MANAGERIAL ACCOUNTING.

VerifiedAdded on 2023/04/05

|25

|4535

|301

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

MANAGERIAL ACCOUNTING

Table of Contents

Question No 1..................................................................................................................................3

Requirement 1a............................................................................................................................3

Requirement 1b............................................................................................................................4

Requirement 1c............................................................................................................................6

Question No 2..................................................................................................................................7

Requirement 2a............................................................................................................................7

Requirement 2a............................................................................................................................8

Requirement 2c............................................................................................................................9

Requirement 2d............................................................................................................................9

Requirement 2e..........................................................................................................................10

Question 3:.....................................................................................................................................12

Part A:........................................................................................................................................12

Requirement a:.......................................................................................................................13

Requirement b:.......................................................................................................................14

Part B:........................................................................................................................................15

Question 4:.....................................................................................................................................15

Requirement a:...........................................................................................................................15

Requirement b:...........................................................................................................................16

Question 5:.....................................................................................................................................19

MANAGERIAL ACCOUNTING

Table of Contents

Question No 1..................................................................................................................................3

Requirement 1a............................................................................................................................3

Requirement 1b............................................................................................................................4

Requirement 1c............................................................................................................................6

Question No 2..................................................................................................................................7

Requirement 2a............................................................................................................................7

Requirement 2a............................................................................................................................8

Requirement 2c............................................................................................................................9

Requirement 2d............................................................................................................................9

Requirement 2e..........................................................................................................................10

Question 3:.....................................................................................................................................12

Part A:........................................................................................................................................12

Requirement a:.......................................................................................................................13

Requirement b:.......................................................................................................................14

Part B:........................................................................................................................................15

Question 4:.....................................................................................................................................15

Requirement a:...........................................................................................................................15

Requirement b:...........................................................................................................................16

Question 5:.....................................................................................................................................19

2

MANAGERIAL ACCOUNTING

Requirement a:...........................................................................................................................19

Part (i):...................................................................................................................................19

Part (ii):..................................................................................................................................19

Requirement b:...........................................................................................................................20

Requirement c:...........................................................................................................................21

References:....................................................................................................................................23

MANAGERIAL ACCOUNTING

Requirement a:...........................................................................................................................19

Part (i):...................................................................................................................................19

Part (ii):..................................................................................................................................19

Requirement b:...........................................................................................................................20

Requirement c:...........................................................................................................................21

References:....................................................................................................................................23

3

MANAGERIAL ACCOUNTING

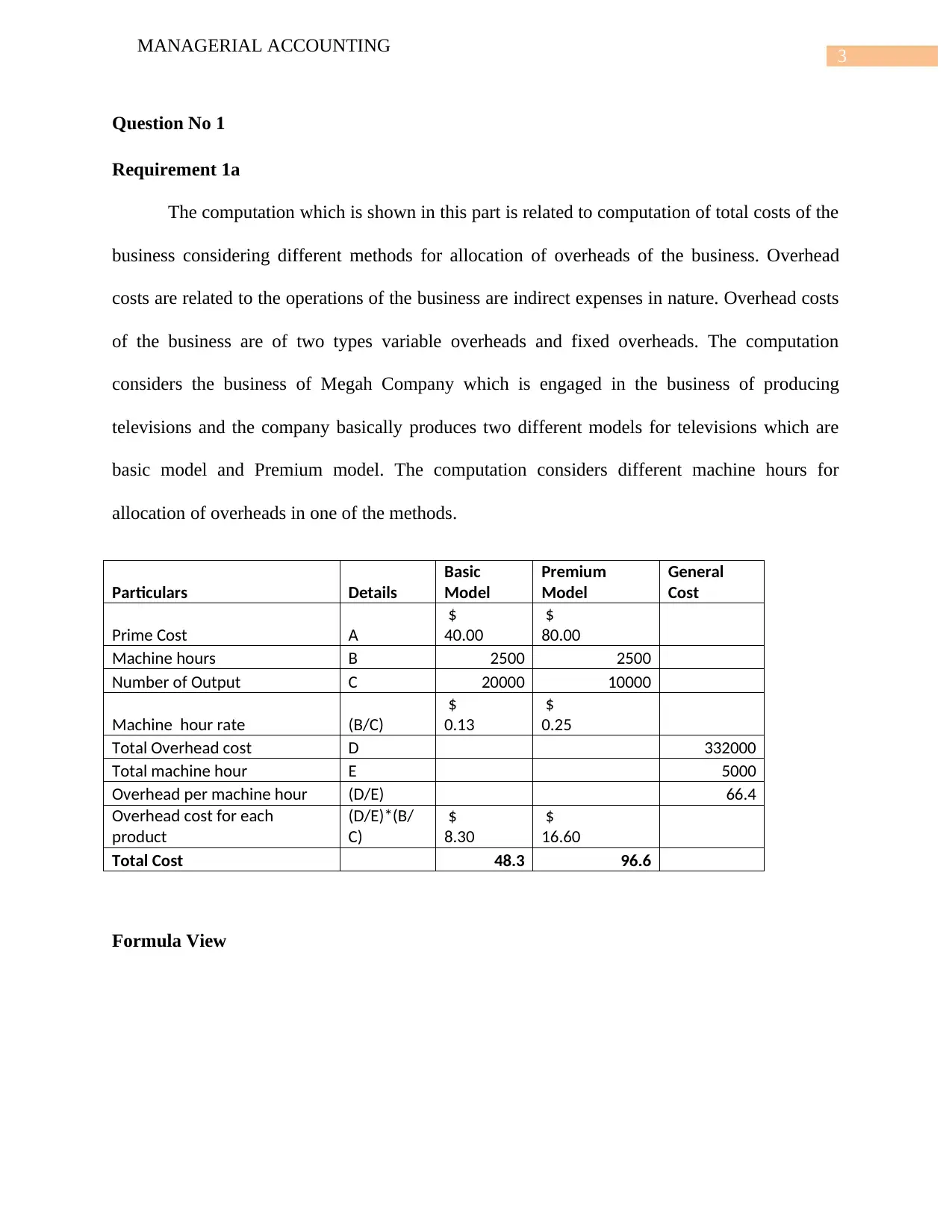

Question No 1

Requirement 1a

The computation which is shown in this part is related to computation of total costs of the

business considering different methods for allocation of overheads of the business. Overhead

costs are related to the operations of the business are indirect expenses in nature. Overhead costs

of the business are of two types variable overheads and fixed overheads. The computation

considers the business of Megah Company which is engaged in the business of producing

televisions and the company basically produces two different models for televisions which are

basic model and Premium model. The computation considers different machine hours for

allocation of overheads in one of the methods.

Particulars Details

Basic

Model

Premium

Model

General

Cost

Prime Cost A

$

40.00

$

80.00

Machine hours B 2500 2500

Number of Output C 20000 10000

Machine hour rate (B/C)

$

0.13

$

0.25

Total Overhead cost D 332000

Total machine hour E 5000

Overhead per machine hour (D/E) 66.4

Overhead cost for each

product

(D/E)*(B/

C)

$

8.30

$

16.60

Total Cost 48.3 96.6

Formula View

MANAGERIAL ACCOUNTING

Question No 1

Requirement 1a

The computation which is shown in this part is related to computation of total costs of the

business considering different methods for allocation of overheads of the business. Overhead

costs are related to the operations of the business are indirect expenses in nature. Overhead costs

of the business are of two types variable overheads and fixed overheads. The computation

considers the business of Megah Company which is engaged in the business of producing

televisions and the company basically produces two different models for televisions which are

basic model and Premium model. The computation considers different machine hours for

allocation of overheads in one of the methods.

Particulars Details

Basic

Model

Premium

Model

General

Cost

Prime Cost A

$

40.00

$

80.00

Machine hours B 2500 2500

Number of Output C 20000 10000

Machine hour rate (B/C)

$

0.13

$

0.25

Total Overhead cost D 332000

Total machine hour E 5000

Overhead per machine hour (D/E) 66.4

Overhead cost for each

product

(D/E)*(B/

C)

$

8.30

$

16.60

Total Cost 48.3 96.6

Formula View

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

MANAGERIAL ACCOUNTING

It can be seen from the above calculation that company cost for its product are different.

The total cost of the product has been determined by adding prime cost and overhead cost. The

overhead cost is calculated by total productive machine hours. The overhead costs which is

computed has an important part in computing the totals costs of the business and also deciding

how much profits can be generated by the business.

Requirement 1b

The calculation of unit cost of each model with the help of four activity driver

Activity Cost Driver

Estimated

Overhead Cost

Estimated Cost Driver

Activity

Predetermined Cost

Overhead

Purchasing

Material

Purchase

Requisitions 87000 2000 43.5

Maintaining

Equipment

Maintaince

Hour 220000 8000 27.5

Setting up

Equipment Set up time 112000 40 2800

Below we can see the total cost of the product under activity based costing

Particular Details

Basic

Model

Premium

Model General

Prime Cost A

$

40.00

$

80.00

Number of Requisitions B 500 1500

Maintaince Hour C 2000 6000

Set up time D 8 32

Overhead on Maintance E 27.5

Overhead on Purchase F 43.5

MANAGERIAL ACCOUNTING

It can be seen from the above calculation that company cost for its product are different.

The total cost of the product has been determined by adding prime cost and overhead cost. The

overhead cost is calculated by total productive machine hours. The overhead costs which is

computed has an important part in computing the totals costs of the business and also deciding

how much profits can be generated by the business.

Requirement 1b

The calculation of unit cost of each model with the help of four activity driver

Activity Cost Driver

Estimated

Overhead Cost

Estimated Cost Driver

Activity

Predetermined Cost

Overhead

Purchasing

Material

Purchase

Requisitions 87000 2000 43.5

Maintaining

Equipment

Maintaince

Hour 220000 8000 27.5

Setting up

Equipment Set up time 112000 40 2800

Below we can see the total cost of the product under activity based costing

Particular Details

Basic

Model

Premium

Model General

Prime Cost A

$

40.00

$

80.00

Number of Requisitions B 500 1500

Maintaince Hour C 2000 6000

Set up time D 8 32

Overhead on Maintance E 27.5

Overhead on Purchase F 43.5

5

MANAGERIAL ACCOUNTING

Overhead on Set up G 2800

overhead chareged for all product H

$

99,150.00

$

3,19,850.00

Number of unit produced I 20000 10000

Overhead per product (H/I) 4.9575 31.985

Total cost

$

44.96

$

111.99

Formula View

Activity based costing refers to the costing which allocate the overhead as per the activity

perform. It sees the relation of the overhead, the cost and the manufacturing and through the

relationship it allocates the overhead cost. Activity based costing is considered to be one of the

most useful techniques for the purpose of identifying and accurately allocating the costs of the

business to the products. The costing technique is used in major businesses for computing anf

allocating costs of the business. As there some expenses which are of high costly nature so this

help the organization about the level of increasing the cost of the product. As there are many

costs which cannot be allocated through cost accounting method so to remove the barrier these

costs came into the picture.

MANAGERIAL ACCOUNTING

Overhead on Set up G 2800

overhead chareged for all product H

$

99,150.00

$

3,19,850.00

Number of unit produced I 20000 10000

Overhead per product (H/I) 4.9575 31.985

Total cost

$

44.96

$

111.99

Formula View

Activity based costing refers to the costing which allocate the overhead as per the activity

perform. It sees the relation of the overhead, the cost and the manufacturing and through the

relationship it allocates the overhead cost. Activity based costing is considered to be one of the

most useful techniques for the purpose of identifying and accurately allocating the costs of the

business to the products. The costing technique is used in major businesses for computing anf

allocating costs of the business. As there some expenses which are of high costly nature so this

help the organization about the level of increasing the cost of the product. As there are many

costs which cannot be allocated through cost accounting method so to remove the barrier these

costs came into the picture.

6

MANAGERIAL ACCOUNTING

Requirement 1c

Costing is a process which help the company to evaluate the cost of its business and help

them to get an overview of the market. Each company follow the different method of costing.

The process of computing the costs of the business is considered to be very important as they

have direct impact on the revenue and profits which is generated by the business. In addition to

this, the costs of the business also have an important role in determination of the price for the

products which is offered by the business. There are different costing techniques which are

available to the management of the company for computing total costs of the business and also

allocation of the indirect costs of the business. In the above it has been seen that company has

used two different method of costing one is Plant Wide Rate and another one is Activity Based

Costing.

Plant wide rate –It is the rate which assign all the company manufacturing overhead cost

to its production cost. It is a simple concept as it allocates at one rate so the costing of the

overhead become very easy and no complex method is used. The method is followed by

businesses as the method does not involve any complexities and it is much easier to

understand while conducting a review of the system.

Activity based costing – Under this method the cost is allocate as per the activity. It is

done for different overhead different rates are being used. The allocation of indirect costs

of the business are done on the basis of the activities which are carried out by the

business. This is considered to be the most popular and effective method for allocation

and computation of costs of the business and in most of the situation, the method is

known to provide the most accurate estimates.

MANAGERIAL ACCOUNTING

Requirement 1c

Costing is a process which help the company to evaluate the cost of its business and help

them to get an overview of the market. Each company follow the different method of costing.

The process of computing the costs of the business is considered to be very important as they

have direct impact on the revenue and profits which is generated by the business. In addition to

this, the costs of the business also have an important role in determination of the price for the

products which is offered by the business. There are different costing techniques which are

available to the management of the company for computing total costs of the business and also

allocation of the indirect costs of the business. In the above it has been seen that company has

used two different method of costing one is Plant Wide Rate and another one is Activity Based

Costing.

Plant wide rate –It is the rate which assign all the company manufacturing overhead cost

to its production cost. It is a simple concept as it allocates at one rate so the costing of the

overhead become very easy and no complex method is used. The method is followed by

businesses as the method does not involve any complexities and it is much easier to

understand while conducting a review of the system.

Activity based costing – Under this method the cost is allocate as per the activity. It is

done for different overhead different rates are being used. The allocation of indirect costs

of the business are done on the basis of the activities which are carried out by the

business. This is considered to be the most popular and effective method for allocation

and computation of costs of the business and in most of the situation, the method is

known to provide the most accurate estimates.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGERIAL ACCOUNTING

Activity based costing is better method than plant wide method as in activity costing the

overhead are allocated as per the activity so it helps the organization to know how the product

price is rising. The main advantage of activity-based costing is that it gives an accurate

estimation of costs and appropriate allocation of overhead costs on the basis of activities which is

carried out by businesses. Therefore, it can be clearly indicated that if the business follows

activity-based costing techniques than it would give a better presentation of the total cost and

also assist in the determination of prices for the business.

Question No 2

Requirement 2a

Break even analysis is a widely used technique by management accountants and

production manager. It is based on the production costs which are divided into two parts one is

variable cost which varies with the production unit and another one is fixed cost which remain

same in respect of production unit. Both cost is combined than it is compared with sales revenue

to get the position where by selling certain amount of goods company is earning neither profit

nor loss and that point is termed as break-even point.

In other words, breakeven analysis is very useful tool for taking vital decisions of the

business. The breakeven analysis tells the management the required units or revenue which the

management of the company needs to generate in order to at least cover the costs of the business

and reach a no profit no loss situation. On the basis of breakeven analysis, the management of

the company decide what prices are to be set for the products and what quantity of products the

management needs to sell in order to reach a no profit no loss situation. In addition to this,

breakeven point needs to be achieved by the business in order to ensure that the business

MANAGERIAL ACCOUNTING

Activity based costing is better method than plant wide method as in activity costing the

overhead are allocated as per the activity so it helps the organization to know how the product

price is rising. The main advantage of activity-based costing is that it gives an accurate

estimation of costs and appropriate allocation of overhead costs on the basis of activities which is

carried out by businesses. Therefore, it can be clearly indicated that if the business follows

activity-based costing techniques than it would give a better presentation of the total cost and

also assist in the determination of prices for the business.

Question No 2

Requirement 2a

Break even analysis is a widely used technique by management accountants and

production manager. It is based on the production costs which are divided into two parts one is

variable cost which varies with the production unit and another one is fixed cost which remain

same in respect of production unit. Both cost is combined than it is compared with sales revenue

to get the position where by selling certain amount of goods company is earning neither profit

nor loss and that point is termed as break-even point.

In other words, breakeven analysis is very useful tool for taking vital decisions of the

business. The breakeven analysis tells the management the required units or revenue which the

management of the company needs to generate in order to at least cover the costs of the business

and reach a no profit no loss situation. On the basis of breakeven analysis, the management of

the company decide what prices are to be set for the products and what quantity of products the

management needs to sell in order to reach a no profit no loss situation. In addition to this,

breakeven point needs to be achieved by the business in order to ensure that the business

8

MANAGERIAL ACCOUNTING

continues its operations for a long period of time. The requirement of the part is to undertake

breakeven and sensitivity analysis for AzamJuta which is engaged in production process.

Management of a company uses breakeven analysis for the purpose of taking important decisions

relating to the business.

Requirement 2a

Calculation of break-even point in unit as well in sales revenue.

Break-even point in units = (Total fixed cost / Contribution per unit)

Particular Details Amount Unit

Contribution A

$

3,50,000.00

No of unit B 100000

Contribution per

unit (A/B)

$

3.50

Particular Details Amount UNIT

Total Fixed Cost A

$

2,10,000.00

Contribution per unit B

$

3.50

Break even in units (A/B) 60000

Break-even point in sales revenue = (Break-even in units * Sales per unit)

Particular Details Amount Unit

Sales A

$

7,50,000.00

No of unit sold B 100000

Sales per unit (A/B)

$

7.50

Break- even unit D 60000

Break-even in sales (A/B)*D

$

4,50,000.00

MANAGERIAL ACCOUNTING

continues its operations for a long period of time. The requirement of the part is to undertake

breakeven and sensitivity analysis for AzamJuta which is engaged in production process.

Management of a company uses breakeven analysis for the purpose of taking important decisions

relating to the business.

Requirement 2a

Calculation of break-even point in unit as well in sales revenue.

Break-even point in units = (Total fixed cost / Contribution per unit)

Particular Details Amount Unit

Contribution A

$

3,50,000.00

No of unit B 100000

Contribution per

unit (A/B)

$

3.50

Particular Details Amount UNIT

Total Fixed Cost A

$

2,10,000.00

Contribution per unit B

$

3.50

Break even in units (A/B) 60000

Break-even point in sales revenue = (Break-even in units * Sales per unit)

Particular Details Amount Unit

Sales A

$

7,50,000.00

No of unit sold B 100000

Sales per unit (A/B)

$

7.50

Break- even unit D 60000

Break-even in sales (A/B)*D

$

4,50,000.00

9

MANAGERIAL ACCOUNTING

Requirement 2c

Calculation of margin of safety in both units as well as sale revenue

Margin of safety in units = (Total profit / Contribution per unit)

Particular Details Amount Unit

Total profit A

$

1,40,000.00

Contribution per

unit B

$

3.50

MOS in unit (A/B) 40000

Margin of safety in sales revenue = (Total Sales – Break-Even sales)

Particular Details Amount

Total Sales A

$

7,50,000.00

Break-even sales B

$

4,50,000.00

MOS in sales (A-B)

$

3,00,000.00

Requirement 2d

As the company want to increase their sales from 8000 units and for that the company is

ready to incur for advertisement expenses. The estimation of the sales manager is that increase in

the sales of the business would be enhancing the revenue of the business. The calculations which

MANAGERIAL ACCOUNTING

Requirement 2c

Calculation of margin of safety in both units as well as sale revenue

Margin of safety in units = (Total profit / Contribution per unit)

Particular Details Amount Unit

Total profit A

$

1,40,000.00

Contribution per

unit B

$

3.50

MOS in unit (A/B) 40000

Margin of safety in sales revenue = (Total Sales – Break-Even sales)

Particular Details Amount

Total Sales A

$

7,50,000.00

Break-even sales B

$

4,50,000.00

MOS in sales (A-B)

$

3,00,000.00

Requirement 2d

As the company want to increase their sales from 8000 units and for that the company is

ready to incur for advertisement expenses. The estimation of the sales manager is that increase in

the sales of the business would be enhancing the revenue of the business. The calculations which

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

MANAGERIAL ACCOUNTING

is presented below shows the extra expenses which the management of the company is willing to

undertake for the purpose of enhancing the sales of the business.

Calculation as per company new proposal

Particular Details Amount Unit

Sales in unit A 108000

Sales per unit B

$

7.50

Total sales (A*B)

$

8,10,000.00

Variable cost per unit D

$

4.00

Total variable cost (D*A)

$

4,32,000.00

Total fixed cost E

$

2,10,000.00

Advertisement cost F

$

22,000.00

Total cost (D*A)+E+F

$

6,64,000.00

Total profit (A*B)-{(D*A)+E+F}

$

1,46,000.00

It can be seen from the above calculation that previously the company was earning

$140000 when they were selling 100000 units but when they did advertisement expense of

$22000 than they able to sell 108000 and then the profit was $146000 so it can be said that by

the new proposal which company is thinking for implement than they will able to earn (146000-

140000) profit that is more $6000 profit they will able to earn if they invest $22000 on

advertisement so there income will increase by $6000.

Requirement 2e

The maximum amount which the company can invest on advertisement to increase their

sale by 8000 units and not by affecting the current profit. The amount which can be invested is

MANAGERIAL ACCOUNTING

is presented below shows the extra expenses which the management of the company is willing to

undertake for the purpose of enhancing the sales of the business.

Calculation as per company new proposal

Particular Details Amount Unit

Sales in unit A 108000

Sales per unit B

$

7.50

Total sales (A*B)

$

8,10,000.00

Variable cost per unit D

$

4.00

Total variable cost (D*A)

$

4,32,000.00

Total fixed cost E

$

2,10,000.00

Advertisement cost F

$

22,000.00

Total cost (D*A)+E+F

$

6,64,000.00

Total profit (A*B)-{(D*A)+E+F}

$

1,46,000.00

It can be seen from the above calculation that previously the company was earning

$140000 when they were selling 100000 units but when they did advertisement expense of

$22000 than they able to sell 108000 and then the profit was $146000 so it can be said that by

the new proposal which company is thinking for implement than they will able to earn (146000-

140000) profit that is more $6000 profit they will able to earn if they invest $22000 on

advertisement so there income will increase by $6000.

Requirement 2e

The maximum amount which the company can invest on advertisement to increase their

sale by 8000 units and not by affecting the current profit. The amount which can be invested is

11

MANAGERIAL ACCOUNTING

(22000+6000) = 28000 so till $28000 company can invest in advertisement and this will not

make any impact on their current profit which is $140000.

MANAGERIAL ACCOUNTING

(22000+6000) = 28000 so till $28000 company can invest in advertisement and this will not

make any impact on their current profit which is $140000.

12

MANAGERIAL ACCOUNTING

Question 3:

Part A:

For computing the relevant and irrelevant costs and benefits of expanding into new space,

the following calculation has been performed:

Particulars Details Amount

Benefits:

Increase in sales per month A $ 10,000

Total benefits B=A $ 10,000

Relevant costs:

Increase in variable cost per

month C=Ax40% $ 4,000

Increase in rent per month D $ 12,000

Refrigerators and counters costs E $ 25,000

Cost of cash registers F=$1,500x2 $ 3,000

Total relevant costs G=C+D+E+F $ 44,000

Irrelevant cost:

Depreciation of current cash

register H $ 250

Total irrelevant cost H=I $ 250

MANAGERIAL ACCOUNTING

Question 3:

Part A:

For computing the relevant and irrelevant costs and benefits of expanding into new space,

the following calculation has been performed:

Particulars Details Amount

Benefits:

Increase in sales per month A $ 10,000

Total benefits B=A $ 10,000

Relevant costs:

Increase in variable cost per

month C=Ax40% $ 4,000

Increase in rent per month D $ 12,000

Refrigerators and counters costs E $ 25,000

Cost of cash registers F=$1,500x2 $ 3,000

Total relevant costs G=C+D+E+F $ 44,000

Irrelevant cost:

Depreciation of current cash

register H $ 250

Total irrelevant cost H=I $ 250

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

MANAGERIAL ACCOUNTING

Requirement a:

With the help of relevant costing, it is possible to ascertain the objective cost of a

business decision (Benson et al., 2015). An objective measure of the business decision cost is the

degree of cash outflows, which would result from its implementation. The identification of

relevant costing techniques would help in making appropriate strategies for the business. In

addition to this, the management of the company can effectively identify relevant costs and

formulate strategies for eliminating the non-relevant costs of the business. The focus of relevant

costing is only on undertaking sound business decisions and it does not take into consideration

the other costs, which have no impact on future cash flows (Braun et al., 2014).

From the provided information, it has been identified that Masha Mekar has to bear

certain relevant costs. These costs mainly include the following:

Increase in variable cost per month by $4,000

Increase in rent per month by $12,000

Cost of new refrigerators and counters amounting to $25,000

Cost of two new cash registers costing $1,500 each

By expanding into a new space, Masha Mekar would be able to serve additional

customers and it is anticipated that there would be increase in sales revenue by $10,000 each

month. Moreover, it becomes possible to diversify the products and services as well. One

product might not be popular in a region; however, the situation might be different in other

regions (Butler & Ghosh, 2015). Thus, with the help of multiple locations, Always Blooming

could buffer its business from losses.

MANAGERIAL ACCOUNTING

Requirement a:

With the help of relevant costing, it is possible to ascertain the objective cost of a

business decision (Benson et al., 2015). An objective measure of the business decision cost is the

degree of cash outflows, which would result from its implementation. The identification of

relevant costing techniques would help in making appropriate strategies for the business. In

addition to this, the management of the company can effectively identify relevant costs and

formulate strategies for eliminating the non-relevant costs of the business. The focus of relevant

costing is only on undertaking sound business decisions and it does not take into consideration

the other costs, which have no impact on future cash flows (Braun et al., 2014).

From the provided information, it has been identified that Masha Mekar has to bear

certain relevant costs. These costs mainly include the following:

Increase in variable cost per month by $4,000

Increase in rent per month by $12,000

Cost of new refrigerators and counters amounting to $25,000

Cost of two new cash registers costing $1,500 each

By expanding into a new space, Masha Mekar would be able to serve additional

customers and it is anticipated that there would be increase in sales revenue by $10,000 each

month. Moreover, it becomes possible to diversify the products and services as well. One

product might not be popular in a region; however, the situation might be different in other

regions (Butler & Ghosh, 2015). Thus, with the help of multiple locations, Always Blooming

could buffer its business from losses.

14

MANAGERIAL ACCOUNTING

The benefits of business growth are not limited to business diversification, as expansion

into new areas provides the opportunity for increased brand recognition. In addition to this,

this also means that the business would be able to generate more sales for the business and

also reach out to more customers. When Always Blooming has planned to expand its

business, it implies the chances of arriving at a broader audience by enforcing marketing

tactics to increase the awareness of the organisation among the current and prospective

customers. This will help the management of the company in creating a brand name for itself

and also enhancing the level of operations of the business. Moreover, the revenue which is

generated by the management of the company would also enhance significantly.

Requirement b:

In the words of Dopson and Hayes (2016), sunk cost is an expense that has been incurred

already in the past. This cost is deemed to be not relevant, since it has no impact on the future

business cash flows. In case of the provided case study, the old refrigerator and cash register

could be categorised under sunk cost, since they have been purchased two years ago. Moreover,

the depreciation cost of the current cash register is not relevant, since they do not have impact on

the cash flows of the organisation. The other irrelevant costs for Always Blooming include the

following:

Current rental cost of $1,000 per month

Purchase price of the two refrigerators bought two years ago for $6,000 each

Purchase price of the existing cash register bought two years back for $1,000

Existing sales volume

Existing variable costs

MANAGERIAL ACCOUNTING

The benefits of business growth are not limited to business diversification, as expansion

into new areas provides the opportunity for increased brand recognition. In addition to this,

this also means that the business would be able to generate more sales for the business and

also reach out to more customers. When Always Blooming has planned to expand its

business, it implies the chances of arriving at a broader audience by enforcing marketing

tactics to increase the awareness of the organisation among the current and prospective

customers. This will help the management of the company in creating a brand name for itself

and also enhancing the level of operations of the business. Moreover, the revenue which is

generated by the management of the company would also enhance significantly.

Requirement b:

In the words of Dopson and Hayes (2016), sunk cost is an expense that has been incurred

already in the past. This cost is deemed to be not relevant, since it has no impact on the future

business cash flows. In case of the provided case study, the old refrigerator and cash register

could be categorised under sunk cost, since they have been purchased two years ago. Moreover,

the depreciation cost of the current cash register is not relevant, since they do not have impact on

the cash flows of the organisation. The other irrelevant costs for Always Blooming include the

following:

Current rental cost of $1,000 per month

Purchase price of the two refrigerators bought two years ago for $6,000 each

Purchase price of the existing cash register bought two years back for $1,000

Existing sales volume

Existing variable costs

15

MANAGERIAL ACCOUNTING

Therefore, it could be said that irrelevant costs are the costs, which are not influenced by the

final decision. More precisely, these costs have to be incurred in all considered managerial

incentives (Gitman, Juchau & Flanagan, 2015). Since these costs stay same in all alternatives,

they are irrelevant and they need not be considered in computations conducted for managerial

analysis. The management only needs to consider the relevant costs of the business in decision

making process and provide all efforts in reducing the costs of the business for enhancing the

profitability of the business.

Part B:

The costs that would be incurred irrespective of accepting or rejecting a special order

decision are deemed to be irrelevant for special order decisions. On certain occasions, the

recurring fixed costs of an organisation would stay the same in total; in case of acceptance of a

special order (Horngren & Harrison, 2015). Moreover, when a special order is accepted, it might

lead to additional fixed expenses. In such cases, relevance could be found in these excess fixed

costs and therefore, consideration needs to be made in incremental analysis. However, there is no

relevance of sunk costs with any process of special order decision. Special order decisions are

considered only when an organisation is running below capacity. As a result, there would be

existence of fixed overhead cost regardless of accepting or rejecting an order (Kaplan &

Atkinson, 2015). Since fixed overhead is classified as sunk cost, it could be ignored at the time

of undertaking special order decisions.

Question 4:

Requirement a:

Production budget of Allison Company for the months March to May:

MANAGERIAL ACCOUNTING

Therefore, it could be said that irrelevant costs are the costs, which are not influenced by the

final decision. More precisely, these costs have to be incurred in all considered managerial

incentives (Gitman, Juchau & Flanagan, 2015). Since these costs stay same in all alternatives,

they are irrelevant and they need not be considered in computations conducted for managerial

analysis. The management only needs to consider the relevant costs of the business in decision

making process and provide all efforts in reducing the costs of the business for enhancing the

profitability of the business.

Part B:

The costs that would be incurred irrespective of accepting or rejecting a special order

decision are deemed to be irrelevant for special order decisions. On certain occasions, the

recurring fixed costs of an organisation would stay the same in total; in case of acceptance of a

special order (Horngren & Harrison, 2015). Moreover, when a special order is accepted, it might

lead to additional fixed expenses. In such cases, relevance could be found in these excess fixed

costs and therefore, consideration needs to be made in incremental analysis. However, there is no

relevance of sunk costs with any process of special order decision. Special order decisions are

considered only when an organisation is running below capacity. As a result, there would be

existence of fixed overhead cost regardless of accepting or rejecting an order (Kaplan &

Atkinson, 2015). Since fixed overhead is classified as sunk cost, it could be ignored at the time

of undertaking special order decisions.

Question 4:

Requirement a:

Production budget of Allison Company for the months March to May:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16

MANAGERIAL ACCOUNTING

Particulars March April May June

Budgeted unit sales (A) 25,000

34,00

0

50,00

0

70,00

0

Desired ending inventory (20% of next month's sales) (B) 6,800

10,00

0

14,00

0

Total needs (C) = (A) + (B) 31,800

44,00

0

64,00

0

Less: Opening inventory 3,100

6,80

0

10,00

0

Total production units (E) = (C) - (D) 28,700

37,20

0

54,00

0

Requirement b:

Budgeting plays a crucial role for any business organisation. The preparation of a master

budget needs the preparation of financial budgets and operating budgets, which include a number

of components like sales budget, production budget, cost of goods sold budget and others

(Kravet, 2014). Production budget could be defined as the element of the operating budget,

which ascertains the units of production for meeting sales and closing inventory needs. This

budget is utilised to prepare other elements of the operating budget constituting of direct material

purchases budget, direct labour budget and others. The different forms of budgets which are

utilised in a business are done for the process of decision making and also controlling the

activities of the business. The budgets which are prepared by the management of the company

MANAGERIAL ACCOUNTING

Particulars March April May June

Budgeted unit sales (A) 25,000

34,00

0

50,00

0

70,00

0

Desired ending inventory (20% of next month's sales) (B) 6,800

10,00

0

14,00

0

Total needs (C) = (A) + (B) 31,800

44,00

0

64,00

0

Less: Opening inventory 3,100

6,80

0

10,00

0

Total production units (E) = (C) - (D) 28,700

37,20

0

54,00

0

Requirement b:

Budgeting plays a crucial role for any business organisation. The preparation of a master

budget needs the preparation of financial budgets and operating budgets, which include a number

of components like sales budget, production budget, cost of goods sold budget and others

(Kravet, 2014). Production budget could be defined as the element of the operating budget,

which ascertains the units of production for meeting sales and closing inventory needs. This

budget is utilised to prepare other elements of the operating budget constituting of direct material

purchases budget, direct labour budget and others. The different forms of budgets which are

utilised in a business are done for the process of decision making and also controlling the

activities of the business. The budgets which are prepared by the management of the company

17

MANAGERIAL ACCOUNTING

are also used for communicating the objectives and goals of the business to different

departments.

Production budget is denoted in terms of physical units and not costs. The period of

production budget varies on the product cycle and the operating environment of the organisation.

Due to this, it differs in quarter, length, year, product cycle, product year and others (Krstevski &

Mancheski, 2016). For instance, during tough economic conditions, it would be feasible to

shorten the period of production budget owing to increased uncertainty about product demand or

sales. This budget takes into account both budgeted sales data as well as estimated closing levels

f inventory. At the time of ascertaining the needed levels of inventory, both benefits and costs

have to be taken into consideration.

There might be effect of product demand on estimated levels of production. The

increased product demand could lead to rise in product manufacturing, while falling demand

levels could need the organisation in cutting back production (Narayanaswamy, 2017). A

production budget assists the organisation in estimating production levels for periods at the time

of fluctuating demand. In case, an organisation knows its demand and low production levels in a

month, it could use downtime to manufacture additional product in hand for the upcoming period

with rise in demand. This assists the organisation in avoiding a situation, in which it needs to

manufacture or have on hand, more of a product; however, it lacks the manufacturing capacity in

fulfilling that demand (Otley, 2016).

A production budget projects the costs of producing a product irrespective of whether it’s

for an organisation manufacturing products in-house or an organisation outsourcing the

manufacturing a product to a third party. With the help of production budget, it becomes possible

MANAGERIAL ACCOUNTING

are also used for communicating the objectives and goals of the business to different

departments.

Production budget is denoted in terms of physical units and not costs. The period of

production budget varies on the product cycle and the operating environment of the organisation.

Due to this, it differs in quarter, length, year, product cycle, product year and others (Krstevski &

Mancheski, 2016). For instance, during tough economic conditions, it would be feasible to

shorten the period of production budget owing to increased uncertainty about product demand or

sales. This budget takes into account both budgeted sales data as well as estimated closing levels

f inventory. At the time of ascertaining the needed levels of inventory, both benefits and costs

have to be taken into consideration.

There might be effect of product demand on estimated levels of production. The

increased product demand could lead to rise in product manufacturing, while falling demand

levels could need the organisation in cutting back production (Narayanaswamy, 2017). A

production budget assists the organisation in estimating production levels for periods at the time

of fluctuating demand. In case, an organisation knows its demand and low production levels in a

month, it could use downtime to manufacture additional product in hand for the upcoming period

with rise in demand. This assists the organisation in avoiding a situation, in which it needs to

manufacture or have on hand, more of a product; however, it lacks the manufacturing capacity in

fulfilling that demand (Otley, 2016).

A production budget projects the costs of producing a product irrespective of whether it’s

for an organisation manufacturing products in-house or an organisation outsourcing the

manufacturing a product to a third party. With the help of production budget, it becomes possible

18

MANAGERIAL ACCOUNTING

to estimate the cost of having the goods produced by other (Park & Jang, 2014). This could

constitute of making the products along with the costs of the third-party producer charges for

labour and time.

A production budget provides a projection, which might change depending upon changes

outside the organisation. For instance, manufacturing needs the use of raw materials. As a result,

rise in the price of raw materials, rise in the price of raw materials could increase the costs

required for manufacturing a product (Parker & Fleischman, 2017). In addition, the

unavailability of raw material or any ingredient could need an organisation to outsource a new

material for usage in the manufacturing of the product. This might result in increased costs;

however, it could result in cost savings as well; if the organisation could obtain the new

ingredient for lower than the original cost.

It is necessary to budget production expenses for estimation of working capital

requirements and for projecting future impact on inventory levels and cash position. The

production budget is a comprehensive plan, which takes into consideration all manufacturing

jobs to be worked on during a provided financial year along with revealing timing and

expenditure amount on such projects. It is not possible to forecast the cost of goods sold in

operating budget and inventory in a pro-forma balance sheet before the completion of the

production budget.

MANAGERIAL ACCOUNTING

to estimate the cost of having the goods produced by other (Park & Jang, 2014). This could

constitute of making the products along with the costs of the third-party producer charges for

labour and time.

A production budget provides a projection, which might change depending upon changes

outside the organisation. For instance, manufacturing needs the use of raw materials. As a result,

rise in the price of raw materials, rise in the price of raw materials could increase the costs

required for manufacturing a product (Parker & Fleischman, 2017). In addition, the

unavailability of raw material or any ingredient could need an organisation to outsource a new

material for usage in the manufacturing of the product. This might result in increased costs;

however, it could result in cost savings as well; if the organisation could obtain the new

ingredient for lower than the original cost.

It is necessary to budget production expenses for estimation of working capital

requirements and for projecting future impact on inventory levels and cash position. The

production budget is a comprehensive plan, which takes into consideration all manufacturing

jobs to be worked on during a provided financial year along with revealing timing and

expenditure amount on such projects. It is not possible to forecast the cost of goods sold in

operating budget and inventory in a pro-forma balance sheet before the completion of the

production budget.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19

MANAGERIAL ACCOUNTING

Question 5:

Requirement a:

Part (i):

Material Price and Quantity Variance:-

Particulars Details Units Comment

Standard price A $ 1.20

Actual price B $ 1.23

Quantity (in yards) C 150,000

Direct material variance

D=(C x B)-(C x

A) 4,500 Unfavourable

Part (ii):

Labour Rate and Efficiency Variance:-

Particulars Details Units Comment

Standard direct labour cost per

hour A $ 9.00

Actual direct labour cost per hour B $ 9.25

Actual direct labour hours C 36,800

Direct labour variance

D=(C x B)-(C

x A) 9,200

Unfavourabl

e

MANAGERIAL ACCOUNTING

Question 5:

Requirement a:

Part (i):

Material Price and Quantity Variance:-

Particulars Details Units Comment

Standard price A $ 1.20

Actual price B $ 1.23

Quantity (in yards) C 150,000

Direct material variance

D=(C x B)-(C x

A) 4,500 Unfavourable

Part (ii):

Labour Rate and Efficiency Variance:-

Particulars Details Units Comment

Standard direct labour cost per

hour A $ 9.00

Actual direct labour cost per hour B $ 9.25

Actual direct labour hours C 36,800

Direct labour variance

D=(C x B)-(C

x A) 9,200

Unfavourabl

e

20

MANAGERIAL ACCOUNTING

Requirement b:

Any unfavourable quantity variance denotes additional use of direct materials. Such

additional usage of direct materials could be due to a number of reasons including the following:

Untrained or inexperienced staffs

Lack of adequate supervision

Lack of motivation

Usage of outdated machinery

Faulty equipment

Frequent power failures (there might be wastage owing to unscheduled stop and start of

equipment and machinery)

Purchase of substandard or unsuitable materials

Generally, the change in labour rates does not lead to labour rate variance, since they are

normally predictable. An inherent cause of an unfavourable labour rate variance is ineffective us

of labour by the production supervisors (Ponisciakova, Gogolova & Ivankova, 2015). All tasks

do not like identically skilled staffs. Some tasks are more complex and they need additional

experienced staffs than others. It needs to be borne in mind when the tasks are allocated to the

staffs. In case; the tasks that are less complex are allocated to the experienced staffs, there might

be unfavourable labour rate variance. This is because the experienced staffs receive higher

wages. On the contrary, if poorly trained workers are allocated tasks needing high expertise

level, there might be favourable labour rate variance. The reason is that these workers receive

lower wages. However, the efficiency of these workers might not be sufficient.

MANAGERIAL ACCOUNTING

Requirement b:

Any unfavourable quantity variance denotes additional use of direct materials. Such

additional usage of direct materials could be due to a number of reasons including the following:

Untrained or inexperienced staffs

Lack of adequate supervision

Lack of motivation

Usage of outdated machinery

Faulty equipment

Frequent power failures (there might be wastage owing to unscheduled stop and start of

equipment and machinery)

Purchase of substandard or unsuitable materials

Generally, the change in labour rates does not lead to labour rate variance, since they are

normally predictable. An inherent cause of an unfavourable labour rate variance is ineffective us

of labour by the production supervisors (Ponisciakova, Gogolova & Ivankova, 2015). All tasks

do not like identically skilled staffs. Some tasks are more complex and they need additional

experienced staffs than others. It needs to be borne in mind when the tasks are allocated to the

staffs. In case; the tasks that are less complex are allocated to the experienced staffs, there might

be unfavourable labour rate variance. This is because the experienced staffs receive higher

wages. On the contrary, if poorly trained workers are allocated tasks needing high expertise

level, there might be favourable labour rate variance. The reason is that these workers receive

lower wages. However, the efficiency of these workers might not be sufficient.

21

MANAGERIAL ACCOUNTING

Requirement c:

One method to set standards is the evaluation of historical data. The data associated with

historical cost provides an indication of future costs. The methods to analyse cost behaviour are

utilised for estimating future costs by using the historical cost basis. Such estimations form the

basis for setting standards.

Historical experience often acts as a poor basis in order to set standards, since historical

data might include additional inefficiencies than required. In the past, it might occur that an

organisation was not performing at complete efficiency. There might be change in managerial

positions or new standards that the management has set for optimum resource utilisation. These

all impact the guidelines for setting standards (Shields, 2015). In addition, there might be some

external factors to the organisation that might change standards. This might constitute of the

introduction of research methodology, change in government rules and policies, new market and

others. The economical and geographical changes might have impact on the standard setting of

the organisation as well.

Another method of setting standards is the engineering method. In this method, the

manufacturing process is analysed for ascertaining the costs to manufacture a particular product.

The emphasis converts from the historical cost of the product to the future estimated cost of the

product. An instance of engineering method is time and motion study carried out for ascertaining

the time taken by direct labour for performing each step. The analysis pertaining to historical

data is less costly compared to the engineering method. Therefore, historical cost method might

be preferred by many business organisations. However, when there are new processes or

products, accurate standards could not be obtained with the assistance of historical data. Under

such situations, it is possible to utilise the engineering methods.

MANAGERIAL ACCOUNTING

Requirement c:

One method to set standards is the evaluation of historical data. The data associated with

historical cost provides an indication of future costs. The methods to analyse cost behaviour are

utilised for estimating future costs by using the historical cost basis. Such estimations form the

basis for setting standards.

Historical experience often acts as a poor basis in order to set standards, since historical

data might include additional inefficiencies than required. In the past, it might occur that an

organisation was not performing at complete efficiency. There might be change in managerial

positions or new standards that the management has set for optimum resource utilisation. These

all impact the guidelines for setting standards (Shields, 2015). In addition, there might be some

external factors to the organisation that might change standards. This might constitute of the

introduction of research methodology, change in government rules and policies, new market and

others. The economical and geographical changes might have impact on the standard setting of

the organisation as well.

Another method of setting standards is the engineering method. In this method, the

manufacturing process is analysed for ascertaining the costs to manufacture a particular product.

The emphasis converts from the historical cost of the product to the future estimated cost of the

product. An instance of engineering method is time and motion study carried out for ascertaining

the time taken by direct labour for performing each step. The analysis pertaining to historical

data is less costly compared to the engineering method. Therefore, historical cost method might

be preferred by many business organisations. However, when there are new processes or

products, accurate standards could not be obtained with the assistance of historical data. Under

such situations, it is possible to utilise the engineering methods.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

22

MANAGERIAL ACCOUNTING

The standards to be regarded include ideal standards demanding a maximum efficiency

and this could be accomplished only; in case, there have been perfect operations of all aspects.

There is no room for machine breakdown and momentary slack of skills. In addition, the other

standard includes the currently attainable standards that could be accomplished under effective

working conditions. However, there is allowance for normal interruptions, breakdowns and

lower than perfect skills.

For responding to these factors, it is necessary to consider all the aspects along with

preparing budget and estimating yearly depending on the existing market scenario, aligning with

the mission of the organisation and existing performance of the competitors. There needs to be

projections based on financial parameters, economic and political scenario. Moreover, there

needs to be revision of operational allowance and setting up standards in accordance with the

available efficiency and technology (Weygandt, Kimmel & Kieso, 2015). Therefore, the new

standard developed by considering the above aspects are deemed to be more useful than those

based on historical data. In other words, historical cost method contains certain loopholes that

might hamper the process of setting standards for any business organisation in formulation of

standards for undertaking final decisions and thus, it needs to be exercised with utmost caution.

MANAGERIAL ACCOUNTING

The standards to be regarded include ideal standards demanding a maximum efficiency

and this could be accomplished only; in case, there have been perfect operations of all aspects.

There is no room for machine breakdown and momentary slack of skills. In addition, the other

standard includes the currently attainable standards that could be accomplished under effective

working conditions. However, there is allowance for normal interruptions, breakdowns and

lower than perfect skills.

For responding to these factors, it is necessary to consider all the aspects along with

preparing budget and estimating yearly depending on the existing market scenario, aligning with

the mission of the organisation and existing performance of the competitors. There needs to be

projections based on financial parameters, economic and political scenario. Moreover, there

needs to be revision of operational allowance and setting up standards in accordance with the

available efficiency and technology (Weygandt, Kimmel & Kieso, 2015). Therefore, the new

standard developed by considering the above aspects are deemed to be more useful than those

based on historical data. In other words, historical cost method contains certain loopholes that

might hamper the process of setting standards for any business organisation in formulation of

standards for undertaking final decisions and thus, it needs to be exercised with utmost caution.

23

MANAGERIAL ACCOUNTING

References:

Benson, K., Clarkson, P. M., Smith, T., & Tutticci, I. (2015). A review of accounting research in

the Asia Pacific region. Australian Journal of Management, 40(1), 36-88.

Braun, K. W., Tietz, W. M., Harrison, W. T., Bamber, L. S., & Horngren, C. T.

(2014). Managerial accounting. Boston: Pearson.

Butler, S. A., & Ghosh, D. (2015). Individual differences in managerial accounting judgments

and decision making. The British Accounting Review, 47(1), 33-45.

Dopson, L. R., & Hayes, D. K. (2016). Managerial accounting for the hospitality industry.

Wiley Global Education.

Gitman, L. J., Juchau, R., & Flanagan, J. (2015). Principles of managerial finance. Pearson

Higher Education AU.

Horngren, C., & Harrison, W. (2015). ACCOUNTING: BSB110. Pearson Higher Education AU.

Kaplan, R. S., & Atkinson, A. A. (2015). Advanced management accounting. PHI Learning.

Kravet, T. D. (2014). Accounting conservatism and managerial risk-taking: Corporate

acquisitions. Journal of Accounting and Economics, 57(2-3), 218-240.

Krstevski, D., & Mancheski, G. (2016). Managerial accounting: Modeling customer lifetime

value-An application in the telecommunication industry. European journal of business

and social sciences, 5(01), 64-77.

MANAGERIAL ACCOUNTING

References:

Benson, K., Clarkson, P. M., Smith, T., & Tutticci, I. (2015). A review of accounting research in

the Asia Pacific region. Australian Journal of Management, 40(1), 36-88.

Braun, K. W., Tietz, W. M., Harrison, W. T., Bamber, L. S., & Horngren, C. T.

(2014). Managerial accounting. Boston: Pearson.

Butler, S. A., & Ghosh, D. (2015). Individual differences in managerial accounting judgments

and decision making. The British Accounting Review, 47(1), 33-45.

Dopson, L. R., & Hayes, D. K. (2016). Managerial accounting for the hospitality industry.

Wiley Global Education.

Gitman, L. J., Juchau, R., & Flanagan, J. (2015). Principles of managerial finance. Pearson

Higher Education AU.

Horngren, C., & Harrison, W. (2015). ACCOUNTING: BSB110. Pearson Higher Education AU.

Kaplan, R. S., & Atkinson, A. A. (2015). Advanced management accounting. PHI Learning.

Kravet, T. D. (2014). Accounting conservatism and managerial risk-taking: Corporate

acquisitions. Journal of Accounting and Economics, 57(2-3), 218-240.

Krstevski, D., & Mancheski, G. (2016). Managerial accounting: Modeling customer lifetime

value-An application in the telecommunication industry. European journal of business

and social sciences, 5(01), 64-77.

24

MANAGERIAL ACCOUNTING

Narayanaswamy, R. (2017). Financial accounting: a managerial perspective. PHI Learning Pvt.

Ltd.

Otley, D. (2016). The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, 45-62.

Park, K., & Jang, S. (2014). Hospitality finance and managerial accounting research: Suggesting

an interdisciplinary research agenda. International Journal of Contemporary Hospitality

Management, 26(5), 751-777.

Parker, L. D., & Fleischman, R. K. (2017). What is Past is Prologue: Cost Accounting in the

British Industrial Revolution, 1760-1850. Routledge.

Ponisciakova, O., Gogolova, M., & Ivankova, K. (2015). Calculations in managerial

accounting. Procedia Economics and Finance, 26, 431-437.

Shields, M. D. (2015). Established management accounting knowledge. Journal of Management

Accounting Research, 27(1), 123-132.

Weygandt, J. J., Kimmel, P. D., & Kieso, D. E. (2015). Financial & managerial accounting.

John Wiley & Sons.

MANAGERIAL ACCOUNTING

Narayanaswamy, R. (2017). Financial accounting: a managerial perspective. PHI Learning Pvt.

Ltd.

Otley, D. (2016). The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, 45-62.

Park, K., & Jang, S. (2014). Hospitality finance and managerial accounting research: Suggesting

an interdisciplinary research agenda. International Journal of Contemporary Hospitality

Management, 26(5), 751-777.

Parker, L. D., & Fleischman, R. K. (2017). What is Past is Prologue: Cost Accounting in the

British Industrial Revolution, 1760-1850. Routledge.

Ponisciakova, O., Gogolova, M., & Ivankova, K. (2015). Calculations in managerial

accounting. Procedia Economics and Finance, 26, 431-437.

Shields, M. D. (2015). Established management accounting knowledge. Journal of Management

Accounting Research, 27(1), 123-132.

Weygandt, J. J., Kimmel, P. D., & Kieso, D. E. (2015). Financial & managerial accounting.

John Wiley & Sons.

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.