Management and Environment Accounting Report 2022

VerifiedAdded on 2022/10/17

|10

|3145

|18

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MANAGEMENT AND ENVIRONMENT ACCOUNTING

MANAGEMENT AND ENVIRONMENT ACCOUNTING

Name of the Student:

Name of the University:

Author Note

MANAGEMENT AND ENVIRONMENT ACCOUNTING

Name of the Student:

Name of the University:

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1MANAGEMENT AND ENVIRONMENT ACCOUNTING

Table of Contents

Introduction...................................................................................................................2

Part A – Critical analysis of Westpac Group................................................................2

Environment and Social impacts of Westpac Group’s operations............................2

Comparison with other firm.......................................................................................3

Key Challenges in complying with GRI.....................................................................3

Benefits of GRI Reporting Standards complained report.........................................4

Part B – Strategic Initiative of Jerry Pty Limited...........................................................5

Balanced Scorecard..................................................................................................5

Break Even Point Analysis........................................................................................6

Conclusion....................................................................................................................6

References...................................................................................................................8

Table of Contents

Introduction...................................................................................................................2

Part A – Critical analysis of Westpac Group................................................................2

Environment and Social impacts of Westpac Group’s operations............................2

Comparison with other firm.......................................................................................3

Key Challenges in complying with GRI.....................................................................3

Benefits of GRI Reporting Standards complained report.........................................4

Part B – Strategic Initiative of Jerry Pty Limited...........................................................5

Balanced Scorecard..................................................................................................5

Break Even Point Analysis........................................................................................6

Conclusion....................................................................................................................6

References...................................................................................................................8

2MANAGEMENT AND ENVIRONMENT ACCOUNTING

Introduction

This report is prepped to analyse the environment accounting as well as the

management accounting of the firms. The main focus of the report is to analyse all

the related aspect of environment accounting as well as management accounting. In

the current time environment accounting is very necessary for the firm for the future

sustainability. While, the management accounting is required for the firm to be

operative in current competitive business world. Hence, this report mainly have two

parts, the first part of the report is critical analysis in which report analyse the

external report of Westpac Group to understand the impact of the organisation

operations in environment including the Global Reporting Initiative to understand the

various aspect of the environmental aspect reporting of the firm. While, the second

part of the report is mainly focus in the strategic initiative and it is prepared to

analyse the management accounting of Jerry Pty Limited. This analyse the firm’s

management accounting system of the firm by preparing and analysing the balance

scorecard.

Part A – Critical analysis of Westpac Group

Environment and Social impacts of Westpac Group’s operations

Westpac Group is one of the Australia’s oldest banking company as this one

of the oldest banking group of Australia. Not only that, this is also one out of four

major bank of Australia. Westpac is also one among the largest bank of New

Zealand. The main business of this group includes the various banking as well as

asset management services to the consumers, institutional and business groups.

This Group was founded in the year 1817 with having name Bank of New South

Wales and changed its name in 1982 and become Westpac Banking Corporation

(Westpac, 2019). The Group played the important role in the economy of Australia in

last 200 years. In the basis of the current environment policy report of the group, the

followings are the some important environment impacts of the firm’s operations: -

The operations of firm negatively impact the environment as the firm

consumes high energy and paper. The uses of the energy and paper directly

affect the environment as energy is limited while the use of paper reduces the

numbers of trees.

Secondly, the firm emission of the green – house gases by the firm during its

operations also directly impact the environment. As we all know that the

green – house gases are very harmful for our environment as well as the

peoples (Westpac, 2019).

The investment made by the firm in the energy efficient technologies as well

as firm also tries to develop the system to recycle the materials positively

affect the environment, this not only saves the natural resources but also

save the environment from the harmful emissions.

As per the information provided by the firm in their official website, the followings

are social impact of the Westpac Group’s operations: -

The firm is investing the leader of tomorrow, the firm positively affect the

society by providing the education, training as well as opportunities to the

people which helps them to achieve their aspirations (Westpac, 2019). In

simple words, the firm positively impact the social aspect by providing

employment to the peoples.

Introduction

This report is prepped to analyse the environment accounting as well as the

management accounting of the firms. The main focus of the report is to analyse all

the related aspect of environment accounting as well as management accounting. In

the current time environment accounting is very necessary for the firm for the future

sustainability. While, the management accounting is required for the firm to be

operative in current competitive business world. Hence, this report mainly have two

parts, the first part of the report is critical analysis in which report analyse the

external report of Westpac Group to understand the impact of the organisation

operations in environment including the Global Reporting Initiative to understand the

various aspect of the environmental aspect reporting of the firm. While, the second

part of the report is mainly focus in the strategic initiative and it is prepared to

analyse the management accounting of Jerry Pty Limited. This analyse the firm’s

management accounting system of the firm by preparing and analysing the balance

scorecard.

Part A – Critical analysis of Westpac Group

Environment and Social impacts of Westpac Group’s operations

Westpac Group is one of the Australia’s oldest banking company as this one

of the oldest banking group of Australia. Not only that, this is also one out of four

major bank of Australia. Westpac is also one among the largest bank of New

Zealand. The main business of this group includes the various banking as well as

asset management services to the consumers, institutional and business groups.

This Group was founded in the year 1817 with having name Bank of New South

Wales and changed its name in 1982 and become Westpac Banking Corporation

(Westpac, 2019). The Group played the important role in the economy of Australia in

last 200 years. In the basis of the current environment policy report of the group, the

followings are the some important environment impacts of the firm’s operations: -

The operations of firm negatively impact the environment as the firm

consumes high energy and paper. The uses of the energy and paper directly

affect the environment as energy is limited while the use of paper reduces the

numbers of trees.

Secondly, the firm emission of the green – house gases by the firm during its

operations also directly impact the environment. As we all know that the

green – house gases are very harmful for our environment as well as the

peoples (Westpac, 2019).

The investment made by the firm in the energy efficient technologies as well

as firm also tries to develop the system to recycle the materials positively

affect the environment, this not only saves the natural resources but also

save the environment from the harmful emissions.

As per the information provided by the firm in their official website, the followings

are social impact of the Westpac Group’s operations: -

The firm is investing the leader of tomorrow, the firm positively affect the

society by providing the education, training as well as opportunities to the

people which helps them to achieve their aspirations (Westpac, 2019). In

simple words, the firm positively impact the social aspect by providing

employment to the peoples.

3MANAGEMENT AND ENVIRONMENT ACCOUNTING

Secondly, firm also positively impact the society and their social responsibility

by providing the positive working environment to their employee. While, firm

ensures that this must be free from every issues like inequality and all.

Another social impact of the firm’ operation is that the firm always plays a vital

role in the development of the small firm by providing them required financial

help.

Comparison with other firm

To compare the quality and depth of the social and environment information

provided by the Westpac Group, this report chooses the Common Wealth Bank of

Australia. In the basis of the environment and sustainability report of the both the firm

it can be said both are among the top banking group of Australia and both the firms

are highly concern with their social and environment aspects especially about the

impact of their business operations in the social and environment. Hence, both the

firm responsible disclose their operation related information mainly those which

impact the social and environment aspects. Not only that both firm takes several

initiative to save the environment from the negative impact of their operations and to

do welfare of the social by operating their business accordingly.

The comparing the report of both the firm it can be said that the various

information regarding the impact of the social and environment of their business

have several common information. Those are how both the firm manage direct

environment impacts within the group as well as the indirect environmental impacts.

Both the firm explains their initiative to minimize their negative impact in the

environment (Westpac, 2019). While, there are some differences in the reporting of

the information related to their impact like Westpac separately mention the future

plans of the firm to reduce the negative impact of its operations in the environment

while Common Wealth Bank of Australia does not report separately in their report

and includes this under the same heading of managing direct and indirect

environment impacts (Commbank, 2019).

While, if we talk about the information related to social impact of the firm’s

operation then Westpac Group reported this information in the reports as well as in

the website of the firm while the Common Wealth Bank of Australia does not

reported clearly in their reports. In this regard the information are more clearly

reported by the Westpac Group compare to the Common Wealth Bank of Australia.

By analysing the all the related reports published by both firm, it is ascertain

that Westpac Group report the more clear and quality information regarding the

social and environment impact of its operations compare to the Common Wealth

Bank of Australia.

Key Challenges in complying with GRI

Global Reporting Initiative (GRI) is the standard of reporting the sustainability

information of the firm since 1990s. This standard is rapidly adopted by the firm in

the current timer to report their sustainability. This one of the most trusted and

globally adopted framework for the sustainability reporting. This helps the firm by

various means not only the businesses but this also helps government and others.

The followings are the some key challenges usually faced by the firm while

adopting the GRI in their reporting standards: -

Secondly, firm also positively impact the society and their social responsibility

by providing the positive working environment to their employee. While, firm

ensures that this must be free from every issues like inequality and all.

Another social impact of the firm’ operation is that the firm always plays a vital

role in the development of the small firm by providing them required financial

help.

Comparison with other firm

To compare the quality and depth of the social and environment information

provided by the Westpac Group, this report chooses the Common Wealth Bank of

Australia. In the basis of the environment and sustainability report of the both the firm

it can be said both are among the top banking group of Australia and both the firms

are highly concern with their social and environment aspects especially about the

impact of their business operations in the social and environment. Hence, both the

firm responsible disclose their operation related information mainly those which

impact the social and environment aspects. Not only that both firm takes several

initiative to save the environment from the negative impact of their operations and to

do welfare of the social by operating their business accordingly.

The comparing the report of both the firm it can be said that the various

information regarding the impact of the social and environment of their business

have several common information. Those are how both the firm manage direct

environment impacts within the group as well as the indirect environmental impacts.

Both the firm explains their initiative to minimize their negative impact in the

environment (Westpac, 2019). While, there are some differences in the reporting of

the information related to their impact like Westpac separately mention the future

plans of the firm to reduce the negative impact of its operations in the environment

while Common Wealth Bank of Australia does not report separately in their report

and includes this under the same heading of managing direct and indirect

environment impacts (Commbank, 2019).

While, if we talk about the information related to social impact of the firm’s

operation then Westpac Group reported this information in the reports as well as in

the website of the firm while the Common Wealth Bank of Australia does not

reported clearly in their reports. In this regard the information are more clearly

reported by the Westpac Group compare to the Common Wealth Bank of Australia.

By analysing the all the related reports published by both firm, it is ascertain

that Westpac Group report the more clear and quality information regarding the

social and environment impact of its operations compare to the Common Wealth

Bank of Australia.

Key Challenges in complying with GRI

Global Reporting Initiative (GRI) is the standard of reporting the sustainability

information of the firm since 1990s. This standard is rapidly adopted by the firm in

the current timer to report their sustainability. This one of the most trusted and

globally adopted framework for the sustainability reporting. This helps the firm by

various means not only the businesses but this also helps government and others.

The followings are the some key challenges usually faced by the firm while

adopting the GRI in their reporting standards: -

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4MANAGEMENT AND ENVIRONMENT ACCOUNTING

It is very difficult choice for the firm as it requires a huge commitment and

effort of the organisation as well as the firm also needs to make sure that

there must be a value in the process of reporting sustainability as per the GRI

(Vigneau, Humphreys & Moon, 2015).

Adopting the GRI in the sustainability reporting means firm really seems to

work on their reported information not only for the keeping the record.

The firm needs to revise all its existing policy and procedure to report the

information that is another challenge of adopting GRI.

This can be make the firm think towards their environment and social apart

from the profit hence sometime few firms face issues in adopting the GRI for

reporting the sustainability.

Lastly, the requirement of the GRI is vast, for which the firm needs to perform

various activities those activities consumes time as well as money which is

another issues with this reporting standards.

Benefits of GRI Reporting Standards complained report

The sustainability report prepared by the companies in compliances with the

Global Reporting Initiative is beneficial not only for the firm but also for the

stakeholders of the firm. A proper sustainability report prepared in the basis of the

GRI can benefits investors, shareholders and other stakeholders of the firm. The

followings are the some major benefits which the investors, shareholders or other

stakeholders of the firm: -

Better Communication: - This report helps the investors, shareholders and

other stakeholders to under the risk management policy as well as the

activities of the firm in better way as well as this provides the better

communication platform to the stakeholders to communicate with the

company (del Mar Alonso-Almeida et al, 2015).

Better relationship: - This sustainability reporting standards improve the

stakeholder’s engagement of the firm which establish strong and better

relationship between stakeholders and firm.

Internal data management: - This system strengthen the internal data of the

firm so that investors or the shareholders can help in their decision making

process.

Reveals sustainability strategy: - This report shows the sustainability

strategy of the firm which can guide the investors and other stakeholders to

make sound decisions related to their investment.

Future planning of Firms: - This provide a brief idea to the stakeholders of

the firm about the future sustainability of the firm which help them to take

investment related decisions.

Apart from the above benefits, the sustainability report compliance with the GRI

helps in several other ways to the investors, stakeholders and other stakeholders.

This mainly shows the sustainability of the firm along with the firm policy and

planning regarding the future sustainability which provides the brief idea about the

sustainability of the firm (Maas, Schaltegger & Crutzen, 2016). This information helps

the stakeholders in making the several decision especially investment related

decisions.

It is very difficult choice for the firm as it requires a huge commitment and

effort of the organisation as well as the firm also needs to make sure that

there must be a value in the process of reporting sustainability as per the GRI

(Vigneau, Humphreys & Moon, 2015).

Adopting the GRI in the sustainability reporting means firm really seems to

work on their reported information not only for the keeping the record.

The firm needs to revise all its existing policy and procedure to report the

information that is another challenge of adopting GRI.

This can be make the firm think towards their environment and social apart

from the profit hence sometime few firms face issues in adopting the GRI for

reporting the sustainability.

Lastly, the requirement of the GRI is vast, for which the firm needs to perform

various activities those activities consumes time as well as money which is

another issues with this reporting standards.

Benefits of GRI Reporting Standards complained report

The sustainability report prepared by the companies in compliances with the

Global Reporting Initiative is beneficial not only for the firm but also for the

stakeholders of the firm. A proper sustainability report prepared in the basis of the

GRI can benefits investors, shareholders and other stakeholders of the firm. The

followings are the some major benefits which the investors, shareholders or other

stakeholders of the firm: -

Better Communication: - This report helps the investors, shareholders and

other stakeholders to under the risk management policy as well as the

activities of the firm in better way as well as this provides the better

communication platform to the stakeholders to communicate with the

company (del Mar Alonso-Almeida et al, 2015).

Better relationship: - This sustainability reporting standards improve the

stakeholder’s engagement of the firm which establish strong and better

relationship between stakeholders and firm.

Internal data management: - This system strengthen the internal data of the

firm so that investors or the shareholders can help in their decision making

process.

Reveals sustainability strategy: - This report shows the sustainability

strategy of the firm which can guide the investors and other stakeholders to

make sound decisions related to their investment.

Future planning of Firms: - This provide a brief idea to the stakeholders of

the firm about the future sustainability of the firm which help them to take

investment related decisions.

Apart from the above benefits, the sustainability report compliance with the GRI

helps in several other ways to the investors, stakeholders and other stakeholders.

This mainly shows the sustainability of the firm along with the firm policy and

planning regarding the future sustainability which provides the brief idea about the

sustainability of the firm (Maas, Schaltegger & Crutzen, 2016). This information helps

the stakeholders in making the several decision especially investment related

decisions.

5MANAGEMENT AND ENVIRONMENT ACCOUNTING

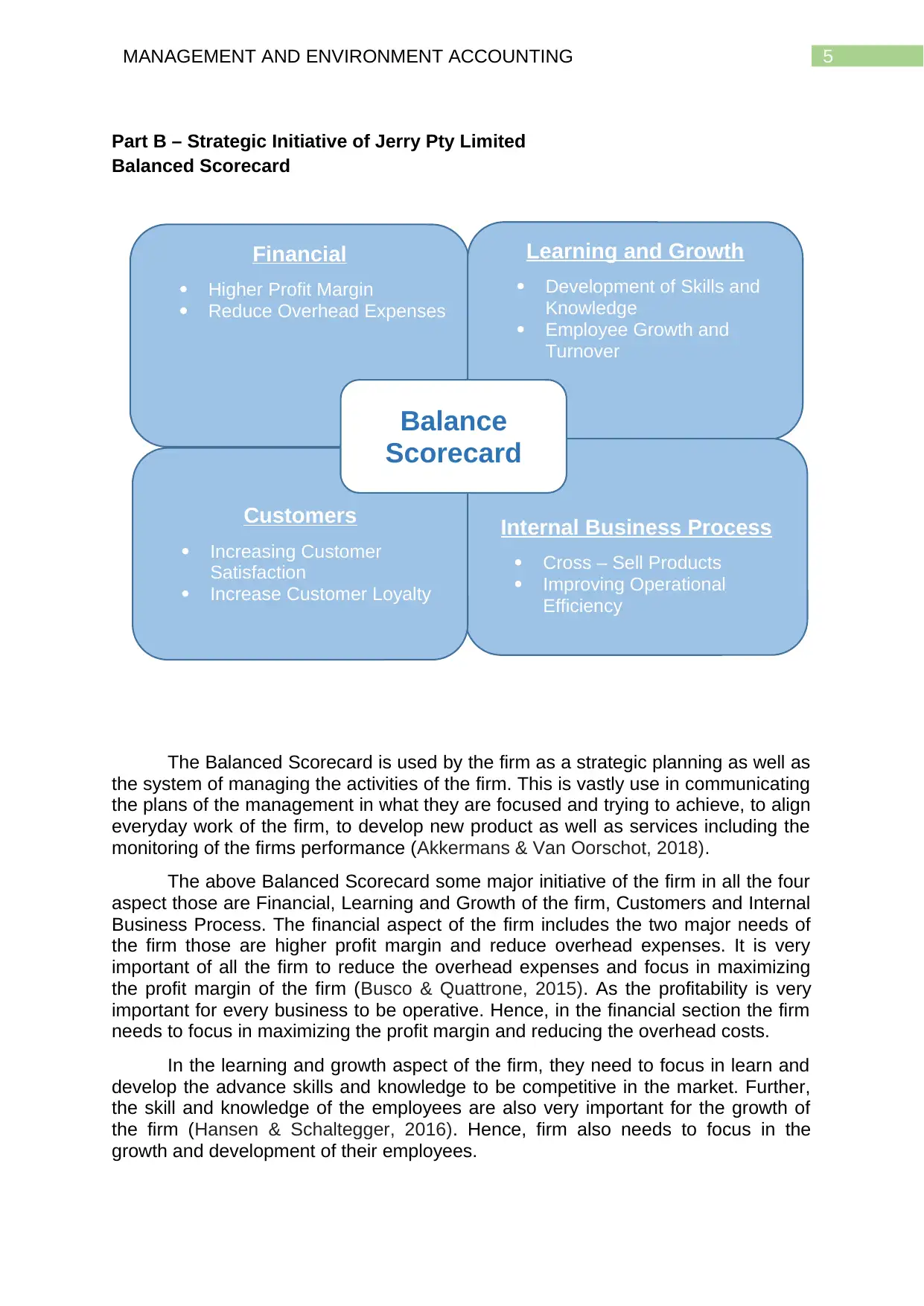

Part B – Strategic Initiative of Jerry Pty Limited

Balanced Scorecard

The Balanced Scorecard is used by the firm as a strategic planning as well as

the system of managing the activities of the firm. This is vastly use in communicating

the plans of the management in what they are focused and trying to achieve, to align

everyday work of the firm, to develop new product as well as services including the

monitoring of the firms performance (Akkermans & Van Oorschot, 2018).

The above Balanced Scorecard some major initiative of the firm in all the four

aspect those are Financial, Learning and Growth of the firm, Customers and Internal

Business Process. The financial aspect of the firm includes the two major needs of

the firm those are higher profit margin and reduce overhead expenses. It is very

important of all the firm to reduce the overhead expenses and focus in maximizing

the profit margin of the firm (Busco & Quattrone, 2015). As the profitability is very

important for every business to be operative. Hence, in the financial section the firm

needs to focus in maximizing the profit margin and reducing the overhead costs.

In the learning and growth aspect of the firm, they need to focus in learn and

develop the advance skills and knowledge to be competitive in the market. Further,

the skill and knowledge of the employees are also very important for the growth of

the firm (Hansen & Schaltegger, 2016). Hence, firm also needs to focus in the

growth and development of their employees.

Financial

Higher Profit Margin

Reduce Overhead Expenses

Learning and Growth

Development of Skills and

Knowledge

Employee Growth and

Turnover

Internal Business Process

Cross – Sell Products

Improving Operational

Efficiency

Customers

Increasing Customer

Satisfaction

Increase Customer Loyalty

Balance

Scorecard

Part B – Strategic Initiative of Jerry Pty Limited

Balanced Scorecard

The Balanced Scorecard is used by the firm as a strategic planning as well as

the system of managing the activities of the firm. This is vastly use in communicating

the plans of the management in what they are focused and trying to achieve, to align

everyday work of the firm, to develop new product as well as services including the

monitoring of the firms performance (Akkermans & Van Oorschot, 2018).

The above Balanced Scorecard some major initiative of the firm in all the four

aspect those are Financial, Learning and Growth of the firm, Customers and Internal

Business Process. The financial aspect of the firm includes the two major needs of

the firm those are higher profit margin and reduce overhead expenses. It is very

important of all the firm to reduce the overhead expenses and focus in maximizing

the profit margin of the firm (Busco & Quattrone, 2015). As the profitability is very

important for every business to be operative. Hence, in the financial section the firm

needs to focus in maximizing the profit margin and reducing the overhead costs.

In the learning and growth aspect of the firm, they need to focus in learn and

develop the advance skills and knowledge to be competitive in the market. Further,

the skill and knowledge of the employees are also very important for the growth of

the firm (Hansen & Schaltegger, 2016). Hence, firm also needs to focus in the

growth and development of their employees.

Financial

Higher Profit Margin

Reduce Overhead Expenses

Learning and Growth

Development of Skills and

Knowledge

Employee Growth and

Turnover

Internal Business Process

Cross – Sell Products

Improving Operational

Efficiency

Customers

Increasing Customer

Satisfaction

Increase Customer Loyalty

Balance

Scorecard

6MANAGEMENT AND ENVIRONMENT ACCOUNTING

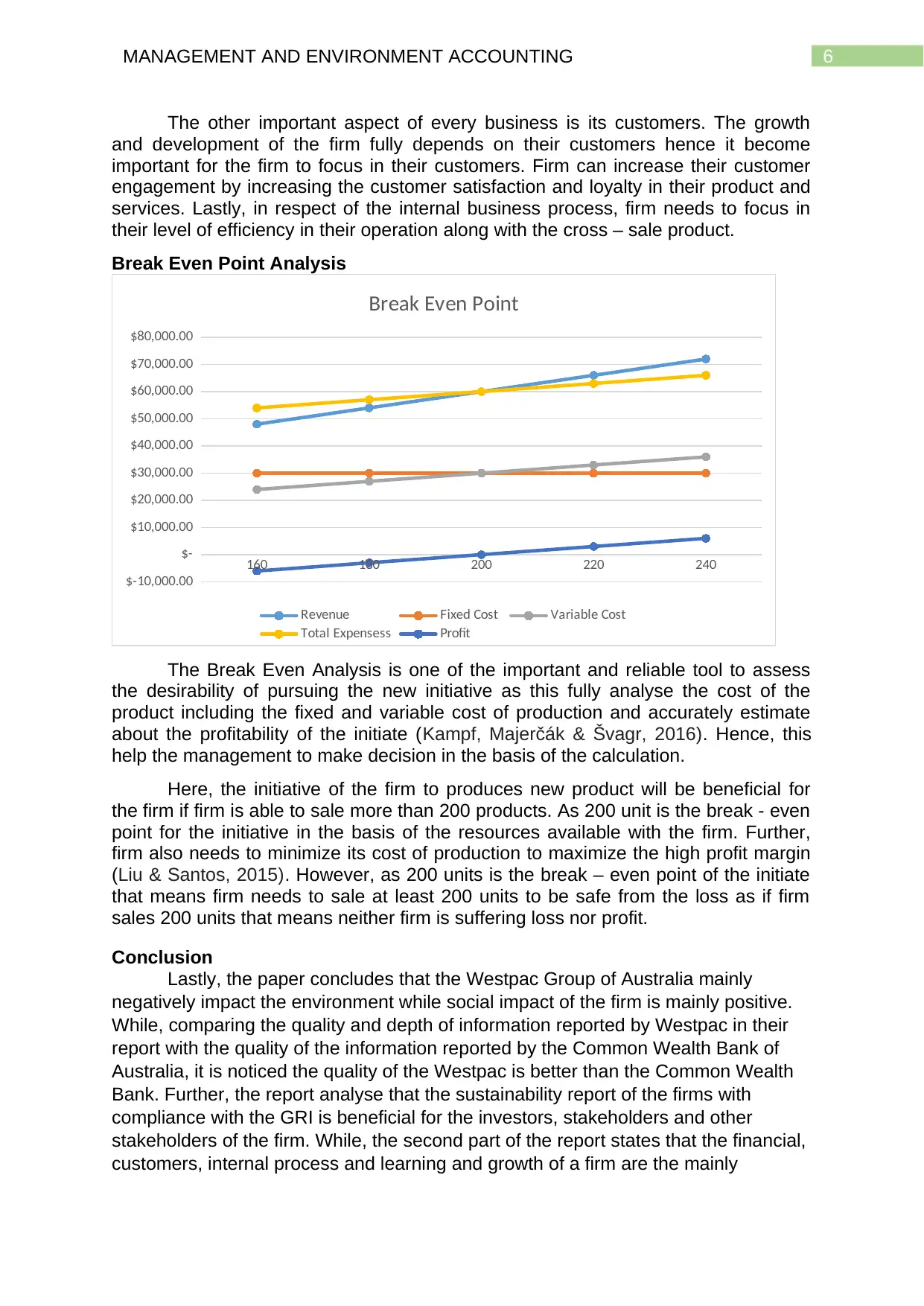

The other important aspect of every business is its customers. The growth

and development of the firm fully depends on their customers hence it become

important for the firm to focus in their customers. Firm can increase their customer

engagement by increasing the customer satisfaction and loyalty in their product and

services. Lastly, in respect of the internal business process, firm needs to focus in

their level of efficiency in their operation along with the cross – sale product.

Break Even Point Analysis

160 180 200 220 240

$-10,000.00

$-

$10,000.00

$20,000.00

$30,000.00

$40,000.00

$50,000.00

$60,000.00

$70,000.00

$80,000.00

Break Even Point

Revenue Fixed Cost Variable Cost

Total Expensess Profit

The Break Even Analysis is one of the important and reliable tool to assess

the desirability of pursuing the new initiative as this fully analyse the cost of the

product including the fixed and variable cost of production and accurately estimate

about the profitability of the initiate (Kampf, Majerčák & Švagr, 2016). Hence, this

help the management to make decision in the basis of the calculation.

Here, the initiative of the firm to produces new product will be beneficial for

the firm if firm is able to sale more than 200 products. As 200 unit is the break - even

point for the initiative in the basis of the resources available with the firm. Further,

firm also needs to minimize its cost of production to maximize the high profit margin

(Liu & Santos, 2015). However, as 200 units is the break – even point of the initiate

that means firm needs to sale at least 200 units to be safe from the loss as if firm

sales 200 units that means neither firm is suffering loss nor profit.

Conclusion

Lastly, the paper concludes that the Westpac Group of Australia mainly

negatively impact the environment while social impact of the firm is mainly positive.

While, comparing the quality and depth of information reported by Westpac in their

report with the quality of the information reported by the Common Wealth Bank of

Australia, it is noticed the quality of the Westpac is better than the Common Wealth

Bank. Further, the report analyse that the sustainability report of the firms with

compliance with the GRI is beneficial for the investors, stakeholders and other

stakeholders of the firm. While, the second part of the report states that the financial,

customers, internal process and learning and growth of a firm are the mainly

The other important aspect of every business is its customers. The growth

and development of the firm fully depends on their customers hence it become

important for the firm to focus in their customers. Firm can increase their customer

engagement by increasing the customer satisfaction and loyalty in their product and

services. Lastly, in respect of the internal business process, firm needs to focus in

their level of efficiency in their operation along with the cross – sale product.

Break Even Point Analysis

160 180 200 220 240

$-10,000.00

$-

$10,000.00

$20,000.00

$30,000.00

$40,000.00

$50,000.00

$60,000.00

$70,000.00

$80,000.00

Break Even Point

Revenue Fixed Cost Variable Cost

Total Expensess Profit

The Break Even Analysis is one of the important and reliable tool to assess

the desirability of pursuing the new initiative as this fully analyse the cost of the

product including the fixed and variable cost of production and accurately estimate

about the profitability of the initiate (Kampf, Majerčák & Švagr, 2016). Hence, this

help the management to make decision in the basis of the calculation.

Here, the initiative of the firm to produces new product will be beneficial for

the firm if firm is able to sale more than 200 products. As 200 unit is the break - even

point for the initiative in the basis of the resources available with the firm. Further,

firm also needs to minimize its cost of production to maximize the high profit margin

(Liu & Santos, 2015). However, as 200 units is the break – even point of the initiate

that means firm needs to sale at least 200 units to be safe from the loss as if firm

sales 200 units that means neither firm is suffering loss nor profit.

Conclusion

Lastly, the paper concludes that the Westpac Group of Australia mainly

negatively impact the environment while social impact of the firm is mainly positive.

While, comparing the quality and depth of information reported by Westpac in their

report with the quality of the information reported by the Common Wealth Bank of

Australia, it is noticed the quality of the Westpac is better than the Common Wealth

Bank. Further, the report analyse that the sustainability report of the firms with

compliance with the GRI is beneficial for the investors, stakeholders and other

stakeholders of the firm. While, the second part of the report states that the financial,

customers, internal process and learning and growth of a firm are the mainly

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT AND ENVIRONMENT ACCOUNTING

important aspects and they need to focus to increase the efficiency in this areas for

which they can use balanced scorecard. Lastly, the report states that break – even

analysis one of the important tool for assessing the desirability of pursuing any new

initiative.

important aspects and they need to focus to increase the efficiency in this areas for

which they can use balanced scorecard. Lastly, the report states that break – even

analysis one of the important tool for assessing the desirability of pursuing any new

initiative.

8MANAGEMENT AND ENVIRONMENT ACCOUNTING

References

Akkermans, H. A., & Van Oorschot, K. E. (2018). Relevance assumed: a case study

of balanced scorecard development using system dynamics. In System

Dynamics (pp. 107-132). Palgrave Macmillan, London.

Busco, C., & Quattrone, P. (2015). Exploring how the balanced scorecard engages

and unfolds: Articulating the visual power of accounting

inscriptions. Contemporary Accounting Research, 32(3), 1236-1262.

Commbank. (2019). Retrieved 22 September 2019, from

https://www.commbank.com.au/about-us/docs/sustainability-20151103-group-environment-

policy.pdf

del Mar Alonso-Almeida, M., Marimon, F., Casani, F., & Rodriguez-Pomeda, J.

(2015). Diffusion of sustainability reporting in universities: current situation

and future perspectives. Journal of cleaner production, 106, 144-154.

Hansen, E. G., & Schaltegger, S. (2016). The sustainability balanced scorecard: A

systematic review of architectures. Journal of Business Ethics, 133(2), 193-

221.

Herremans, I. M., Nazari, J. A., & Mahmoudian, F. (2016). Stakeholder relationships,

engagement, and sustainability reporting. Journal of Business Ethics, 138(3),

417-435.

Ioannou, I., & Serafeim, G. (2017). The consequences of mandatory corporate

sustainability reporting. Harvard Business School research working paper,

(11-100).

Kampf, R., Majerčák, P., & Švagr, P. (2016). Application of break-even point

analysis. NAŠE MORE: znanstveno-stručni časopis za more i

pomorstvo, 63(3 Special Issue), 126-128.

Khouri, S., Istok, M., Rosova, A., & Straka, M. (2018). THE BREAK-EVEN POINT

CALCULATION IN ONSHORE AND OFFSHORE BUSINESSES IN

REGARDS TO TAXATION. Transformations in Business & Economics, 17.

Liu, J., & Santos, G. (2015). Decarbonizing the road transport sector: Break-even

point and consequent potential consumers' behavior for the US

case. International Journal of Sustainable Transportation, 9(3), 159-175.

Maas, K., Schaltegger, S., & Crutzen, N. (2016). Integrating corporate sustainability

assessment, management accounting, control, and reporting. Journal of

Cleaner Production, 136, 237-248.

Stacchezzini, R., Melloni, G., & Lai, A. (2016). Sustainability management and

reporting: the role of integrated reporting for communicating corporate

sustainability management. Journal of Cleaner Production, 136, 102-110.

Vigneau, L., Humphreys, M., & Moon, J. (2015). How do firms comply with

international sustainability standards? Processes and consequences of

adopting the global reporting initiative. Journal of Business Ethics, 131(2),

469-486.

References

Akkermans, H. A., & Van Oorschot, K. E. (2018). Relevance assumed: a case study

of balanced scorecard development using system dynamics. In System

Dynamics (pp. 107-132). Palgrave Macmillan, London.

Busco, C., & Quattrone, P. (2015). Exploring how the balanced scorecard engages

and unfolds: Articulating the visual power of accounting

inscriptions. Contemporary Accounting Research, 32(3), 1236-1262.

Commbank. (2019). Retrieved 22 September 2019, from

https://www.commbank.com.au/about-us/docs/sustainability-20151103-group-environment-

policy.pdf

del Mar Alonso-Almeida, M., Marimon, F., Casani, F., & Rodriguez-Pomeda, J.

(2015). Diffusion of sustainability reporting in universities: current situation

and future perspectives. Journal of cleaner production, 106, 144-154.

Hansen, E. G., & Schaltegger, S. (2016). The sustainability balanced scorecard: A

systematic review of architectures. Journal of Business Ethics, 133(2), 193-

221.

Herremans, I. M., Nazari, J. A., & Mahmoudian, F. (2016). Stakeholder relationships,

engagement, and sustainability reporting. Journal of Business Ethics, 138(3),

417-435.

Ioannou, I., & Serafeim, G. (2017). The consequences of mandatory corporate

sustainability reporting. Harvard Business School research working paper,

(11-100).

Kampf, R., Majerčák, P., & Švagr, P. (2016). Application of break-even point

analysis. NAŠE MORE: znanstveno-stručni časopis za more i

pomorstvo, 63(3 Special Issue), 126-128.

Khouri, S., Istok, M., Rosova, A., & Straka, M. (2018). THE BREAK-EVEN POINT

CALCULATION IN ONSHORE AND OFFSHORE BUSINESSES IN

REGARDS TO TAXATION. Transformations in Business & Economics, 17.

Liu, J., & Santos, G. (2015). Decarbonizing the road transport sector: Break-even

point and consequent potential consumers' behavior for the US

case. International Journal of Sustainable Transportation, 9(3), 159-175.

Maas, K., Schaltegger, S., & Crutzen, N. (2016). Integrating corporate sustainability

assessment, management accounting, control, and reporting. Journal of

Cleaner Production, 136, 237-248.

Stacchezzini, R., Melloni, G., & Lai, A. (2016). Sustainability management and

reporting: the role of integrated reporting for communicating corporate

sustainability management. Journal of Cleaner Production, 136, 102-110.

Vigneau, L., Humphreys, M., & Moon, J. (2015). How do firms comply with

international sustainability standards? Processes and consequences of

adopting the global reporting initiative. Journal of Business Ethics, 131(2),

469-486.

9MANAGEMENT AND ENVIRONMENT ACCOUNTING

Westpac. (2019). Company overview | Westpac. Retrieved 22 September 2019, from

https://www.westpac.com.au/about-westpac/westpac-group/company-overview/

Westpac. (2019). Retrieved 22 September 2019, from

https://www.westpac.com.au/docs/pdf/aw/EnvironmentalPolicy.pdf

Westpac. (2019). Social impact framework and assessment | Westpac. Retrieved 22

September 2019, from

https://www.westpac.com.au/about-westpac/sustainability/initiatives-for-you/social-

enterprises-social-impact/

Westpac. (2019). Company overview | Westpac. Retrieved 22 September 2019, from

https://www.westpac.com.au/about-westpac/westpac-group/company-overview/

Westpac. (2019). Retrieved 22 September 2019, from

https://www.westpac.com.au/docs/pdf/aw/EnvironmentalPolicy.pdf

Westpac. (2019). Social impact framework and assessment | Westpac. Retrieved 22

September 2019, from

https://www.westpac.com.au/about-westpac/sustainability/initiatives-for-you/social-

enterprises-social-impact/

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.