Comprehensive Management Accounting Systems Report Analysis

VerifiedAdded on 2020/07/22

|17

|4109

|78

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and practices. It begins with an introduction to management accounting, its types, and its importance, differentiating it from financial accounting. The report then delves into various cost accounting systems, including actual, normal, and standard costing, as well as inventory management methods like FIFO, LIFO, and weighted average. Furthermore, the report explores job costing systems, including batch, process, contract, and service costing. The report also covers the presentation of financial information, managerial accounting reports, and their significance. The report then discusses budgeting, its advantages, disadvantages, and the budget preparation process. Finally, the report examines the balanced scorecard approach as a tool to overcome financial distress. The report incorporates various models and diagrams (M1, D1, M2, D2, M3, D3, M4) to illustrate the concepts discussed.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTORDUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

a). Explanation of management accounting and its types:.....................................................3

B) Presenting Financial information:.....................................................................................7

M1...........................................................................................................................................7

D1...........................................................................................................................................8

TASK 2............................................................................................................................................8

M2:.......................................................................................................................................11

D2:........................................................................................................................................11

TASK 3..........................................................................................................................................11

a). Budgets and their advantages and disadvantages:...........................................................11

b). Budget preparation process covering identifying of the pricing and diverse costing

systems:................................................................................................................................12

C). Importance of budget:.....................................................................................................13

M3:.......................................................................................................................................13

D3.........................................................................................................................................14

TASK 4..........................................................................................................................................14

Explain ways by which the Balanced Scorecard approach can be used to overcome the

financial distress of an organisation:....................................................................................14

M4.........................................................................................................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

2

INTORDUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

a). Explanation of management accounting and its types:.....................................................3

B) Presenting Financial information:.....................................................................................7

M1...........................................................................................................................................7

D1...........................................................................................................................................8

TASK 2............................................................................................................................................8

M2:.......................................................................................................................................11

D2:........................................................................................................................................11

TASK 3..........................................................................................................................................11

a). Budgets and their advantages and disadvantages:...........................................................11

b). Budget preparation process covering identifying of the pricing and diverse costing

systems:................................................................................................................................12

C). Importance of budget:.....................................................................................................13

M3:.......................................................................................................................................13

D3.........................................................................................................................................14

TASK 4..........................................................................................................................................14

Explain ways by which the Balanced Scorecard approach can be used to overcome the

financial distress of an organisation:....................................................................................14

M4.........................................................................................................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

2

INTORDUCTION

In this competitive world, this can be rightly observed that the management accounting is

the tool that can be used by a firm in order to gain the sustainable development. There are

various tools which can be used by the organisation in order to gain the sustainability in an

effective manner. Manager of the cited firm is required to adopt these accounting tools that can

assist to gain the pre-set target. Management could gain the sustainable development. Now, there

is a strong need to adopt various costing method that can be used by the organisation in order to

optimise the profits in an effective manner (Lavia López and Hiebl, 2014). Various planning

tools are implemented by the organisation in order to optimise the profits. Various accounting

tools are used by the organisation in order to overcome the various financial issues.

TASK 1

a). Explanation of management accounting and its types:

MA system is the most crucial process which can be implemented by the organisation for

identifying, analysing, assessing and evaluating the non-financial problems. Now, this can be

rightly said that the MA systems are the best tool through which the organisation could get the

competitive advantages over the others. In other words, this is the process of presentation of the

accounting information for making the policies which can be considered by the organisation in

order to make their routine activities. This simply means that management assist to perform

whole its functions covering planning, organising, staffing, directing and controlling (Christ,

2014).

1. Difference between financial management and management accounting.

Financial accounting is the MA such as the two legs of the similar human. Function of both

of them is to ensure that management development toward better future. But on the other hand,

management accounting is broader than financial accounting in assisting management since

subject “management accounting” is formed by the organisation in an effective manner.

Financial management Management accounting

Financial management concentrates on

formulation of financial statements of

particular business organisation that is required

Management accounting is performed by the

organisation in Order to supply all relevant and

materialistic information to manager that

3

In this competitive world, this can be rightly observed that the management accounting is

the tool that can be used by a firm in order to gain the sustainable development. There are

various tools which can be used by the organisation in order to gain the sustainability in an

effective manner. Manager of the cited firm is required to adopt these accounting tools that can

assist to gain the pre-set target. Management could gain the sustainable development. Now, there

is a strong need to adopt various costing method that can be used by the organisation in order to

optimise the profits in an effective manner (Lavia López and Hiebl, 2014). Various planning

tools are implemented by the organisation in order to optimise the profits. Various accounting

tools are used by the organisation in order to overcome the various financial issues.

TASK 1

a). Explanation of management accounting and its types:

MA system is the most crucial process which can be implemented by the organisation for

identifying, analysing, assessing and evaluating the non-financial problems. Now, this can be

rightly said that the MA systems are the best tool through which the organisation could get the

competitive advantages over the others. In other words, this is the process of presentation of the

accounting information for making the policies which can be considered by the organisation in

order to make their routine activities. This simply means that management assist to perform

whole its functions covering planning, organising, staffing, directing and controlling (Christ,

2014).

1. Difference between financial management and management accounting.

Financial accounting is the MA such as the two legs of the similar human. Function of both

of them is to ensure that management development toward better future. But on the other hand,

management accounting is broader than financial accounting in assisting management since

subject “management accounting” is formed by the organisation in an effective manner.

Financial management Management accounting

Financial management concentrates on

formulation of financial statements of

particular business organisation that is required

Management accounting is performed by the

organisation in Order to supply all relevant and

materialistic information to manager that

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

by different parties that are associated with that

company.

results in formulation of effective and efficient

strategy for the company.

This type of management accounting is utilised

by the internal and external parties associated

with that company. Hence, it has broader

scope.

The main user of this accounting system is

internal management and therefore, it has

narrower scope.

It has to be published properly as its basic aim

is to deliver financial information to several

users. Apart from it, these accounting system is

audited by the auditors.

Management accounting is neither published

nor audited as it is of internal use, hence there

is no requirement for the same.

This type of accounting is framed at the end of

the financial time period.

This is conducted as per the need arises by

management in the company.

It is developed in proper structure and format. There is no proper format hence it is drawn as

per the convenience of manager.

This type of statements delivers information

that is of monetary nature.

This type of accounting consists of data and

information that is of monetary and non-

monetary in nature.

The primary objective of this type of financial

statement is to deliver all information to

outside users that include, investors, creditors,

debtors etc.

The basic aim and objective of this

management system is to help the manager to

take effective decisions on number of

important information (Moser, 2012).

Management have to conduct this financial

management regularly, thus it is compulsory

for the manager to perform it.

It is not compulsory for the management to

conduct this process as it is performed as the

need arises.

There are certain standard and norms on which

it is performed.

There are not specific rules and regulations that

have to followed by the management.

4

company.

results in formulation of effective and efficient

strategy for the company.

This type of management accounting is utilised

by the internal and external parties associated

with that company. Hence, it has broader

scope.

The main user of this accounting system is

internal management and therefore, it has

narrower scope.

It has to be published properly as its basic aim

is to deliver financial information to several

users. Apart from it, these accounting system is

audited by the auditors.

Management accounting is neither published

nor audited as it is of internal use, hence there

is no requirement for the same.

This type of accounting is framed at the end of

the financial time period.

This is conducted as per the need arises by

management in the company.

It is developed in proper structure and format. There is no proper format hence it is drawn as

per the convenience of manager.

This type of statements delivers information

that is of monetary nature.

This type of accounting consists of data and

information that is of monetary and non-

monetary in nature.

The primary objective of this type of financial

statement is to deliver all information to

outside users that include, investors, creditors,

debtors etc.

The basic aim and objective of this

management system is to help the manager to

take effective decisions on number of

important information (Moser, 2012).

Management have to conduct this financial

management regularly, thus it is compulsory

for the manager to perform it.

It is not compulsory for the management to

conduct this process as it is performed as the

need arises.

There are certain standard and norms on which

it is performed.

There are not specific rules and regulations that

have to followed by the management.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Importance of management accounting: Management of the cited organisation is

required to make various management accounting tools which can be implemented by the

firm for achieving its pre-set targets in an effective manner (Weygandt, Kimmel, and

Kieso, 2015). This is the term which is implemented to elaborates the accounting tools,

systems and tools which, with special knowledge and ability, assist management in its

task of optimising profits of lowering losses. Management Accounting helps management

in planning and also creating policies by forming predict about manufacturing, selling,

inflows and outflow of the cash. Nowadays, this can be rightly said that the management

of the cited organisation in order to gain the business decisions in an effective manner.

Now, this is the main tool which can be used by the organisation in order to gain the

sustainability.

3. Cost accounting systems: This is the accounting system which is implemented by the

organisation in order to make the production of the goods. Now, there is a strong need to

adopt this by using this tool in an effective manner. Cost accounting system is the crucial

tool which can be implemented by the cited organisation for making the organisation

objectives in an effective manner. With the help of this, organisation is planning to

implement its objectives in an effective manner so that the business in an effective

manner. Cost accounting systems are further categorised into actual, normal and standard

costing which are further elaborated under this.

Actual costing: this is the recording of the product costs which are totally relied upon the

following factors: Actual cost of labour, Actual overheads costs occurred, allocating

implementing actual quantity of the allocation base experienced at the time of reporting

period.

Normal costing: This is implemented to value manufacturing products along with actual

material costs, actual direct labour costs and manufacturing related overhead which are

totally relied upon the forecasted production overhead rate. These three costs are related

to the product costs and are implemented for the cost of goods sold and for inventory

valuation.

5

required to make various management accounting tools which can be implemented by the

firm for achieving its pre-set targets in an effective manner (Weygandt, Kimmel, and

Kieso, 2015). This is the term which is implemented to elaborates the accounting tools,

systems and tools which, with special knowledge and ability, assist management in its

task of optimising profits of lowering losses. Management Accounting helps management

in planning and also creating policies by forming predict about manufacturing, selling,

inflows and outflow of the cash. Nowadays, this can be rightly said that the management

of the cited organisation in order to gain the business decisions in an effective manner.

Now, this is the main tool which can be used by the organisation in order to gain the

sustainability.

3. Cost accounting systems: This is the accounting system which is implemented by the

organisation in order to make the production of the goods. Now, there is a strong need to

adopt this by using this tool in an effective manner. Cost accounting system is the crucial

tool which can be implemented by the cited organisation for making the organisation

objectives in an effective manner. With the help of this, organisation is planning to

implement its objectives in an effective manner so that the business in an effective

manner. Cost accounting systems are further categorised into actual, normal and standard

costing which are further elaborated under this.

Actual costing: this is the recording of the product costs which are totally relied upon the

following factors: Actual cost of labour, Actual overheads costs occurred, allocating

implementing actual quantity of the allocation base experienced at the time of reporting

period.

Normal costing: This is implemented to value manufacturing products along with actual

material costs, actual direct labour costs and manufacturing related overhead which are

totally relied upon the forecasted production overhead rate. These three costs are related

to the product costs and are implemented for the cost of goods sold and for inventory

valuation.

5

Standard Costing: This is the practice of substituting forecasted cost for an actual cost

in the accounting records, and then periodically recording variances which reflects

differences between the forecasted and actual costs.

Inventory management system: This is the main tool through which inventory is

managed in an effective manner. Now, this is rightly observed that the management of

the cited organisation is required to adopt inventory management system which would

help out to gain the sustainable development. There are mostly three methods which

would help out to manage the inventory in an effective manner. some of them are

mentioned hereunder:

FIFO Method: This is the method under which inventory which is firstly placed is to be

considered at the time of calculating the inventory (Leitner, 2013). However, this can be rightly

said that the management of the cited organisation is required to optimise the inventory in an

effective manner. In this, costs which are assigned to those goods which are the costs for first

product brought.

LIFO Method: This is the method which consider all the last items which were

introduced are the first items to be sold. This cited method said that last inventories purchased

are first ones to disposed of. This tool assumes that last stocks introduced which are firstly one to

be sold, and that stocks bring first are sold last.

Weighted Average Method: This method is basically implemented in the production

organisations where stock is piled or mixed together and cannot be differentiated, like raw

material and so on.

5. Job costing system: This is the main system which is used by the management in order to

gain the objectives in an effective manner. Although, this is the system for assigning production

costs to an individual good or batches of goods (Akbar, 2010). Normally, this is implemented

only when organisations produced which are sufficiently different from each other.

Batch costing: It is known as of the specific form of particular order costing. It is more

similar to job order costing which is have data of manufacturing on it.

Process costing: It is said to be reliable term used to cost accounting that describe single

method for collecting and producing cost to an individual units produced.

Contract costing: As per this tracking of cost related with a particular contract with the

client. It is mainly used for the large construction work.

6

in the accounting records, and then periodically recording variances which reflects

differences between the forecasted and actual costs.

Inventory management system: This is the main tool through which inventory is

managed in an effective manner. Now, this is rightly observed that the management of

the cited organisation is required to adopt inventory management system which would

help out to gain the sustainable development. There are mostly three methods which

would help out to manage the inventory in an effective manner. some of them are

mentioned hereunder:

FIFO Method: This is the method under which inventory which is firstly placed is to be

considered at the time of calculating the inventory (Leitner, 2013). However, this can be rightly

said that the management of the cited organisation is required to optimise the inventory in an

effective manner. In this, costs which are assigned to those goods which are the costs for first

product brought.

LIFO Method: This is the method which consider all the last items which were

introduced are the first items to be sold. This cited method said that last inventories purchased

are first ones to disposed of. This tool assumes that last stocks introduced which are firstly one to

be sold, and that stocks bring first are sold last.

Weighted Average Method: This method is basically implemented in the production

organisations where stock is piled or mixed together and cannot be differentiated, like raw

material and so on.

5. Job costing system: This is the main system which is used by the management in order to

gain the objectives in an effective manner. Although, this is the system for assigning production

costs to an individual good or batches of goods (Akbar, 2010). Normally, this is implemented

only when organisations produced which are sufficiently different from each other.

Batch costing: It is known as of the specific form of particular order costing. It is more

similar to job order costing which is have data of manufacturing on it.

Process costing: It is said to be reliable term used to cost accounting that describe single

method for collecting and producing cost to an individual units produced.

Contract costing: As per this tracking of cost related with a particular contract with the

client. It is mainly used for the large construction work.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Service costing: It is considering as one of the type of operation costing that is used in an

organisation which would provide services irrespective of manufacturing products.

B) Presenting Financial information:

1. Diverse kinds of managerial accounting reports:

There are so many repots which are used by the organisation for gain the sustainability.

However, this can be rightly said that the management of the cited organisation is required to

adopt various options that can be help out to get the competitive advantages. There are some of

the budgets are mentioned hereunder:

Budget reports: This is the reports which is made on the basis of specific revenues and

expenses for a certain period of time. However, this can be rightly said that the management of

the cited organisation is required to adopt budget as per the organisation needs. This is needed to

be done as per the management that can help out to form the business objectives accordingly.

With the help of this, manager can evaluate the actual and forecasted figure accordingly.

Account receivable aging report: This is the report under which unpaid consumer

invoices and unused credit memos are to be recorded in an effective manner. The main aim is

implemented by gathering personnel in order to identify which invoices which are overdue for

payment. The report is like implemented by management to identify efficiency of the credit and

gathering functions.

2. Importance of Management accounting information:

This various management accounting information are so much crucial as these all assist in

gaining the sustainable development in an effective manner (Eierle and Schultze, 2013).

management accounting information are used by the cited organisation for gaining the

sustainability in an effective manner. this management accounting information would help out to

gain the sustainable development in an effective manner various management accounting

systems are used by the managers in order to get the sustainability efficient manner.

M1

There are so many tools which can be used by the organisation for making the business

objectives in an effective manner. Management Accounting systems are used which could be

implemented in order to gain the sustainability in an effective manner. On the other way, this is

the most efficient tool which would help out to form efficient tool that would help out to gain the

sustainability effectively and efficiently.

7

organisation which would provide services irrespective of manufacturing products.

B) Presenting Financial information:

1. Diverse kinds of managerial accounting reports:

There are so many repots which are used by the organisation for gain the sustainability.

However, this can be rightly said that the management of the cited organisation is required to

adopt various options that can be help out to get the competitive advantages. There are some of

the budgets are mentioned hereunder:

Budget reports: This is the reports which is made on the basis of specific revenues and

expenses for a certain period of time. However, this can be rightly said that the management of

the cited organisation is required to adopt budget as per the organisation needs. This is needed to

be done as per the management that can help out to form the business objectives accordingly.

With the help of this, manager can evaluate the actual and forecasted figure accordingly.

Account receivable aging report: This is the report under which unpaid consumer

invoices and unused credit memos are to be recorded in an effective manner. The main aim is

implemented by gathering personnel in order to identify which invoices which are overdue for

payment. The report is like implemented by management to identify efficiency of the credit and

gathering functions.

2. Importance of Management accounting information:

This various management accounting information are so much crucial as these all assist in

gaining the sustainable development in an effective manner (Eierle and Schultze, 2013).

management accounting information are used by the cited organisation for gaining the

sustainability in an effective manner. this management accounting information would help out to

gain the sustainable development in an effective manner various management accounting

systems are used by the managers in order to get the sustainability efficient manner.

M1

There are so many tools which can be used by the organisation for making the business

objectives in an effective manner. Management Accounting systems are used which could be

implemented in order to gain the sustainability in an effective manner. On the other way, this is

the most efficient tool which would help out to form efficient tool that would help out to gain the

sustainability effectively and efficiently.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

D1

Management accounting systems and reporting is integrated throughout firms’ process.

This can be rightly said that the management accounting systems are the most effective tools

which would ultimately help out to make various reports that could assist to integrate in an

effective manner. now, there are various management accounting systems are used by the cited

organisation in order to integrate the MA systems to the MA reports.

TASK 2

Cost is the most important aspect for a firm that are linked with the manufacturing of goods

and services. This is totally linked to the organisation There are so many kinds of the costs

which are linked to be considered. Few of them are elaborated as under:

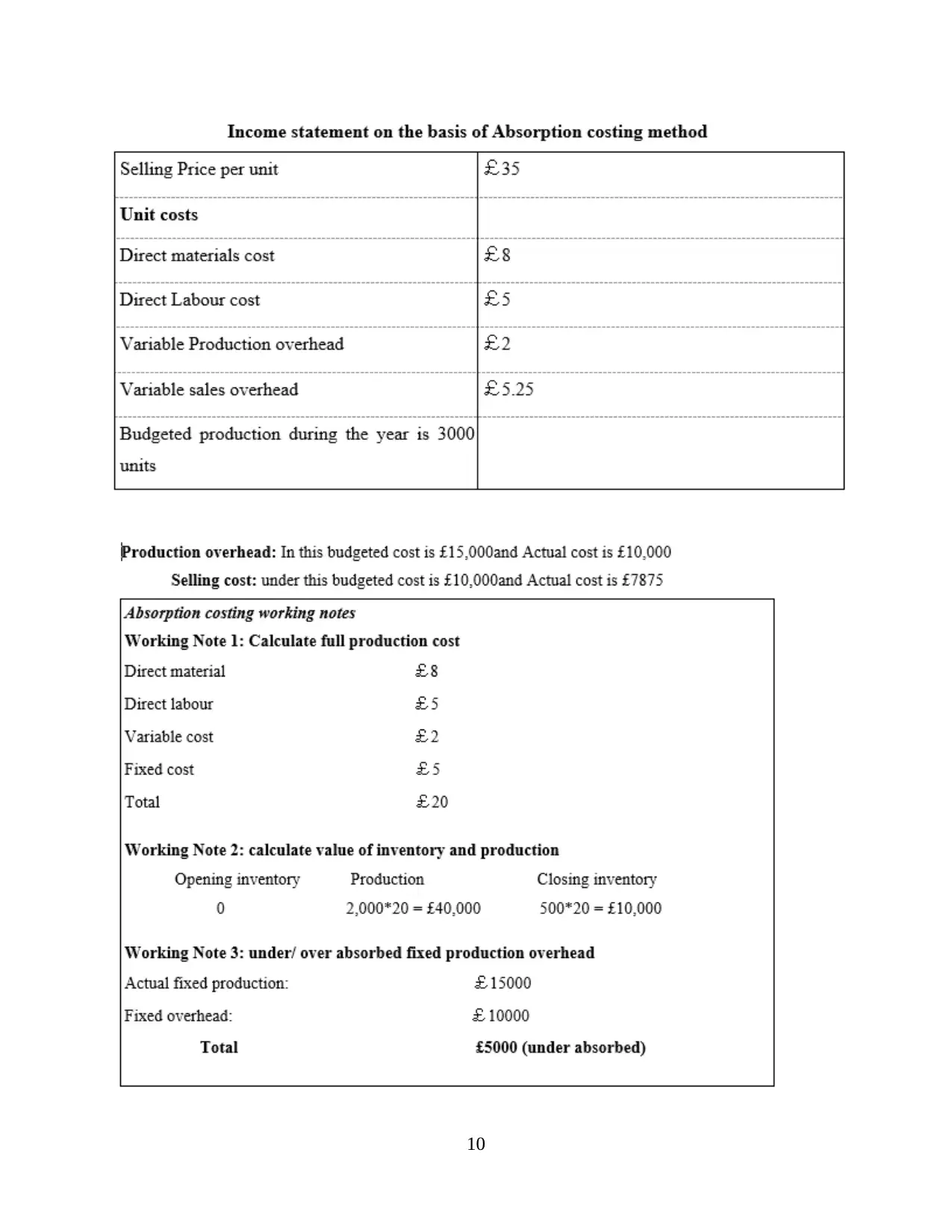

Absorption Costing: This is the costing method under which all the costs which are related to

the production of the goods, considered (Becker, Ulrich and Staffel, 2011). This is the most

effective tool which can be used by the Tech UK for optimising the net profits.

Marginal costing: This is the costing method which is used by the production manager

under which consider all the variable costs whether that was related to the production or not.

This is the most effective tool which could be optimised in an effective manner.

Cost volume profit: This is most effective tool which assist for calculating diverse kinds of

modification in the costs and total volume that will affect operating incomes of a cited company.

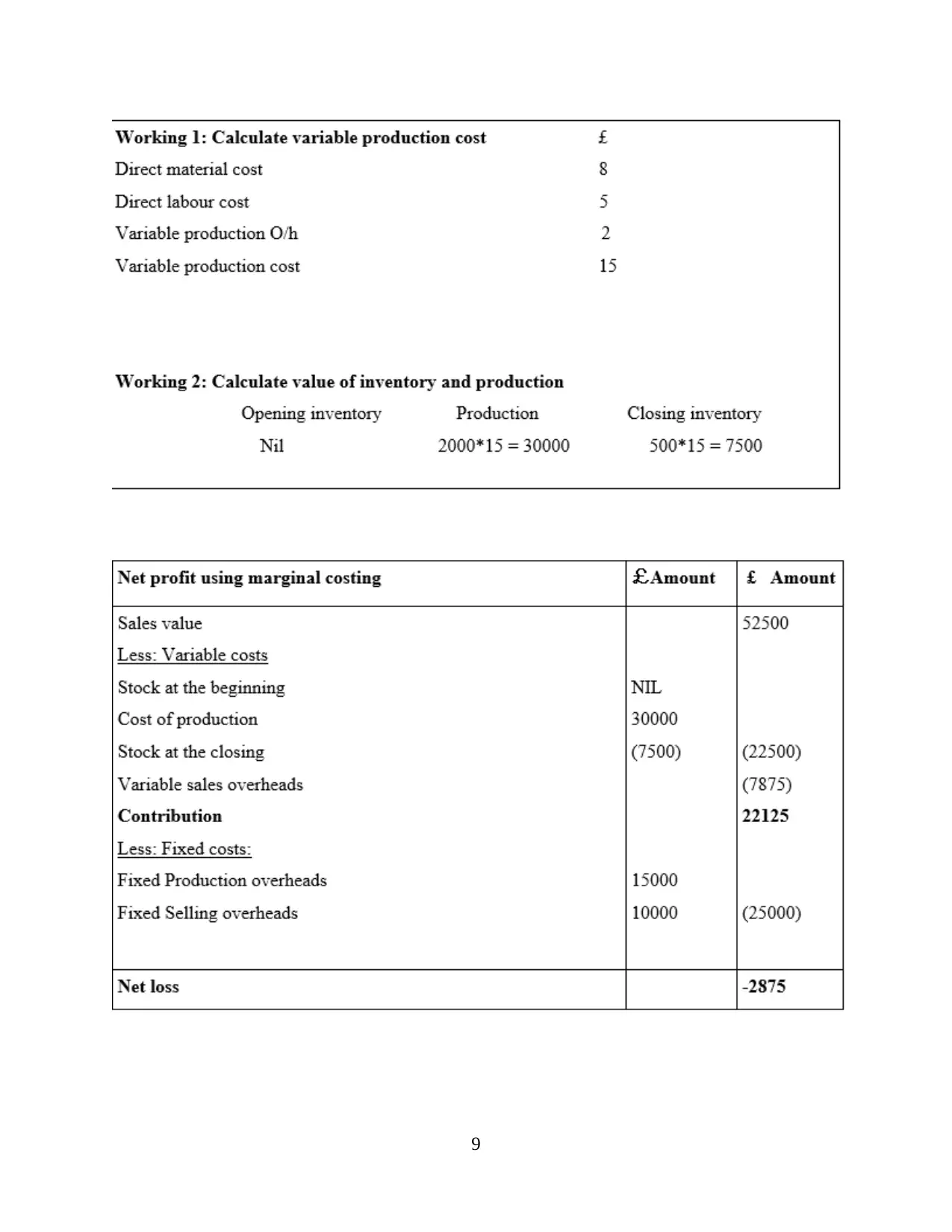

Income statement on the basis of Marginal costing method:

8

Management accounting systems and reporting is integrated throughout firms’ process.

This can be rightly said that the management accounting systems are the most effective tools

which would ultimately help out to make various reports that could assist to integrate in an

effective manner. now, there are various management accounting systems are used by the cited

organisation in order to integrate the MA systems to the MA reports.

TASK 2

Cost is the most important aspect for a firm that are linked with the manufacturing of goods

and services. This is totally linked to the organisation There are so many kinds of the costs

which are linked to be considered. Few of them are elaborated as under:

Absorption Costing: This is the costing method under which all the costs which are related to

the production of the goods, considered (Becker, Ulrich and Staffel, 2011). This is the most

effective tool which can be used by the Tech UK for optimising the net profits.

Marginal costing: This is the costing method which is used by the production manager

under which consider all the variable costs whether that was related to the production or not.

This is the most effective tool which could be optimised in an effective manner.

Cost volume profit: This is most effective tool which assist for calculating diverse kinds of

modification in the costs and total volume that will affect operating incomes of a cited company.

Income statement on the basis of Marginal costing method:

8

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

M2:

There are so many kinds of tools which assist in accounting process of a cited company.

Product costs tools are highly justifiable in enhancing entire growth for the organisation.

Standard costs are helpful for forming comparison of the cited organisation in related to the

budget one. While marginal costing tools is highly effective for the management for enhancing

entire development for the organisation.

D2:

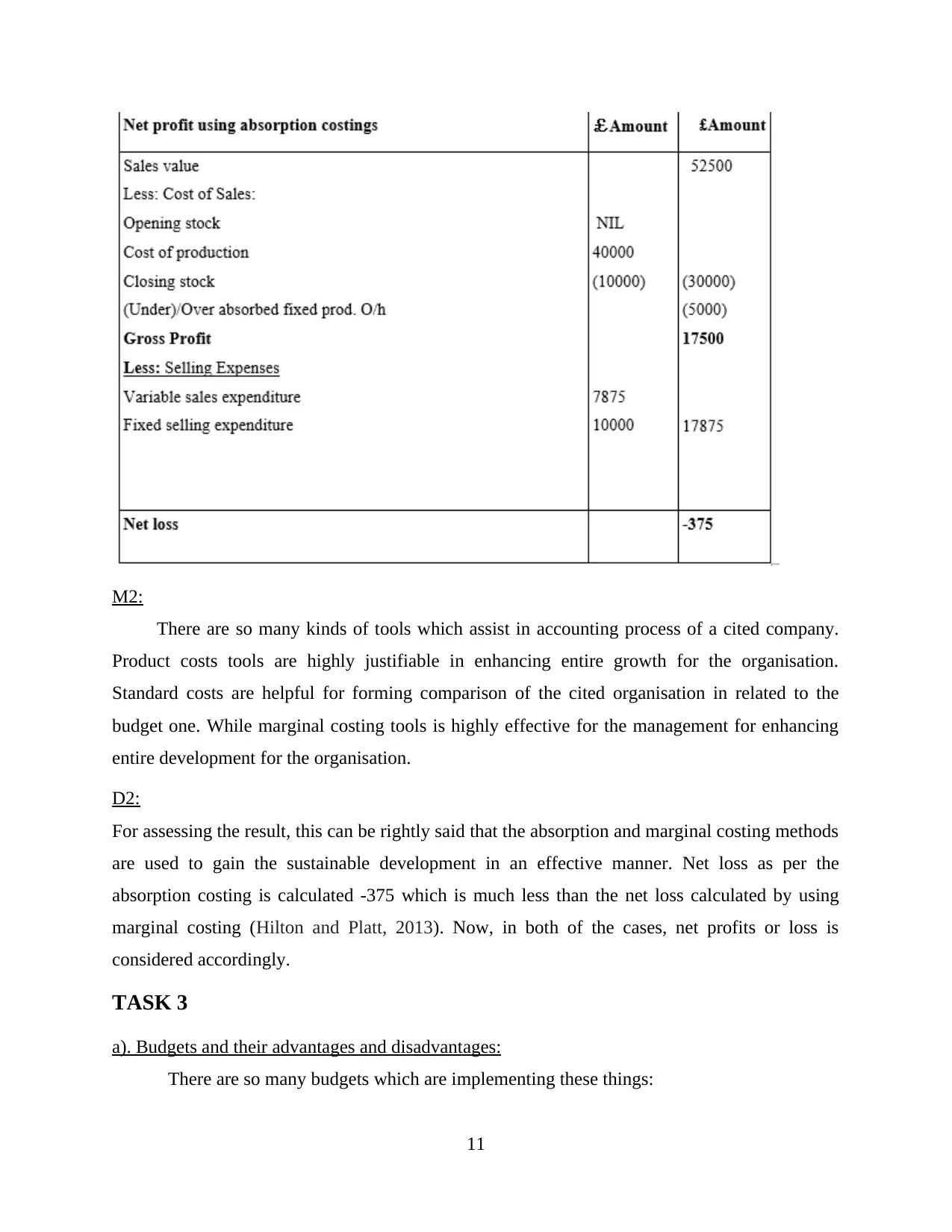

For assessing the result, this can be rightly said that the absorption and marginal costing methods

are used to gain the sustainable development in an effective manner. Net loss as per the

absorption costing is calculated -375 which is much less than the net loss calculated by using

marginal costing (Hilton and Platt, 2013). Now, in both of the cases, net profits or loss is

considered accordingly.

TASK 3

a). Budgets and their advantages and disadvantages:

There are so many budgets which are implementing these things:

11

There are so many kinds of tools which assist in accounting process of a cited company.

Product costs tools are highly justifiable in enhancing entire growth for the organisation.

Standard costs are helpful for forming comparison of the cited organisation in related to the

budget one. While marginal costing tools is highly effective for the management for enhancing

entire development for the organisation.

D2:

For assessing the result, this can be rightly said that the absorption and marginal costing methods

are used to gain the sustainable development in an effective manner. Net loss as per the

absorption costing is calculated -375 which is much less than the net loss calculated by using

marginal costing (Hilton and Platt, 2013). Now, in both of the cases, net profits or loss is

considered accordingly.

TASK 3

a). Budgets and their advantages and disadvantages:

There are so many budgets which are implementing these things:

11

Flexible Budget: This is the budget which can vary for the change in the volume of the

activity. Flexible budget is highly sophisticated and this is more effective than the static budget

that remains at one amount related to the volume of the activities.

Advantages:

The main advantage of this budget is that it can be varied as per the requirement.

This can be rightly said that the management of the cited organisation is specifically

required to adopt this in an effective manner.

Now, flexible budget of cited organisation helps to gain the sustainability in an

effective manner.

Disadvantages:

This does not always reflect the genuine data which ultimately restrict the firm to grow at a more

effective rate (Moser, 2012).

This is the complex one as this requires changes according to the need.

Static Budget: This is the budget which is fixed and does not change as per the change in

the circumstances. This is the most effective tool through which the static budget does

not vary accordingly. This is a kind of budget which form forecasted values about input

and outputs which are conceived before the time in question starts. At the time of

comparing the actual outcome which are attained after the fact, numbers from static

budgets are usually quite different from actual outcome.

Advantages:

The main advantage of this budget is that this forecast the future expected value

about inputs and outputs.

This helps to get the sustainability by using this in an effective manner.

Disadvantages:

Once it was formed, it can’t be changed. This is rigid and can’t be changed.

b). Budget preparation process covering identifying of the pricing and diverse costing systems:

Here are so many steps which are needed to be adhered and control performance of the UK tech.

some of them are:

At the initial stage, an adequate format of budget requires to be determined by the managers.

According to an adequate idea budget needed are to be considered (Christ, 2014).

12

activity. Flexible budget is highly sophisticated and this is more effective than the static budget

that remains at one amount related to the volume of the activities.

Advantages:

The main advantage of this budget is that it can be varied as per the requirement.

This can be rightly said that the management of the cited organisation is specifically

required to adopt this in an effective manner.

Now, flexible budget of cited organisation helps to gain the sustainability in an

effective manner.

Disadvantages:

This does not always reflect the genuine data which ultimately restrict the firm to grow at a more

effective rate (Moser, 2012).

This is the complex one as this requires changes according to the need.

Static Budget: This is the budget which is fixed and does not change as per the change in

the circumstances. This is the most effective tool through which the static budget does

not vary accordingly. This is a kind of budget which form forecasted values about input

and outputs which are conceived before the time in question starts. At the time of

comparing the actual outcome which are attained after the fact, numbers from static

budgets are usually quite different from actual outcome.

Advantages:

The main advantage of this budget is that this forecast the future expected value

about inputs and outputs.

This helps to get the sustainability by using this in an effective manner.

Disadvantages:

Once it was formed, it can’t be changed. This is rigid and can’t be changed.

b). Budget preparation process covering identifying of the pricing and diverse costing systems:

Here are so many steps which are needed to be adhered and control performance of the UK tech.

some of them are:

At the initial stage, an adequate format of budget requires to be determined by the managers.

According to an adequate idea budget needed are to be considered (Christ, 2014).

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.