Analysis of Cost, Volume, and Profit in Accounting Fundamentals

VerifiedAdded on 2023/01/06

|9

|1192

|77

Homework Assignment

AI Summary

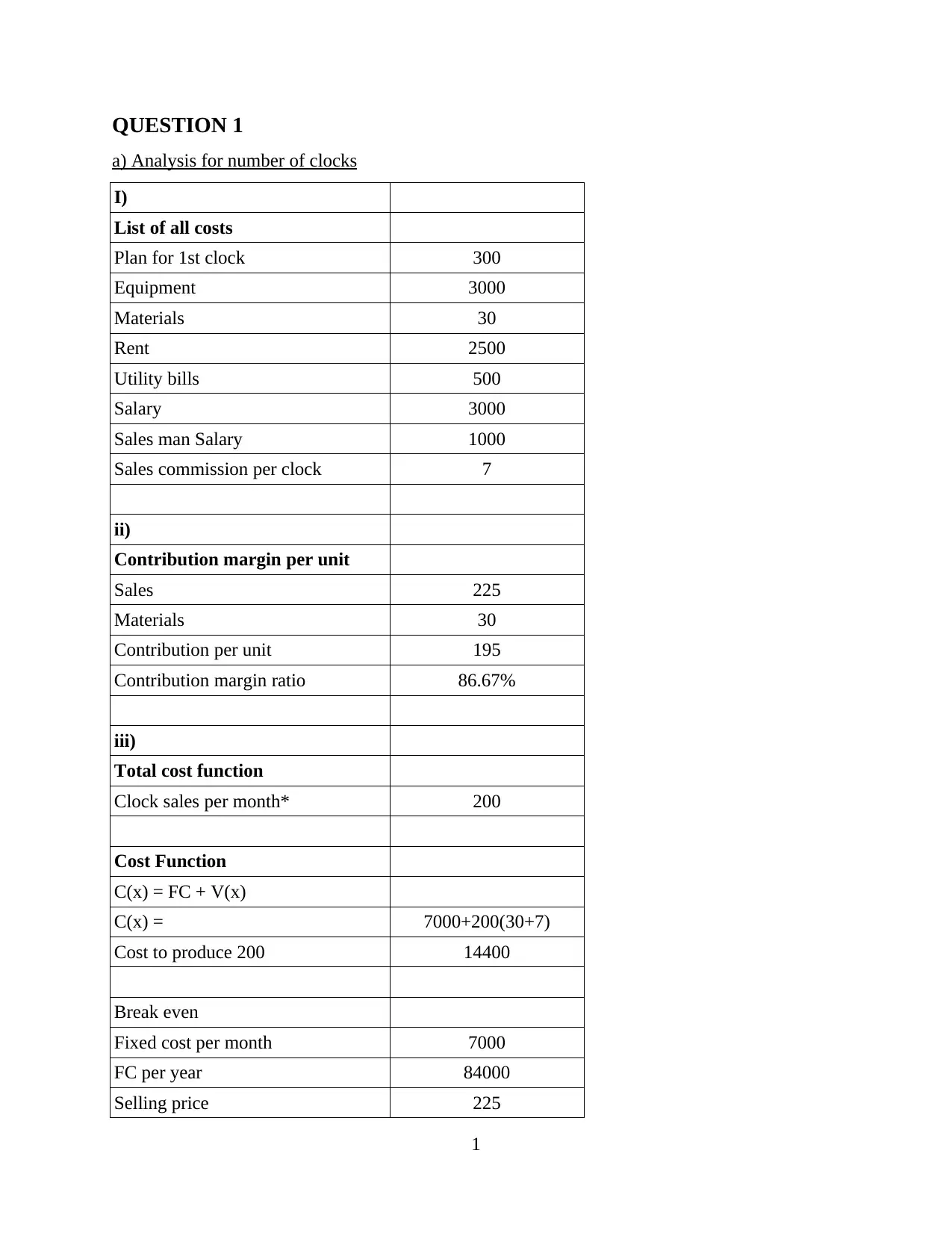

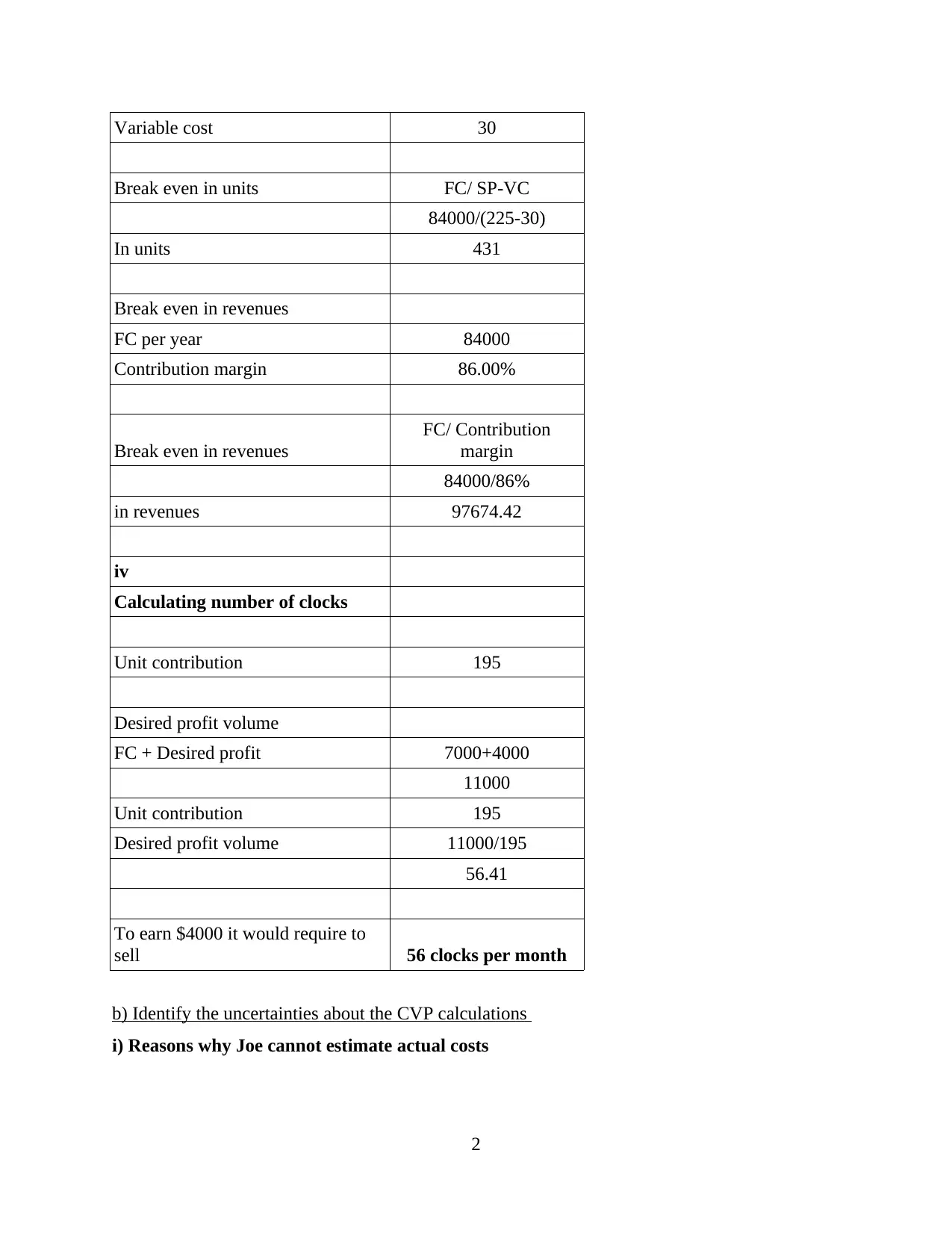

This assignment solution provides a comprehensive analysis of accounting fundamentals, focusing on cost-volume-profit (CVP) analysis and break-even calculations. The solution begins with an analysis of costs associated with producing a product, including material, labor, and overhead costs. It then delves into the uncertainties inherent in CVP calculations, such as fluctuating material costs, rent, utilities, and sales estimations, and how these uncertainties impact break-even analysis. The assignment further explores the potential biases in revenue and cost estimates, emphasizing the importance of accurate data. The solution also includes a detailed calculation of missing amounts in a production report and presents a production cost report for a coating department, covering units completed, equivalent units, and cost per equivalent unit. The report also includes the value of ending work in progress and costs of goods completed and transferred out, providing a thorough overview of the production process. This student-contributed paper is available on Desklib, a platform offering study tools for students.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.