Management Accounting Report: Jeffrey & Sons Case Study Analysis

VerifiedAdded on 2020/01/23

|18

|5348

|67

Report

AI Summary

This management accounting report examines various aspects of cost accounting and management control within the context of Jeffrey & Sons, a manufacturing company. It begins with an overview of different cost classifications, including elements, nature, function, and behavior, along with relevant examples. The report then proceeds to calculate production costs using both machine hours and labor hours, comparing the results. A job cost sheet is presented to determine total and per-unit costs. The report also includes a variance analysis, comparing budgeted and actual costs, and identifies potential improvements using key performance indicators like turnover and profitability. Budgeting processes, including production, material purchase, and cash budgets, are also discussed. Finally, the report calculates variances, identifies potential causes, and recommends corrective actions, alongside an operating statement and a discussion of responsibility centers. The conclusion summarizes the key findings and recommendations based on the analysis.

Management accounting

Your introduction should be on a separate page

In task 1.1 you need to explain different classifications under each class:

Elements: direct labour, direct material and direct expenses. Each must be

explained with examples

Nature of costs: Direct and indirect costs. Each must be explained with

examples.

Functions of costs: Production and Non production costs: Each must be

explained with examples and

The behaviour of costs: Fixed, variable, semi variable, stepped fixed costs.

Each explained with example

In task 1.3 you need to calculate the production cost per unit based on

machine hours.

In task 1.4 you need to recalculate the production cost per unit based on

labours and then compare both. Please both are missing.

In task 2.2 you need to elaborate a bit more of the performance indicators

with reference to Jeffrey and Sons.

In task 2.3 you need to expand a bit more.

In task 3.1 you need to explain the purpose and nature of the process with

reference to Jeffrey and Sons.

In task 3.3 and 3.4 you need to show your workings.

In task 4.1 you need to show all your workings

IN TASK 4.3, your report should discuss the possible reasons for the

variances

Your introduction should be on a separate page

In task 1.1 you need to explain different classifications under each class:

Elements: direct labour, direct material and direct expenses. Each must be

explained with examples

Nature of costs: Direct and indirect costs. Each must be explained with

examples.

Functions of costs: Production and Non production costs: Each must be

explained with examples and

The behaviour of costs: Fixed, variable, semi variable, stepped fixed costs.

Each explained with example

In task 1.3 you need to calculate the production cost per unit based on

machine hours.

In task 1.4 you need to recalculate the production cost per unit based on

labours and then compare both. Please both are missing.

In task 2.2 you need to elaborate a bit more of the performance indicators

with reference to Jeffrey and Sons.

In task 2.3 you need to expand a bit more.

In task 3.1 you need to explain the purpose and nature of the process with

reference to Jeffrey and Sons.

In task 3.3 and 3.4 you need to show your workings.

In task 4.1 you need to show all your workings

IN TASK 4.3, your report should discuss the possible reasons for the

variances

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction................................................................................................................................1

Task 1.........................................................................................................................................1

AC 1.1 Different types of costs.............................................................................................1

AC 1.2 Job cost sheet............................................................................................................1

AC 1.3 Calculation of cost of Exquisite................................................................................2

AC 1.4 Analysis of cost.........................................................................................................3

AC 2.1 Preparation of cost sheet for 1900 units for variance analysis..................................4

AC 2.2 Identify the potential improvement through various performance indicators...........5

AC 2.3 Ways to reduce the cost and to enhance the value and quality.................................5

TASK 2......................................................................................................................................6

AC 3.1 Purpose and nature of budgeting process..................................................................6

AC 3.2 Appropriate budgeting method and its need.............................................................6

AC 3.3 Preparation of production and material purchase budget for Jeffrey & Son's..........6

AC 3.4 Preparation of cash budget for Jeffrey & Son's.........................................................7

Task 3.........................................................................................................................................8

AC 4.1 calculation of variances, identify possible causes and recommend corrective

actions....................................................................................................................................8

AC 4.2 Operating statements includes both budgeted and actual results............................10

AC 4.3 Responsibility centre...............................................................................................10

Conclusion ...............................................................................................................................10

REFERENCES.........................................................................................................................12

Introduction................................................................................................................................1

Task 1.........................................................................................................................................1

AC 1.1 Different types of costs.............................................................................................1

AC 1.2 Job cost sheet............................................................................................................1

AC 1.3 Calculation of cost of Exquisite................................................................................2

AC 1.4 Analysis of cost.........................................................................................................3

AC 2.1 Preparation of cost sheet for 1900 units for variance analysis..................................4

AC 2.2 Identify the potential improvement through various performance indicators...........5

AC 2.3 Ways to reduce the cost and to enhance the value and quality.................................5

TASK 2......................................................................................................................................6

AC 3.1 Purpose and nature of budgeting process..................................................................6

AC 3.2 Appropriate budgeting method and its need.............................................................6

AC 3.3 Preparation of production and material purchase budget for Jeffrey & Son's..........6

AC 3.4 Preparation of cash budget for Jeffrey & Son's.........................................................7

Task 3.........................................................................................................................................8

AC 4.1 calculation of variances, identify possible causes and recommend corrective

actions....................................................................................................................................8

AC 4.2 Operating statements includes both budgeted and actual results............................10

AC 4.3 Responsibility centre...............................................................................................10

Conclusion ...............................................................................................................................10

REFERENCES.........................................................................................................................12

INTRODUCTION

Management accounting plays a very important role in the organization. It helps to

take different kinds of decisions through implementing distinct management tools. Jeffrey &

Sons is a manufacturing company that produces different kinds of products called Exquisite.

The report presenting here helps to identify various management tools such as budget and

variance analysis technique for Jeffrey & Son's. Further, the report describes the way by

which business can increase its value in order to achieve the business goals. On the contrary,

different types of costs and cost sheet will also be discussed in this report.

1 | P a g e

Management accounting plays a very important role in the organization. It helps to

take different kinds of decisions through implementing distinct management tools. Jeffrey &

Sons is a manufacturing company that produces different kinds of products called Exquisite.

The report presenting here helps to identify various management tools such as budget and

variance analysis technique for Jeffrey & Son's. Further, the report describes the way by

which business can increase its value in order to achieve the business goals. On the contrary,

different types of costs and cost sheet will also be discussed in this report.

1 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 1

AC 1.1 Different types of costs

Different types of costs are incurred in the manufacturing process. On the basis of

elements, costs can be classified into three elements that are material, labour and overhead.

Jeffrey & Son's company need to purchase raw material for production of product Exquisite

known as material cost. Labour convert raw material into the finished goods known as labour

cost such as wages payment. Other direct expenses include royalty that can be charged to the

product directly.

However, on the basis of function, it can be classified into factory cost, administration

cost and selling and distribution cost. Production cost involves the expenses that can be

charged to a specific cost object such as productive wages and factory lighting (Cinquini and

Tenucci, n.d.). However, expenses that cannot be charged to the cost object called non

productive expenses such as administration cost selling and marketing expenses.

Administration cost involves office stationery, staff salary and manager remuneration. On the

contrary, selling and distribution overhead includes advertisement and sales promotion.

However, according to the nature, it can be classified into direct as well as indirect

expenses. Direct cost is directly related to a specific element. However, indirect cost cannot

be attributed to a specified element. Material, labour and wages are direct production cost for

Jeffrey & Son's while indirect cost is office stationery, building rent and staff salary.

Further, on the basis of behaviour, it can be distributed to fixed, variable and semi

variable cost (Kaplan and Atkinson, 2015). Fixed cost is unrelated to the Jeffrey & Son’s

production such as building depreciation. However, variable cost is directly related to the

business production. Material, labour and overhead are variable in nature. Stepped fixed cost

gets not changed up to a specified production unit and when it gets reached it tends to

increase such as Supervisor salary. Higher the number of subordinates tends to increase their

supervisor salary. Semi variable cost remains unchanged up to a certain level after that it get

changed accordingly the production such as telephone bill.

AC 1.2 Job cost sheet

Total cost and cost per unit for Jeffrey & Son's is prepared as under:

Particulars Total cost

Direct Material 40000

Direct Labour 54000

2 | P a g e

AC 1.1 Different types of costs

Different types of costs are incurred in the manufacturing process. On the basis of

elements, costs can be classified into three elements that are material, labour and overhead.

Jeffrey & Son's company need to purchase raw material for production of product Exquisite

known as material cost. Labour convert raw material into the finished goods known as labour

cost such as wages payment. Other direct expenses include royalty that can be charged to the

product directly.

However, on the basis of function, it can be classified into factory cost, administration

cost and selling and distribution cost. Production cost involves the expenses that can be

charged to a specific cost object such as productive wages and factory lighting (Cinquini and

Tenucci, n.d.). However, expenses that cannot be charged to the cost object called non

productive expenses such as administration cost selling and marketing expenses.

Administration cost involves office stationery, staff salary and manager remuneration. On the

contrary, selling and distribution overhead includes advertisement and sales promotion.

However, according to the nature, it can be classified into direct as well as indirect

expenses. Direct cost is directly related to a specific element. However, indirect cost cannot

be attributed to a specified element. Material, labour and wages are direct production cost for

Jeffrey & Son's while indirect cost is office stationery, building rent and staff salary.

Further, on the basis of behaviour, it can be distributed to fixed, variable and semi

variable cost (Kaplan and Atkinson, 2015). Fixed cost is unrelated to the Jeffrey & Son’s

production such as building depreciation. However, variable cost is directly related to the

business production. Material, labour and overhead are variable in nature. Stepped fixed cost

gets not changed up to a specified production unit and when it gets reached it tends to

increase such as Supervisor salary. Higher the number of subordinates tends to increase their

supervisor salary. Semi variable cost remains unchanged up to a certain level after that it get

changed accordingly the production such as telephone bill.

AC 1.2 Job cost sheet

Total cost and cost per unit for Jeffrey & Son's is prepared as under:

Particulars Total cost

Direct Material 40000

Direct Labour 54000

2 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

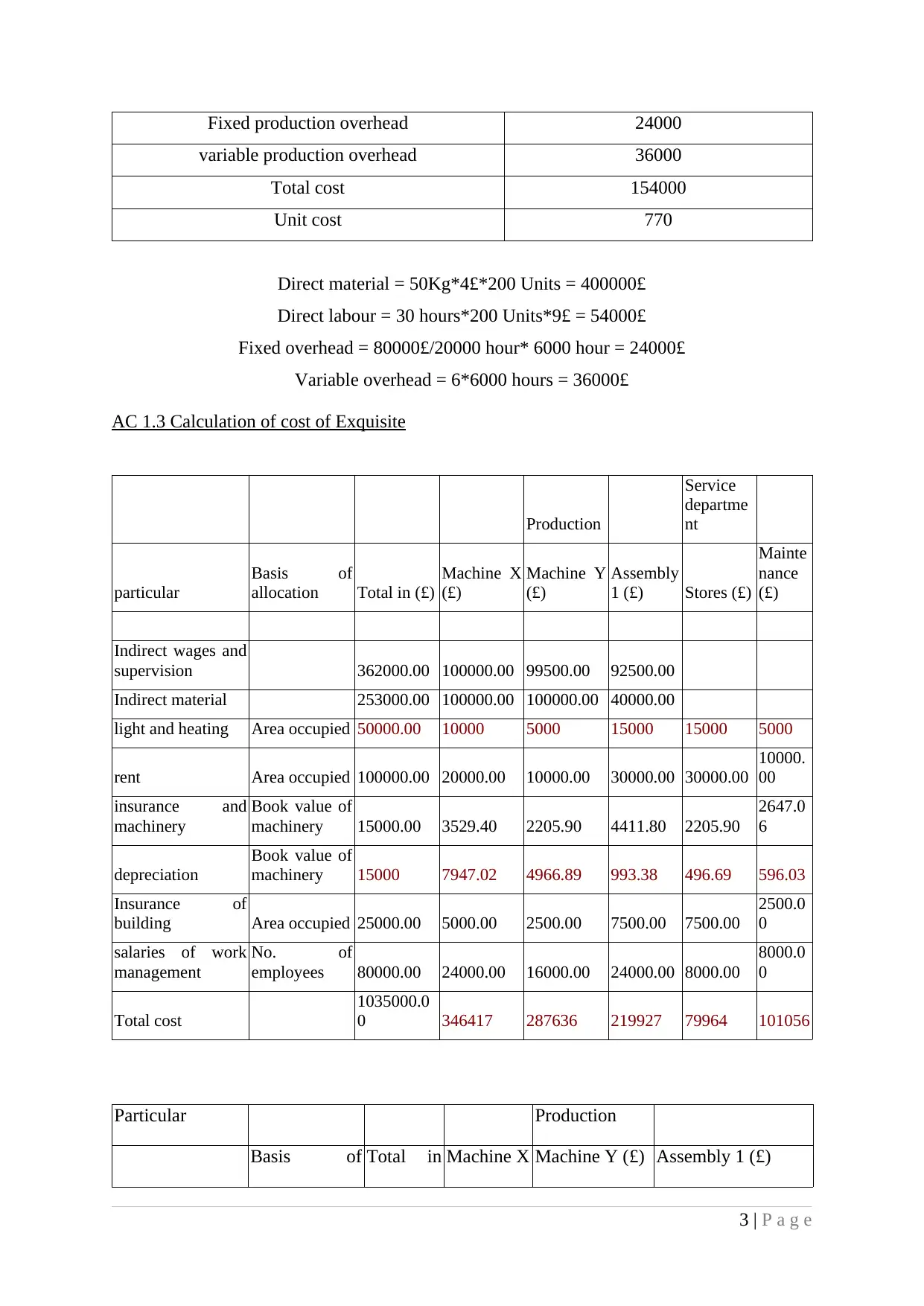

Fixed production overhead 24000

variable production overhead 36000

Total cost 154000

Unit cost 770

Direct material = 50Kg*4£*200 Units = 400000£

Direct labour = 30 hours*200 Units*9£ = 54000£

Fixed overhead = 80000£/20000 hour* 6000 hour = 24000£

Variable overhead = 6*6000 hours = 36000£

AC 1.3 Calculation of cost of Exquisite

Production

Service

departme

nt

particular

Basis of

allocation Total in (£)

Machine X

(£)

Machine Y

(£)

Assembly

1 (£) Stores (£)

Mainte

nance

(£)

Indirect wages and

supervision 362000.00 100000.00 99500.00 92500.00

Indirect material 253000.00 100000.00 100000.00 40000.00

light and heating Area occupied 50000.00 10000 5000 15000 15000 5000

rent Area occupied 100000.00 20000.00 10000.00 30000.00 30000.00

10000.

00

insurance and

machinery

Book value of

machinery 15000.00 3529.40 2205.90 4411.80 2205.90

2647.0

6

depreciation

Book value of

machinery 15000 7947.02 4966.89 993.38 496.69 596.03

Insurance of

building Area occupied 25000.00 5000.00 2500.00 7500.00 7500.00

2500.0

0

salaries of work

management

No. of

employees 80000.00 24000.00 16000.00 24000.00 8000.00

8000.0

0

Total cost

1035000.0

0 346417 287636 219927 79964 101056

Particular Production

Basis of Total in Machine X Machine Y (£) Assembly 1 (£)

3 | P a g e

variable production overhead 36000

Total cost 154000

Unit cost 770

Direct material = 50Kg*4£*200 Units = 400000£

Direct labour = 30 hours*200 Units*9£ = 54000£

Fixed overhead = 80000£/20000 hour* 6000 hour = 24000£

Variable overhead = 6*6000 hours = 36000£

AC 1.3 Calculation of cost of Exquisite

Production

Service

departme

nt

particular

Basis of

allocation Total in (£)

Machine X

(£)

Machine Y

(£)

Assembly

1 (£) Stores (£)

Mainte

nance

(£)

Indirect wages and

supervision 362000.00 100000.00 99500.00 92500.00

Indirect material 253000.00 100000.00 100000.00 40000.00

light and heating Area occupied 50000.00 10000 5000 15000 15000 5000

rent Area occupied 100000.00 20000.00 10000.00 30000.00 30000.00

10000.

00

insurance and

machinery

Book value of

machinery 15000.00 3529.40 2205.90 4411.80 2205.90

2647.0

6

depreciation

Book value of

machinery 15000 7947.02 4966.89 993.38 496.69 596.03

Insurance of

building Area occupied 25000.00 5000.00 2500.00 7500.00 7500.00

2500.0

0

salaries of work

management

No. of

employees 80000.00 24000.00 16000.00 24000.00 8000.00

8000.0

0

Total cost

1035000.0

0 346417 287636 219927 79964 101056

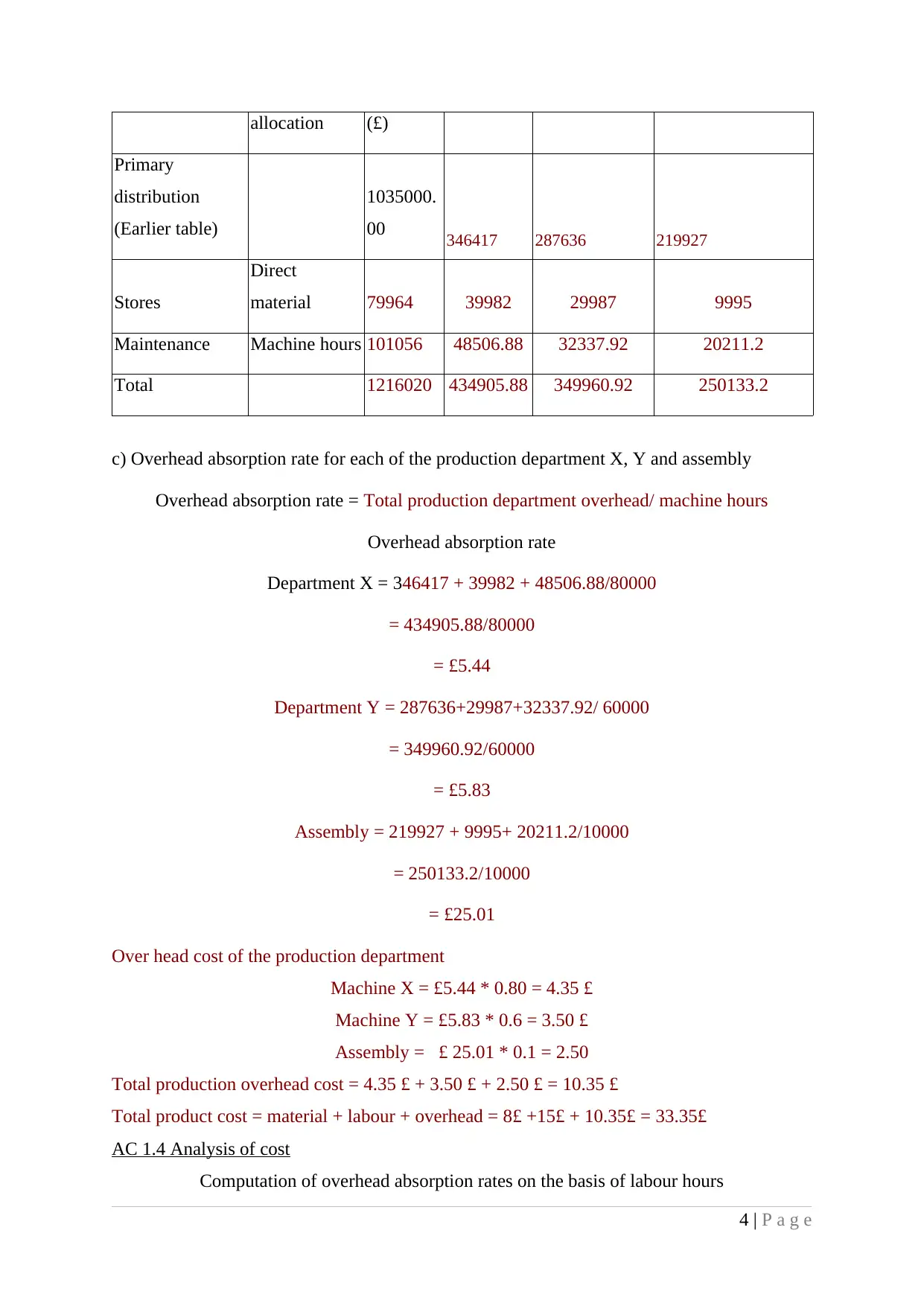

Particular Production

Basis of Total in Machine X Machine Y (£) Assembly 1 (£)

3 | P a g e

allocation (£)

Primary

distribution

(Earlier table)

1035000.

00 346417 287636 219927

Stores

Direct

material 79964 39982 29987 9995

Maintenance Machine hours 101056 48506.88 32337.92 20211.2

Total 1216020 434905.88 349960.92 250133.2

c) Overhead absorption rate for each of the production department X, Y and assembly

Overhead absorption rate = Total production department overhead/ machine hours

Overhead absorption rate

Department X = 346417 + 39982 + 48506.88/80000

= 434905.88/80000

= £5.44

Department Y = 287636+29987+32337.92/ 60000

= 349960.92/60000

= £5.83

Assembly = 219927 + 9995+ 20211.2/10000

= 250133.2/10000

= £25.01

Over head cost of the production department

Machine X = £5.44 * 0.80 = 4.35 £

Machine Y = £5.83 * 0.6 = 3.50 £

Assembly = £ 25.01 * 0.1 = 2.50

Total production overhead cost = 4.35 £ + 3.50 £ + 2.50 £ = 10.35 £

Total product cost = material + labour + overhead = 8£ +15£ + 10.35£ = 33.35£

AC 1.4 Analysis of cost

Computation of overhead absorption rates on the basis of labour hours

4 | P a g e

Primary

distribution

(Earlier table)

1035000.

00 346417 287636 219927

Stores

Direct

material 79964 39982 29987 9995

Maintenance Machine hours 101056 48506.88 32337.92 20211.2

Total 1216020 434905.88 349960.92 250133.2

c) Overhead absorption rate for each of the production department X, Y and assembly

Overhead absorption rate = Total production department overhead/ machine hours

Overhead absorption rate

Department X = 346417 + 39982 + 48506.88/80000

= 434905.88/80000

= £5.44

Department Y = 287636+29987+32337.92/ 60000

= 349960.92/60000

= £5.83

Assembly = 219927 + 9995+ 20211.2/10000

= 250133.2/10000

= £25.01

Over head cost of the production department

Machine X = £5.44 * 0.80 = 4.35 £

Machine Y = £5.83 * 0.6 = 3.50 £

Assembly = £ 25.01 * 0.1 = 2.50

Total production overhead cost = 4.35 £ + 3.50 £ + 2.50 £ = 10.35 £

Total product cost = material + labour + overhead = 8£ +15£ + 10.35£ = 33.35£

AC 1.4 Analysis of cost

Computation of overhead absorption rates on the basis of labour hours

4 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

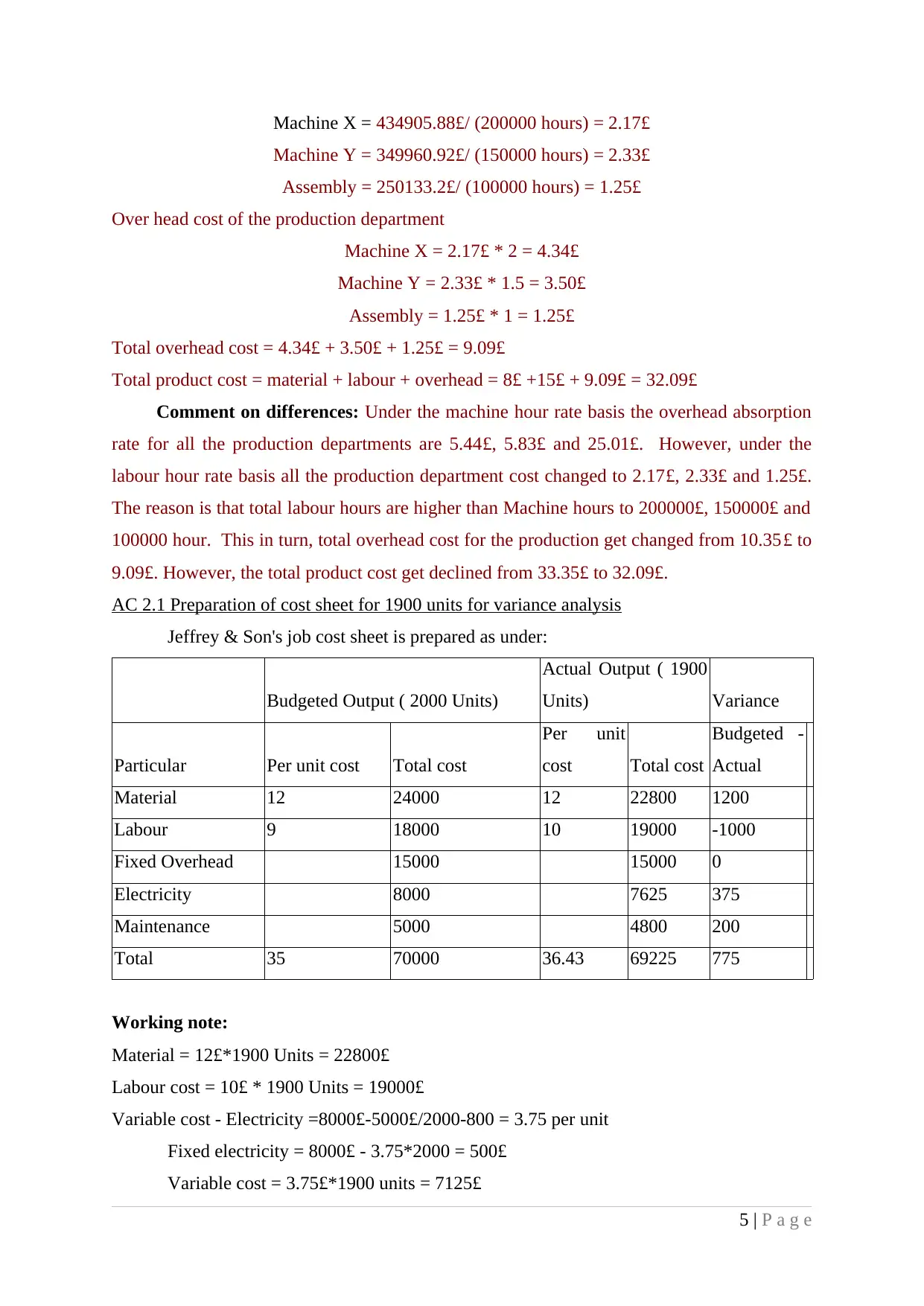

Machine X = 434905.88£/ (200000 hours) = 2.17£

Machine Y = 349960.92£/ (150000 hours) = 2.33£

Assembly = 250133.2£/ (100000 hours) = 1.25£

Over head cost of the production department

Machine X = 2.17£ * 2 = 4.34£

Machine Y = 2.33£ * 1.5 = 3.50£

Assembly = 1.25£ * 1 = 1.25£

Total overhead cost = 4.34£ + 3.50£ + 1.25£ = 9.09£

Total product cost = material + labour + overhead = 8£ +15£ + 9.09£ = 32.09£

Comment on differences: Under the machine hour rate basis the overhead absorption

rate for all the production departments are 5.44£, 5.83£ and 25.01£. However, under the

labour hour rate basis all the production department cost changed to 2.17£, 2.33£ and 1.25£.

The reason is that total labour hours are higher than Machine hours to 200000£, 150000£ and

100000 hour. This in turn, total overhead cost for the production get changed from 10.35£ to

9.09£. However, the total product cost get declined from 33.35£ to 32.09£.

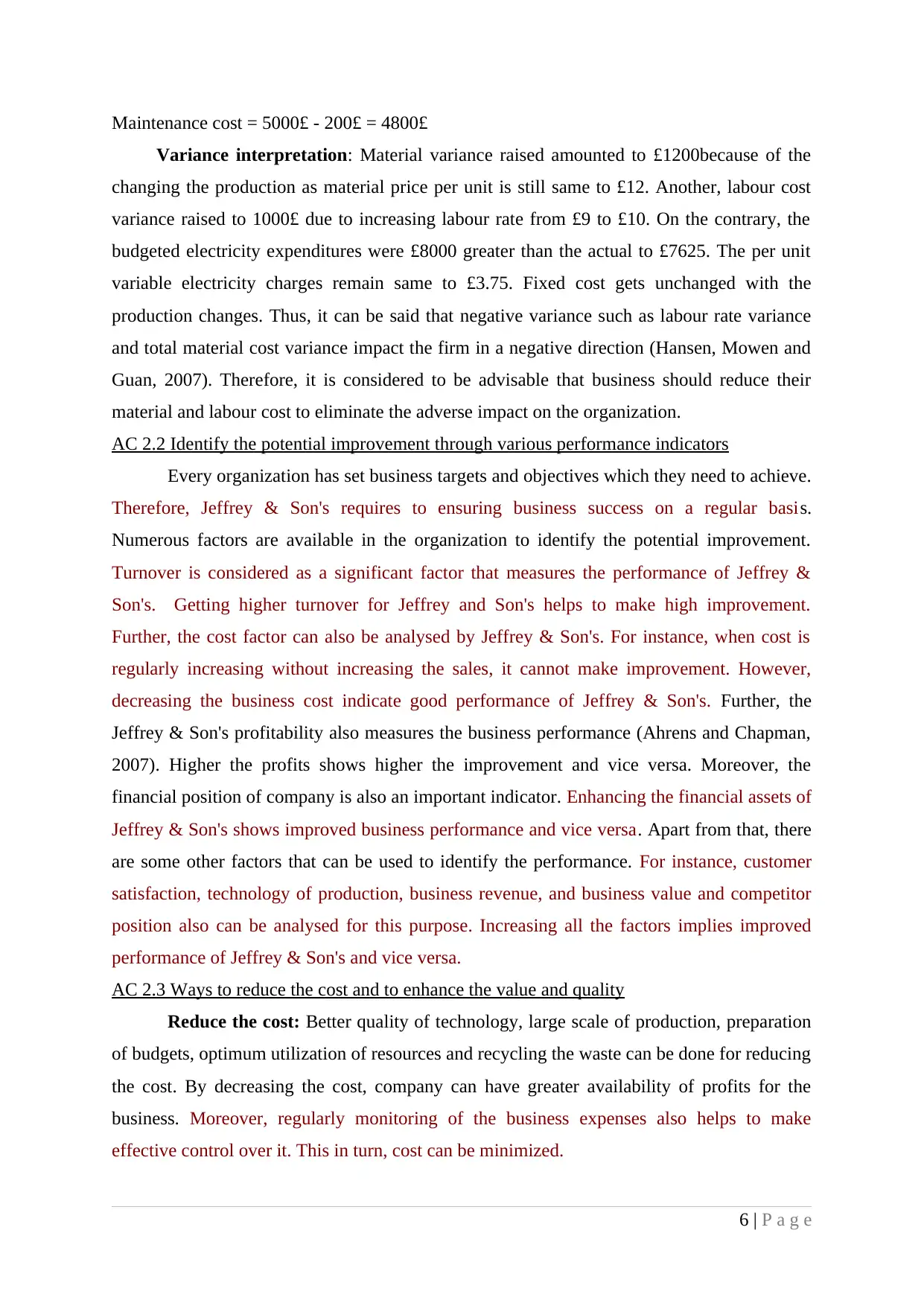

AC 2.1 Preparation of cost sheet for 1900 units for variance analysis

Jeffrey & Son's job cost sheet is prepared as under:

Budgeted Output ( 2000 Units)

Actual Output ( 1900

Units) Variance

Particular Per unit cost Total cost

Per unit

cost Total cost

Budgeted -

Actual

Material 12 24000 12 22800 1200

Labour 9 18000 10 19000 -1000

Fixed Overhead 15000 15000 0

Electricity 8000 7625 375

Maintenance 5000 4800 200

Total 35 70000 36.43 69225 775

Working note:

Material = 12£*1900 Units = 22800£

Labour cost = 10£ * 1900 Units = 19000£

Variable cost - Electricity =8000£-5000£/2000-800 = 3.75 per unit

Fixed electricity = 8000£ - 3.75*2000 = 500£

Variable cost = 3.75£*1900 units = 7125£

5 | P a g e

Machine Y = 349960.92£/ (150000 hours) = 2.33£

Assembly = 250133.2£/ (100000 hours) = 1.25£

Over head cost of the production department

Machine X = 2.17£ * 2 = 4.34£

Machine Y = 2.33£ * 1.5 = 3.50£

Assembly = 1.25£ * 1 = 1.25£

Total overhead cost = 4.34£ + 3.50£ + 1.25£ = 9.09£

Total product cost = material + labour + overhead = 8£ +15£ + 9.09£ = 32.09£

Comment on differences: Under the machine hour rate basis the overhead absorption

rate for all the production departments are 5.44£, 5.83£ and 25.01£. However, under the

labour hour rate basis all the production department cost changed to 2.17£, 2.33£ and 1.25£.

The reason is that total labour hours are higher than Machine hours to 200000£, 150000£ and

100000 hour. This in turn, total overhead cost for the production get changed from 10.35£ to

9.09£. However, the total product cost get declined from 33.35£ to 32.09£.

AC 2.1 Preparation of cost sheet for 1900 units for variance analysis

Jeffrey & Son's job cost sheet is prepared as under:

Budgeted Output ( 2000 Units)

Actual Output ( 1900

Units) Variance

Particular Per unit cost Total cost

Per unit

cost Total cost

Budgeted -

Actual

Material 12 24000 12 22800 1200

Labour 9 18000 10 19000 -1000

Fixed Overhead 15000 15000 0

Electricity 8000 7625 375

Maintenance 5000 4800 200

Total 35 70000 36.43 69225 775

Working note:

Material = 12£*1900 Units = 22800£

Labour cost = 10£ * 1900 Units = 19000£

Variable cost - Electricity =8000£-5000£/2000-800 = 3.75 per unit

Fixed electricity = 8000£ - 3.75*2000 = 500£

Variable cost = 3.75£*1900 units = 7125£

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Maintenance cost = 5000£ - 200£ = 4800£

Variance interpretation: Material variance raised amounted to £1200because of the

changing the production as material price per unit is still same to £12. Another, labour cost

variance raised to 1000£ due to increasing labour rate from £9 to £10. On the contrary, the

budgeted electricity expenditures were £8000 greater than the actual to £7625. The per unit

variable electricity charges remain same to £3.75. Fixed cost gets unchanged with the

production changes. Thus, it can be said that negative variance such as labour rate variance

and total material cost variance impact the firm in a negative direction (Hansen, Mowen and

Guan, 2007). Therefore, it is considered to be advisable that business should reduce their

material and labour cost to eliminate the adverse impact on the organization.

AC 2.2 Identify the potential improvement through various performance indicators

Every organization has set business targets and objectives which they need to achieve.

Therefore, Jeffrey & Son's requires to ensuring business success on a regular basis.

Numerous factors are available in the organization to identify the potential improvement.

Turnover is considered as a significant factor that measures the performance of Jeffrey &

Son's. Getting higher turnover for Jeffrey and Son's helps to make high improvement.

Further, the cost factor can also be analysed by Jeffrey & Son's. For instance, when cost is

regularly increasing without increasing the sales, it cannot make improvement. However,

decreasing the business cost indicate good performance of Jeffrey & Son's. Further, the

Jeffrey & Son's profitability also measures the business performance (Ahrens and Chapman,

2007). Higher the profits shows higher the improvement and vice versa. Moreover, the

financial position of company is also an important indicator. Enhancing the financial assets of

Jeffrey & Son's shows improved business performance and vice versa. Apart from that, there

are some other factors that can be used to identify the performance. For instance, customer

satisfaction, technology of production, business revenue, and business value and competitor

position also can be analysed for this purpose. Increasing all the factors implies improved

performance of Jeffrey & Son's and vice versa.

AC 2.3 Ways to reduce the cost and to enhance the value and quality

Reduce the cost: Better quality of technology, large scale of production, preparation

of budgets, optimum utilization of resources and recycling the waste can be done for reducing

the cost. By decreasing the cost, company can have greater availability of profits for the

business. Moreover, regularly monitoring of the business expenses also helps to make

effective control over it. This in turn, cost can be minimized.

6 | P a g e

Variance interpretation: Material variance raised amounted to £1200because of the

changing the production as material price per unit is still same to £12. Another, labour cost

variance raised to 1000£ due to increasing labour rate from £9 to £10. On the contrary, the

budgeted electricity expenditures were £8000 greater than the actual to £7625. The per unit

variable electricity charges remain same to £3.75. Fixed cost gets unchanged with the

production changes. Thus, it can be said that negative variance such as labour rate variance

and total material cost variance impact the firm in a negative direction (Hansen, Mowen and

Guan, 2007). Therefore, it is considered to be advisable that business should reduce their

material and labour cost to eliminate the adverse impact on the organization.

AC 2.2 Identify the potential improvement through various performance indicators

Every organization has set business targets and objectives which they need to achieve.

Therefore, Jeffrey & Son's requires to ensuring business success on a regular basis.

Numerous factors are available in the organization to identify the potential improvement.

Turnover is considered as a significant factor that measures the performance of Jeffrey &

Son's. Getting higher turnover for Jeffrey and Son's helps to make high improvement.

Further, the cost factor can also be analysed by Jeffrey & Son's. For instance, when cost is

regularly increasing without increasing the sales, it cannot make improvement. However,

decreasing the business cost indicate good performance of Jeffrey & Son's. Further, the

Jeffrey & Son's profitability also measures the business performance (Ahrens and Chapman,

2007). Higher the profits shows higher the improvement and vice versa. Moreover, the

financial position of company is also an important indicator. Enhancing the financial assets of

Jeffrey & Son's shows improved business performance and vice versa. Apart from that, there

are some other factors that can be used to identify the performance. For instance, customer

satisfaction, technology of production, business revenue, and business value and competitor

position also can be analysed for this purpose. Increasing all the factors implies improved

performance of Jeffrey & Son's and vice versa.

AC 2.3 Ways to reduce the cost and to enhance the value and quality

Reduce the cost: Better quality of technology, large scale of production, preparation

of budgets, optimum utilization of resources and recycling the waste can be done for reducing

the cost. By decreasing the cost, company can have greater availability of profits for the

business. Moreover, regularly monitoring of the business expenses also helps to make

effective control over it. This in turn, cost can be minimized.

6 | P a g e

Enhance value: Value can be increased through stabilizing or increasing the earnings

of business. Further, it can be enhanced through increasing the sales value and not the sales

prices. On the contrary, diversifying the customers and industry also help the organization for

that purpose (Lord, 2007). Moreover, lower the cost also helps to create a base against the

competitors. This in turn results in a way that business can enhance their market position that

will lead to increase the business value. Large number of customers and attract new

customers, increased shareholders return helps to enhance business value.

Quality: Quality can be enhanced through using better quality of material, innovative

techniques and implementing quality and implementing quality measurement tools so as to

ensure the qualitative products (Bhimani and et. al., 2013). This helps to get higher the

customer satisfaction level and also, to increase the number of customers that results in

increased sales and profitability. Upgraded technology, best quality of material and skilled

and abled workforce helps to improve the product quality. Quality measurement techniques

can also be applied to remove any negative consequences. This in turn, quality can be

improved.

TASK 2

AC 3.1 Purpose and nature of budgeting process

Purpose and nature of budgeting process is explained as below:

Budgeting process: It is an effective tool that is prepared through determining the

future period revenues and expenditures. It avails the positive cash balance at the end of

period. The purpose of Jeffrey & Son’s budget is to determine the business revenues and

expenditures for a given period (Lukka, 2007). Moreover, the purpose of preparing budget for

Jeffrey & Son's to determine the cash balance. It helps to determine that Jeffrey & Son's is

overspending or earnings more than the expenditures. Furthermore, identifying the net cash

flow and ending cash balance of Jeffrey & Son's is the another purpose of it. On the basis of

prepared budget, Jeffrey & Son's can control its expenditures and can eliminate the negative

variance as well.

Jeffrey & Son's managers prepare budgets through forecasting the incomes and

expenses for forthcoming year. Net cash flow is determining through identifying the

difference between total cash inflow and outflow. However, adding the opening cash balance

to the net cash flow comprises ending balance of cash for Jeffrey & Son's. In the process,

manager pays his focus on the sales volume of business. In this process, they want to enhance

the total sales volume on a regular basis so as to increase the business profits. This is because;

7 | P a g e

of business. Further, it can be enhanced through increasing the sales value and not the sales

prices. On the contrary, diversifying the customers and industry also help the organization for

that purpose (Lord, 2007). Moreover, lower the cost also helps to create a base against the

competitors. This in turn results in a way that business can enhance their market position that

will lead to increase the business value. Large number of customers and attract new

customers, increased shareholders return helps to enhance business value.

Quality: Quality can be enhanced through using better quality of material, innovative

techniques and implementing quality and implementing quality measurement tools so as to

ensure the qualitative products (Bhimani and et. al., 2013). This helps to get higher the

customer satisfaction level and also, to increase the number of customers that results in

increased sales and profitability. Upgraded technology, best quality of material and skilled

and abled workforce helps to improve the product quality. Quality measurement techniques

can also be applied to remove any negative consequences. This in turn, quality can be

improved.

TASK 2

AC 3.1 Purpose and nature of budgeting process

Purpose and nature of budgeting process is explained as below:

Budgeting process: It is an effective tool that is prepared through determining the

future period revenues and expenditures. It avails the positive cash balance at the end of

period. The purpose of Jeffrey & Son’s budget is to determine the business revenues and

expenditures for a given period (Lukka, 2007). Moreover, the purpose of preparing budget for

Jeffrey & Son's to determine the cash balance. It helps to determine that Jeffrey & Son's is

overspending or earnings more than the expenditures. Furthermore, identifying the net cash

flow and ending cash balance of Jeffrey & Son's is the another purpose of it. On the basis of

prepared budget, Jeffrey & Son's can control its expenditures and can eliminate the negative

variance as well.

Jeffrey & Son's managers prepare budgets through forecasting the incomes and

expenses for forthcoming year. Net cash flow is determining through identifying the

difference between total cash inflow and outflow. However, adding the opening cash balance

to the net cash flow comprises ending balance of cash for Jeffrey & Son's. In the process,

manager pays his focus on the sales volume of business. In this process, they want to enhance

the total sales volume on a regular basis so as to increase the business profits. This is because;

7 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

they require establishing coordination in their budgeting process. Thus, it can be said that

they are following the incremental budgeting technique for the budget preparation (Fullerton,

Kennedy and Widener, 2013). Then after, the actual results will be compared with the

budgeted figures to calculate the variance. Therefore, business can take necessary decisions

to remove such variances.

AC 3.2 Appropriate budgeting method and its need

Jeffrey & Son's prepare its budgets according to the incremental budgeting system.

The problem with this method is that management is not considering the market volatility and

its impact on the organization. Thus, they cannot meet the budgeted incomes and

expenditures to the actual values. Therefore, the organization requires changing the method

adopted. Zero base budgeting will be most suitable or appropriate method for the budget

preparation as it overcomes the limitations of incremental budgeting In search of

management accounting theory (Zimmerman and Yahya-Zadeh, 2011). In this method, the

managers estimate the entire operational cost and all the revenues as per the market

behaviour. They analyse the market changes and budget is prepared through considering their

impacts. The need for this method is that organization can remove or reduce the impact of

market uncertainties through effective planning.

AC 3.3 Preparation of production and material purchase budget for Jeffrey & Son's

Production and material purchase budget is prepared as per the given details. It helps

to identify the total production that organization requires to produce for the future period

(Lukka and Modell, 2010). Further, material purchase budget identifies the total quantity of

material that is required to purchase from the supplier for producing the required units.

Production Budget

Sales 105000 90000 105000

Op. Stock 11000 13500 15750

Total 94000 76500 89250

Closing stock 13500 15750 16500

Production 107500 92250 105750

Required working notes are given as under:

Calculation of closing stock of production = 15% of next month.

July = 15% of 90000 Units = 13500 units

August = 15% of 1050000 units = 15750 units

September = 15% of 110000 units = 16500 units

8 | P a g e

they are following the incremental budgeting technique for the budget preparation (Fullerton,

Kennedy and Widener, 2013). Then after, the actual results will be compared with the

budgeted figures to calculate the variance. Therefore, business can take necessary decisions

to remove such variances.

AC 3.2 Appropriate budgeting method and its need

Jeffrey & Son's prepare its budgets according to the incremental budgeting system.

The problem with this method is that management is not considering the market volatility and

its impact on the organization. Thus, they cannot meet the budgeted incomes and

expenditures to the actual values. Therefore, the organization requires changing the method

adopted. Zero base budgeting will be most suitable or appropriate method for the budget

preparation as it overcomes the limitations of incremental budgeting In search of

management accounting theory (Zimmerman and Yahya-Zadeh, 2011). In this method, the

managers estimate the entire operational cost and all the revenues as per the market

behaviour. They analyse the market changes and budget is prepared through considering their

impacts. The need for this method is that organization can remove or reduce the impact of

market uncertainties through effective planning.

AC 3.3 Preparation of production and material purchase budget for Jeffrey & Son's

Production and material purchase budget is prepared as per the given details. It helps

to identify the total production that organization requires to produce for the future period

(Lukka and Modell, 2010). Further, material purchase budget identifies the total quantity of

material that is required to purchase from the supplier for producing the required units.

Production Budget

Sales 105000 90000 105000

Op. Stock 11000 13500 15750

Total 94000 76500 89250

Closing stock 13500 15750 16500

Production 107500 92250 105750

Required working notes are given as under:

Calculation of closing stock of production = 15% of next month.

July = 15% of 90000 Units = 13500 units

August = 15% of 1050000 units = 15750 units

September = 15% of 110000 units = 16500 units

8 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Material Purchase Budget

Material Require 215000 184500 211500

Less- Opening stock 52000 45000 52500

Total 163000 139500 159000

Add- Closing stock 46125 52875 54250

Purchase 209125 19125 212875

Required working notes are given as under:

Calculation of closing stock of material = 25% of next month.

July = 25% of (92250 units*2kg per unit) = 46125 Kg

August = 25% of (105750 units*2Kg per unit) = 52875 kg

September = 25% of (108500 units*2kg per unit) = 54250 kg

AC 3.4 Preparation of cash budget for Jeffrey & Son's

Cash Budget is prepared through combining all the cash related transactions. It includes cash

incomes and expenditures incurred by the organization. In this budget, cash balance has two

types that are surplus or deficit. Surplus is the excess of cash incomes over the expenditures

(Malmi and Granlund, 2009). However, deficit is the negative cash balance that is the excess

of cash expenditures over the incomes.

Particular July August September

Cash balance 16000 44031 67993

Cash Receipts

Cash sales 900000 821250 864000

Total cash Income 916000 865281 931993

Cash Expenditures

Material Purchase 365969 334688 372531

Direct wages 322500 276750 317250

Variable overhead 108500 98350 100350

Fixed Overhead 75000 87500 87500

Total cash expenses 871969 797288 877631

Cash balance 44031 67993 54362

Working note:

Particular July August September

Monthly sales ( 60% ) 567000 486000 567000

9 | P a g e

Material Require 215000 184500 211500

Less- Opening stock 52000 45000 52500

Total 163000 139500 159000

Add- Closing stock 46125 52875 54250

Purchase 209125 19125 212875

Required working notes are given as under:

Calculation of closing stock of material = 25% of next month.

July = 25% of (92250 units*2kg per unit) = 46125 Kg

August = 25% of (105750 units*2Kg per unit) = 52875 kg

September = 25% of (108500 units*2kg per unit) = 54250 kg

AC 3.4 Preparation of cash budget for Jeffrey & Son's

Cash Budget is prepared through combining all the cash related transactions. It includes cash

incomes and expenditures incurred by the organization. In this budget, cash balance has two

types that are surplus or deficit. Surplus is the excess of cash incomes over the expenditures

(Malmi and Granlund, 2009). However, deficit is the negative cash balance that is the excess

of cash expenditures over the incomes.

Particular July August September

Cash balance 16000 44031 67993

Cash Receipts

Cash sales 900000 821250 864000

Total cash Income 916000 865281 931993

Cash Expenditures

Material Purchase 365969 334688 372531

Direct wages 322500 276750 317250

Variable overhead 108500 98350 100350

Fixed Overhead 75000 87500 87500

Total cash expenses 871969 797288 877631

Cash balance 44031 67993 54362

Working note:

Particular July August September

Monthly sales ( 60% ) 567000 486000 567000

9 | P a g e

Previous month sales (25%) 247500 236250 202500

Sales before two months (10%) 85500 99000 94500

Total 900000 821250 864000

Raw material: July = 1.75£ * 209125 kg of material = 365969£

August = 1.75£ * 191250 kg of material = 334688£

September = 1.75£ * 212875 = 372531£

Direct wages: July = 3£ * 107500 units = 322500£

August = 3£ * 92250 units = 276750£

September = 3£ * 105750 units = 317250£

Variable overhead: July = (107500£*60%) + (110000£*40%) = 108500£

August = (92250*60%) + (107500£*40%) = 98350£

September = (105750£*60%) + (92250£*40%) = 100350£

Interpretation of budget: Sales of the business shows a decreasing trend from

90000£ to 821250£. Further, it get improved to 864000£ in the month of September.

Therefore, the business total cash income declined in the month of August and increased in

the month of September. Further, the direct wages of the business get declined from 322500£

to 276750£ in the month of August. However, in the month of September it gets increased to

317250£. On contrary, the total variable overhead of the business get decreased in the month

of August to 98350£ while inclined to 100350£ in the month of September. However, the

cash balance at the end of the months are 44031£, 67993£ and 54362£. On the basis of that, it

can be reported that business has to increase its sales and reduce its cost throw curtailment of

unnecessary expenditures (Bisbe, Batista-Foguet and Chenhall, 2007). This in turn, Jeffrey &

Son's will be able to increase the positive cash balance at the end of the period.

10 | P a g e

Sales before two months (10%) 85500 99000 94500

Total 900000 821250 864000

Raw material: July = 1.75£ * 209125 kg of material = 365969£

August = 1.75£ * 191250 kg of material = 334688£

September = 1.75£ * 212875 = 372531£

Direct wages: July = 3£ * 107500 units = 322500£

August = 3£ * 92250 units = 276750£

September = 3£ * 105750 units = 317250£

Variable overhead: July = (107500£*60%) + (110000£*40%) = 108500£

August = (92250*60%) + (107500£*40%) = 98350£

September = (105750£*60%) + (92250£*40%) = 100350£

Interpretation of budget: Sales of the business shows a decreasing trend from

90000£ to 821250£. Further, it get improved to 864000£ in the month of September.

Therefore, the business total cash income declined in the month of August and increased in

the month of September. Further, the direct wages of the business get declined from 322500£

to 276750£ in the month of August. However, in the month of September it gets increased to

317250£. On contrary, the total variable overhead of the business get decreased in the month

of August to 98350£ while inclined to 100350£ in the month of September. However, the

cash balance at the end of the months are 44031£, 67993£ and 54362£. On the basis of that, it

can be reported that business has to increase its sales and reduce its cost throw curtailment of

unnecessary expenditures (Bisbe, Batista-Foguet and Chenhall, 2007). This in turn, Jeffrey &

Son's will be able to increase the positive cash balance at the end of the period.

10 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.