Management Accounts for Costs and Control

Added on 2023-06-12

18 Pages2151 Words67 Views

Management Accounts for Costs and Control

Student Name

[Pick the date]

Student Name

[Pick the date]

Question 1

a) The various differences between management accounting and financial accounting are

reflected in the tabular format shown as follows (Drury, 2016).

Management Accounting Financial Accounting

1) The management accounting is

carried out with the underlying

objective of providing information to

management so as to assist them in

decision making .

1) In contrast, financial accounting is carried

out with the underlying objective of

capturing the financial transactions which in

turn would highlight the financial

performance and position of the company.

2) The targeted audience for

management accounting are the internal

stakeholders particularly the

management that needs to take

decisions and hence requires crucial

business inputs provided in the form of

management reports

2) These are essentially directed at the

external stakeholders so that periodic

information could be provided to the external

stakeholders about the company's

performance which aims at satisfying their

informational needs for decision making

about relationship with company.

3) There is high degree of flexibility in

terms of formatting since the report

format is based on the needs of the

management or other internal

stakeholders. Hence, there is no fixed

format which needs to be necessarily

adhered to.

3) The degree of flexibility tends to be quite

limited since these are accounting standards

and other guidelines that need to be adhered

so that the external users can interpret the

financial reports and also draw comparison

with peers and past performance. Hence,

standardised reports are desirable.

4) The frequency in case of

management accounting tends to exhibit

a high degree of flexibility since these

reports are provided as and when

required by management.

4) In sharp contrast, the frequency of

financial reports is fixed with quarterly being

the most common and certain other reports

released on an annual basis. Thus, the

financial reports are not released on ad-hoc

basis.

5) The concern of reports produced

under management accounting are

based on the present and forecasting of

possible future scenarios based on

underlying decision made in present.

5) On the contrary, financial accounting

reports are essentially aimed at captured

aspects about the past performance and are

not directed at the future.

b) The various functions of management accounting are highlighted and briefly explained as

shown below.

1

a) The various differences between management accounting and financial accounting are

reflected in the tabular format shown as follows (Drury, 2016).

Management Accounting Financial Accounting

1) The management accounting is

carried out with the underlying

objective of providing information to

management so as to assist them in

decision making .

1) In contrast, financial accounting is carried

out with the underlying objective of

capturing the financial transactions which in

turn would highlight the financial

performance and position of the company.

2) The targeted audience for

management accounting are the internal

stakeholders particularly the

management that needs to take

decisions and hence requires crucial

business inputs provided in the form of

management reports

2) These are essentially directed at the

external stakeholders so that periodic

information could be provided to the external

stakeholders about the company's

performance which aims at satisfying their

informational needs for decision making

about relationship with company.

3) There is high degree of flexibility in

terms of formatting since the report

format is based on the needs of the

management or other internal

stakeholders. Hence, there is no fixed

format which needs to be necessarily

adhered to.

3) The degree of flexibility tends to be quite

limited since these are accounting standards

and other guidelines that need to be adhered

so that the external users can interpret the

financial reports and also draw comparison

with peers and past performance. Hence,

standardised reports are desirable.

4) The frequency in case of

management accounting tends to exhibit

a high degree of flexibility since these

reports are provided as and when

required by management.

4) In sharp contrast, the frequency of

financial reports is fixed with quarterly being

the most common and certain other reports

released on an annual basis. Thus, the

financial reports are not released on ad-hoc

basis.

5) The concern of reports produced

under management accounting are

based on the present and forecasting of

possible future scenarios based on

underlying decision made in present.

5) On the contrary, financial accounting

reports are essentially aimed at captured

aspects about the past performance and are

not directed at the future.

b) The various functions of management accounting are highlighted and briefly explained as

shown below.

1

Planning – Organisational planning needs to be carried out for the short term and long term

which would focus on procurement of resources in a time bound manner and usage of the

same to generate value for the shareholders. Management accounting is an enabler in this

regards as it helps the managers and decision makers to plan for the future considering the

likely scenarios to emerge based on different scenarios. Also, management accounting would

help the company in making strategic decision related to product pricing, production which in

turn can enable future forecasting of the performance in the form of budgets (Emmauel &

Otley, 2015).

Organising – It is imperative that the available resources must be used in an organised manner

so that the underlying business objectives may be achieved. This requires the organisation to

have a defined structure where the various personnel should be aware of their underlying

responsibilities and also there should be a defined line of authority. Management accounting

plays a pivotal role in this regards as it provides a communication medium between the upper

and lower level of management. Various strategic decisions regarding operational aspects of

the company are taken at the top and then communicated to product managers or line

managers so that the operations can be suitably organised to achieve the objectives

(Northington, 2015).

Controlling – This is an essential activity which is directed at ensuring that the performance of

the company does not deviate from the planned performance levels. This is essentially

achieved through the feedback mechanism which allows for remedial measures to be taken in

a timely manner. The control and performance reports that are regularly generated tend to

highlight the variances in the performance and thereby allow for any corrective measure to be

taken on time so as to control these variances (Damodaran, 2015).

Decision making – One of the key roles of the management is to make strategic decisions for

the company taking into perspective the future business environment. However, considering

the host of parameters that the company’s performance is dependent on and the underlying

risks, management reports are necessary for decision making. This could be in the form of any

strategic investment or capital outlay that the company may be planning. In order to decide

whether to proceed with it or not, a host of information about the likely future scenarios based

on the key decisions variables is required coupled with application of acceptable decision

making tools and techniques. The management reports tends to provide such analysis which

enables prudent decision making by management (Heisinger, 2014).

c) Panopticism refers to the surveillance required to instil discipline and avoid any wrongdoing.

Management accounting plays a crucial role in ensuring control, discipline and minimising

the incidence of corruption. This is because it deals with internal report generation which is

primarily based on technology. Such internal reports tend to work as excellent surveillance

mechanism and can assist in internal financial audits of the company. The management

2

which would focus on procurement of resources in a time bound manner and usage of the

same to generate value for the shareholders. Management accounting is an enabler in this

regards as it helps the managers and decision makers to plan for the future considering the

likely scenarios to emerge based on different scenarios. Also, management accounting would

help the company in making strategic decision related to product pricing, production which in

turn can enable future forecasting of the performance in the form of budgets (Emmauel &

Otley, 2015).

Organising – It is imperative that the available resources must be used in an organised manner

so that the underlying business objectives may be achieved. This requires the organisation to

have a defined structure where the various personnel should be aware of their underlying

responsibilities and also there should be a defined line of authority. Management accounting

plays a pivotal role in this regards as it provides a communication medium between the upper

and lower level of management. Various strategic decisions regarding operational aspects of

the company are taken at the top and then communicated to product managers or line

managers so that the operations can be suitably organised to achieve the objectives

(Northington, 2015).

Controlling – This is an essential activity which is directed at ensuring that the performance of

the company does not deviate from the planned performance levels. This is essentially

achieved through the feedback mechanism which allows for remedial measures to be taken in

a timely manner. The control and performance reports that are regularly generated tend to

highlight the variances in the performance and thereby allow for any corrective measure to be

taken on time so as to control these variances (Damodaran, 2015).

Decision making – One of the key roles of the management is to make strategic decisions for

the company taking into perspective the future business environment. However, considering

the host of parameters that the company’s performance is dependent on and the underlying

risks, management reports are necessary for decision making. This could be in the form of any

strategic investment or capital outlay that the company may be planning. In order to decide

whether to proceed with it or not, a host of information about the likely future scenarios based

on the key decisions variables is required coupled with application of acceptable decision

making tools and techniques. The management reports tends to provide such analysis which

enables prudent decision making by management (Heisinger, 2014).

c) Panopticism refers to the surveillance required to instil discipline and avoid any wrongdoing.

Management accounting plays a crucial role in ensuring control, discipline and minimising

the incidence of corruption. This is because it deals with internal report generation which is

primarily based on technology. Such internal reports tend to work as excellent surveillance

mechanism and can assist in internal financial audits of the company. The management

2

reports are regularly provided to the internal audit committee which takes requisite measures

in order to bring down the audit risk and thereby avoid the risk of financial corruption and

potential misstatement (Emmauel & Otley, 2015).

Further, as highlighted in the previous question, management accounting through performance

and control reports tends to highlight the variances in actual and budgeted performance and

thereby enable in controlling the firm’s performance. Simultaneously, it also ensures that

discipline particularly in the form of cost discipline is practiced by taking corrective measures to

minimise variances which are often responsible for lacking discipline in the firm (Brealey, Myers

& Allen, 2014).

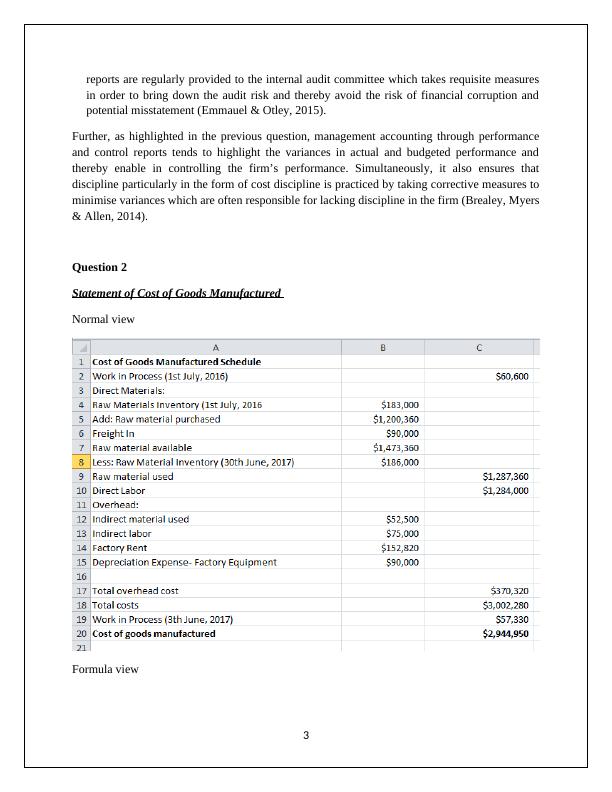

Question 2

Statement of Cost of Goods Manufactured

Normal view

Formula view

3

in order to bring down the audit risk and thereby avoid the risk of financial corruption and

potential misstatement (Emmauel & Otley, 2015).

Further, as highlighted in the previous question, management accounting through performance

and control reports tends to highlight the variances in actual and budgeted performance and

thereby enable in controlling the firm’s performance. Simultaneously, it also ensures that

discipline particularly in the form of cost discipline is practiced by taking corrective measures to

minimise variances which are often responsible for lacking discipline in the firm (Brealey, Myers

& Allen, 2014).

Question 2

Statement of Cost of Goods Manufactured

Normal view

Formula view

3

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Management Accounting: Theoretical Underpinnings, Role of Accountant, and Cost Classificationlg...

|8

|2323

|61

ACCOUNTING FOR MANAGERS.lg...

|3

|407

|240

Ratio Analysis in Finance: Understanding Financial Statements and Performancelg...

|5

|1031

|209

Role of Conceptual Framework in Accounting Standardslg...

|2

|516

|204

Comparison of Financial Accounting and Managerial Accounting, Importance of Budgetary Control Processlg...

|7

|592

|206

CORPORATE ACCOUNTING INTEGRATED REPORTING STUDENT ID: [Pick the date]lg...

|10

|2762

|353