Holmes Institute HI5017: Managerial Accounting Case Study Analysis

VerifiedAdded on 2022/11/13

|10

|3523

|76

Case Study

AI Summary

This report presents a detailed analysis of managerial accounting, focusing on its application in real-life scenarios. The study examines two distinct situations: the first involves a couple planning to open a home-based daycare, where the concepts of managerial accounting are applied to assess the profitability of the venture, including cost analysis and decision-making regarding expenses. The second part of the analysis is a literature review that explores how Canon Inc. and Apple Computer Inc. utilized managerial accounting to create innovative products by integrating their internal capabilities. The analysis includes the determination of different types of costs, such as fixed, variable, and sunk costs, and their relevance in decision-making. Furthermore, the report assesses various options for laundry services, the impact of hiring an additional employee, and the strategic decision of relocating to a larger facility, providing detailed computations and recommendations for optimal outcomes. The report also references a provided journal article for additional context.

Managerial Accounting – Case Study Analysis

Introduction

The report is an analysis on the perspective of managerial accounting in

terms of how it helps in financial analysis and non-financial analysis in real life

situations. The managerial accounting helps individuals take decisions pertaining to

problems in real life. Here, we have used the concepts of managerial accounting in

two distinct situations:

Situation 1: A couple by the name of Douglas and Pamela Frank wish to open a day

care at their home in the town after their retirement. They want to analyze the

profitability of the venture using the concepts of managerial accounting.

Situation 2: A case study analysis of how two companies Canon Inc. and Apple

Computer Inc. created innovative products by combining their internal capabilities

and information from management accounting. This is more of a literature review to

understand the application of the concepts of management accounting.

Part A – Case Study Analysis

The couple who wishes to open a day care for children at their home “Nanna’s

House” has given information on estimated costs and revenues and wants us to

analyze the profitability of the idea based on facts and figures. We will use the

concepts of managerial accounting to assist them in taking effective decisions.

Solution to Question 1:

The 3 different types of cost described in the case study are as under: -

a) Cost – fixed in Nature – These are costs which are lumpsum, generally

onetime payment in a year. They are pre-determined and must be paid on

the specified date to avoid penalties. These are stagnant and do not

changes with the change in the activity level of the firm. As far as decision

making is considered, these costs are irrelevant as they have been

incurred and thus unavoidable. For Frank couple, the annual license fee of

$225 to be paid to the state for running the day care facility is an example

of fixed cost. This will not change with change in number of children and is

fixed annual payment to the state for running the business.

b) Cost – variable in nature– These are recurring expenses for the business

based on the actual activity level of the concern. These are costs which

are paid on the basis of change in some variable on which the cost are

dependent. As far as decision making is considered, these costs are

relevant as they will be incurred based on the decision made. For Frank

couple, the cost of the meal and snack @ $3.20 per child is variable on the

number of children enrolled at the facility run by them.

c) Cost – Sunk in nature–Sunk costs are those costs which have already

been incurred in the past and cannot be reversed now by the concern.

They have been paid historically. These costs generally are large

payments whose benefits are derived by the firm for a larger span of time.

For any decision making, these costs are irrelevant as they have been

Introduction

The report is an analysis on the perspective of managerial accounting in

terms of how it helps in financial analysis and non-financial analysis in real life

situations. The managerial accounting helps individuals take decisions pertaining to

problems in real life. Here, we have used the concepts of managerial accounting in

two distinct situations:

Situation 1: A couple by the name of Douglas and Pamela Frank wish to open a day

care at their home in the town after their retirement. They want to analyze the

profitability of the venture using the concepts of managerial accounting.

Situation 2: A case study analysis of how two companies Canon Inc. and Apple

Computer Inc. created innovative products by combining their internal capabilities

and information from management accounting. This is more of a literature review to

understand the application of the concepts of management accounting.

Part A – Case Study Analysis

The couple who wishes to open a day care for children at their home “Nanna’s

House” has given information on estimated costs and revenues and wants us to

analyze the profitability of the idea based on facts and figures. We will use the

concepts of managerial accounting to assist them in taking effective decisions.

Solution to Question 1:

The 3 different types of cost described in the case study are as under: -

a) Cost – fixed in Nature – These are costs which are lumpsum, generally

onetime payment in a year. They are pre-determined and must be paid on

the specified date to avoid penalties. These are stagnant and do not

changes with the change in the activity level of the firm. As far as decision

making is considered, these costs are irrelevant as they have been

incurred and thus unavoidable. For Frank couple, the annual license fee of

$225 to be paid to the state for running the day care facility is an example

of fixed cost. This will not change with change in number of children and is

fixed annual payment to the state for running the business.

b) Cost – variable in nature– These are recurring expenses for the business

based on the actual activity level of the concern. These are costs which

are paid on the basis of change in some variable on which the cost are

dependent. As far as decision making is considered, these costs are

relevant as they will be incurred based on the decision made. For Frank

couple, the cost of the meal and snack @ $3.20 per child is variable on the

number of children enrolled at the facility run by them.

c) Cost – Sunk in nature–Sunk costs are those costs which have already

been incurred in the past and cannot be reversed now by the concern.

They have been paid historically. These costs generally are large

payments whose benefits are derived by the firm for a larger span of time.

For any decision making, these costs are irrelevant as they have been

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Accounting – Case Study Analysis

incurred and will not change now with any decisions. For the Frank couple,

the renovation cost of $79,500 that has been paid to enhance the life of

the house by 25 years is a perfect example of sunk cost. This has been

incurred, is a large payment, benefits for 25 years will be accrued and

irrelevant for any decision making.

Solution to Question 2:

In context to purchase of the appliances by the couple, the analysis of the cost is as

below:

The couple wishes to purchase appliances for doing laundry in house themselves.

The information or costs that are relevant to the purchase of appliances are costs

which are variable or semi variable in nature as these will be affected by the decision

of the couple. Here, for the couple the following costs or information will be relevant

for effective decision making:

Cost of the appliances

Installation cost of the appliances

Cost of the accessories required for the appliances

Increase in energy costs due to the use of appliances

Life of the appliances to understand the implication of depreciation

Annual cost outlay when availing other available options for doing laundry,

including using the services of Red Oak @ $52 per month or doing the

laundry at the nearest Laundromat.

Further, the information or costs which are irrelevant for the decision on purchasing

the appliances are:

Cost of the old appliances

Life of the old appliances

Insurance Cost

Cost of the renovation made

Cost of the meals and snacks

Utilities cost for the children.

Solution to Question 3:

At the day care facility that the couple wishes to open, they will have to arrange for

the laundry of the spoiled clothes of the children enrolled at the facility. The couple

has three different options to this effect and the decision on the same will be based

on the lowest cost outlay to the couple.

The three available options to the couple are as below:

a. Purchase appliances (washer and dryer), purchase detergent and do in

house laundry by them at the day care facility only.

b. Hire the services of red Oak laundry services that will pick up the stained

clothes and deliver the washed clothes at a charge of $52 per month.

c. Do the laundry themselves by purchasing detergent and availing the

service of the Laundromat which is 3 miles away from their home.

incurred and will not change now with any decisions. For the Frank couple,

the renovation cost of $79,500 that has been paid to enhance the life of

the house by 25 years is a perfect example of sunk cost. This has been

incurred, is a large payment, benefits for 25 years will be accrued and

irrelevant for any decision making.

Solution to Question 2:

In context to purchase of the appliances by the couple, the analysis of the cost is as

below:

The couple wishes to purchase appliances for doing laundry in house themselves.

The information or costs that are relevant to the purchase of appliances are costs

which are variable or semi variable in nature as these will be affected by the decision

of the couple. Here, for the couple the following costs or information will be relevant

for effective decision making:

Cost of the appliances

Installation cost of the appliances

Cost of the accessories required for the appliances

Increase in energy costs due to the use of appliances

Life of the appliances to understand the implication of depreciation

Annual cost outlay when availing other available options for doing laundry,

including using the services of Red Oak @ $52 per month or doing the

laundry at the nearest Laundromat.

Further, the information or costs which are irrelevant for the decision on purchasing

the appliances are:

Cost of the old appliances

Life of the old appliances

Insurance Cost

Cost of the renovation made

Cost of the meals and snacks

Utilities cost for the children.

Solution to Question 3:

At the day care facility that the couple wishes to open, they will have to arrange for

the laundry of the spoiled clothes of the children enrolled at the facility. The couple

has three different options to this effect and the decision on the same will be based

on the lowest cost outlay to the couple.

The three available options to the couple are as below:

a. Purchase appliances (washer and dryer), purchase detergent and do in

house laundry by them at the day care facility only.

b. Hire the services of red Oak laundry services that will pick up the stained

clothes and deliver the washed clothes at a charge of $52 per month.

c. Do the laundry themselves by purchasing detergent and availing the

service of the Laundromat which is 3 miles away from their home.

Managerial Accounting – Case Study Analysis

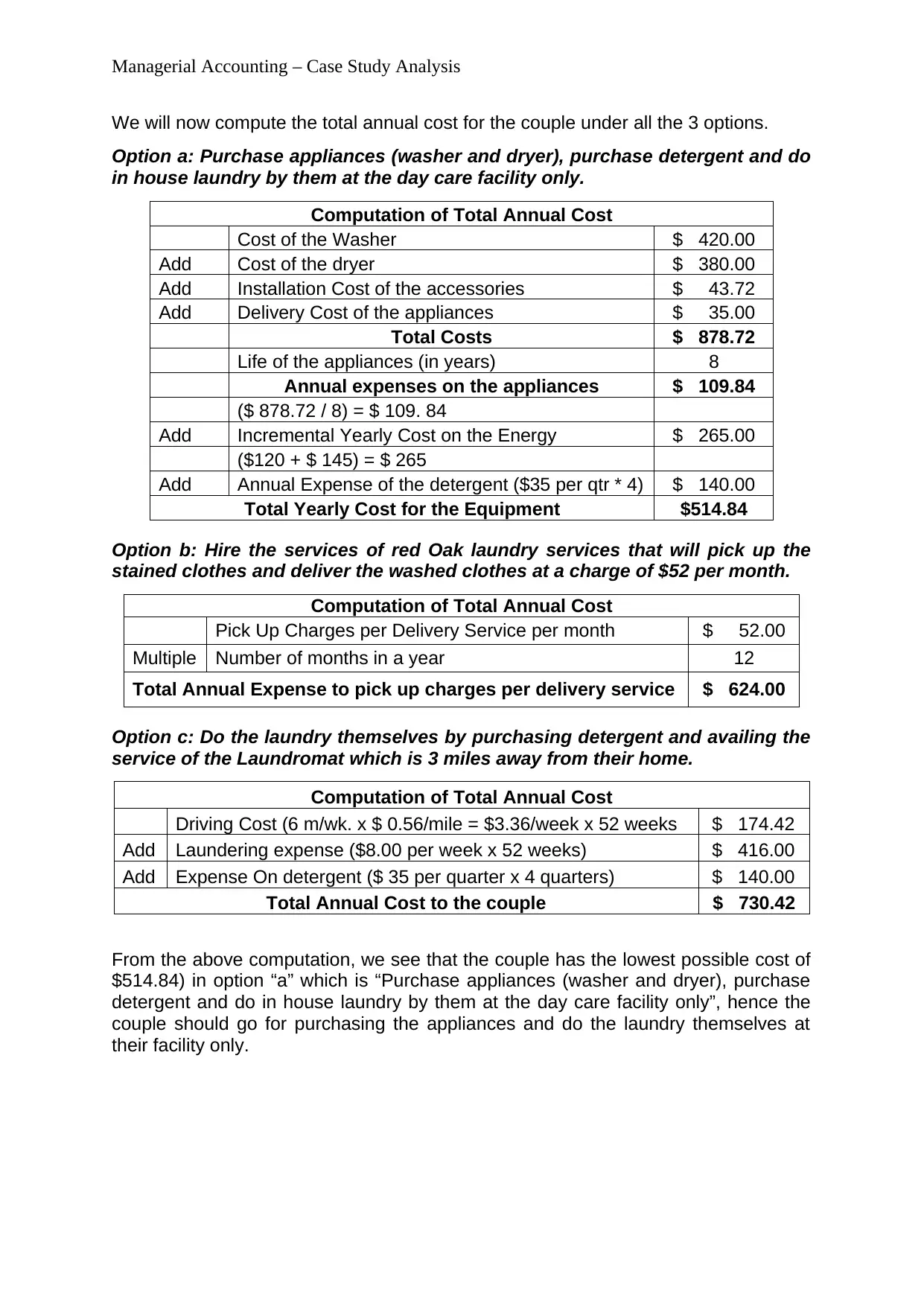

We will now compute the total annual cost for the couple under all the 3 options.

Option a: Purchase appliances (washer and dryer), purchase detergent and do

in house laundry by them at the day care facility only.

Computation of Total Annual Cost

Cost of the Washer $ 420.00

Add Cost of the dryer $ 380.00

Add Installation Cost of the accessories $ 43.72

Add Delivery Cost of the appliances $ 35.00

Total Costs $ 878.72

Life of the appliances (in years) 8

Annual expenses on the appliances $ 109.84

($ 878.72 / 8) = $ 109. 84

Add Incremental Yearly Cost on the Energy $ 265.00

($120 + $ 145) = $ 265

Add Annual Expense of the detergent ($35 per qtr * 4) $ 140.00

Total Yearly Cost for the Equipment $514.84

Option b: Hire the services of red Oak laundry services that will pick up the

stained clothes and deliver the washed clothes at a charge of $52 per month.

Computation of Total Annual Cost

Pick Up Charges per Delivery Service per month $ 52.00

Multiple Number of months in a year 12

Total Annual Expense to pick up charges per delivery service $ 624.00

Option c: Do the laundry themselves by purchasing detergent and availing the

service of the Laundromat which is 3 miles away from their home.

Computation of Total Annual Cost

Driving Cost (6 m/wk. x $ 0.56/mile = $3.36/week x 52 weeks $ 174.42

Add Laundering expense ($8.00 per week x 52 weeks) $ 416.00

Add Expense On detergent ($ 35 per quarter x 4 quarters) $ 140.00

Total Annual Cost to the couple $ 730.42

From the above computation, we see that the couple has the lowest possible cost of

$514.84) in option “a” which is “Purchase appliances (washer and dryer), purchase

detergent and do in house laundry by them at the day care facility only”, hence the

couple should go for purchasing the appliances and do the laundry themselves at

their facility only.

We will now compute the total annual cost for the couple under all the 3 options.

Option a: Purchase appliances (washer and dryer), purchase detergent and do

in house laundry by them at the day care facility only.

Computation of Total Annual Cost

Cost of the Washer $ 420.00

Add Cost of the dryer $ 380.00

Add Installation Cost of the accessories $ 43.72

Add Delivery Cost of the appliances $ 35.00

Total Costs $ 878.72

Life of the appliances (in years) 8

Annual expenses on the appliances $ 109.84

($ 878.72 / 8) = $ 109. 84

Add Incremental Yearly Cost on the Energy $ 265.00

($120 + $ 145) = $ 265

Add Annual Expense of the detergent ($35 per qtr * 4) $ 140.00

Total Yearly Cost for the Equipment $514.84

Option b: Hire the services of red Oak laundry services that will pick up the

stained clothes and deliver the washed clothes at a charge of $52 per month.

Computation of Total Annual Cost

Pick Up Charges per Delivery Service per month $ 52.00

Multiple Number of months in a year 12

Total Annual Expense to pick up charges per delivery service $ 624.00

Option c: Do the laundry themselves by purchasing detergent and availing the

service of the Laundromat which is 3 miles away from their home.

Computation of Total Annual Cost

Driving Cost (6 m/wk. x $ 0.56/mile = $3.36/week x 52 weeks $ 174.42

Add Laundering expense ($8.00 per week x 52 weeks) $ 416.00

Add Expense On detergent ($ 35 per quarter x 4 quarters) $ 140.00

Total Annual Cost to the couple $ 730.42

From the above computation, we see that the couple has the lowest possible cost of

$514.84) in option “a” which is “Purchase appliances (washer and dryer), purchase

detergent and do in house laundry by them at the day care facility only”, hence the

couple should go for purchasing the appliances and do the laundry themselves at

their facility only.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managerial Accounting – Case Study Analysis

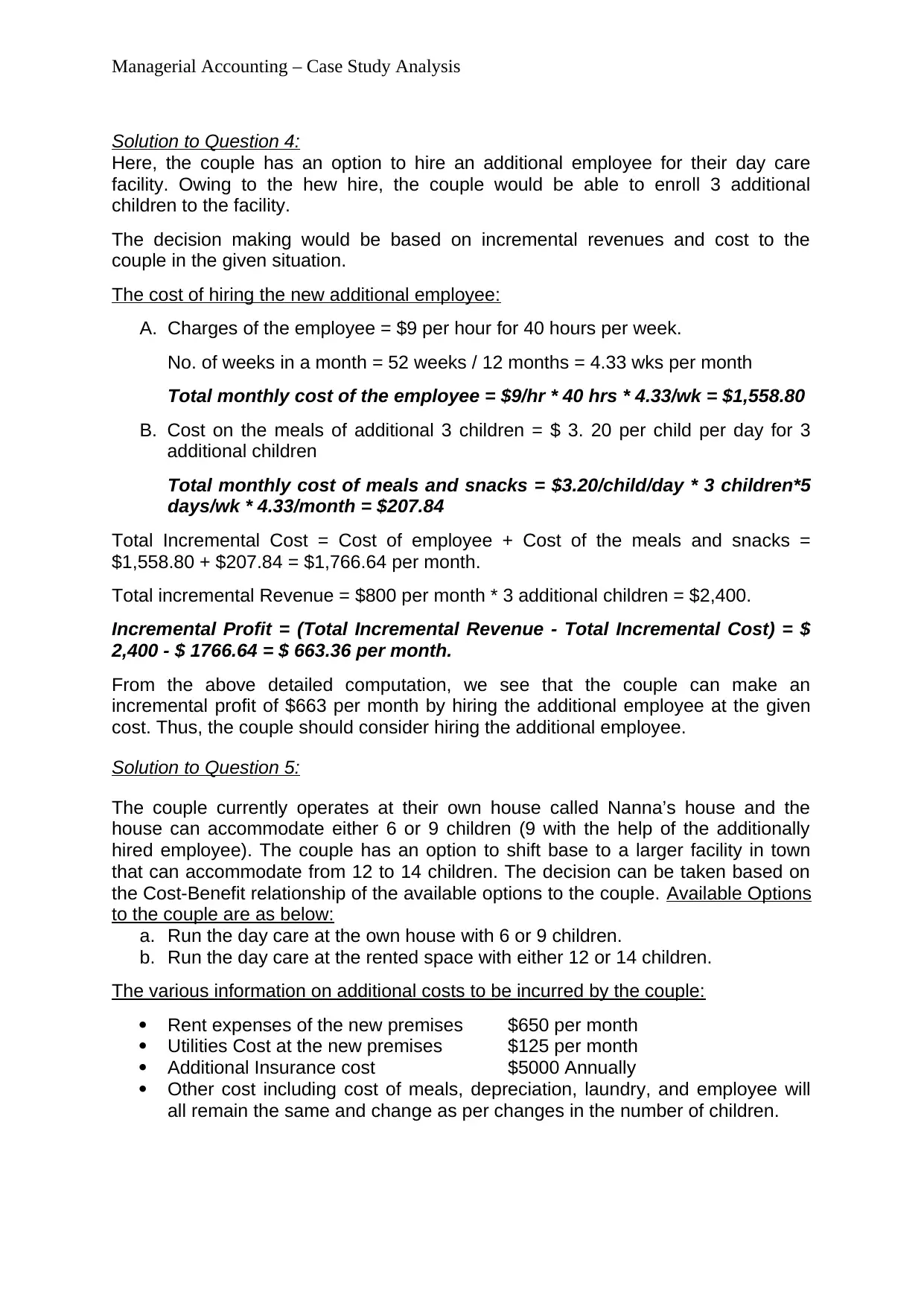

Solution to Question 4:

Here, the couple has an option to hire an additional employee for their day care

facility. Owing to the hew hire, the couple would be able to enroll 3 additional

children to the facility.

The decision making would be based on incremental revenues and cost to the

couple in the given situation.

The cost of hiring the new additional employee:

A. Charges of the employee = $9 per hour for 40 hours per week.

No. of weeks in a month = 52 weeks / 12 months = 4.33 wks per month

Total monthly cost of the employee = $9/hr * 40 hrs * 4.33/wk = $1,558.80

B. Cost on the meals of additional 3 children = $ 3. 20 per child per day for 3

additional children

Total monthly cost of meals and snacks = $3.20/child/day * 3 children*5

days/wk * 4.33/month = $207.84

Total Incremental Cost = Cost of employee + Cost of the meals and snacks =

$1,558.80 + $207.84 = $1,766.64 per month.

Total incremental Revenue = $800 per month * 3 additional children = $2,400.

Incremental Profit = (Total Incremental Revenue - Total Incremental Cost) = $

2,400 - $ 1766.64 = $ 663.36 per month.

From the above detailed computation, we see that the couple can make an

incremental profit of $663 per month by hiring the additional employee at the given

cost. Thus, the couple should consider hiring the additional employee.

Solution to Question 5:

The couple currently operates at their own house called Nanna’s house and the

house can accommodate either 6 or 9 children (9 with the help of the additionally

hired employee). The couple has an option to shift base to a larger facility in town

that can accommodate from 12 to 14 children. The decision can be taken based on

the Cost-Benefit relationship of the available options to the couple. Available Options

to the couple are as below:

a. Run the day care at the own house with 6 or 9 children.

b. Run the day care at the rented space with either 12 or 14 children.

The various information on additional costs to be incurred by the couple:

Rent expenses of the new premises $650 per month

Utilities Cost at the new premises $125 per month

Additional Insurance cost $5000 Annually

Other cost including cost of meals, depreciation, laundry, and employee will

all remain the same and change as per changes in the number of children.

Solution to Question 4:

Here, the couple has an option to hire an additional employee for their day care

facility. Owing to the hew hire, the couple would be able to enroll 3 additional

children to the facility.

The decision making would be based on incremental revenues and cost to the

couple in the given situation.

The cost of hiring the new additional employee:

A. Charges of the employee = $9 per hour for 40 hours per week.

No. of weeks in a month = 52 weeks / 12 months = 4.33 wks per month

Total monthly cost of the employee = $9/hr * 40 hrs * 4.33/wk = $1,558.80

B. Cost on the meals of additional 3 children = $ 3. 20 per child per day for 3

additional children

Total monthly cost of meals and snacks = $3.20/child/day * 3 children*5

days/wk * 4.33/month = $207.84

Total Incremental Cost = Cost of employee + Cost of the meals and snacks =

$1,558.80 + $207.84 = $1,766.64 per month.

Total incremental Revenue = $800 per month * 3 additional children = $2,400.

Incremental Profit = (Total Incremental Revenue - Total Incremental Cost) = $

2,400 - $ 1766.64 = $ 663.36 per month.

From the above detailed computation, we see that the couple can make an

incremental profit of $663 per month by hiring the additional employee at the given

cost. Thus, the couple should consider hiring the additional employee.

Solution to Question 5:

The couple currently operates at their own house called Nanna’s house and the

house can accommodate either 6 or 9 children (9 with the help of the additionally

hired employee). The couple has an option to shift base to a larger facility in town

that can accommodate from 12 to 14 children. The decision can be taken based on

the Cost-Benefit relationship of the available options to the couple. Available Options

to the couple are as below:

a. Run the day care at the own house with 6 or 9 children.

b. Run the day care at the rented space with either 12 or 14 children.

The various information on additional costs to be incurred by the couple:

Rent expenses of the new premises $650 per month

Utilities Cost at the new premises $125 per month

Additional Insurance cost $5000 Annually

Other cost including cost of meals, depreciation, laundry, and employee will

all remain the same and change as per changes in the number of children.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Accounting – Case Study Analysis

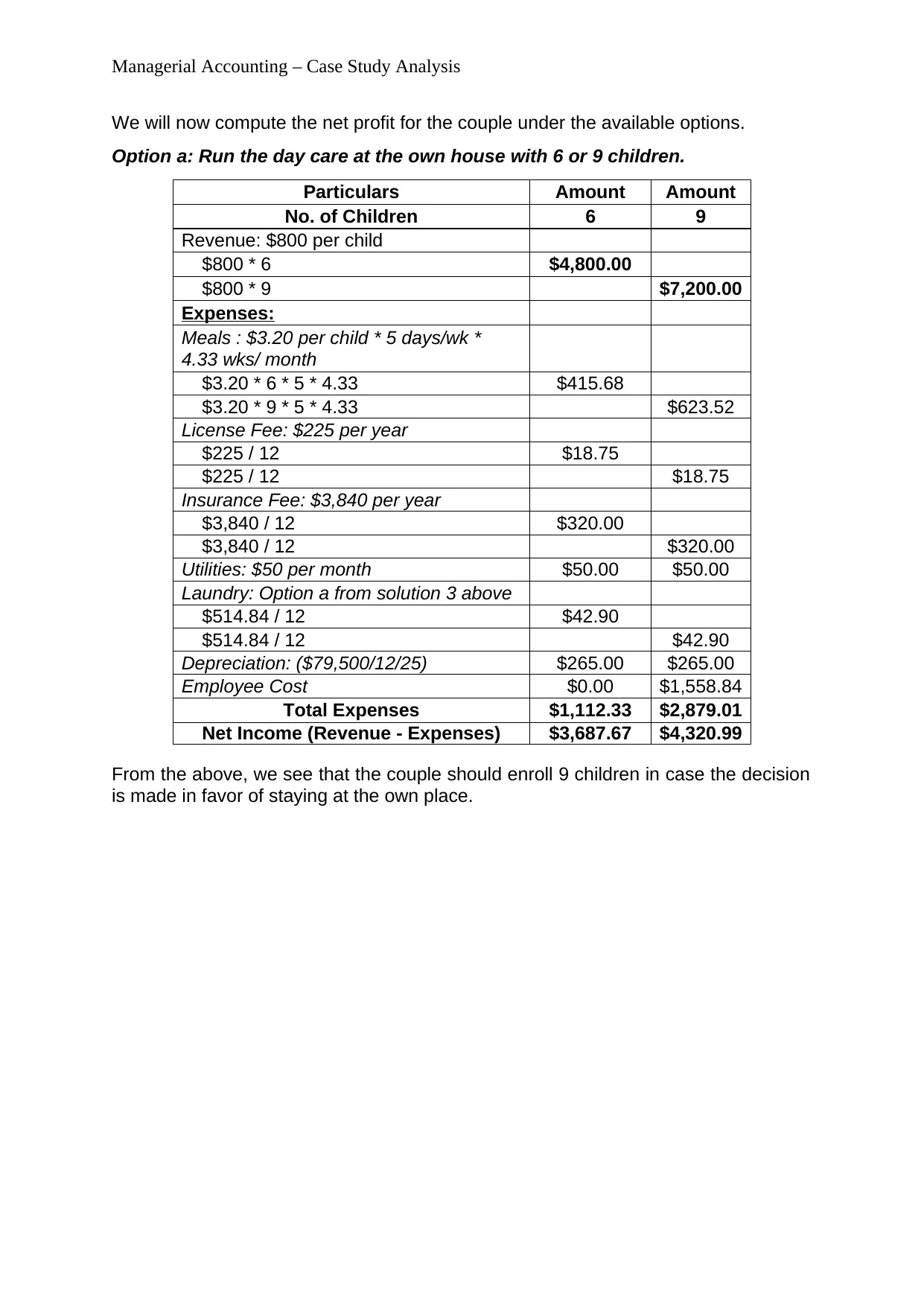

We will now compute the net profit for the couple under the available options.

Option a: Run the day care at the own house with 6 or 9 children.

Particulars Amount Amount

No. of Children 6 9

Revenue: $800 per child

$800 * 6 $4,800.00

$800 * 9 $7,200.00

Expenses:

Meals : $3.20 per child * 5 days/wk *

4.33 wks/ month

$3.20 * 6 * 5 * 4.33 $415.68

$3.20 * 9 * 5 * 4.33 $623.52

License Fee: $225 per year

$225 / 12 $18.75

$225 / 12 $18.75

Insurance Fee: $3,840 per year

$3,840 / 12 $320.00

$3,840 / 12 $320.00

Utilities: $50 per month $50.00 $50.00

Laundry: Option a from solution 3 above

$514.84 / 12 $42.90

$514.84 / 12 $42.90

Depreciation: ($79,500/12/25) $265.00 $265.00

Employee Cost $0.00 $1,558.84

Total Expenses $1,112.33 $2,879.01

Net Income (Revenue - Expenses) $3,687.67 $4,320.99

From the above, we see that the couple should enroll 9 children in case the decision

is made in favor of staying at the own place.

We will now compute the net profit for the couple under the available options.

Option a: Run the day care at the own house with 6 or 9 children.

Particulars Amount Amount

No. of Children 6 9

Revenue: $800 per child

$800 * 6 $4,800.00

$800 * 9 $7,200.00

Expenses:

Meals : $3.20 per child * 5 days/wk *

4.33 wks/ month

$3.20 * 6 * 5 * 4.33 $415.68

$3.20 * 9 * 5 * 4.33 $623.52

License Fee: $225 per year

$225 / 12 $18.75

$225 / 12 $18.75

Insurance Fee: $3,840 per year

$3,840 / 12 $320.00

$3,840 / 12 $320.00

Utilities: $50 per month $50.00 $50.00

Laundry: Option a from solution 3 above

$514.84 / 12 $42.90

$514.84 / 12 $42.90

Depreciation: ($79,500/12/25) $265.00 $265.00

Employee Cost $0.00 $1,558.84

Total Expenses $1,112.33 $2,879.01

Net Income (Revenue - Expenses) $3,687.67 $4,320.99

From the above, we see that the couple should enroll 9 children in case the decision

is made in favor of staying at the own place.

Managerial Accounting – Case Study Analysis

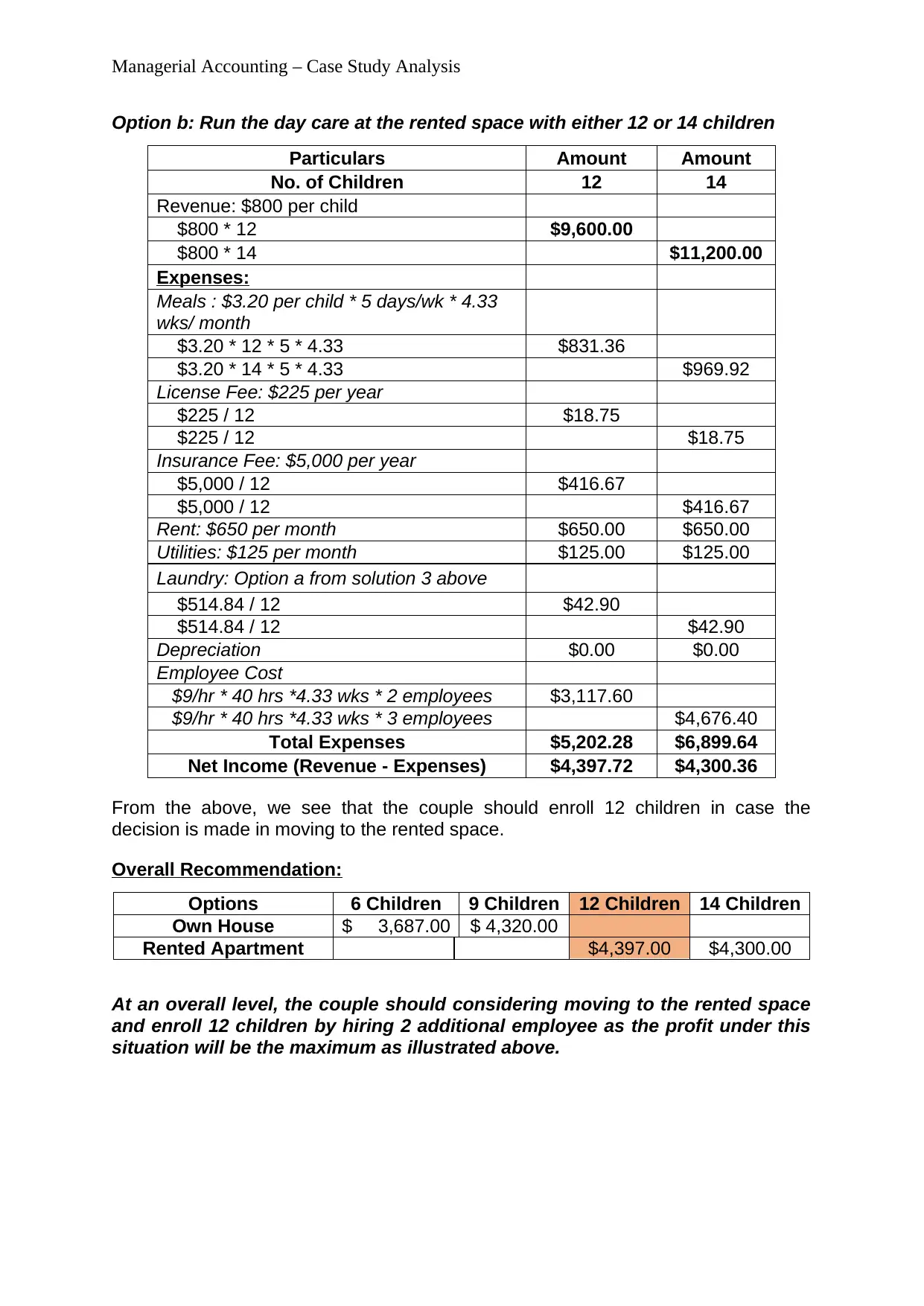

Option b: Run the day care at the rented space with either 12 or 14 children

Particulars Amount Amount

No. of Children 12 14

Revenue: $800 per child

$800 * 12 $9,600.00

$800 * 14 $11,200.00

Expenses:

Meals : $3.20 per child * 5 days/wk * 4.33

wks/ month

$3.20 * 12 * 5 * 4.33 $831.36

$3.20 * 14 * 5 * 4.33 $969.92

License Fee: $225 per year

$225 / 12 $18.75

$225 / 12 $18.75

Insurance Fee: $5,000 per year

$5,000 / 12 $416.67

$5,000 / 12 $416.67

Rent: $650 per month $650.00 $650.00

Utilities: $125 per month $125.00 $125.00

Laundry: Option a from solution 3 above

$514.84 / 12 $42.90

$514.84 / 12 $42.90

Depreciation $0.00 $0.00

Employee Cost

$9/hr * 40 hrs *4.33 wks * 2 employees $3,117.60

$9/hr * 40 hrs *4.33 wks * 3 employees $4,676.40

Total Expenses $5,202.28 $6,899.64

Net Income (Revenue - Expenses) $4,397.72 $4,300.36

From the above, we see that the couple should enroll 12 children in case the

decision is made in moving to the rented space.

Overall Recommendation:

Options 6 Children 9 Children 12 Children 14 Children

Own House $ 3,687.00 $ 4,320.00

Rented Apartment $4,397.00 $4,300.00

At an overall level, the couple should considering moving to the rented space

and enroll 12 children by hiring 2 additional employee as the profit under this

situation will be the maximum as illustrated above.

Option b: Run the day care at the rented space with either 12 or 14 children

Particulars Amount Amount

No. of Children 12 14

Revenue: $800 per child

$800 * 12 $9,600.00

$800 * 14 $11,200.00

Expenses:

Meals : $3.20 per child * 5 days/wk * 4.33

wks/ month

$3.20 * 12 * 5 * 4.33 $831.36

$3.20 * 14 * 5 * 4.33 $969.92

License Fee: $225 per year

$225 / 12 $18.75

$225 / 12 $18.75

Insurance Fee: $5,000 per year

$5,000 / 12 $416.67

$5,000 / 12 $416.67

Rent: $650 per month $650.00 $650.00

Utilities: $125 per month $125.00 $125.00

Laundry: Option a from solution 3 above

$514.84 / 12 $42.90

$514.84 / 12 $42.90

Depreciation $0.00 $0.00

Employee Cost

$9/hr * 40 hrs *4.33 wks * 2 employees $3,117.60

$9/hr * 40 hrs *4.33 wks * 3 employees $4,676.40

Total Expenses $5,202.28 $6,899.64

Net Income (Revenue - Expenses) $4,397.72 $4,300.36

From the above, we see that the couple should enroll 12 children in case the

decision is made in moving to the rented space.

Overall Recommendation:

Options 6 Children 9 Children 12 Children 14 Children

Own House $ 3,687.00 $ 4,320.00

Rented Apartment $4,397.00 $4,300.00

At an overall level, the couple should considering moving to the rented space

and enroll 12 children by hiring 2 additional employee as the profit under this

situation will be the maximum as illustrated above.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managerial Accounting – Case Study Analysis

Part B – Journal Critique Analysis

Solution to Question 1:

The concepts of management accountancy used in Canon Inc.

The organization used team work in their approach to working towards the solution

of replacing heavy weight printers. The team would sit together and brain storm

solutions with ideas coming from employees even at the lowest rank in the hierarchy.

The information flow in the system was controlled by the top management, who

would announce the problems to the team. The team was then entrusted to work in

cohesion towards finding solution to the identified problem. This was absent in the

company earlier, but with time, the company was able to realize the importance of

information flow and that helped the company grow and prosper. The Management

Accountant provided timely information on cost and benefit to keep the project team

informed about the profitability of their venture. Thus, at an overall level, the

management accountant was able to provide the team a financial perspective on

their innovation and ideas to create a balanced working environment.

Examples: Use of financial constraints (price should be within 1,000 yen)

The concepts of management accountancy used in Apple Computer Inc: -

Here, the approach was top-down approach with clearly charted out authorities and

responsibilities for each team member. The team was controlled centrally by one

person known as the central hub. They were centralized, authoritative and

bureaucratic in their approach. That one single person with the controlling powers

was Steve Jobs himself. He has meticulously reviewed the organization and made it

what it is known today. The products were also centrally controlled with one closed-

circuit part that was of key importance for the entire product. The company has been

fundamental in outlasting all the products in the market only because of innovation

that it made and that too on profit margins which were on a higher side.

Example: Setting up of target costs based on internal information regarding factory

costs.

Solution to Question 2:

“Innovation as a Process of Information creation”

Both the organization took drastic steps to promote innovation within the company

and was able to create a culture that fostered ideas and innovation all the time. The

specific examples are as below:

For Canon Inc.

1) Technology improvement with thrust on reviewing the progress regularly was

the motto of innovating the products with ease for the company. The company

followed the same vigor and model to replicate good practices across the

organization. The outcome was products that were user-friendly and easily

adaptable.

Part B – Journal Critique Analysis

Solution to Question 1:

The concepts of management accountancy used in Canon Inc.

The organization used team work in their approach to working towards the solution

of replacing heavy weight printers. The team would sit together and brain storm

solutions with ideas coming from employees even at the lowest rank in the hierarchy.

The information flow in the system was controlled by the top management, who

would announce the problems to the team. The team was then entrusted to work in

cohesion towards finding solution to the identified problem. This was absent in the

company earlier, but with time, the company was able to realize the importance of

information flow and that helped the company grow and prosper. The Management

Accountant provided timely information on cost and benefit to keep the project team

informed about the profitability of their venture. Thus, at an overall level, the

management accountant was able to provide the team a financial perspective on

their innovation and ideas to create a balanced working environment.

Examples: Use of financial constraints (price should be within 1,000 yen)

The concepts of management accountancy used in Apple Computer Inc: -

Here, the approach was top-down approach with clearly charted out authorities and

responsibilities for each team member. The team was controlled centrally by one

person known as the central hub. They were centralized, authoritative and

bureaucratic in their approach. That one single person with the controlling powers

was Steve Jobs himself. He has meticulously reviewed the organization and made it

what it is known today. The products were also centrally controlled with one closed-

circuit part that was of key importance for the entire product. The company has been

fundamental in outlasting all the products in the market only because of innovation

that it made and that too on profit margins which were on a higher side.

Example: Setting up of target costs based on internal information regarding factory

costs.

Solution to Question 2:

“Innovation as a Process of Information creation”

Both the organization took drastic steps to promote innovation within the company

and was able to create a culture that fostered ideas and innovation all the time. The

specific examples are as below:

For Canon Inc.

1) Technology improvement with thrust on reviewing the progress regularly was

the motto of innovating the products with ease for the company. The company

followed the same vigor and model to replicate good practices across the

organization. The outcome was products that were user-friendly and easily

adaptable.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Accounting – Case Study Analysis

2) The team effort and team work worked successfully for the company as the

team interacted very often. The communication was regular, open, and useful

for teams to develop self and company. This helped teams create products

that were interactive and easy to use by the consumers.

For Apple Computer Inc.

1) The company created its own operating system by the name of Macintosh.

This was new, fresh, vibrant, interactive, user friendly, full of energy, colorful

and what not. It was a pure customer delight. This product made the brand in

the world and enable them create a mark in the global world.

2) The company adopted the Japanese system where focus was made for being

on time every time. The company adopted their culture. This lead to presence

of strong loyalty, trust and bonding among the employees.

Solution to Question 3:

The case study has some exemplary outcomes that can be used by management

accountants in Australian companies for betterment and effective decision making.

These outcomes that have real life applications in Australia are as below:

For Canon Inc.

1) The organization promoted the concept of team effort and teamwork to garner

profits, goodwill and prosperity for the firm in the long run. The idea was to

understand and implement that no one can work in isolation and it is a team

that makes or breaks the organization.

2) The company was able to prove that ideas and innovation can come even

from the lowest ranks in a concern. It is only by working in cohesive teams

that one get to interact with others and promote development of ideas and

innovation from all corners of the company.

For Apple Computer Inc.

1) Apple computer Inc. showed how a clearly promoted mission and vision of the

company helps the employees reach their goals with ease. The employees

should show trust in the policies and goals of the company and align their

goals with that of the company’s.

2) The crux of doing any business is making profit and Apple preached that ROI

or the Return on Investment is crucial for the success of any firm and that

firms should track their ROI closely along with their efforts to understand the

profitability of the company.

2) The team effort and team work worked successfully for the company as the

team interacted very often. The communication was regular, open, and useful

for teams to develop self and company. This helped teams create products

that were interactive and easy to use by the consumers.

For Apple Computer Inc.

1) The company created its own operating system by the name of Macintosh.

This was new, fresh, vibrant, interactive, user friendly, full of energy, colorful

and what not. It was a pure customer delight. This product made the brand in

the world and enable them create a mark in the global world.

2) The company adopted the Japanese system where focus was made for being

on time every time. The company adopted their culture. This lead to presence

of strong loyalty, trust and bonding among the employees.

Solution to Question 3:

The case study has some exemplary outcomes that can be used by management

accountants in Australian companies for betterment and effective decision making.

These outcomes that have real life applications in Australia are as below:

For Canon Inc.

1) The organization promoted the concept of team effort and teamwork to garner

profits, goodwill and prosperity for the firm in the long run. The idea was to

understand and implement that no one can work in isolation and it is a team

that makes or breaks the organization.

2) The company was able to prove that ideas and innovation can come even

from the lowest ranks in a concern. It is only by working in cohesive teams

that one get to interact with others and promote development of ideas and

innovation from all corners of the company.

For Apple Computer Inc.

1) Apple computer Inc. showed how a clearly promoted mission and vision of the

company helps the employees reach their goals with ease. The employees

should show trust in the policies and goals of the company and align their

goals with that of the company’s.

2) The crux of doing any business is making profit and Apple preached that ROI

or the Return on Investment is crucial for the success of any firm and that

firms should track their ROI closely along with their efforts to understand the

profitability of the company.

Managerial Accounting – Case Study Analysis

Conclusion

The report on the case study analysis provides an overall view of how management

accountancy concepts helps individuals in real life situation by enabling them take

effective decisions. Both the above case studies were different in their approach bit

similar to the concepts that they were promoting. The case study on couple

illustrates how proper information on cost and revenues enable one take informed

business decisions in a way that maximize their profitability. The case study on

innovation by Canon Inc. and Apple Computer Inc. illustrates how important non-

financial decisions help companies reach their goals. This is an account of how

managerial accounting and its concepts promote effective and efficient decision

making in a concern.

Conclusion

The report on the case study analysis provides an overall view of how management

accountancy concepts helps individuals in real life situation by enabling them take

effective decisions. Both the above case studies were different in their approach bit

similar to the concepts that they were promoting. The case study on couple

illustrates how proper information on cost and revenues enable one take informed

business decisions in a way that maximize their profitability. The case study on

innovation by Canon Inc. and Apple Computer Inc. illustrates how important non-

financial decisions help companies reach their goals. This is an account of how

managerial accounting and its concepts promote effective and efficient decision

making in a concern.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managerial Accounting – Case Study Analysis

References

Askarany, D., 2016. Attributes of innovation and management accounting changes.

Contemporary Management Research, pp.455-466.

Breuer, A., Frumusanu, M.L. and Manciu, A., 2013. The role of management

accounting in the decision making process: Case study Caras Severin county.

Annales Universitatis Apulensis: Series Oeconomica, 15(2), p.355.

Chen, S.S., Huang, C.W., Hwang, C.Y. and Wang, Y., 2019. Voluntary Disclosure

and Corporate Innovation. Available at SSRN 3311932.

Nonala, I. and Kenney, M. (1991). Towards a new theory of innovation management:

A case study comparing Canon, Inc. and Apple Computer, Inc. Journal of

Engineering and Technology Management, 8(1), pp.67-83.

Otley, D., 2016. The contingency theory of management accounting and control:

1980–2014. Management accounting research, 31, pp.45-62.

Quinn, W., 2012. Managing innovation: Controlled chaos. Harv. Bus. Rev., (May-

June): 73 80.

Zanin, F., Comuzzi, E. and Costantini, A., 2019. Management Control Systems:

Concepts and Approaches. In Human Performance Technology: Concepts,

Methodologies, Tools, and Applications (pp. 455-473). IGI Global.

References

Askarany, D., 2016. Attributes of innovation and management accounting changes.

Contemporary Management Research, pp.455-466.

Breuer, A., Frumusanu, M.L. and Manciu, A., 2013. The role of management

accounting in the decision making process: Case study Caras Severin county.

Annales Universitatis Apulensis: Series Oeconomica, 15(2), p.355.

Chen, S.S., Huang, C.W., Hwang, C.Y. and Wang, Y., 2019. Voluntary Disclosure

and Corporate Innovation. Available at SSRN 3311932.

Nonala, I. and Kenney, M. (1991). Towards a new theory of innovation management:

A case study comparing Canon, Inc. and Apple Computer, Inc. Journal of

Engineering and Technology Management, 8(1), pp.67-83.

Otley, D., 2016. The contingency theory of management accounting and control:

1980–2014. Management accounting research, 31, pp.45-62.

Quinn, W., 2012. Managing innovation: Controlled chaos. Harv. Bus. Rev., (May-

June): 73 80.

Zanin, F., Comuzzi, E. and Costantini, A., 2019. Management Control Systems:

Concepts and Approaches. In Human Performance Technology: Concepts,

Methodologies, Tools, and Applications (pp. 455-473). IGI Global.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.