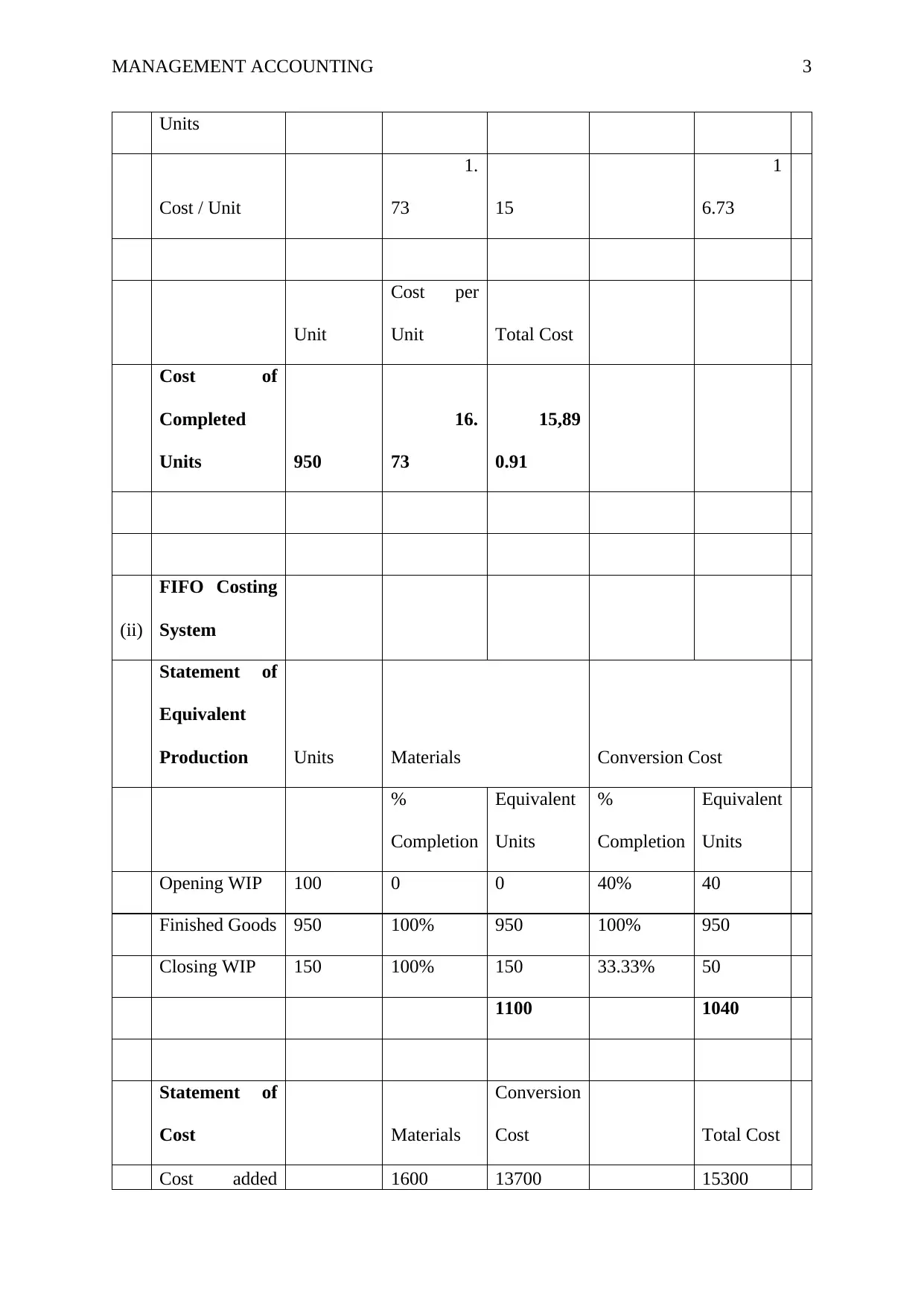

MANAGEMENT ACCOUNTING 3

Units

Cost / Unit

1.

73 15

1

6.73

Unit

Cost per

Unit Total Cost

Cost of

Completed

Units 950

16.

73

15,89

0.91

(ii)

FIFO Costing

System

Statement of

Equivalent

Production Units Materials Conversion Cost

%

Completion

Equivalent

Units

%

Completion

Equivalent

Units

Opening WIP 100 0 0 40% 40

Finished Goods 950 100% 950 100% 950

Closing WIP 150 100% 150 33.33% 50

1100 1040

Statement of

Cost Materials

Conversion

Cost Total Cost

Cost added 1600 13700 15300

Units

Cost / Unit

1.

73 15

1

6.73

Unit

Cost per

Unit Total Cost

Cost of

Completed

Units 950

16.

73

15,89

0.91

(ii)

FIFO Costing

System

Statement of

Equivalent

Production Units Materials Conversion Cost

%

Completion

Equivalent

Units

%

Completion

Equivalent

Units

Opening WIP 100 0 0 40% 40

Finished Goods 950 100% 950 100% 950

Closing WIP 150 100% 150 33.33% 50

1100 1040

Statement of

Cost Materials

Conversion

Cost Total Cost

Cost added 1600 13700 15300

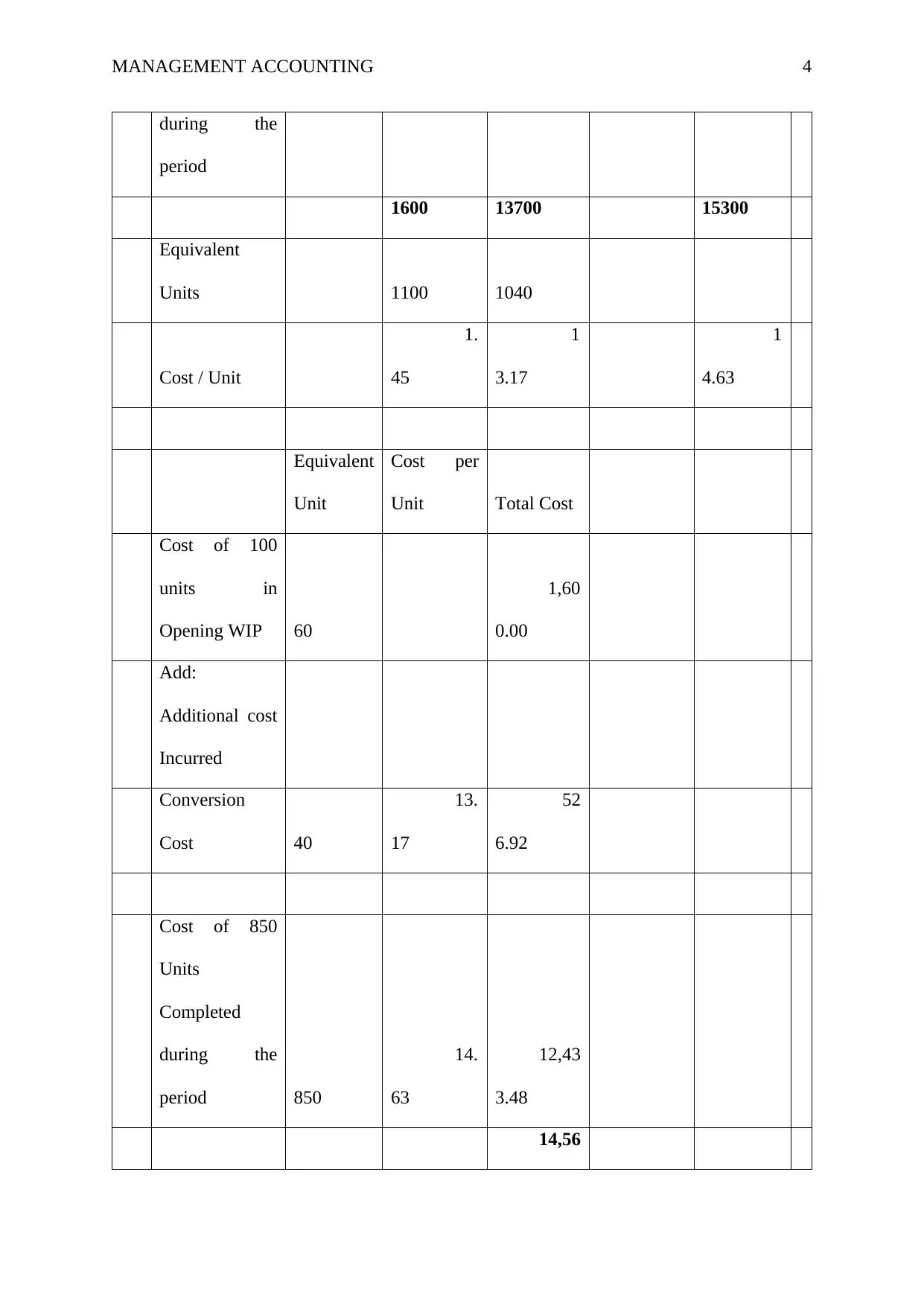

MANAGEMENT ACCOUNTING 4

during the

period

1600 13700 15300

Equivalent

Units 1100 1040

Cost / Unit

1.

45

1

3.17

1

4.63

Equivalent

Unit

Cost per

Unit Total Cost

Cost of 100

units in

Opening WIP 60

1,60

0.00

Add:

Additional cost

Incurred

Conversion

Cost 40

13.

17

52

6.92

Cost of 850

Units

Completed

during the

period 850

14.

63

12,43

3.48

14,56

during the

period

1600 13700 15300

Equivalent

Units 1100 1040

Cost / Unit

1.

45

1

3.17

1

4.63

Equivalent

Unit

Cost per

Unit Total Cost

Cost of 100

units in

Opening WIP 60

1,60

0.00

Add:

Additional cost

Incurred

Conversion

Cost 40

13.

17

52

6.92

Cost of 850

Units

Completed

during the

period 850

14.

63

12,43

3.48

14,56

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MANAGEMENT ACCOUNTING 5

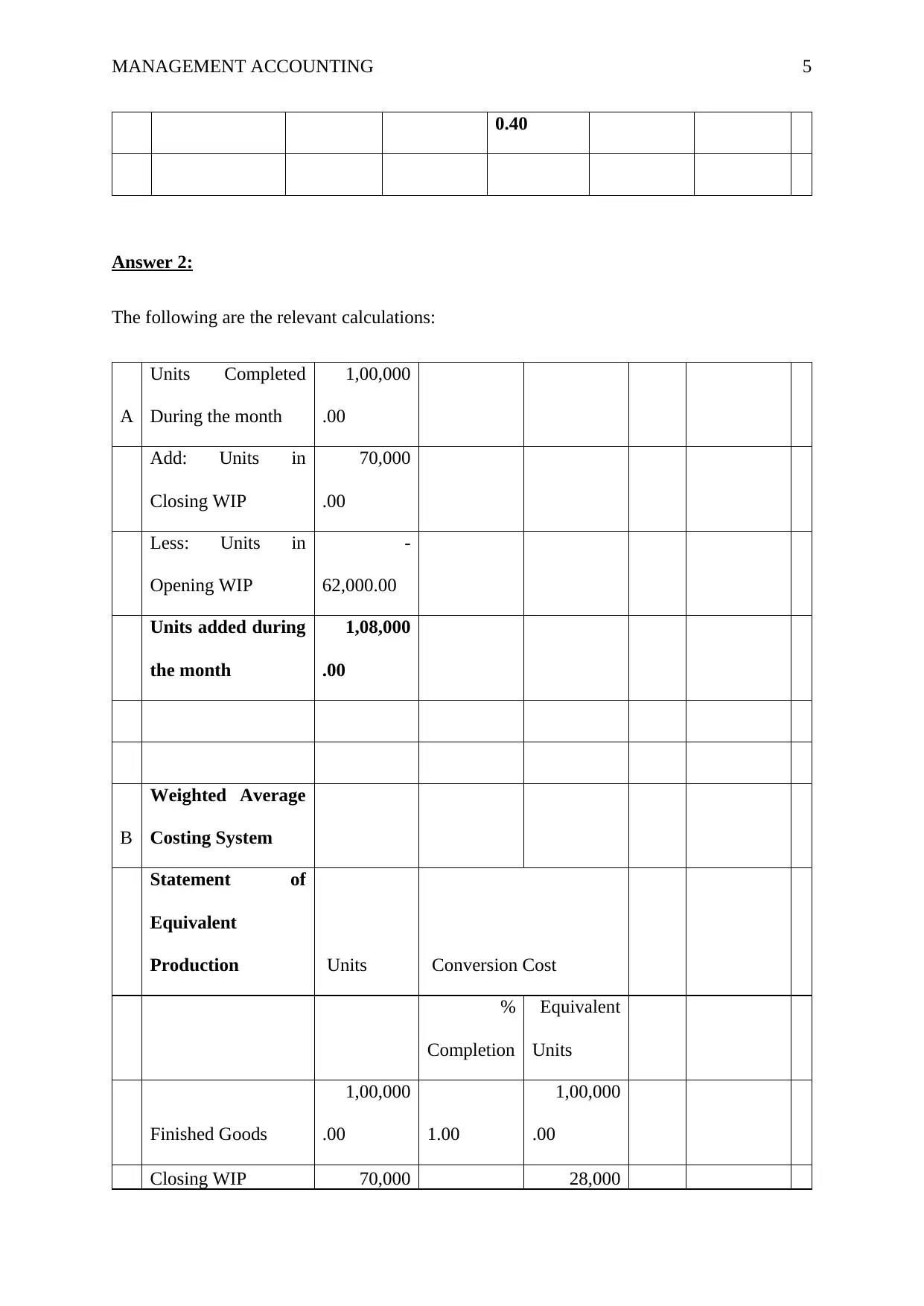

0.40

Answer 2:

The following are the relevant calculations:

A

Units Completed

During the month

1,00,000

.00

Add: Units in

Closing WIP

70,000

.00

Less: Units in

Opening WIP

-

62,000.00

Units added during

the month

1,08,000

.00

B

Weighted Average

Costing System

Statement of

Equivalent

Production Units Conversion Cost

%

Completion

Equivalent

Units

Finished Goods

1,00,000

.00 1.00

1,00,000

.00

Closing WIP 70,000 28,000

0.40

Answer 2:

The following are the relevant calculations:

A

Units Completed

During the month

1,00,000

.00

Add: Units in

Closing WIP

70,000

.00

Less: Units in

Opening WIP

-

62,000.00

Units added during

the month

1,08,000

.00

B

Weighted Average

Costing System

Statement of

Equivalent

Production Units Conversion Cost

%

Completion

Equivalent

Units

Finished Goods

1,00,000

.00 1.00

1,00,000

.00

Closing WIP 70,000 28,000

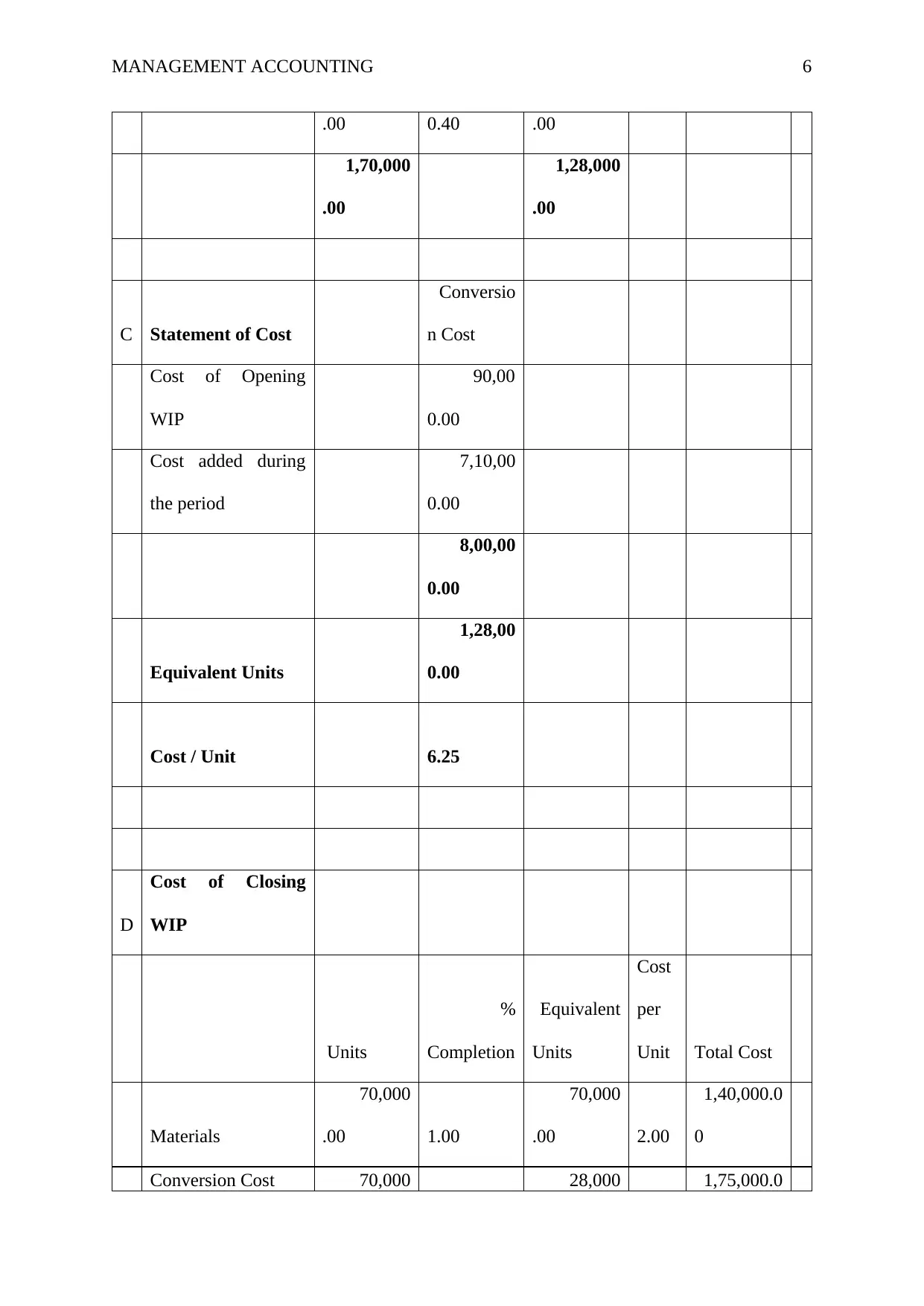

MANAGEMENT ACCOUNTING 6

.00 0.40 .00

1,70,000

.00

1,28,000

.00

C Statement of Cost

Conversio

n Cost

Cost of Opening

WIP

90,00

0.00

Cost added during

the period

7,10,00

0.00

8,00,00

0.00

Equivalent Units

1,28,00

0.00

Cost / Unit 6.25

D

Cost of Closing

WIP

Units

%

Completion

Equivalent

Units

Cost

per

Unit Total Cost

Materials

70,000

.00 1.00

70,000

.00 2.00

1,40,000.0

0

Conversion Cost 70,000 28,000 1,75,000.0

.00 0.40 .00

1,70,000

.00

1,28,000

.00

C Statement of Cost

Conversio

n Cost

Cost of Opening

WIP

90,00

0.00

Cost added during

the period

7,10,00

0.00

8,00,00

0.00

Equivalent Units

1,28,00

0.00

Cost / Unit 6.25

D

Cost of Closing

WIP

Units

%

Completion

Equivalent

Units

Cost

per

Unit Total Cost

Materials

70,000

.00 1.00

70,000

.00 2.00

1,40,000.0

0

Conversion Cost 70,000 28,000 1,75,000.0

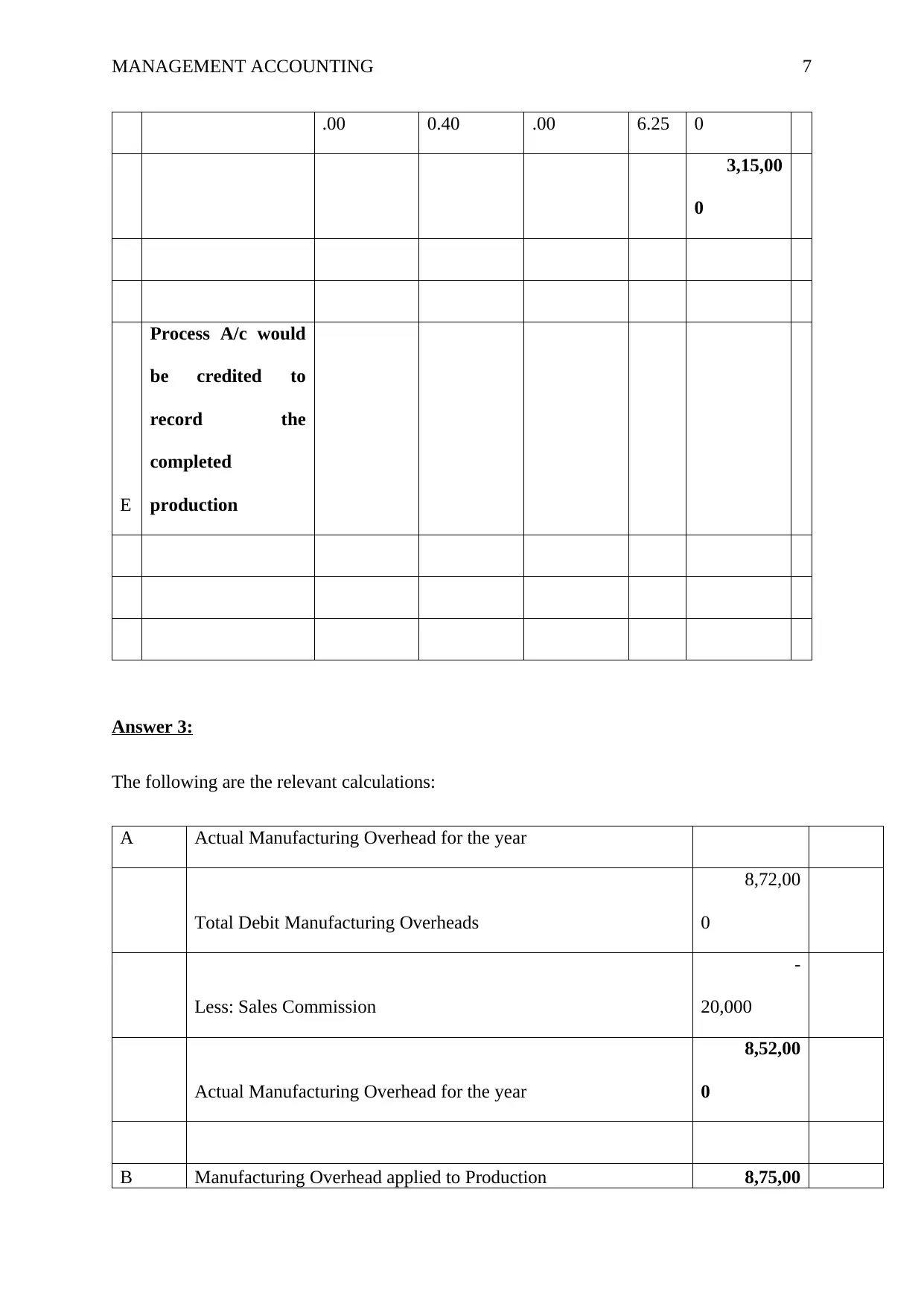

MANAGEMENT ACCOUNTING 7

.00 0.40 .00 6.25 0

3,15,00

0

E

Process A/c would

be credited to

record the

completed

production

Answer 3:

The following are the relevant calculations:

A Actual Manufacturing Overhead for the year

Total Debit Manufacturing Overheads

8,72,00

0

Less: Sales Commission

-

20,000

Actual Manufacturing Overhead for the year

8,52,00

0

B Manufacturing Overhead applied to Production 8,75,00

.00 0.40 .00 6.25 0

3,15,00

0

E

Process A/c would

be credited to

record the

completed

production

Answer 3:

The following are the relevant calculations:

A Actual Manufacturing Overhead for the year

Total Debit Manufacturing Overheads

8,72,00

0

Less: Sales Commission

-

20,000

Actual Manufacturing Overhead for the year

8,52,00

0

B Manufacturing Overhead applied to Production 8,75,00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

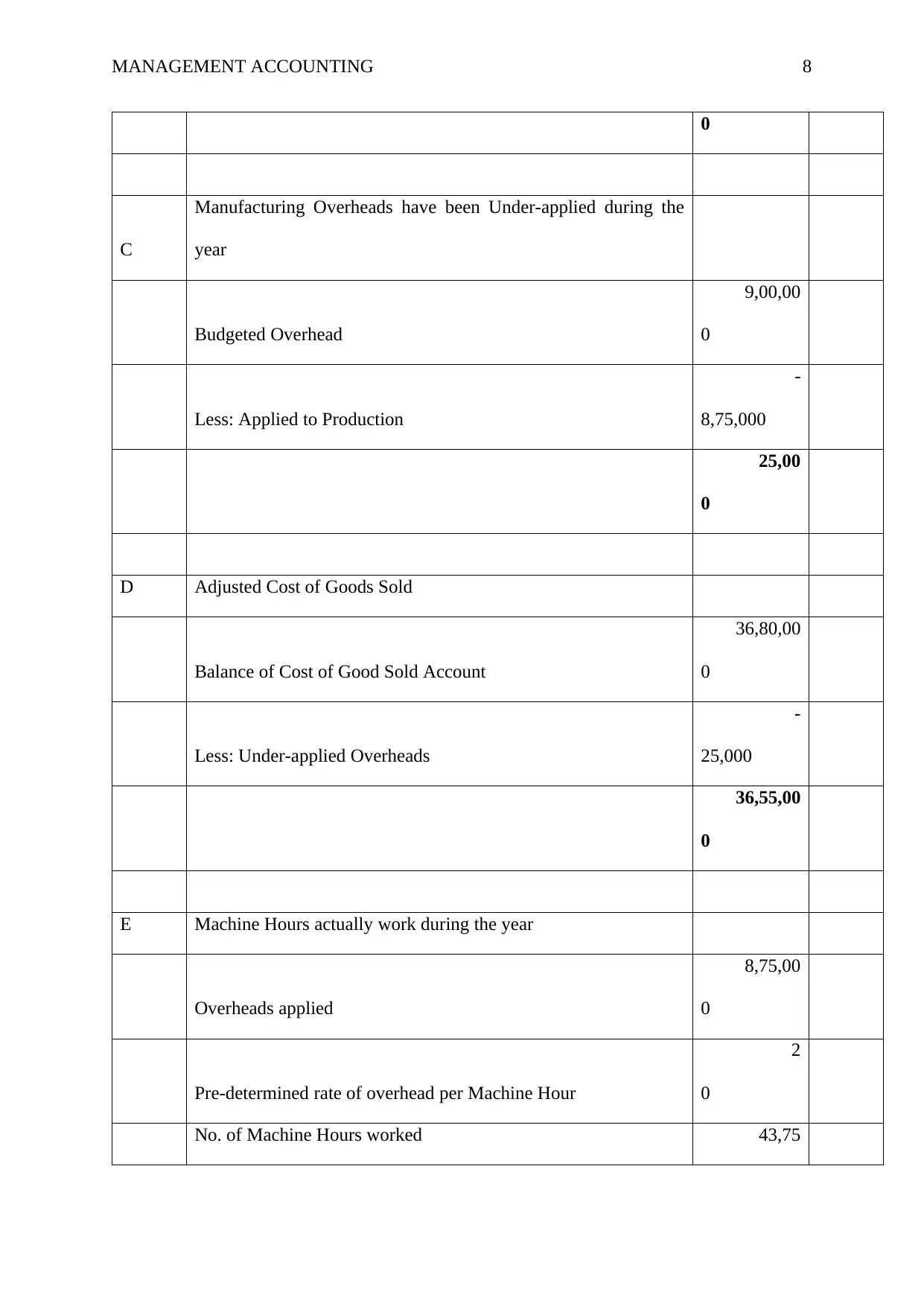

MANAGEMENT ACCOUNTING 8

0

C

Manufacturing Overheads have been Under-applied during the

year

Budgeted Overhead

9,00,00

0

Less: Applied to Production

-

8,75,000

25,00

0

D Adjusted Cost of Goods Sold

Balance of Cost of Good Sold Account

36,80,00

0

Less: Under-applied Overheads

-

25,000

36,55,00

0

E Machine Hours actually work during the year

Overheads applied

8,75,00

0

Pre-determined rate of overhead per Machine Hour

2

0

No. of Machine Hours worked 43,75

0

C

Manufacturing Overheads have been Under-applied during the

year

Budgeted Overhead

9,00,00

0

Less: Applied to Production

-

8,75,000

25,00

0

D Adjusted Cost of Goods Sold

Balance of Cost of Good Sold Account

36,80,00

0

Less: Under-applied Overheads

-

25,000

36,55,00

0

E Machine Hours actually work during the year

Overheads applied

8,75,00

0

Pre-determined rate of overhead per Machine Hour

2

0

No. of Machine Hours worked 43,75

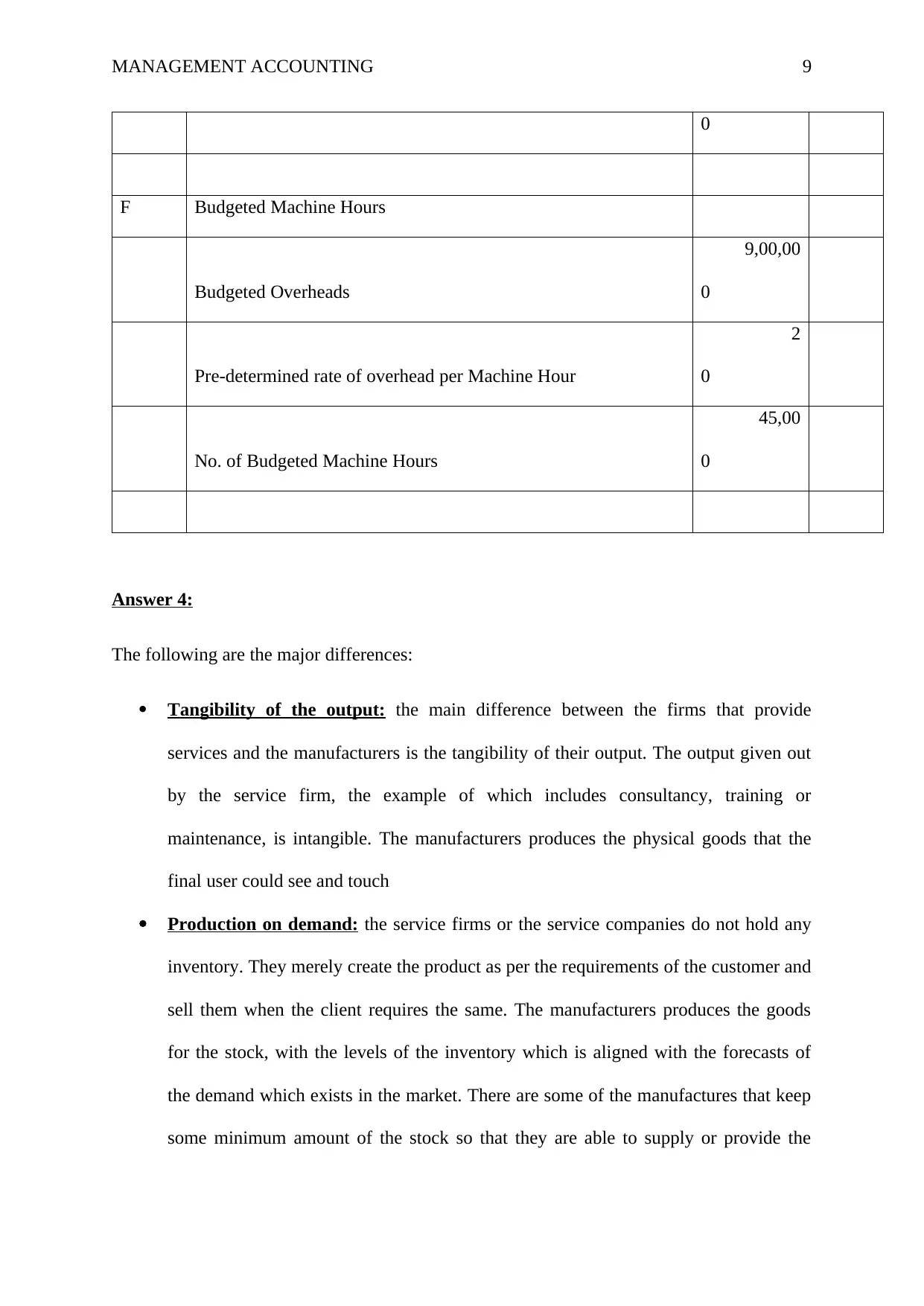

MANAGEMENT ACCOUNTING 9

0

F Budgeted Machine Hours

Budgeted Overheads

9,00,00

0

Pre-determined rate of overhead per Machine Hour

2

0

No. of Budgeted Machine Hours

45,00

0

Answer 4:

The following are the major differences:

Tangibility of the output: the main difference between the firms that provide

services and the manufacturers is the tangibility of their output. The output given out

by the service firm, the example of which includes consultancy, training or

maintenance, is intangible. The manufacturers produces the physical goods that the

final user could see and touch

Production on demand: the service firms or the service companies do not hold any

inventory. They merely create the product as per the requirements of the customer and

sell them when the client requires the same. The manufacturers produces the goods

for the stock, with the levels of the inventory which is aligned with the forecasts of

the demand which exists in the market. There are some of the manufactures that keep

some minimum amount of the stock so that they are able to supply or provide the

0

F Budgeted Machine Hours

Budgeted Overheads

9,00,00

0

Pre-determined rate of overhead per Machine Hour

2

0

No. of Budgeted Machine Hours

45,00

0

Answer 4:

The following are the major differences:

Tangibility of the output: the main difference between the firms that provide

services and the manufacturers is the tangibility of their output. The output given out

by the service firm, the example of which includes consultancy, training or

maintenance, is intangible. The manufacturers produces the physical goods that the

final user could see and touch

Production on demand: the service firms or the service companies do not hold any

inventory. They merely create the product as per the requirements of the customer and

sell them when the client requires the same. The manufacturers produces the goods

for the stock, with the levels of the inventory which is aligned with the forecasts of

the demand which exists in the market. There are some of the manufactures that keep

some minimum amount of the stock so that they are able to supply or provide the

MANAGEMENT ACCOUNTING 10

goods as and when the demand arises for the same. The inventory also shows the cost

for the manufacturing company.

Customer specific production: the firms that provide some service to the customers

do not mainly produce any sort of a service unless and until the customer’s order the

same. This happens when the company designs and develops the products in

accordance with the orders. The firms manufactures the products as per the specific

requirements of each customer such as 12 hours of consultancy, 14 hours of deigning

etc. these manufacturers are able to produce the goods without any order of the

customer or forecasting of the customer demand. Hence, the production of any sort of

the goods aiming at meeting the market demand is considered to be of a poor strategy.

Labour requirements and the processes of automation: the firms that provide

some specific services to the customers hire the people with some specific knowledge

and skill set. These companies are mainly labour intensive and these services are

capable of being automated. The management is able to create a knowledge centre for

such services. The manufacturers of the products are able to automate the process of

production for the reason of reducing the labour requirements, even when there are

some if the companies that are labour intensive, especially in the countries that have

low labour costs (Oreilly, 2019).

Physical production location: There are many of the firms that provides the services

which do not have any production site. The people that create the products for the

others can be found anywhere. The audit firms such as PWC have some established

communication networks so that they can approach clients from anywhere in the

world. But this is not possible for the manufacturers. The production of the goods

need not be on the site of the owner and thus can take place at any point in the chain

of supply (Small business chron, 2019).

goods as and when the demand arises for the same. The inventory also shows the cost

for the manufacturing company.

Customer specific production: the firms that provide some service to the customers

do not mainly produce any sort of a service unless and until the customer’s order the

same. This happens when the company designs and develops the products in

accordance with the orders. The firms manufactures the products as per the specific

requirements of each customer such as 12 hours of consultancy, 14 hours of deigning

etc. these manufacturers are able to produce the goods without any order of the

customer or forecasting of the customer demand. Hence, the production of any sort of

the goods aiming at meeting the market demand is considered to be of a poor strategy.

Labour requirements and the processes of automation: the firms that provide

some specific services to the customers hire the people with some specific knowledge

and skill set. These companies are mainly labour intensive and these services are

capable of being automated. The management is able to create a knowledge centre for

such services. The manufacturers of the products are able to automate the process of

production for the reason of reducing the labour requirements, even when there are

some if the companies that are labour intensive, especially in the countries that have

low labour costs (Oreilly, 2019).

Physical production location: There are many of the firms that provides the services

which do not have any production site. The people that create the products for the

others can be found anywhere. The audit firms such as PWC have some established

communication networks so that they can approach clients from anywhere in the

world. But this is not possible for the manufacturers. The production of the goods

need not be on the site of the owner and thus can take place at any point in the chain

of supply (Small business chron, 2019).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MANAGEMENT ACCOUNTING 11

Answer 5:

The following are the main differences that exists:

The product based companies offer much more in terms of knowledge when

compared with the service based companies

The work of development plays a major role in the product based companies but the

same is not possible in the case of service based companies.

In the product based companies, one is allowed to learn new technologies and apply

own creativity so as to develop new products but this is not so in the service based

companies. In the service based companies, the existing technologies have to be used

and managed accordingly.

The product based companies are able to allow more increments to the customers due

to longer product cycle and small number of employees. Keeping in mind the size of

the team, the delivery of the dependency is much high and this helps in finding the

replacements costlier.

These companies are able to drive the process on one hand and drive innovation on

the other. These companies are ready invest money even in these processes

Answer 6:

The following are the desired calculations:

A

Let the total cost of Personnel Department including cost

allocated from Computing Department be "P"

Let the total cost of Computing Department including cost

allocated from Personnel Department be "C"

The cost of Personnel department will have allocated cost of

Computing Department which is allocated in the ratio of Service

Hours, i.e. Personnel Department will have 1/5th of total cost of

Computing Department

Similarly, the cost of Computing department will have allocated

cost of Personnel Department which is allocated in the ratio of

Answer 5:

The following are the main differences that exists:

The product based companies offer much more in terms of knowledge when

compared with the service based companies

The work of development plays a major role in the product based companies but the

same is not possible in the case of service based companies.

In the product based companies, one is allowed to learn new technologies and apply

own creativity so as to develop new products but this is not so in the service based

companies. In the service based companies, the existing technologies have to be used

and managed accordingly.

The product based companies are able to allow more increments to the customers due

to longer product cycle and small number of employees. Keeping in mind the size of

the team, the delivery of the dependency is much high and this helps in finding the

replacements costlier.

These companies are able to drive the process on one hand and drive innovation on

the other. These companies are ready invest money even in these processes

Answer 6:

The following are the desired calculations:

A

Let the total cost of Personnel Department including cost

allocated from Computing Department be "P"

Let the total cost of Computing Department including cost

allocated from Personnel Department be "C"

The cost of Personnel department will have allocated cost of

Computing Department which is allocated in the ratio of Service

Hours, i.e. Personnel Department will have 1/5th of total cost of

Computing Department

Similarly, the cost of Computing department will have allocated

cost of Personnel Department which is allocated in the ratio of

MANAGEMENT ACCOUNTING 12

number of Employees, i.e. Computing Department will have

1/11th of total cost of Personnel Department

Mathematically, equations are as under:

P = 40000 + C*1/5

Eq

ua

tio

n

1

C = 72000 + P*1/11

Eq

ua

tio

n

2

Multiply equation 1 by 1/11

P*1/11 = 40000*1/11 + C*1/55

Eq

ua

tio

n

3

Rearrange equation 2

- P*1/11 = 72000 - C

Eq

ua

tio

n

4

Add: Equation 3 & 4

C - C*1/55 = 72000+40000*1/11

This gives us C =

77

03

7.

04

Putting this value of C in equation 1 gives us P

55

40

7.

41

i.e Total Cost allocated out of Personnel Department

(rounded) $ 55407

B

Total Support Department Cost allocated to Assembly

Department

$ R $

number of Employees, i.e. Computing Department will have

1/11th of total cost of Personnel Department

Mathematically, equations are as under:

P = 40000 + C*1/5

Eq

ua

tio

n

1

C = 72000 + P*1/11

Eq

ua

tio

n

2

Multiply equation 1 by 1/11

P*1/11 = 40000*1/11 + C*1/55

Eq

ua

tio

n

3

Rearrange equation 2

- P*1/11 = 72000 - C

Eq

ua

tio

n

4

Add: Equation 3 & 4

C - C*1/55 = 72000+40000*1/11

This gives us C =

77

03

7.

04

Putting this value of C in equation 1 gives us P

55

40

7.

41

i.e Total Cost allocated out of Personnel Department

(rounded) $ 55407

B

Total Support Department Cost allocated to Assembly

Department

$ R $

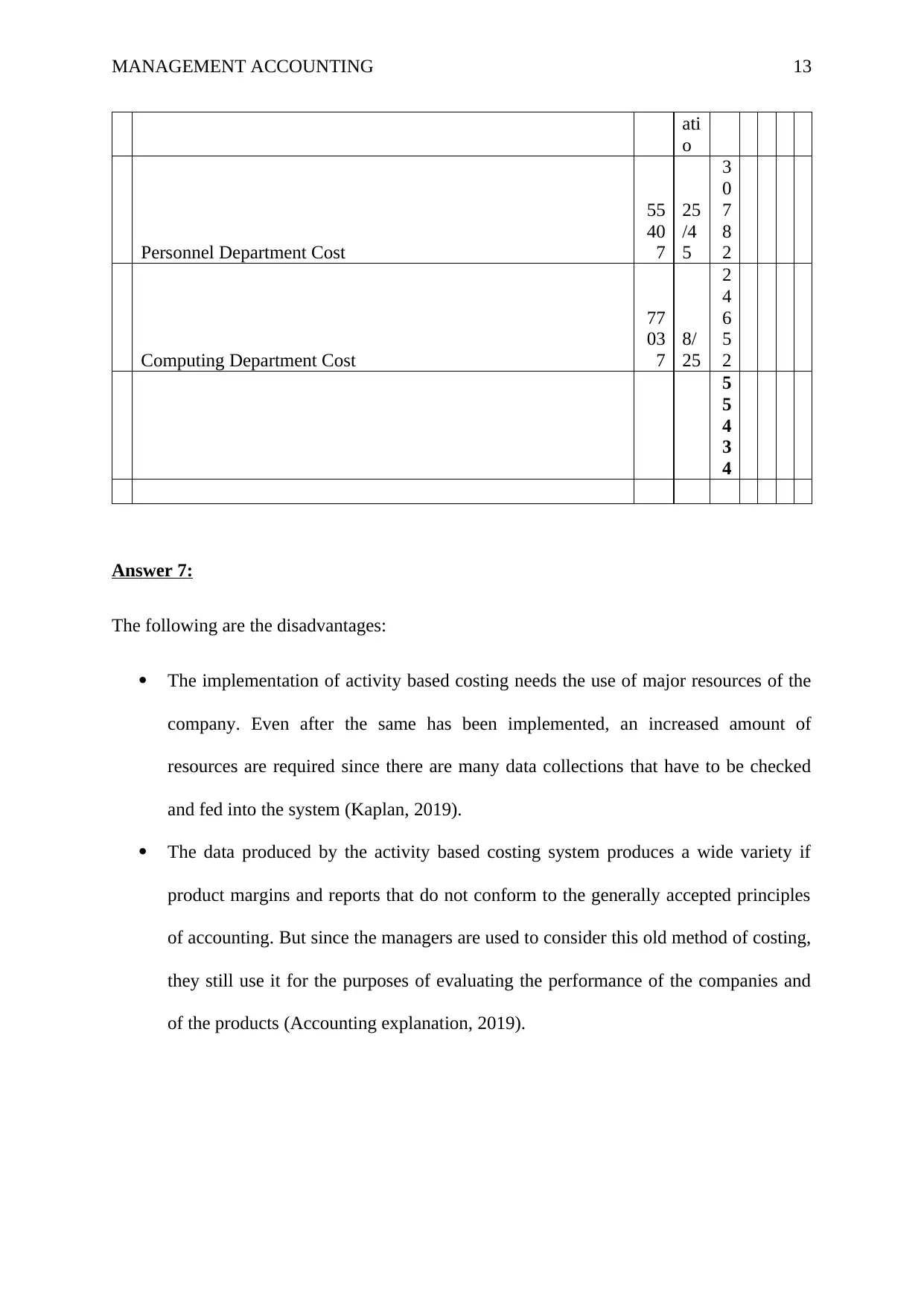

MANAGEMENT ACCOUNTING 13

ati

o

Personnel Department Cost

55

40

7

25

/4

5

3

0

7

8

2

Computing Department Cost

77

03

7

8/

25

2

4

6

5

2

5

5

4

3

4

Answer 7:

The following are the disadvantages:

The implementation of activity based costing needs the use of major resources of the

company. Even after the same has been implemented, an increased amount of

resources are required since there are many data collections that have to be checked

and fed into the system (Kaplan, 2019).

The data produced by the activity based costing system produces a wide variety if

product margins and reports that do not conform to the generally accepted principles

of accounting. But since the managers are used to consider this old method of costing,

they still use it for the purposes of evaluating the performance of the companies and

of the products (Accounting explanation, 2019).

ati

o

Personnel Department Cost

55

40

7

25

/4

5

3

0

7

8

2

Computing Department Cost

77

03

7

8/

25

2

4

6

5

2

5

5

4

3

4

Answer 7:

The following are the disadvantages:

The implementation of activity based costing needs the use of major resources of the

company. Even after the same has been implemented, an increased amount of

resources are required since there are many data collections that have to be checked

and fed into the system (Kaplan, 2019).

The data produced by the activity based costing system produces a wide variety if

product margins and reports that do not conform to the generally accepted principles

of accounting. But since the managers are used to consider this old method of costing,

they still use it for the purposes of evaluating the performance of the companies and

of the products (Accounting explanation, 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING 14

References:

Accountingexplanation.com. (2019). Advantages, Disadvantages and Limitations of Activity

Based Costing (ABC) System - AccountingExplanation.com. [online] Available at:

http://www.accountingexplanation.com/advantages_disadvantages_and_limitations_of_activi

ty_based_costing.htm [Accessed 6 May 2019].

Smallbusiness.chron.com. (2019). Five Differences Between Service and Manufacturing

Organizations. [online] Available at: https://smallbusiness.chron.com/five-differences-

between-service-manufacturing-organizations-19073.html [Accessed 6 May 2019].

Kfknowledgebank.kaplan.co.uk. (2019). ABC. [online] Available at:

http://kfknowledgebank.kaplan.co.uk/KFKB/Wiki%20Pages/Activity%20Based%20Costing

%20(ABC).aspx [Accessed 7 May 2019].

O’Reilly | Safari. (2019). Operations Management: An Integrated Approach, 5th Edition.

[online] Available at:

https://www.oreilly.com/library/view/operations-management-an/9781118122679/ch1-

sec006.html [Accessed 7 May 2019].

References:

Accountingexplanation.com. (2019). Advantages, Disadvantages and Limitations of Activity

Based Costing (ABC) System - AccountingExplanation.com. [online] Available at:

http://www.accountingexplanation.com/advantages_disadvantages_and_limitations_of_activi

ty_based_costing.htm [Accessed 6 May 2019].

Smallbusiness.chron.com. (2019). Five Differences Between Service and Manufacturing

Organizations. [online] Available at: https://smallbusiness.chron.com/five-differences-

between-service-manufacturing-organizations-19073.html [Accessed 6 May 2019].

Kfknowledgebank.kaplan.co.uk. (2019). ABC. [online] Available at:

http://kfknowledgebank.kaplan.co.uk/KFKB/Wiki%20Pages/Activity%20Based%20Costing

%20(ABC).aspx [Accessed 7 May 2019].

O’Reilly | Safari. (2019). Operations Management: An Integrated Approach, 5th Edition.

[online] Available at:

https://www.oreilly.com/library/view/operations-management-an/9781118122679/ch1-

sec006.html [Accessed 7 May 2019].

1 out of 14

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.