Strategic Information Systems: Bell Studio Case Study Analysis

VerifiedAdded on 2023/02/01

|13

|3427

|40

Case Study

AI Summary

This case study analyzes the strategic information systems of Bell Studio, a wholesale art supplies company based in Adelaide. The assignment examines the cash disbursement, payroll, and purchase systems, highlighting internal control weaknesses such as lack of segregation of duties, peer review, and manual processes. It identifies potential risks, including cash embezzlement, errors in record-keeping, and collusion, and recommends implementing automated systems like QuickBooks and biometric time tracking, along with improved internal control procedures. The study emphasizes the need for proper authorization, physical inventory counts, and segregation of duties to mitigate risks and ensure accurate financial reporting. The assignment underscores the importance of financial controls and addresses the need for investment in system development and employee training to secure the company's financial health.

MANAGEMENT 1

STRATEGIC INFORMATION SYSTEMS FOR BUSINESSES

Name of student

Name of institution

Name of instructor

Course code

Date

STRATEGIC INFORMATION SYSTEMS FOR BUSINESSES

Name of student

Name of institution

Name of instructor

Course code

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT 2

Executive summary

Bell studio is based in Adelaide and deals with the wholesale of art supplies. The

studio has developed various departments to efficiently perform various activities.

The departments include cash disbursement, purchase system and payroll system.

The various systems have a proper organisation that shows the hierarchy of

activities and flow of data from one stage to the next. Bell studio emphasises that the

employees follow the stages without fail to prevent errors and override of authority.

Moreover, Bell studio faces various internal control problems that introduce risks to

the accounting system. The company fails to implement internal control principles

such as segregation of duties, authorisation of activities, peer review and physical

inspections. The failure to implement the internal control standards could cause risks

such as cash embezzlement in the cash disbursement office, collusion with suppliers

and errors of commission and omission. The availability of errors and loopholes to

misappropriate finances could result in undermining the going concern of the

company.

Furthermore, Bell studio should focus on developing an automated system to avoid

the problems that arise from manual systems. The company should purchase

accounting software such as QuickBooks and sage that ensure accurate entries. Bell

studio should ensure the implementation of the internal control systems to prevent

shortages of working capital.

However, the implementation of the system will require a huge financial outlay to pay

for the various expenses. The expenses include hiring a consultant, buying computer

software and corresponding hardware. Other expenses include training the

employees to understand the need to implement proper financial controls. Therefore,

the company should ensure the availability of the finance to avoid hitches in system

development and implementation.

Executive summary

Bell studio is based in Adelaide and deals with the wholesale of art supplies. The

studio has developed various departments to efficiently perform various activities.

The departments include cash disbursement, purchase system and payroll system.

The various systems have a proper organisation that shows the hierarchy of

activities and flow of data from one stage to the next. Bell studio emphasises that the

employees follow the stages without fail to prevent errors and override of authority.

Moreover, Bell studio faces various internal control problems that introduce risks to

the accounting system. The company fails to implement internal control principles

such as segregation of duties, authorisation of activities, peer review and physical

inspections. The failure to implement the internal control standards could cause risks

such as cash embezzlement in the cash disbursement office, collusion with suppliers

and errors of commission and omission. The availability of errors and loopholes to

misappropriate finances could result in undermining the going concern of the

company.

Furthermore, Bell studio should focus on developing an automated system to avoid

the problems that arise from manual systems. The company should purchase

accounting software such as QuickBooks and sage that ensure accurate entries. Bell

studio should ensure the implementation of the internal control systems to prevent

shortages of working capital.

However, the implementation of the system will require a huge financial outlay to pay

for the various expenses. The expenses include hiring a consultant, buying computer

software and corresponding hardware. Other expenses include training the

employees to understand the need to implement proper financial controls. Therefore,

the company should ensure the availability of the finance to avoid hitches in system

development and implementation.

MANAGEMENT 3

Table of Contents

Executive summary......................................................................................................2

Introduction...................................................................................................................4

Cash disbursement system..........................................................................................4

Data flow diagram of a cash disbursement system......................................................4

Internal control weaknesses.........................................................................................5

The possible risks arising from the weaknesses..........................................................5

Payroll system..............................................................................................................6

Data flowchart of payroll...............................................................................................6

The internal control weaknesses of the payroll system................................................7

The risks posed by the internal control weaknesses....................................................7

Purchase system..........................................................................................................8

Data flow system of purchase system..........................................................................9

The internal control weakness in the purchase system...............................................9

The risks caused by the internal control weaknesses................................................10

Conclusion..................................................................................................................10

Bibliography................................................................................................................11

Table of Contents

Executive summary......................................................................................................2

Introduction...................................................................................................................4

Cash disbursement system..........................................................................................4

Data flow diagram of a cash disbursement system......................................................4

Internal control weaknesses.........................................................................................5

The possible risks arising from the weaknesses..........................................................5

Payroll system..............................................................................................................6

Data flowchart of payroll...............................................................................................6

The internal control weaknesses of the payroll system................................................7

The risks posed by the internal control weaknesses....................................................7

Purchase system..........................................................................................................8

Data flow system of purchase system..........................................................................9

The internal control weakness in the purchase system...............................................9

The risks caused by the internal control weaknesses................................................10

Conclusion..................................................................................................................10

Bibliography................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT 4

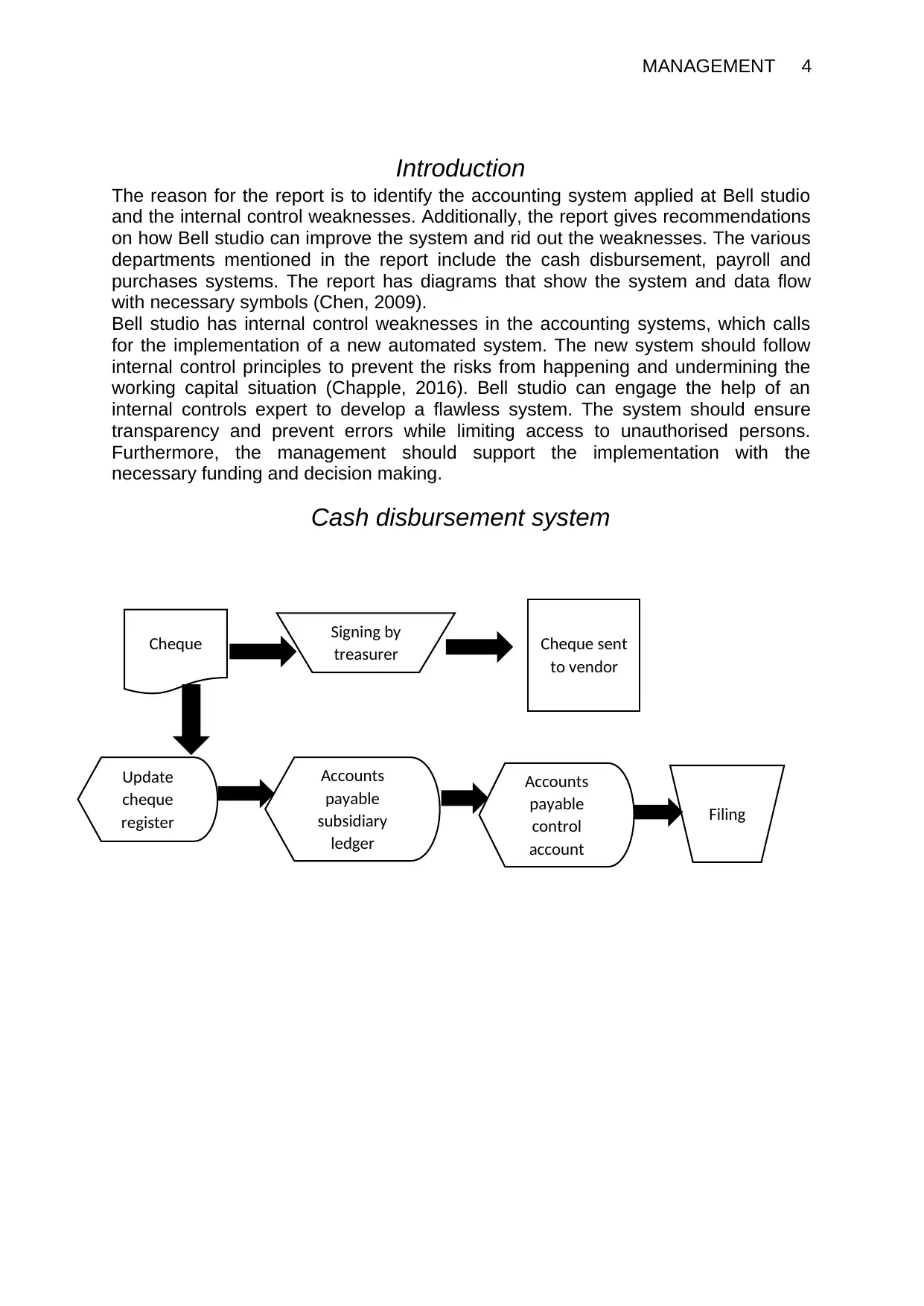

Introduction

The reason for the report is to identify the accounting system applied at Bell studio

and the internal control weaknesses. Additionally, the report gives recommendations

on how Bell studio can improve the system and rid out the weaknesses. The various

departments mentioned in the report include the cash disbursement, payroll and

purchases systems. The report has diagrams that show the system and data flow

with necessary symbols (Chen, 2009).

Bell studio has internal control weaknesses in the accounting systems, which calls

for the implementation of a new automated system. The new system should follow

internal control principles to prevent the risks from happening and undermining the

working capital situation (Chapple, 2016). Bell studio can engage the help of an

internal controls expert to develop a flawless system. The system should ensure

transparency and prevent errors while limiting access to unauthorised persons.

Furthermore, the management should support the implementation with the

necessary funding and decision making.

Cash disbursement system

Filing

Update

cheque

register

Signing by

treasurer

Cheque Cheque sent

to vendor

Accounts

payable

subsidiary

ledger

Accounts

payable

control

account

Introduction

The reason for the report is to identify the accounting system applied at Bell studio

and the internal control weaknesses. Additionally, the report gives recommendations

on how Bell studio can improve the system and rid out the weaknesses. The various

departments mentioned in the report include the cash disbursement, payroll and

purchases systems. The report has diagrams that show the system and data flow

with necessary symbols (Chen, 2009).

Bell studio has internal control weaknesses in the accounting systems, which calls

for the implementation of a new automated system. The new system should follow

internal control principles to prevent the risks from happening and undermining the

working capital situation (Chapple, 2016). Bell studio can engage the help of an

internal controls expert to develop a flawless system. The system should ensure

transparency and prevent errors while limiting access to unauthorised persons.

Furthermore, the management should support the implementation with the

necessary funding and decision making.

Cash disbursement system

Filing

Update

cheque

register

Signing by

treasurer

Cheque Cheque sent

to vendor

Accounts

payable

subsidiary

ledger

Accounts

payable

control

account

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT 5

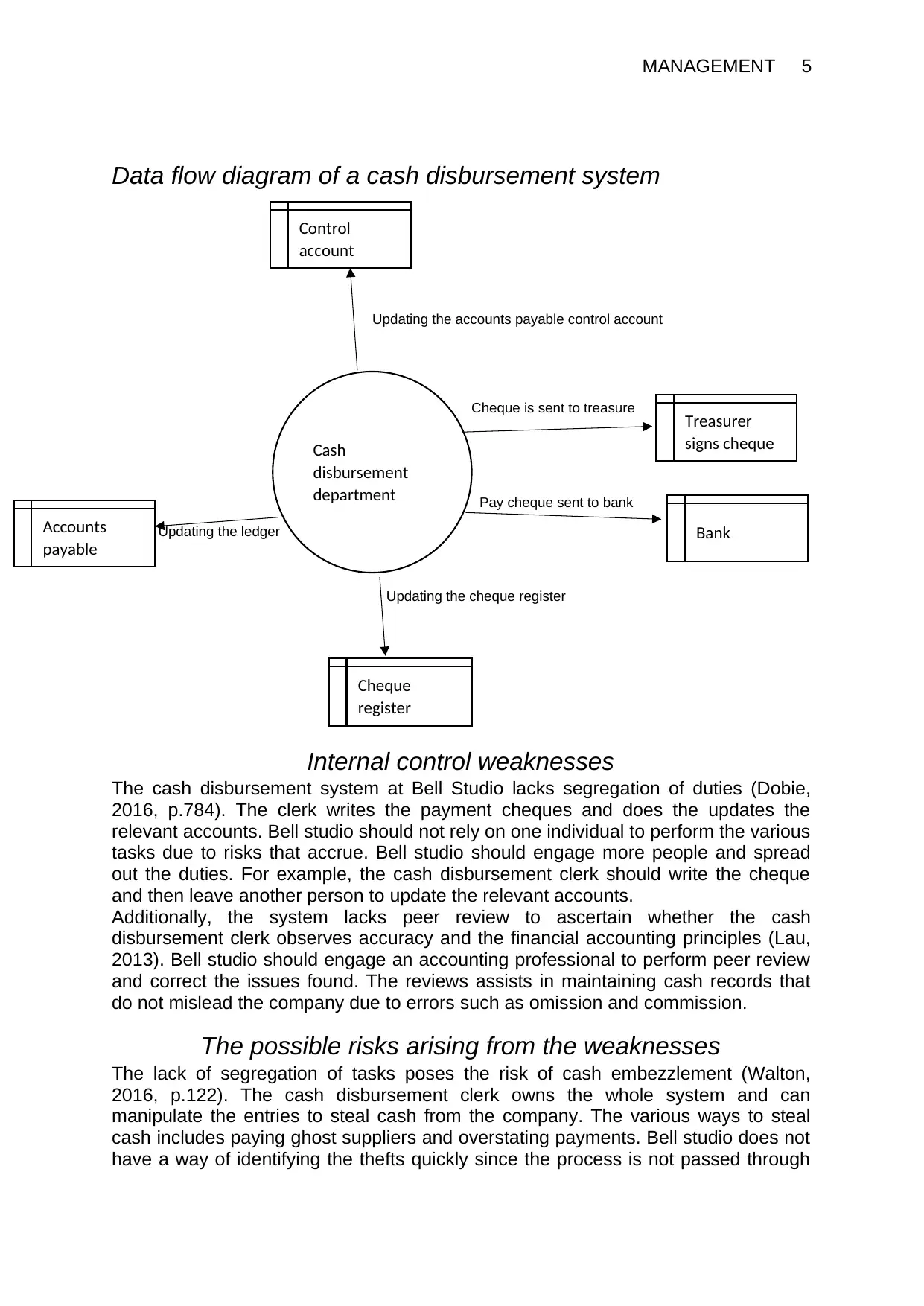

Data flow diagram of a cash disbursement system

Updating the accounts payable control account

Cheque is sent to treasure

Pay cheque sent to bank

Updating the ledger

Updating the cheque register

Internal control weaknesses

The cash disbursement system at Bell Studio lacks segregation of duties (Dobie,

2016, p.784). The clerk writes the payment cheques and does the updates the

relevant accounts. Bell studio should not rely on one individual to perform the various

tasks due to risks that accrue. Bell studio should engage more people and spread

out the duties. For example, the cash disbursement clerk should write the cheque

and then leave another person to update the relevant accounts.

Additionally, the system lacks peer review to ascertain whether the cash

disbursement clerk observes accuracy and the financial accounting principles (Lau,

2013). Bell studio should engage an accounting professional to perform peer review

and correct the issues found. The reviews assists in maintaining cash records that

do not mislead the company due to errors such as omission and commission.

The possible risks arising from the weaknesses

The lack of segregation of tasks poses the risk of cash embezzlement (Walton,

2016, p.122). The cash disbursement clerk owns the whole system and can

manipulate the entries to steal cash from the company. The various ways to steal

cash includes paying ghost suppliers and overstating payments. Bell studio does not

have a way of identifying the thefts quickly since the process is not passed through

Cash

disbursement

department

Treasurer

signs cheque

Bank

Cheque

register

Accounts

payable

Control

account

Data flow diagram of a cash disbursement system

Updating the accounts payable control account

Cheque is sent to treasure

Pay cheque sent to bank

Updating the ledger

Updating the cheque register

Internal control weaknesses

The cash disbursement system at Bell Studio lacks segregation of duties (Dobie,

2016, p.784). The clerk writes the payment cheques and does the updates the

relevant accounts. Bell studio should not rely on one individual to perform the various

tasks due to risks that accrue. Bell studio should engage more people and spread

out the duties. For example, the cash disbursement clerk should write the cheque

and then leave another person to update the relevant accounts.

Additionally, the system lacks peer review to ascertain whether the cash

disbursement clerk observes accuracy and the financial accounting principles (Lau,

2013). Bell studio should engage an accounting professional to perform peer review

and correct the issues found. The reviews assists in maintaining cash records that

do not mislead the company due to errors such as omission and commission.

The possible risks arising from the weaknesses

The lack of segregation of tasks poses the risk of cash embezzlement (Walton,

2016, p.122). The cash disbursement clerk owns the whole system and can

manipulate the entries to steal cash from the company. The various ways to steal

cash includes paying ghost suppliers and overstating payments. Bell studio does not

have a way of identifying the thefts quickly since the process is not passed through

Cash

disbursement

department

Treasurer

signs cheque

Bank

Cheque

register

Accounts

payable

Control

account

MANAGEMENT 6

different persons. Therefore, the company could face cash shortages that could lead

to an inability to pay suppliers (Sahut, 2014, p.665).

Additionally, the system faces the risk of poor application of financial accounting

principles in record keeping (Siegel, 2015, p.366). The clerk could wrongly classify

expenses without correction since no one else interacts with the system. For

example, the clerk could fail to identify unpaid vendors as accounts payables and

record as expenses. The error causes poor decision making while planning for

receivables since the company will allocate a smaller amount than required.

The lack of peer review introduces the risk of errors and misapplication of accounting

standards. The risk continues to occur since the cash disbursement system does not

undergo a check and balance procedure (Tangpong, 2010, p.346). The involvement

of peer reviewers will assist in identifying the errors and do necessary corrections to

the records.

Moreover, failing to review the work done by the cash disbursement clerk could

result in errors of omission and commission (Windsor, 2010, p.80). The errors result

in records that do not tell the true and fair cash situation of the company. Therefore,

bell studio could end up with a cash record that does not match the actual amount of

cash at hand and in the bank.

Furthermore, the lack of segregation of duties poses the risk of collusion between

the cash disbursement clerk and the vendors (Phillips, 2010, p.177). The suppliers

could agree with the clerk to record exaggerated quantities and get paid.

Additionally, the suppliers could fail to indicate discounts on the invoices and reverse

the amounts to the cash disbursement clerk. Therefore, Bell studio could fail to enjoy

the benefits of buying products at a discount.

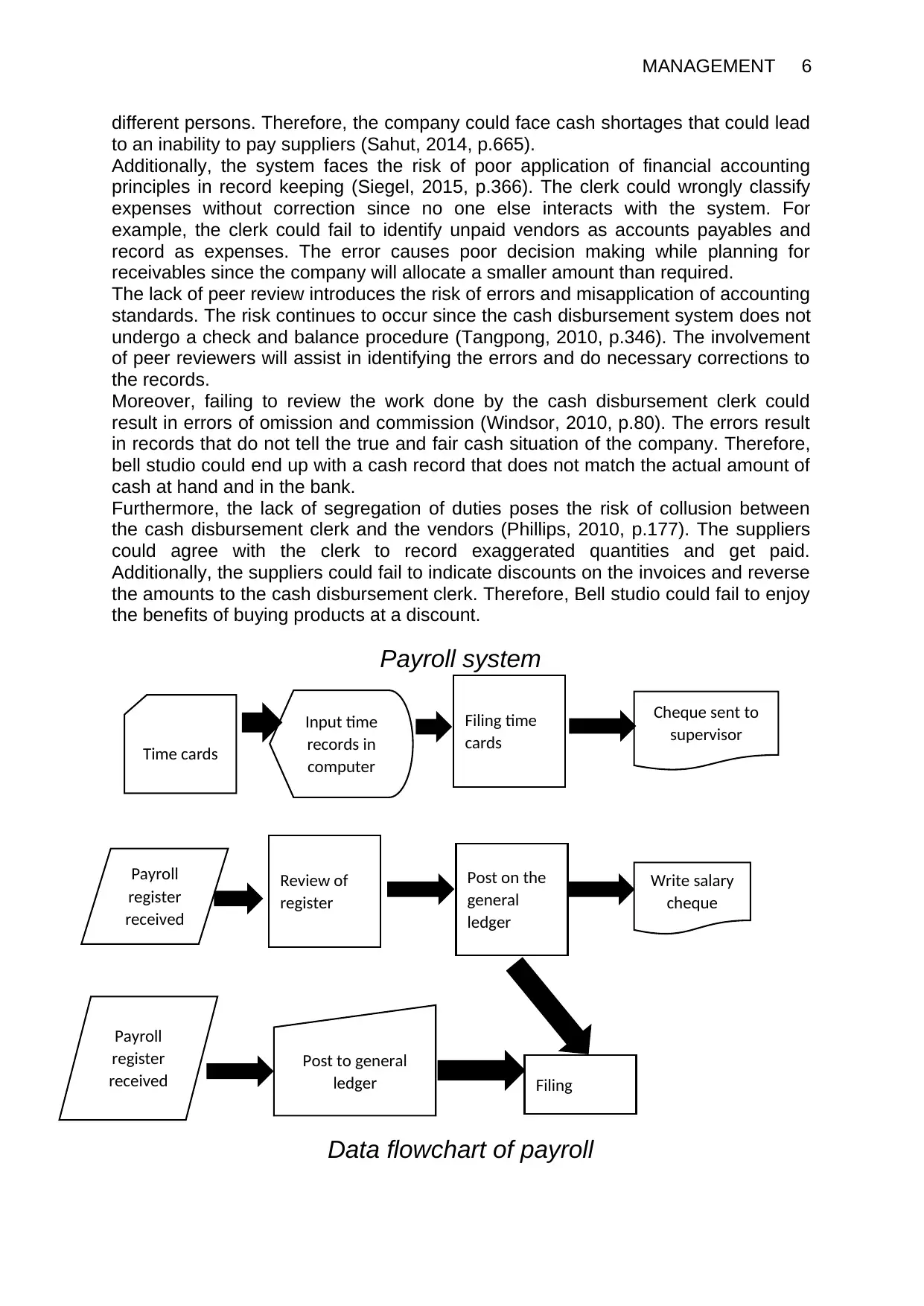

Payroll system

Data flowchart of payroll

Time cards

Input time

records in

computer

Filing time

cards

Payroll

register

received

Review of

register

Cheque sent to

supervisor

Post on the

general

ledger

Write salary

cheque

Payroll

register

received

Post to general

ledger Filing

different persons. Therefore, the company could face cash shortages that could lead

to an inability to pay suppliers (Sahut, 2014, p.665).

Additionally, the system faces the risk of poor application of financial accounting

principles in record keeping (Siegel, 2015, p.366). The clerk could wrongly classify

expenses without correction since no one else interacts with the system. For

example, the clerk could fail to identify unpaid vendors as accounts payables and

record as expenses. The error causes poor decision making while planning for

receivables since the company will allocate a smaller amount than required.

The lack of peer review introduces the risk of errors and misapplication of accounting

standards. The risk continues to occur since the cash disbursement system does not

undergo a check and balance procedure (Tangpong, 2010, p.346). The involvement

of peer reviewers will assist in identifying the errors and do necessary corrections to

the records.

Moreover, failing to review the work done by the cash disbursement clerk could

result in errors of omission and commission (Windsor, 2010, p.80). The errors result

in records that do not tell the true and fair cash situation of the company. Therefore,

bell studio could end up with a cash record that does not match the actual amount of

cash at hand and in the bank.

Furthermore, the lack of segregation of duties poses the risk of collusion between

the cash disbursement clerk and the vendors (Phillips, 2010, p.177). The suppliers

could agree with the clerk to record exaggerated quantities and get paid.

Additionally, the suppliers could fail to indicate discounts on the invoices and reverse

the amounts to the cash disbursement clerk. Therefore, Bell studio could fail to enjoy

the benefits of buying products at a discount.

Payroll system

Data flowchart of payroll

Time cards

Input time

records in

computer

Filing time

cards

Payroll

register

received

Review of

register

Cheque sent to

supervisor

Post on the

general

ledger

Write salary

cheque

Payroll

register

received

Post to general

ledger Filing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

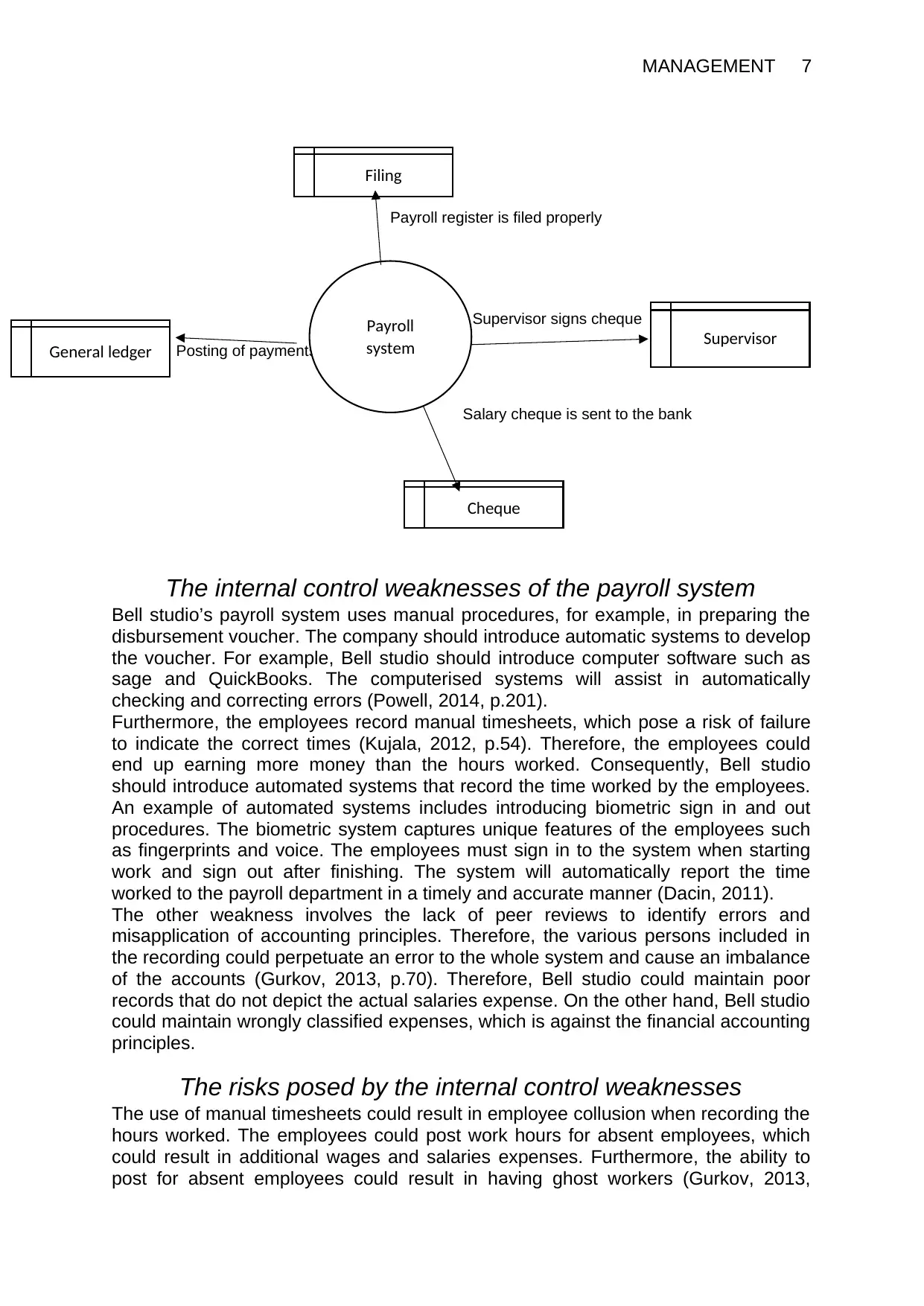

MANAGEMENT 7

Payroll register is filed properly

Supervisor signs cheque

Posting of payments

Salary cheque is sent to the bank

The internal control weaknesses of the payroll system

Bell studio’s payroll system uses manual procedures, for example, in preparing the

disbursement voucher. The company should introduce automatic systems to develop

the voucher. For example, Bell studio should introduce computer software such as

sage and QuickBooks. The computerised systems will assist in automatically

checking and correcting errors (Powell, 2014, p.201).

Furthermore, the employees record manual timesheets, which pose a risk of failure

to indicate the correct times (Kujala, 2012, p.54). Therefore, the employees could

end up earning more money than the hours worked. Consequently, Bell studio

should introduce automated systems that record the time worked by the employees.

An example of automated systems includes introducing biometric sign in and out

procedures. The biometric system captures unique features of the employees such

as fingerprints and voice. The employees must sign in to the system when starting

work and sign out after finishing. The system will automatically report the time

worked to the payroll department in a timely and accurate manner (Dacin, 2011).

The other weakness involves the lack of peer reviews to identify errors and

misapplication of accounting principles. Therefore, the various persons included in

the recording could perpetuate an error to the whole system and cause an imbalance

of the accounts (Gurkov, 2013, p.70). Therefore, Bell studio could maintain poor

records that do not depict the actual salaries expense. On the other hand, Bell studio

could maintain wrongly classified expenses, which is against the financial accounting

principles.

The risks posed by the internal control weaknesses

The use of manual timesheets could result in employee collusion when recording the

hours worked. The employees could post work hours for absent employees, which

could result in additional wages and salaries expenses. Furthermore, the ability to

post for absent employees could result in having ghost workers (Gurkov, 2013,

Payroll

system

Filing

General ledger

Cheque

Supervisor

Payroll register is filed properly

Supervisor signs cheque

Posting of payments

Salary cheque is sent to the bank

The internal control weaknesses of the payroll system

Bell studio’s payroll system uses manual procedures, for example, in preparing the

disbursement voucher. The company should introduce automatic systems to develop

the voucher. For example, Bell studio should introduce computer software such as

sage and QuickBooks. The computerised systems will assist in automatically

checking and correcting errors (Powell, 2014, p.201).

Furthermore, the employees record manual timesheets, which pose a risk of failure

to indicate the correct times (Kujala, 2012, p.54). Therefore, the employees could

end up earning more money than the hours worked. Consequently, Bell studio

should introduce automated systems that record the time worked by the employees.

An example of automated systems includes introducing biometric sign in and out

procedures. The biometric system captures unique features of the employees such

as fingerprints and voice. The employees must sign in to the system when starting

work and sign out after finishing. The system will automatically report the time

worked to the payroll department in a timely and accurate manner (Dacin, 2011).

The other weakness involves the lack of peer reviews to identify errors and

misapplication of accounting principles. Therefore, the various persons included in

the recording could perpetuate an error to the whole system and cause an imbalance

of the accounts (Gurkov, 2013, p.70). Therefore, Bell studio could maintain poor

records that do not depict the actual salaries expense. On the other hand, Bell studio

could maintain wrongly classified expenses, which is against the financial accounting

principles.

The risks posed by the internal control weaknesses

The use of manual timesheets could result in employee collusion when recording the

hours worked. The employees could post work hours for absent employees, which

could result in additional wages and salaries expenses. Furthermore, the ability to

post for absent employees could result in having ghost workers (Gurkov, 2013,

Payroll

system

Filing

General ledger

Cheque

Supervisor

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT 8

p.71). The ghost workers could arise from employee collusion with the supervisors to

approve additional time sheets for workers who do not exist. Therefore, Bell Studio

incurs more expenses than required. However, the introduction of the biometric

system could solve the risk by directly communicating with the payroll system.

The other risk involves the possible loss of information in the case of damage or loss

of time sheets. The system lacks a back-up system to supplement the payroll

department with information. Therefore, the loss or damage of time sheets could

result in guesswork and estimations to come up with employee work hours. The

estimations and guesswork could cause errors and wrong calculations, which could

result in higher salary and wages than expected (Dacin, 2011). To prevent the risk

form happening, Bell studio should invest in cloud computing to secure and have a

back-up for data in case of loss. The current data back-up plans offer great storage

capacity for a long time, therefore, Bell studio will have no fear of loss of data.

Additionally, the cloud data systems offer security protocols to prevent unauthorised

access, which prevents malicious damage. Another benefit of cloud back-up is the

reduction of paper work in the form of document filing since authorised parties log in

to the system and access the necessary information.

The other risk includes omission and commission when posting manually. The error

could happen when the payroll clerk is posting the time sheets into the computer

system. The clerk could fail to post employees work hours or post the wrong amount.

The mistake results in an employee earning the wrong salary compared to the hours

worked (Hemphill, 2012, p.127).

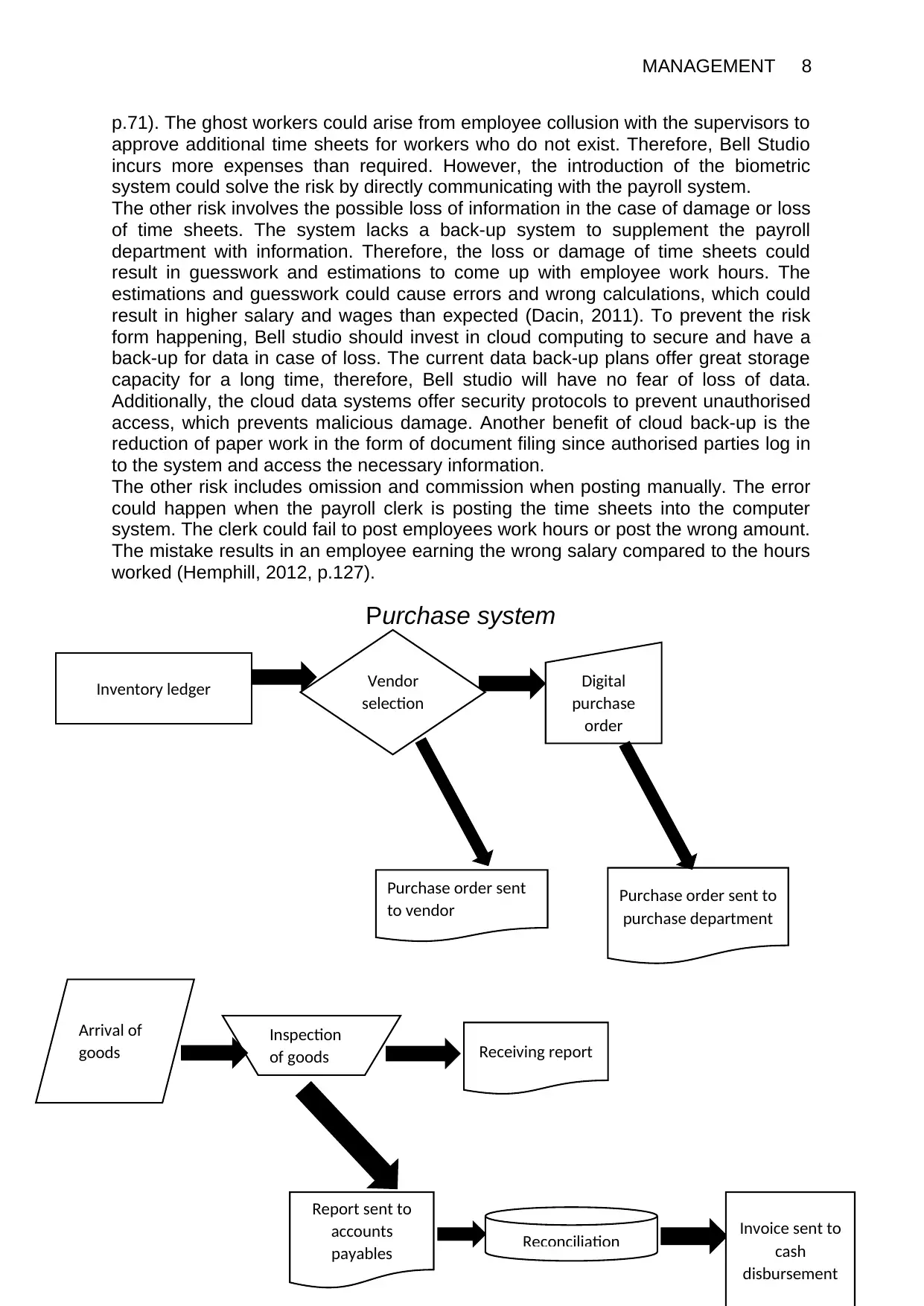

Purchase system

Receiving report

Inventory ledger Vendor

selection

Digital

purchase

order

Purchase order sent

to vendor Purchase order sent to

purchase department

Arrival of

goods

Inspection

of goods

Report sent to

accounts

payables Reconciliation Invoice sent to

cash

disbursement

p.71). The ghost workers could arise from employee collusion with the supervisors to

approve additional time sheets for workers who do not exist. Therefore, Bell Studio

incurs more expenses than required. However, the introduction of the biometric

system could solve the risk by directly communicating with the payroll system.

The other risk involves the possible loss of information in the case of damage or loss

of time sheets. The system lacks a back-up system to supplement the payroll

department with information. Therefore, the loss or damage of time sheets could

result in guesswork and estimations to come up with employee work hours. The

estimations and guesswork could cause errors and wrong calculations, which could

result in higher salary and wages than expected (Dacin, 2011). To prevent the risk

form happening, Bell studio should invest in cloud computing to secure and have a

back-up for data in case of loss. The current data back-up plans offer great storage

capacity for a long time, therefore, Bell studio will have no fear of loss of data.

Additionally, the cloud data systems offer security protocols to prevent unauthorised

access, which prevents malicious damage. Another benefit of cloud back-up is the

reduction of paper work in the form of document filing since authorised parties log in

to the system and access the necessary information.

The other risk includes omission and commission when posting manually. The error

could happen when the payroll clerk is posting the time sheets into the computer

system. The clerk could fail to post employees work hours or post the wrong amount.

The mistake results in an employee earning the wrong salary compared to the hours

worked (Hemphill, 2012, p.127).

Purchase system

Receiving report

Inventory ledger Vendor

selection

Digital

purchase

order

Purchase order sent

to vendor Purchase order sent to

purchase department

Arrival of

goods

Inspection

of goods

Report sent to

accounts

payables Reconciliation Invoice sent to

cash

disbursement

MANAGEMENT 9

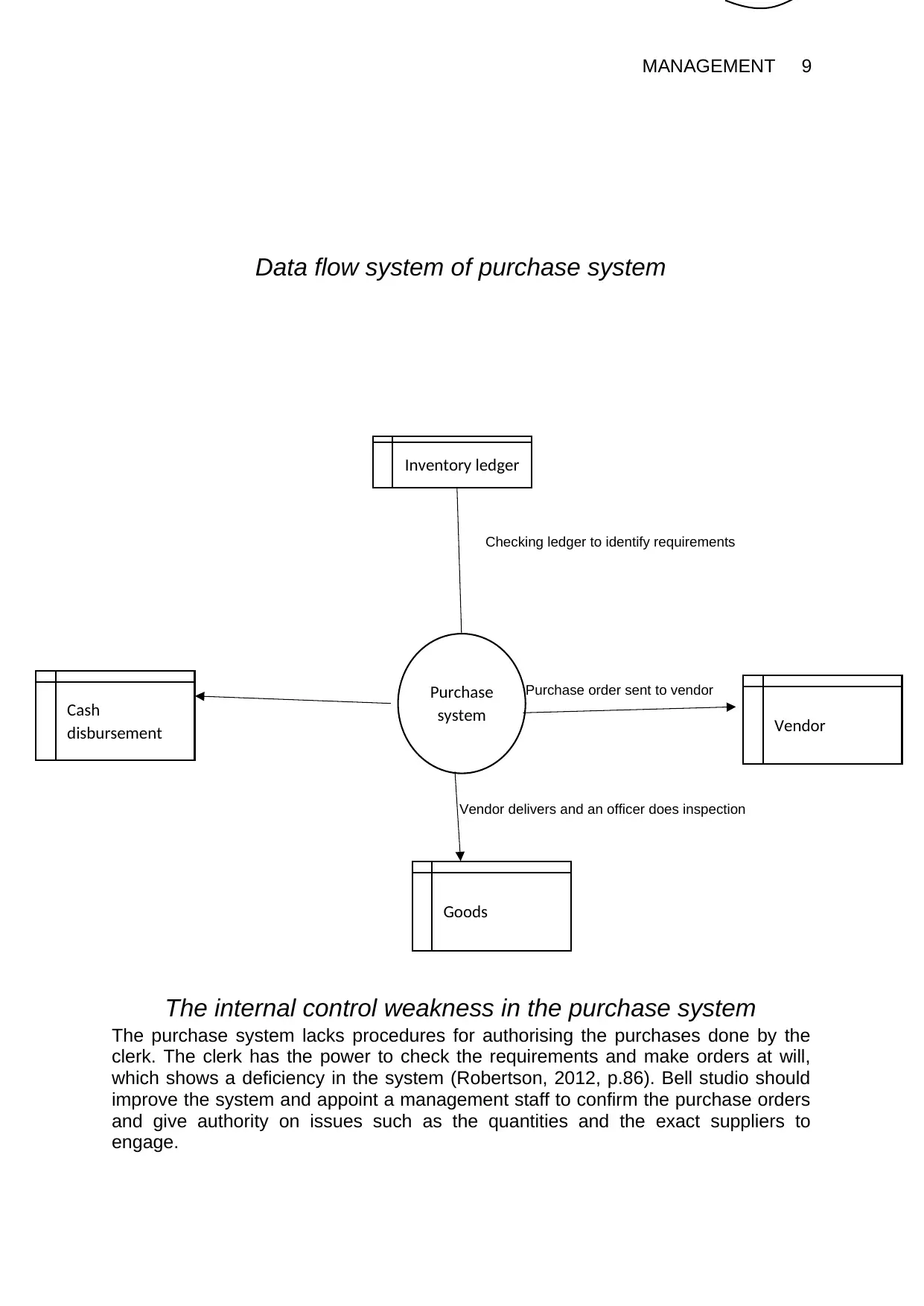

Data flow system of purchase system

Checking ledger to identify requirements

Purchase order sent to vendor

Vendor delivers and an officer does inspection

The internal control weakness in the purchase system

The purchase system lacks procedures for authorising the purchases done by the

clerk. The clerk has the power to check the requirements and make orders at will,

which shows a deficiency in the system (Robertson, 2012, p.86). Bell studio should

improve the system and appoint a management staff to confirm the purchase orders

and give authority on issues such as the quantities and the exact suppliers to

engage.

Inventory ledger

Purchase

system Vendor

Goods

Cash

disbursement

Data flow system of purchase system

Checking ledger to identify requirements

Purchase order sent to vendor

Vendor delivers and an officer does inspection

The internal control weakness in the purchase system

The purchase system lacks procedures for authorising the purchases done by the

clerk. The clerk has the power to check the requirements and make orders at will,

which shows a deficiency in the system (Robertson, 2012, p.86). Bell studio should

improve the system and appoint a management staff to confirm the purchase orders

and give authority on issues such as the quantities and the exact suppliers to

engage.

Inventory ledger

Purchase

system Vendor

Goods

Cash

disbursement

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT 10

The other weakness includes the lack of segregation of duties (Newbert, 2014,

p.143). For example, the receiving clerk inspects the received goods and proceeds

to update the relevant account. Relying on one person to do all the activities exposes

a weakness in the purchase system run by the company. Consequently, the

company should engage more employees to update the various accounts to avoid

errors and abuse of powers.

The system also fails to emphasise on physical counting of the goods received

(Gillingham, 2012, p.431). The receiving clerk only compares the digital purchase

order and the packing slip, which do not give conclusive evidence that the packed

goods match requirements. Therefore, Bell studio should insist on physically

counting and checking the goods received to establish a match with the digital

purchase slip.

The risks caused by the internal control weaknesses

The lack of authorisation procedures could result in theft of money through fake

purchases (Chapple, 2016). The purchase clerk could buy products for personal use

since no authority confirms whether the requested amounts match requirements.

Additionally, the clerk can select a supplier based on the willingness to collude in

stealing from Bell studio. The suppliers can agree to overcharge products and revert

the extra amounts to the purchase clerk.

On the other hand, the failure to segregate duties gives the purchase and receiving

clerk an opportunity to commit fraud (Dobie, 2016, p.785). The clerks can overstate

the product prices or fail to disclose discounts offered on the received goods.

Therefore, Bell studio fails to enjoy the benefits of economies of scale. However, with

segregation of duties the various parties involved can detect the fraud and report to

the relevant authorities.

Additionally, the failure to physically count and check the received goods could result

in the wrong quality and quantity of products (Lau, 2016). The physical checking

allows the receiving clerk to interact with the goods an establish a much with the

purchase order specifications. Furthermore, the lack of emphasis on physically

counting the products opens up an opportunity for collusion with the suppliers to

deliver the wrong products. For example, the receiving clerk could accept a smaller

amount of goods to cash in on part of the payment made to the supplier.

Conclusion

Bell Company has the opportunity to develop a flawless system by implementing

proper internal control systems. The major problem facing Bell studio includes a lack

of segregation of duties. Therefore, the company should bring in more employees to

perform different tasks. The failure to implement proper internal controls could cause

cash embezzlement, which could undermine the going concern.

Moreover, Bell studio should engage an internal controls expert to assist in the

implementation of the internal controls. The expert will play a major role in ensuring

that the internal control systems have no errors and meet the requirements.

Additionally, the expert will train the employees on better control methods. For

example, the receiving clerk could understand the need to physically count the

goods before accepting.

Furthermore, Bell studio should concentrate on automating the system and eliminate

all manual procedures. The manual procedures have a high risk of errors and

inputting the wrong amounts. Therefore, Bell studio should consider various software

The other weakness includes the lack of segregation of duties (Newbert, 2014,

p.143). For example, the receiving clerk inspects the received goods and proceeds

to update the relevant account. Relying on one person to do all the activities exposes

a weakness in the purchase system run by the company. Consequently, the

company should engage more employees to update the various accounts to avoid

errors and abuse of powers.

The system also fails to emphasise on physical counting of the goods received

(Gillingham, 2012, p.431). The receiving clerk only compares the digital purchase

order and the packing slip, which do not give conclusive evidence that the packed

goods match requirements. Therefore, Bell studio should insist on physically

counting and checking the goods received to establish a match with the digital

purchase slip.

The risks caused by the internal control weaknesses

The lack of authorisation procedures could result in theft of money through fake

purchases (Chapple, 2016). The purchase clerk could buy products for personal use

since no authority confirms whether the requested amounts match requirements.

Additionally, the clerk can select a supplier based on the willingness to collude in

stealing from Bell studio. The suppliers can agree to overcharge products and revert

the extra amounts to the purchase clerk.

On the other hand, the failure to segregate duties gives the purchase and receiving

clerk an opportunity to commit fraud (Dobie, 2016, p.785). The clerks can overstate

the product prices or fail to disclose discounts offered on the received goods.

Therefore, Bell studio fails to enjoy the benefits of economies of scale. However, with

segregation of duties the various parties involved can detect the fraud and report to

the relevant authorities.

Additionally, the failure to physically count and check the received goods could result

in the wrong quality and quantity of products (Lau, 2016). The physical checking

allows the receiving clerk to interact with the goods an establish a much with the

purchase order specifications. Furthermore, the lack of emphasis on physically

counting the products opens up an opportunity for collusion with the suppliers to

deliver the wrong products. For example, the receiving clerk could accept a smaller

amount of goods to cash in on part of the payment made to the supplier.

Conclusion

Bell Company has the opportunity to develop a flawless system by implementing

proper internal control systems. The major problem facing Bell studio includes a lack

of segregation of duties. Therefore, the company should bring in more employees to

perform different tasks. The failure to implement proper internal controls could cause

cash embezzlement, which could undermine the going concern.

Moreover, Bell studio should engage an internal controls expert to assist in the

implementation of the internal controls. The expert will play a major role in ensuring

that the internal control systems have no errors and meet the requirements.

Additionally, the expert will train the employees on better control methods. For

example, the receiving clerk could understand the need to physically count the

goods before accepting.

Furthermore, Bell studio should concentrate on automating the system and eliminate

all manual procedures. The manual procedures have a high risk of errors and

inputting the wrong amounts. Therefore, Bell studio should consider various software

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT 11

such as sage and QuickBooks that automatically update related accounts. The

accounting software does not accept wrong records, which acts as a review

procedure.

The development of internal controls will require Bell studio to set aside a huge

amount of finances to ensure adequate purchase of necessary components. For

example, the development of an automated system requires Bell studio to purchase

accounting software and hardware for proper functioning. Additionally, the company

requires to train workers to understand internal control systems and procedures. The

training will require Bell studio to hire coaches and send employees to seminars,

which costs money. On the other hand, the help of external experts is necessary to

ensure successful implementation of the system. Therefore, Bell studio should set

aside adequate finances to ensure success and effective shift to the new internal

controls system.

Bibliography

Chapple, (2016). Book Review: Aiming for Global Accounting Standards: The

International Accounting Standards Board, 2001–2011. Accounting History, 21(2-3),

pp.364-365.

Chen, (2009). On the Challenge of Accounting Standards for Enterprise towards

Enterprise Internal Control. Journal of Sustainable Development, 1(2).

Dacin, (2011). Social Entrepreneurship: A Critique and Future Directions.

Organization Science, 22(5), pp.1203-1213.

Dobie, A. (2016). Aiming for Global Accounting Standards: The International

Accounting Standards Board, 2001–2011. Accounting and Business Research,

46(7), pp.784-785.

Gillingham, P. (2012). The Development of Electronic Information Systems for the

Future: Practitioners, 'Embodied Structures' and 'Technologies-in-Practice'. British

Journal of Social Work, 43(3), pp.430-445.

such as sage and QuickBooks that automatically update related accounts. The

accounting software does not accept wrong records, which acts as a review

procedure.

The development of internal controls will require Bell studio to set aside a huge

amount of finances to ensure adequate purchase of necessary components. For

example, the development of an automated system requires Bell studio to purchase

accounting software and hardware for proper functioning. Additionally, the company

requires to train workers to understand internal control systems and procedures. The

training will require Bell studio to hire coaches and send employees to seminars,

which costs money. On the other hand, the help of external experts is necessary to

ensure successful implementation of the system. Therefore, Bell studio should set

aside adequate finances to ensure success and effective shift to the new internal

controls system.

Bibliography

Chapple, (2016). Book Review: Aiming for Global Accounting Standards: The

International Accounting Standards Board, 2001–2011. Accounting History, 21(2-3),

pp.364-365.

Chen, (2009). On the Challenge of Accounting Standards for Enterprise towards

Enterprise Internal Control. Journal of Sustainable Development, 1(2).

Dacin, (2011). Social Entrepreneurship: A Critique and Future Directions.

Organization Science, 22(5), pp.1203-1213.

Dobie, A. (2016). Aiming for Global Accounting Standards: The International

Accounting Standards Board, 2001–2011. Accounting and Business Research,

46(7), pp.784-785.

Gillingham, P. (2012). The Development of Electronic Information Systems for the

Future: Practitioners, 'Embodied Structures' and 'Technologies-in-Practice'. British

Journal of Social Work, 43(3), pp.430-445.

MANAGEMENT 12

Gurkov, I. (2013). Why Some Russian Industrial Companies Innovate Regularly:

Determinants of Firms’ Decisions to Innovate and Associated Routines. Journal of

East European Management Studies, 18(1), pp.66-96.

Hemphill, (2012). A U.S. Manufacturing Strategy for the 21st Century: What Policies

Yield National Sector Competitiveness? Business Economics, 47(2), pp.126-147.

Kujala, (2012). Understanding the Nature of Stakeholder Relationships: An Empirical

Examination of a Conflict Situation. Journal of Business Ethics, 109(1), pp.53-65

Lau, (2013). What Can Accounting Standards Convey? The Mechanism of

Accounting Standards. SSRN Electronic Journal.

Newbert, (2014). Rarely Pure and Never Simple: Assessing Cumulative Evidence in

Strategic Management. Strategic Organization, 12(2), pp.142-154.

Phillips, (2010). Strategy, Stakeholders and Managerial Discretion. Strategic

Organization, 8(2), pp.176-183.

Powell, (2014). Strategic Management and the Person. Strategic Organization,

12(3), pp.200-207.

Robertson, (2012). A Five-Year Review, Update, and Assessment of Ethics and

Governance in Strategic Management Journal. Journal of Business Ethics, 117(1),

pp.85-91.

Sahut, (2014). Small Business, Innovation, and Entrepreneurship. Small Business

Economics, 42(4), pp.663-668.

Siegel, (2015). Special Issue of Strategic Organization: “Strategic Management

Theory and Universities”. Strategic Organization, 13(4), pp.365-367.

Tangpong, (2010). Stakeholder Prescription and Managerial Decisions: An

Investigation of the Universality of Stakeholder Prescription. Journal of Managerial

Issues, 22(3), pp.345-367.

Gurkov, I. (2013). Why Some Russian Industrial Companies Innovate Regularly:

Determinants of Firms’ Decisions to Innovate and Associated Routines. Journal of

East European Management Studies, 18(1), pp.66-96.

Hemphill, (2012). A U.S. Manufacturing Strategy for the 21st Century: What Policies

Yield National Sector Competitiveness? Business Economics, 47(2), pp.126-147.

Kujala, (2012). Understanding the Nature of Stakeholder Relationships: An Empirical

Examination of a Conflict Situation. Journal of Business Ethics, 109(1), pp.53-65

Lau, (2013). What Can Accounting Standards Convey? The Mechanism of

Accounting Standards. SSRN Electronic Journal.

Newbert, (2014). Rarely Pure and Never Simple: Assessing Cumulative Evidence in

Strategic Management. Strategic Organization, 12(2), pp.142-154.

Phillips, (2010). Strategy, Stakeholders and Managerial Discretion. Strategic

Organization, 8(2), pp.176-183.

Powell, (2014). Strategic Management and the Person. Strategic Organization,

12(3), pp.200-207.

Robertson, (2012). A Five-Year Review, Update, and Assessment of Ethics and

Governance in Strategic Management Journal. Journal of Business Ethics, 117(1),

pp.85-91.

Sahut, (2014). Small Business, Innovation, and Entrepreneurship. Small Business

Economics, 42(4), pp.663-668.

Siegel, (2015). Special Issue of Strategic Organization: “Strategic Management

Theory and Universities”. Strategic Organization, 13(4), pp.365-367.

Tangpong, (2010). Stakeholder Prescription and Managerial Decisions: An

Investigation of the Universality of Stakeholder Prescription. Journal of Managerial

Issues, 22(3), pp.345-367.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.