Management Of Cost Accounting : Assignment

VerifiedAdded on 2021/01/02

|18

|5683

|22

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management

Accounting Systems

&

Techniques

Accounting Systems

&

Techniques

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Explain management accounting and essential requirements of various types of

management accounting systems................................................................................................3

P2. Explain different methods used for management accounting reporting...............................6

TASK 2............................................................................................................................................7

P3. Calculate costs using appropriate techniques of cost analysis to prepare and income

statement using marginal and absorption costs...........................................................................7

TASK 3..........................................................................................................................................11

P4 Advantages and disadvantages of different types of planning tools used for budgetary

control ......................................................................................................................................11

TASK 4..........................................................................................................................................14

P5. Compare how organisations are adapting management accounting systems to respond to

financial problems.....................................................................................................................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

.......................................................................................................................................................17

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Explain management accounting and essential requirements of various types of

management accounting systems................................................................................................3

P2. Explain different methods used for management accounting reporting...............................6

TASK 2............................................................................................................................................7

P3. Calculate costs using appropriate techniques of cost analysis to prepare and income

statement using marginal and absorption costs...........................................................................7

TASK 3..........................................................................................................................................11

P4 Advantages and disadvantages of different types of planning tools used for budgetary

control ......................................................................................................................................11

TASK 4..........................................................................................................................................14

P5. Compare how organisations are adapting management accounting systems to respond to

financial problems.....................................................................................................................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

.......................................................................................................................................................17

INTRODUCTION

Management accounting is concerned with the process of assessing costs incurred in

business operations to prepare internal financial report, accounts and records for making

informed decision to accomplish organizational goals (DRURY, 2013). It is also known as

managerial or cost accounting. UK Financial Consultants Ltd. Has been chosen for this report.

Further, it covers meaning of management accounting along with its essential requirements and

different methods used for management accounting reporting. Furthermore, calculation of costs

through appropriate techniques of cost analysis and advantages and disadvantages of different

types of planing tools for budgetary control. Lastly, comparison of organizations opting

management accounting system to address financial problems.

TASK 1

P1. Explain management accounting and essential requirements of various types of management

accounting systems

The Institute of Cost and Management Accountants, London, has defined

Management Accounting as “The application of professional knowledge and skill in the

preparation of accounting information in such a way as to assist management in the formulation

of policies and in the planning and control of the operation of the undertakings.” In simple

words, it involves business activities of planning, organising, staffing, directing and controlling

the day-to-day activities for achieving goals and objectives of an entity. Policies are a major part

of this accounting by following which decisions are made (Hilton, and Platt, 2013).

Management Accounting System comprise of actions and framework which are applied

to each departments functioning in an organization. It forms a co-ordination between internal

parties. The scope of this system is vast as it takes into both financial as well as non-financial

data. Johnson and Kaplan defined that management accounting system should effective enough

to provide accurate, reliable and timely information so that costs can be controlled, measured in

order to improve productivity by implementing better production processes.

Managerial accounting can provide numerous benefits to an entity which can have

significant impact on its operations. Further, it is importance to make a part in as internal parties

use qualitative and quantitative information to make decisions. This encourages continuous

Management accounting is concerned with the process of assessing costs incurred in

business operations to prepare internal financial report, accounts and records for making

informed decision to accomplish organizational goals (DRURY, 2013). It is also known as

managerial or cost accounting. UK Financial Consultants Ltd. Has been chosen for this report.

Further, it covers meaning of management accounting along with its essential requirements and

different methods used for management accounting reporting. Furthermore, calculation of costs

through appropriate techniques of cost analysis and advantages and disadvantages of different

types of planing tools for budgetary control. Lastly, comparison of organizations opting

management accounting system to address financial problems.

TASK 1

P1. Explain management accounting and essential requirements of various types of management

accounting systems

The Institute of Cost and Management Accountants, London, has defined

Management Accounting as “The application of professional knowledge and skill in the

preparation of accounting information in such a way as to assist management in the formulation

of policies and in the planning and control of the operation of the undertakings.” In simple

words, it involves business activities of planning, organising, staffing, directing and controlling

the day-to-day activities for achieving goals and objectives of an entity. Policies are a major part

of this accounting by following which decisions are made (Hilton, and Platt, 2013).

Management Accounting System comprise of actions and framework which are applied

to each departments functioning in an organization. It forms a co-ordination between internal

parties. The scope of this system is vast as it takes into both financial as well as non-financial

data. Johnson and Kaplan defined that management accounting system should effective enough

to provide accurate, reliable and timely information so that costs can be controlled, measured in

order to improve productivity by implementing better production processes.

Managerial accounting can provide numerous benefits to an entity which can have

significant impact on its operations. Further, it is importance to make a part in as internal parties

use qualitative and quantitative information to make decisions. This encourages continuous

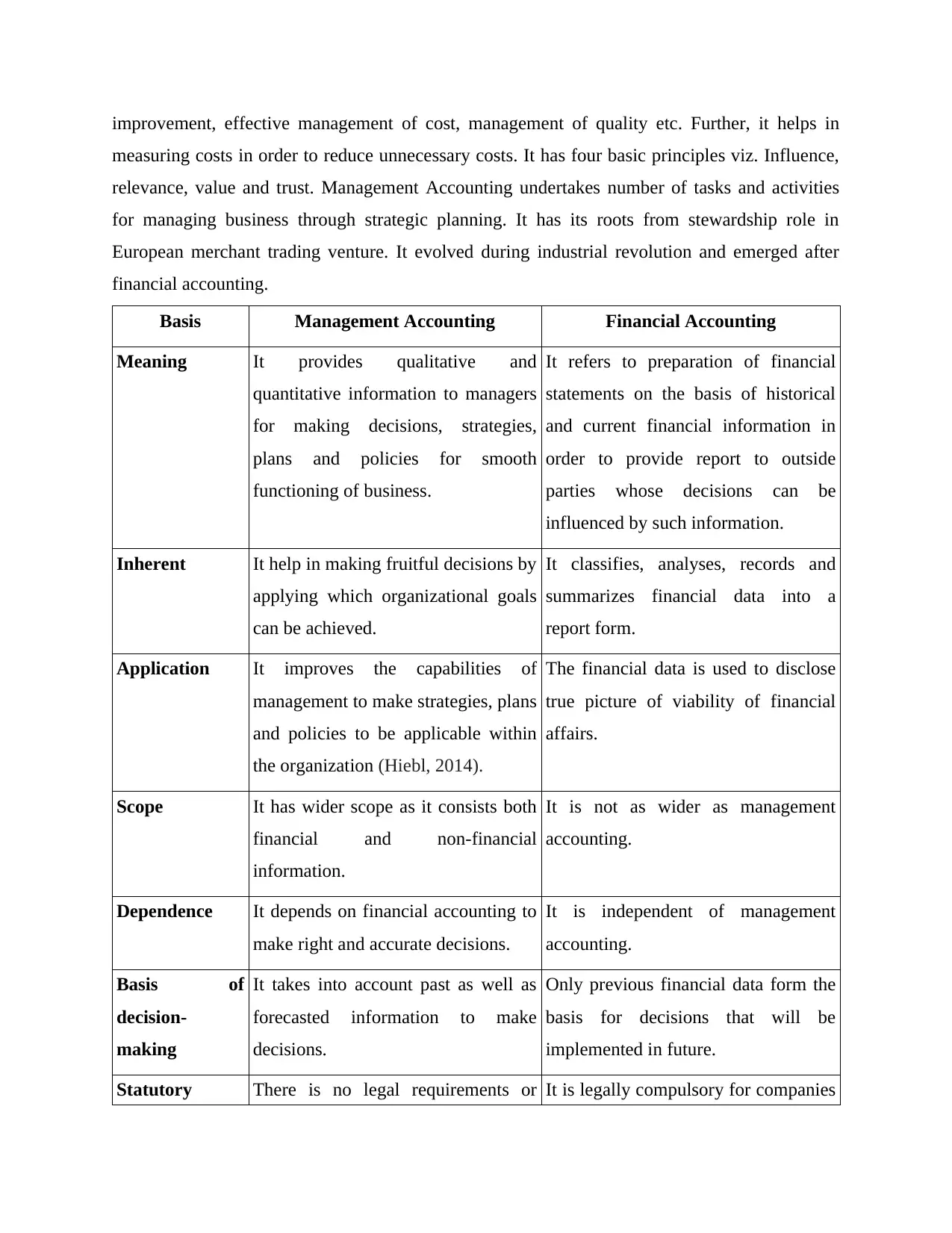

improvement, effective management of cost, management of quality etc. Further, it helps in

measuring costs in order to reduce unnecessary costs. It has four basic principles viz. Influence,

relevance, value and trust. Management Accounting undertakes number of tasks and activities

for managing business through strategic planning. It has its roots from stewardship role in

European merchant trading venture. It evolved during industrial revolution and emerged after

financial accounting.

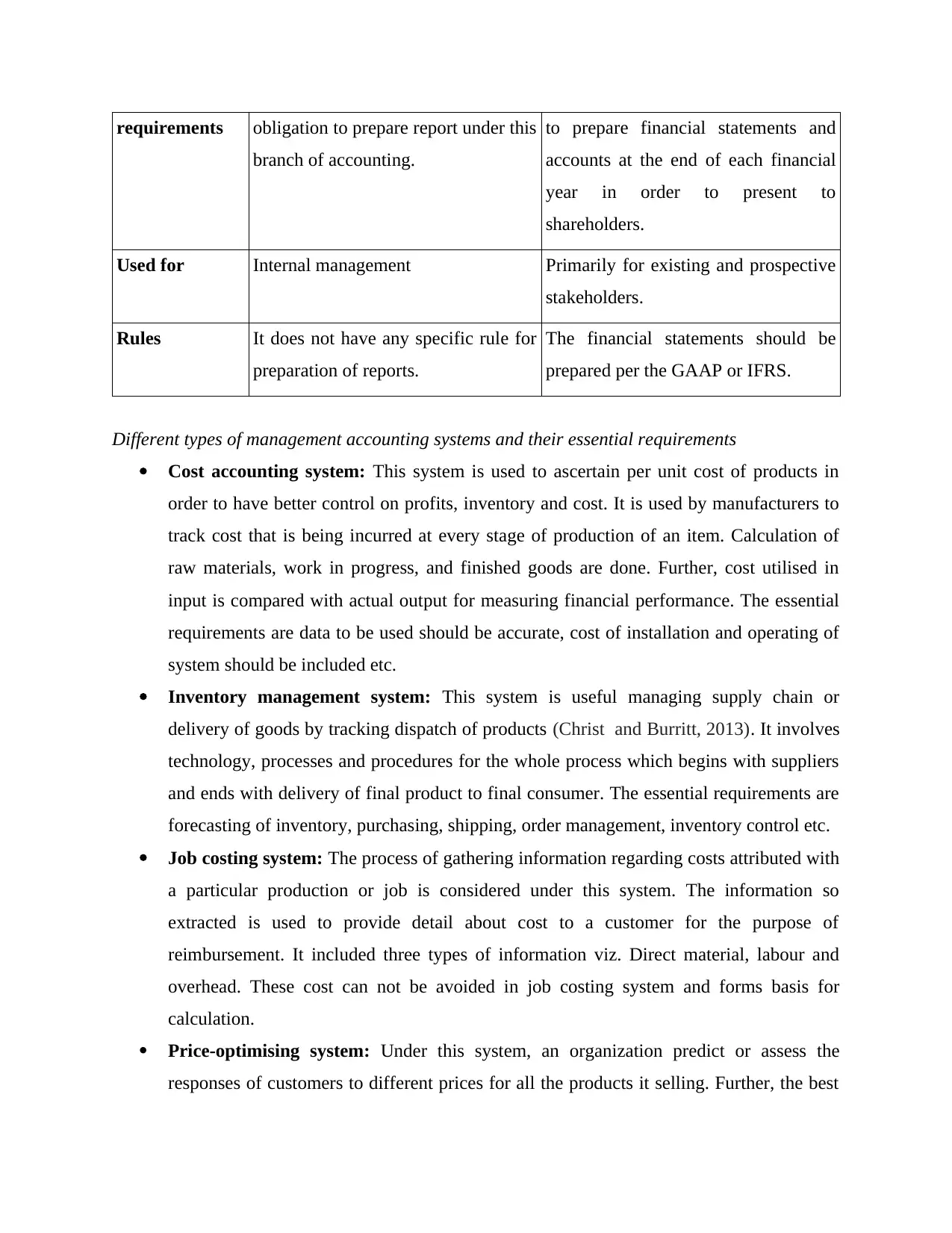

Basis Management Accounting Financial Accounting

Meaning It provides qualitative and

quantitative information to managers

for making decisions, strategies,

plans and policies for smooth

functioning of business.

It refers to preparation of financial

statements on the basis of historical

and current financial information in

order to provide report to outside

parties whose decisions can be

influenced by such information.

Inherent It help in making fruitful decisions by

applying which organizational goals

can be achieved.

It classifies, analyses, records and

summarizes financial data into a

report form.

Application It improves the capabilities of

management to make strategies, plans

and policies to be applicable within

the organization (Hiebl, 2014).

The financial data is used to disclose

true picture of viability of financial

affairs.

Scope It has wider scope as it consists both

financial and non-financial

information.

It is not as wider as management

accounting.

Dependence It depends on financial accounting to

make right and accurate decisions.

It is independent of management

accounting.

Basis of

decision-

making

It takes into account past as well as

forecasted information to make

decisions.

Only previous financial data form the

basis for decisions that will be

implemented in future.

Statutory There is no legal requirements or It is legally compulsory for companies

measuring costs in order to reduce unnecessary costs. It has four basic principles viz. Influence,

relevance, value and trust. Management Accounting undertakes number of tasks and activities

for managing business through strategic planning. It has its roots from stewardship role in

European merchant trading venture. It evolved during industrial revolution and emerged after

financial accounting.

Basis Management Accounting Financial Accounting

Meaning It provides qualitative and

quantitative information to managers

for making decisions, strategies,

plans and policies for smooth

functioning of business.

It refers to preparation of financial

statements on the basis of historical

and current financial information in

order to provide report to outside

parties whose decisions can be

influenced by such information.

Inherent It help in making fruitful decisions by

applying which organizational goals

can be achieved.

It classifies, analyses, records and

summarizes financial data into a

report form.

Application It improves the capabilities of

management to make strategies, plans

and policies to be applicable within

the organization (Hiebl, 2014).

The financial data is used to disclose

true picture of viability of financial

affairs.

Scope It has wider scope as it consists both

financial and non-financial

information.

It is not as wider as management

accounting.

Dependence It depends on financial accounting to

make right and accurate decisions.

It is independent of management

accounting.

Basis of

decision-

making

It takes into account past as well as

forecasted information to make

decisions.

Only previous financial data form the

basis for decisions that will be

implemented in future.

Statutory There is no legal requirements or It is legally compulsory for companies

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

requirements obligation to prepare report under this

branch of accounting.

to prepare financial statements and

accounts at the end of each financial

year in order to present to

shareholders.

Used for Internal management Primarily for existing and prospective

stakeholders.

Rules It does not have any specific rule for

preparation of reports.

The financial statements should be

prepared per the GAAP or IFRS.

Different types of management accounting systems and their essential requirements

Cost accounting system: This system is used to ascertain per unit cost of products in

order to have better control on profits, inventory and cost. It is used by manufacturers to

track cost that is being incurred at every stage of production of an item. Calculation of

raw materials, work in progress, and finished goods are done. Further, cost utilised in

input is compared with actual output for measuring financial performance. The essential

requirements are data to be used should be accurate, cost of installation and operating of

system should be included etc.

Inventory management system: This system is useful managing supply chain or

delivery of goods by tracking dispatch of products (Christ and Burritt, 2013). It involves

technology, processes and procedures for the whole process which begins with suppliers

and ends with delivery of final product to final consumer. The essential requirements are

forecasting of inventory, purchasing, shipping, order management, inventory control etc.

Job costing system: The process of gathering information regarding costs attributed with

a particular production or job is considered under this system. The information so

extracted is used to provide detail about cost to a customer for the purpose of

reimbursement. It included three types of information viz. Direct material, labour and

overhead. These cost can not be avoided in job costing system and forms basis for

calculation.

Price-optimising system: Under this system, an organization predict or assess the

responses of customers to different prices for all the products it selling. Further, the best

branch of accounting.

to prepare financial statements and

accounts at the end of each financial

year in order to present to

shareholders.

Used for Internal management Primarily for existing and prospective

stakeholders.

Rules It does not have any specific rule for

preparation of reports.

The financial statements should be

prepared per the GAAP or IFRS.

Different types of management accounting systems and their essential requirements

Cost accounting system: This system is used to ascertain per unit cost of products in

order to have better control on profits, inventory and cost. It is used by manufacturers to

track cost that is being incurred at every stage of production of an item. Calculation of

raw materials, work in progress, and finished goods are done. Further, cost utilised in

input is compared with actual output for measuring financial performance. The essential

requirements are data to be used should be accurate, cost of installation and operating of

system should be included etc.

Inventory management system: This system is useful managing supply chain or

delivery of goods by tracking dispatch of products (Christ and Burritt, 2013). It involves

technology, processes and procedures for the whole process which begins with suppliers

and ends with delivery of final product to final consumer. The essential requirements are

forecasting of inventory, purchasing, shipping, order management, inventory control etc.

Job costing system: The process of gathering information regarding costs attributed with

a particular production or job is considered under this system. The information so

extracted is used to provide detail about cost to a customer for the purpose of

reimbursement. It included three types of information viz. Direct material, labour and

overhead. These cost can not be avoided in job costing system and forms basis for

calculation.

Price-optimising system: Under this system, an organization predict or assess the

responses of customers to different prices for all the products it selling. Further, the best

price is chosen which fits all the criteria such as objectives of the entity. Such information

can be obtained by conducting survey data, operating costs, inventories etc. The essential

requirements for this system are adopting a suitable optimization model, collection of

past data, monitoring results etc.

P2. Explain different methods used for management accounting reporting

Management accounting report is made in a comprehensive way which include all

information are included so that right decisions are taken. There are many types of reports

available that are prepared in management accounting which are as follows:

Inventory report: These are the reports prepared to track movement of inventory in

different locations such as manufacturing plant, warehouse etc. It is prepared in a

summary form comprising comprehensive accounts of stock and its supply. Further, it be

categorised into different parts for recording amount of various items.

Performance report: This report is prepared to assess the work performed by each

individual. There are specified standard which are used as a basis to compare the actual

results obtained by each employee to find out variance. Furthermore, a company dispatch

this report to each personnel explaining their achievements along with differences that

have occurred (Schaltegger and Burritt, 2017).

Accounts receivable report: This report comprise information about invoices of unpaid

customers and unused credit bills within date so prescribed. In other words, it

differentiate account receivable on the basis time of an invoice has been outstanding. A

inventors is always interested in knowing the time that is being taken by company to

collect its receivables. This helps in determining financial soundness of an entity. Further,

major decisions can be taken on the basis of such reports about lowering credit risk in

sales. Further, a total of receivables of a company is shown at the bottom according to

time given for such credit.

Cost accounting report: A company selling products has to incurred costs for raw

material and each such process through which it passes in order to become a final goods.

The report contain information about expenses and revenues that have been credited to or

debited from cost centres, attribution of total cost to each element of product, transactions

of cost accounting and a summary detail financial and cost accounting. Hence, it is

prepared on the costs that have been spent in making a finished product.

can be obtained by conducting survey data, operating costs, inventories etc. The essential

requirements for this system are adopting a suitable optimization model, collection of

past data, monitoring results etc.

P2. Explain different methods used for management accounting reporting

Management accounting report is made in a comprehensive way which include all

information are included so that right decisions are taken. There are many types of reports

available that are prepared in management accounting which are as follows:

Inventory report: These are the reports prepared to track movement of inventory in

different locations such as manufacturing plant, warehouse etc. It is prepared in a

summary form comprising comprehensive accounts of stock and its supply. Further, it be

categorised into different parts for recording amount of various items.

Performance report: This report is prepared to assess the work performed by each

individual. There are specified standard which are used as a basis to compare the actual

results obtained by each employee to find out variance. Furthermore, a company dispatch

this report to each personnel explaining their achievements along with differences that

have occurred (Schaltegger and Burritt, 2017).

Accounts receivable report: This report comprise information about invoices of unpaid

customers and unused credit bills within date so prescribed. In other words, it

differentiate account receivable on the basis time of an invoice has been outstanding. A

inventors is always interested in knowing the time that is being taken by company to

collect its receivables. This helps in determining financial soundness of an entity. Further,

major decisions can be taken on the basis of such reports about lowering credit risk in

sales. Further, a total of receivables of a company is shown at the bottom according to

time given for such credit.

Cost accounting report: A company selling products has to incurred costs for raw

material and each such process through which it passes in order to become a final goods.

The report contain information about expenses and revenues that have been credited to or

debited from cost centres, attribution of total cost to each element of product, transactions

of cost accounting and a summary detail financial and cost accounting. Hence, it is

prepared on the costs that have been spent in making a finished product.

Cash flow report: It is an important part of financial statement which is prepared to

show inflow and outflow of cash in business operations. It presents an overview of

financial activity in the company for a specified time period. These may be prepared on a

quarterly basis to have better control on management of costs. Further, it may include

balance sheets, income statement, statement of changes in equity, prime transactions of

company which may have significant impact etc.

TASK 2

P3. Calculate costs using appropriate techniques of cost analysis to prepare and income statement

using marginal and absorption costs

Cost is an amount refers to an amount expressed in monetary value that is spent by

company in order to manufacture a product. This is spent for creation of a goods or service.

Moreover, profits are not included while calculating costs.

Absorption costing: It is associated with involving the cost attributed to production of a

particular product. These include direct costs such as wages, raw material etc. which form the

basis for whole calculation. It is also called full costing whereby fixed overhead charges are

included as product cost (Anandarajan , Anandarajan and Srinivasan,Eds., 2012).

Marginal costing: Under this costing system, only variable costs are considered and

fixed costs are not at all taken into account for the calculation. Further, it involves additional

costs incurred for producing an extra unit of output which can be computed by total variable cost

assigned to one unit.

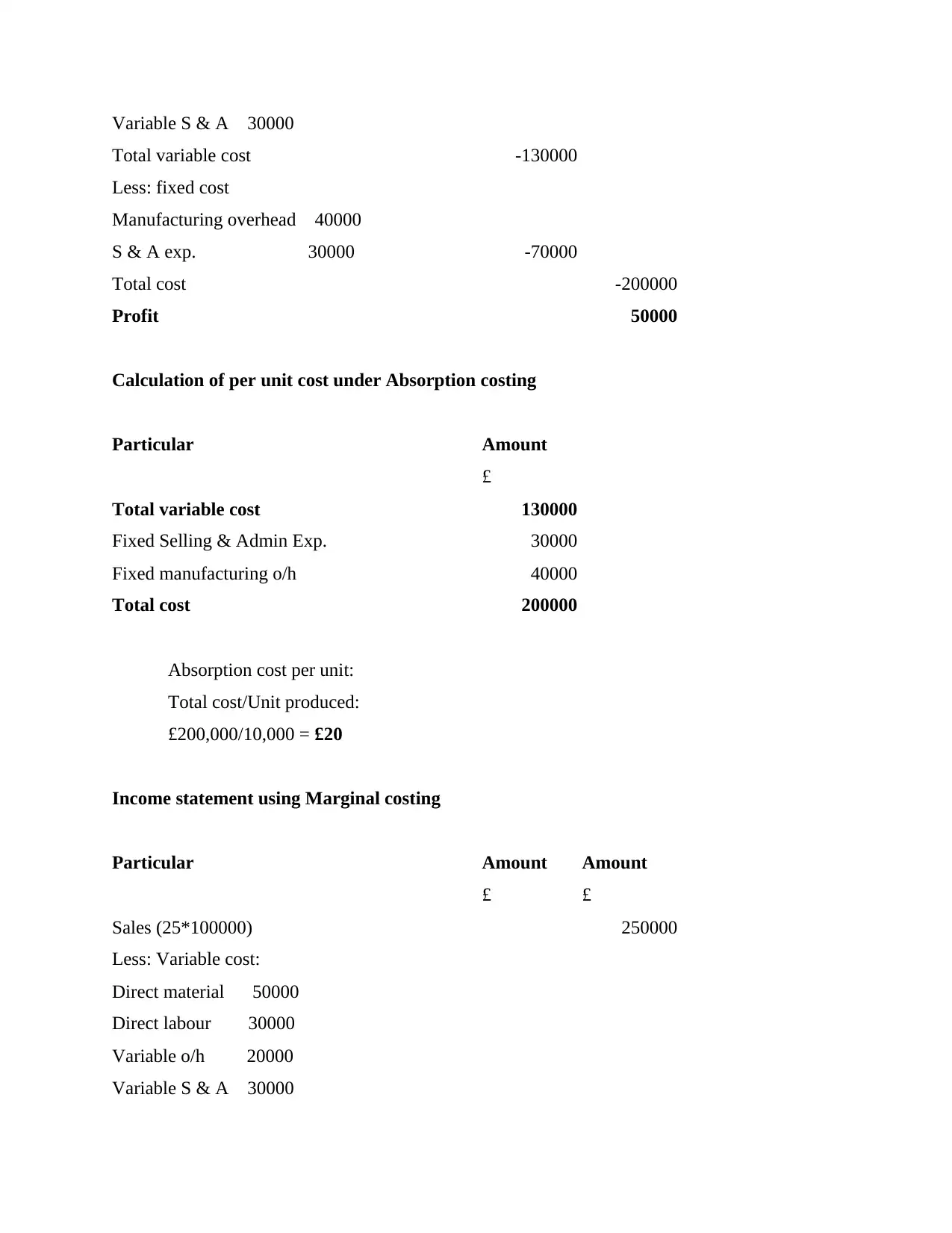

Income statement using Absorption costing

Particular Amount Amount

£ £

Sales (25*100000) 250000

Less: Variable cost:

Direct material 50000

Direct labour 30000

Variable o/h 20000

show inflow and outflow of cash in business operations. It presents an overview of

financial activity in the company for a specified time period. These may be prepared on a

quarterly basis to have better control on management of costs. Further, it may include

balance sheets, income statement, statement of changes in equity, prime transactions of

company which may have significant impact etc.

TASK 2

P3. Calculate costs using appropriate techniques of cost analysis to prepare and income statement

using marginal and absorption costs

Cost is an amount refers to an amount expressed in monetary value that is spent by

company in order to manufacture a product. This is spent for creation of a goods or service.

Moreover, profits are not included while calculating costs.

Absorption costing: It is associated with involving the cost attributed to production of a

particular product. These include direct costs such as wages, raw material etc. which form the

basis for whole calculation. It is also called full costing whereby fixed overhead charges are

included as product cost (Anandarajan , Anandarajan and Srinivasan,Eds., 2012).

Marginal costing: Under this costing system, only variable costs are considered and

fixed costs are not at all taken into account for the calculation. Further, it involves additional

costs incurred for producing an extra unit of output which can be computed by total variable cost

assigned to one unit.

Income statement using Absorption costing

Particular Amount Amount

£ £

Sales (25*100000) 250000

Less: Variable cost:

Direct material 50000

Direct labour 30000

Variable o/h 20000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Variable S & A 30000

Total variable cost -130000

Less: fixed cost

Manufacturing overhead 40000

S & A exp. 30000 -70000

Total cost -200000

Profit 50000

Calculation of per unit cost under Absorption costing

Particular Amount

£

Total variable cost 130000

Fixed Selling & Admin Exp. 30000

Fixed manufacturing o/h 40000

Total cost 200000

Absorption cost per unit:

Total cost/Unit produced:

£200,000/10,000 = £20

Income statement using Marginal costing

Particular Amount Amount

£ £

Sales (25*100000) 250000

Less: Variable cost:

Direct material 50000

Direct labour 30000

Variable o/h 20000

Variable S & A 30000

Total variable cost -130000

Less: fixed cost

Manufacturing overhead 40000

S & A exp. 30000 -70000

Total cost -200000

Profit 50000

Calculation of per unit cost under Absorption costing

Particular Amount

£

Total variable cost 130000

Fixed Selling & Admin Exp. 30000

Fixed manufacturing o/h 40000

Total cost 200000

Absorption cost per unit:

Total cost/Unit produced:

£200,000/10,000 = £20

Income statement using Marginal costing

Particular Amount Amount

£ £

Sales (25*100000) 250000

Less: Variable cost:

Direct material 50000

Direct labour 30000

Variable o/h 20000

Variable S & A 30000

Total variable cost -130000

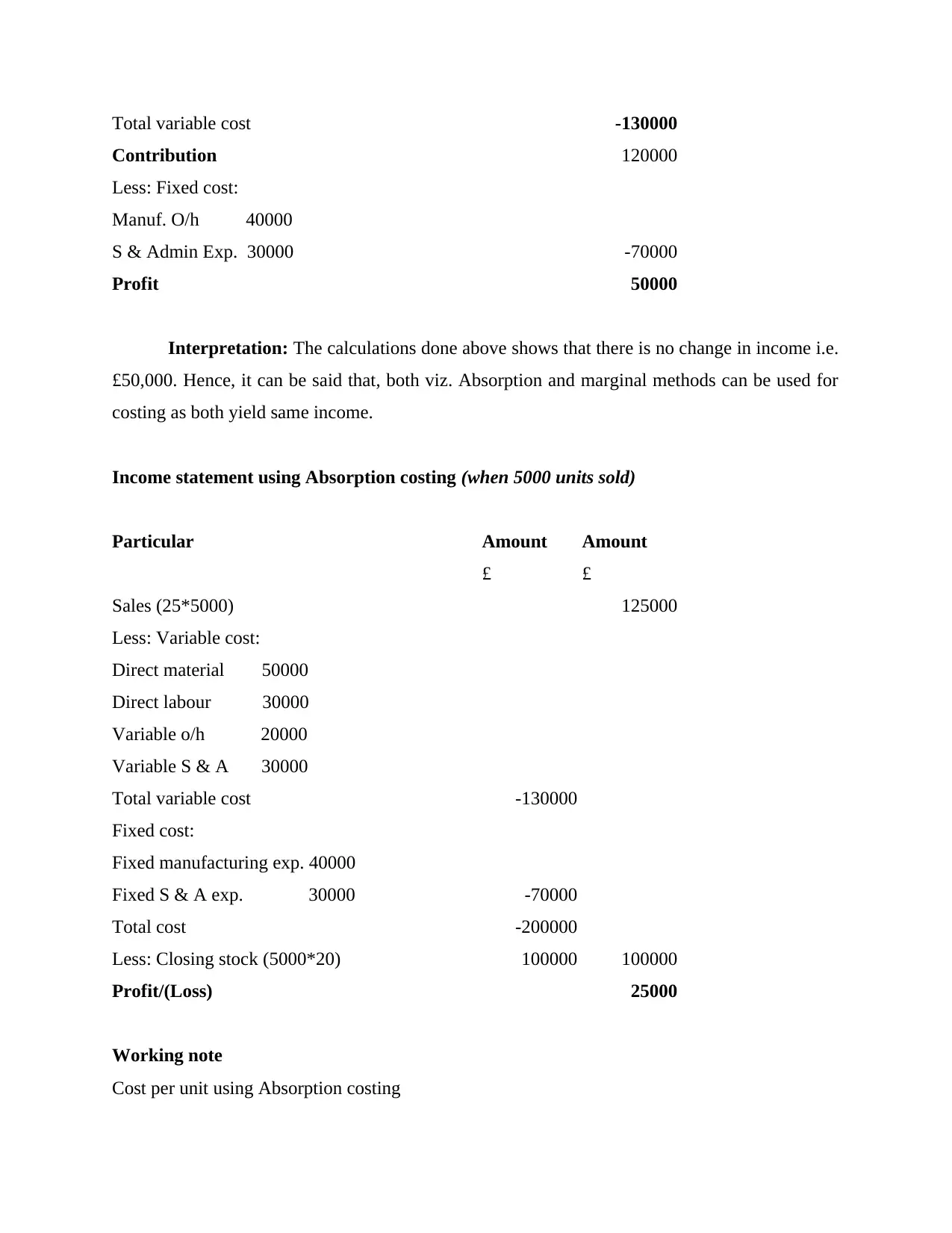

Contribution 120000

Less: Fixed cost:

Manuf. O/h 40000

S & Admin Exp. 30000 -70000

Profit 50000

Interpretation: The calculations done above shows that there is no change in income i.e.

£50,000. Hence, it can be said that, both viz. Absorption and marginal methods can be used for

costing as both yield same income.

Income statement using Absorption costing (when 5000 units sold)

Particular Amount Amount

£ £

Sales (25*5000) 125000

Less: Variable cost:

Direct material 50000

Direct labour 30000

Variable o/h 20000

Variable S & A 30000

Total variable cost -130000

Fixed cost:

Fixed manufacturing exp. 40000

Fixed S & A exp. 30000 -70000

Total cost -200000

Less: Closing stock (5000*20) 100000 100000

Profit/(Loss) 25000

Working note

Cost per unit using Absorption costing

Contribution 120000

Less: Fixed cost:

Manuf. O/h 40000

S & Admin Exp. 30000 -70000

Profit 50000

Interpretation: The calculations done above shows that there is no change in income i.e.

£50,000. Hence, it can be said that, both viz. Absorption and marginal methods can be used for

costing as both yield same income.

Income statement using Absorption costing (when 5000 units sold)

Particular Amount Amount

£ £

Sales (25*5000) 125000

Less: Variable cost:

Direct material 50000

Direct labour 30000

Variable o/h 20000

Variable S & A 30000

Total variable cost -130000

Fixed cost:

Fixed manufacturing exp. 40000

Fixed S & A exp. 30000 -70000

Total cost -200000

Less: Closing stock (5000*20) 100000 100000

Profit/(Loss) 25000

Working note

Cost per unit using Absorption costing

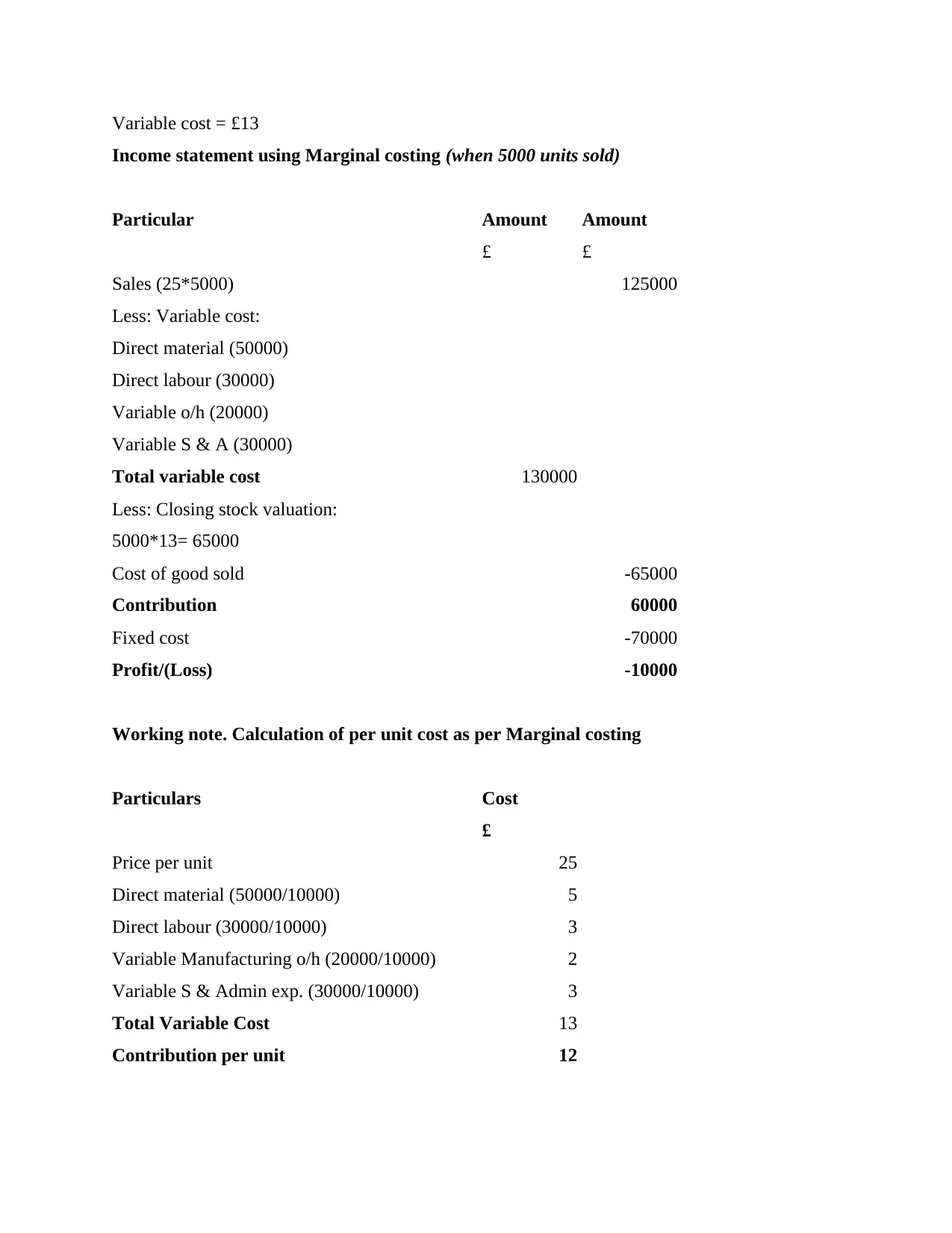

Variable cost = £13

Income statement using Marginal costing (when 5000 units sold)

Particular Amount Amount

£ £

Sales (25*5000) 125000

Less: Variable cost:

Direct material (50000)

Direct labour (30000)

Variable o/h (20000)

Variable S & A (30000)

Total variable cost 130000

Less: Closing stock valuation:

5000*13= 65000

Cost of good sold -65000

Contribution 60000

Fixed cost -70000

Profit/(Loss) -10000

Working note. Calculation of per unit cost as per Marginal costing

Particulars Cost

£

Price per unit 25

Direct material (50000/10000) 5

Direct labour (30000/10000) 3

Variable Manufacturing o/h (20000/10000) 2

Variable S & Admin exp. (30000/10000) 3

Total Variable Cost 13

Contribution per unit 12

Income statement using Marginal costing (when 5000 units sold)

Particular Amount Amount

£ £

Sales (25*5000) 125000

Less: Variable cost:

Direct material (50000)

Direct labour (30000)

Variable o/h (20000)

Variable S & A (30000)

Total variable cost 130000

Less: Closing stock valuation:

5000*13= 65000

Cost of good sold -65000

Contribution 60000

Fixed cost -70000

Profit/(Loss) -10000

Working note. Calculation of per unit cost as per Marginal costing

Particulars Cost

£

Price per unit 25

Direct material (50000/10000) 5

Direct labour (30000/10000) 3

Variable Manufacturing o/h (20000/10000) 2

Variable S & Admin exp. (30000/10000) 3

Total Variable Cost 13

Contribution per unit 12

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

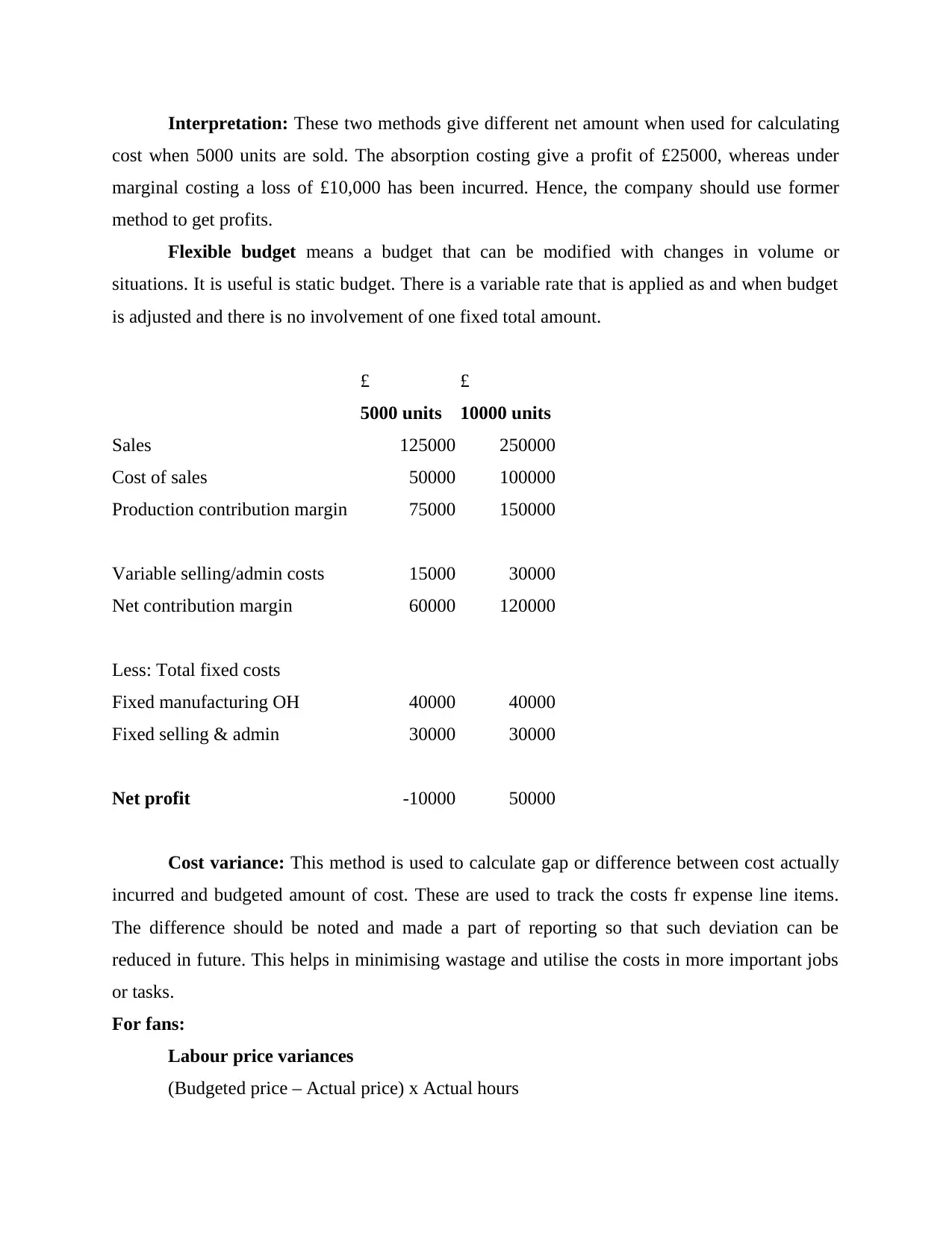

Interpretation: These two methods give different net amount when used for calculating

cost when 5000 units are sold. The absorption costing give a profit of £25000, whereas under

marginal costing a loss of £10,000 has been incurred. Hence, the company should use former

method to get profits.

Flexible budget means a budget that can be modified with changes in volume or

situations. It is useful is static budget. There is a variable rate that is applied as and when budget

is adjusted and there is no involvement of one fixed total amount.

£ £

5000 units 10000 units

Sales 125000 250000

Cost of sales 50000 100000

Production contribution margin 75000 150000

Variable selling/admin costs 15000 30000

Net contribution margin 60000 120000

Less: Total fixed costs

Fixed manufacturing OH 40000 40000

Fixed selling & admin 30000 30000

Net profit -10000 50000

Cost variance: This method is used to calculate gap or difference between cost actually

incurred and budgeted amount of cost. These are used to track the costs fr expense line items.

The difference should be noted and made a part of reporting so that such deviation can be

reduced in future. This helps in minimising wastage and utilise the costs in more important jobs

or tasks.

For fans:

Labour price variances

(Budgeted price – Actual price) x Actual hours

cost when 5000 units are sold. The absorption costing give a profit of £25000, whereas under

marginal costing a loss of £10,000 has been incurred. Hence, the company should use former

method to get profits.

Flexible budget means a budget that can be modified with changes in volume or

situations. It is useful is static budget. There is a variable rate that is applied as and when budget

is adjusted and there is no involvement of one fixed total amount.

£ £

5000 units 10000 units

Sales 125000 250000

Cost of sales 50000 100000

Production contribution margin 75000 150000

Variable selling/admin costs 15000 30000

Net contribution margin 60000 120000

Less: Total fixed costs

Fixed manufacturing OH 40000 40000

Fixed selling & admin 30000 30000

Net profit -10000 50000

Cost variance: This method is used to calculate gap or difference between cost actually

incurred and budgeted amount of cost. These are used to track the costs fr expense line items.

The difference should be noted and made a part of reporting so that such deviation can be

reduced in future. This helps in minimising wastage and utilise the costs in more important jobs

or tasks.

For fans:

Labour price variances

(Budgeted price – Actual price) x Actual hours

(5 – 5.20) x 3400

= -680 Unfavourable

Labour usage variance

(Budgeted Hours – Actual Hours) x Budgeted Price

(3000-3400) x 5

= -2000 Unfavourable

For packaging boxes:

Material Price Variances

(Budgeted price – Actual price) x Actual usage

(10 – 9.5) x 2200

= 1100 Favourable

Material usage variance

(Budgeted Use – Actual Use) x Budgeted Price

(2000 – 2200) x 10

= -2000 Unfavourable

Actual costing system: It is a process of recording product cost which is based on

various factors such as actual cost of materials, actual cost of labour, and actual overhead costs.

Along with this, the main concept of actual costing system is they used only actual cost and

allocate base experienced.

Normal costing system: In this system includes all those cost which helps in making a

product such as material cost, actual direct cost and manufacturing overhead. The key point of

normal costing system is to find the overall cost of particular product which use in making up the

product.

Standard costing system: It is a tool which use in preparing budget, managing and

controlling cost, and also to evaluate it for measuring performance. Along with this, standard

costing system main motive is to evaluate the different cost such as standard and actual for

maintaining the productivity of their organisation.

Job costing: This costing helps in determining the manufacturing costs by categorised it

in three parts such as overhead, direct material and direct labor cost for estimating its actual

value. Also it is a process of keeping an account in the form of direct cost and indirect cost.

= -680 Unfavourable

Labour usage variance

(Budgeted Hours – Actual Hours) x Budgeted Price

(3000-3400) x 5

= -2000 Unfavourable

For packaging boxes:

Material Price Variances

(Budgeted price – Actual price) x Actual usage

(10 – 9.5) x 2200

= 1100 Favourable

Material usage variance

(Budgeted Use – Actual Use) x Budgeted Price

(2000 – 2200) x 10

= -2000 Unfavourable

Actual costing system: It is a process of recording product cost which is based on

various factors such as actual cost of materials, actual cost of labour, and actual overhead costs.

Along with this, the main concept of actual costing system is they used only actual cost and

allocate base experienced.

Normal costing system: In this system includes all those cost which helps in making a

product such as material cost, actual direct cost and manufacturing overhead. The key point of

normal costing system is to find the overall cost of particular product which use in making up the

product.

Standard costing system: It is a tool which use in preparing budget, managing and

controlling cost, and also to evaluate it for measuring performance. Along with this, standard

costing system main motive is to evaluate the different cost such as standard and actual for

maintaining the productivity of their organisation.

Job costing: This costing helps in determining the manufacturing costs by categorised it

in three parts such as overhead, direct material and direct labor cost for estimating its actual

value. Also it is a process of keeping an account in the form of direct cost and indirect cost.

Process costing: It is a cost accounting method in which they determine a cost of product

at each and every stage. This method is opt by Factories and Industries where they standardize

their products and make it into the final product.

Batch costing: In this method, same identical product should be taken but their batch is

differ from its manufacturing size. Along with this, it is some where similar with job costing.

Contract costing: This costing is mostly used in civil construction, engineering projects,

construction of bridges and so on. Contract costing method is applying when specific time

should be taken for completing it accordingly.

SWOT analysis

Strength: Financial sound. Weakness: Failure to adopt competitors

strategy.

Opportunities: Expansion at global level. Threats: High competition from new

companies.

Management accounting provides various techniques that are used for calculations so that

accurate financial statements can be prepared. Further, these help analysis of costs and its impact

on business activities. UK Financial Consultants Ltd. Can use methods of management

accounting for preparing balance sheet, income statement etc. This will enhance quality of

reports and information that will be presented to internal management and investors for making

informed decisions (Wickramasinghe and Alawattage, 2012).

TASK 3

P4 Advantages and disadvantages of different types of planning tools used for budgetary control

Budgetary control refers to the procedure through which financial objectives of company

are formulated by evaluated budget of previous years. It can be said that leaders and managers of

business organisations are monitoring operational activity related to finance and then control it

by adopting this technique. It can be said that this control in business activities helps an

organisation in enhancing their business growth. This is effectively done by monitoring

operational activities which maximises their profits as well. The specific technique helps an

company in forecasting their income and expenses. Along with this, budgetary control is also

used by business organisations in evaluating financial positions for enhancing their knowledge

at each and every stage. This method is opt by Factories and Industries where they standardize

their products and make it into the final product.

Batch costing: In this method, same identical product should be taken but their batch is

differ from its manufacturing size. Along with this, it is some where similar with job costing.

Contract costing: This costing is mostly used in civil construction, engineering projects,

construction of bridges and so on. Contract costing method is applying when specific time

should be taken for completing it accordingly.

SWOT analysis

Strength: Financial sound. Weakness: Failure to adopt competitors

strategy.

Opportunities: Expansion at global level. Threats: High competition from new

companies.

Management accounting provides various techniques that are used for calculations so that

accurate financial statements can be prepared. Further, these help analysis of costs and its impact

on business activities. UK Financial Consultants Ltd. Can use methods of management

accounting for preparing balance sheet, income statement etc. This will enhance quality of

reports and information that will be presented to internal management and investors for making

informed decisions (Wickramasinghe and Alawattage, 2012).

TASK 3

P4 Advantages and disadvantages of different types of planning tools used for budgetary control

Budgetary control refers to the procedure through which financial objectives of company

are formulated by evaluated budget of previous years. It can be said that leaders and managers of

business organisations are monitoring operational activity related to finance and then control it

by adopting this technique. It can be said that this control in business activities helps an

organisation in enhancing their business growth. This is effectively done by monitoring

operational activities which maximises their profits as well. The specific technique helps an

company in forecasting their income and expenses. Along with this, budgetary control is also

used by business organisations in evaluating financial positions for enhancing their knowledge

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

on competitive market. In context to UK Financial Consultants Ltd. , its leaders are mainly

identifying different elements of monitoring and controlling financial operations. Advantages

and disadvantages of different planning tool for budgetary control are described as:

Contingency Planning- This planning tool is mainly used to control risk which develops

because of uncertain situations at the time of implementing operational activities at organisation.

Contingency planning tool helps business organisation in creating various strategies, tools and

plans that supports in overcoming and handling different situation. In relation to UK Financial

Consultants Ltd., management team of this company is using this specific planning tool for

formulating various policies, plans and strategies so that they can handle risky situations and also

reduces impact of non-adjustable situations at workplace (Schaltegger and Csutora, 2012).

Advantages

The first and foremost advantage of this planning tool is that it reduces risk of uncertain

situations which might occur at workplace. This is effectively done by planning effective

strategies and plans.

Along with this, this planning tool helps company in formulating corrective steps so that

business problem can be resolved effectively. It also guides management team that how

they can handle different but uncertain organisational situation. It also provides solutions

for the same.

Disadvantages

It has been analysed that main drawback of this contingency planning is that the company

might face difficult situations as excessive planning includes more interaction of

employees during planning or strategy formulation. This might create conflicts among

team leaders as they supports only their provided suggestions.

The next disadvantage of this planning tool is that it is time consuming method. This is

because every planning is done evaluating each and every fact which consumes excessive

time of individuals. Along with this, it also requires huge amount of money so that they

could cover each area effectively.

Flexible Budget- It is another effective tool which is used by business organisations for

making valuable changes in overall budget. In context to UK Financial Consultants Ltd., its

manager is using this tool in their company for controlling budget effectively. This kind of

identifying different elements of monitoring and controlling financial operations. Advantages

and disadvantages of different planning tool for budgetary control are described as:

Contingency Planning- This planning tool is mainly used to control risk which develops

because of uncertain situations at the time of implementing operational activities at organisation.

Contingency planning tool helps business organisation in creating various strategies, tools and

plans that supports in overcoming and handling different situation. In relation to UK Financial

Consultants Ltd., management team of this company is using this specific planning tool for

formulating various policies, plans and strategies so that they can handle risky situations and also

reduces impact of non-adjustable situations at workplace (Schaltegger and Csutora, 2012).

Advantages

The first and foremost advantage of this planning tool is that it reduces risk of uncertain

situations which might occur at workplace. This is effectively done by planning effective

strategies and plans.

Along with this, this planning tool helps company in formulating corrective steps so that

business problem can be resolved effectively. It also guides management team that how

they can handle different but uncertain organisational situation. It also provides solutions

for the same.

Disadvantages

It has been analysed that main drawback of this contingency planning is that the company

might face difficult situations as excessive planning includes more interaction of

employees during planning or strategy formulation. This might create conflicts among

team leaders as they supports only their provided suggestions.

The next disadvantage of this planning tool is that it is time consuming method. This is

because every planning is done evaluating each and every fact which consumes excessive

time of individuals. Along with this, it also requires huge amount of money so that they

could cover each area effectively.

Flexible Budget- It is another effective tool which is used by business organisations for

making valuable changes in overall budget. In context to UK Financial Consultants Ltd., its

manager is using this tool in their company for controlling budget effectively. This kind of

planning tool also helps company in deciding revenue and expenses of company. Further, it can

be said that this flexible budget helps businesses in evaluating key successful and unsuccessful

operational areas of finance department. It can be said that with the help of this budget manager

of UK Financial Consultants Ltd. Can easily executes changes at workplace effectively without

facing much difficulty.

Advantages

Main advantage of flexible budget is that it helps in co-operating with different business

activities. It also provides irregular earning to company. This is because their managers

grabs advantage at convenient and feasible time. Along with this, it also helps them min

us8ing funds at most needed time that can save them from big uncertain situation

(Chenhall, and Moers, 2015).

Another advantage of this budget is that it provides effective results to the UK Financial

Consultants Ltd. This is because, management of this company evaluates each and every

aspect at the time of preparing this budget. As a result, company gains profits rapidly.

Disadvantages

Flexible budget are more confusing because they includes numerous of variables. Thus,

its difficult for management team to cover each and every thing in single budget. As a

result, it creates difficulty for management team to rely on the single budget.

Forecasting Tools- This type of planning tool basically focuses on making prediction and

assumption for future by evaluating current and previous budget records of company. It can be

said that this financial tool helps company in enhancing their financial performance and make

future plan for the same. In context to UK Financial Consultants Ltd., it can be said that its

managers are using this forecasting technique which helps and guides them in forecasting future

estimation on needs and requirements of company.

Advantages

The main advantage for forecasting tool for UK Financial Consultants Ltd., is that it

satisfies clients at highest level as it provides them rough estimation in advance which is

completely based on budgetary report.

At next, another advantage of this planning tool states that it improves decision making

power of managers as well as leaders effectively. It also helps them in formulation and

implementing plans, procedures and strategies at workplace in effective manner.

be said that this flexible budget helps businesses in evaluating key successful and unsuccessful

operational areas of finance department. It can be said that with the help of this budget manager

of UK Financial Consultants Ltd. Can easily executes changes at workplace effectively without

facing much difficulty.

Advantages

Main advantage of flexible budget is that it helps in co-operating with different business

activities. It also provides irregular earning to company. This is because their managers

grabs advantage at convenient and feasible time. Along with this, it also helps them min

us8ing funds at most needed time that can save them from big uncertain situation

(Chenhall, and Moers, 2015).

Another advantage of this budget is that it provides effective results to the UK Financial

Consultants Ltd. This is because, management of this company evaluates each and every

aspect at the time of preparing this budget. As a result, company gains profits rapidly.

Disadvantages

Flexible budget are more confusing because they includes numerous of variables. Thus,

its difficult for management team to cover each and every thing in single budget. As a

result, it creates difficulty for management team to rely on the single budget.

Forecasting Tools- This type of planning tool basically focuses on making prediction and

assumption for future by evaluating current and previous budget records of company. It can be

said that this financial tool helps company in enhancing their financial performance and make

future plan for the same. In context to UK Financial Consultants Ltd., it can be said that its

managers are using this forecasting technique which helps and guides them in forecasting future

estimation on needs and requirements of company.

Advantages

The main advantage for forecasting tool for UK Financial Consultants Ltd., is that it

satisfies clients at highest level as it provides them rough estimation in advance which is

completely based on budgetary report.

At next, another advantage of this planning tool states that it improves decision making

power of managers as well as leaders effectively. It also helps them in formulation and

implementing plans, procedures and strategies at workplace in effective manner.

Disadvantage

The information that is collected through several department of UK Financial

Consultancy Ltd may not proof adequate for formulating effective strategies as well as

plans regarding the actions to be taken in future.

In case of implementing budgetary control UK Financial Consultancy Ltd is required to

allocate resources and personnel for effective budget control. But when workforce is

limited it become difficult as company have to divert employees and payroll hours from

activities which support them in producing income.

TASK 4

P5. Compare how organisations are adapting management accounting systems to respond to

financial problems

Financial problems refers to situations which impact the financial viability in a significant

and negative way. The after effect can be for number of years which may cause huge financial

loss. Every business organization suffer from such difficulties during the lifespan of the business.

Such circumstances can be made good by formulating effective plans, policies and strategies

together with, making adjustments in procedures as per the situation demands. UK Financial

Consultants Ltd. Can assess its financial position and viability so that desired results can be

achieved and sustain for a long term by resolving the problems (Arroyo, 2012). The common

financial problems that a business face irrespective of its nature are as follows:

Cash flow: It is associated with inflow and outflow of cash in the business. Cash is a

vital requirement which should be managed in an effective way so that entity does not

run out of it. There may arise situations such as failure to repay obligation or liabilities,

purchasing of assets, blockage of funds etc. These may have major effect on operations

and profits of business. Hence, UK Financial Consultants Ltd. Is a growing company

which needs good amount of working capital and other resources to conduct business

activities. Further, its face credit risk at high level.

Risk management: A business has to make strategies and plans to survive in the cut

throat competition. Further, all the risks that could affect entity should be assessed and

evaluated in order to minimise their impact. Risks should be balanced as higher the risks

The information that is collected through several department of UK Financial

Consultancy Ltd may not proof adequate for formulating effective strategies as well as

plans regarding the actions to be taken in future.

In case of implementing budgetary control UK Financial Consultancy Ltd is required to

allocate resources and personnel for effective budget control. But when workforce is

limited it become difficult as company have to divert employees and payroll hours from

activities which support them in producing income.

TASK 4

P5. Compare how organisations are adapting management accounting systems to respond to

financial problems

Financial problems refers to situations which impact the financial viability in a significant

and negative way. The after effect can be for number of years which may cause huge financial

loss. Every business organization suffer from such difficulties during the lifespan of the business.

Such circumstances can be made good by formulating effective plans, policies and strategies

together with, making adjustments in procedures as per the situation demands. UK Financial

Consultants Ltd. Can assess its financial position and viability so that desired results can be

achieved and sustain for a long term by resolving the problems (Arroyo, 2012). The common

financial problems that a business face irrespective of its nature are as follows:

Cash flow: It is associated with inflow and outflow of cash in the business. Cash is a

vital requirement which should be managed in an effective way so that entity does not

run out of it. There may arise situations such as failure to repay obligation or liabilities,

purchasing of assets, blockage of funds etc. These may have major effect on operations

and profits of business. Hence, UK Financial Consultants Ltd. Is a growing company

which needs good amount of working capital and other resources to conduct business

activities. Further, its face credit risk at high level.

Risk management: A business has to make strategies and plans to survive in the cut

throat competition. Further, all the risks that could affect entity should be assessed and

evaluated in order to minimise their impact. Risks should be balanced as higher the risks

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

higher the chances of failure of business. UK Financial Consultants Ltd. Should hire an

expert to evaluate the degree of risks on the business for reversing their impact and create

opportunities for future expansion and success.

Capital assets: A business has day-to-day work or tasks which should be achieved.

There comes a huge requirement of working capital in order to accomplish such tasks. It

is calculated by deducting current liabilities from current assets. These should be a

sufficient amount of working capital which should be utilised in an efficient manner. UK

Financial Consultants Ltd. Has been suffering from debt issues due to insufficient

working capital, hence, it should have strong rules and procedures for its application.

Financial governance: It is the procedures through which a company collects, manages,

monitors and controls information that are important for preparing financial statements. Further,

these can be used to manage the amount of financial transactions, performance, compliance with

legislation, business activities, reporting and disclosures (Strauß,and Zecher, 2013).

Management accounting approach: There are different techniques which are used to

resolve problems arising in the business of company. Some of the approaches that can be used by

UK Financial Consultants Ltd. Are as follows:

KPI: It is the abbreviated form of Key Performance Indicator which is opted and applied

for assessing strategies and procedures by comparing with other business organizations.

The main aim of KPI is to make the entity capable to accomplish its goals and objectives.

Benchmarking: This technique is used for to evaluate co-ordination and efficiency with

the existing competition. This helps in improving performance by addressing challenges.

Comparison between UK Financial Consultants Ltd. And Ultra Financial Services

Basis UK Financial Consultants Ltd. Ultra Financial Services

Problem The company faces difficulties in

meeting financial obligations.

Further, working capital is also a

huge problem and require effective

management. Moreover, company is

facing problem with in managing

cash in order to meet day-to-day

Ultra Financial services problems

of employee turnover, due to

which it is failing to manage its

resources. Further, it has not

utilised its funds in an optimum

manner which can cause long

expert to evaluate the degree of risks on the business for reversing their impact and create

opportunities for future expansion and success.

Capital assets: A business has day-to-day work or tasks which should be achieved.

There comes a huge requirement of working capital in order to accomplish such tasks. It

is calculated by deducting current liabilities from current assets. These should be a

sufficient amount of working capital which should be utilised in an efficient manner. UK

Financial Consultants Ltd. Has been suffering from debt issues due to insufficient

working capital, hence, it should have strong rules and procedures for its application.

Financial governance: It is the procedures through which a company collects, manages,

monitors and controls information that are important for preparing financial statements. Further,

these can be used to manage the amount of financial transactions, performance, compliance with

legislation, business activities, reporting and disclosures (Strauß,and Zecher, 2013).

Management accounting approach: There are different techniques which are used to

resolve problems arising in the business of company. Some of the approaches that can be used by

UK Financial Consultants Ltd. Are as follows:

KPI: It is the abbreviated form of Key Performance Indicator which is opted and applied

for assessing strategies and procedures by comparing with other business organizations.

The main aim of KPI is to make the entity capable to accomplish its goals and objectives.

Benchmarking: This technique is used for to evaluate co-ordination and efficiency with

the existing competition. This helps in improving performance by addressing challenges.

Comparison between UK Financial Consultants Ltd. And Ultra Financial Services

Basis UK Financial Consultants Ltd. Ultra Financial Services

Problem The company faces difficulties in

meeting financial obligations.

Further, working capital is also a

huge problem and require effective

management. Moreover, company is

facing problem with in managing

cash in order to meet day-to-day

Ultra Financial services problems

of employee turnover, due to

which it is failing to manage its

resources. Further, it has not

utilised its funds in an optimum

manner which can cause long

activities. Apart from this, company

has failed to manage its risks in a

way as to reducing the effects.

term effect.

Approach The company can use variety of

techniques to overcome the issued

faced by it. It can adopt KPI to

assess the viability of strategies

which are formulated by its

competitors.

Ultra Financial services can use

benchmarking technique to form

co-ordination for minimising risk

of employees turnover and fund

management.

CONCLUSION

From the above report, it has been concluded that, management accounting is a branch of

accounting that deals with non-financial information and shows its impact on business

operations. Further, there are various techniques and methods that should be used according to

situation in order to attain goals and objectives by removing the problems. Along with this,

importance of reporting should also be understood so that each information can be included

before presenting investors. Furthermore, system of management accounting should be used so

that cost element of managerial activities can be disclosed in the financial statements.

REFERENCES

Books & Journals:

Anandarajan, M., Anandarajan, A. and Srinivasan, C.A. eds., 2012. Business intelligence

techniques: a perspective from accounting and finance. Springer Science & Business

Media.

Arroyo, P., 2012. Management accounting change and sustainability: an institutional

approach. Journal of Accounting & Organizational Change, 8(3), pp.286-309.

has failed to manage its risks in a

way as to reducing the effects.

term effect.

Approach The company can use variety of

techniques to overcome the issued

faced by it. It can adopt KPI to

assess the viability of strategies

which are formulated by its

competitors.

Ultra Financial services can use

benchmarking technique to form

co-ordination for minimising risk

of employees turnover and fund

management.

CONCLUSION

From the above report, it has been concluded that, management accounting is a branch of

accounting that deals with non-financial information and shows its impact on business

operations. Further, there are various techniques and methods that should be used according to

situation in order to attain goals and objectives by removing the problems. Along with this,

importance of reporting should also be understood so that each information can be included

before presenting investors. Furthermore, system of management accounting should be used so

that cost element of managerial activities can be disclosed in the financial statements.

REFERENCES

Books & Journals:

Anandarajan, M., Anandarajan, A. and Srinivasan, C.A. eds., 2012. Business intelligence

techniques: a perspective from accounting and finance. Springer Science & Business

Media.

Arroyo, P., 2012. Management accounting change and sustainability: an institutional

approach. Journal of Accounting & Organizational Change, 8(3), pp.286-309.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.