Management Accounting Report: Decision Making and Systems

VerifiedAdded on 2020/10/04

|16

|4712

|42

Report

AI Summary

This report examines the role of management accounting in business decision-making, particularly within the context of Zylla Company, a multinational organization. It defines management accounting, contrasting it with financial accounting, and explores various systems such as cost accounting, job costing, and inventory management. The report delves into different managerial reporting methods, including job cost reports, accounts receivable reports, and budget reports. Furthermore, it analyzes cost calculation techniques, specifically marginal costing and absorption costing, providing an example income statement for each method. The report also discusses the advantages and disadvantages of planning tools in budgetary control and explores the application of management accounting systems in addressing financial difficulties. Overall, the report emphasizes the importance of management accounting in improving analysis, decision-making, and responding to financial challenges within a complex business environment.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

LO 1.................................................................................................................................................1

P1 Explaining management accounting and the essential requirement of different systems......1

P2 Different methods used by managers for managerial reporting.............................................3

LO 2.................................................................................................................................................5

P3 Calculating costs using appropriate methods of cost analysis................................................5

LO 3.................................................................................................................................................7

P4 various advantage and drawbacks of various planning tools in budgetary control................7

LO 4...............................................................................................................................................10

P5 Use of management accounting systems to respond financial difficulties...........................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

LO 1.................................................................................................................................................1

P1 Explaining management accounting and the essential requirement of different systems......1

P2 Different methods used by managers for managerial reporting.............................................3

LO 2.................................................................................................................................................5

P3 Calculating costs using appropriate methods of cost analysis................................................5

LO 3.................................................................................................................................................7

P4 various advantage and drawbacks of various planning tools in budgetary control................7

LO 4...............................................................................................................................................10

P5 Use of management accounting systems to respond financial difficulties...........................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Everyday, business owners are faced with endless number of decisions for the growth and

long-lasting survival of an enterprise. Managerial accounting plays an inevitable role in this by

supplying data-driven input to the managers for improving its long-term decision making system.

Business managers utilize it as a powerful tool to make countless decisions that assure

competitive success and build a strong reputation. Zylla company is a large-sized multinational

organization that operating all around the world. In the complex environment, organization

undergone with a significant changes following expansion strategy, acquisition plan,

restructuring. However, in an uncertain macro-environment and technological world, managerial

team are looking for revamping its existing systems by adopting newer ones to improve its

analysis and decision-making system. The proposed research emphasizes upon studying new

systems and its integration for better reporting. Moreover, various techniques of cost

determination, forecasting and minimizing financial turbulence will be examined in detail.

LO 1

P1 Explaining management accounting and the essential requirement of different systems

Definition: Management accounting is a process, in which, only top managers are

involved who make plan, prepare reports and analyse past performance of an entity to create

rational policies and decisions.

History: The concept of MA first came in the period of early 19th century, more

importantly, for overseas and large companies, but, over the period, every companies regardless

their sizes and geographical presences use different tools and techniques of it to make better

policy formation, business control and other decisions.

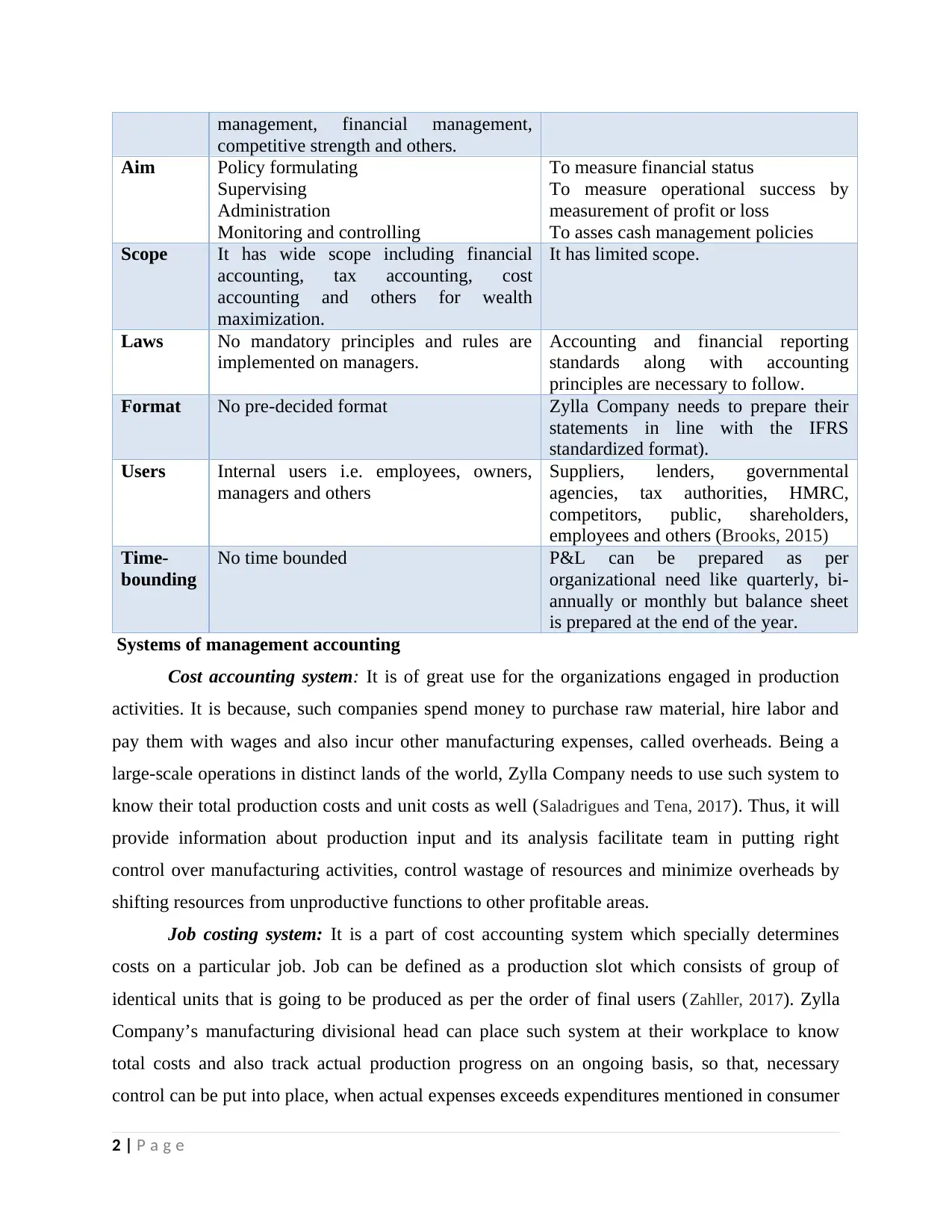

Management accounting Versus Financial accounting

Basis of

differenc

e

Management accounting Financial accounting

Define MA is a procedure wherein top level

executives, business managers and

directors prepare reports and use financial

or statistical information for creating

policies and decisions i.e. risk

It is a method of preparation of

financial statements that present details

about the result of historical trading

function of Zylla Company (Schipper,

Francis and Weil, 2017).

1 | P a g e

Everyday, business owners are faced with endless number of decisions for the growth and

long-lasting survival of an enterprise. Managerial accounting plays an inevitable role in this by

supplying data-driven input to the managers for improving its long-term decision making system.

Business managers utilize it as a powerful tool to make countless decisions that assure

competitive success and build a strong reputation. Zylla company is a large-sized multinational

organization that operating all around the world. In the complex environment, organization

undergone with a significant changes following expansion strategy, acquisition plan,

restructuring. However, in an uncertain macro-environment and technological world, managerial

team are looking for revamping its existing systems by adopting newer ones to improve its

analysis and decision-making system. The proposed research emphasizes upon studying new

systems and its integration for better reporting. Moreover, various techniques of cost

determination, forecasting and minimizing financial turbulence will be examined in detail.

LO 1

P1 Explaining management accounting and the essential requirement of different systems

Definition: Management accounting is a process, in which, only top managers are

involved who make plan, prepare reports and analyse past performance of an entity to create

rational policies and decisions.

History: The concept of MA first came in the period of early 19th century, more

importantly, for overseas and large companies, but, over the period, every companies regardless

their sizes and geographical presences use different tools and techniques of it to make better

policy formation, business control and other decisions.

Management accounting Versus Financial accounting

Basis of

differenc

e

Management accounting Financial accounting

Define MA is a procedure wherein top level

executives, business managers and

directors prepare reports and use financial

or statistical information for creating

policies and decisions i.e. risk

It is a method of preparation of

financial statements that present details

about the result of historical trading

function of Zylla Company (Schipper,

Francis and Weil, 2017).

1 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

management, financial management,

competitive strength and others.

Aim Policy formulating

Supervising

Administration

Monitoring and controlling

To measure financial status

To measure operational success by

measurement of profit or loss

To asses cash management policies

Scope It has wide scope including financial

accounting, tax accounting, cost

accounting and others for wealth

maximization.

It has limited scope.

Laws No mandatory principles and rules are

implemented on managers.

Accounting and financial reporting

standards along with accounting

principles are necessary to follow.

Format No pre-decided format Zylla Company needs to prepare their

statements in line with the IFRS

standardized format).

Users Internal users i.e. employees, owners,

managers and others

Suppliers, lenders, governmental

agencies, tax authorities, HMRC,

competitors, public, shareholders,

employees and others (Brooks, 2015)

Time-

bounding

No time bounded P&L can be prepared as per

organizational need like quarterly, bi-

annually or monthly but balance sheet

is prepared at the end of the year.

Systems of management accounting

Cost accounting system: It is of great use for the organizations engaged in production

activities. It is because, such companies spend money to purchase raw material, hire labor and

pay them with wages and also incur other manufacturing expenses, called overheads. Being a

large-scale operations in distinct lands of the world, Zylla Company needs to use such system to

know their total production costs and unit costs as well (Saladrigues and Tena, 2017). Thus, it will

provide information about production input and its analysis facilitate team in putting right

control over manufacturing activities, control wastage of resources and minimize overheads by

shifting resources from unproductive functions to other profitable areas.

Job costing system: It is a part of cost accounting system which specially determines

costs on a particular job. Job can be defined as a production slot which consists of group of

identical units that is going to be produced as per the order of final users (Zahller, 2017). Zylla

Company’s manufacturing divisional head can place such system at their workplace to know

total costs and also track actual production progress on an ongoing basis, so that, necessary

control can be put into place, when actual expenses exceeds expenditures mentioned in consumer

2 | P a g e

competitive strength and others.

Aim Policy formulating

Supervising

Administration

Monitoring and controlling

To measure financial status

To measure operational success by

measurement of profit or loss

To asses cash management policies

Scope It has wide scope including financial

accounting, tax accounting, cost

accounting and others for wealth

maximization.

It has limited scope.

Laws No mandatory principles and rules are

implemented on managers.

Accounting and financial reporting

standards along with accounting

principles are necessary to follow.

Format No pre-decided format Zylla Company needs to prepare their

statements in line with the IFRS

standardized format).

Users Internal users i.e. employees, owners,

managers and others

Suppliers, lenders, governmental

agencies, tax authorities, HMRC,

competitors, public, shareholders,

employees and others (Brooks, 2015)

Time-

bounding

No time bounded P&L can be prepared as per

organizational need like quarterly, bi-

annually or monthly but balance sheet

is prepared at the end of the year.

Systems of management accounting

Cost accounting system: It is of great use for the organizations engaged in production

activities. It is because, such companies spend money to purchase raw material, hire labor and

pay them with wages and also incur other manufacturing expenses, called overheads. Being a

large-scale operations in distinct lands of the world, Zylla Company needs to use such system to

know their total production costs and unit costs as well (Saladrigues and Tena, 2017). Thus, it will

provide information about production input and its analysis facilitate team in putting right

control over manufacturing activities, control wastage of resources and minimize overheads by

shifting resources from unproductive functions to other profitable areas.

Job costing system: It is a part of cost accounting system which specially determines

costs on a particular job. Job can be defined as a production slot which consists of group of

identical units that is going to be produced as per the order of final users (Zahller, 2017). Zylla

Company’s manufacturing divisional head can place such system at their workplace to know

total costs and also track actual production progress on an ongoing basis, so that, necessary

control can be put into place, when actual expenses exceeds expenditures mentioned in consumer

2 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

quotation. Such analysis also helps firm in price decisions in which a price is charged from the

consumer by adding some margin over the costs.

Inventory management system: Inventory is an important aspect of business that needs

to be managed to an adequate level. Over-stocking is not good because it exceeds cost of caring

unnecessarily whereas under-stocking is dangerous which threaten entity’s survival as company

will not be able to serve market demand resultant loss of customers. Although ERP is useful and

used by many establishments to record inventory but it requires entering raw information which

is automatically processed by the system. Unlike it, inventory management system run

automatically because it uses barcode system and radio frequency identification for electronic

content to track stock incoming and outgoing (Saladrigues and Tena, 2017). Zylla Company is a

multi-national enterprise which must use such system to regularly track their available stock and

place order timely to hold required units. It helps to overcome the risk of inventory stocked

below danger or safety stock.

Price optimization system: It is an advanced software which forecasts possible demand

and sales volume at different offering prices. In economy, law of demand shows that at high

price, customer tends to demand less or vice-versa (Schipper, Francis and Weil, 2017). The system

enable Zylla Company in knowing the elasticity of demand as a result of change in prices

keeping other variable constant. Thus, with the help of it, prices can be set at a correct level to

generate a good share in the industry and gain profitable growth.

Essential requirements for MA systems

Provide relevant and highly useful information

Easy to update so that predictive models such as trend forecasting can be used.

Data accuracy and authenticity

Instant reports

Confidentiality and data security

P2 Different methods used by managers for managerial reporting

Accounting reports are the main source of collection of needed information by the top

managers. Several important reports which Zylla Company managers and policy formulation

must use and examine to aid in successful policy creation are enumerated underneath:

Job cost reports: Job cost system can be implemented by Zylla Company to get instant

reports about costs incurred on a specific job. Such reports help them to know how much costs

3 | P a g e

consumer by adding some margin over the costs.

Inventory management system: Inventory is an important aspect of business that needs

to be managed to an adequate level. Over-stocking is not good because it exceeds cost of caring

unnecessarily whereas under-stocking is dangerous which threaten entity’s survival as company

will not be able to serve market demand resultant loss of customers. Although ERP is useful and

used by many establishments to record inventory but it requires entering raw information which

is automatically processed by the system. Unlike it, inventory management system run

automatically because it uses barcode system and radio frequency identification for electronic

content to track stock incoming and outgoing (Saladrigues and Tena, 2017). Zylla Company is a

multi-national enterprise which must use such system to regularly track their available stock and

place order timely to hold required units. It helps to overcome the risk of inventory stocked

below danger or safety stock.

Price optimization system: It is an advanced software which forecasts possible demand

and sales volume at different offering prices. In economy, law of demand shows that at high

price, customer tends to demand less or vice-versa (Schipper, Francis and Weil, 2017). The system

enable Zylla Company in knowing the elasticity of demand as a result of change in prices

keeping other variable constant. Thus, with the help of it, prices can be set at a correct level to

generate a good share in the industry and gain profitable growth.

Essential requirements for MA systems

Provide relevant and highly useful information

Easy to update so that predictive models such as trend forecasting can be used.

Data accuracy and authenticity

Instant reports

Confidentiality and data security

P2 Different methods used by managers for managerial reporting

Accounting reports are the main source of collection of needed information by the top

managers. Several important reports which Zylla Company managers and policy formulation

must use and examine to aid in successful policy creation are enumerated underneath:

Job cost reports: Job cost system can be implemented by Zylla Company to get instant

reports about costs incurred on a specific job. Such reports help them to know how much costs

3 | P a g e

they paid for acquiring required resources to produce a given number of units. They can also

match their quoted costs with the actual costs and made decisions (Fleischman and Parker,

2017). In addition, it enable establishment in setting an appropriate price by incorporating a

margin to the total costs by covering all fixed and variable costs.

Accounts receivable reports: Zylla Company operates worldwide, many of the business

clients prefer credit transaction, in which, they buy product from the company at credit and then

sell them to the consumers at cash and then make outstanding payment to the organization.

Although, by delivering credit sales, firm take financial risks, but, outstanding amount is paid by

the clients at some extra charges. Besides this, it also increase client base, market share, sales and

income, still, such decisions require careful attention of the team in assessing customer credit

rating, goodwill, ability to pay money and credit decisions (Lynch and Lynch, 2017). Zylla

Company also need regularly tracking their trade receivable to know how much cash is still

stacked and yet to receive. Thus, credit collection divisional managers can use these report for

such purpose and immediately respond and take actions against parties who found in default and

did not pay their debt on due date. It facilitate entity in managing their sources of cash and

minimize possible liquidity crunch in future.

Budget reports: Every-times, budget is prepare to communicate challenging targets to the

departmental heads which they are intended to achieve. Zylla Company’s all the purchase, sales,

production, marketing, research and development and other departments use it to self-evaluate

their progress. It help them to rethink and redesign plans and strategies to minimize costs and

maximize revenues keeping in mind the core focus on goals.

Inventory management reports: The best way of getting instant and quicker inventory

management reports is to use inventory management systems. As the system automatically

adjusts and alter the level of stocked units thus, reports are changed accordingly and alert

manager about possible inventory issues (Xu, 2018). Regular check of it helps to overcome the

risk of inappropriate inventory level by placing order on a right time that avoid under storage and

over storage.

Manufacturing reporting: Zylla Company can use ERP and manufacturing software

system that serves managers with a more real-time reporting beyond production reports.

Enterprise IQ manufacturing reports provide more authentic and sophisticated reporting

including configurable reporting for material, labor and overheads, real time equipment

4 | P a g e

match their quoted costs with the actual costs and made decisions (Fleischman and Parker,

2017). In addition, it enable establishment in setting an appropriate price by incorporating a

margin to the total costs by covering all fixed and variable costs.

Accounts receivable reports: Zylla Company operates worldwide, many of the business

clients prefer credit transaction, in which, they buy product from the company at credit and then

sell them to the consumers at cash and then make outstanding payment to the organization.

Although, by delivering credit sales, firm take financial risks, but, outstanding amount is paid by

the clients at some extra charges. Besides this, it also increase client base, market share, sales and

income, still, such decisions require careful attention of the team in assessing customer credit

rating, goodwill, ability to pay money and credit decisions (Lynch and Lynch, 2017). Zylla

Company also need regularly tracking their trade receivable to know how much cash is still

stacked and yet to receive. Thus, credit collection divisional managers can use these report for

such purpose and immediately respond and take actions against parties who found in default and

did not pay their debt on due date. It facilitate entity in managing their sources of cash and

minimize possible liquidity crunch in future.

Budget reports: Every-times, budget is prepare to communicate challenging targets to the

departmental heads which they are intended to achieve. Zylla Company’s all the purchase, sales,

production, marketing, research and development and other departments use it to self-evaluate

their progress. It help them to rethink and redesign plans and strategies to minimize costs and

maximize revenues keeping in mind the core focus on goals.

Inventory management reports: The best way of getting instant and quicker inventory

management reports is to use inventory management systems. As the system automatically

adjusts and alter the level of stocked units thus, reports are changed accordingly and alert

manager about possible inventory issues (Xu, 2018). Regular check of it helps to overcome the

risk of inappropriate inventory level by placing order on a right time that avoid under storage and

over storage.

Manufacturing reporting: Zylla Company can use ERP and manufacturing software

system that serves managers with a more real-time reporting beyond production reports.

Enterprise IQ manufacturing reports provide more authentic and sophisticated reporting

including configurable reporting for material, labor and overheads, real time equipment

4 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

effectiveness, easier readability, variance reporting, automatic labelling, automatic bar code

reading and data management (Manufacturing Production Reporting, 2016). It will assist

production head of the company in key areas i.e. stock control, warehouse management, quality

assurance and control, preventive maintenance and Overall Equipment Effectiveness (OEE).

LO 2

P3 Calculating costs using appropriate methods of cost analysis

Cost measurement is an important area of business decisions. It may be of different types such as

fixed and fluctuating, first remains constant at varied level of production and cannot be allocated to each

unit or item manufactured by Zylla Company. Unlike this, later changes in the same direction, means,

with the high level of production, such cost also tends to increase otherwise fall. There are two popular

ways which can be used to determine costs, that are presented here as under:

Marginal costing (MC): It is also called variable costing because, it uses only the variable means

fluctuating costs that changes in the same direction with the change in production (Horngren and et.al.,

2010). However, fixed costs is excluded in measuring production cost and deducted from the contribution

to present the net return.

Absorption costing (AC): Unlike MC, this method absorbed fixed overhead also using an

overhead absorption rate taking into account machinery hours and direct labor hours as a basis of

allocation. Although, it is used by companies, still, it is not a better way because allocating overhead

taking any aspect as base is not appropriate and thereby display misleading results (Macintosh and

Quattrone, 2010).

Example:

Costs: Material: GBP6, direct labor: GBP 5, production overheads (Variable): GBP2

Sales information: 600 units at the rate of GBP 35/each

Beginning stock: Nil

Budgeted overheads: Fixed manufacturing: GBP 2100

Administration: GBP 700

Sales overheads: GBP 1 on each unit

Income Statement according to variable costing method

Particulars Amount Amount

Revenue for the current year (600U0*@GBP 35 each unit ) 21000

5 | P a g e

reading and data management (Manufacturing Production Reporting, 2016). It will assist

production head of the company in key areas i.e. stock control, warehouse management, quality

assurance and control, preventive maintenance and Overall Equipment Effectiveness (OEE).

LO 2

P3 Calculating costs using appropriate methods of cost analysis

Cost measurement is an important area of business decisions. It may be of different types such as

fixed and fluctuating, first remains constant at varied level of production and cannot be allocated to each

unit or item manufactured by Zylla Company. Unlike this, later changes in the same direction, means,

with the high level of production, such cost also tends to increase otherwise fall. There are two popular

ways which can be used to determine costs, that are presented here as under:

Marginal costing (MC): It is also called variable costing because, it uses only the variable means

fluctuating costs that changes in the same direction with the change in production (Horngren and et.al.,

2010). However, fixed costs is excluded in measuring production cost and deducted from the contribution

to present the net return.

Absorption costing (AC): Unlike MC, this method absorbed fixed overhead also using an

overhead absorption rate taking into account machinery hours and direct labor hours as a basis of

allocation. Although, it is used by companies, still, it is not a better way because allocating overhead

taking any aspect as base is not appropriate and thereby display misleading results (Macintosh and

Quattrone, 2010).

Example:

Costs: Material: GBP6, direct labor: GBP 5, production overheads (Variable): GBP2

Sales information: 600 units at the rate of GBP 35/each

Beginning stock: Nil

Budgeted overheads: Fixed manufacturing: GBP 2100

Administration: GBP 700

Sales overheads: GBP 1 on each unit

Income Statement according to variable costing method

Particulars Amount Amount

Revenue for the current year (600U0*@GBP 35 each unit ) 21000

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

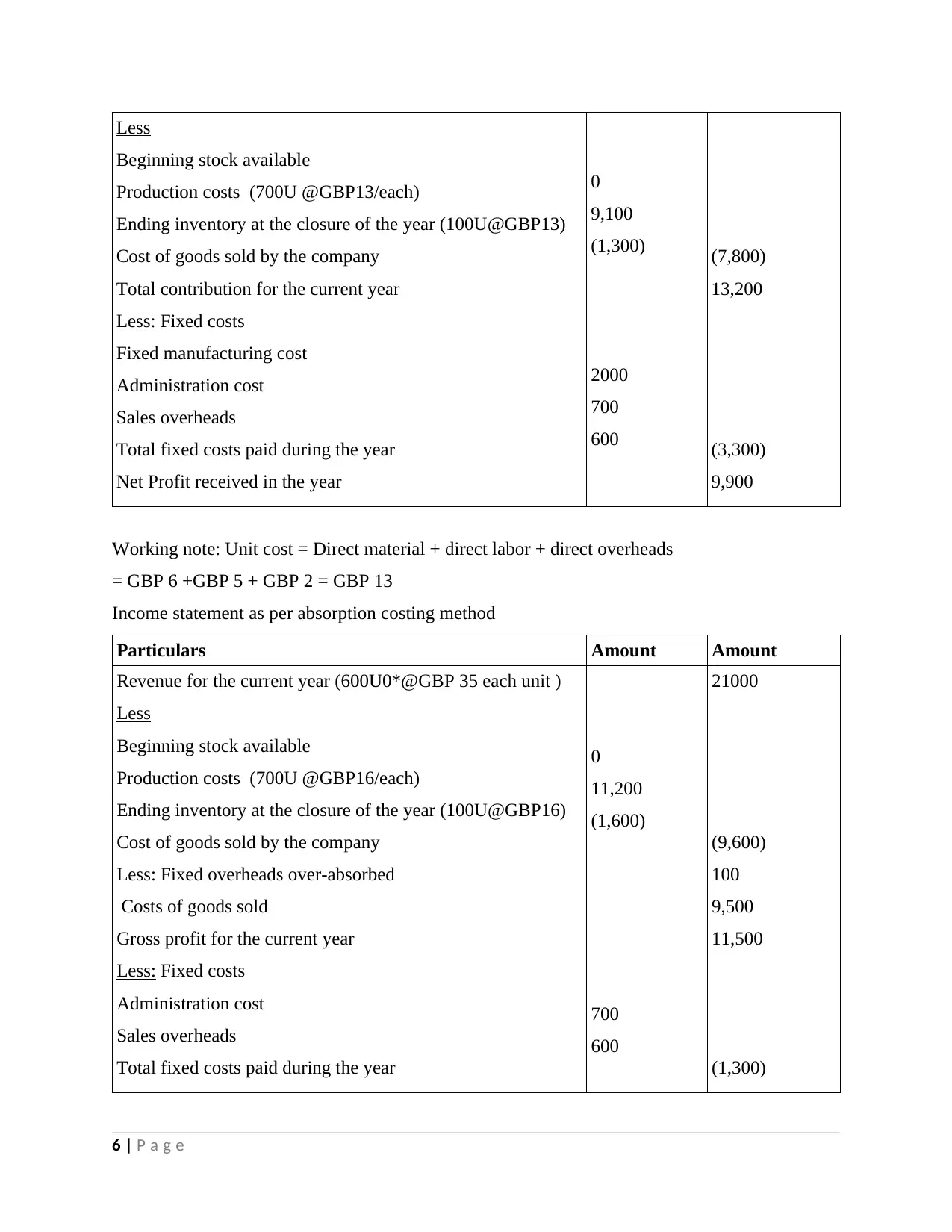

Less

Beginning stock available

Production costs (700U @GBP13/each)

Ending inventory at the closure of the year (100U@GBP13)

Cost of goods sold by the company

Total contribution for the current year

Less: Fixed costs

Fixed manufacturing cost

Administration cost

Sales overheads

Total fixed costs paid during the year

Net Profit received in the year

0

9,100

(1,300)

2000

700

600

(7,800)

13,200

(3,300)

9,900

Working note: Unit cost = Direct material + direct labor + direct overheads

= GBP 6 +GBP 5 + GBP 2 = GBP 13

Income statement as per absorption costing method

Particulars Amount Amount

Revenue for the current year (600U0*@GBP 35 each unit )

Less

Beginning stock available

Production costs (700U @GBP16/each)

Ending inventory at the closure of the year (100U@GBP16)

Cost of goods sold by the company

Less: Fixed overheads over-absorbed

Costs of goods sold

Gross profit for the current year

Less: Fixed costs

Administration cost

Sales overheads

Total fixed costs paid during the year

0

11,200

(1,600)

700

600

21000

(9,600)

100

9,500

11,500

(1,300)

6 | P a g e

Beginning stock available

Production costs (700U @GBP13/each)

Ending inventory at the closure of the year (100U@GBP13)

Cost of goods sold by the company

Total contribution for the current year

Less: Fixed costs

Fixed manufacturing cost

Administration cost

Sales overheads

Total fixed costs paid during the year

Net Profit received in the year

0

9,100

(1,300)

2000

700

600

(7,800)

13,200

(3,300)

9,900

Working note: Unit cost = Direct material + direct labor + direct overheads

= GBP 6 +GBP 5 + GBP 2 = GBP 13

Income statement as per absorption costing method

Particulars Amount Amount

Revenue for the current year (600U0*@GBP 35 each unit )

Less

Beginning stock available

Production costs (700U @GBP16/each)

Ending inventory at the closure of the year (100U@GBP16)

Cost of goods sold by the company

Less: Fixed overheads over-absorbed

Costs of goods sold

Gross profit for the current year

Less: Fixed costs

Administration cost

Sales overheads

Total fixed costs paid during the year

0

11,200

(1,600)

700

600

21000

(9,600)

100

9,500

11,500

(1,300)

6 | P a g e

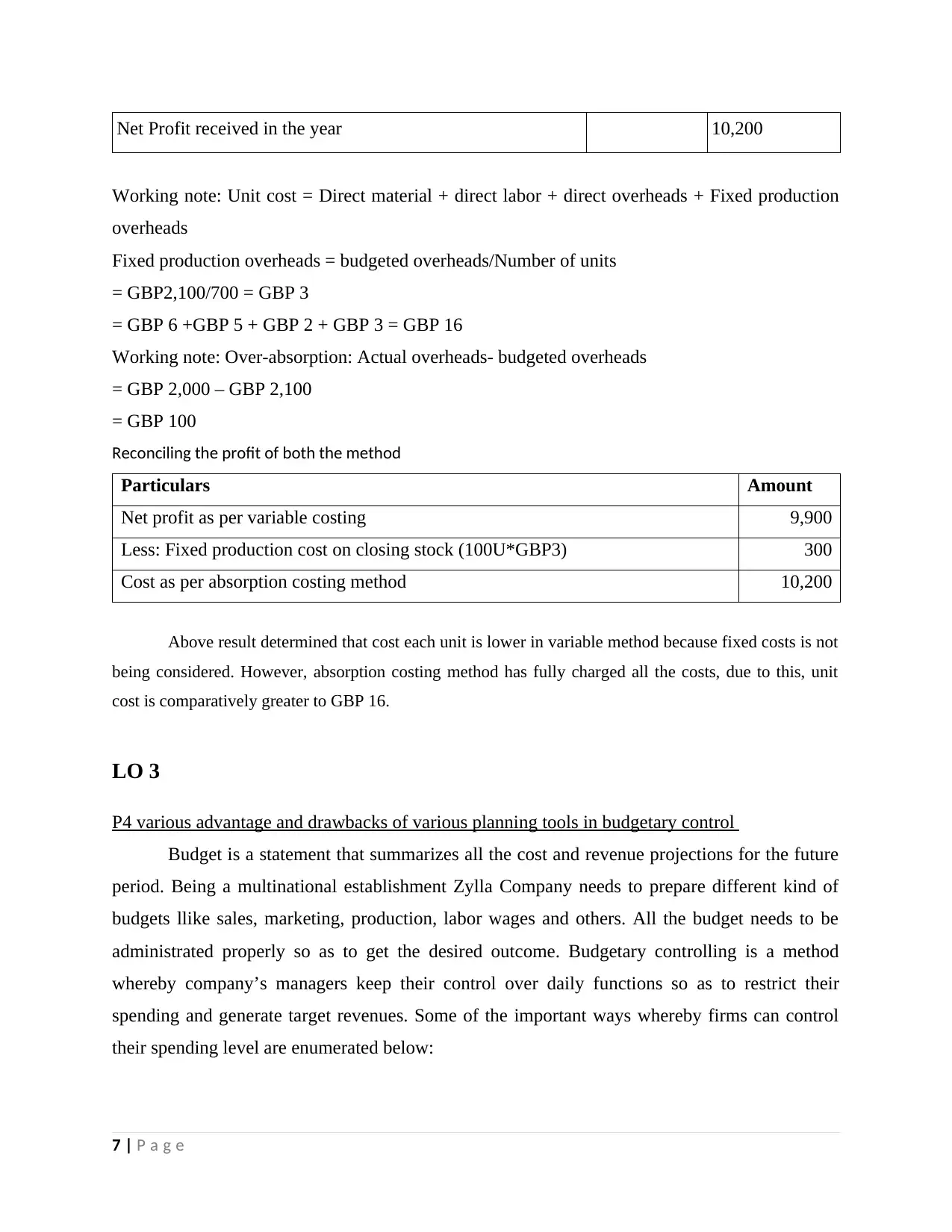

Net Profit received in the year 10,200

Working note: Unit cost = Direct material + direct labor + direct overheads + Fixed production

overheads

Fixed production overheads = budgeted overheads/Number of units

= GBP2,100/700 = GBP 3

= GBP 6 +GBP 5 + GBP 2 + GBP 3 = GBP 16

Working note: Over-absorption: Actual overheads- budgeted overheads

= GBP 2,000 – GBP 2,100

= GBP 100

Reconciling the profit of both the method

Particulars Amount

Net profit as per variable costing 9,900

Less: Fixed production cost on closing stock (100U*GBP3) 300

Cost as per absorption costing method 10,200

Above result determined that cost each unit is lower in variable method because fixed costs is not

being considered. However, absorption costing method has fully charged all the costs, due to this, unit

cost is comparatively greater to GBP 16.

LO 3

P4 various advantage and drawbacks of various planning tools in budgetary control

Budget is a statement that summarizes all the cost and revenue projections for the future

period. Being a multinational establishment Zylla Company needs to prepare different kind of

budgets llike sales, marketing, production, labor wages and others. All the budget needs to be

administrated properly so as to get the desired outcome. Budgetary controlling is a method

whereby company’s managers keep their control over daily functions so as to restrict their

spending and generate target revenues. Some of the important ways whereby firms can control

their spending level are enumerated below:

7 | P a g e

Working note: Unit cost = Direct material + direct labor + direct overheads + Fixed production

overheads

Fixed production overheads = budgeted overheads/Number of units

= GBP2,100/700 = GBP 3

= GBP 6 +GBP 5 + GBP 2 + GBP 3 = GBP 16

Working note: Over-absorption: Actual overheads- budgeted overheads

= GBP 2,000 – GBP 2,100

= GBP 100

Reconciling the profit of both the method

Particulars Amount

Net profit as per variable costing 9,900

Less: Fixed production cost on closing stock (100U*GBP3) 300

Cost as per absorption costing method 10,200

Above result determined that cost each unit is lower in variable method because fixed costs is not

being considered. However, absorption costing method has fully charged all the costs, due to this, unit

cost is comparatively greater to GBP 16.

LO 3

P4 various advantage and drawbacks of various planning tools in budgetary control

Budget is a statement that summarizes all the cost and revenue projections for the future

period. Being a multinational establishment Zylla Company needs to prepare different kind of

budgets llike sales, marketing, production, labor wages and others. All the budget needs to be

administrated properly so as to get the desired outcome. Budgetary controlling is a method

whereby company’s managers keep their control over daily functions so as to restrict their

spending and generate target revenues. Some of the important ways whereby firms can control

their spending level are enumerated below:

7 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Standard costing & Variance analysis: In this method of budgetary control, initially,

before running the actual operations, Zylla Company’s mangers forecasts and anticipate possible

future occurrence that will either result in income generation and outgoings to pay material, staff

wages, overhead and others. Thereafter, when period for which budget is prepared completed,

then actual results are matched and compared with forecasts to know deviations (Brooks, 2015)).

For instance, actual purchase price of material may be higher due to limited supply with high

demand, labor rate variance may be negative due to high wages demanded by competent

workforce and others. Through such analysis, Zylla’s departments can explore the reasons

behind unfavourable results that brought financial trouble. This in turn, corrective measures are

undertaken by the managerial team to reduce such occurrence.

Advantages:

In current times, activity based budgeting can be used for setting standards and helps in

accurate prediction.

Comparative analysis of actual and standard helps in finding deviation along with its

causes and impact, thus, managers can design suitable plans accordingly to restrict it. For

instance, adverse price variance can be reduce through finding supplier overseas to get it

at cheaper rate, bargain with existing suppliers etc, overheads can be controlled through

tighten monitoring practices and others (Schipper, Francis and Weil, 2017).

Various budgets are prepared and communicated to all the divisions of Zylla Company

and in order to perform best, everyone put hard work and dedication resultant higher

productivity.

Disadvantages:

The main downfall side associated with the method is actual outcome is compared at the

end and its analysis takes time. Thus, the process of actual corrective decision and its

sound implementation may delay (Mauro and Cinquini 2016).

In case, if budget is prepared through traditional methods like incremental and others,

then it is not found appropriate because targets are not challenging and competition.

It does not help entities in motivating their employees, because, managers are concerned

about adverse results and does not pay attention to the areas where targets have

successful reached.

8 | P a g e

before running the actual operations, Zylla Company’s mangers forecasts and anticipate possible

future occurrence that will either result in income generation and outgoings to pay material, staff

wages, overhead and others. Thereafter, when period for which budget is prepared completed,

then actual results are matched and compared with forecasts to know deviations (Brooks, 2015)).

For instance, actual purchase price of material may be higher due to limited supply with high

demand, labor rate variance may be negative due to high wages demanded by competent

workforce and others. Through such analysis, Zylla’s departments can explore the reasons

behind unfavourable results that brought financial trouble. This in turn, corrective measures are

undertaken by the managerial team to reduce such occurrence.

Advantages:

In current times, activity based budgeting can be used for setting standards and helps in

accurate prediction.

Comparative analysis of actual and standard helps in finding deviation along with its

causes and impact, thus, managers can design suitable plans accordingly to restrict it. For

instance, adverse price variance can be reduce through finding supplier overseas to get it

at cheaper rate, bargain with existing suppliers etc, overheads can be controlled through

tighten monitoring practices and others (Schipper, Francis and Weil, 2017).

Various budgets are prepared and communicated to all the divisions of Zylla Company

and in order to perform best, everyone put hard work and dedication resultant higher

productivity.

Disadvantages:

The main downfall side associated with the method is actual outcome is compared at the

end and its analysis takes time. Thus, the process of actual corrective decision and its

sound implementation may delay (Mauro and Cinquini 2016).

In case, if budget is prepared through traditional methods like incremental and others,

then it is not found appropriate because targets are not challenging and competition.

It does not help entities in motivating their employees, because, managers are concerned

about adverse results and does not pay attention to the areas where targets have

successful reached.

8 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Responsibility budgeting: This method assigns responsibility to different centres who are

allocated with different duties and accountability for varied aspects. The method is so useful to

reduce or minimize such cost elements that are controllable for enterprise. The key centres to

whom responsibility is allocated are as follows:

Cost centres: This centre holds a single authority as well as accountability to control all the

cost incurring elements like material, supplies, manufacturing overheads, staff wages, admin

overheads, research and develop and others (Parmenter, 2015). Such centre head must follow

proper precautions to not exceed their actual spending beyond the target set by Zylla Company’s

executives and top-level policy formulators.

Revenue centre: The key responsibility of revenue centre is to ensure that company generates

expected revenues or more. Although, such centre have no authority to control any kind of costs,

still, it has certain control over Zylla Company’s marketing division. They continuously matches

their revenues with the forecasts to know that what decisions they must undertook to maximize

their revenues such as increase in selling price, using new channels of marketing like social

media, website marketing and others, open more branch, expand its presence and others ((Lynch

and Lynch, 2017).

Profit centre: This particular centre keep focus on both the costs and revenue elements

because higher the costs reduce profit whereas high income resultant greater yield. Thus, the

centre focuses on maximizing their total profit through tight control on the spending level and

assuring generating target revenues.

Advantages:

It helps Zylla Company in minimizing their excessive costs through better control, cost-

cutting plans, elimination of unproductive activities and many others that improve saving.

This budgetary controlling method assists in key decisions like setting a correct selling

price, cost-cutting measurement, set an appropriate mark-up by balancing their own profit

desires and consumer willingness to pay.

It also may assist firm in work specification through hiring people in different centres as

per their excellency and proficiency.

Disadvantages:

The method just pay attention to the costs which are under control of the organization.

9 | P a g e

allocated with different duties and accountability for varied aspects. The method is so useful to

reduce or minimize such cost elements that are controllable for enterprise. The key centres to

whom responsibility is allocated are as follows:

Cost centres: This centre holds a single authority as well as accountability to control all the

cost incurring elements like material, supplies, manufacturing overheads, staff wages, admin

overheads, research and develop and others (Parmenter, 2015). Such centre head must follow

proper precautions to not exceed their actual spending beyond the target set by Zylla Company’s

executives and top-level policy formulators.

Revenue centre: The key responsibility of revenue centre is to ensure that company generates

expected revenues or more. Although, such centre have no authority to control any kind of costs,

still, it has certain control over Zylla Company’s marketing division. They continuously matches

their revenues with the forecasts to know that what decisions they must undertook to maximize

their revenues such as increase in selling price, using new channels of marketing like social

media, website marketing and others, open more branch, expand its presence and others ((Lynch

and Lynch, 2017).

Profit centre: This particular centre keep focus on both the costs and revenue elements

because higher the costs reduce profit whereas high income resultant greater yield. Thus, the

centre focuses on maximizing their total profit through tight control on the spending level and

assuring generating target revenues.

Advantages:

It helps Zylla Company in minimizing their excessive costs through better control, cost-

cutting plans, elimination of unproductive activities and many others that improve saving.

This budgetary controlling method assists in key decisions like setting a correct selling

price, cost-cutting measurement, set an appropriate mark-up by balancing their own profit

desires and consumer willingness to pay.

It also may assist firm in work specification through hiring people in different centres as

per their excellency and proficiency.

Disadvantages:

The method just pay attention to the costs which are under control of the organization.

9 | P a g e

Its sound and successful implement is based on internal business organizational structure,

a structured system to delegate responsibility, an appropriate method of reporting and

others

LO 4

P5 Use of management accounting systems to respond financial difficulties

Key performance indicators: It is a performance measurement tool that assess firm

success on a particular project, process or activity. Choosing a right KPI is a key decision for the

organization that depends upon the type of operation, targets and key activities. For instance,

Zylla Company can use defect rates, consumer satisfaction score, turnover by segments, product

quality, rejection rate, cycle time ratio, average delivery time and others as their important KPIs

to know their progress (Parmenter, 2015). Growth in favourable aspects such as quality, user

satisfaction, profitability, turnover and decrease waiting time, rejection rate and others indicates

strong performance. It aware Zylla Company’s team to detect that in which of the key areas,

company yet need to improve itself and attain financial success. It is a better way over ratio

analysis because it only analyse accounting information, however, KPIs uses both financial and

non-financial information i.e. rejection rate, employee productivity, consumer satisfaction and

others and thereby assist entity in resolving such issues.

Benchmarking: In traditional times, managers prefer ratio analysis to measure, evaluate

and analyse their financial results. Moreover, current year’s ratios are compared against previous

year to assess that whether business had improved their financial position or not. Although, the

method is still used in current corporate world, still, it does not take into account competitors

actions. Therefore, benchmarking is found much better wherein external analysis is undertaken

through matching Zylla Company’s performance with the industry’s best player. It is a method

wherein an entity’s own processes is compared with the standard taking into account industry’s

best performer. Thus, it begins with identifying the best market player with similar processes and

thereafter, results are studied against own performance (Bligaard and et.al., 2016). It helps to

know that how well Zylla Company attained goals and inform managers that why benchmarked

company is more successful. It is use to assess performance taking into account specific

indicators like cycle time, count of flaws, productivity, cost per unit and others and thereby allow

10 | P a g e

a structured system to delegate responsibility, an appropriate method of reporting and

others

LO 4

P5 Use of management accounting systems to respond financial difficulties

Key performance indicators: It is a performance measurement tool that assess firm

success on a particular project, process or activity. Choosing a right KPI is a key decision for the

organization that depends upon the type of operation, targets and key activities. For instance,

Zylla Company can use defect rates, consumer satisfaction score, turnover by segments, product

quality, rejection rate, cycle time ratio, average delivery time and others as their important KPIs

to know their progress (Parmenter, 2015). Growth in favourable aspects such as quality, user

satisfaction, profitability, turnover and decrease waiting time, rejection rate and others indicates

strong performance. It aware Zylla Company’s team to detect that in which of the key areas,

company yet need to improve itself and attain financial success. It is a better way over ratio

analysis because it only analyse accounting information, however, KPIs uses both financial and

non-financial information i.e. rejection rate, employee productivity, consumer satisfaction and

others and thereby assist entity in resolving such issues.

Benchmarking: In traditional times, managers prefer ratio analysis to measure, evaluate

and analyse their financial results. Moreover, current year’s ratios are compared against previous

year to assess that whether business had improved their financial position or not. Although, the

method is still used in current corporate world, still, it does not take into account competitors

actions. Therefore, benchmarking is found much better wherein external analysis is undertaken

through matching Zylla Company’s performance with the industry’s best player. It is a method

wherein an entity’s own processes is compared with the standard taking into account industry’s

best performer. Thus, it begins with identifying the best market player with similar processes and

thereafter, results are studied against own performance (Bligaard and et.al., 2016). It helps to

know that how well Zylla Company attained goals and inform managers that why benchmarked

company is more successful. It is use to assess performance taking into account specific

indicators like cycle time, count of flaws, productivity, cost per unit and others and thereby allow

10 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.