Management Accounting: Types, Methods, and Tools for Budgetary Control

VerifiedAdded on 2023/01/19

|21

|3797

|40

AI Summary

This article provides an in-depth understanding of management accounting, including its types and functions. It also discusses different methods used for management accounting reporting and the advantages and disadvantages of planning tools used for budgetary control. The content covers topics such as cash budgeting, capital budgeting, and more.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and its types..................................................................................1

P2. Different methods used for management accounting reporting............................................2

TASK 2............................................................................................................................................2

P3 Income statement under absorption and marginal costing.....................................................2

TASK 3............................................................................................................................................2

P4. Advantages and disadvantages of different types of planning tools used for budgetary

control.........................................................................................................................................2

TASK 4............................................................................................................................................2

P5. Comparison of organisation in order to sort out financial issues by help of management

accounting system.......................................................................................................................2

CONCLUSION ...............................................................................................................................2

REFERENCES................................................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and its types..................................................................................1

P2. Different methods used for management accounting reporting............................................2

TASK 2............................................................................................................................................2

P3 Income statement under absorption and marginal costing.....................................................2

TASK 3............................................................................................................................................2

P4. Advantages and disadvantages of different types of planning tools used for budgetary

control.........................................................................................................................................2

TASK 4............................................................................................................................................2

P5. Comparison of organisation in order to sort out financial issues by help of management

accounting system.......................................................................................................................2

CONCLUSION ...............................................................................................................................2

REFERENCES................................................................................................................................2

INTRODUCTION

Management accounting is a way of recording company's monetary and non monetary

transactions in an effective manner with an objective of management of internal aspects

(Fullerton, Kennedy and Widener, 2013). Under this accounting internal reports are produced for

managers so that they can take suitable actions in the direction of achieving company's goals and

objectives. Basically, the main objective of this project report is to describing and understanding

term management accounting in a detailed way. For better understanding of different task of

project report a business is selected which is Q clothing company. This company is located in

London, United Kingdom and operates in manufacturing of cloths. The project report covers

about vital range of accounting systems, MA reports, income statements as well as role of MAS

in order to assess financial issues.

TASK 1

P1. Management accounting and its types.

The management accounting is broad term which starts with process of collecting

monetary and non monetary outcomes of companies and ends with preparation of internal

reports. This accounting consists a vital range of functions which are mentioned below such as :

Provide data – This is a main function of MA which consists information about

quantitative and qualitative transaction about company.

Modify data – Another function of MA is to analysing and modifying collected data so

that it can be utilised for further use (Kihn and Ihantola, 2015).

Analyse and interpret data – As well as MA is linked with analysing and interpretation of

data so that managers can aware about financial position.

Quantitative and qualitative – This is the main function of MA which states that under it

both kind of information is gathered including financial and non financial transaction.

Types of accounting system:

Financial accounting system – This can be defined as a kind of accounting system

which is applied in companies for collecting and analysing financial information. It is

formulated financial system which are being represented to both stakeholder internal and

external. Within this, it is crucial to perform auditing of whole developed financial

1

Management accounting is a way of recording company's monetary and non monetary

transactions in an effective manner with an objective of management of internal aspects

(Fullerton, Kennedy and Widener, 2013). Under this accounting internal reports are produced for

managers so that they can take suitable actions in the direction of achieving company's goals and

objectives. Basically, the main objective of this project report is to describing and understanding

term management accounting in a detailed way. For better understanding of different task of

project report a business is selected which is Q clothing company. This company is located in

London, United Kingdom and operates in manufacturing of cloths. The project report covers

about vital range of accounting systems, MA reports, income statements as well as role of MAS

in order to assess financial issues.

TASK 1

P1. Management accounting and its types.

The management accounting is broad term which starts with process of collecting

monetary and non monetary outcomes of companies and ends with preparation of internal

reports. This accounting consists a vital range of functions which are mentioned below such as :

Provide data – This is a main function of MA which consists information about

quantitative and qualitative transaction about company.

Modify data – Another function of MA is to analysing and modifying collected data so

that it can be utilised for further use (Kihn and Ihantola, 2015).

Analyse and interpret data – As well as MA is linked with analysing and interpretation of

data so that managers can aware about financial position.

Quantitative and qualitative – This is the main function of MA which states that under it

both kind of information is gathered including financial and non financial transaction.

Types of accounting system:

Financial accounting system – This can be defined as a kind of accounting system

which is applied in companies for collecting and analysing financial information. It is

formulated financial system which are being represented to both stakeholder internal and

external. Within this, it is crucial to perform auditing of whole developed financial

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

statements in order to evaluate effectiveness. For example: Q clothing company

formulate the income statement for evaluating its profit as well as loss at the year end.

Cost accounting system: This system includes procedures of projecting future cost as

well as assigning funds consequently. It is essential system within firm as they required

this for effective utilisation of available financial resources. Therefore, this is

significantly required in organisation for minimising as well as controlling total cost of

several activities. For example: Q clothing company are applying this system for

reducing the whole activities and operations cost of manufacturing cloths.

Management accounting system: It is the system which aids firms monetary

information as well as prepare reports for managers to make decisions (Kihn and

Ihantola, 2015). Mainly, this system is significant to making effectual decisions as this

reports includes financial and non financial data which are required through managers. Q

clothing company use this system to take decision regarding various activities as well as

operations associated to clothing production. For example: Utilisation of price

optimisation system leads towards effectual setting of price.

Tax accounting system: This is also considered as the kind of accounting system. Its

main aim is to manage whole taxation activities. Herein, firms have to company given

regulations as well as rules while calculating tax return. For example: there are global

taxation rules that are crucial for organisation to utilise into procedures of computing tax

rate. So, Q clothing company can calculate tax at the end of the year through assistance

of this accounting system.

P2. Different methods used for management accounting reporting.

Management accounting reporting can be considered as the procedures of formulating

internal reports for helping broad of directors into decision making. Few kinds of management

accounting reporting are discussed below:

Cost accounting report: Within this particular report, data about whole cost of activities is

involved. Through utilising this report, organisations can approximate the future time

periods. Also, this become simple to evaluate those activities that outcomes in higher cost

in compare to last accounting duration. Q clothing company accountants prepare this

report in order to aware whole expenses within accounting period.

2

formulate the income statement for evaluating its profit as well as loss at the year end.

Cost accounting system: This system includes procedures of projecting future cost as

well as assigning funds consequently. It is essential system within firm as they required

this for effective utilisation of available financial resources. Therefore, this is

significantly required in organisation for minimising as well as controlling total cost of

several activities. For example: Q clothing company are applying this system for

reducing the whole activities and operations cost of manufacturing cloths.

Management accounting system: It is the system which aids firms monetary

information as well as prepare reports for managers to make decisions (Kihn and

Ihantola, 2015). Mainly, this system is significant to making effectual decisions as this

reports includes financial and non financial data which are required through managers. Q

clothing company use this system to take decision regarding various activities as well as

operations associated to clothing production. For example: Utilisation of price

optimisation system leads towards effectual setting of price.

Tax accounting system: This is also considered as the kind of accounting system. Its

main aim is to manage whole taxation activities. Herein, firms have to company given

regulations as well as rules while calculating tax return. For example: there are global

taxation rules that are crucial for organisation to utilise into procedures of computing tax

rate. So, Q clothing company can calculate tax at the end of the year through assistance

of this accounting system.

P2. Different methods used for management accounting reporting.

Management accounting reporting can be considered as the procedures of formulating

internal reports for helping broad of directors into decision making. Few kinds of management

accounting reporting are discussed below:

Cost accounting report: Within this particular report, data about whole cost of activities is

involved. Through utilising this report, organisations can approximate the future time

periods. Also, this become simple to evaluate those activities that outcomes in higher cost

in compare to last accounting duration. Q clothing company accountants prepare this

report in order to aware whole expenses within accounting period.

2

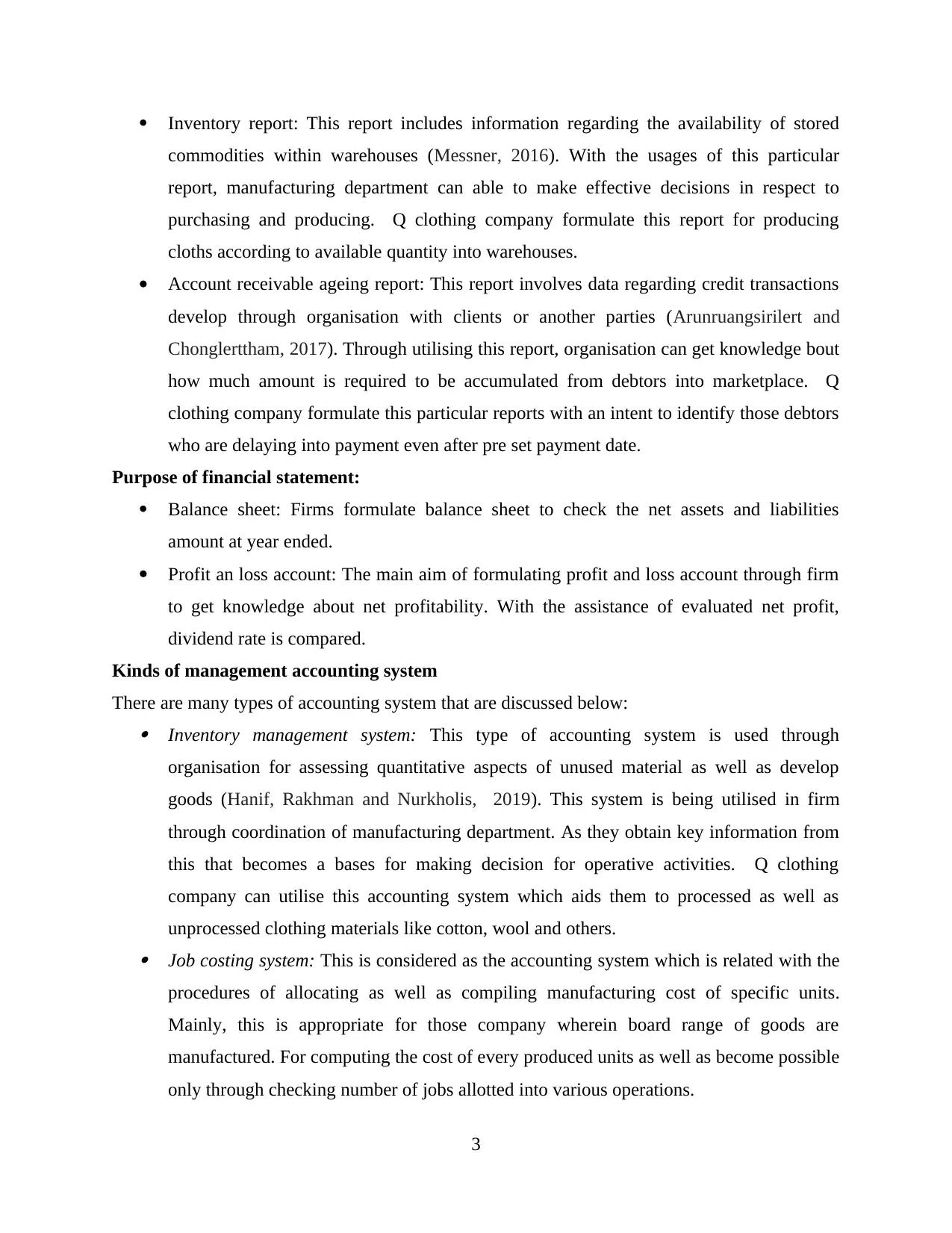

Inventory report: This report includes information regarding the availability of stored

commodities within warehouses (Messner, 2016). With the usages of this particular

report, manufacturing department can able to make effective decisions in respect to

purchasing and producing. Q clothing company formulate this report for producing

cloths according to available quantity into warehouses.

Account receivable ageing report: This report involves data regarding credit transactions

develop through organisation with clients or another parties (Arunruangsirilert and

Chonglerttham, 2017). Through utilising this report, organisation can get knowledge bout

how much amount is required to be accumulated from debtors into marketplace. Q

clothing company formulate this particular reports with an intent to identify those debtors

who are delaying into payment even after pre set payment date.

Purpose of financial statement:

Balance sheet: Firms formulate balance sheet to check the net assets and liabilities

amount at year ended.

Profit an loss account: The main aim of formulating profit and loss account through firm

to get knowledge about net profitability. With the assistance of evaluated net profit,

dividend rate is compared.

Kinds of management accounting system

There are many types of accounting system that are discussed below: Inventory management system: This type of accounting system is used through

organisation for assessing quantitative aspects of unused material as well as develop

goods (Hanif, Rakhman and Nurkholis, 2019). This system is being utilised in firm

through coordination of manufacturing department. As they obtain key information from

this that becomes a bases for making decision for operative activities. Q clothing

company can utilise this accounting system which aids them to processed as well as

unprocessed clothing materials like cotton, wool and others. Job costing system: This is considered as the accounting system which is related with the

procedures of allocating as well as compiling manufacturing cost of specific units.

Mainly, this is appropriate for those company wherein board range of goods are

manufactured. For computing the cost of every produced units as well as become possible

only through checking number of jobs allotted into various operations.

3

commodities within warehouses (Messner, 2016). With the usages of this particular

report, manufacturing department can able to make effective decisions in respect to

purchasing and producing. Q clothing company formulate this report for producing

cloths according to available quantity into warehouses.

Account receivable ageing report: This report involves data regarding credit transactions

develop through organisation with clients or another parties (Arunruangsirilert and

Chonglerttham, 2017). Through utilising this report, organisation can get knowledge bout

how much amount is required to be accumulated from debtors into marketplace. Q

clothing company formulate this particular reports with an intent to identify those debtors

who are delaying into payment even after pre set payment date.

Purpose of financial statement:

Balance sheet: Firms formulate balance sheet to check the net assets and liabilities

amount at year ended.

Profit an loss account: The main aim of formulating profit and loss account through firm

to get knowledge about net profitability. With the assistance of evaluated net profit,

dividend rate is compared.

Kinds of management accounting system

There are many types of accounting system that are discussed below: Inventory management system: This type of accounting system is used through

organisation for assessing quantitative aspects of unused material as well as develop

goods (Hanif, Rakhman and Nurkholis, 2019). This system is being utilised in firm

through coordination of manufacturing department. As they obtain key information from

this that becomes a bases for making decision for operative activities. Q clothing

company can utilise this accounting system which aids them to processed as well as

unprocessed clothing materials like cotton, wool and others. Job costing system: This is considered as the accounting system which is related with the

procedures of allocating as well as compiling manufacturing cost of specific units.

Mainly, this is appropriate for those company wherein board range of goods are

manufactured. For computing the cost of every produced units as well as become possible

only through checking number of jobs allotted into various operations.

3

Price optimisation system: This is related with the procedures of directing the

organisation's manager for setting product price as well as services (Zvezdov and

Schaltegger, 2015). Within this, price are set through accumulating consumers feedbacks

upon alternative prices as well as demands into marketplace. Thus, this system is required

within firm to keep product prices at level that is acceptable through whole consumers

and advantageous for organisations. Q clothing company can executed this system that

help them to set cost of manufacturing cloths according to the analysis of clients

feedbacks.

TASK 2

P3 Income statement under absorption and marginal costing.

Absorption costing – It is a kind of costing method in which both costs are absorbed for

preparation of income statements.

Marginal costing – Under this method, fixed cost is taken as unit cost while variable cost as unit

cost.

Case 1 :

(a) Cost card using marginal costing :

Cost card (Marginal costing method)

£/unit

Direct material 50

Direct labour 15

Variable overhead 5

Marginal cost 70

Selling price 150

Marginal cost 70

Contribution 80

4

organisation's manager for setting product price as well as services (Zvezdov and

Schaltegger, 2015). Within this, price are set through accumulating consumers feedbacks

upon alternative prices as well as demands into marketplace. Thus, this system is required

within firm to keep product prices at level that is acceptable through whole consumers

and advantageous for organisations. Q clothing company can executed this system that

help them to set cost of manufacturing cloths according to the analysis of clients

feedbacks.

TASK 2

P3 Income statement under absorption and marginal costing.

Absorption costing – It is a kind of costing method in which both costs are absorbed for

preparation of income statements.

Marginal costing – Under this method, fixed cost is taken as unit cost while variable cost as unit

cost.

Case 1 :

(a) Cost card using marginal costing :

Cost card (Marginal costing method)

£/unit

Direct material 50

Direct labour 15

Variable overhead 5

Marginal cost 70

Selling price 150

Marginal cost 70

Contribution 80

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(b) Profit and loss account:

Profit and loss statement for month of January:

Particulars DR CR

Sales revenue (12000 * 150) 1800000

Direct material (15000*50) 750000

Direct labour (15000*15) 225000

Variable cost (15000*5) 75000

Fixed production overhead 30000

Less : Closing stock (3000*70) 210000

Less: Cost of sales 870000

Profit 930000

Profit and loss statement for month of February

Particulars DR CR

Sales revenue (14000 * 150) 2100000

Direct material (12000*50) 600000

Direct labour (12000*15) 180000

Variable cost (12000*5) 60000

Add : Opening stock (3000*70) 210000

Fixed production overhead 24000

Less- Closing stock (1000*70) 70000

Less: Cost of sales 1004000

Profit 1096000

5

Profit and loss statement for month of January:

Particulars DR CR

Sales revenue (12000 * 150) 1800000

Direct material (15000*50) 750000

Direct labour (15000*15) 225000

Variable cost (15000*5) 75000

Fixed production overhead 30000

Less : Closing stock (3000*70) 210000

Less: Cost of sales 870000

Profit 930000

Profit and loss statement for month of February

Particulars DR CR

Sales revenue (14000 * 150) 2100000

Direct material (12000*50) 600000

Direct labour (12000*15) 180000

Variable cost (12000*5) 60000

Add : Opening stock (3000*70) 210000

Fixed production overhead 24000

Less- Closing stock (1000*70) 70000

Less: Cost of sales 1004000

Profit 1096000

5

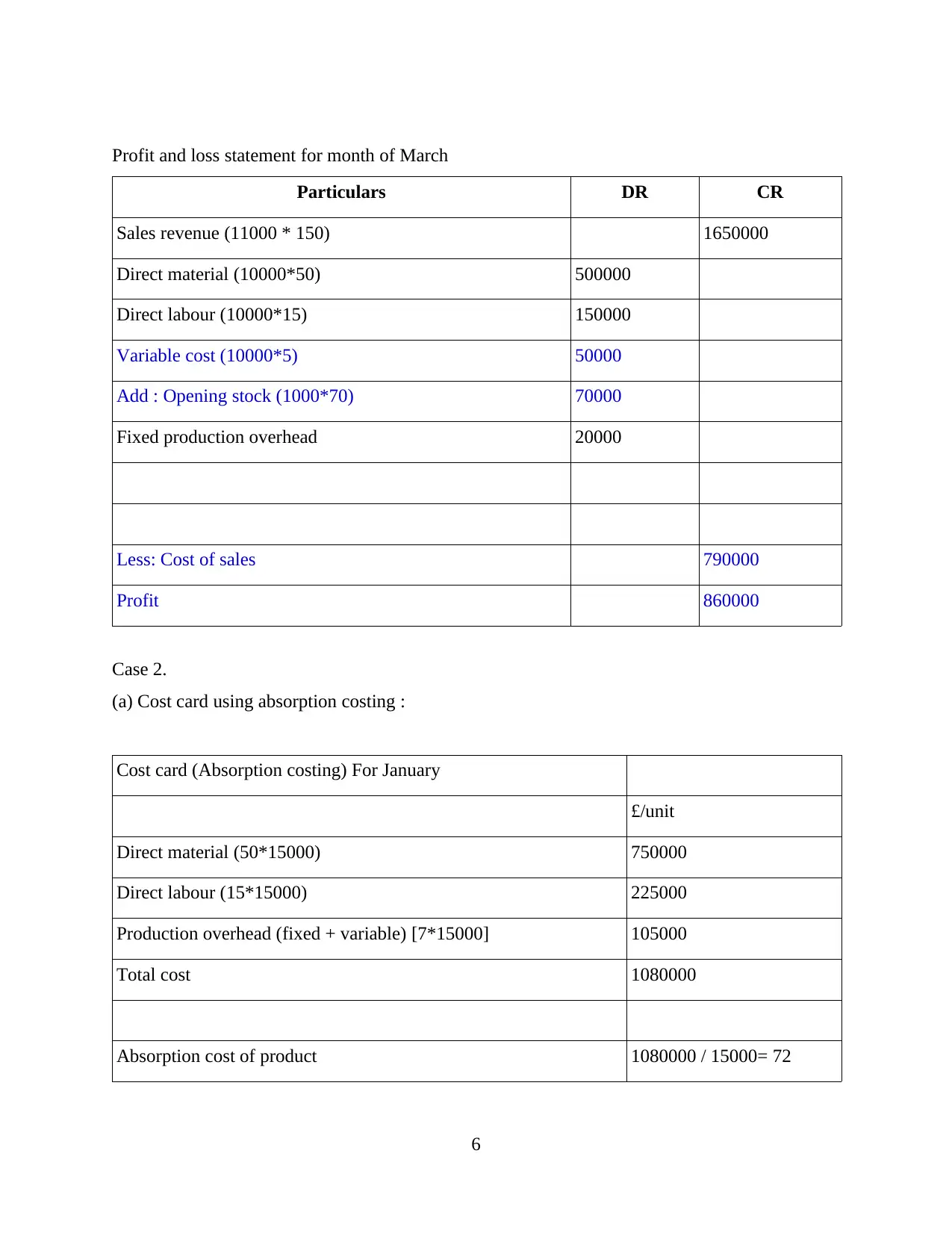

Profit and loss statement for month of March

Particulars DR CR

Sales revenue (11000 * 150) 1650000

Direct material (10000*50) 500000

Direct labour (10000*15) 150000

Variable cost (10000*5) 50000

Add : Opening stock (1000*70) 70000

Fixed production overhead 20000

Less: Cost of sales 790000

Profit 860000

Case 2.

(a) Cost card using absorption costing :

Cost card (Absorption costing) For January

£/unit

Direct material (50*15000) 750000

Direct labour (15*15000) 225000

Production overhead (fixed + variable) [7*15000] 105000

Total cost 1080000

Absorption cost of product 1080000 / 15000= 72

6

Particulars DR CR

Sales revenue (11000 * 150) 1650000

Direct material (10000*50) 500000

Direct labour (10000*15) 150000

Variable cost (10000*5) 50000

Add : Opening stock (1000*70) 70000

Fixed production overhead 20000

Less: Cost of sales 790000

Profit 860000

Case 2.

(a) Cost card using absorption costing :

Cost card (Absorption costing) For January

£/unit

Direct material (50*15000) 750000

Direct labour (15*15000) 225000

Production overhead (fixed + variable) [7*15000] 105000

Total cost 1080000

Absorption cost of product 1080000 / 15000= 72

6

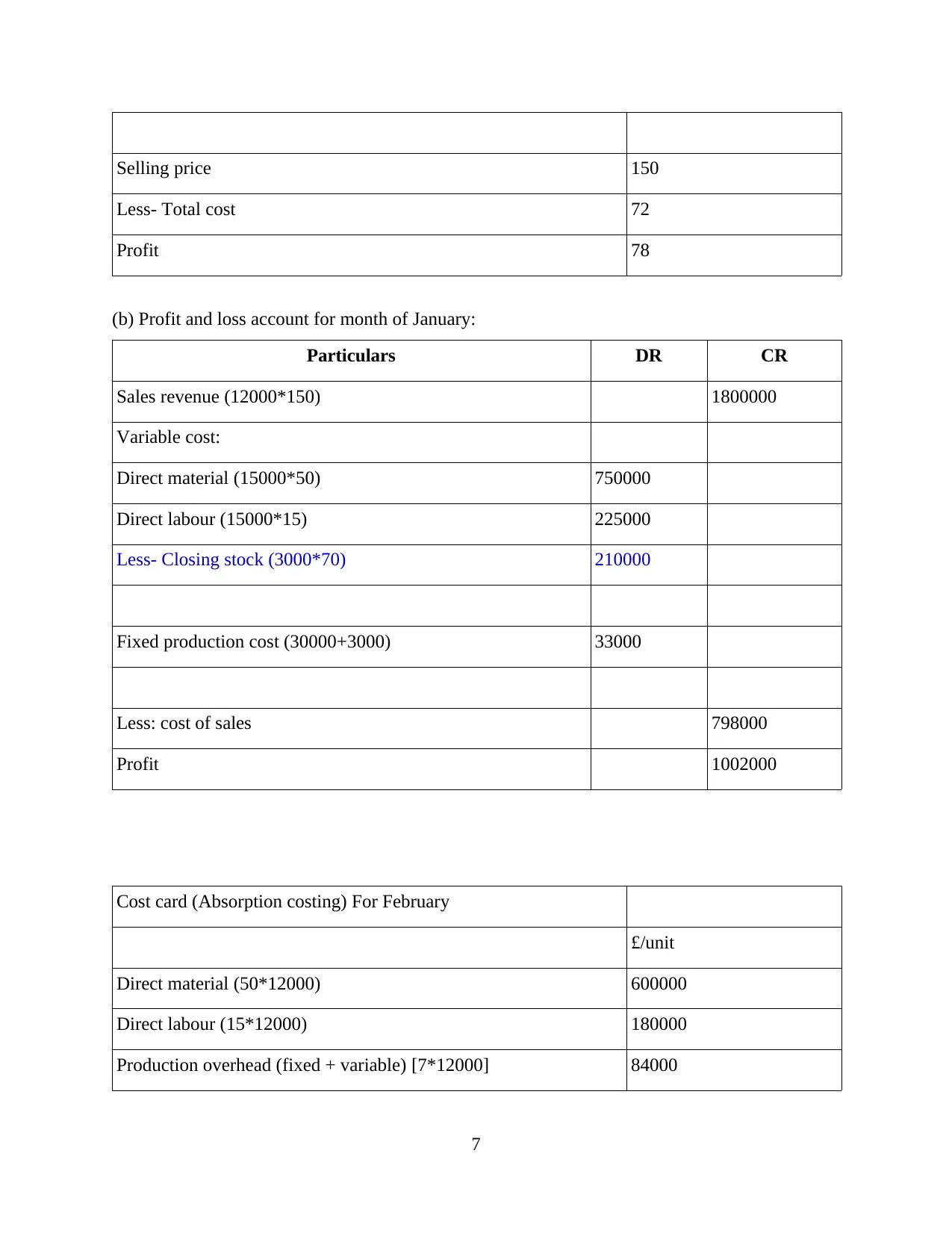

Selling price 150

Less- Total cost 72

Profit 78

(b) Profit and loss account for month of January:

Particulars DR CR

Sales revenue (12000*150) 1800000

Variable cost:

Direct material (15000*50) 750000

Direct labour (15000*15) 225000

Less- Closing stock (3000*70) 210000

Fixed production cost (30000+3000) 33000

Less: cost of sales 798000

Profit 1002000

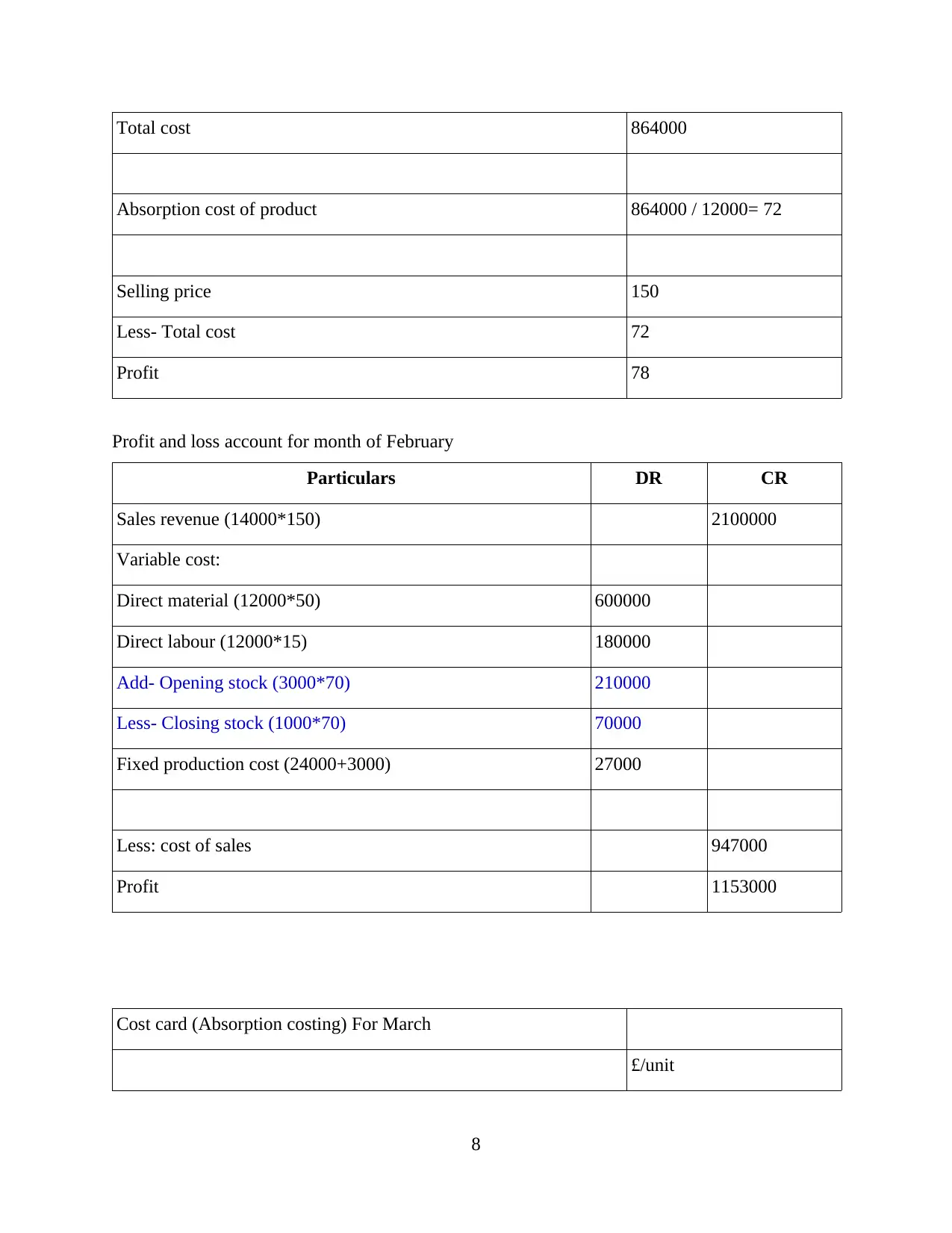

Cost card (Absorption costing) For February

£/unit

Direct material (50*12000) 600000

Direct labour (15*12000) 180000

Production overhead (fixed + variable) [7*12000] 84000

7

Less- Total cost 72

Profit 78

(b) Profit and loss account for month of January:

Particulars DR CR

Sales revenue (12000*150) 1800000

Variable cost:

Direct material (15000*50) 750000

Direct labour (15000*15) 225000

Less- Closing stock (3000*70) 210000

Fixed production cost (30000+3000) 33000

Less: cost of sales 798000

Profit 1002000

Cost card (Absorption costing) For February

£/unit

Direct material (50*12000) 600000

Direct labour (15*12000) 180000

Production overhead (fixed + variable) [7*12000] 84000

7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Total cost 864000

Absorption cost of product 864000 / 12000= 72

Selling price 150

Less- Total cost 72

Profit 78

Profit and loss account for month of February

Particulars DR CR

Sales revenue (14000*150) 2100000

Variable cost:

Direct material (12000*50) 600000

Direct labour (12000*15) 180000

Add- Opening stock (3000*70) 210000

Less- Closing stock (1000*70) 70000

Fixed production cost (24000+3000) 27000

Less: cost of sales 947000

Profit 1153000

Cost card (Absorption costing) For March

£/unit

8

Absorption cost of product 864000 / 12000= 72

Selling price 150

Less- Total cost 72

Profit 78

Profit and loss account for month of February

Particulars DR CR

Sales revenue (14000*150) 2100000

Variable cost:

Direct material (12000*50) 600000

Direct labour (12000*15) 180000

Add- Opening stock (3000*70) 210000

Less- Closing stock (1000*70) 70000

Fixed production cost (24000+3000) 27000

Less: cost of sales 947000

Profit 1153000

Cost card (Absorption costing) For March

£/unit

8

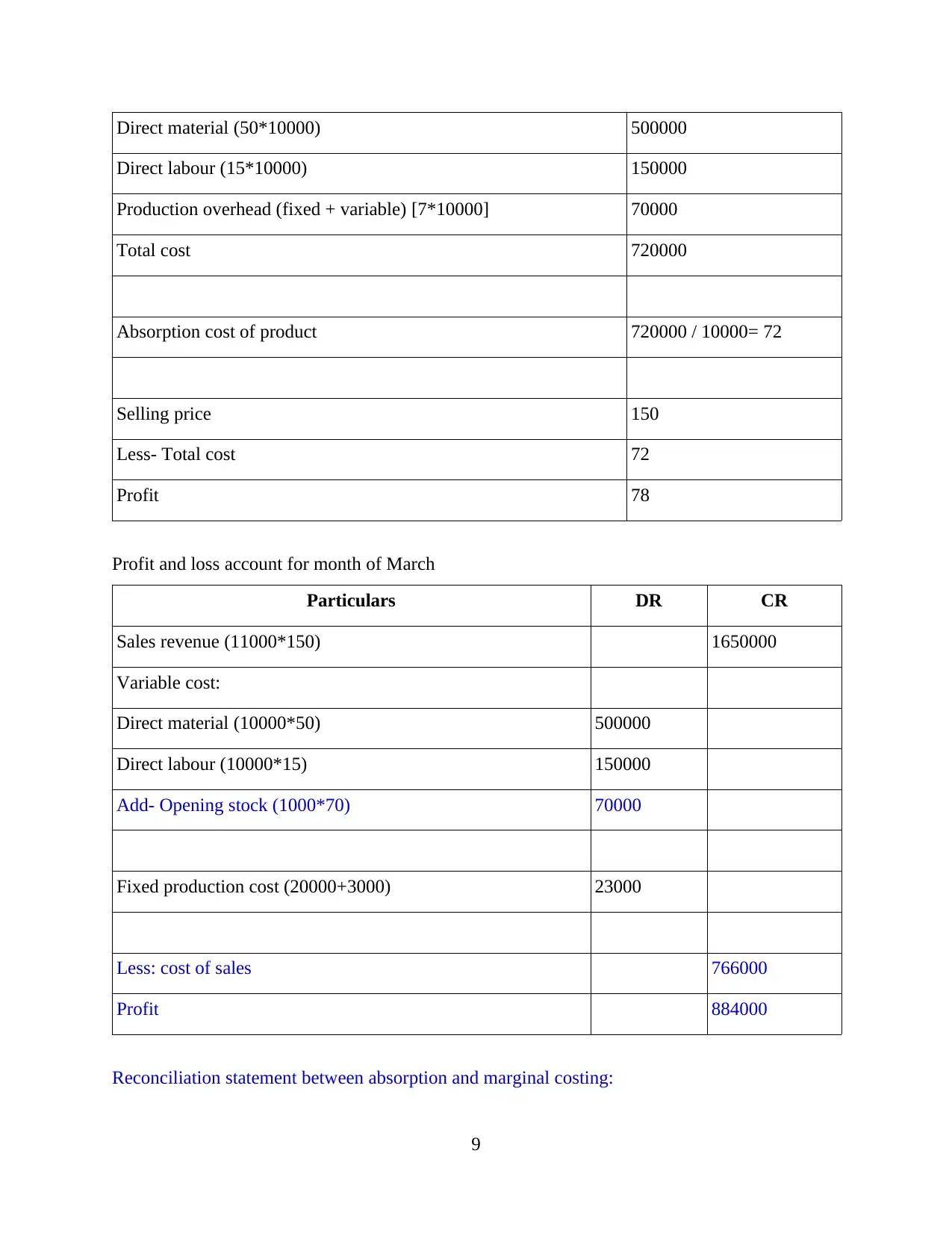

Direct material (50*10000) 500000

Direct labour (15*10000) 150000

Production overhead (fixed + variable) [7*10000] 70000

Total cost 720000

Absorption cost of product 720000 / 10000= 72

Selling price 150

Less- Total cost 72

Profit 78

Profit and loss account for month of March

Particulars DR CR

Sales revenue (11000*150) 1650000

Variable cost:

Direct material (10000*50) 500000

Direct labour (10000*15) 150000

Add- Opening stock (1000*70) 70000

Fixed production cost (20000+3000) 23000

Less: cost of sales 766000

Profit 884000

Reconciliation statement between absorption and marginal costing:

9

Direct labour (15*10000) 150000

Production overhead (fixed + variable) [7*10000] 70000

Total cost 720000

Absorption cost of product 720000 / 10000= 72

Selling price 150

Less- Total cost 72

Profit 78

Profit and loss account for month of March

Particulars DR CR

Sales revenue (11000*150) 1650000

Variable cost:

Direct material (10000*50) 500000

Direct labour (10000*15) 150000

Add- Opening stock (1000*70) 70000

Fixed production cost (20000+3000) 23000

Less: cost of sales 766000

Profit 884000

Reconciliation statement between absorption and marginal costing:

9

Profit/ marginal costing (for all three months) 2886000

Marginal cost/unit 70

Absorption cost/unit 72

Difference 2

Profit/Absorption costing 3039000

TASK 3

P4. Advantages and disadvantages of different types of planning tools used for budgetary

control.

Budgetary control is considered as the procedure od approximating the monetary as well

as non monetary results with the assistance of budgets. By utilising this, firms can able to

compare their exact performance.

Budget is considered as the procedures of creating projection of future revenue as well as

expenditures for comparing exact results. Mainly, the budget is developed for approx a year. So,

some kind some kinds of budgets are discussed below: Cash Budget: This kind of budget involves activities related to approximated cash

receipts as well as payable at certain time duration (Luft, 2016). With the assistance of

this, they can understand the cash position in future time. Q clothing company accountant

formulate this particular budget in managing as well as enhancing cash position.

Advantage: With the help of this, firms allocates cash in several operative activities

which aids respective company to savage from unnecessary expenditure.

Disadvantage: It bounds spending power as well as because of this they fail to obtain

appropriate opportunity on time. Capital Budget: It is the kinds of budget that is developed through organisation for

evaluating their efficiencies for long term investments (Aouni and Abdulkarim, 2017).

Also, firm formulate future decisions for long term investment through the assistances of

10

Marginal cost/unit 70

Absorption cost/unit 72

Difference 2

Profit/Absorption costing 3039000

TASK 3

P4. Advantages and disadvantages of different types of planning tools used for budgetary

control.

Budgetary control is considered as the procedure od approximating the monetary as well

as non monetary results with the assistance of budgets. By utilising this, firms can able to

compare their exact performance.

Budget is considered as the procedures of creating projection of future revenue as well as

expenditures for comparing exact results. Mainly, the budget is developed for approx a year. So,

some kind some kinds of budgets are discussed below: Cash Budget: This kind of budget involves activities related to approximated cash

receipts as well as payable at certain time duration (Luft, 2016). With the assistance of

this, they can understand the cash position in future time. Q clothing company accountant

formulate this particular budget in managing as well as enhancing cash position.

Advantage: With the help of this, firms allocates cash in several operative activities

which aids respective company to savage from unnecessary expenditure.

Disadvantage: It bounds spending power as well as because of this they fail to obtain

appropriate opportunity on time. Capital Budget: It is the kinds of budget that is developed through organisation for

evaluating their efficiencies for long term investments (Aouni and Abdulkarim, 2017).

Also, firm formulate future decisions for long term investment through the assistances of

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

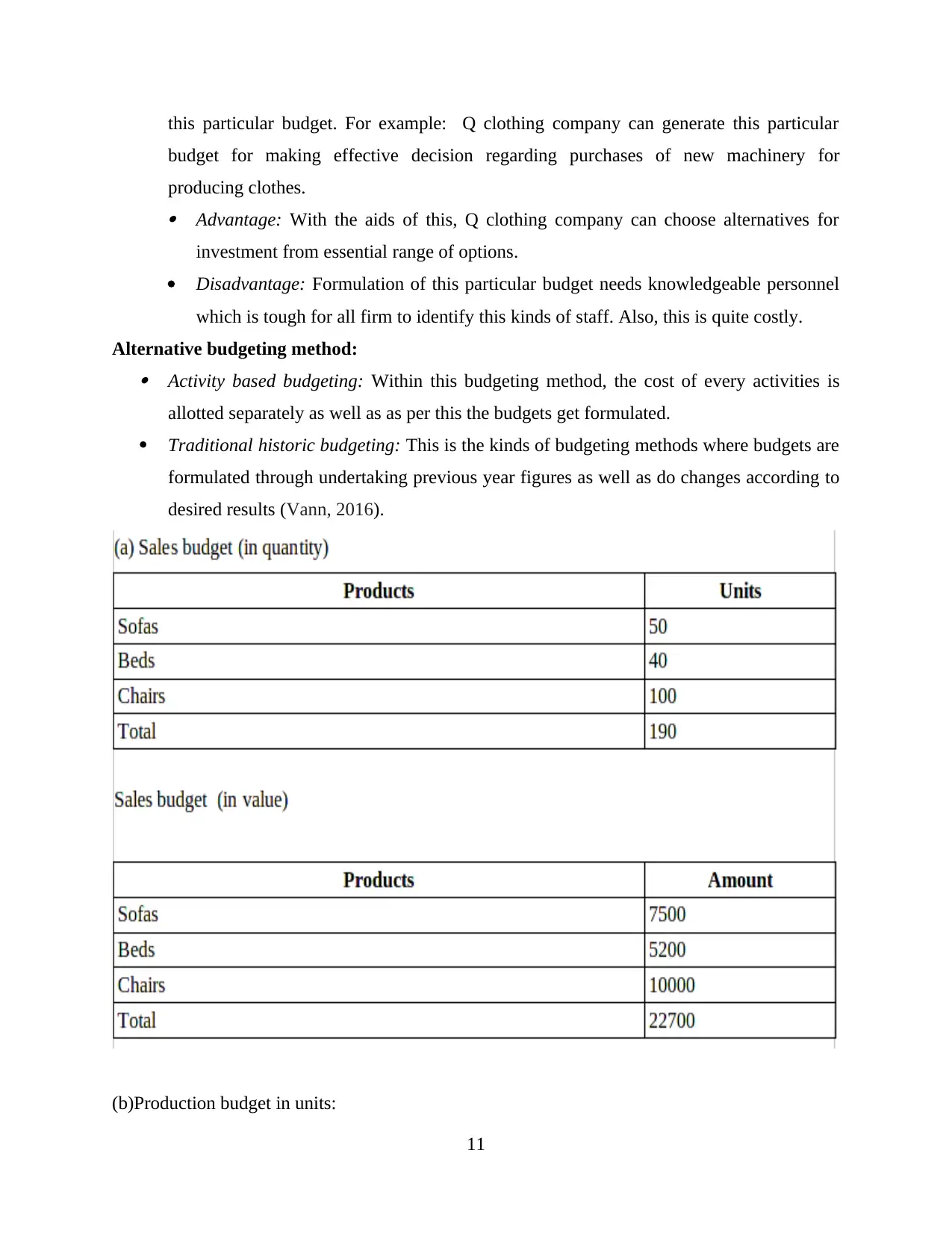

this particular budget. For example: Q clothing company can generate this particular

budget for making effective decision regarding purchases of new machinery for

producing clothes.

Advantage: With the aids of this, Q clothing company can choose alternatives for

investment from essential range of options.

Disadvantage: Formulation of this particular budget needs knowledgeable personnel

which is tough for all firm to identify this kinds of staff. Also, this is quite costly.

Alternative budgeting method: Activity based budgeting: Within this budgeting method, the cost of every activities is

allotted separately as well as as per this the budgets get formulated.

Traditional historic budgeting: This is the kinds of budgeting methods where budgets are

formulated through undertaking previous year figures as well as do changes according to

desired results (Vann, 2016).

(b)Production budget in units:

11

budget for making effective decision regarding purchases of new machinery for

producing clothes.

Advantage: With the aids of this, Q clothing company can choose alternatives for

investment from essential range of options.

Disadvantage: Formulation of this particular budget needs knowledgeable personnel

which is tough for all firm to identify this kinds of staff. Also, this is quite costly.

Alternative budgeting method: Activity based budgeting: Within this budgeting method, the cost of every activities is

allotted separately as well as as per this the budgets get formulated.

Traditional historic budgeting: This is the kinds of budgeting methods where budgets are

formulated through undertaking previous year figures as well as do changes according to

desired results (Vann, 2016).

(b)Production budget in units:

11

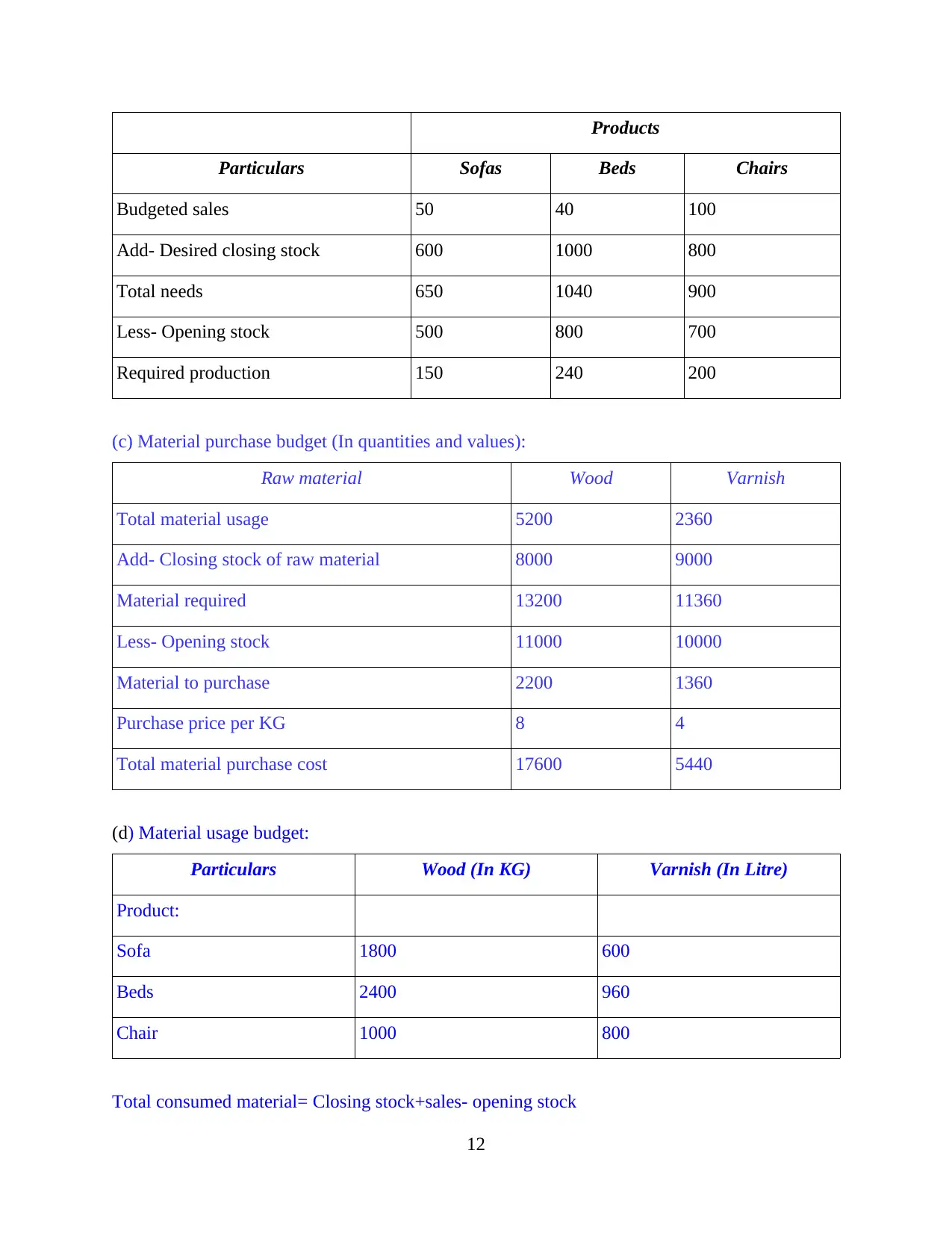

Products

Particulars Sofas Beds Chairs

Budgeted sales 50 40 100

Add- Desired closing stock 600 1000 800

Total needs 650 1040 900

Less- Opening stock 500 800 700

Required production 150 240 200

(c) Material purchase budget (In quantities and values):

Raw material Wood Varnish

Total material usage 5200 2360

Add- Closing stock of raw material 8000 9000

Material required 13200 11360

Less- Opening stock 11000 10000

Material to purchase 2200 1360

Purchase price per KG 8 4

Total material purchase cost 17600 5440

(d) Material usage budget:

Particulars Wood (In KG) Varnish (In Litre)

Product:

Sofa 1800 600

Beds 2400 960

Chair 1000 800

Total consumed material= Closing stock+sales- opening stock

12

Particulars Sofas Beds Chairs

Budgeted sales 50 40 100

Add- Desired closing stock 600 1000 800

Total needs 650 1040 900

Less- Opening stock 500 800 700

Required production 150 240 200

(c) Material purchase budget (In quantities and values):

Raw material Wood Varnish

Total material usage 5200 2360

Add- Closing stock of raw material 8000 9000

Material required 13200 11360

Less- Opening stock 11000 10000

Material to purchase 2200 1360

Purchase price per KG 8 4

Total material purchase cost 17600 5440

(d) Material usage budget:

Particulars Wood (In KG) Varnish (In Litre)

Product:

Sofa 1800 600

Beds 2400 960

Chair 1000 800

Total consumed material= Closing stock+sales- opening stock

12

13

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

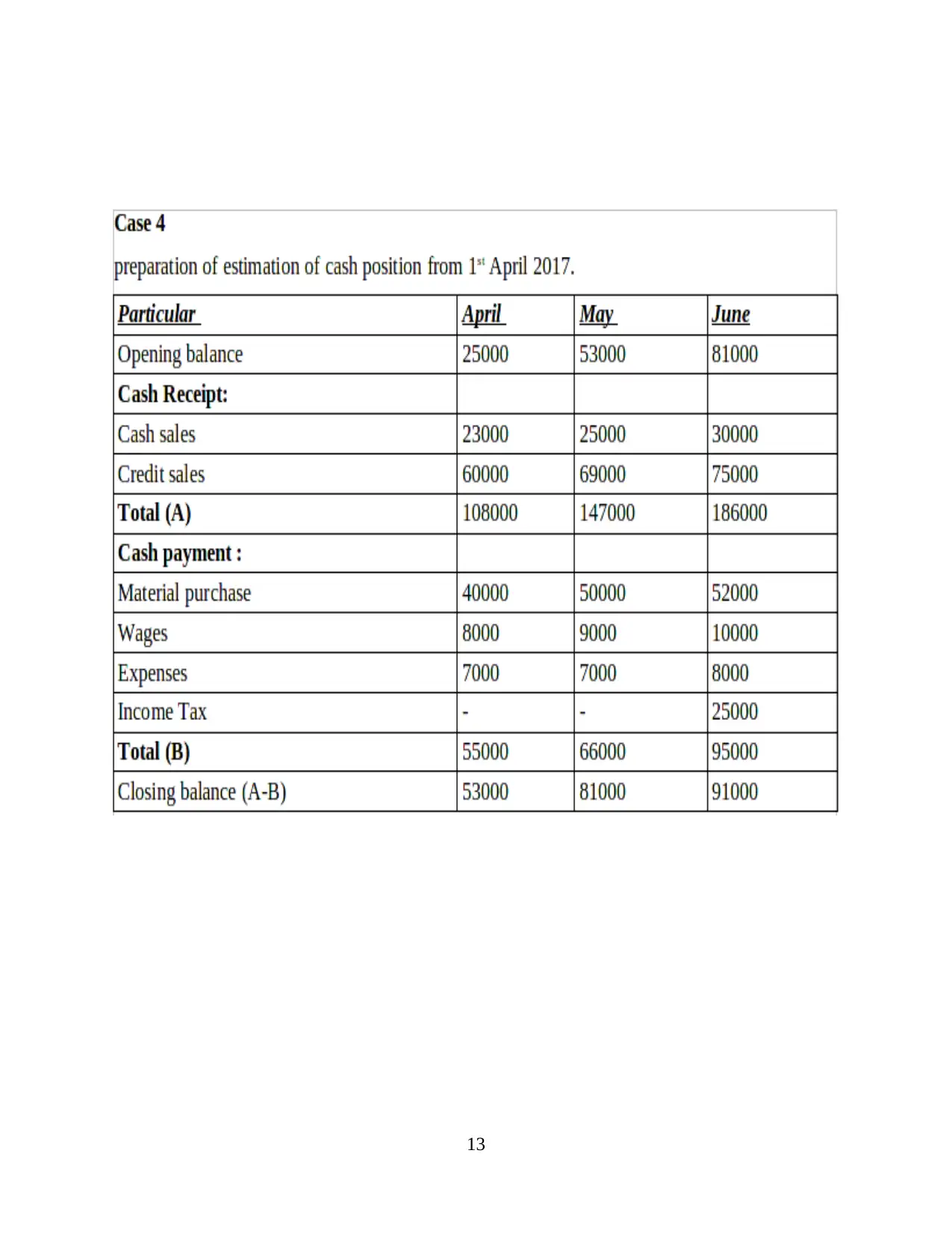

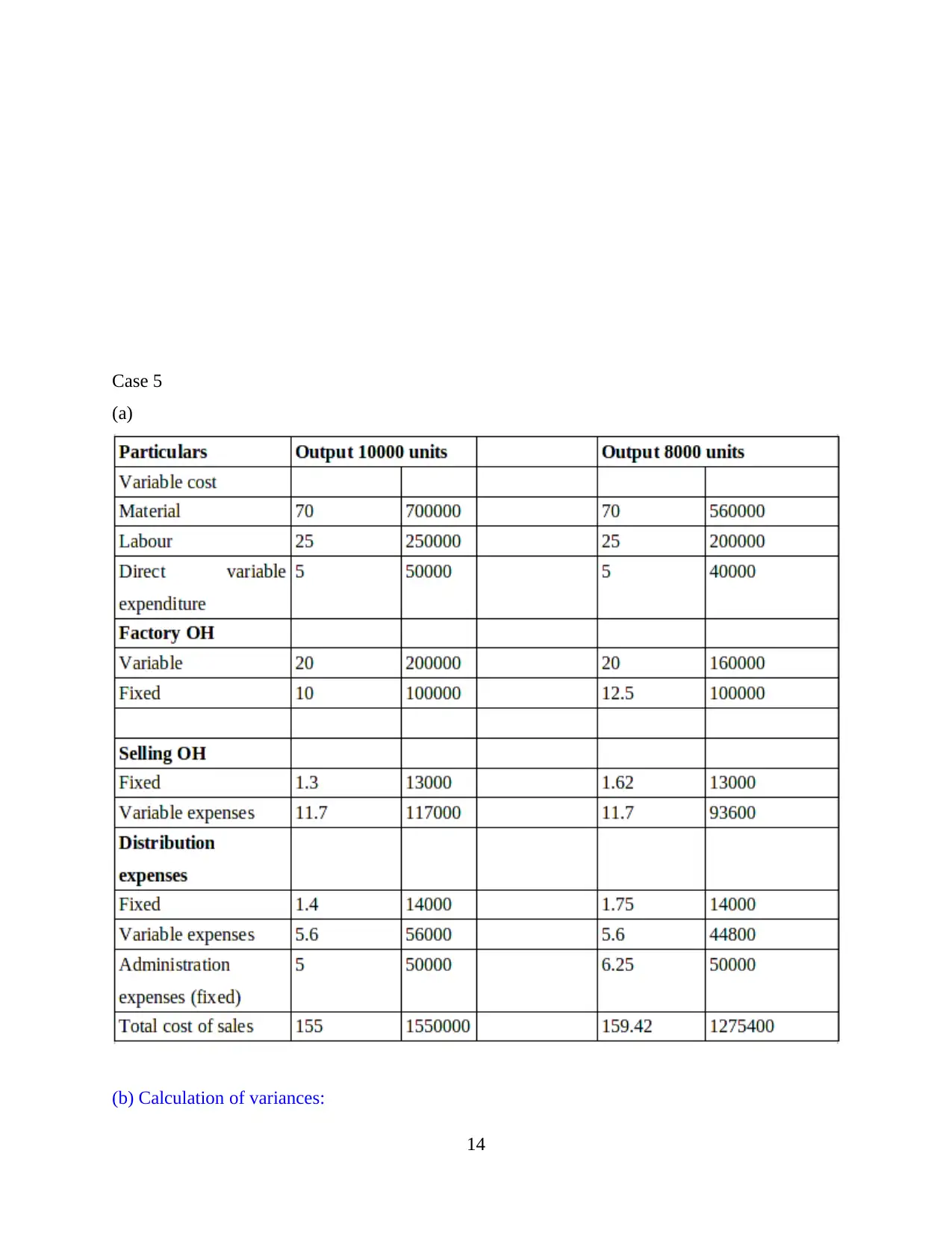

Case 5

(a)

(b) Calculation of variances:

14

(a)

(b) Calculation of variances:

14

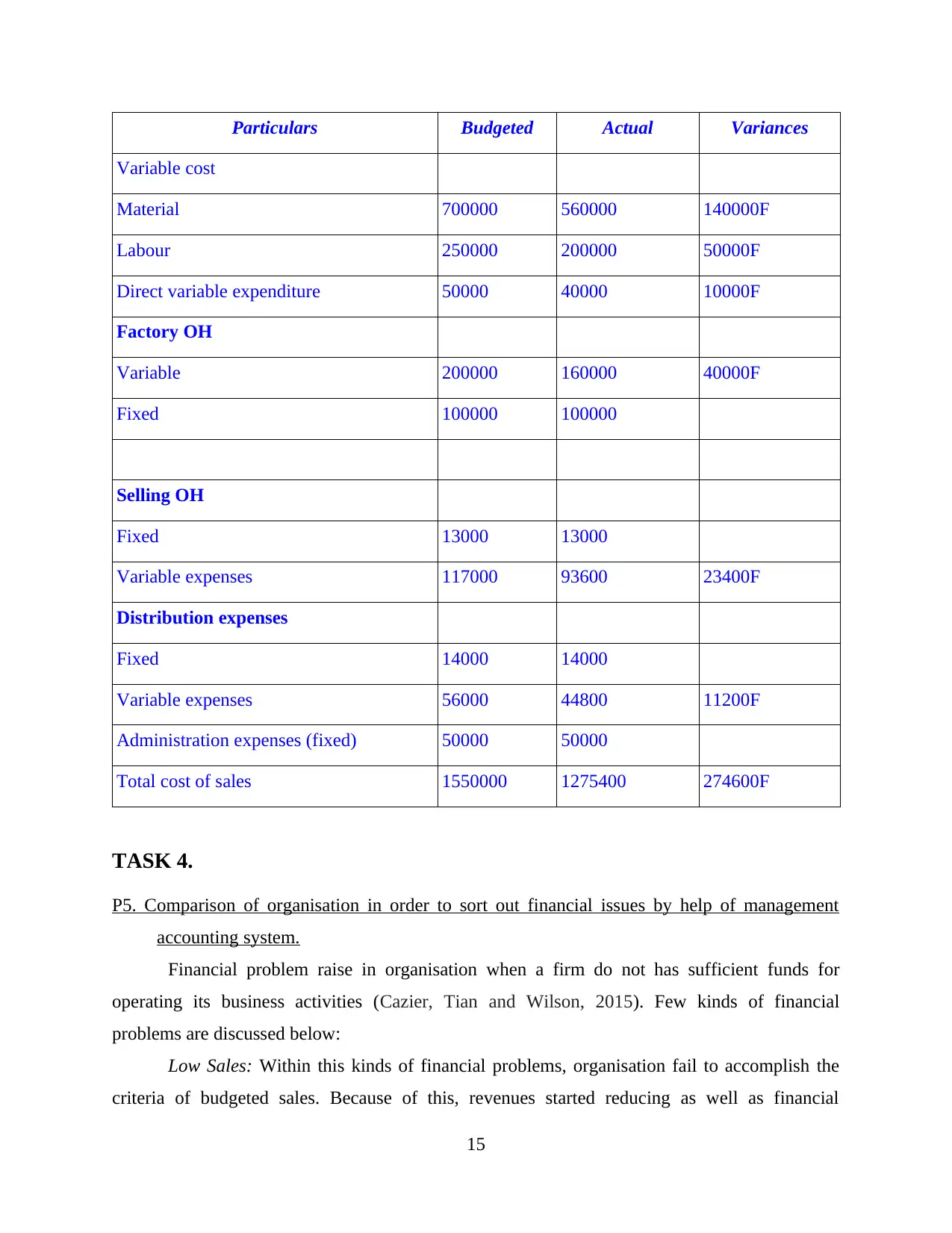

Particulars Budgeted Actual Variances

Variable cost

Material 700000 560000 140000F

Labour 250000 200000 50000F

Direct variable expenditure 50000 40000 10000F

Factory OH

Variable 200000 160000 40000F

Fixed 100000 100000

Selling OH

Fixed 13000 13000

Variable expenses 117000 93600 23400F

Distribution expenses

Fixed 14000 14000

Variable expenses 56000 44800 11200F

Administration expenses (fixed) 50000 50000

Total cost of sales 1550000 1275400 274600F

TASK 4.

P5. Comparison of organisation in order to sort out financial issues by help of management

accounting system.

Financial problem raise in organisation when a firm do not has sufficient funds for

operating its business activities (Cazier, Tian and Wilson, 2015). Few kinds of financial

problems are discussed below:

Low Sales: Within this kinds of financial problems, organisation fail to accomplish the

criteria of budgeted sales. Because of this, revenues started reducing as well as financial

15

Variable cost

Material 700000 560000 140000F

Labour 250000 200000 50000F

Direct variable expenditure 50000 40000 10000F

Factory OH

Variable 200000 160000 40000F

Fixed 100000 100000

Selling OH

Fixed 13000 13000

Variable expenses 117000 93600 23400F

Distribution expenses

Fixed 14000 14000

Variable expenses 56000 44800 11200F

Administration expenses (fixed) 50000 50000

Total cost of sales 1550000 1275400 274600F

TASK 4.

P5. Comparison of organisation in order to sort out financial issues by help of management

accounting system.

Financial problem raise in organisation when a firm do not has sufficient funds for

operating its business activities (Cazier, Tian and Wilson, 2015). Few kinds of financial

problems are discussed below:

Low Sales: Within this kinds of financial problems, organisation fail to accomplish the

criteria of budgeted sales. Because of this, revenues started reducing as well as financial

15

problems arises. For example: In Q clothing company, they are dealing with this particular

problems as its clothing sales is minimising continuously.

Enhanced expenses: This is the another problems that is generally faced through mos t of

the firms. Main reason of having this problems is in appropriate allocation of funds into activities

as well as lack of control over expenditures.

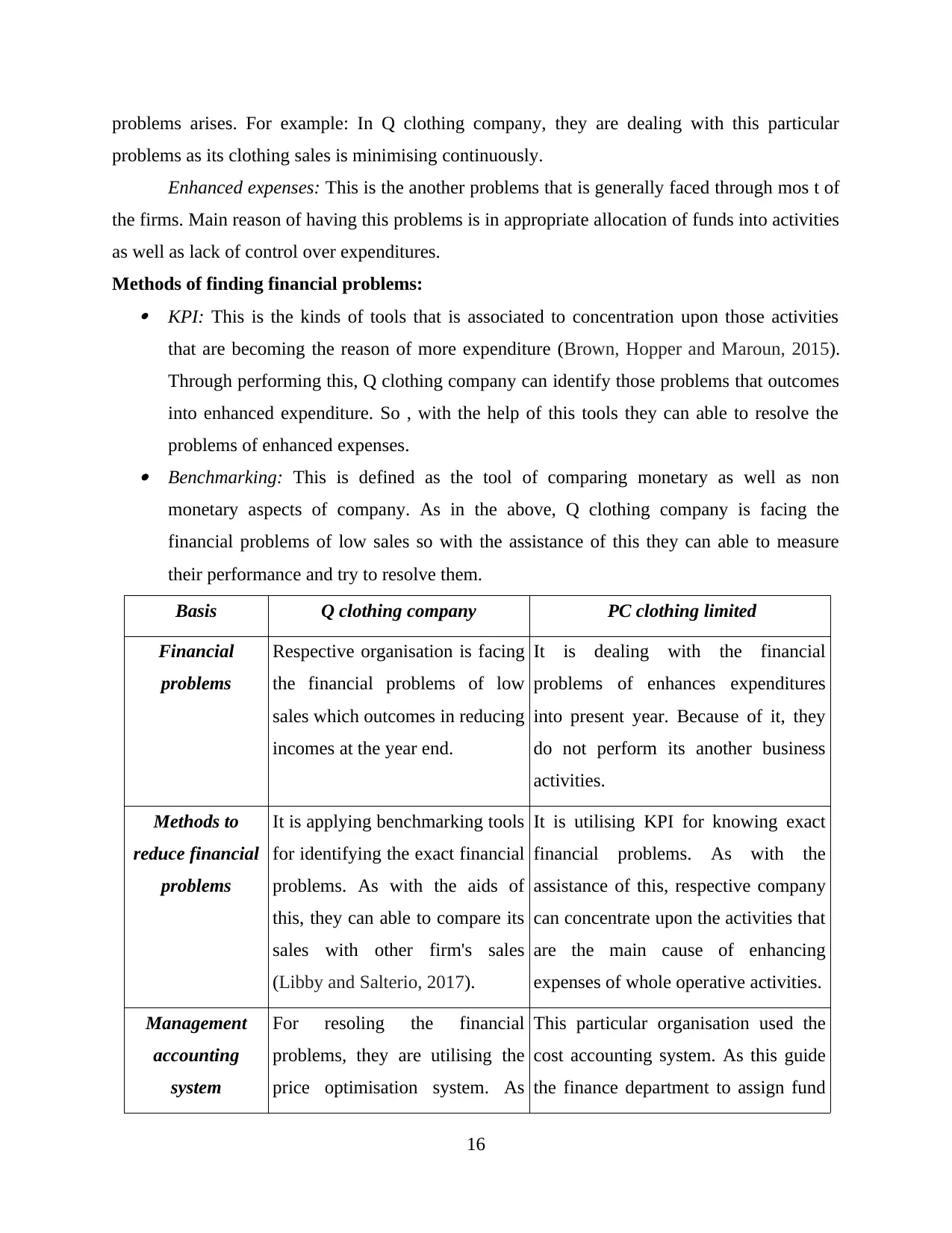

Methods of finding financial problems: KPI: This is the kinds of tools that is associated to concentration upon those activities

that are becoming the reason of more expenditure (Brown, Hopper and Maroun, 2015).

Through performing this, Q clothing company can identify those problems that outcomes

into enhanced expenditure. So , with the help of this tools they can able to resolve the

problems of enhanced expenses. Benchmarking: This is defined as the tool of comparing monetary as well as non

monetary aspects of company. As in the above, Q clothing company is facing the

financial problems of low sales so with the assistance of this they can able to measure

their performance and try to resolve them.

Basis Q clothing company PC clothing limited

Financial

problems

Respective organisation is facing

the financial problems of low

sales which outcomes in reducing

incomes at the year end.

It is dealing with the financial

problems of enhances expenditures

into present year. Because of it, they

do not perform its another business

activities.

Methods to

reduce financial

problems

It is applying benchmarking tools

for identifying the exact financial

problems. As with the aids of

this, they can able to compare its

sales with other firm's sales

(Libby and Salterio, 2017).

It is utilising KPI for knowing exact

financial problems. As with the

assistance of this, respective company

can concentrate upon the activities that

are the main cause of enhancing

expenses of whole operative activities.

Management

accounting

system

For resoling the financial

problems, they are utilising the

price optimisation system. As

This particular organisation used the

cost accounting system. As this guide

the finance department to assign fund

16

problems as its clothing sales is minimising continuously.

Enhanced expenses: This is the another problems that is generally faced through mos t of

the firms. Main reason of having this problems is in appropriate allocation of funds into activities

as well as lack of control over expenditures.

Methods of finding financial problems: KPI: This is the kinds of tools that is associated to concentration upon those activities

that are becoming the reason of more expenditure (Brown, Hopper and Maroun, 2015).

Through performing this, Q clothing company can identify those problems that outcomes

into enhanced expenditure. So , with the help of this tools they can able to resolve the

problems of enhanced expenses. Benchmarking: This is defined as the tool of comparing monetary as well as non

monetary aspects of company. As in the above, Q clothing company is facing the

financial problems of low sales so with the assistance of this they can able to measure

their performance and try to resolve them.

Basis Q clothing company PC clothing limited

Financial

problems

Respective organisation is facing

the financial problems of low

sales which outcomes in reducing

incomes at the year end.

It is dealing with the financial

problems of enhances expenditures

into present year. Because of it, they

do not perform its another business

activities.

Methods to

reduce financial

problems

It is applying benchmarking tools

for identifying the exact financial

problems. As with the aids of

this, they can able to compare its

sales with other firm's sales

(Libby and Salterio, 2017).

It is utilising KPI for knowing exact

financial problems. As with the

assistance of this, respective company

can concentrate upon the activities that

are the main cause of enhancing

expenses of whole operative activities.

Management

accounting

system

For resoling the financial

problems, they are utilising the

price optimisation system. As

This particular organisation used the

cost accounting system. As this guide

the finance department to assign fund

16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

this aids them to set the effective

price of cloths which is

appropriate for clients. Through

doing this, Q clothing company

can enhance its sales along with

revenue.

efficaciously. Also through using this,

they can minimises its useless

expenses and solved their financial

problems.

CONCLUSION

As per the above report, it have been concluded that management accounting is plays

crucial role in organisation as this help them to manager all financial reports, information and

others effectively and efficiently. There are some management accounting system such as cost,

tax etc. which assist them to set price and so on. Moreover, there are few management

accounting report like inventory, cost accounting and may others aids them in making decisions

in effective and efficient manner.

17

price of cloths which is

appropriate for clients. Through

doing this, Q clothing company

can enhance its sales along with

revenue.

efficaciously. Also through using this,

they can minimises its useless

expenses and solved their financial

problems.

CONCLUSION

As per the above report, it have been concluded that management accounting is plays

crucial role in organisation as this help them to manager all financial reports, information and

others effectively and efficiently. There are some management accounting system such as cost,

tax etc. which assist them to set price and so on. Moreover, there are few management

accounting report like inventory, cost accounting and may others aids them in making decisions

in effective and efficient manner.

17

REFERENCES

Books and Journals

Fullerton, R. R., Kennedy, F. A. and Widener, S. K., 2013. Management accounting and control

practices in a lean manufacturing environment. Accounting, Organizations and

Society. 38(1). pp.50-71.

Kihn, L. A. and Ihantola, E. M., 2015. Approaches to validation and evaluation in qualitative

studies of management accounting. Qualitative Research in Accounting & Management. 12(3).

pp.230-255.

Kihn, L. A. and Ihantola, E. M., 2015. Approaches to validation and evaluation in qualitative

studies of management accounting. Qualitative Research in Accounting &

Management. 12(3). pp.230-255.

Messner, M., 2016. Does industry matter? How industry context shapes management accounting

practice. Management Accounting Research. 31. pp.103-111.

Hanif, H., Rakhman, A. and Nurkholis, M., 2019. The Construction of Entrepreneurial

Accounting: Evidence from Indonesia. Reference to this paper should be made as

follows: Hanif, H. pp.104-117.

Zvezdov, D. and Schaltegger, S., 2015. Decision support through carbon management

accounting—A framework-based literature review. In Corporate carbon and climate

accounting(pp. 27-44). Springer, Cham.

Luft, J., 2016. Cooperation and competition among employees: Experimental evidence on the

role of management control systems. Management Accounting Research. 31. pp.75-85.

Cazier, R., Rego, S., Tian, X. and Wilson, R., 2015. The impact of increased disclosure

requirements and the standardization of accounting practices on earnings management

through the reserve for income taxes. Review of Accounting Studies. 20(1). pp.436-469.

Brown, J., Dillard, J., Hopper, T., Atkins, J., Atkins, B.C., Thomson, I. and Maroun, W., 2015.

“Good” news from nowhere: imagining utopian sustainable accounting. Accounting,

Auditing & Accountability Journal.

Libby, T. and Salterio, S. E., 2017. Deception in Management Accounting Experimental

Research:" A Tricky Issue" Revisited. Journal of Management Accounting Research.

Aouni, B., McGillis, S. and Abdulkarim, M .E., 2017. Goal programming model for management

accounting and auditing: a new typology. Annals of Operations Research. 251(1-2).

pp.41-54.

Vann, C .E., 2016. Strategic benefits of integrating the managerial accounting function with

supply chain management. Journal of Corporate Accounting & Finance. 27(3). pp.21-

30.

Arunruangsirilert, T. and Chonglerttham, S., 2017. Effect of corporate governance characteristics

on strategic management accounting in Thailand. Asian Review of Accounting. 25(1).

pp.85-105.

18

Books and Journals

Fullerton, R. R., Kennedy, F. A. and Widener, S. K., 2013. Management accounting and control

practices in a lean manufacturing environment. Accounting, Organizations and

Society. 38(1). pp.50-71.

Kihn, L. A. and Ihantola, E. M., 2015. Approaches to validation and evaluation in qualitative

studies of management accounting. Qualitative Research in Accounting & Management. 12(3).

pp.230-255.

Kihn, L. A. and Ihantola, E. M., 2015. Approaches to validation and evaluation in qualitative

studies of management accounting. Qualitative Research in Accounting &

Management. 12(3). pp.230-255.

Messner, M., 2016. Does industry matter? How industry context shapes management accounting

practice. Management Accounting Research. 31. pp.103-111.

Hanif, H., Rakhman, A. and Nurkholis, M., 2019. The Construction of Entrepreneurial

Accounting: Evidence from Indonesia. Reference to this paper should be made as

follows: Hanif, H. pp.104-117.

Zvezdov, D. and Schaltegger, S., 2015. Decision support through carbon management

accounting—A framework-based literature review. In Corporate carbon and climate

accounting(pp. 27-44). Springer, Cham.

Luft, J., 2016. Cooperation and competition among employees: Experimental evidence on the

role of management control systems. Management Accounting Research. 31. pp.75-85.

Cazier, R., Rego, S., Tian, X. and Wilson, R., 2015. The impact of increased disclosure

requirements and the standardization of accounting practices on earnings management

through the reserve for income taxes. Review of Accounting Studies. 20(1). pp.436-469.

Brown, J., Dillard, J., Hopper, T., Atkins, J., Atkins, B.C., Thomson, I. and Maroun, W., 2015.

“Good” news from nowhere: imagining utopian sustainable accounting. Accounting,

Auditing & Accountability Journal.

Libby, T. and Salterio, S. E., 2017. Deception in Management Accounting Experimental

Research:" A Tricky Issue" Revisited. Journal of Management Accounting Research.

Aouni, B., McGillis, S. and Abdulkarim, M .E., 2017. Goal programming model for management

accounting and auditing: a new typology. Annals of Operations Research. 251(1-2).

pp.41-54.

Vann, C .E., 2016. Strategic benefits of integrating the managerial accounting function with

supply chain management. Journal of Corporate Accounting & Finance. 27(3). pp.21-

30.

Arunruangsirilert, T. and Chonglerttham, S., 2017. Effect of corporate governance characteristics

on strategic management accounting in Thailand. Asian Review of Accounting. 25(1).

pp.85-105.

18

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.