Managerial Accounting And Business Performance

VerifiedAdded on 2022/08/25

|17

|4004

|22

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: MANAGERIAL ACCOUNTING

MANAGERIAL ACCOUNTING

Name of the Student

Name of the University

Author Note

MANAGERIAL ACCOUNTING

Name of the Student

Name of the University

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1MANAGERIAL ACCOUNTING

Abstract

The main purpose of this report is to identify the different method of costing, which

can help a manager in efficient decision-making. The study is supported by analyzing the

journal article of both the costing techniques. It is found that, both the costing methods is

helpful in increasing the business performance. Target costing technique is best for planning

purpose and standard costing technique is best system for controlling the cost of the business

operations.

Abstract

The main purpose of this report is to identify the different method of costing, which

can help a manager in efficient decision-making. The study is supported by analyzing the

journal article of both the costing techniques. It is found that, both the costing methods is

helpful in increasing the business performance. Target costing technique is best for planning

purpose and standard costing technique is best system for controlling the cost of the business

operations.

2MANAGERIAL ACCOUNTING

Table of Contents

Introduction................................................................................................................................3

Discussions.................................................................................................................................3

Features of Standard Costing.................................................................................................3

Relevance of Standard Costing..............................................................................................5

Comparison of target costing with Standard Costing............................................................7

Relevance of Target Costing..................................................................................................8

Recommendations................................................................................................................11

Conclusion................................................................................................................................11

References................................................................................................................................13

Table of Contents

Introduction................................................................................................................................3

Discussions.................................................................................................................................3

Features of Standard Costing.................................................................................................3

Relevance of Standard Costing..............................................................................................5

Comparison of target costing with Standard Costing............................................................7

Relevance of Target Costing..................................................................................................8

Recommendations................................................................................................................11

Conclusion................................................................................................................................11

References................................................................................................................................13

3MANAGERIAL ACCOUNTING

Introduction

Costing system is very important framework in an accounting system and is used to

estimate the costs of a product. This system is used for analyzing the profitability of the

business. The paper has discussed on the concept of costing techniques that are used by

organizations. It will highlight the importance of standard costing and target costing in the

business environment. The paper is related to journal article of standard costing and target

costing. The positive aspects of standard costing and target costing are discussed in this

paper. The main objective is this report is to identify the best method of costing techniques

that can help the manager in efficient decision-making.

Discussions

Features of Standard Costing

Standard costing is a practice of accounting that is used to substitute the expected cost

from the actual cost of the goods. This is a traditional system of accounting. This system will

identify the variance differences between the actual costs of the goods and the expected costs

of the goods. This is a simplified approach relative to other costing system like LIFO and

FIFO methods (Tsai, Lan and Huang 2019). This is because, in LIFO and FIFO methods,

historical information related to the goods are noted for calculating the cost of the inventories

or stock. Standard costing system is used to calculate the estimation cost for all the activities

of a business. This system of costing uses several of applications to find the cost of the goods.

The application of standard costing helps in budgeting the expected cost with its

expected costs. This predetermines the cost of manufacturing of the specific products in that

Introduction

Costing system is very important framework in an accounting system and is used to

estimate the costs of a product. This system is used for analyzing the profitability of the

business. The paper has discussed on the concept of costing techniques that are used by

organizations. It will highlight the importance of standard costing and target costing in the

business environment. The paper is related to journal article of standard costing and target

costing. The positive aspects of standard costing and target costing are discussed in this

paper. The main objective is this report is to identify the best method of costing techniques

that can help the manager in efficient decision-making.

Discussions

Features of Standard Costing

Standard costing is a practice of accounting that is used to substitute the expected cost

from the actual cost of the goods. This is a traditional system of accounting. This system will

identify the variance differences between the actual costs of the goods and the expected costs

of the goods. This is a simplified approach relative to other costing system like LIFO and

FIFO methods (Tsai, Lan and Huang 2019). This is because, in LIFO and FIFO methods,

historical information related to the goods are noted for calculating the cost of the inventories

or stock. Standard costing system is used to calculate the estimation cost for all the activities

of a business. This system of costing uses several of applications to find the cost of the goods.

The application of standard costing helps in budgeting the expected cost with its

expected costs. This predetermines the cost of manufacturing of the specific products in that

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4MANAGERIAL ACCOUNTING

specific time (Bargerstock and Shi 2016). This is also known as planned costs of a goods or

product. The basic features of standard cost are:

It helps in comparing the expected cost with the actual cost of the good or product.

It helps in determine the actual cost of the product by examining the past and future

price trend of the product (Maskell, Baggaley and Grasso 2017).

It controls the variances of the cost of goods. The management of the company

checks the variance and accordingly controls the business operations.

It helps in providing proper suggestions to management for efficient decision-

making.

Standard cost helps the management in making efficient decision. This is done by

estimating the cost of goods; and if the actual cost is found to be more than the standard cost,

then the variances of the goods is not in good condition (Cengiz and Ersoy 2017). This

indicates that, the cost associated with the product has a negative impact on the business

profitability. In this case, the management will make decisions to balance the variance

observed. They analyse the causes of variations in the costing system of manufacturing

activities. This includes all the errors and mistakes that have been achieved during the costing

process (Tsifora and Chatzoglou 2016). The management of a company finds the best

solutions to their business strategy for minimizing the cost. Therefore, standard costing helps

to evaluate the operating performance of a business. In this way, the business can control

their costs and earn more profit from their business operations. Standard costing also helps to

reduce any unwanted costs associated with the business operations (Manyaeva, Piskunov and

Fomin 2016). It allows the workforce and management to be more responsible towards their

work. This technical process helps the employees to coordinately do their job. This system of

costing must be designed to identify the cost of production. When higher authorities set the

specific time (Bargerstock and Shi 2016). This is also known as planned costs of a goods or

product. The basic features of standard cost are:

It helps in comparing the expected cost with the actual cost of the good or product.

It helps in determine the actual cost of the product by examining the past and future

price trend of the product (Maskell, Baggaley and Grasso 2017).

It controls the variances of the cost of goods. The management of the company

checks the variance and accordingly controls the business operations.

It helps in providing proper suggestions to management for efficient decision-

making.

Standard cost helps the management in making efficient decision. This is done by

estimating the cost of goods; and if the actual cost is found to be more than the standard cost,

then the variances of the goods is not in good condition (Cengiz and Ersoy 2017). This

indicates that, the cost associated with the product has a negative impact on the business

profitability. In this case, the management will make decisions to balance the variance

observed. They analyse the causes of variations in the costing system of manufacturing

activities. This includes all the errors and mistakes that have been achieved during the costing

process (Tsifora and Chatzoglou 2016). The management of a company finds the best

solutions to their business strategy for minimizing the cost. Therefore, standard costing helps

to evaluate the operating performance of a business. In this way, the business can control

their costs and earn more profit from their business operations. Standard costing also helps to

reduce any unwanted costs associated with the business operations (Manyaeva, Piskunov and

Fomin 2016). It allows the workforce and management to be more responsible towards their

work. This technical process helps the employees to coordinately do their job. This system of

costing must be designed to identify the cost of production. When higher authorities set the

5MANAGERIAL ACCOUNTING

standards of each of operations, then the supervisors and the employees will be more focus

towards the management and development of standards of the business.

There are certain disadvantages of standard costing: This system reports the variances of

actual cost and the expected cost. This may drive the management to take wrong decisions

(Cuzdriorean 2017). For example. In order to improve the variance of purchase of raw

materials, they may purchase a larger quantity of raw material.

This costing system assumes that cost does not change. However, with the continuous

development & improvement of the product, the cost of the product changes

continuously (Potkany et al. 2017).

This system gives a very slow feedback after reporting the accounting process.

Relevance of Standard Costing

This case study is based on the practice of the accounting method of standard costing

in the manufacturing industries. It is relevant to the managerial accounting system. The

author has clearly described this process. According to the author, standard costing system is

not sufficient to meet the business requirements of manufacturing industries (Anon, 2020).

The operational manager of ASL States acknowledged that the production process of ASL

states has reduced the costs. However, there could be an improvement in meeting the

demands of the customer. Hence, from the evaluation various limitations and benefits of

standard costing were evaluated. The case study has discussed on the characteristics of

standard accounting. This accounting system includes the costs related to raw material,

business expenses and other employee related expenses. The standard cost are estimated in

terms of prices. The cost for material and labour are budgeted as overhead costs. The

standard costs are used for comparing with the actual cost and valuation of the inventories.

The difference between estimated costs and actual cost will give the variance of the cost.

standards of each of operations, then the supervisors and the employees will be more focus

towards the management and development of standards of the business.

There are certain disadvantages of standard costing: This system reports the variances of

actual cost and the expected cost. This may drive the management to take wrong decisions

(Cuzdriorean 2017). For example. In order to improve the variance of purchase of raw

materials, they may purchase a larger quantity of raw material.

This costing system assumes that cost does not change. However, with the continuous

development & improvement of the product, the cost of the product changes

continuously (Potkany et al. 2017).

This system gives a very slow feedback after reporting the accounting process.

Relevance of Standard Costing

This case study is based on the practice of the accounting method of standard costing

in the manufacturing industries. It is relevant to the managerial accounting system. The

author has clearly described this process. According to the author, standard costing system is

not sufficient to meet the business requirements of manufacturing industries (Anon, 2020).

The operational manager of ASL States acknowledged that the production process of ASL

states has reduced the costs. However, there could be an improvement in meeting the

demands of the customer. Hence, from the evaluation various limitations and benefits of

standard costing were evaluated. The case study has discussed on the characteristics of

standard accounting. This accounting system includes the costs related to raw material,

business expenses and other employee related expenses. The standard cost are estimated in

terms of prices. The cost for material and labour are budgeted as overhead costs. The

standard costs are used for comparing with the actual cost and valuation of the inventories.

The difference between estimated costs and actual cost will give the variance of the cost.

6MANAGERIAL ACCOUNTING

Variance can be used to take control measures on costs. Standard costing system has various

benefits in the production process. It helps in enhancing the budgeting process. The suppliers

can easily be changed & better raw materials can be generated for enhancing the production

process. Standard costing system helps the management to control their operations cost and

get involve towards their job. The staffs and the management to get a positive result on the

variance can manipulate standard costing system. They can estimate a higher cost for their

own benefit. ASL States should focus on improving the financial and operational

performance of the business. This can be done by adopting a better cost control system in the

business. Modern accounting system of Total Quality Management will focus on the financial

improvement of the business. This system measures the efficiency by analyzing the

complaints of the customers and returns on the business. But, ASL depends on standard

costing system because, the modern system cannot cut the costs related to the business

operations. The company is focusing on the cost leadership strategy to meet the customers

needs. This helps the company to charge a premium on the price. Therefore, the cost

leadership strategy will help the company to control their cost of business operation. In

differentiation strategy, the cost leadership cannot be executed. The operational manager of

ASL States that, standard costing system will help in controlling the costs of the production

process and increase the efficiency of manufacturing activities. But, the standard costing

system should be advanced and retained to increase the efficiency of cost control in the

business. Then , the modern costing system of activity based costing can be used to create

value for the customers.

The above features of standard costing doesnot satisfies to the real standard costing

system of accounting system. This is because the main purpose of standard costing system is

to determine the expected cost with the actual cost of the goods and services. In the today’s

Variance can be used to take control measures on costs. Standard costing system has various

benefits in the production process. It helps in enhancing the budgeting process. The suppliers

can easily be changed & better raw materials can be generated for enhancing the production

process. Standard costing system helps the management to control their operations cost and

get involve towards their job. The staffs and the management to get a positive result on the

variance can manipulate standard costing system. They can estimate a higher cost for their

own benefit. ASL States should focus on improving the financial and operational

performance of the business. This can be done by adopting a better cost control system in the

business. Modern accounting system of Total Quality Management will focus on the financial

improvement of the business. This system measures the efficiency by analyzing the

complaints of the customers and returns on the business. But, ASL depends on standard

costing system because, the modern system cannot cut the costs related to the business

operations. The company is focusing on the cost leadership strategy to meet the customers

needs. This helps the company to charge a premium on the price. Therefore, the cost

leadership strategy will help the company to control their cost of business operation. In

differentiation strategy, the cost leadership cannot be executed. The operational manager of

ASL States that, standard costing system will help in controlling the costs of the production

process and increase the efficiency of manufacturing activities. But, the standard costing

system should be advanced and retained to increase the efficiency of cost control in the

business. Then , the modern costing system of activity based costing can be used to create

value for the customers.

The above features of standard costing doesnot satisfies to the real standard costing

system of accounting system. This is because the main purpose of standard costing system is

to determine the expected cost with the actual cost of the goods and services. In the today’s

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL ACCOUNTING

business state, this system cannot be accurate to determine the expected cost, because the

expected cost may vary as we compare it to the real cost associated with the goods.

Moreover, costing system is used to maintain the cost and enhance the business outcome.

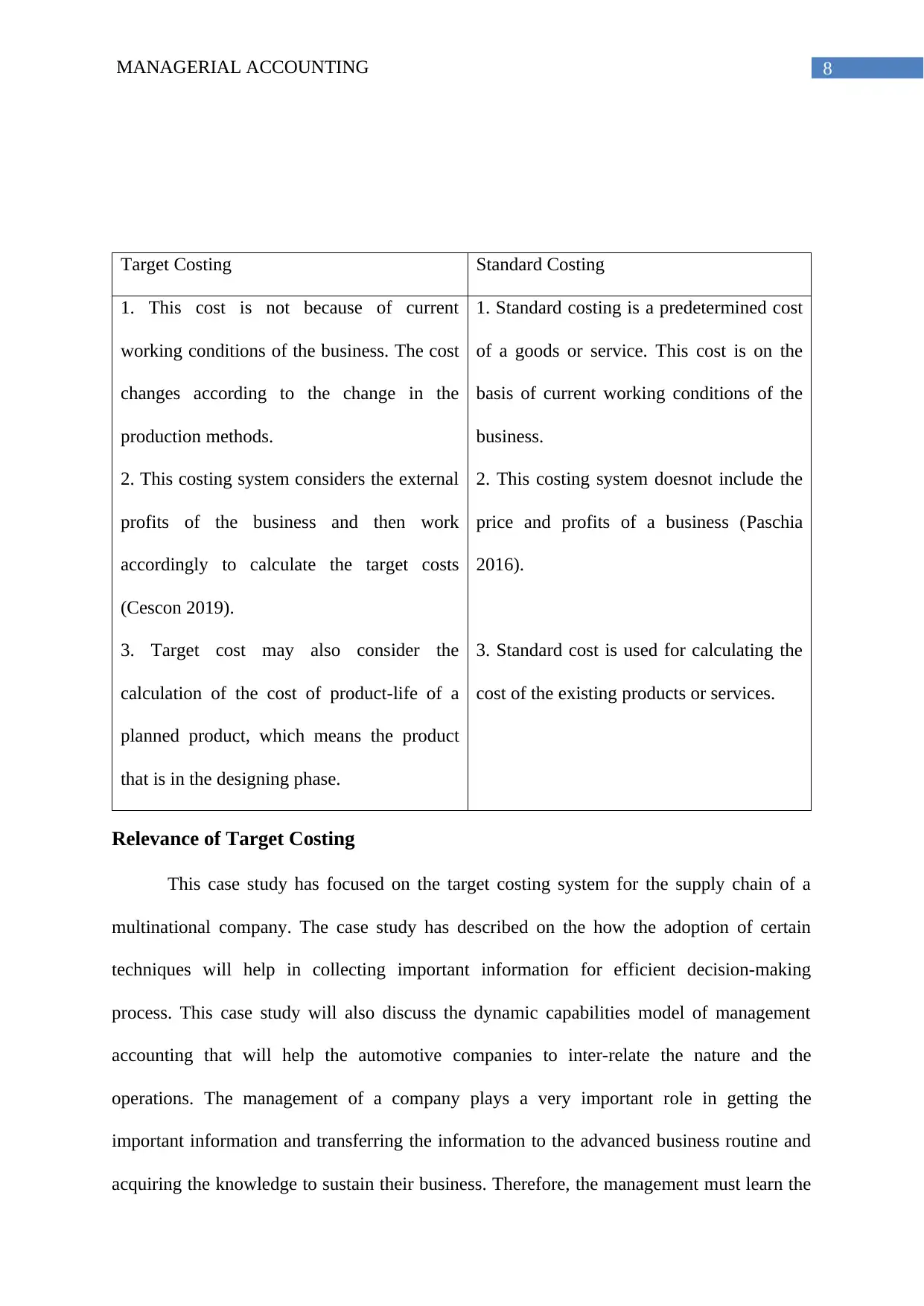

Comparison of target costing with Standard Costing

Target costing is used to determine the cost of product life cycle. This is used to set a

target cost of a product that a firm can use. It is the maximum amount of cost that is

associated with the product. This cost maintains the quality and functionality of the product

(Helms et al. 2005). This cost is used during the product-designing phase of the product life

cycle. This is a type of cost planning process, which focuses on reducing the cost associated

during the product-designing phase. Target costing includes three faces; the first phase

focuses mainly on the long-term profit that can be generated from the product. This phase

identifies market conditions of the product (Hassan and Mohamed 2018). The second phase

involves utilization of various strategies for cost reduction in the product designing process.

The third phase includes a component-level cost. This tool is also a managerial tool in

estimating the price associated with project designing process (Steyn 2017). The management

can plan its project using this costing tool. This tool also helps to make a consistent profit

especially in the health care and construction sectors (Rasit and Ismail 2017). The

management can evaluate the target cost of the product by analyzing the demand and supply

of that product in the market place. There are certain factors that affects the target cost of a

product. These factors includes; the intensity of competition in the market place, the product

level strategy in the business and the supplier’s strategy related to the product (Clermont,

Ahn and Schwetschke 2018). These factors change over time in a marketplace and can

change the company strategy of doing product operations.

Comparison:

business state, this system cannot be accurate to determine the expected cost, because the

expected cost may vary as we compare it to the real cost associated with the goods.

Moreover, costing system is used to maintain the cost and enhance the business outcome.

Comparison of target costing with Standard Costing

Target costing is used to determine the cost of product life cycle. This is used to set a

target cost of a product that a firm can use. It is the maximum amount of cost that is

associated with the product. This cost maintains the quality and functionality of the product

(Helms et al. 2005). This cost is used during the product-designing phase of the product life

cycle. This is a type of cost planning process, which focuses on reducing the cost associated

during the product-designing phase. Target costing includes three faces; the first phase

focuses mainly on the long-term profit that can be generated from the product. This phase

identifies market conditions of the product (Hassan and Mohamed 2018). The second phase

involves utilization of various strategies for cost reduction in the product designing process.

The third phase includes a component-level cost. This tool is also a managerial tool in

estimating the price associated with project designing process (Steyn 2017). The management

can plan its project using this costing tool. This tool also helps to make a consistent profit

especially in the health care and construction sectors (Rasit and Ismail 2017). The

management can evaluate the target cost of the product by analyzing the demand and supply

of that product in the market place. There are certain factors that affects the target cost of a

product. These factors includes; the intensity of competition in the market place, the product

level strategy in the business and the supplier’s strategy related to the product (Clermont,

Ahn and Schwetschke 2018). These factors change over time in a marketplace and can

change the company strategy of doing product operations.

Comparison:

8MANAGERIAL ACCOUNTING

Target Costing Standard Costing

1. This cost is not because of current

working conditions of the business. The cost

changes according to the change in the

production methods.

2. This costing system considers the external

profits of the business and then work

accordingly to calculate the target costs

(Cescon 2019).

3. Target cost may also consider the

calculation of the cost of product-life of a

planned product, which means the product

that is in the designing phase.

1. Standard costing is a predetermined cost

of a goods or service. This cost is on the

basis of current working conditions of the

business.

2. This costing system doesnot include the

price and profits of a business (Paschia

2016).

3. Standard cost is used for calculating the

cost of the existing products or services.

Relevance of Target Costing

This case study has focused on the target costing system for the supply chain of a

multinational company. The case study has described on the how the adoption of certain

techniques will help in collecting important information for efficient decision-making

process. This case study will also discuss the dynamic capabilities model of management

accounting that will help the automotive companies to inter-relate the nature and the

operations. The management of a company plays a very important role in getting the

important information and transferring the information to the advanced business routine and

acquiring the knowledge to sustain their business. Therefore, the management must learn the

Target Costing Standard Costing

1. This cost is not because of current

working conditions of the business. The cost

changes according to the change in the

production methods.

2. This costing system considers the external

profits of the business and then work

accordingly to calculate the target costs

(Cescon 2019).

3. Target cost may also consider the

calculation of the cost of product-life of a

planned product, which means the product

that is in the designing phase.

1. Standard costing is a predetermined cost

of a goods or service. This cost is on the

basis of current working conditions of the

business.

2. This costing system doesnot include the

price and profits of a business (Paschia

2016).

3. Standard cost is used for calculating the

cost of the existing products or services.

Relevance of Target Costing

This case study has focused on the target costing system for the supply chain of a

multinational company. The case study has described on the how the adoption of certain

techniques will help in collecting important information for efficient decision-making

process. This case study will also discuss the dynamic capabilities model of management

accounting that will help the automotive companies to inter-relate the nature and the

operations. The management of a company plays a very important role in getting the

important information and transferring the information to the advanced business routine and

acquiring the knowledge to sustain their business. Therefore, the management must learn the

9MANAGERIAL ACCOUNTING

dynamic capabilities to integrate with the business strategy. The managers can include the

dynamic capabilities by adopting a proper managerial accounting system. Dynamic

capabilities is applied with the target costing techniques in the organisation process for

efficient decision-making process. The case study adds an external pressure to the

management on proper implementation of target costing in today’s automotive world. Failing

in proper understand of the various issues in the company. The resource and dynamic

capabilities is the most competitive advantages of this firm. An organisational can be tangible

and intangible asset that can control the business operations (Knight and Collier, 2009). The

administrative department make this decisions on providing wider opportunities to the

management for successful decision making process. It support the management in providing

the resources. An organisation have the capabilities to properly perform their task in order to

get their desired result. But, the dynamic capabilities change. This includes change in

operational and language capabilities in the manufacturing activities. But, these dynamic

capabilities are embedded in the organisational culture and structure for making strategic

planning and processing. Dynamic capabilities create a value in providing the competitive

advantages. Hence, the value lies in resources and integrating the business process in the

operations. Dynamic capabilities have different product life cycles that help the firm to

emerge in the developing environment. Hence, it provides opportunities and threats to create

a competitive advantage. Organistaions should be capable of changing the dynamic

capabilities. In this, dynamic managerial capabilities is also equally important. Target costing

was developed in Toyota Motor Corporation. They created a target price for the vehicle and

analysed the targeted profit for the suppliers and assemblers. It includes each stage of

production process. It includes product-costing, requirements for the customers and

customer’s willingness to pay. This costing system was regarded as the most efficient

planning technique for the accountants.

dynamic capabilities to integrate with the business strategy. The managers can include the

dynamic capabilities by adopting a proper managerial accounting system. Dynamic

capabilities is applied with the target costing techniques in the organisation process for

efficient decision-making process. The case study adds an external pressure to the

management on proper implementation of target costing in today’s automotive world. Failing

in proper understand of the various issues in the company. The resource and dynamic

capabilities is the most competitive advantages of this firm. An organisational can be tangible

and intangible asset that can control the business operations (Knight and Collier, 2009). The

administrative department make this decisions on providing wider opportunities to the

management for successful decision making process. It support the management in providing

the resources. An organisation have the capabilities to properly perform their task in order to

get their desired result. But, the dynamic capabilities change. This includes change in

operational and language capabilities in the manufacturing activities. But, these dynamic

capabilities are embedded in the organisational culture and structure for making strategic

planning and processing. Dynamic capabilities create a value in providing the competitive

advantages. Hence, the value lies in resources and integrating the business process in the

operations. Dynamic capabilities have different product life cycles that help the firm to

emerge in the developing environment. Hence, it provides opportunities and threats to create

a competitive advantage. Organistaions should be capable of changing the dynamic

capabilities. In this, dynamic managerial capabilities is also equally important. Target costing

was developed in Toyota Motor Corporation. They created a target price for the vehicle and

analysed the targeted profit for the suppliers and assemblers. It includes each stage of

production process. It includes product-costing, requirements for the customers and

customer’s willingness to pay. This costing system was regarded as the most efficient

planning technique for the accountants.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10MANAGERIAL ACCOUNTING

From the above case study, it was found that, various factors are influencing in the

functions of target costing. Some of the environmental factors like cultural and organisational

differences influence the target coting system. The other factors are organisational factors

like size of the organisation, managerial support and the organisational capabilities. This

process of market research include the entire infrastructure and culture of organisation. The

different stages for implementing the target costing system is mentioned in the case study.

This include; understanding the dynamic capabilities, which is used to understand the issues

in making strategic decision-making. This is the first stage. The next stage is on integrating

the managerial accounting system with resource and the organisational capabilities. . The

next is product-level of target costing, which focus on achieving the target cost of the product

and transfers to the suppliers. The last stage is component-level target costing section, which

helps the suppliers to efficiently do their work. Target costing is a systematic tool that is used

to do a research on the competitive market. However, various issues are linked to this costing

system. They are:

Recommendations

It is recommended that, out of the two costing system, target costing system is the

best costing system for contemporary organistaions. This is because; the contemporary

organistaions is designed in a simpler and functional design in their business structure. The

managers of a contemporary organisation is involved in deriving the goals of the business.

This costing system can allow the manager to easily make decisions on business goals. But,

target costing system should only be used in a planning process of the product designing

stage (Armitage, Webb and Glynn 2016). Managers should use a combination of both the

target costing system and standard costing system for an efficient business operation. This is

because, target costing system cannot be used for estimating the cost. Therefore, in this case,

From the above case study, it was found that, various factors are influencing in the

functions of target costing. Some of the environmental factors like cultural and organisational

differences influence the target coting system. The other factors are organisational factors

like size of the organisation, managerial support and the organisational capabilities. This

process of market research include the entire infrastructure and culture of organisation. The

different stages for implementing the target costing system is mentioned in the case study.

This include; understanding the dynamic capabilities, which is used to understand the issues

in making strategic decision-making. This is the first stage. The next stage is on integrating

the managerial accounting system with resource and the organisational capabilities. . The

next is product-level of target costing, which focus on achieving the target cost of the product

and transfers to the suppliers. The last stage is component-level target costing section, which

helps the suppliers to efficiently do their work. Target costing is a systematic tool that is used

to do a research on the competitive market. However, various issues are linked to this costing

system. They are:

Recommendations

It is recommended that, out of the two costing system, target costing system is the

best costing system for contemporary organistaions. This is because; the contemporary

organistaions is designed in a simpler and functional design in their business structure. The

managers of a contemporary organisation is involved in deriving the goals of the business.

This costing system can allow the manager to easily make decisions on business goals. But,

target costing system should only be used in a planning process of the product designing

stage (Armitage, Webb and Glynn 2016). Managers should use a combination of both the

target costing system and standard costing system for an efficient business operation. This is

because, target costing system cannot be used for estimating the cost. Therefore, in this case,

11MANAGERIAL ACCOUNTING

standard costing system will be efficient for proper estimation of the cost and accordingly

control their cost by comparing their estimation cost with the actual cost of the goods. Both,

the system is required for properly determining the cost of the product (Patil and Kshatriya

2016). Target costing system is very important to set the business target and standard costing

system is important to control the cost (Maisenbacher et al. 2016). Target costing system will

help in determining the quality and price for the product functions, and standard costing will

help in providing better suggestions for decision-making process.

Conclusion

Therefore, it can be concluded from the above discussion that, both the techniques of

costing is very much important in today’s competitive environment. The significance of both

the target costing and standard costing plays a very important role in managerial decision-

making process. From both the articles, the implementation of standard costing & target

costing had played a very important role for easy managerial decision-making process. These

costing systems can also increase the business productivity and profitability. It can be found

from the above two articles that, the above costing techniques has improved the pricing

strategy of the products. Both the standard costing and target costing system has advantages

& disadvantages. The pharmaceutical & chemical industry is successful in maintaining their

cost from the standard costing technique method. The manufacturing industry are successful

in making decisions. The target costing system is also successful in today’s competitive

environment of the business. Therefore, it is clear that, standard costing system is the best

system for cost controlling and target costing technique is the best technique for planning

purpose of the business.

standard costing system will be efficient for proper estimation of the cost and accordingly

control their cost by comparing their estimation cost with the actual cost of the goods. Both,

the system is required for properly determining the cost of the product (Patil and Kshatriya

2016). Target costing system is very important to set the business target and standard costing

system is important to control the cost (Maisenbacher et al. 2016). Target costing system will

help in determining the quality and price for the product functions, and standard costing will

help in providing better suggestions for decision-making process.

Conclusion

Therefore, it can be concluded from the above discussion that, both the techniques of

costing is very much important in today’s competitive environment. The significance of both

the target costing and standard costing plays a very important role in managerial decision-

making process. From both the articles, the implementation of standard costing & target

costing had played a very important role for easy managerial decision-making process. These

costing systems can also increase the business productivity and profitability. It can be found

from the above two articles that, the above costing techniques has improved the pricing

strategy of the products. Both the standard costing and target costing system has advantages

& disadvantages. The pharmaceutical & chemical industry is successful in maintaining their

cost from the standard costing technique method. The manufacturing industry are successful

in making decisions. The target costing system is also successful in today’s competitive

environment of the business. Therefore, it is clear that, standard costing system is the best

system for cost controlling and target costing technique is the best technique for planning

purpose of the business.

12MANAGERIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13MANAGERIAL ACCOUNTING

References

Anon, (2020). [online] Available at:

https://www.researchgate.net/publication/306446664_IMPLICATIONS_OF_STANDARD_

COSTING_SYSTEM_IN_MANUFACTURING_A_CASE_STUDY [Accessed 25 Jan.

2020].

Armitage, H.M., Webb, A. and Glynn, J., 2016. The use of management accounting

techniques by small and medium‐sized enterprises: a field study of Canadian and Australian

practice. Accounting Perspectives, 15(1), pp.31-69.

Bangara, S.N., 2017. Contextual Factors Influencing Management Accounting Practices

Adopted by Large Manufacturing Companies in Kenya. Res. J. Financ. Account, 23, pp.7-19.

Bargerstock, A. and Shi, Y., 2016. Leaning away from standard costing. Инновации в

менеджменте, (2), pp.4-11.

Cengiz, E. and Ersoy, A., 2017. Decision On Cost Reduction: A Holistic View. Journal of

Accounting & Finance, (75).

Cescon, F., 2019. Costing to support strategy for new product development: a study of

practice in large international companies.

Clermont, M., Ahn, H. and Schwetschke, S., 2018. Research on Target Costing: Past, Present

and Future.

Cuzdriorean, D.D., 2017. The use of management accounting practices by Romanian small

and medium-sized enterprises: A field study. Journal of Accounting and Management

Information Systems, 16(2), pp.291-312.

References

Anon, (2020). [online] Available at:

https://www.researchgate.net/publication/306446664_IMPLICATIONS_OF_STANDARD_

COSTING_SYSTEM_IN_MANUFACTURING_A_CASE_STUDY [Accessed 25 Jan.

2020].

Armitage, H.M., Webb, A. and Glynn, J., 2016. The use of management accounting

techniques by small and medium‐sized enterprises: a field study of Canadian and Australian

practice. Accounting Perspectives, 15(1), pp.31-69.

Bangara, S.N., 2017. Contextual Factors Influencing Management Accounting Practices

Adopted by Large Manufacturing Companies in Kenya. Res. J. Financ. Account, 23, pp.7-19.

Bargerstock, A. and Shi, Y., 2016. Leaning away from standard costing. Инновации в

менеджменте, (2), pp.4-11.

Cengiz, E. and Ersoy, A., 2017. Decision On Cost Reduction: A Holistic View. Journal of

Accounting & Finance, (75).

Cescon, F., 2019. Costing to support strategy for new product development: a study of

practice in large international companies.

Clermont, M., Ahn, H. and Schwetschke, S., 2018. Research on Target Costing: Past, Present

and Future.

Cuzdriorean, D.D., 2017. The use of management accounting practices by Romanian small

and medium-sized enterprises: A field study. Journal of Accounting and Management

Information Systems, 16(2), pp.291-312.

14MANAGERIAL ACCOUNTING

HASSAN, K.M. and MOHAMED, A.H.A., 2018. The Impact of Target Costing (TC) on

Reduction of Manufacturing Costs “Empirical Study”.

Helms, M.M., Ettkin, L.P., Baxter, J.T. and Gordon, M.W., 2005. Managerial implications of

target costing. Competitiveness Review: An International Business Journal, 15(1), pp.49-56.

Knight, K. and Collier, P. (2009). Target Costing in the Automotive Industry: A Case Study

of Dynamic Capabilities. SSRN Electronic Journal.

Maisenbacher, S., Klöppel, M., Laubmann, J., Behncke, F. and Mörtl, M., 2016, September.

Integrated value engineering: Consideration of total cost of ownership for better concept

decision. In 2016 Portland International Conference on Management of Engineering and

Technology (PICMET) (pp. 623-632). IEEE.

Manyaeva, V.A., Piskunov, V.A. and Fomin, V.P., 2016. Strategic management accounting

of company costs. International Review of Management and Marketing, 6(5S), pp.255-264.

Maskell, B.H., Baggaley, B. and Grasso, L., 2017. Practical lean accounting: a proven

system for measuring and managing the lean enterprise. Productivity Press.

Monden, Y. and Hamada, K., 1991. Target costing and kaizen costing in Japanese automobile

companies. Journal of Management Accounting Research, 3(1), pp.16-34.

Paschia, L., 2016. Implementing target costs method in romanian higher education

institutions. Hyperion Economic Journal, 4(1), pp.21-28.

Patil, R. and Kshatriya, A., 2016. Maturity of Cost Management Systems in Organisations.

Journal of Applied Management Accounting Research, 14(2), p.47.

HASSAN, K.M. and MOHAMED, A.H.A., 2018. The Impact of Target Costing (TC) on

Reduction of Manufacturing Costs “Empirical Study”.

Helms, M.M., Ettkin, L.P., Baxter, J.T. and Gordon, M.W., 2005. Managerial implications of

target costing. Competitiveness Review: An International Business Journal, 15(1), pp.49-56.

Knight, K. and Collier, P. (2009). Target Costing in the Automotive Industry: A Case Study

of Dynamic Capabilities. SSRN Electronic Journal.

Maisenbacher, S., Klöppel, M., Laubmann, J., Behncke, F. and Mörtl, M., 2016, September.

Integrated value engineering: Consideration of total cost of ownership for better concept

decision. In 2016 Portland International Conference on Management of Engineering and

Technology (PICMET) (pp. 623-632). IEEE.

Manyaeva, V.A., Piskunov, V.A. and Fomin, V.P., 2016. Strategic management accounting

of company costs. International Review of Management and Marketing, 6(5S), pp.255-264.

Maskell, B.H., Baggaley, B. and Grasso, L., 2017. Practical lean accounting: a proven

system for measuring and managing the lean enterprise. Productivity Press.

Monden, Y. and Hamada, K., 1991. Target costing and kaizen costing in Japanese automobile

companies. Journal of Management Accounting Research, 3(1), pp.16-34.

Paschia, L., 2016. Implementing target costs method in romanian higher education

institutions. Hyperion Economic Journal, 4(1), pp.21-28.

Patil, R. and Kshatriya, A., 2016. Maturity of Cost Management Systems in Organisations.

Journal of Applied Management Accounting Research, 14(2), p.47.

15MANAGERIAL ACCOUNTING

Piersiala, L., 2017. Cost accounting for management of health services in a hospital. Acta

Universitatis Lodziensis. Folia Oeconomica, 3(329), pp.213-225.

Potkány, M., Novák, P., Kováč, R. and Hitka, M., 2017. Innovation of a Technological

Product with Utilizing the Target Costing Methodology. International Review of

Management and Marketing, 7(2), pp.130-137.

Rasit, Z.A. and Ismail, K., 2017. Incorporating Contingency Theory in Understanding Factors

Influencing Target Costing Adoption. Advanced Science Letters, 23(8), pp.7804-7808.

Rasyid, A., Sugiarto, E. and Kosasih, W., 2017. MANAGEMENT ACCOUNTING

TECHNIQUES AND CORPORATE PERFORMANCE OF MANUFACTURING

INDUSTRIES. RISK GOVERNANCE & CONTROL: Financial markets and institutions,

p.116.

Sharaf-Addin, H.H., Omar, N. and Sulaiman, S., 2018. Relationship between Organizational

Capabilities, Implementation Decision on Target Costing and Organisational Performance:

An Empirical Study of Malaysian Automotive Industry. Pertanika Journal of Social Sciences

& Humanities, 26(2).

Steyn, E., 2017. An evaluation of a standard costing framework to manage transport costs

for a South African logistics company (Doctoral dissertation, North-West University (South

Africa), Potchefstroom Campus).

Tsai, W.H., Lan, S.H. and Huang, C.T., 2019. Activity-Based Standard Costing Product-Mix

Decision in the Future Digital Era: Green Recycling Steel-Scrap Material for Steel Industry.

Sustainability, 11(3), p.899.

Piersiala, L., 2017. Cost accounting for management of health services in a hospital. Acta

Universitatis Lodziensis. Folia Oeconomica, 3(329), pp.213-225.

Potkány, M., Novák, P., Kováč, R. and Hitka, M., 2017. Innovation of a Technological

Product with Utilizing the Target Costing Methodology. International Review of

Management and Marketing, 7(2), pp.130-137.

Rasit, Z.A. and Ismail, K., 2017. Incorporating Contingency Theory in Understanding Factors

Influencing Target Costing Adoption. Advanced Science Letters, 23(8), pp.7804-7808.

Rasyid, A., Sugiarto, E. and Kosasih, W., 2017. MANAGEMENT ACCOUNTING

TECHNIQUES AND CORPORATE PERFORMANCE OF MANUFACTURING

INDUSTRIES. RISK GOVERNANCE & CONTROL: Financial markets and institutions,

p.116.

Sharaf-Addin, H.H., Omar, N. and Sulaiman, S., 2018. Relationship between Organizational

Capabilities, Implementation Decision on Target Costing and Organisational Performance:

An Empirical Study of Malaysian Automotive Industry. Pertanika Journal of Social Sciences

& Humanities, 26(2).

Steyn, E., 2017. An evaluation of a standard costing framework to manage transport costs

for a South African logistics company (Doctoral dissertation, North-West University (South

Africa), Potchefstroom Campus).

Tsai, W.H., Lan, S.H. and Huang, C.T., 2019. Activity-Based Standard Costing Product-Mix

Decision in the Future Digital Era: Green Recycling Steel-Scrap Material for Steel Industry.

Sustainability, 11(3), p.899.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16MANAGERIAL ACCOUNTING

Tsifora, E.I. and Chatzoglou, P.D., 2016. Exploring the effects of firm and product

characteristics on cost system’s features. International Journal of Economics & Business

Administration (IJEBA), 4(3), pp.93-116.

Tsifora, E.I. and Chatzoglou, P.D., 2016. Exploring the effects of firm and product

characteristics on cost system’s features. International Journal of Economics & Business

Administration (IJEBA), 4(3), pp.93-116.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.