Work Contract in Spain: Employment Contract

VerifiedAdded on 2023/01/16

|12

|3846

|60

AI Summary

This document is an employment contract for an Administrative Assistant in Spain. It includes details such as the site of employment, contract duration, employee's position, salary, working hours, overtime pay, leave entitlements, and transportation provisions. It also discusses the difference between Spanish and UK work contracts. The document explains the calculation of base salary in Spain, including factors such as complemento absorbible and seniority. It provides steps to prepare the payroll for an Administrative Assistant and a Visual Designer, including understanding labor laws, employment contracts, contract registration, probationary period, overtime compensation, holidays, and pay for sick leave.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management International

Financial Services

Financial Services

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

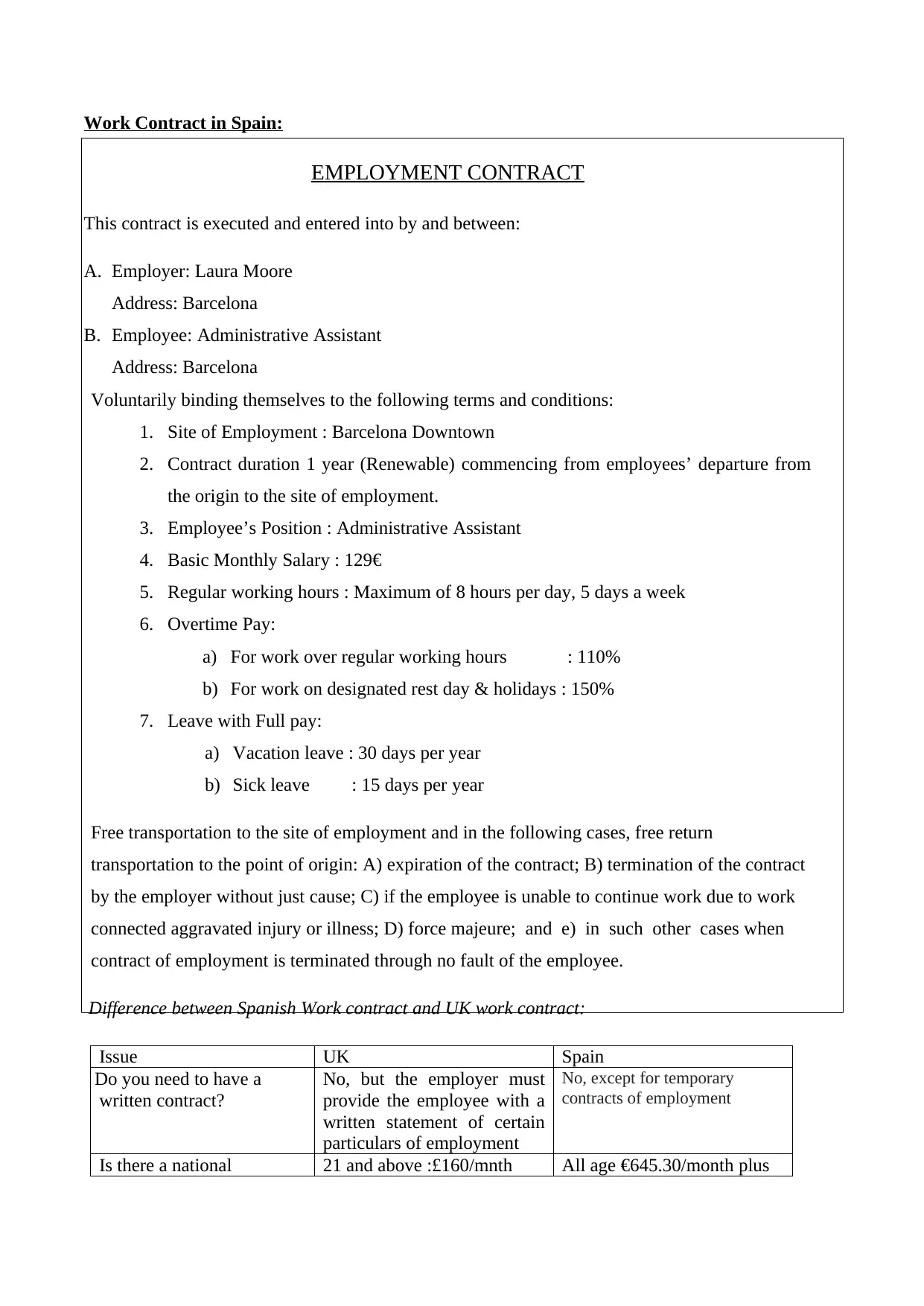

Work Contract in Spain:

EMPLOYMENT CONTRACT

This contract is executed and entered into by and between:

A. Employer: Laura Moore

Address: Barcelona

B. Employee: Administrative Assistant

Address: Barcelona

Voluntarily binding themselves to the following terms and conditions:

1. Site of Employment : Barcelona Downtown

2. Contract duration 1 year (Renewable) commencing from employees’ departure from

the origin to the site of employment.

3. Employee’s Position : Administrative Assistant

4. Basic Monthly Salary : 129€

5. Regular working hours : Maximum of 8 hours per day, 5 days a week

6. Overtime Pay:

a) For work over regular working hours : 110%

b) For work on designated rest day & holidays : 150%

7. Leave with Full pay:

a) Vacation leave : 30 days per year

b) Sick leave : 15 days per year

Free transportation to the site of employment and in the following cases, free return

transportation to the point of origin: A) expiration of the contract; B) termination of the contract

by the employer without just cause; C) if the employee is unable to continue work due to work

connected aggravated injury or illness; D) force majeure; and e) in such other cases when

contract of employment is terminated through no fault of the employee.

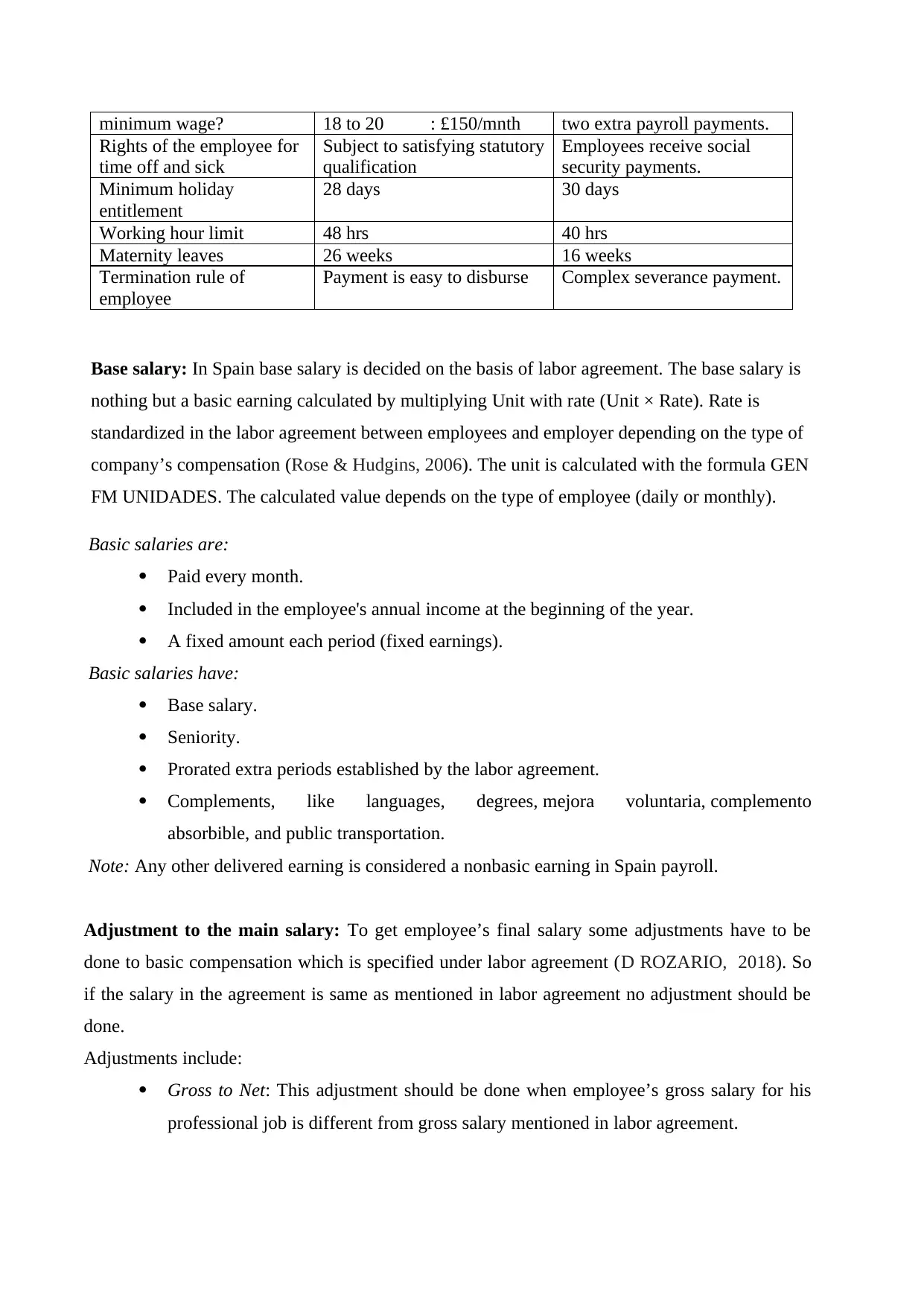

Difference between Spanish Work contract and UK work contract:

Issue UK Spain

Do you need to have a

written contract?

No, but the employer must

provide the employee with a

written statement of certain

particulars of employment

No, except for temporary

contracts of employment

Is there a national 21 and above :£160/mnth All age €645.30/month plus

EMPLOYMENT CONTRACT

This contract is executed and entered into by and between:

A. Employer: Laura Moore

Address: Barcelona

B. Employee: Administrative Assistant

Address: Barcelona

Voluntarily binding themselves to the following terms and conditions:

1. Site of Employment : Barcelona Downtown

2. Contract duration 1 year (Renewable) commencing from employees’ departure from

the origin to the site of employment.

3. Employee’s Position : Administrative Assistant

4. Basic Monthly Salary : 129€

5. Regular working hours : Maximum of 8 hours per day, 5 days a week

6. Overtime Pay:

a) For work over regular working hours : 110%

b) For work on designated rest day & holidays : 150%

7. Leave with Full pay:

a) Vacation leave : 30 days per year

b) Sick leave : 15 days per year

Free transportation to the site of employment and in the following cases, free return

transportation to the point of origin: A) expiration of the contract; B) termination of the contract

by the employer without just cause; C) if the employee is unable to continue work due to work

connected aggravated injury or illness; D) force majeure; and e) in such other cases when

contract of employment is terminated through no fault of the employee.

Difference between Spanish Work contract and UK work contract:

Issue UK Spain

Do you need to have a

written contract?

No, but the employer must

provide the employee with a

written statement of certain

particulars of employment

No, except for temporary

contracts of employment

Is there a national 21 and above :£160/mnth All age €645.30/month plus

minimum wage? 18 to 20 : £150/mnth two extra payroll payments.

Rights of the employee for

time off and sick

Subject to satisfying statutory

qualification

Employees receive social

security payments.

Minimum holiday

entitlement

28 days 30 days

Working hour limit 48 hrs 40 hrs

Maternity leaves 26 weeks 16 weeks

Termination rule of

employee

Payment is easy to disburse Complex severance payment.

Base salary: In Spain base salary is decided on the basis of labor agreement. The base salary is

nothing but a basic earning calculated by multiplying Unit with rate (Unit × Rate). Rate is

standardized in the labor agreement between employees and employer depending on the type of

company’s compensation (Rose & Hudgins, 2006). The unit is calculated with the formula GEN

FM UNIDADES. The calculated value depends on the type of employee (daily or monthly).

Basic salaries are:

Paid every month.

Included in the employee's annual income at the beginning of the year.

A fixed amount each period (fixed earnings).

Basic salaries have:

Base salary.

Seniority.

Prorated extra periods established by the labor agreement.

Complements, like languages, degrees, mejora voluntaria, complemento

absorbible, and public transportation.

Note: Any other delivered earning is considered a nonbasic earning in Spain payroll.

Adjustment to the main salary: To get employee’s final salary some adjustments have to be

done to basic compensation which is specified under labor agreement (D ROZARIO, 2018). So

if the salary in the agreement is same as mentioned in labor agreement no adjustment should be

done.

Adjustments include:

Gross to Net: This adjustment should be done when employee’s gross salary for his

professional job is different from gross salary mentioned in labor agreement.

Rights of the employee for

time off and sick

Subject to satisfying statutory

qualification

Employees receive social

security payments.

Minimum holiday

entitlement

28 days 30 days

Working hour limit 48 hrs 40 hrs

Maternity leaves 26 weeks 16 weeks

Termination rule of

employee

Payment is easy to disburse Complex severance payment.

Base salary: In Spain base salary is decided on the basis of labor agreement. The base salary is

nothing but a basic earning calculated by multiplying Unit with rate (Unit × Rate). Rate is

standardized in the labor agreement between employees and employer depending on the type of

company’s compensation (Rose & Hudgins, 2006). The unit is calculated with the formula GEN

FM UNIDADES. The calculated value depends on the type of employee (daily or monthly).

Basic salaries are:

Paid every month.

Included in the employee's annual income at the beginning of the year.

A fixed amount each period (fixed earnings).

Basic salaries have:

Base salary.

Seniority.

Prorated extra periods established by the labor agreement.

Complements, like languages, degrees, mejora voluntaria, complemento

absorbible, and public transportation.

Note: Any other delivered earning is considered a nonbasic earning in Spain payroll.

Adjustment to the main salary: To get employee’s final salary some adjustments have to be

done to basic compensation which is specified under labor agreement (D ROZARIO, 2018). So

if the salary in the agreement is same as mentioned in labor agreement no adjustment should be

done.

Adjustments include:

Gross to Net: This adjustment should be done when employee’s gross salary for his

professional job is different from gross salary mentioned in labor agreement.

Net to Gross: This adjustment has to be done when the calculation of employee’s

annual gross salary is required.

Factors effecting base salary:

1. Complemento Absorbible: This can be defined by taking difference between real gross

salary and total salary receives in their professional category. While in case of net

guarantee, complement absorbable is defined as the difference between the calculated

gross earnings and the total earnings on the basis of professional job role of an

employee.

How to calculate complemento absorbible: It can be calculated by multiplying Unit with

Rate. Here Unit is defined as no. of days worked in a month and Rate should be taken

from code GEN RC COM ABS EST. Before calculating complemento absorbible,

variable GEN VR TIPO AJ SAL should be avoided. Employees uses the

value BRUTO for calculating gross to net adjustment or NETO for net to gross

adjustments.

2. Seniority: This factor plays a major role in deciding basic pay of an employee. In Spain,

seniority is calculated by subtracting the seniority date from the payroll period to end

date. For modifying the calculation method, a custom duration or formula to calculate

seniority years for a labor agreement on the Labor Agreement - Seniority page should be

specify else change the code of formula CLI FM ANTIG DESDE.

(*Absences can decrease seniority years based on the number of months absent.)

Seniority can be measure in multiples of three years (trienniums) or four

years (cuatrenniums) or as a mixture of years.

The best way to calculate seniority is to add the value with a triennium

or cuatrennium. For example, an employee is getting 20 EUR per month for the first

triennium and 23 EUR per month for the second triennium. So if an employee has six

years of seniority, he would get 43 EUR per month in seniority earnings.

Seniority can be calculated by another method which is a percentage method. In this

method, percentage over the base salary or base salary plus a complement is taken.

For example:

Suppose owner is hiring a programmer of Salary Level 4, salary = 600 EUR/month. The

labor agreement treats seniority as a cuatrennium, which means it should be 4 percent of

the base salary. The programmer has eight years of seniority, which is equal to

two cuatrenniums. His seniority earnings per month have calculated as:

annual gross salary is required.

Factors effecting base salary:

1. Complemento Absorbible: This can be defined by taking difference between real gross

salary and total salary receives in their professional category. While in case of net

guarantee, complement absorbable is defined as the difference between the calculated

gross earnings and the total earnings on the basis of professional job role of an

employee.

How to calculate complemento absorbible: It can be calculated by multiplying Unit with

Rate. Here Unit is defined as no. of days worked in a month and Rate should be taken

from code GEN RC COM ABS EST. Before calculating complemento absorbible,

variable GEN VR TIPO AJ SAL should be avoided. Employees uses the

value BRUTO for calculating gross to net adjustment or NETO for net to gross

adjustments.

2. Seniority: This factor plays a major role in deciding basic pay of an employee. In Spain,

seniority is calculated by subtracting the seniority date from the payroll period to end

date. For modifying the calculation method, a custom duration or formula to calculate

seniority years for a labor agreement on the Labor Agreement - Seniority page should be

specify else change the code of formula CLI FM ANTIG DESDE.

(*Absences can decrease seniority years based on the number of months absent.)

Seniority can be measure in multiples of three years (trienniums) or four

years (cuatrenniums) or as a mixture of years.

The best way to calculate seniority is to add the value with a triennium

or cuatrennium. For example, an employee is getting 20 EUR per month for the first

triennium and 23 EUR per month for the second triennium. So if an employee has six

years of seniority, he would get 43 EUR per month in seniority earnings.

Seniority can be calculated by another method which is a percentage method. In this

method, percentage over the base salary or base salary plus a complement is taken.

For example:

Suppose owner is hiring a programmer of Salary Level 4, salary = 600 EUR/month. The

labor agreement treats seniority as a cuatrennium, which means it should be 4 percent of

the base salary. The programmer has eight years of seniority, which is equal to

two cuatrenniums. His seniority earnings per month have calculated as:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

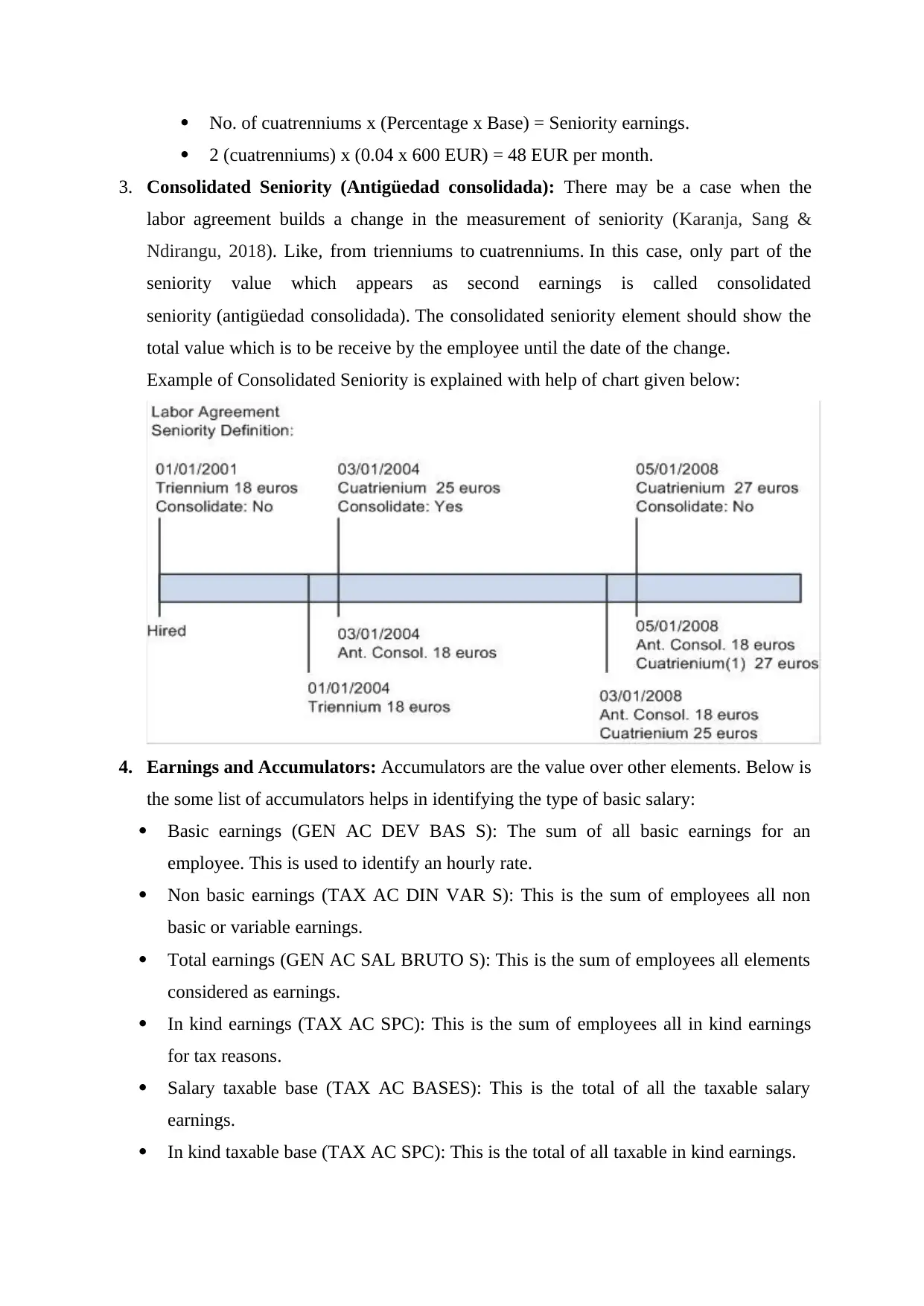

No. of cuatrenniums x (Percentage x Base) = Seniority earnings.

2 (cuatrenniums) x (0.04 x 600 EUR) = 48 EUR per month.

3. Consolidated Seniority (Antigüedad consolidada): There may be a case when the

labor agreement builds a change in the measurement of seniority (Karanja, Sang &

Ndirangu, 2018). Like, from trienniums to cuatrenniums. In this case, only part of the

seniority value which appears as second earnings is called consolidated

seniority (antigüedad consolidada). The consolidated seniority element should show the

total value which is to be receive by the employee until the date of the change.

Example of Consolidated Seniority is explained with help of chart given below:

4. Earnings and Accumulators: Accumulators are the value over other elements. Below is

the some list of accumulators helps in identifying the type of basic salary:

Basic earnings (GEN AC DEV BAS S): The sum of all basic earnings for an

employee. This is used to identify an hourly rate.

Non basic earnings (TAX AC DIN VAR S): This is the sum of employees all non

basic or variable earnings.

Total earnings (GEN AC SAL BRUTO S): This is the sum of employees all elements

considered as earnings.

In kind earnings (TAX AC SPC): This is the sum of employees all in kind earnings

for tax reasons.

Salary taxable base (TAX AC BASES): This is the total of all the taxable salary

earnings.

In kind taxable base (TAX AC SPC): This is the total of all taxable in kind earnings.

2 (cuatrenniums) x (0.04 x 600 EUR) = 48 EUR per month.

3. Consolidated Seniority (Antigüedad consolidada): There may be a case when the

labor agreement builds a change in the measurement of seniority (Karanja, Sang &

Ndirangu, 2018). Like, from trienniums to cuatrenniums. In this case, only part of the

seniority value which appears as second earnings is called consolidated

seniority (antigüedad consolidada). The consolidated seniority element should show the

total value which is to be receive by the employee until the date of the change.

Example of Consolidated Seniority is explained with help of chart given below:

4. Earnings and Accumulators: Accumulators are the value over other elements. Below is

the some list of accumulators helps in identifying the type of basic salary:

Basic earnings (GEN AC DEV BAS S): The sum of all basic earnings for an

employee. This is used to identify an hourly rate.

Non basic earnings (TAX AC DIN VAR S): This is the sum of employees all non

basic or variable earnings.

Total earnings (GEN AC SAL BRUTO S): This is the sum of employees all elements

considered as earnings.

In kind earnings (TAX AC SPC): This is the sum of employees all in kind earnings

for tax reasons.

Salary taxable base (TAX AC BASES): This is the total of all the taxable salary

earnings.

In kind taxable base (TAX AC SPC): This is the total of all taxable in kind earnings.

Employee's Social Security common contribution base (SS AC BSE D S and SS AC

BSE M S): This is the total of all the contribution earnings.

Different steps to follow to prepare the payroll of Administrative Assistant and Visual

designer:

1. Understanding Key Labor Laws: The first step in preparing payroll is to understand

country’s labor laws, standardized by country’s Labor Guide. Administered by

the Ministry of Employment and Social Security, this law highlights the essential

points required for hiring employees. For example, the minimum wage requirement

by the law is €21.84/day and maximum is €655.20 /month, for overtime law has made

regulations that any employee working more than nine hours per day or in excess of

40 hours per week is entitled to overtime pay. Spain’s Labor Guide also details the

areas of employment contracts, collective bargaining agreements and worker’s

compensation. Hence in case of administrator assistant he has 3 months seniority but

as per seniority rule he should complete at least 3 years or trienniums to get seniority

benefits. On the other hand, Visual designer has also not completed 3 years therefore

he is also not covering under seniority benefits. But both are at logical job which is

separate from labor job, hence they should get basic salary higher than labor wages.

2. Employment Contracts: Employee contract is of two types permanent and temporary.

Both types have different regulations and restrictions while calculating net salary.

Below is the explanation of both types:

Permanent or Indefinite Contract: This includes the normal indefinite contract as

well as several types of indefinite contracts with government incentives.

The main characteristics of the normal indefinite contract are:

It is automatically applicable in the absence of any formalized contract type.

Severance pay for improper dismissal is decided to be maximum of 45 days of

salary worked each year; it is liable to paid maximum of 42 months of

equivalent salary.

There are no social security subsidies or any other financial incentives.

Administrative Assistant proposed for permanent contract, so he should get severance pay

for 45 days worked each year.

Temporary Contract: These types of contracts include:

Severance pay for improper dismissal is 33 days of salary for each year

worked with a maximum of 24 months of equivalent salary.

Subsidies of up to 75% from the employer's social security contribution.

BSE M S): This is the total of all the contribution earnings.

Different steps to follow to prepare the payroll of Administrative Assistant and Visual

designer:

1. Understanding Key Labor Laws: The first step in preparing payroll is to understand

country’s labor laws, standardized by country’s Labor Guide. Administered by

the Ministry of Employment and Social Security, this law highlights the essential

points required for hiring employees. For example, the minimum wage requirement

by the law is €21.84/day and maximum is €655.20 /month, for overtime law has made

regulations that any employee working more than nine hours per day or in excess of

40 hours per week is entitled to overtime pay. Spain’s Labor Guide also details the

areas of employment contracts, collective bargaining agreements and worker’s

compensation. Hence in case of administrator assistant he has 3 months seniority but

as per seniority rule he should complete at least 3 years or trienniums to get seniority

benefits. On the other hand, Visual designer has also not completed 3 years therefore

he is also not covering under seniority benefits. But both are at logical job which is

separate from labor job, hence they should get basic salary higher than labor wages.

2. Employment Contracts: Employee contract is of two types permanent and temporary.

Both types have different regulations and restrictions while calculating net salary.

Below is the explanation of both types:

Permanent or Indefinite Contract: This includes the normal indefinite contract as

well as several types of indefinite contracts with government incentives.

The main characteristics of the normal indefinite contract are:

It is automatically applicable in the absence of any formalized contract type.

Severance pay for improper dismissal is decided to be maximum of 45 days of

salary worked each year; it is liable to paid maximum of 42 months of

equivalent salary.

There are no social security subsidies or any other financial incentives.

Administrative Assistant proposed for permanent contract, so he should get severance pay

for 45 days worked each year.

Temporary Contract: These types of contracts include:

Severance pay for improper dismissal is 33 days of salary for each year

worked with a maximum of 24 months of equivalent salary.

Subsidies of up to 75% from the employer's social security contribution.

Tax benefits.

Visual designer is hiring on temporary contract basis, the reason behind this is visual

designer’s nature of work is temporary as they only required at the time of graphic

design of an app, later they don’t have any major role (Chaflekar and et.al., 2018).

3. Contract Registration: It is obligatory for any company to register the employment

contract with social security authorities and the national employment service. Before

the start of employment new contracts and terminations are necessary to be registered

with social security as well as with the Public Employment Service within 6 days.

4. Probationary Period: Qualified technical personnel have a 6 months probationary

period; and for rest of employees its 2 months (for small size companies having 25

employees or less, the probationary period can be up to 3 months). During this time,

either the employer or employee can terminate employment without prior notice or

reason and without the need for the employer to pay severance. Both the employees

have technical nature of job hence their probationary period can be up to 6 months.

5. Overtime Compensation: Spain workers are allowed to work a maximum of 80 hours

of overtime per year but immediate damage repair is exceptional (Blyton & Morris,

2017). Therefore taking average they can work 6 hours of overtime per month.

Overtime pay is taxable and comes under specific social security tax percentages.

6. Holidays: Spain employees get a vacation equals to minimum of 30 calendar days

each year, this number can be modify according to individual employment contracts

or collective agreements (although some collective agreements change this 30-day

period, considering weekends, bank holidays, etc., to 22 working days per year) as

well as 14 national, regional and local holidays. Additional to this employee are

allowed 13 days leaves at the time of child birth and 20 days in case there are three or

more than three children in the family, 15 days leave for his/her marriage, one day

paid leave for shifting to a new house, and paid leave for various civic or union duties.

Two additional days leave are granted for multiple births. Employees are also entitled

to get 16 weeks of maternity leave, as well as paid leave for prenatal examinations.

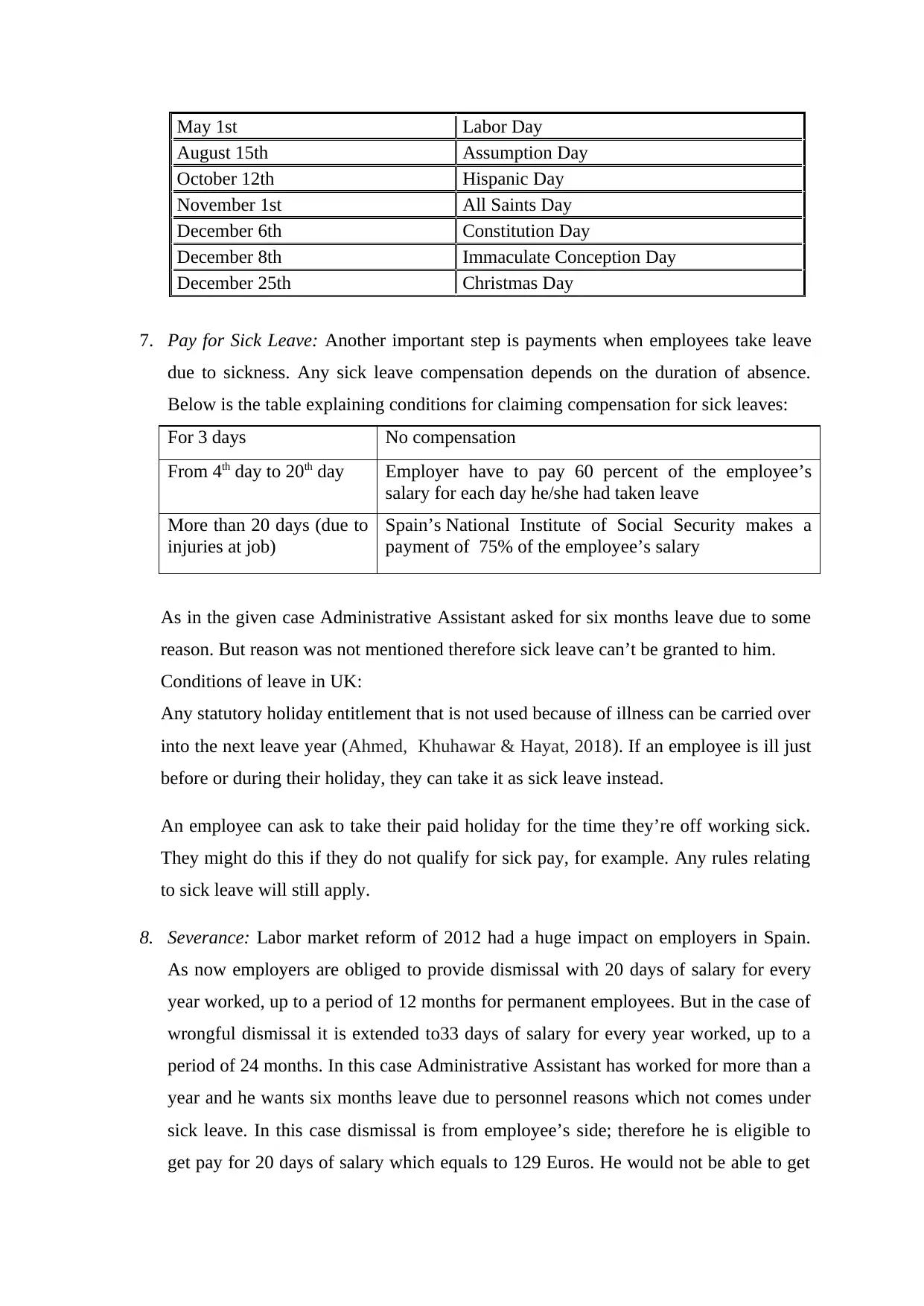

Below is the list of Spain’s Public holidays given to each employees:

Date Spain's Public Holiday Schedule

January 1st New Year's Day

January 6th Epiphany Day

Friday before Easter Sunday Good Friday

Visual designer is hiring on temporary contract basis, the reason behind this is visual

designer’s nature of work is temporary as they only required at the time of graphic

design of an app, later they don’t have any major role (Chaflekar and et.al., 2018).

3. Contract Registration: It is obligatory for any company to register the employment

contract with social security authorities and the national employment service. Before

the start of employment new contracts and terminations are necessary to be registered

with social security as well as with the Public Employment Service within 6 days.

4. Probationary Period: Qualified technical personnel have a 6 months probationary

period; and for rest of employees its 2 months (for small size companies having 25

employees or less, the probationary period can be up to 3 months). During this time,

either the employer or employee can terminate employment without prior notice or

reason and without the need for the employer to pay severance. Both the employees

have technical nature of job hence their probationary period can be up to 6 months.

5. Overtime Compensation: Spain workers are allowed to work a maximum of 80 hours

of overtime per year but immediate damage repair is exceptional (Blyton & Morris,

2017). Therefore taking average they can work 6 hours of overtime per month.

Overtime pay is taxable and comes under specific social security tax percentages.

6. Holidays: Spain employees get a vacation equals to minimum of 30 calendar days

each year, this number can be modify according to individual employment contracts

or collective agreements (although some collective agreements change this 30-day

period, considering weekends, bank holidays, etc., to 22 working days per year) as

well as 14 national, regional and local holidays. Additional to this employee are

allowed 13 days leaves at the time of child birth and 20 days in case there are three or

more than three children in the family, 15 days leave for his/her marriage, one day

paid leave for shifting to a new house, and paid leave for various civic or union duties.

Two additional days leave are granted for multiple births. Employees are also entitled

to get 16 weeks of maternity leave, as well as paid leave for prenatal examinations.

Below is the list of Spain’s Public holidays given to each employees:

Date Spain's Public Holiday Schedule

January 1st New Year's Day

January 6th Epiphany Day

Friday before Easter Sunday Good Friday

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

May 1st Labor Day

August 15th Assumption Day

October 12th Hispanic Day

November 1st All Saints Day

December 6th Constitution Day

December 8th Immaculate Conception Day

December 25th Christmas Day

7. Pay for Sick Leave: Another important step is payments when employees take leave

due to sickness. Any sick leave compensation depends on the duration of absence.

Below is the table explaining conditions for claiming compensation for sick leaves:

For 3 days No compensation

From 4th day to 20th day Employer have to pay 60 percent of the employee’s

salary for each day he/she had taken leave

More than 20 days (due to

injuries at job)

Spain’s National Institute of Social Security makes a

payment of 75% of the employee’s salary

As in the given case Administrative Assistant asked for six months leave due to some

reason. But reason was not mentioned therefore sick leave can’t be granted to him.

Conditions of leave in UK:

Any statutory holiday entitlement that is not used because of illness can be carried over

into the next leave year (Ahmed, Khuhawar & Hayat, 2018). If an employee is ill just

before or during their holiday, they can take it as sick leave instead.

An employee can ask to take their paid holiday for the time they’re off working sick.

They might do this if they do not qualify for sick pay, for example. Any rules relating

to sick leave will still apply.

8. Severance: Labor market reform of 2012 had a huge impact on employers in Spain.

As now employers are obliged to provide dismissal with 20 days of salary for every

year worked, up to a period of 12 months for permanent employees. But in the case of

wrongful dismissal it is extended to33 days of salary for every year worked, up to a

period of 24 months. In this case Administrative Assistant has worked for more than a

year and he wants six months leave due to personnel reasons which not comes under

sick leave. In this case dismissal is from employee’s side; therefore he is eligible to

get pay for 20 days of salary which equals to 129 Euros. He would not be able to get

August 15th Assumption Day

October 12th Hispanic Day

November 1st All Saints Day

December 6th Constitution Day

December 8th Immaculate Conception Day

December 25th Christmas Day

7. Pay for Sick Leave: Another important step is payments when employees take leave

due to sickness. Any sick leave compensation depends on the duration of absence.

Below is the table explaining conditions for claiming compensation for sick leaves:

For 3 days No compensation

From 4th day to 20th day Employer have to pay 60 percent of the employee’s

salary for each day he/she had taken leave

More than 20 days (due to

injuries at job)

Spain’s National Institute of Social Security makes a

payment of 75% of the employee’s salary

As in the given case Administrative Assistant asked for six months leave due to some

reason. But reason was not mentioned therefore sick leave can’t be granted to him.

Conditions of leave in UK:

Any statutory holiday entitlement that is not used because of illness can be carried over

into the next leave year (Ahmed, Khuhawar & Hayat, 2018). If an employee is ill just

before or during their holiday, they can take it as sick leave instead.

An employee can ask to take their paid holiday for the time they’re off working sick.

They might do this if they do not qualify for sick pay, for example. Any rules relating

to sick leave will still apply.

8. Severance: Labor market reform of 2012 had a huge impact on employers in Spain.

As now employers are obliged to provide dismissal with 20 days of salary for every

year worked, up to a period of 12 months for permanent employees. But in the case of

wrongful dismissal it is extended to33 days of salary for every year worked, up to a

period of 24 months. In this case Administrative Assistant has worked for more than a

year and he wants six months leave due to personnel reasons which not comes under

sick leave. In this case dismissal is from employee’s side; therefore he is eligible to

get pay for 20 days of salary which equals to 129 Euros. He would not be able to get

any remuneration for 10 days leave pending, because in Spain pending leaves

cancelled if not used by employees and it is not subject to be paid back to employee.

9. Social Security Contributions: The employer has obligation for monthly contributions

to Spain’s National Social Security Institute and withhold contributions from their

employees’ paychecks. The amount of these social security contributions, which

cover pension plans, labor accidents and illnesses, is depend on various factors like

length of employment or type of employment contract. Typically, the employer will

be responsible for paying between 30.8% to 39.25% of an employee’s salary, on the

other hand employee only have to contribute between 6.35% to 6.4% of his or her

salary.

10. Income Tax Payments: Employers in Spain have to deduct income tax from their

employee’s paychecks (Robinson, 2020). The amount of tax to be withheld typically

ranges from 24.75% to 52% depending on the employee’s salary. Employers are

obliged to submit these payments to Spain’s Tax Authority, employers in the Basque

and Navarra regions will submit income taxes to local authorities. In addition, there

are rules establishing when the company must submit its tax payments; those with

more than €6,010,121 in tax revenue are required to pay taxes on a monthly basis,

while all other employers must do so on a quarterly basis. In this case both the

employees have salary less than €6,010,121 hence they are liable to pay tax quarterly.

11. Compensating Employees: Employers of Spain are obliged to pay their employees on

a monthly basis depending upon their employment contract and collective bargaining

agreements (Madura, 2020). In addition to the minimum of 12 monthly payments,

many collective agreements require two additional payments in July and December,

which are prorated and included in monthly payrolls. All payments must be made by

check or direct bank deposit, and, for payments made by check, the employer must

provide a pay slip with the amount of payment and withholdings to be signed by the

employee.

cancelled if not used by employees and it is not subject to be paid back to employee.

9. Social Security Contributions: The employer has obligation for monthly contributions

to Spain’s National Social Security Institute and withhold contributions from their

employees’ paychecks. The amount of these social security contributions, which

cover pension plans, labor accidents and illnesses, is depend on various factors like

length of employment or type of employment contract. Typically, the employer will

be responsible for paying between 30.8% to 39.25% of an employee’s salary, on the

other hand employee only have to contribute between 6.35% to 6.4% of his or her

salary.

10. Income Tax Payments: Employers in Spain have to deduct income tax from their

employee’s paychecks (Robinson, 2020). The amount of tax to be withheld typically

ranges from 24.75% to 52% depending on the employee’s salary. Employers are

obliged to submit these payments to Spain’s Tax Authority, employers in the Basque

and Navarra regions will submit income taxes to local authorities. In addition, there

are rules establishing when the company must submit its tax payments; those with

more than €6,010,121 in tax revenue are required to pay taxes on a monthly basis,

while all other employers must do so on a quarterly basis. In this case both the

employees have salary less than €6,010,121 hence they are liable to pay tax quarterly.

11. Compensating Employees: Employers of Spain are obliged to pay their employees on

a monthly basis depending upon their employment contract and collective bargaining

agreements (Madura, 2020). In addition to the minimum of 12 monthly payments,

many collective agreements require two additional payments in July and December,

which are prorated and included in monthly payrolls. All payments must be made by

check or direct bank deposit, and, for payments made by check, the employer must

provide a pay slip with the amount of payment and withholdings to be signed by the

employee.

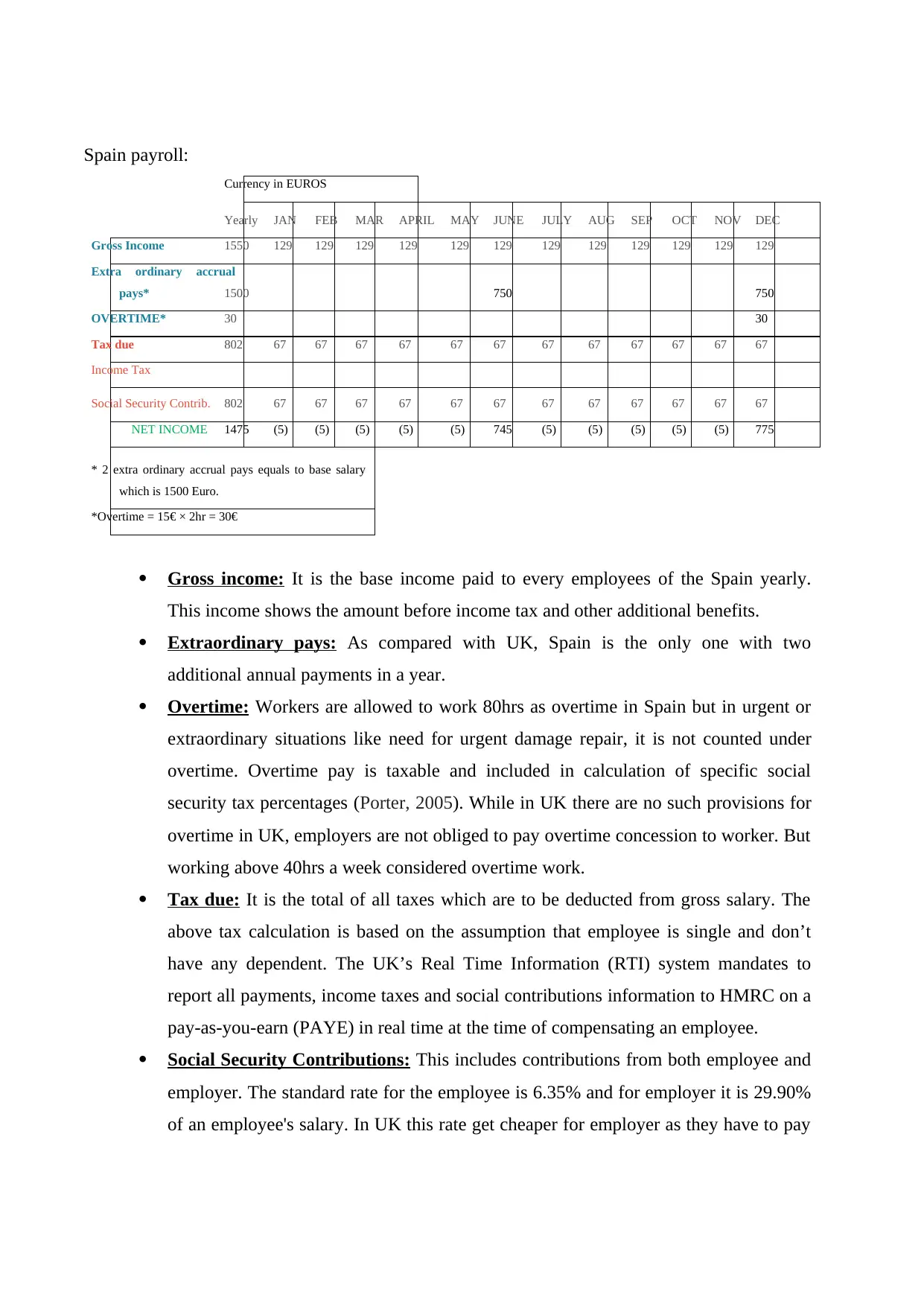

Spain payroll:

Currency in EUROS

Yearly JAN FEB MAR APRIL MAY JUNE JULY AUG SEP OCT NOV DEC

Gross Income 1550 129 129 129 129 129 129 129 129 129 129 129 129

Extra ordinary accrual

pays* 1500 750 750

OVERTIME* 30 30

Tax due 802 67 67 67 67 67 67 67 67 67 67 67 67

Income Tax

Social Security Contrib. 802 67 67 67 67 67 67 67 67 67 67 67 67

NET INCOME 1475 (5) (5) (5) (5) (5) 745 (5) (5) (5) (5) (5) 775

* 2 extra ordinary accrual pays equals to base salary

which is 1500 Euro.

*Overtime = 15€ × 2hr = 30€

Gross income: It is the base income paid to every employees of the Spain yearly.

This income shows the amount before income tax and other additional benefits.

Extraordinary pays: As compared with UK, Spain is the only one with two

additional annual payments in a year.

Overtime: Workers are allowed to work 80hrs as overtime in Spain but in urgent or

extraordinary situations like need for urgent damage repair, it is not counted under

overtime. Overtime pay is taxable and included in calculation of specific social

security tax percentages (Porter, 2005). While in UK there are no such provisions for

overtime in UK, employers are not obliged to pay overtime concession to worker. But

working above 40hrs a week considered overtime work.

Tax due: It is the total of all taxes which are to be deducted from gross salary. The

above tax calculation is based on the assumption that employee is single and don’t

have any dependent. The UK’s Real Time Information (RTI) system mandates to

report all payments, income taxes and social contributions information to HMRC on a

pay-as-you-earn (PAYE) in real time at the time of compensating an employee.

Social Security Contributions: This includes contributions from both employee and

employer. The standard rate for the employee is 6.35% and for employer it is 29.90%

of an employee's salary. In UK this rate get cheaper for employer as they have to pay

Currency in EUROS

Yearly JAN FEB MAR APRIL MAY JUNE JULY AUG SEP OCT NOV DEC

Gross Income 1550 129 129 129 129 129 129 129 129 129 129 129 129

Extra ordinary accrual

pays* 1500 750 750

OVERTIME* 30 30

Tax due 802 67 67 67 67 67 67 67 67 67 67 67 67

Income Tax

Social Security Contrib. 802 67 67 67 67 67 67 67 67 67 67 67 67

NET INCOME 1475 (5) (5) (5) (5) (5) 745 (5) (5) (5) (5) (5) 775

* 2 extra ordinary accrual pays equals to base salary

which is 1500 Euro.

*Overtime = 15€ × 2hr = 30€

Gross income: It is the base income paid to every employees of the Spain yearly.

This income shows the amount before income tax and other additional benefits.

Extraordinary pays: As compared with UK, Spain is the only one with two

additional annual payments in a year.

Overtime: Workers are allowed to work 80hrs as overtime in Spain but in urgent or

extraordinary situations like need for urgent damage repair, it is not counted under

overtime. Overtime pay is taxable and included in calculation of specific social

security tax percentages (Porter, 2005). While in UK there are no such provisions for

overtime in UK, employers are not obliged to pay overtime concession to worker. But

working above 40hrs a week considered overtime work.

Tax due: It is the total of all taxes which are to be deducted from gross salary. The

above tax calculation is based on the assumption that employee is single and don’t

have any dependent. The UK’s Real Time Information (RTI) system mandates to

report all payments, income taxes and social contributions information to HMRC on a

pay-as-you-earn (PAYE) in real time at the time of compensating an employee.

Social Security Contributions: This includes contributions from both employee and

employer. The standard rate for the employee is 6.35% and for employer it is 29.90%

of an employee's salary. In UK this rate get cheaper for employer as they have to pay

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

only 13.8% of employee’s salary. So it could be cheaper for employer to choose UK

to start a new business.

Net Income: It is the balance amount which an employee takes home or take it home

salary.

to start a new business.

Net Income: It is the balance amount which an employee takes home or take it home

salary.

REFERENCES

Books and journals

Rose, P., & Hudgins, S., 2006. Bank management and financial services. The McGraw− Hill.

Porter, T., 2005. Globalization and finance (p. 230). Cambridge: Polity.

Cassis, Y., & Wójcik, D. (Eds.). 2018. International financial centres after the global financial

crisis and Brexit. Oxford University Press.

Madura, J., 2020. International financial management. Cengage Learning.

Robinson, T. R., 2020. International financial statement analysis. John Wiley & Sons.

Ahmed, A., Khuhawar, S. A., & Hayat, S., 2018. FGEHF: Authenticated Web Based Application

for Human Resource Management System. Indian Journal of Science and

Technology, 11(43), 1-12.

Chaflekar, S. and et.al., 2018. Payroll system Using Fingerprint and Face Detection.

Karanja, D., Sang, A. K. A., & Ndirangu, M., 2018. Influence of Integration of ICT on human

resource management in Kenyan public universities. International Journal of Sustainability

Management and Information Technologies, 3(6), 73.

D ROZARIO, M. A., 2018. PROJECT ON EMPLOYEE DATABASE AND PAYROLL

MANAGEMENT SYSTEM (Doctoral dissertation, University of Technology).

Vettori, S., 2016. The employment contract and the changed world of work. Routledge.

Blyton, P., & Morris, J. (Eds.)., 2017. A Flexible Future?: Prospects for Employment and

Organization (Vol. 30). Walter de Gruyter GmbH & Co KG.

Books and journals

Rose, P., & Hudgins, S., 2006. Bank management and financial services. The McGraw− Hill.

Porter, T., 2005. Globalization and finance (p. 230). Cambridge: Polity.

Cassis, Y., & Wójcik, D. (Eds.). 2018. International financial centres after the global financial

crisis and Brexit. Oxford University Press.

Madura, J., 2020. International financial management. Cengage Learning.

Robinson, T. R., 2020. International financial statement analysis. John Wiley & Sons.

Ahmed, A., Khuhawar, S. A., & Hayat, S., 2018. FGEHF: Authenticated Web Based Application

for Human Resource Management System. Indian Journal of Science and

Technology, 11(43), 1-12.

Chaflekar, S. and et.al., 2018. Payroll system Using Fingerprint and Face Detection.

Karanja, D., Sang, A. K. A., & Ndirangu, M., 2018. Influence of Integration of ICT on human

resource management in Kenyan public universities. International Journal of Sustainability

Management and Information Technologies, 3(6), 73.

D ROZARIO, M. A., 2018. PROJECT ON EMPLOYEE DATABASE AND PAYROLL

MANAGEMENT SYSTEM (Doctoral dissertation, University of Technology).

Vettori, S., 2016. The employment contract and the changed world of work. Routledge.

Blyton, P., & Morris, J. (Eds.)., 2017. A Flexible Future?: Prospects for Employment and

Organization (Vol. 30). Walter de Gruyter GmbH & Co KG.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.