University Management Accounting Homework Assignment Solution

VerifiedAdded on 2022/12/27

|10

|1395

|36

Homework Assignment

AI Summary

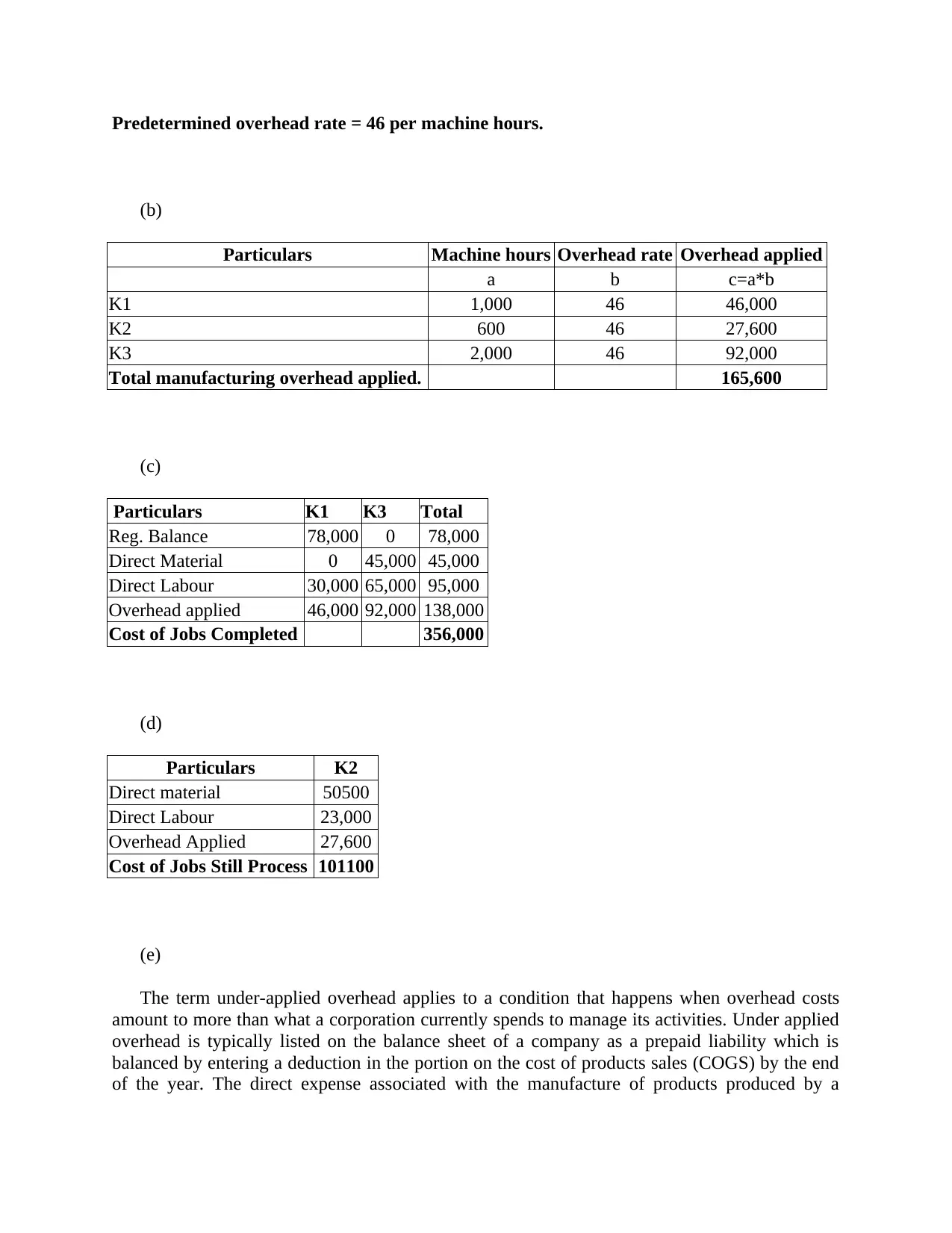

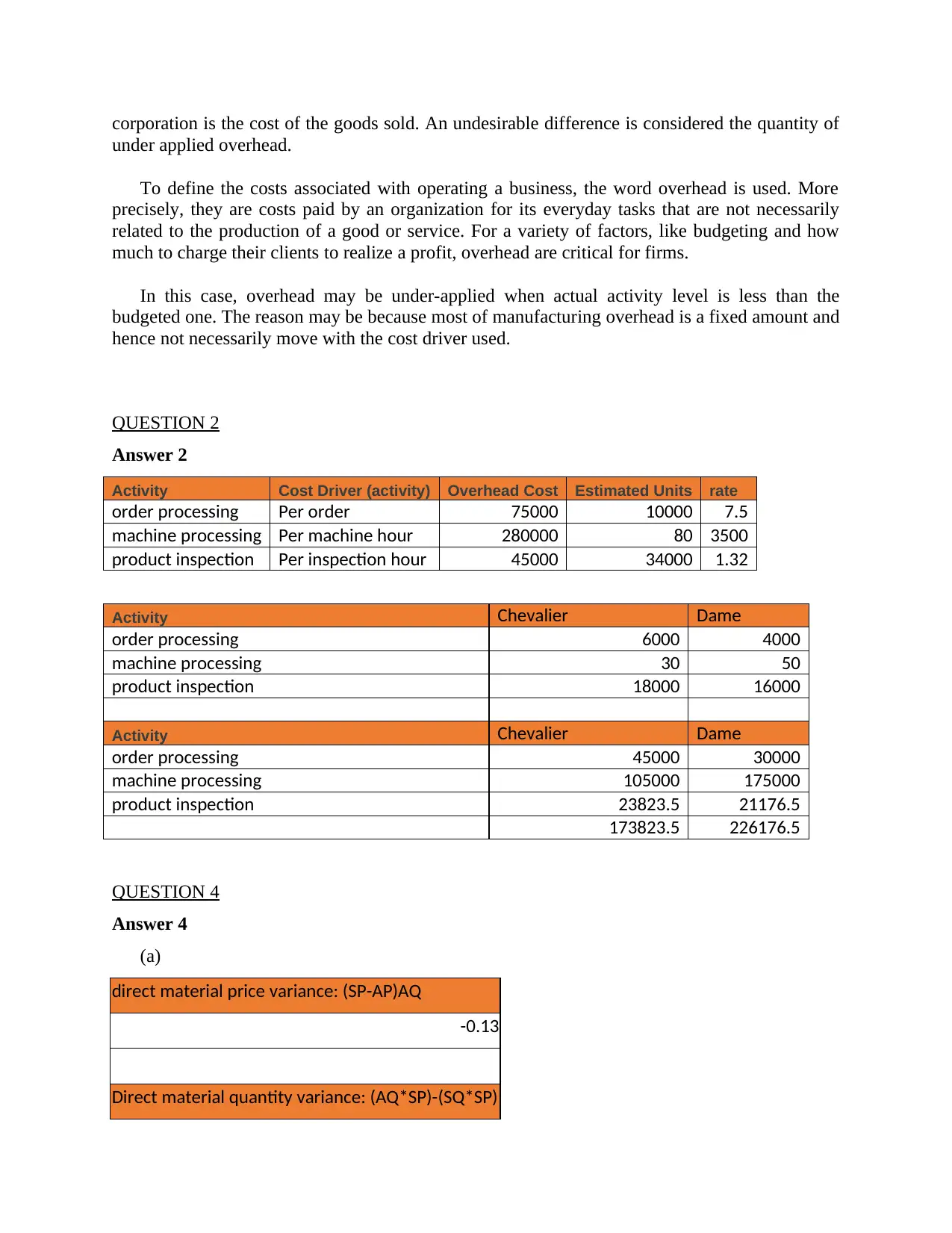

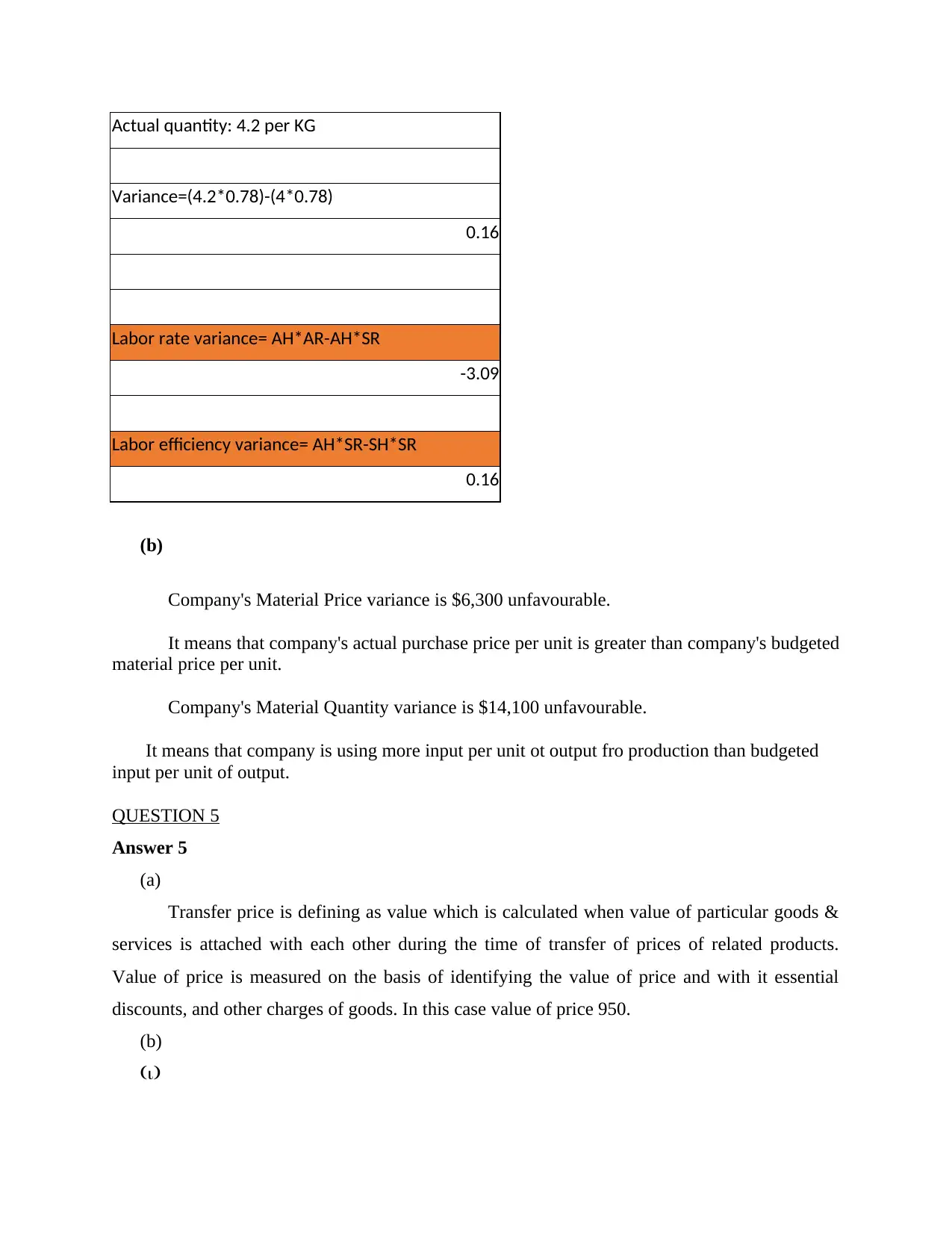

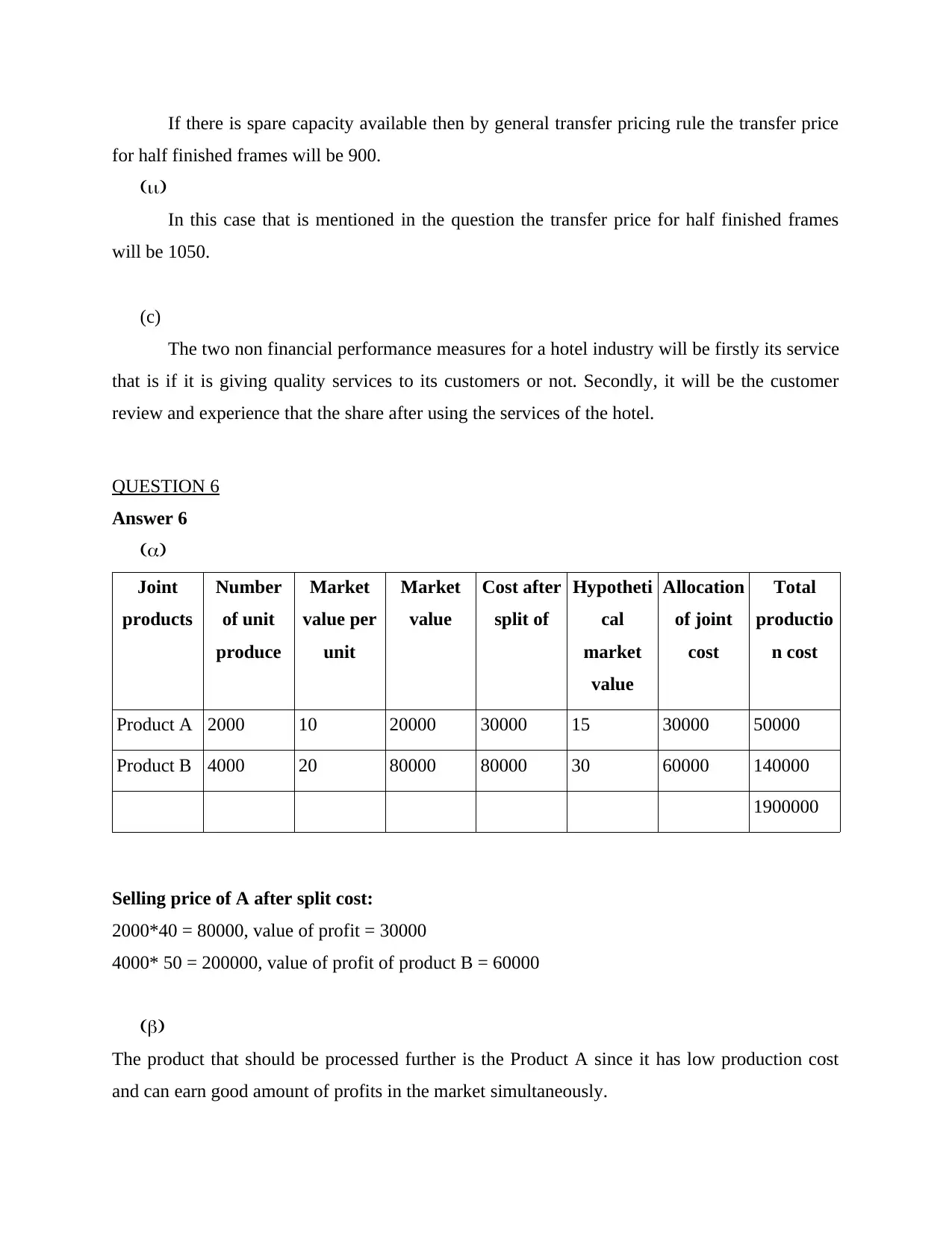

This document presents a comprehensive solution to a management accounting assignment, addressing key concepts such as variable and fixed costs, overhead allocation, variance analysis, and transfer pricing. The solution includes detailed calculations and explanations for each question, covering topics like cost behavior analysis, predetermined overhead rates, job costing, material and labor variance analysis, and the determination of transfer prices. The assignment also delves into joint product costing and the decision-making process regarding further processing. References to relevant literature further enhance the understanding of management accounting principles. The solution is designed to aid students in grasping the practical application of management accounting techniques.

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.