Management Accounting Report for Nike Inc. - Costing and Budgeting

VerifiedAdded on 2022/06/08

|19

|6949

|53

Report

AI Summary

This report analyzes the management accounting practices of Nike Inc., a multinational corporation. It begins with an introduction to Nike and outlines the report's objectives. The core of the report focuses on cost analysis, defining various cost classifications such as direct materials, direct labor, manufacturing overhead, and variable versus fixed costs. It then delves into applying marginal and absorption costing techniques to prepare an income statement. The report also explores different planning tools used for budgetary control, including the use of budgets for planning, pricing strategies, and strategic planning using PEST analysis. Through these analyses, the report aims to provide insights into Nike's financial strategies and decision-making processes, concluding with a summary of the findings and a list of references.

ASSIGNMENT 02 FRONT SHEET

Qualification BTEC Level 4 HND Diploma in Business

Unit number and title Unit 5: Management Accounting

Submission date 23/12/2021 Date received (1st Submission)

Re-submission date 28/12/2021 Date received (2nd Submission)

Student Name Nguyen Thi Kim Phung Student ID GBS200568

Class No. GBS0908B Assessor Name QUYNHNTN

Student declaration

I certify that the assignment submission is entirely my own work and I fully understand the consequences of plagiarism.

I understand that making a false declaration is a form of malpractice.

Student Signature

Grading grid

P3 P4 M2 M3 D2

1

Qualification BTEC Level 4 HND Diploma in Business

Unit number and title Unit 5: Management Accounting

Submission date 23/12/2021 Date received (1st Submission)

Re-submission date 28/12/2021 Date received (2nd Submission)

Student Name Nguyen Thi Kim Phung Student ID GBS200568

Class No. GBS0908B Assessor Name QUYNHNTN

Student declaration

I certify that the assignment submission is entirely my own work and I fully understand the consequences of plagiarism.

I understand that making a false declaration is a form of malpractice.

Student Signature

Grading grid

P3 P4 M2 M3 D2

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Summative Feedbacks Resubmission Feedbacks

Grade: Assessor Signature: Date:

Internal Verifier’s Comments:

2

Grade: Assessor Signature: Date:

Internal Verifier’s Comments:

2

Signature & Date:

Table of Contents

I. Introduction....................................................................................................................3

1. Ojective and content of report..................................................................................................3

2. Short introduction for Nike, Inc.................................................................................................3

II. Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs......................................................................4

1. Definion of costs........................................................................................................................4

2. Different costs...........................................................................................................................4

3. Cost-volume profit and cost variances.......................................................................................6

4. Applying absorption and marginal costing (variable costing).....................................................7

III. Explain the advantages and disadvantages of different types of planning tools used

for budgetary control..............................................................................................................8

1. Using budgets for planning and control.....................................................................................8

2. Pricing......................................................................................................................................11

3. Strategic planning ( PEST ).......................................................................................................12

IV. Conclusion.................................................................................................................13

V. References.....................................................................................................................13

I. Introduction

1. Ojective and content of report

Nike, Inc. is a multinational corporation established in the United States that designs,

develops, manufactures, and sells clothes, footwear, accessories, equipment, and services

worldwide. I work to increase the accounting department's efficiency as a member of Nike's

board of directors. The goal of this research was to give information about Nike's varied

budgeting and costing procedures.

2. Short introduction for Nike, Inc

3

Table of Contents

I. Introduction....................................................................................................................3

1. Ojective and content of report..................................................................................................3

2. Short introduction for Nike, Inc.................................................................................................3

II. Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs......................................................................4

1. Definion of costs........................................................................................................................4

2. Different costs...........................................................................................................................4

3. Cost-volume profit and cost variances.......................................................................................6

4. Applying absorption and marginal costing (variable costing).....................................................7

III. Explain the advantages and disadvantages of different types of planning tools used

for budgetary control..............................................................................................................8

1. Using budgets for planning and control.....................................................................................8

2. Pricing......................................................................................................................................11

3. Strategic planning ( PEST ).......................................................................................................12

IV. Conclusion.................................................................................................................13

V. References.....................................................................................................................13

I. Introduction

1. Ojective and content of report

Nike, Inc. is a multinational corporation established in the United States that designs,

develops, manufactures, and sells clothes, footwear, accessories, equipment, and services

worldwide. I work to increase the accounting department's efficiency as a member of Nike's

board of directors. The goal of this research was to give information about Nike's varied

budgeting and costing procedures.

2. Short introduction for Nike, Inc

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The company's global headquarters are located near Beaverton, Oregon, in the Portland

metropolitan area (USA). It is a well-known sports equipment firm and one of the world's

leading providers of athletic shoes and equipment. It employs over 44,000 people worldwide,

and its brand was valued at $19 billion (€17,5 billion) in 2014, making it the most valuable in

the sports sector. On January 25, 1964, Bill Bowerman and Phil Knight created Blue Ribbon

Sports, which later became Nike, Inc. on May 30, 1971. Nike (N) is the Greek goddess of

victory, after whom the company was called. Nike's products are sold under the Nike Pro,

Nike+, Nike Golf, Nike Blazers, Air Jordan, Air Max, and other brands, as well as

subsidiaries like as Jordan, Hurley International, and Converse. Nike sponsors a number of

well-known athletes and sports teams around the world, and its trademarks "Just Do It" and

"Swoosh" are well-known (which represents the wing of the Greek goddess Nike).

II. Calculate costs using appropriate techniques of cost analysis to prepare an

income statement using marginal and absorption costs

1. Definion of costs

Amount of resources, effort, time, and utilities that must be spent, surrendered, or given up in

order to attain a certain goal, such as:

• Manufacturing a specific product

• Providing a specific service to a customer

All costs are expenses, but not all costs are expenses

— Expenses are the costs deducted from income in a certain accounting period.

Cost classification systems vary per business. Cost classification makes it easier for

management accountants to execute duties such as planning, regulating, organizing, and

making decisions.

2. Different costs

4

metropolitan area (USA). It is a well-known sports equipment firm and one of the world's

leading providers of athletic shoes and equipment. It employs over 44,000 people worldwide,

and its brand was valued at $19 billion (€17,5 billion) in 2014, making it the most valuable in

the sports sector. On January 25, 1964, Bill Bowerman and Phil Knight created Blue Ribbon

Sports, which later became Nike, Inc. on May 30, 1971. Nike (N) is the Greek goddess of

victory, after whom the company was called. Nike's products are sold under the Nike Pro,

Nike+, Nike Golf, Nike Blazers, Air Jordan, Air Max, and other brands, as well as

subsidiaries like as Jordan, Hurley International, and Converse. Nike sponsors a number of

well-known athletes and sports teams around the world, and its trademarks "Just Do It" and

"Swoosh" are well-known (which represents the wing of the Greek goddess Nike).

II. Calculate costs using appropriate techniques of cost analysis to prepare an

income statement using marginal and absorption costs

1. Definion of costs

Amount of resources, effort, time, and utilities that must be spent, surrendered, or given up in

order to attain a certain goal, such as:

• Manufacturing a specific product

• Providing a specific service to a customer

All costs are expenses, but not all costs are expenses

— Expenses are the costs deducted from income in a certain accounting period.

Cost classification systems vary per business. Cost classification makes it easier for

management accountants to execute duties such as planning, regulating, organizing, and

making decisions.

2. Different costs

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

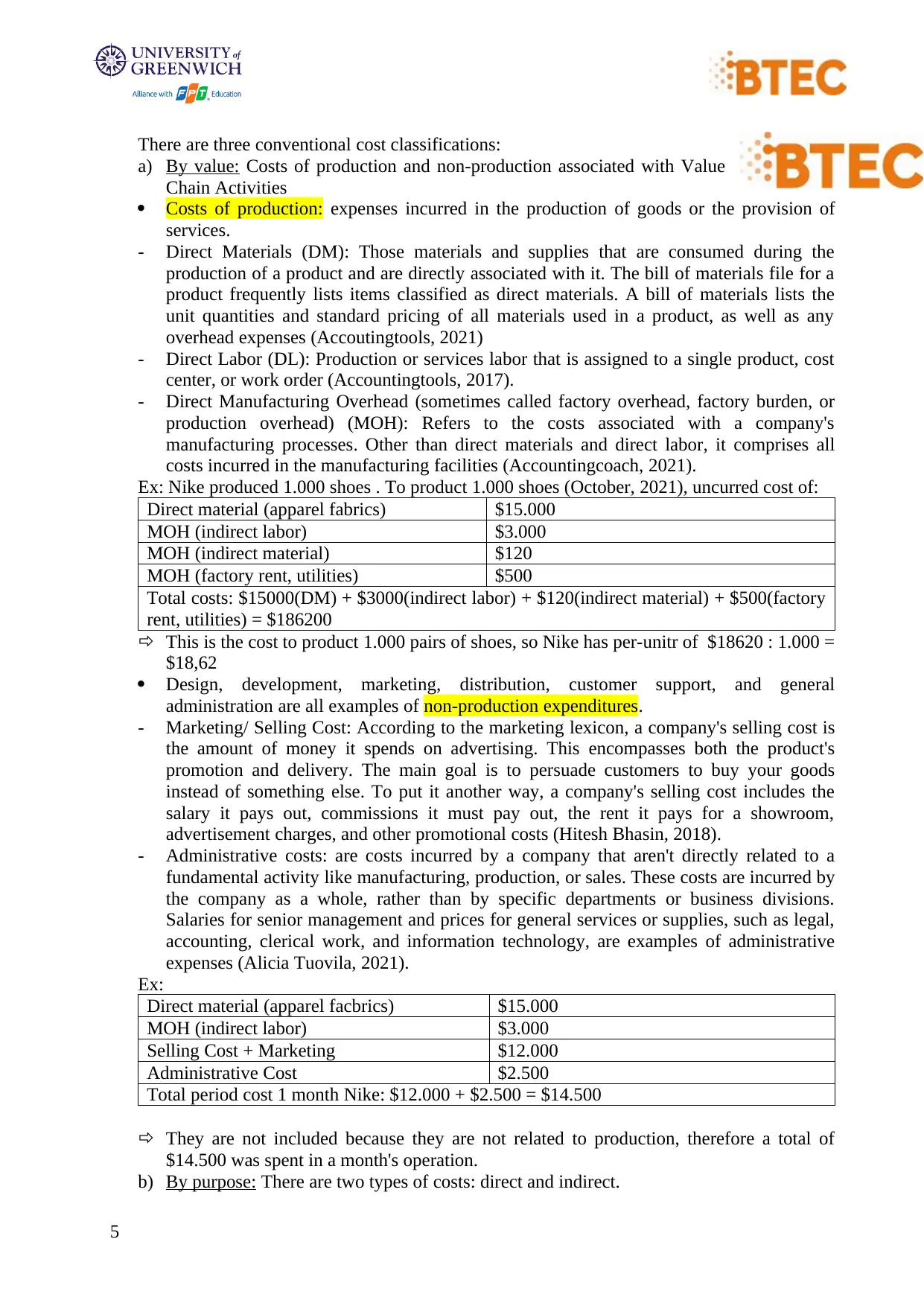

There are three conventional cost classifications:

a) By value: Costs of production and non-production associated with Value

Chain Activities

Costs of production: expenses incurred in the production of goods or the provision of

services.

- Direct Materials (DM): Those materials and supplies that are consumed during the

production of a product and are directly associated with it. The bill of materials file for a

product frequently lists items classified as direct materials. A bill of materials lists the

unit quantities and standard pricing of all materials used in a product, as well as any

overhead expenses (Accoutingtools, 2021)

- Direct Labor (DL): Production or services labor that is assigned to a single product, cost

center, or work order (Accountingtools, 2017).

- Direct Manufacturing Overhead (sometimes called factory overhead, factory burden, or

production overhead) (MOH): Refers to the costs associated with a company's

manufacturing processes. Other than direct materials and direct labor, it comprises all

costs incurred in the manufacturing facilities (Accountingcoach, 2021).

Ex: Nike produced 1.000 shoes . To product 1.000 shoes (October, 2021), uncurred cost of:

Direct material (apparel fabrics) $15.000

MOH (indirect labor) $3.000

MOH (indirect material) $120

MOH (factory rent, utilities) $500

Total costs: $15000(DM) + $3000(indirect labor) + $120(indirect material) + $500(factory

rent, utilities) = $186200

This is the cost to product 1.000 pairs of shoes, so Nike has per-unitr of $18620 : 1.000 =

$18,62

Design, development, marketing, distribution, customer support, and general

administration are all examples of non-production expenditures.

- Marketing/ Selling Cost: According to the marketing lexicon, a company's selling cost is

the amount of money it spends on advertising. This encompasses both the product's

promotion and delivery. The main goal is to persuade customers to buy your goods

instead of something else. To put it another way, a company's selling cost includes the

salary it pays out, commissions it must pay out, the rent it pays for a showroom,

advertisement charges, and other promotional costs (Hitesh Bhasin, 2018).

- Administrative costs: are costs incurred by a company that aren't directly related to a

fundamental activity like manufacturing, production, or sales. These costs are incurred by

the company as a whole, rather than by specific departments or business divisions.

Salaries for senior management and prices for general services or supplies, such as legal,

accounting, clerical work, and information technology, are examples of administrative

expenses (Alicia Tuovila, 2021).

Ex:

Direct material (apparel facbrics) $15.000

MOH (indirect labor) $3.000

Selling Cost + Marketing $12.000

Administrative Cost $2.500

Total period cost 1 month Nike: $12.000 + $2.500 = $14.500

They are not included because they are not related to production, therefore a total of

$14.500 was spent in a month's operation.

b) By purpose: There are two types of costs: direct and indirect.

5

a) By value: Costs of production and non-production associated with Value

Chain Activities

Costs of production: expenses incurred in the production of goods or the provision of

services.

- Direct Materials (DM): Those materials and supplies that are consumed during the

production of a product and are directly associated with it. The bill of materials file for a

product frequently lists items classified as direct materials. A bill of materials lists the

unit quantities and standard pricing of all materials used in a product, as well as any

overhead expenses (Accoutingtools, 2021)

- Direct Labor (DL): Production or services labor that is assigned to a single product, cost

center, or work order (Accountingtools, 2017).

- Direct Manufacturing Overhead (sometimes called factory overhead, factory burden, or

production overhead) (MOH): Refers to the costs associated with a company's

manufacturing processes. Other than direct materials and direct labor, it comprises all

costs incurred in the manufacturing facilities (Accountingcoach, 2021).

Ex: Nike produced 1.000 shoes . To product 1.000 shoes (October, 2021), uncurred cost of:

Direct material (apparel fabrics) $15.000

MOH (indirect labor) $3.000

MOH (indirect material) $120

MOH (factory rent, utilities) $500

Total costs: $15000(DM) + $3000(indirect labor) + $120(indirect material) + $500(factory

rent, utilities) = $186200

This is the cost to product 1.000 pairs of shoes, so Nike has per-unitr of $18620 : 1.000 =

$18,62

Design, development, marketing, distribution, customer support, and general

administration are all examples of non-production expenditures.

- Marketing/ Selling Cost: According to the marketing lexicon, a company's selling cost is

the amount of money it spends on advertising. This encompasses both the product's

promotion and delivery. The main goal is to persuade customers to buy your goods

instead of something else. To put it another way, a company's selling cost includes the

salary it pays out, commissions it must pay out, the rent it pays for a showroom,

advertisement charges, and other promotional costs (Hitesh Bhasin, 2018).

- Administrative costs: are costs incurred by a company that aren't directly related to a

fundamental activity like manufacturing, production, or sales. These costs are incurred by

the company as a whole, rather than by specific departments or business divisions.

Salaries for senior management and prices for general services or supplies, such as legal,

accounting, clerical work, and information technology, are examples of administrative

expenses (Alicia Tuovila, 2021).

Ex:

Direct material (apparel facbrics) $15.000

MOH (indirect labor) $3.000

Selling Cost + Marketing $12.000

Administrative Cost $2.500

Total period cost 1 month Nike: $12.000 + $2.500 = $14.500

They are not included because they are not related to production, therefore a total of

$14.500 was spent in a month's operation.

b) By purpose: There are two types of costs: direct and indirect.

5

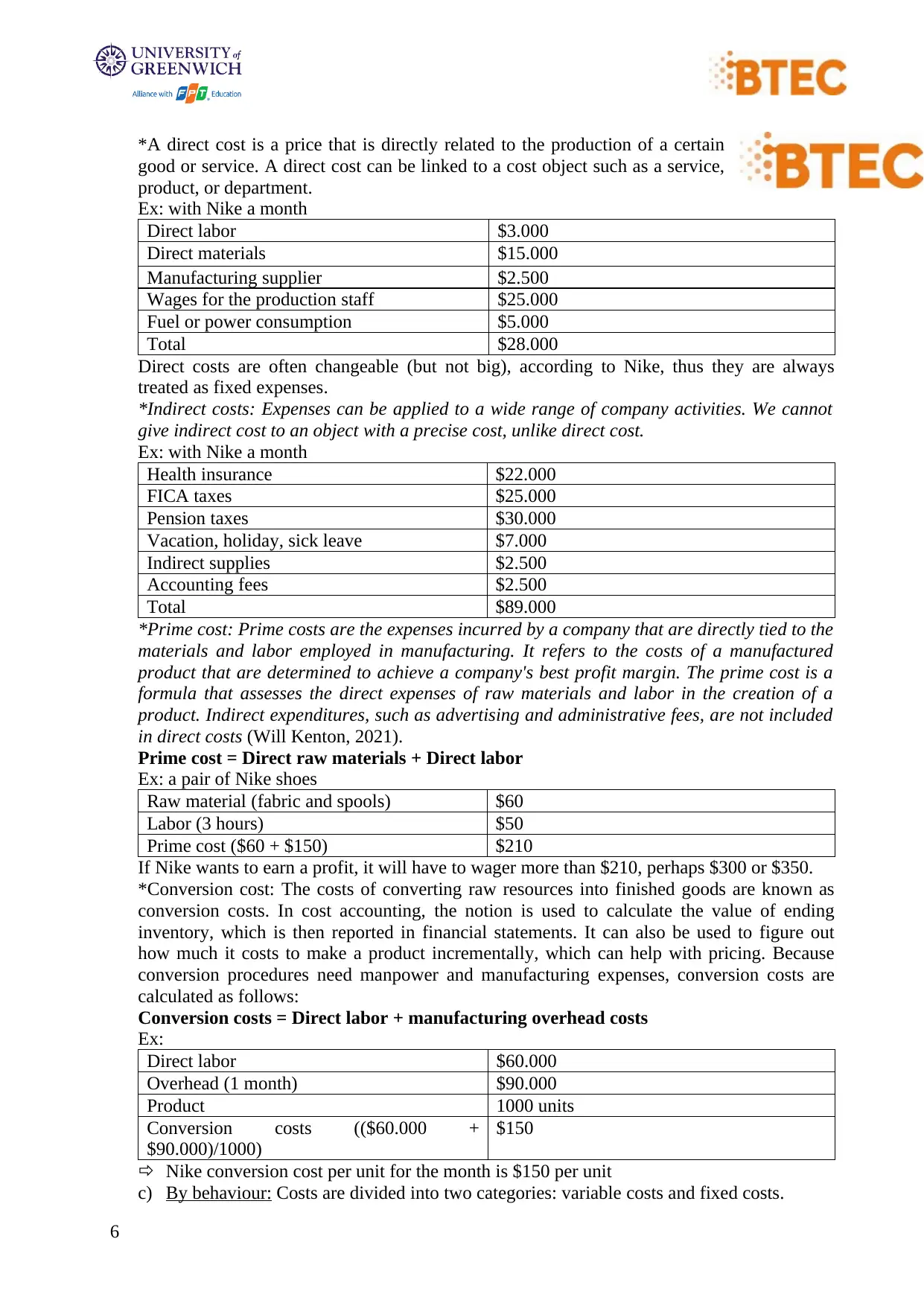

*A direct cost is a price that is directly related to the production of a certain

good or service. A direct cost can be linked to a cost object such as a service,

product, or department.

Ex: with Nike a month

Direct labor $3.000

Direct materials $15.000

Manufacturing supplier $2.500

Wages for the production staff $25.000

Fuel or power consumption $5.000

Total $28.000

Direct costs are often changeable (but not big), according to Nike, thus they are always

treated as fixed expenses.

*Indirect costs: Expenses can be applied to a wide range of company activities. We cannot

give indirect cost to an object with a precise cost, unlike direct cost.

Ex: with Nike a month

Health insurance $22.000

FICA taxes $25.000

Pension taxes $30.000

Vacation, holiday, sick leave $7.000

Indirect supplies $2.500

Accounting fees $2.500

Total $89.000

*Prime cost: Prime costs are the expenses incurred by a company that are directly tied to the

materials and labor employed in manufacturing. It refers to the costs of a manufactured

product that are determined to achieve a company's best profit margin. The prime cost is a

formula that assesses the direct expenses of raw materials and labor in the creation of a

product. Indirect expenditures, such as advertising and administrative fees, are not included

in direct costs (Will Kenton, 2021).

Prime cost = Direct raw materials + Direct labor

Ex: a pair of Nike shoes

Raw material (fabric and spools) $60

Labor (3 hours) $50

Prime cost ($60 + $150) $210

If Nike wants to earn a profit, it will have to wager more than $210, perhaps $300 or $350.

*Conversion cost: The costs of converting raw resources into finished goods are known as

conversion costs. In cost accounting, the notion is used to calculate the value of ending

inventory, which is then reported in financial statements. It can also be used to figure out

how much it costs to make a product incrementally, which can help with pricing. Because

conversion procedures need manpower and manufacturing expenses, conversion costs are

calculated as follows:

Conversion costs = Direct labor + manufacturing overhead costs

Ex:

Direct labor $60.000

Overhead (1 month) $90.000

Product 1000 units

Conversion costs (($60.000 +

$90.000)/1000)

$150

Nike conversion cost per unit for the month is $150 per unit

c) By behaviour: Costs are divided into two categories: variable costs and fixed costs.

6

good or service. A direct cost can be linked to a cost object such as a service,

product, or department.

Ex: with Nike a month

Direct labor $3.000

Direct materials $15.000

Manufacturing supplier $2.500

Wages for the production staff $25.000

Fuel or power consumption $5.000

Total $28.000

Direct costs are often changeable (but not big), according to Nike, thus they are always

treated as fixed expenses.

*Indirect costs: Expenses can be applied to a wide range of company activities. We cannot

give indirect cost to an object with a precise cost, unlike direct cost.

Ex: with Nike a month

Health insurance $22.000

FICA taxes $25.000

Pension taxes $30.000

Vacation, holiday, sick leave $7.000

Indirect supplies $2.500

Accounting fees $2.500

Total $89.000

*Prime cost: Prime costs are the expenses incurred by a company that are directly tied to the

materials and labor employed in manufacturing. It refers to the costs of a manufactured

product that are determined to achieve a company's best profit margin. The prime cost is a

formula that assesses the direct expenses of raw materials and labor in the creation of a

product. Indirect expenditures, such as advertising and administrative fees, are not included

in direct costs (Will Kenton, 2021).

Prime cost = Direct raw materials + Direct labor

Ex: a pair of Nike shoes

Raw material (fabric and spools) $60

Labor (3 hours) $50

Prime cost ($60 + $150) $210

If Nike wants to earn a profit, it will have to wager more than $210, perhaps $300 or $350.

*Conversion cost: The costs of converting raw resources into finished goods are known as

conversion costs. In cost accounting, the notion is used to calculate the value of ending

inventory, which is then reported in financial statements. It can also be used to figure out

how much it costs to make a product incrementally, which can help with pricing. Because

conversion procedures need manpower and manufacturing expenses, conversion costs are

calculated as follows:

Conversion costs = Direct labor + manufacturing overhead costs

Ex:

Direct labor $60.000

Overhead (1 month) $90.000

Product 1000 units

Conversion costs (($60.000 +

$90.000)/1000)

$150

Nike conversion cost per unit for the month is $150 per unit

c) By behaviour: Costs are divided into two categories: variable costs and fixed costs.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

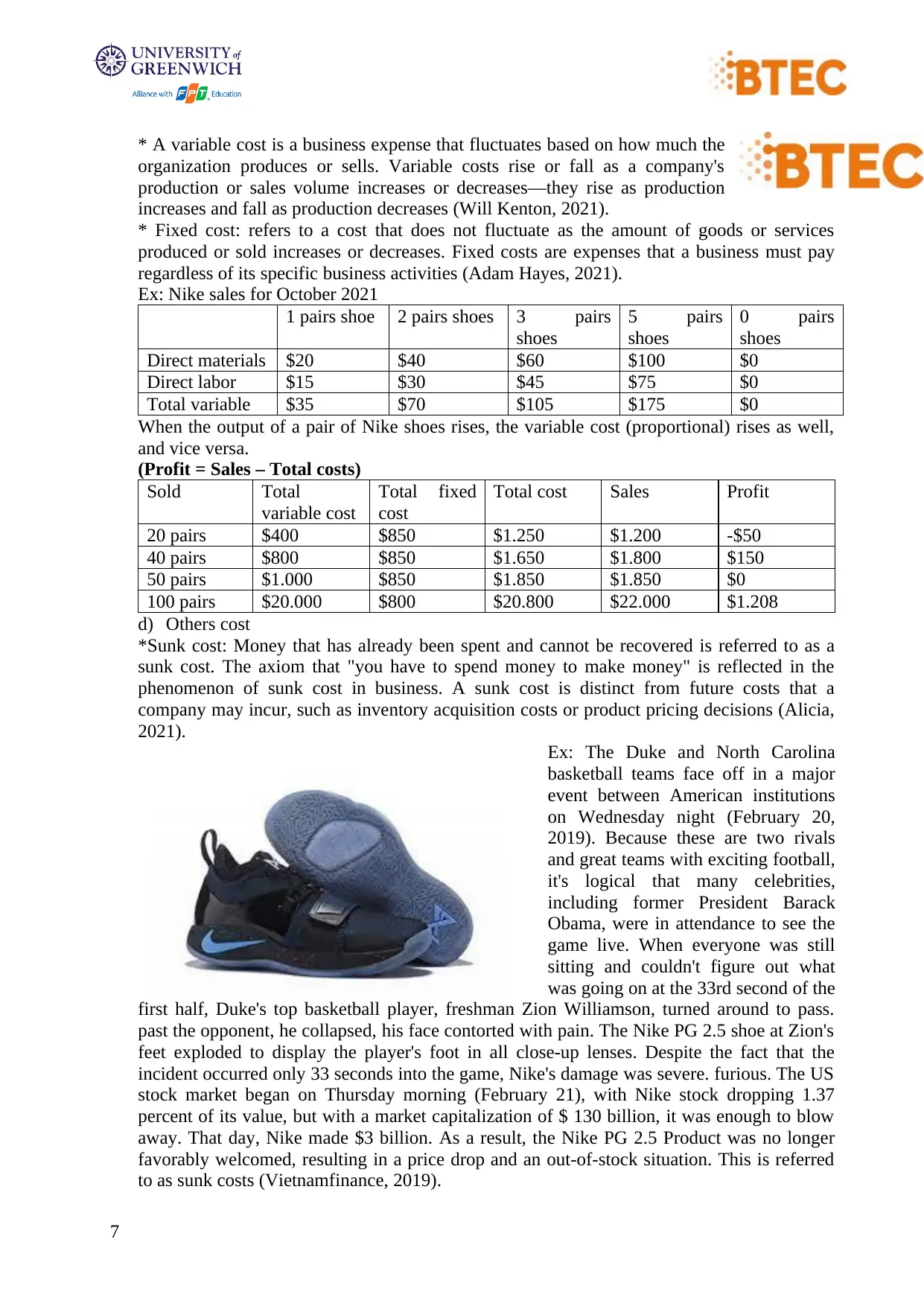

* A variable cost is a business expense that fluctuates based on how much the

organization produces or sells. Variable costs rise or fall as a company's

production or sales volume increases or decreases—they rise as production

increases and fall as production decreases (Will Kenton, 2021).

* Fixed cost: refers to a cost that does not fluctuate as the amount of goods or services

produced or sold increases or decreases. Fixed costs are expenses that a business must pay

regardless of its specific business activities (Adam Hayes, 2021).

Ex: Nike sales for October 2021

1 pairs shoe 2 pairs shoes 3 pairs

shoes

5 pairs

shoes

0 pairs

shoes

Direct materials $20 $40 $60 $100 $0

Direct labor $15 $30 $45 $75 $0

Total variable $35 $70 $105 $175 $0

When the output of a pair of Nike shoes rises, the variable cost (proportional) rises as well,

and vice versa.

(Profit = Sales – Total costs)

Sold Total

variable cost

Total fixed

cost

Total cost Sales Profit

20 pairs $400 $850 $1.250 $1.200 -$50

40 pairs $800 $850 $1.650 $1.800 $150

50 pairs $1.000 $850 $1.850 $1.850 $0

100 pairs $20.000 $800 $20.800 $22.000 $1.208

d) Others cost

*Sunk cost: Money that has already been spent and cannot be recovered is referred to as a

sunk cost. The axiom that "you have to spend money to make money" is reflected in the

phenomenon of sunk cost in business. A sunk cost is distinct from future costs that a

company may incur, such as inventory acquisition costs or product pricing decisions (Alicia,

2021).

Ex: The Duke and North Carolina

basketball teams face off in a major

event between American institutions

on Wednesday night (February 20,

2019). Because these are two rivals

and great teams with exciting football,

it's logical that many celebrities,

including former President Barack

Obama, were in attendance to see the

game live. When everyone was still

sitting and couldn't figure out what

was going on at the 33rd second of the

first half, Duke's top basketball player, freshman Zion Williamson, turned around to pass.

past the opponent, he collapsed, his face contorted with pain. The Nike PG 2.5 shoe at Zion's

feet exploded to display the player's foot in all close-up lenses. Despite the fact that the

incident occurred only 33 seconds into the game, Nike's damage was severe. furious. The US

stock market began on Thursday morning (February 21), with Nike stock dropping 1.37

percent of its value, but with a market capitalization of $ 130 billion, it was enough to blow

away. That day, Nike made $3 billion. As a result, the Nike PG 2.5 Product was no longer

favorably welcomed, resulting in a price drop and an out-of-stock situation. This is referred

to as sunk costs (Vietnamfinance, 2019).

7

organization produces or sells. Variable costs rise or fall as a company's

production or sales volume increases or decreases—they rise as production

increases and fall as production decreases (Will Kenton, 2021).

* Fixed cost: refers to a cost that does not fluctuate as the amount of goods or services

produced or sold increases or decreases. Fixed costs are expenses that a business must pay

regardless of its specific business activities (Adam Hayes, 2021).

Ex: Nike sales for October 2021

1 pairs shoe 2 pairs shoes 3 pairs

shoes

5 pairs

shoes

0 pairs

shoes

Direct materials $20 $40 $60 $100 $0

Direct labor $15 $30 $45 $75 $0

Total variable $35 $70 $105 $175 $0

When the output of a pair of Nike shoes rises, the variable cost (proportional) rises as well,

and vice versa.

(Profit = Sales – Total costs)

Sold Total

variable cost

Total fixed

cost

Total cost Sales Profit

20 pairs $400 $850 $1.250 $1.200 -$50

40 pairs $800 $850 $1.650 $1.800 $150

50 pairs $1.000 $850 $1.850 $1.850 $0

100 pairs $20.000 $800 $20.800 $22.000 $1.208

d) Others cost

*Sunk cost: Money that has already been spent and cannot be recovered is referred to as a

sunk cost. The axiom that "you have to spend money to make money" is reflected in the

phenomenon of sunk cost in business. A sunk cost is distinct from future costs that a

company may incur, such as inventory acquisition costs or product pricing decisions (Alicia,

2021).

Ex: The Duke and North Carolina

basketball teams face off in a major

event between American institutions

on Wednesday night (February 20,

2019). Because these are two rivals

and great teams with exciting football,

it's logical that many celebrities,

including former President Barack

Obama, were in attendance to see the

game live. When everyone was still

sitting and couldn't figure out what

was going on at the 33rd second of the

first half, Duke's top basketball player, freshman Zion Williamson, turned around to pass.

past the opponent, he collapsed, his face contorted with pain. The Nike PG 2.5 shoe at Zion's

feet exploded to display the player's foot in all close-up lenses. Despite the fact that the

incident occurred only 33 seconds into the game, Nike's damage was severe. furious. The US

stock market began on Thursday morning (February 21), with Nike stock dropping 1.37

percent of its value, but with a market capitalization of $ 130 billion, it was enough to blow

away. That day, Nike made $3 billion. As a result, the Nike PG 2.5 Product was no longer

favorably welcomed, resulting in a price drop and an out-of-stock situation. This is referred

to as sunk costs (Vietnamfinance, 2019).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

*Opportunity cost: The potential gains that an individual, investor, or

organization misses out on when choosing one option over another are

referred to as opportunity costs. Because opportunity costs are invisible by

definition, they are easy to overlook. Understanding the opportunities that may be missed

when a company or individual chooses one investment over another aids for more informed

decision-making (Jason Fernando, 2021).

Ex: When considering an investment, the opportunity cost must be weighed against potential

alternatives. Ten-year treasuries are currently yielding 2.16 percent, but when inflation is

factored in, the real return is likely to be closer to 1%. The S&P 500 Index is currently

trading at a Shiller P/E of x 30, implying a 3.3 percent earnings yield. As a result, Nike

appears to offer a lower rate of return for investors willing to take on more risk, and should

be avoided.

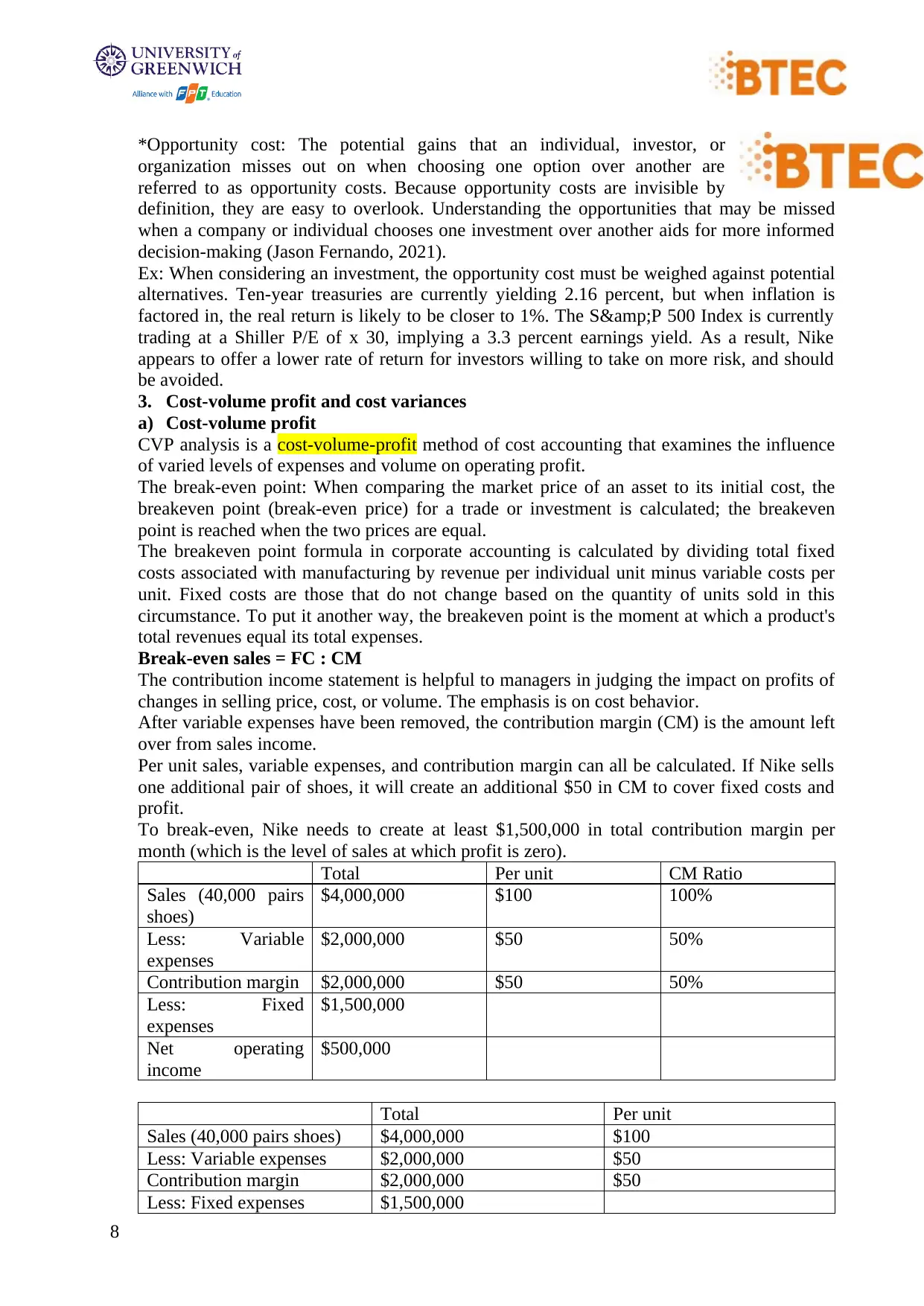

3. Cost-volume profit and cost variances

a) Cost-volume profit

CVP analysis is a cost-volume-profit method of cost accounting that examines the influence

of varied levels of expenses and volume on operating profit.

The break-even point: When comparing the market price of an asset to its initial cost, the

breakeven point (break-even price) for a trade or investment is calculated; the breakeven

point is reached when the two prices are equal.

The breakeven point formula in corporate accounting is calculated by dividing total fixed

costs associated with manufacturing by revenue per individual unit minus variable costs per

unit. Fixed costs are those that do not change based on the quantity of units sold in this

circumstance. To put it another way, the breakeven point is the moment at which a product's

total revenues equal its total expenses.

Break-even sales = FC : CM

The contribution income statement is helpful to managers in judging the impact on profits of

changes in selling price, cost, or volume. The emphasis is on cost behavior.

After variable expenses have been removed, the contribution margin (CM) is the amount left

over from sales income.

Per unit sales, variable expenses, and contribution margin can all be calculated. If Nike sells

one additional pair of shoes, it will create an additional $50 in CM to cover fixed costs and

profit.

To break-even, Nike needs to create at least $1,500,000 in total contribution margin per

month (which is the level of sales at which profit is zero).

Total Per unit CM Ratio

Sales (40,000 pairs

shoes)

$4,000,000 $100 100%

Less: Variable

expenses

$2,000,000 $50 50%

Contribution margin $2,000,000 $50 50%

Less: Fixed

expenses

$1,500,000

Net operating

income

$500,000

Total Per unit

Sales (40,000 pairs shoes) $4,000,000 $100

Less: Variable expenses $2,000,000 $50

Contribution margin $2,000,000 $50

Less: Fixed expenses $1,500,000

8

organization misses out on when choosing one option over another are

referred to as opportunity costs. Because opportunity costs are invisible by

definition, they are easy to overlook. Understanding the opportunities that may be missed

when a company or individual chooses one investment over another aids for more informed

decision-making (Jason Fernando, 2021).

Ex: When considering an investment, the opportunity cost must be weighed against potential

alternatives. Ten-year treasuries are currently yielding 2.16 percent, but when inflation is

factored in, the real return is likely to be closer to 1%. The S&P 500 Index is currently

trading at a Shiller P/E of x 30, implying a 3.3 percent earnings yield. As a result, Nike

appears to offer a lower rate of return for investors willing to take on more risk, and should

be avoided.

3. Cost-volume profit and cost variances

a) Cost-volume profit

CVP analysis is a cost-volume-profit method of cost accounting that examines the influence

of varied levels of expenses and volume on operating profit.

The break-even point: When comparing the market price of an asset to its initial cost, the

breakeven point (break-even price) for a trade or investment is calculated; the breakeven

point is reached when the two prices are equal.

The breakeven point formula in corporate accounting is calculated by dividing total fixed

costs associated with manufacturing by revenue per individual unit minus variable costs per

unit. Fixed costs are those that do not change based on the quantity of units sold in this

circumstance. To put it another way, the breakeven point is the moment at which a product's

total revenues equal its total expenses.

Break-even sales = FC : CM

The contribution income statement is helpful to managers in judging the impact on profits of

changes in selling price, cost, or volume. The emphasis is on cost behavior.

After variable expenses have been removed, the contribution margin (CM) is the amount left

over from sales income.

Per unit sales, variable expenses, and contribution margin can all be calculated. If Nike sells

one additional pair of shoes, it will create an additional $50 in CM to cover fixed costs and

profit.

To break-even, Nike needs to create at least $1,500,000 in total contribution margin per

month (which is the level of sales at which profit is zero).

Total Per unit CM Ratio

Sales (40,000 pairs

shoes)

$4,000,000 $100 100%

Less: Variable

expenses

$2,000,000 $50 50%

Contribution margin $2,000,000 $50 50%

Less: Fixed

expenses

$1,500,000

Net operating

income

$500,000

Total Per unit

Sales (40,000 pairs shoes) $4,000,000 $100

Less: Variable expenses $2,000,000 $50

Contribution margin $2,000,000 $50

Less: Fixed expenses $1,500,000

8

Net operating income $500,000

Nike will be operating at break-even if it sells 30,000 units in a month.

Total Per unit

Sales (30,000 pairs shoes) $3,000,000 $100

Less: Variable expenses $1,500,000 $50

Contribution margin $1,500,000 $50

Less: Fixed expenses $1,500,000

Net operating income $-

Net operating income will rise by $ if Nike sells one additional bike (30,100 pair shoes).

Total Per unit

Sales (30,001 pairs shoes) $3,000,100 $100

Less: Variable expenses $1,505,050 $50

Contribution margin $1,500,050 $50

Less: Fixed expenses $1,500,000

Net operating income $50

Profit = (Sales – Variable expense) -Fixed expenses = (30,001 units x $100 + 30,001 x

$50) – $1,500,000 = $3,000,150

Unit sales to break even = Fixed expenses / CM per unit = $1,500,000 / $50 = $30,000

b) Cost variances

The practice of reviewing your project's financial performance is known as cost variance.

The cost variation is the difference between the budget you set before the project started and

what you actually spent. The difference between BCWP (Budgeted Cost of Work Performed)

and ACWP (Actual Cost of Work Performed) is used to compute this (Actual Cost of Work

Performed).

Variance cost: earned value – actual cost

Cost variance % = (earned value – actual cost)/ earned value

Ex: variance cost of Nike: ($250 - $300) / $250 = -$20

-20% indicates that the project cost is less than the budget for a pair of shoes authorized

in the plan, and the Nike company may proceed with the project without concern of

exceeding the budget.

4. Applying absorption and marginal costing (variable costing)

Basis for comparion Marginal Costing Absorption Cóting

Meaning a method in which the

variable costs are treated as

product costs and the fixed

expenses are treated as

period costs.

considers both fixed and

variable expenses when

calculating product costs.

This way of costing is

critical, especially for

reporting purposes.

Financial and tax reporting

are also included in the

reporting purpose.

About Variable cost is thought to

be the cost of the product,

whereas fixed cost is

assumed to be the cost of the

period.

The cost of a product

includes both fixed and

variable costs.

9

Nike will be operating at break-even if it sells 30,000 units in a month.

Total Per unit

Sales (30,000 pairs shoes) $3,000,000 $100

Less: Variable expenses $1,500,000 $50

Contribution margin $1,500,000 $50

Less: Fixed expenses $1,500,000

Net operating income $-

Net operating income will rise by $ if Nike sells one additional bike (30,100 pair shoes).

Total Per unit

Sales (30,001 pairs shoes) $3,000,100 $100

Less: Variable expenses $1,505,050 $50

Contribution margin $1,500,050 $50

Less: Fixed expenses $1,500,000

Net operating income $50

Profit = (Sales – Variable expense) -Fixed expenses = (30,001 units x $100 + 30,001 x

$50) – $1,500,000 = $3,000,150

Unit sales to break even = Fixed expenses / CM per unit = $1,500,000 / $50 = $30,000

b) Cost variances

The practice of reviewing your project's financial performance is known as cost variance.

The cost variation is the difference between the budget you set before the project started and

what you actually spent. The difference between BCWP (Budgeted Cost of Work Performed)

and ACWP (Actual Cost of Work Performed) is used to compute this (Actual Cost of Work

Performed).

Variance cost: earned value – actual cost

Cost variance % = (earned value – actual cost)/ earned value

Ex: variance cost of Nike: ($250 - $300) / $250 = -$20

-20% indicates that the project cost is less than the budget for a pair of shoes authorized

in the plan, and the Nike company may proceed with the project without concern of

exceeding the budget.

4. Applying absorption and marginal costing (variable costing)

Basis for comparion Marginal Costing Absorption Cóting

Meaning a method in which the

variable costs are treated as

product costs and the fixed

expenses are treated as

period costs.

considers both fixed and

variable expenses when

calculating product costs.

This way of costing is

critical, especially for

reporting purposes.

Financial and tax reporting

are also included in the

reporting purpose.

About Variable cost is thought to

be the cost of the product,

whereas fixed cost is

assumed to be the cost of the

period.

The cost of a product

includes both fixed and

variable costs.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Nature of overheads Fixed and variable expenses. in absorption costing,

overheads are divided into

three categories:

manufacturing, distribution,

and selling and

administration.

Profit calculated The profit volume ratio (P/V

ratio) is a method of

calculating profit.

Because fixed costs are

factored into product costs,

profit is reduced.

Determines The cost of the next unit The cost of each unit.

Opening and Closing stocks Changes in opening/closing

stocks have no effect on the

cost per unit because the

focus is on the next unit.

Because the focus is on each

unit, changes in opening and

closing stocks have an

impact on the cost per unit.

Most important aspect Contribution per unit. Net profit per unit.

Purpose To emphasize the

importance of contributing

to product cost.

To demonstrate the accuracy

and fairness of product

costing.

Presented By laying out the overall

contribution.

For financial and tax

reporting, the most

convenient option.

Ex: Here is some information about a product made by the Nike Company:

Selling price per unit $300

Variable cost per unit $10

Fixed costs for each period $510

31/12/2020 31/3/2021 30/6/2021 30/9/2021

Produced 250 230 280 260

Sold 240 200 220 260

Heald in stock

at nil end of

period

10 30 60 0

Average production level = (250 + 230 + 280 + 260) : 4 = $255

Fixed overhead cost = $510 : $255 = $2/ units

*Absorption cost (Full costing)

31/12/2020 31/3/2021 30/6/2021 30/9/2021 Total

Opening

stock

_ 400 350 550

Cost of production

Variable cost 2550 2460 2600 2200 9810

Fixed cost 600 600 600 600 2400

Closing

stock

300 550 450 _

Cost of

goods sold

2850 3190 3450 3800 13290

Sales 4000 4300 5540 4900 18740

Gross profit 1150 1110 2090 1100 5450

10

overheads are divided into

three categories:

manufacturing, distribution,

and selling and

administration.

Profit calculated The profit volume ratio (P/V

ratio) is a method of

calculating profit.

Because fixed costs are

factored into product costs,

profit is reduced.

Determines The cost of the next unit The cost of each unit.

Opening and Closing stocks Changes in opening/closing

stocks have no effect on the

cost per unit because the

focus is on the next unit.

Because the focus is on each

unit, changes in opening and

closing stocks have an

impact on the cost per unit.

Most important aspect Contribution per unit. Net profit per unit.

Purpose To emphasize the

importance of contributing

to product cost.

To demonstrate the accuracy

and fairness of product

costing.

Presented By laying out the overall

contribution.

For financial and tax

reporting, the most

convenient option.

Ex: Here is some information about a product made by the Nike Company:

Selling price per unit $300

Variable cost per unit $10

Fixed costs for each period $510

31/12/2020 31/3/2021 30/6/2021 30/9/2021

Produced 250 230 280 260

Sold 240 200 220 260

Heald in stock

at nil end of

period

10 30 60 0

Average production level = (250 + 230 + 280 + 260) : 4 = $255

Fixed overhead cost = $510 : $255 = $2/ units

*Absorption cost (Full costing)

31/12/2020 31/3/2021 30/6/2021 30/9/2021 Total

Opening

stock

_ 400 350 550

Cost of production

Variable cost 2550 2460 2600 2200 9810

Fixed cost 600 600 600 600 2400

Closing

stock

300 550 450 _

Cost of

goods sold

2850 3190 3450 3800 13290

Sales 4000 4300 5540 4900 18740

Gross profit 1150 1110 2090 1100 5450

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

*Marginal Costing (Variable costing)

31/12/2020 31/3/2021 30/6/2021 30/9/2021 Total

Opening

stock

_ 350 500 450

Cost of production

Variable cost 2650 2300 2580 2280 9810

Fixed cost 600 600 600 600 2400

Closing

stock

250 650 400 _

Cost of

goods sold

3000 3150 3420 3720 13290

Sales 4160 4630 5390 4560 18740

Gross profit 1160 1480 1970 840 5450

*Profit comparison

31/12/2020 31/3/2021 30/6/2021 30/92021 Total

Absorption

cost

1150 1110 2090 1100 5450

Variable

costing

1160 1480 1970 840 5450

Difference -10 -370 120 270 0

III. Explain the advantages and disadvantages of different types of planning tools

used for budgetary control

1. Using budgets for planning and control

Planning – involves developing objectives and preparing various budgets to achieve those

objectives.

Control – involves the steps taken by management to increase the likelihood that the

objectives set down while planning are attained and that all parts of the organization are

working together toward that goal.

a) The sales budget

The Nike Company is putting together budgets for the quarter ending December 31.

The following are the sales projections for the next three months:

October : 30,000 units

November : 50,000 units

December : 40,000 units

The selling price is $100 per unit.

October November December Quarter

Budgeted sales

in units

30,000 50,000 40,000 120,000

Selling price

per unit

$100 $100 $100 $100

Total budgeted

sales

$300,000 $500,000 $400,000 $1,200,000

All sales are made on credit.

Nike's collecting pattern is as follows: 75% of items are collected in the month of sale, 20%

in the month after sale, and 5% are uncollectible.

The $20,000 accounts receivable sum due on November 31 will be paid in full.

11

31/12/2020 31/3/2021 30/6/2021 30/9/2021 Total

Opening

stock

_ 350 500 450

Cost of production

Variable cost 2650 2300 2580 2280 9810

Fixed cost 600 600 600 600 2400

Closing

stock

250 650 400 _

Cost of

goods sold

3000 3150 3420 3720 13290

Sales 4160 4630 5390 4560 18740

Gross profit 1160 1480 1970 840 5450

*Profit comparison

31/12/2020 31/3/2021 30/6/2021 30/92021 Total

Absorption

cost

1150 1110 2090 1100 5450

Variable

costing

1160 1480 1970 840 5450

Difference -10 -370 120 270 0

III. Explain the advantages and disadvantages of different types of planning tools

used for budgetary control

1. Using budgets for planning and control

Planning – involves developing objectives and preparing various budgets to achieve those

objectives.

Control – involves the steps taken by management to increase the likelihood that the

objectives set down while planning are attained and that all parts of the organization are

working together toward that goal.

a) The sales budget

The Nike Company is putting together budgets for the quarter ending December 31.

The following are the sales projections for the next three months:

October : 30,000 units

November : 50,000 units

December : 40,000 units

The selling price is $100 per unit.

October November December Quarter

Budgeted sales

in units

30,000 50,000 40,000 120,000

Selling price

per unit

$100 $100 $100 $100

Total budgeted

sales

$300,000 $500,000 $400,000 $1,200,000

All sales are made on credit.

Nike's collecting pattern is as follows: 75% of items are collected in the month of sale, 20%

in the month after sale, and 5% are uncollectible.

The $20,000 accounts receivable sum due on November 31 will be paid in full.

11

October November December Quarter

Accounts

receivable 30/11

$20,000 $20,000

October Sales

75% x $300,000 225,000 225,000

20% x $300,000 60,000 60,000

November Sales

75% x $500,000 375,000 375,000

20% x $500,000 100,000 100,000

December Sales

75% x $400,000 300,000 300,000

Total cash

collections

$245,000 $435,000 $400,000 $1,080,000

b) The production budget

Nike Company management wants closing inventory to be equivalent to 20% of the

following month's budgeted unit sales.

On September 30, a total of 5,000 units were available.

Let's get started on the budget for the project:

October November December Quarter

Budgeted Sales 30,000 50,000 40,000 120,000

Add: Desired

ending

inventory

10,000 8,000 6,000 6,000

Total needs 40,000 58,000 46,000 126,000

Less: Beginning

inventory

5,000 10,000 8,000 5,000

Required

production

35,000 48,000 38,000 121,000

c) The direct materials budget

The Nike Company requires five pounds of material every unit of product. Materials equal to

15% of the following month's production should be on hand at the end of each month,

according to management. 20,000 pounds of material are on hand as of September 30. The

cost of the material is $0.50 per pound. Let's get started on the budget for direct materials:

October November December Quarter

Production 35,000 48,000 38,000 121,000

Materials per

unit (pounds)

5 5 5 5

Production

needs

175,000 240,000 190,000 605,000

Add: Desired

ending

inventory

36,000 28,500 12,500 12,500

Total needed 211,000 268,500 202,500 617,500

Less: Beginning

inventory

20,000 36,000 28,500 20,000

Materials to be 191,000 232,500 174,000 597,500

12

Accounts

receivable 30/11

$20,000 $20,000

October Sales

75% x $300,000 225,000 225,000

20% x $300,000 60,000 60,000

November Sales

75% x $500,000 375,000 375,000

20% x $500,000 100,000 100,000

December Sales

75% x $400,000 300,000 300,000

Total cash

collections

$245,000 $435,000 $400,000 $1,080,000

b) The production budget

Nike Company management wants closing inventory to be equivalent to 20% of the

following month's budgeted unit sales.

On September 30, a total of 5,000 units were available.

Let's get started on the budget for the project:

October November December Quarter

Budgeted Sales 30,000 50,000 40,000 120,000

Add: Desired

ending

inventory

10,000 8,000 6,000 6,000

Total needs 40,000 58,000 46,000 126,000

Less: Beginning

inventory

5,000 10,000 8,000 5,000

Required

production

35,000 48,000 38,000 121,000

c) The direct materials budget

The Nike Company requires five pounds of material every unit of product. Materials equal to

15% of the following month's production should be on hand at the end of each month,

according to management. 20,000 pounds of material are on hand as of September 30. The

cost of the material is $0.50 per pound. Let's get started on the budget for direct materials:

October November December Quarter

Production 35,000 48,000 38,000 121,000

Materials per

unit (pounds)

5 5 5 5

Production

needs

175,000 240,000 190,000 605,000

Add: Desired

ending

inventory

36,000 28,500 12,500 12,500

Total needed 211,000 268,500 202,500 617,500

Less: Beginning

inventory

20,000 36,000 28,500 20,000

Materials to be 191,000 232,500 174,000 597,500

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.