Managerial Accounting Assignment Solution: ABC Costing Analysis

VerifiedAdded on 2023/06/07

|10

|1890

|287

Homework Assignment

AI Summary

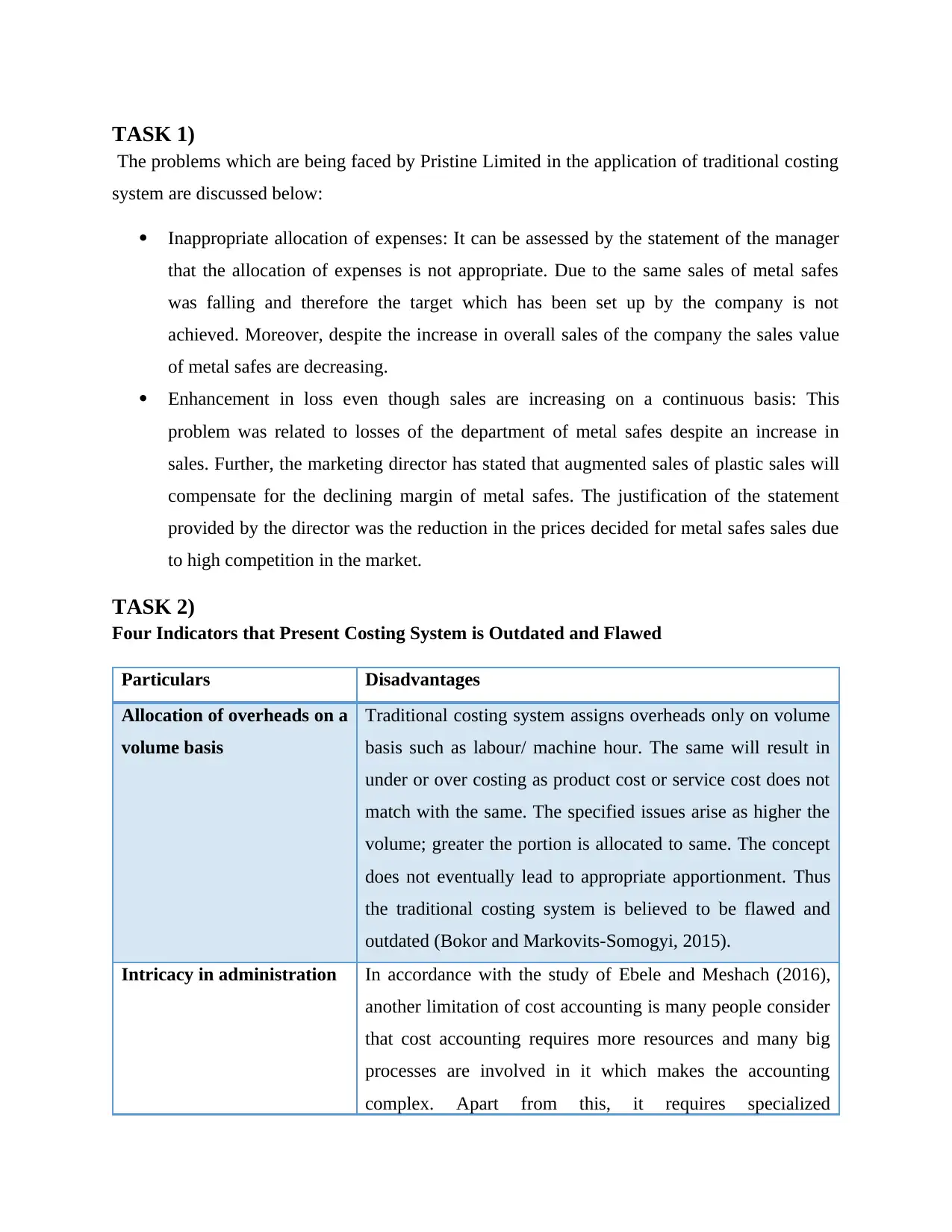

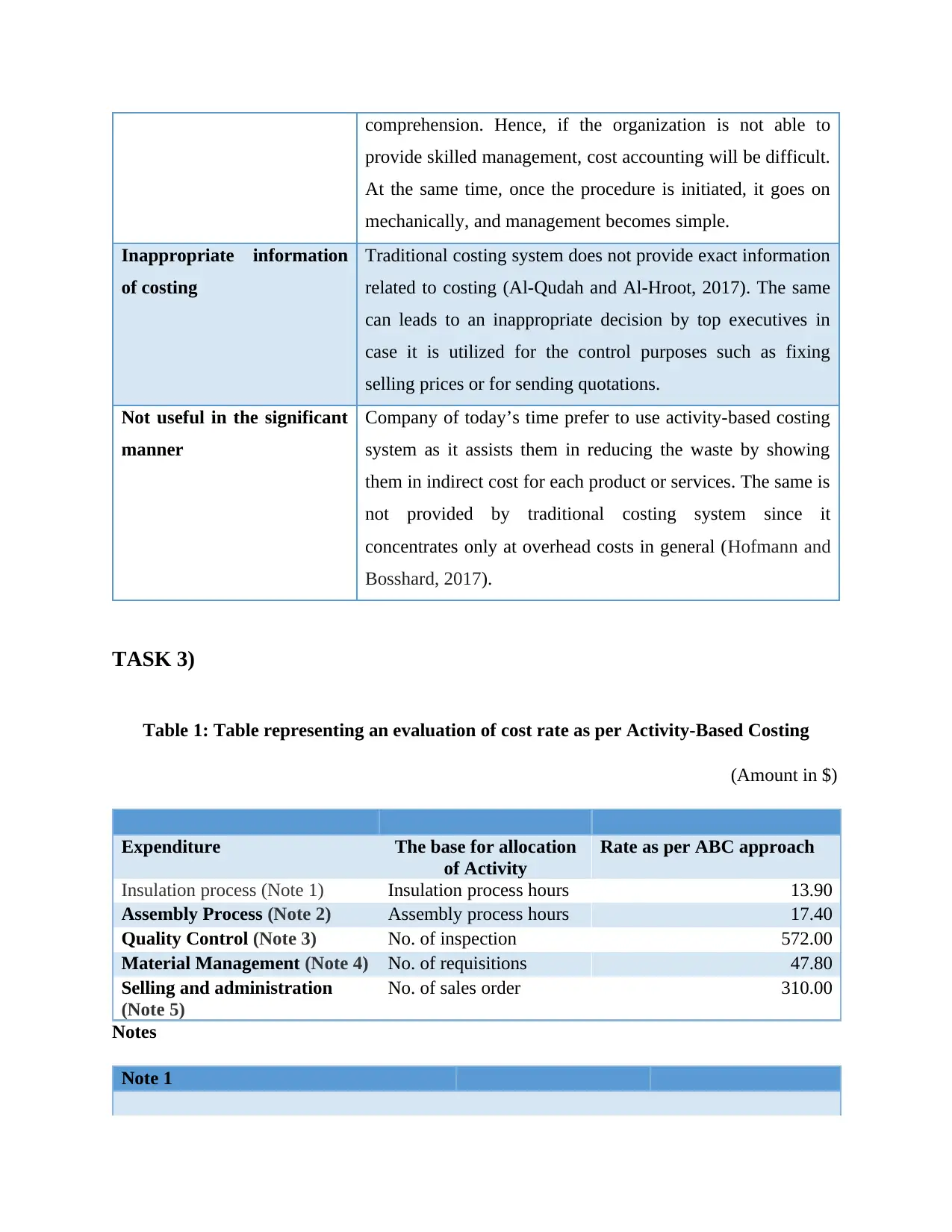

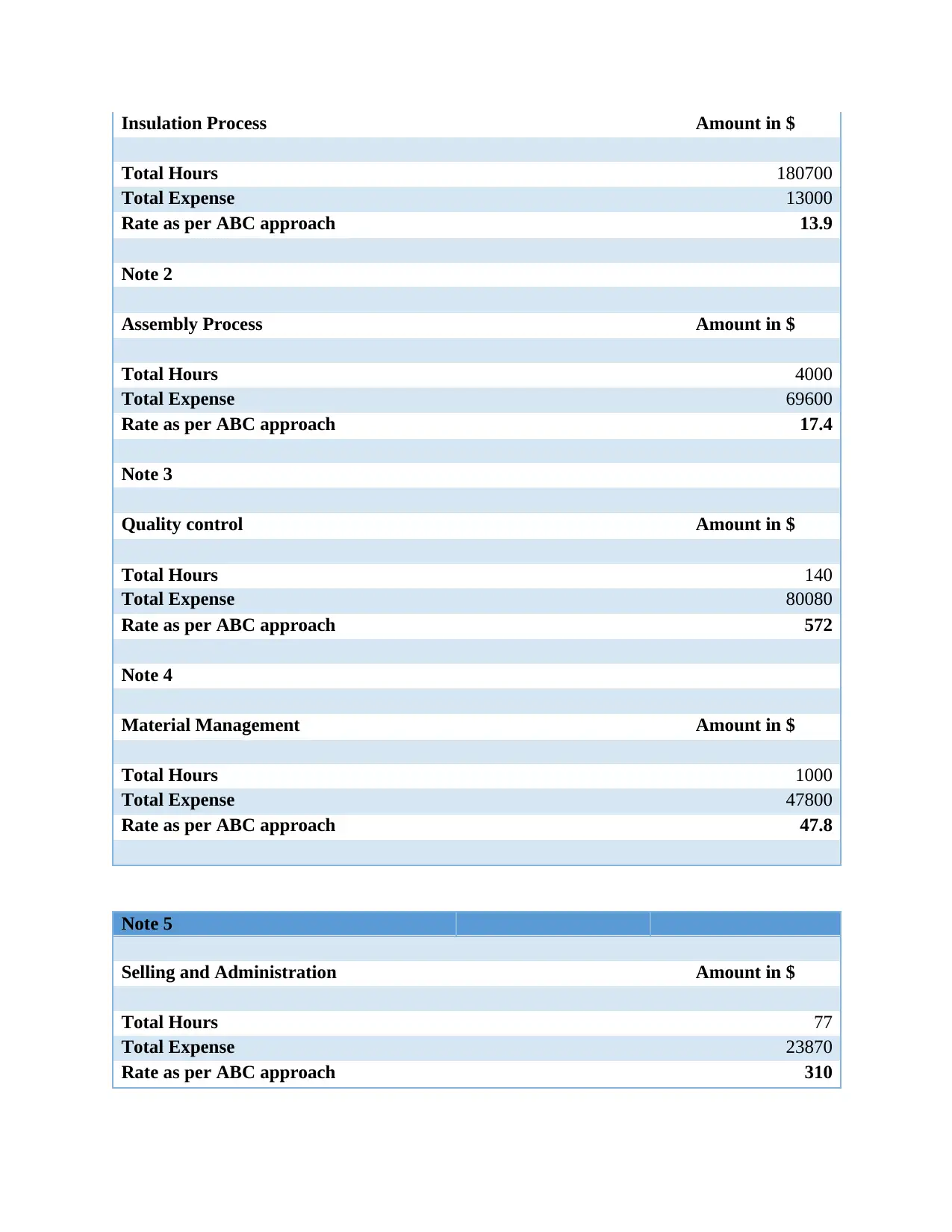

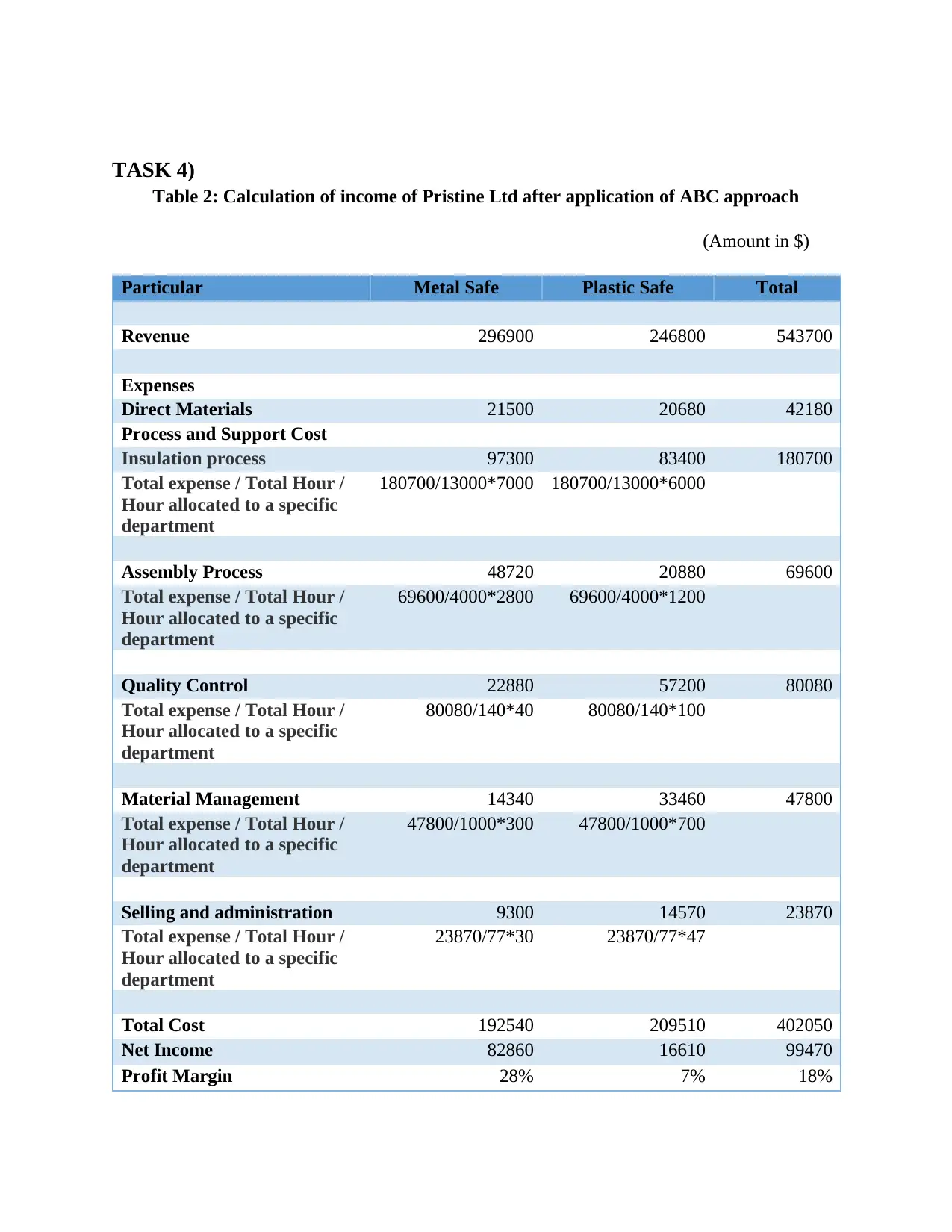

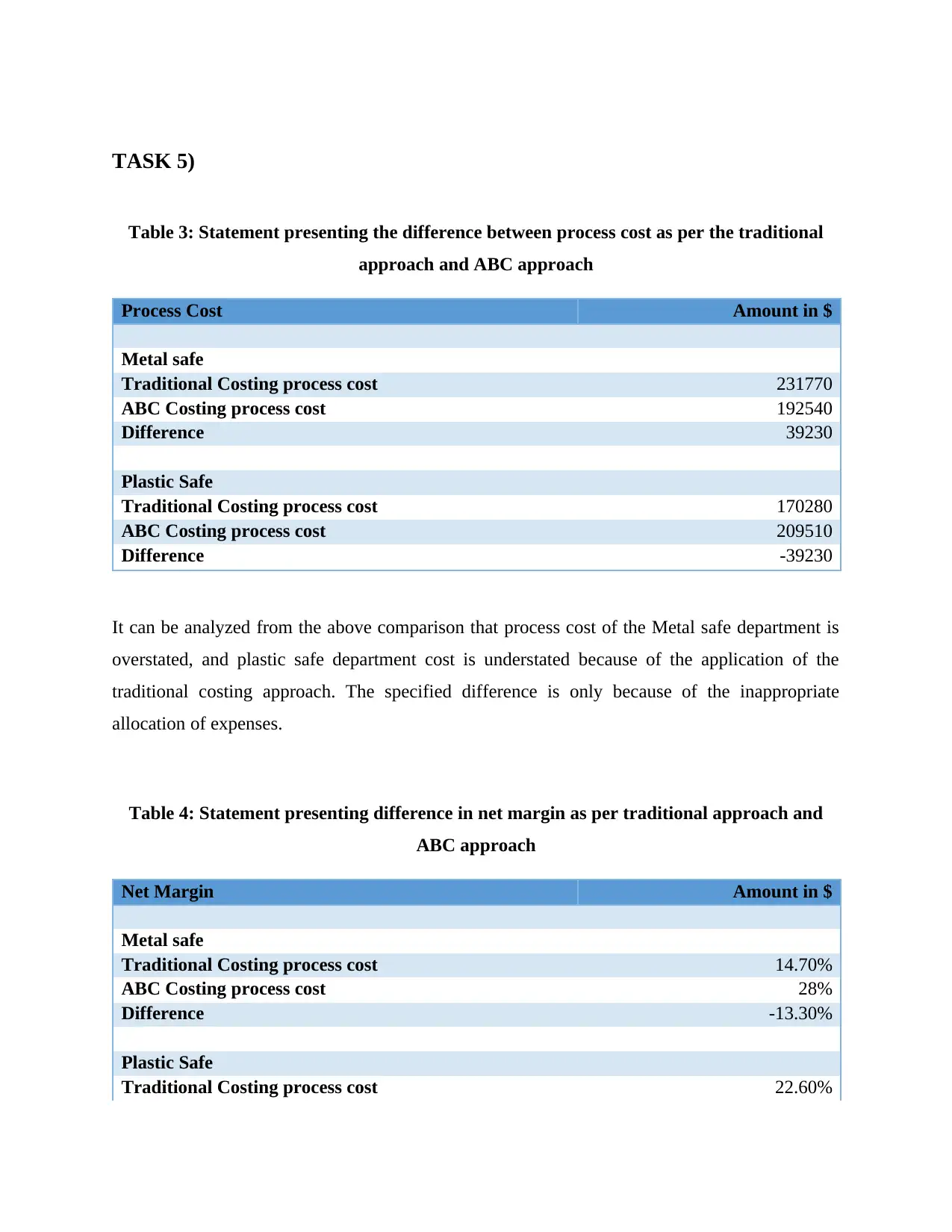

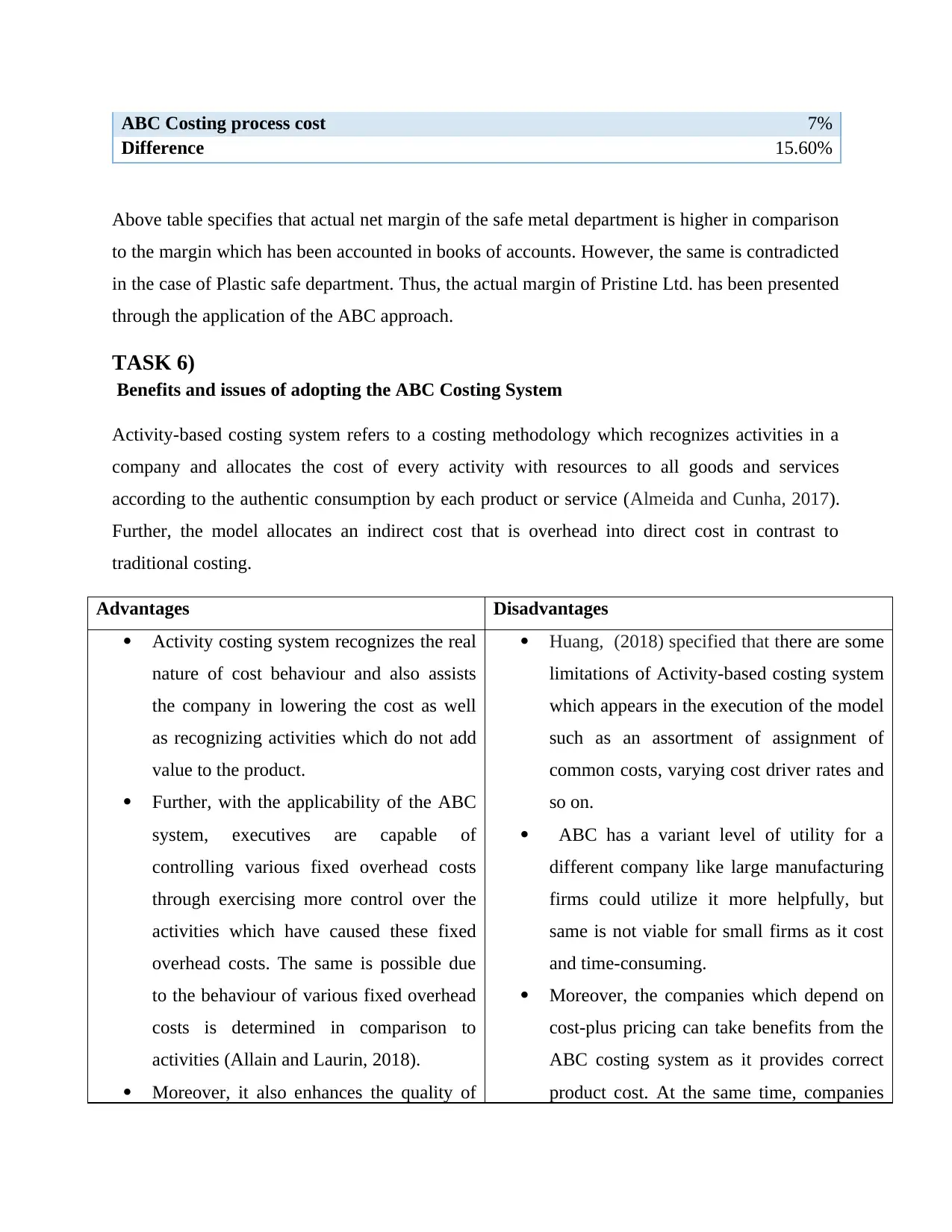

This assignment solution addresses a managerial accounting case study for Pristine Limited, focusing on the implementation and benefits of Activity-Based Costing (ABC) compared to traditional costing methods. The solution begins by identifying the problems Pristine Limited faces with its traditional costing system, such as inappropriate expense allocation, leading to distorted product costs and ultimately affecting profitability. The document then outlines four indicators highlighting the flaws of the traditional costing system, including inappropriate overhead allocation, administrative complexity, inaccurate costing information, and its limited usefulness in today's business environment. A detailed ABC costing approach is then presented, including the calculation of cost rates for various activities like insulation, assembly, quality control, and material management. The solution further calculates the income of Pristine Ltd after applying the ABC approach, comparing the process costs and net margins of metal and plastic safes under both traditional and ABC costing. The analysis reveals significant differences in profitability, underscoring the impact of accurate cost allocation. Finally, the assignment discusses the advantages and disadvantages of adopting the ABC costing system, emphasizing the importance of ABC in enhancing decision-making, cost reduction, and achieving a more accurate product cost. The conclusion recommends transitioning from traditional costing to ABC to accurately reflect the financial position of the company and make informed business decisions.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.