HI5017 - Managerial Accounting: Cost Analysis Case Study Assignment

VerifiedAdded on 2023/03/31

|11

|1915

|64

Homework Assignment

AI Summary

This managerial accounting case study examines cost concepts and their application in a service-based company. The assignment analyzes different cost behaviors, including fixed, variable, and semi-variable costs, and applies them to a scenario involving a day care center. The solution calculates costs for various options, such as laundering clothes, hiring employees, and renting space, to aid in decision-making. The analysis includes revenue and cost comparisons, marginal income analysis, and the preparation of a letter summarizing the findings. The case study demonstrates how cost accounting information can be used to evaluate investment choices, optimize operational efficiency, and make informed business decisions. The solution highlights the importance of considering both quantitative and qualitative factors in the decision-making process.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGERIAL ACCOUNTING

Table of Contents

Part A:........................................................................................................................................2

Sub part1:...............................................................................................................................2

Sub part 2:..............................................................................................................................3

Sub part 3:..............................................................................................................................4

Sub part 4:..............................................................................................................................5

Sub part 5:..............................................................................................................................5

References and bibliography:.....................................................................................................9

Table of Contents

Part A:........................................................................................................................................2

Sub part1:...............................................................................................................................2

Sub part 2:..............................................................................................................................3

Sub part 3:..............................................................................................................................4

Sub part 4:..............................................................................................................................5

Sub part 5:..............................................................................................................................5

References and bibliography:.....................................................................................................9

2MANAGERIAL ACCOUNTING

Part A:

Sub part1:

Cost represents the resources that have been or must be sacrificed to attain a particular

objective. On behalf of behaviour, nature, function and also decisions cost are categories in

many types. Depend on its behaviour cost are classified as Fixed costs, Variable costs, and

Semi variable or Semi fixed costs. Fixed cost is the cost which does not vary with the change

in the volume of activity in the short run; these are not affected by temporary fluctuation in

activity of an enterprise. These are also known as period costs. Whereas the Variable cost is a

cost that tends to vary in direct proportion accordance with level of activity within the

relevant range and within a given period of time. It increases or decreases in the same rate

with increase or decrease in the output. There is a linear relationship between volume and

variable cost. On the other hand, Semi variable or semi fixed costs are such type of a cost

these are neither perfectly variable nor absolutely fixed in relation to change in volume. They

change in the same direction as volume, but not in direct proportion thereto. (Alegre

Sengupta and Lapiedra 2013).

In the given case study, various costs components have been used, such as annual

license fees, annual insurance, these are the examples of fixed costs; remain constant in total

regardless of change in volume up to a certain level of output, they are not affected by change

in the volume of production. Cost of meals and snacks are the example of variable costs,

which depends on the number of child and number of days consisting a linear relationship

between volume and variable cost, the laundry costs are an example of semi variable cost,

where a significant part of the cost is fixed and the rest part varies with the pickup millage

and usage of the laundry facility.

Part A:

Sub part1:

Cost represents the resources that have been or must be sacrificed to attain a particular

objective. On behalf of behaviour, nature, function and also decisions cost are categories in

many types. Depend on its behaviour cost are classified as Fixed costs, Variable costs, and

Semi variable or Semi fixed costs. Fixed cost is the cost which does not vary with the change

in the volume of activity in the short run; these are not affected by temporary fluctuation in

activity of an enterprise. These are also known as period costs. Whereas the Variable cost is a

cost that tends to vary in direct proportion accordance with level of activity within the

relevant range and within a given period of time. It increases or decreases in the same rate

with increase or decrease in the output. There is a linear relationship between volume and

variable cost. On the other hand, Semi variable or semi fixed costs are such type of a cost

these are neither perfectly variable nor absolutely fixed in relation to change in volume. They

change in the same direction as volume, but not in direct proportion thereto. (Alegre

Sengupta and Lapiedra 2013).

In the given case study, various costs components have been used, such as annual

license fees, annual insurance, these are the examples of fixed costs; remain constant in total

regardless of change in volume up to a certain level of output, they are not affected by change

in the volume of production. Cost of meals and snacks are the example of variable costs,

which depends on the number of child and number of days consisting a linear relationship

between volume and variable cost, the laundry costs are an example of semi variable cost,

where a significant part of the cost is fixed and the rest part varies with the pickup millage

and usage of the laundry facility.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGERIAL ACCOUNTING

Sub part 2:

One of the branch of accounting which is leads to provides helps in an organisation to

make key managerial decisions are Cost and management accounting. It provide such costs

related information depend on which certain investment and managerial decision can be taken

by top management. In the given case study, the organisation is having a need of laundering

soiled cloths for babies. The organisation was having an old appliance for the laundry but it is

not in working condition now. They need to purchase a new appliance in its place. As an

alternative to this, the organisation can launder cloths from an external laundry shop at some

specified costs. The external laundering cost includes a weekly costs as well as a cost of

transportation which depends on the distance, hence it is an example of semi variable costs.

On the other hand, purchasing the appliances will increase the power cost and the utility costs

(Alegre Sengupta and Lapiedra 2013).

There is a need of pertinent costing information while Purchasing an article or using

of any services that provide by an outside or external service provider. For the practicability

analysis of purchase of appliance information relating to the cost of new appliances,

increased power costs, and increased utility costs are relevant. On the other hand, costs

related to laundering cloths from external parties are also relevant for such as well.

Such information like annual licence fees, annual insurance, costs of meals & snacks,

and rent of house all those are not so pertinent for making a decision in regards whether to

purchase the appliances or not. The benefits arising from such appliances and also the

analysis of such cost which have no impact by the costs of meals, costs of annual licences and

annual insurance costs are provided through such information related to cost of appliances

and life of the appliances.

Sub part 2:

One of the branch of accounting which is leads to provides helps in an organisation to

make key managerial decisions are Cost and management accounting. It provide such costs

related information depend on which certain investment and managerial decision can be taken

by top management. In the given case study, the organisation is having a need of laundering

soiled cloths for babies. The organisation was having an old appliance for the laundry but it is

not in working condition now. They need to purchase a new appliance in its place. As an

alternative to this, the organisation can launder cloths from an external laundry shop at some

specified costs. The external laundering cost includes a weekly costs as well as a cost of

transportation which depends on the distance, hence it is an example of semi variable costs.

On the other hand, purchasing the appliances will increase the power cost and the utility costs

(Alegre Sengupta and Lapiedra 2013).

There is a need of pertinent costing information while Purchasing an article or using

of any services that provide by an outside or external service provider. For the practicability

analysis of purchase of appliance information relating to the cost of new appliances,

increased power costs, and increased utility costs are relevant. On the other hand, costs

related to laundering cloths from external parties are also relevant for such as well.

Such information like annual licence fees, annual insurance, costs of meals & snacks,

and rent of house all those are not so pertinent for making a decision in regards whether to

purchase the appliances or not. The benefits arising from such appliances and also the

analysis of such cost which have no impact by the costs of meals, costs of annual licences and

annual insurance costs are provided through such information related to cost of appliances

and life of the appliances.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGERIAL ACCOUNTING

Sub part 3:

There is a using of two options for the couple in regards launder cloths for their baby

care centre. Option one : they can purchase the appliances and launder cloths using power

and additional utilities, or Option two : they can wash cloths from the external laundering

shop. Annual costs to launder cloths for each of the options can be calculated as follows.

Option A: Laundering clothes by the Red Oak Laundry:

Monthly costs of laundering $ 52.00

Total Annual Cost of Laundering Cloths $ 624.00

Option B: Self Servicing laundering in Red Oak Laundry:

Weekly costs of using laundry facilities $ 8.00

Pickup Costs in a week (3*2*0.56*4.33) $ 14.55

Weekly costs of using facility and pickup $ 22.55

Cost of facility and pickups in a month (22.55*4.33) $ 97.64

Utilities costs in a month (35/3) $ 11.67

Monthly costs of laundering $ 109.30

Annual Cost of Laundering Cloths $ 1,311.64

Option C: Using New Appliances:

Cost of Appliances (420+380+43.72+35) $ 878.72

Total Annual Depreciation (878.72/8) $ 109.84

Total Annual energy costs (120+145) $ 265.00

Total Annual cost of Utilities (35*4) $ 140.00

Total Annual Cost of Laundering Cloths $ 514.84

From the above calculations, it can be analysis that, the cost of laundering in option B

is the highest one where the self servicing facility of Red Oak Laundry is used and in option

C it is at the lowest where the new appliances are purchased and used incurring increased

energy costs and utilities. Therefore, it can entrust for the couple that to go for the purchasing

of the new appliances (Massaand Tucci2013).

Sub part 3:

There is a using of two options for the couple in regards launder cloths for their baby

care centre. Option one : they can purchase the appliances and launder cloths using power

and additional utilities, or Option two : they can wash cloths from the external laundering

shop. Annual costs to launder cloths for each of the options can be calculated as follows.

Option A: Laundering clothes by the Red Oak Laundry:

Monthly costs of laundering $ 52.00

Total Annual Cost of Laundering Cloths $ 624.00

Option B: Self Servicing laundering in Red Oak Laundry:

Weekly costs of using laundry facilities $ 8.00

Pickup Costs in a week (3*2*0.56*4.33) $ 14.55

Weekly costs of using facility and pickup $ 22.55

Cost of facility and pickups in a month (22.55*4.33) $ 97.64

Utilities costs in a month (35/3) $ 11.67

Monthly costs of laundering $ 109.30

Annual Cost of Laundering Cloths $ 1,311.64

Option C: Using New Appliances:

Cost of Appliances (420+380+43.72+35) $ 878.72

Total Annual Depreciation (878.72/8) $ 109.84

Total Annual energy costs (120+145) $ 265.00

Total Annual cost of Utilities (35*4) $ 140.00

Total Annual Cost of Laundering Cloths $ 514.84

From the above calculations, it can be analysis that, the cost of laundering in option B

is the highest one where the self servicing facility of Red Oak Laundry is used and in option

C it is at the lowest where the new appliances are purchased and used incurring increased

energy costs and utilities. Therefore, it can entrust for the couple that to go for the purchasing

of the new appliances (Massaand Tucci2013).

5MANAGERIAL ACCOUNTING

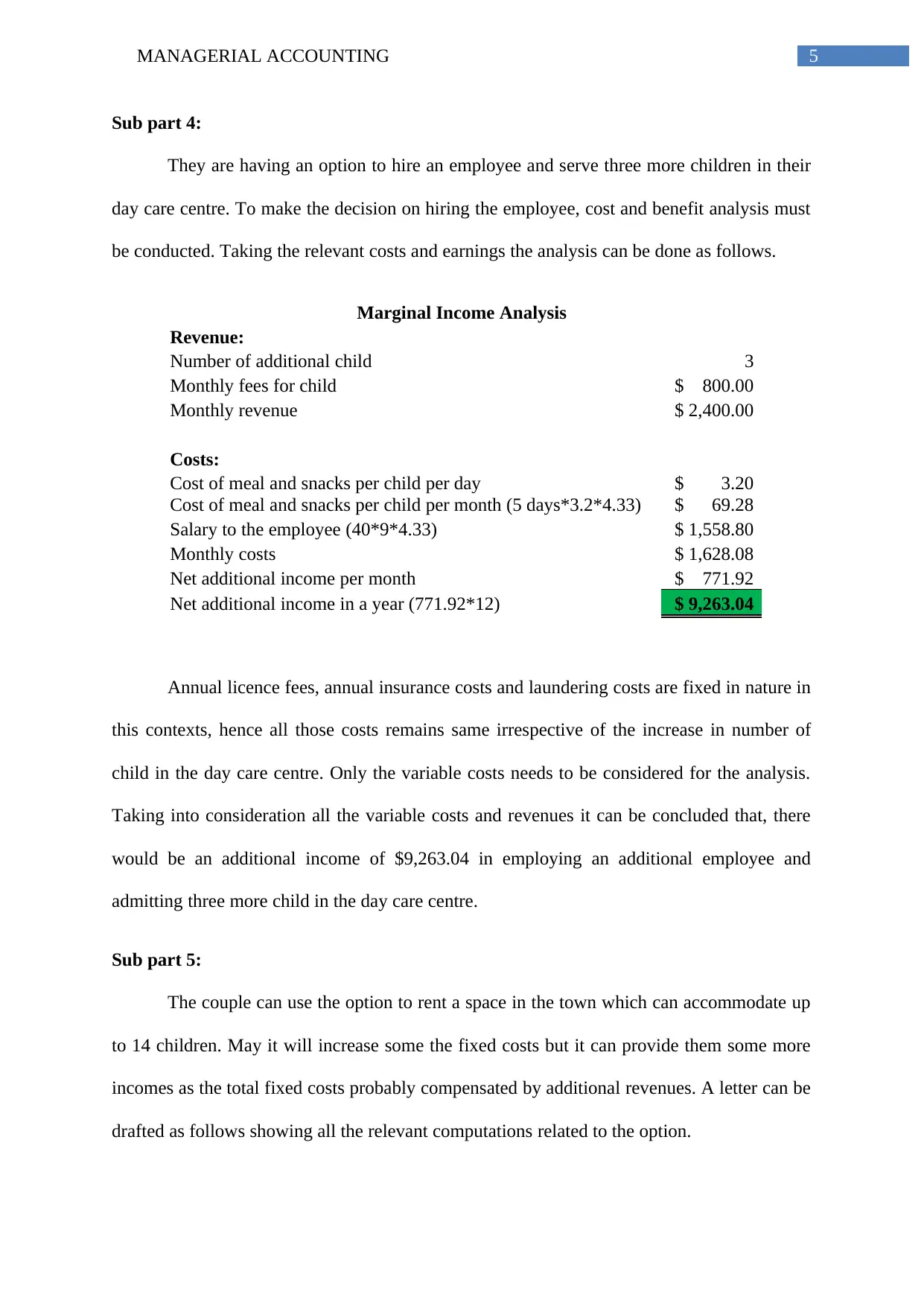

Sub part 4:

They are having an option to hire an employee and serve three more children in their

day care centre. To make the decision on hiring the employee, cost and benefit analysis must

be conducted. Taking the relevant costs and earnings the analysis can be done as follows.

Marginal Income Analysis

Revenue:

Number of additional child 3

Monthly fees for child $ 800.00

Monthly revenue $ 2,400.00

Costs:

Cost of meal and snacks per child per day $ 3.20

Cost of meal and snacks per child per month (5 days*3.2*4.33) $ 69.28

Salary to the employee (40*9*4.33) $ 1,558.80

Monthly costs $ 1,628.08

Net additional income per month $ 771.92

Net additional income in a year (771.92*12) $ 9,263.04

Annual licence fees, annual insurance costs and laundering costs are fixed in nature in

this contexts, hence all those costs remains same irrespective of the increase in number of

child in the day care centre. Only the variable costs needs to be considered for the analysis.

Taking into consideration all the variable costs and revenues it can be concluded that, there

would be an additional income of $9,263.04 in employing an additional employee and

admitting three more child in the day care centre.

Sub part 5:

The couple can use the option to rent a space in the town which can accommodate up

to 14 children. May it will increase some the fixed costs but it can provide them some more

incomes as the total fixed costs probably compensated by additional revenues. A letter can be

drafted as follows showing all the relevant computations related to the option.

Sub part 4:

They are having an option to hire an employee and serve three more children in their

day care centre. To make the decision on hiring the employee, cost and benefit analysis must

be conducted. Taking the relevant costs and earnings the analysis can be done as follows.

Marginal Income Analysis

Revenue:

Number of additional child 3

Monthly fees for child $ 800.00

Monthly revenue $ 2,400.00

Costs:

Cost of meal and snacks per child per day $ 3.20

Cost of meal and snacks per child per month (5 days*3.2*4.33) $ 69.28

Salary to the employee (40*9*4.33) $ 1,558.80

Monthly costs $ 1,628.08

Net additional income per month $ 771.92

Net additional income in a year (771.92*12) $ 9,263.04

Annual licence fees, annual insurance costs and laundering costs are fixed in nature in

this contexts, hence all those costs remains same irrespective of the increase in number of

child in the day care centre. Only the variable costs needs to be considered for the analysis.

Taking into consideration all the variable costs and revenues it can be concluded that, there

would be an additional income of $9,263.04 in employing an additional employee and

admitting three more child in the day care centre.

Sub part 5:

The couple can use the option to rent a space in the town which can accommodate up

to 14 children. May it will increase some the fixed costs but it can provide them some more

incomes as the total fixed costs probably compensated by additional revenues. A letter can be

drafted as follows showing all the relevant computations related to the option.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGERIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL ACCOUNTING

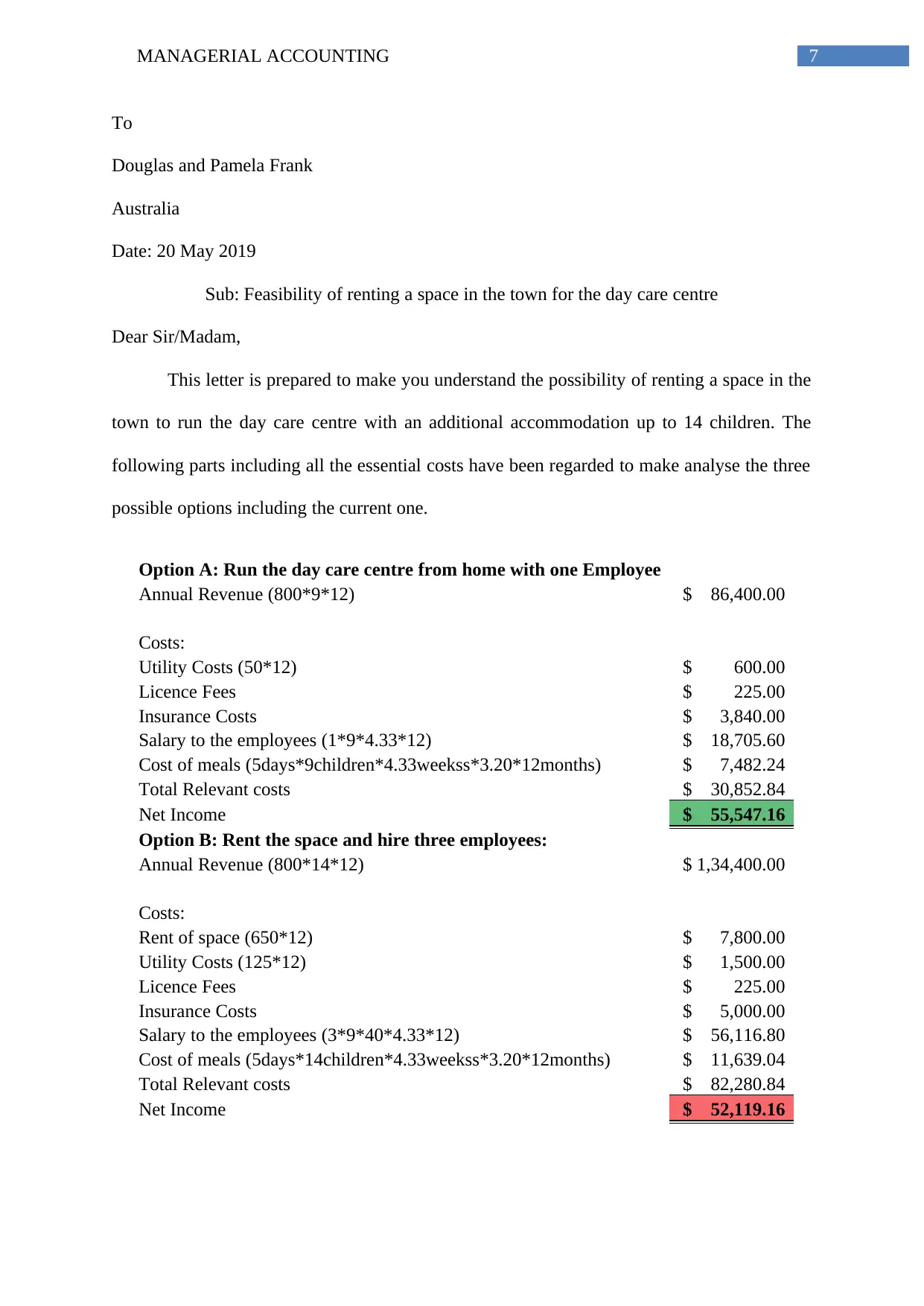

To

Douglas and Pamela Frank

Australia

Date: 20 May 2019

Sub: Feasibility of renting a space in the town for the day care centre

Dear Sir/Madam,

This letter is prepared to make you understand the possibility of renting a space in the

town to run the day care centre with an additional accommodation up to 14 children. The

following parts including all the essential costs have been regarded to make analyse the three

possible options including the current one.

Option A: Run the day care centre from home with one Employee

Annual Revenue (800*9*12) $ 86,400.00

Costs:

Utility Costs (50*12) $ 600.00

Licence Fees $ 225.00

Insurance Costs $ 3,840.00

Salary to the employees (1*9*4.33*12) $ 18,705.60

Cost of meals (5days*9children*4.33weekss*3.20*12months) $ 7,482.24

Total Relevant costs $ 30,852.84

Net Income $ 55,547.16

Option B: Rent the space and hire three employees:

Annual Revenue (800*14*12) $ 1,34,400.00

Costs:

Rent of space (650*12) $ 7,800.00

Utility Costs (125*12) $ 1,500.00

Licence Fees $ 225.00

Insurance Costs $ 5,000.00

Salary to the employees (3*9*40*4.33*12) $ 56,116.80

Cost of meals (5days*14children*4.33weekss*3.20*12months) $ 11,639.04

Total Relevant costs $ 82,280.84

Net Income $ 52,119.16

To

Douglas and Pamela Frank

Australia

Date: 20 May 2019

Sub: Feasibility of renting a space in the town for the day care centre

Dear Sir/Madam,

This letter is prepared to make you understand the possibility of renting a space in the

town to run the day care centre with an additional accommodation up to 14 children. The

following parts including all the essential costs have been regarded to make analyse the three

possible options including the current one.

Option A: Run the day care centre from home with one Employee

Annual Revenue (800*9*12) $ 86,400.00

Costs:

Utility Costs (50*12) $ 600.00

Licence Fees $ 225.00

Insurance Costs $ 3,840.00

Salary to the employees (1*9*4.33*12) $ 18,705.60

Cost of meals (5days*9children*4.33weekss*3.20*12months) $ 7,482.24

Total Relevant costs $ 30,852.84

Net Income $ 55,547.16

Option B: Rent the space and hire three employees:

Annual Revenue (800*14*12) $ 1,34,400.00

Costs:

Rent of space (650*12) $ 7,800.00

Utility Costs (125*12) $ 1,500.00

Licence Fees $ 225.00

Insurance Costs $ 5,000.00

Salary to the employees (3*9*40*4.33*12) $ 56,116.80

Cost of meals (5days*14children*4.33weekss*3.20*12months) $ 11,639.04

Total Relevant costs $ 82,280.84

Net Income $ 52,119.16

8MANAGERIAL ACCOUNTING

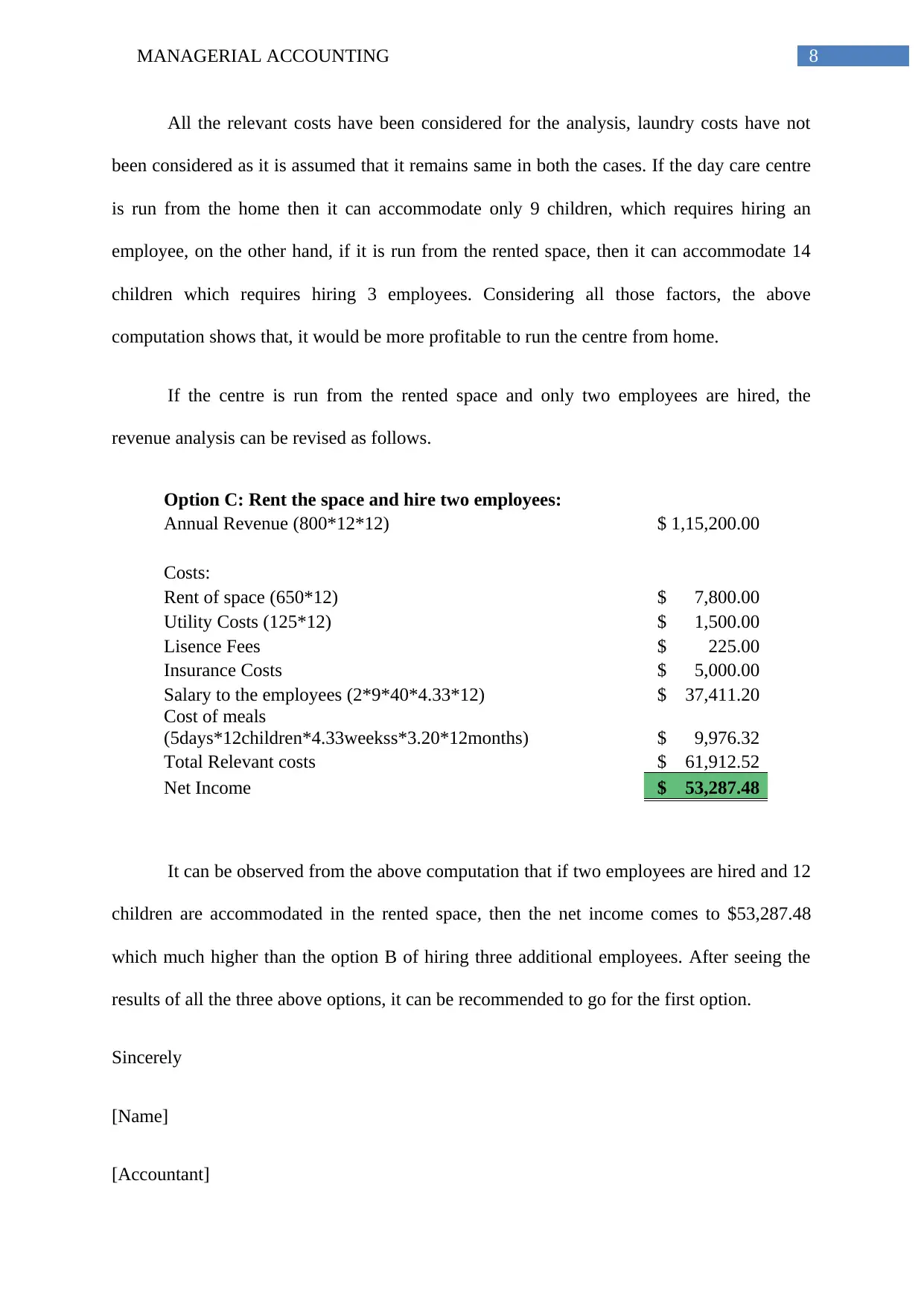

All the relevant costs have been considered for the analysis, laundry costs have not

been considered as it is assumed that it remains same in both the cases. If the day care centre

is run from the home then it can accommodate only 9 children, which requires hiring an

employee, on the other hand, if it is run from the rented space, then it can accommodate 14

children which requires hiring 3 employees. Considering all those factors, the above

computation shows that, it would be more profitable to run the centre from home.

If the centre is run from the rented space and only two employees are hired, the

revenue analysis can be revised as follows.

Option C: Rent the space and hire two employees:

Annual Revenue (800*12*12) $ 1,15,200.00

Costs:

Rent of space (650*12) $ 7,800.00

Utility Costs (125*12) $ 1,500.00

Lisence Fees $ 225.00

Insurance Costs $ 5,000.00

Salary to the employees (2*9*40*4.33*12) $ 37,411.20

Cost of meals

(5days*12children*4.33weekss*3.20*12months) $ 9,976.32

Total Relevant costs $ 61,912.52

Net Income $ 53,287.48

It can be observed from the above computation that if two employees are hired and 12

children are accommodated in the rented space, then the net income comes to $53,287.48

which much higher than the option B of hiring three additional employees. After seeing the

results of all the three above options, it can be recommended to go for the first option.

Sincerely

[Name]

[Accountant]

All the relevant costs have been considered for the analysis, laundry costs have not

been considered as it is assumed that it remains same in both the cases. If the day care centre

is run from the home then it can accommodate only 9 children, which requires hiring an

employee, on the other hand, if it is run from the rented space, then it can accommodate 14

children which requires hiring 3 employees. Considering all those factors, the above

computation shows that, it would be more profitable to run the centre from home.

If the centre is run from the rented space and only two employees are hired, the

revenue analysis can be revised as follows.

Option C: Rent the space and hire two employees:

Annual Revenue (800*12*12) $ 1,15,200.00

Costs:

Rent of space (650*12) $ 7,800.00

Utility Costs (125*12) $ 1,500.00

Lisence Fees $ 225.00

Insurance Costs $ 5,000.00

Salary to the employees (2*9*40*4.33*12) $ 37,411.20

Cost of meals

(5days*12children*4.33weekss*3.20*12months) $ 9,976.32

Total Relevant costs $ 61,912.52

Net Income $ 53,287.48

It can be observed from the above computation that if two employees are hired and 12

children are accommodated in the rented space, then the net income comes to $53,287.48

which much higher than the option B of hiring three additional employees. After seeing the

results of all the three above options, it can be recommended to go for the first option.

Sincerely

[Name]

[Accountant]

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGERIAL ACCOUNTING

References and bibliography:

Alegre, J., Sengupta, K. and Lapiedra, R., 2013. Knowledge management and innovation

performance in a high-tech SMEs industry. International Small Business Journal, 31(4),

pp.454-470.

Alexander, K., 2013. Facilities management: theory and practice. Routledge.

Bratton, J. and Gold, J., 2017. Human resource management: theory and practice. Palgrave.

Dalkir, K., 2013. Knowledge management in theory and practice. Routledge.

Evertson, C.M. and Weinstein, C.S. eds., 2013. Handbook of classroom management:

Research, practice, and contemporary issues. Routledge.

Galliers, R.D. and Leidner, D.E., 2014. Strategic information management: challenges and

strategies in managing information systems. Routledge.

Greenberg, J.S., 2017. Comprehensive stress management. McGraw-Hill Education.

Heding, T., Knudtzen, C.F. and Bjerre, M., 2015. Brand management: Research, theory and

practice. Routledge.

Innovation, C., 2019. Information, Process, Management.

Jarle Gressgård, L., Amundsen, O., Merethe Aasen, T. and Hansen, K., 2014. Use of

information and communication technology to support employee-driven innovation in

organizations: a knowledge management perspective. Journal of Knowledge

Management, 18(4), pp.633-650.

Krajewski, L.J., Ritzman, L.P. and Malhotra, M.K., 2013. Operations management. Pearson,.

References and bibliography:

Alegre, J., Sengupta, K. and Lapiedra, R., 2013. Knowledge management and innovation

performance in a high-tech SMEs industry. International Small Business Journal, 31(4),

pp.454-470.

Alexander, K., 2013. Facilities management: theory and practice. Routledge.

Bratton, J. and Gold, J., 2017. Human resource management: theory and practice. Palgrave.

Dalkir, K., 2013. Knowledge management in theory and practice. Routledge.

Evertson, C.M. and Weinstein, C.S. eds., 2013. Handbook of classroom management:

Research, practice, and contemporary issues. Routledge.

Galliers, R.D. and Leidner, D.E., 2014. Strategic information management: challenges and

strategies in managing information systems. Routledge.

Greenberg, J.S., 2017. Comprehensive stress management. McGraw-Hill Education.

Heding, T., Knudtzen, C.F. and Bjerre, M., 2015. Brand management: Research, theory and

practice. Routledge.

Innovation, C., 2019. Information, Process, Management.

Jarle Gressgård, L., Amundsen, O., Merethe Aasen, T. and Hansen, K., 2014. Use of

information and communication technology to support employee-driven innovation in

organizations: a knowledge management perspective. Journal of Knowledge

Management, 18(4), pp.633-650.

Krajewski, L.J., Ritzman, L.P. and Malhotra, M.K., 2013. Operations management. Pearson,.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGERIAL ACCOUNTING

Laudon, K.C. and Laudon, J.P., 2015. Management Information Systems: Managing the

Digital Firm Plus MyMISLab with Pearson eText--Access Card Package. Prentice Hall Press.

Laudon, K.C. and Laudon, J.P., 2016. Management information system. Pearson Education

India.

Laudon, K.C. and Laudon, J.P., 2016. Management information system. Pearson Education

India.

Majchrzak, A. and Malhotra, A., 2013. Towards an information systems perspective and

research agenda on crowdsourcing for innovation. The Journal of Strategic Information

Systems, 22(4), pp.257-268.

Massa, L. and Tucci, C.L., 2013. Business model innovation. The Oxford handbook of

innovation management, 20(18), pp.420-441.

Laudon, K.C. and Laudon, J.P., 2015. Management Information Systems: Managing the

Digital Firm Plus MyMISLab with Pearson eText--Access Card Package. Prentice Hall Press.

Laudon, K.C. and Laudon, J.P., 2016. Management information system. Pearson Education

India.

Laudon, K.C. and Laudon, J.P., 2016. Management information system. Pearson Education

India.

Majchrzak, A. and Malhotra, A., 2013. Towards an information systems perspective and

research agenda on crowdsourcing for innovation. The Journal of Strategic Information

Systems, 22(4), pp.257-268.

Massa, L. and Tucci, C.L., 2013. Business model innovation. The Oxford handbook of

innovation management, 20(18), pp.420-441.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.