Management Accounting: Variance Analysis and Strategic Implications

VerifiedAdded on 2021/06/14

|8

|817

|89

Homework Assignment

AI Summary

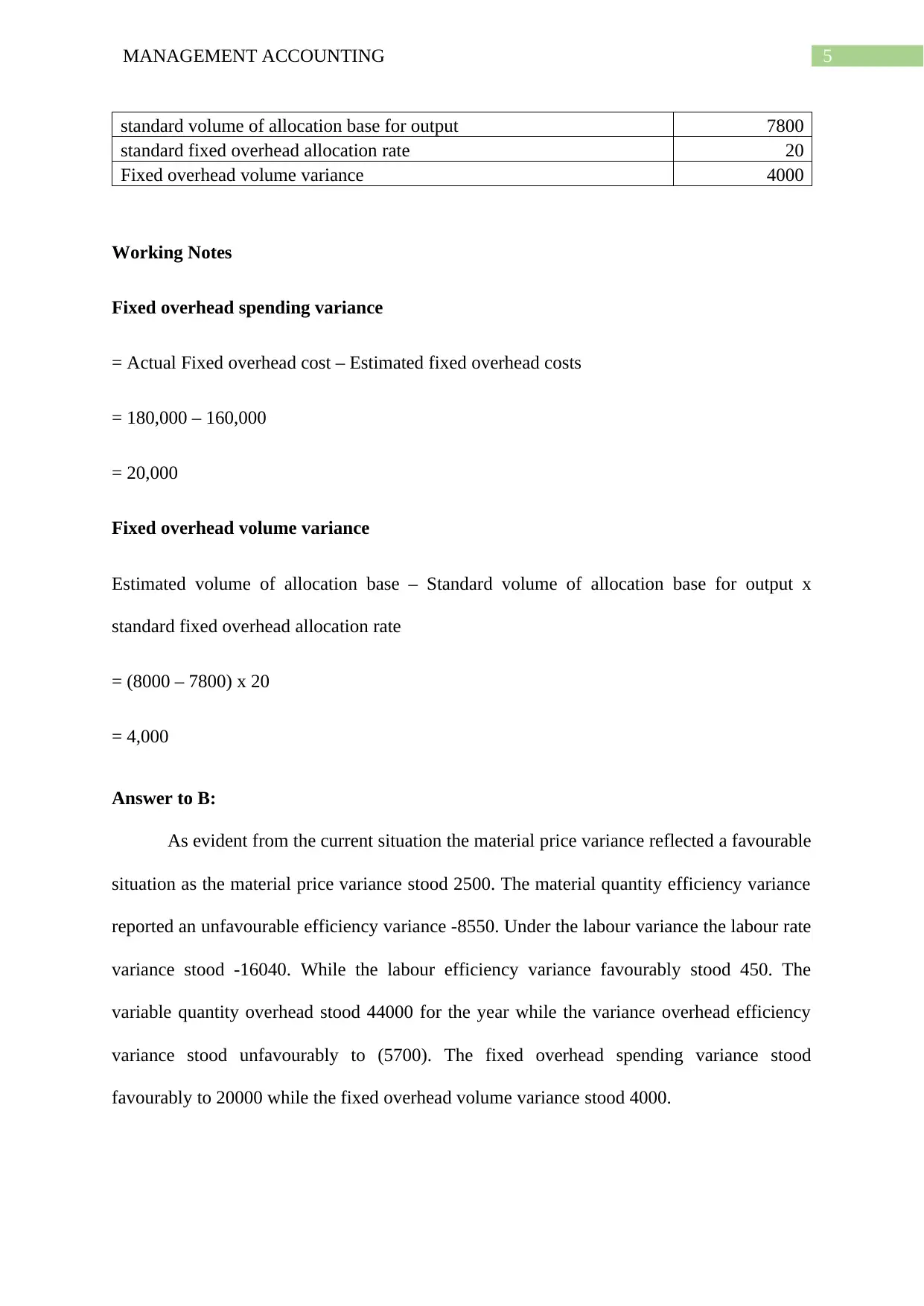

This assignment provides a detailed analysis of variances in management accounting, focusing on material, labor, and overhead costs. It calculates and interprets material price and quantity variances, labor rate and efficiency variances, and variable and fixed overhead spending and efficiency variances. The analysis reveals both favorable and unfavorable variances, highlighting areas needing attention, such as material quantity and labor rate variances. Recommendations are made for further investigation into the causes of unfavorable variances to improve cost control and efficiency. Desklib offers this and other solved assignments to aid students in their studies.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.