TDABC Costing for Woolworths Ltd.

VerifiedAdded on 2020/06/05

|11

|2498

|215

AI Summary

This assignment examines the application of Time-Driven Activity-Based Costing (TDABC) for Woolworths Ltd., highlighting its advantages in managing resources and transactions efficiently. It explores how TDABC can help Woolworths forecast demand, prepare budgets, and improve overall cost control. The analysis emphasizes the practical benefits of TDABC for a company with limited resources.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Managerial Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK ..............................................................................................................................................1

1. Description of Woolworths Limited.......................................................................................1

2.Time driven activity based costing and its features................................................................2

3. Difference between Time driven activity based costing and traditional costing systems.......3

4.Suitability of TDABC for Woolworth s Ltd............................................................................5

CONCLUSION................................................................................................................................6

.........................................................................................................................................................6

REFERENCES................................................................................................................................7

.........................................................................................................................................................8

INTRODUCTION...........................................................................................................................1

TASK ..............................................................................................................................................1

1. Description of Woolworths Limited.......................................................................................1

2.Time driven activity based costing and its features................................................................2

3. Difference between Time driven activity based costing and traditional costing systems.......3

4.Suitability of TDABC for Woolworth s Ltd............................................................................5

CONCLUSION................................................................................................................................6

.........................................................................................................................................................6

REFERENCES................................................................................................................................7

.........................................................................................................................................................8

INTRODUCTION

Time-driven activity-based costing is the revised model which is used by the organisation

to estimate the requirement of resources in completion of each task or product. TDABC is the

simple model which is easy to implement requires less resources in comparison to other costing

models. This model is easily update the changes which are happen in processes, order variety

and cost of resources. TDABS has large number of importance which helps in handling of large

number of transactions and contributes in real time reporting. Woolworths limited is an

Australian company which provides their products and services in Australia and New Zealand.

This company deals in the diversifies products which includes Food, Petrol, Liquor, Home

improvement, General merchandise etc. The bakery indulge in producing organic whole grain

breads and bagels (Anderson and Sollenberger, 2011).

In the present report explain about, Time-driven activity-based costing and its features,

Difference between Time-driven activity-based costing, Activity-based costing and traditional

costing system.

TASK

1. Description of Woolworths Limited

Woolworths Limited is the Australian company which deals in diversified products. This

organisation has large retail interest in Australia and New Zealand. The major areas in which the

company provides their services are Australia, New Zealand and India. The diversified products

which are provide by company in different country includes Food, petrol, liquor, general

merchandise, home improvement, hotels and gambling etc. The large number of employees

around 202000 are working to mange the different function in all over the world. It terms of

revenue Woolworth s Limited is the second largest company in Australia. This organisation is

recognised as the largest retailer of liquor in Australia. This company has large number of

supermarket chains to provide their different products and services in Australia and New

Zealand. This organisation also has hotels and pubs in Australia. In 2016, the profit which is

earned by company from their different business activities is $ 1.2 billion dollar. The main aim

of management is to adopt such costing model which is effective to manage the different

activities and accomplish their targets in stipulated time. For this purpose, they are advised to

adopt Time driven activity based costing system which is the revised model of traditional costing

1

Time-driven activity-based costing is the revised model which is used by the organisation

to estimate the requirement of resources in completion of each task or product. TDABC is the

simple model which is easy to implement requires less resources in comparison to other costing

models. This model is easily update the changes which are happen in processes, order variety

and cost of resources. TDABS has large number of importance which helps in handling of large

number of transactions and contributes in real time reporting. Woolworths limited is an

Australian company which provides their products and services in Australia and New Zealand.

This company deals in the diversifies products which includes Food, Petrol, Liquor, Home

improvement, General merchandise etc. The bakery indulge in producing organic whole grain

breads and bagels (Anderson and Sollenberger, 2011).

In the present report explain about, Time-driven activity-based costing and its features,

Difference between Time-driven activity-based costing, Activity-based costing and traditional

costing system.

TASK

1. Description of Woolworths Limited

Woolworths Limited is the Australian company which deals in diversified products. This

organisation has large retail interest in Australia and New Zealand. The major areas in which the

company provides their services are Australia, New Zealand and India. The diversified products

which are provide by company in different country includes Food, petrol, liquor, general

merchandise, home improvement, hotels and gambling etc. The large number of employees

around 202000 are working to mange the different function in all over the world. It terms of

revenue Woolworth s Limited is the second largest company in Australia. This organisation is

recognised as the largest retailer of liquor in Australia. This company has large number of

supermarket chains to provide their different products and services in Australia and New

Zealand. This organisation also has hotels and pubs in Australia. In 2016, the profit which is

earned by company from their different business activities is $ 1.2 billion dollar. The main aim

of management is to adopt such costing model which is effective to manage the different

activities and accomplish their targets in stipulated time. For this purpose, they are advised to

adopt Time driven activity based costing system which is the revised model of traditional costing

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

system. This model has large number of importance for the manager of company to effectively

allocate the resources to complete their tasks on time. It is very easy model to implement in

organisation as comparison to traditional costing systems.

2.Time driven activity based costing and its features

Activity– based costing is a method in which activities of an organisation are identified

and cost are assigned accordingly the evaluation which is based on allocation of resources to

product and services according to their consumption. In this method the indirect costs are

added to direct costs due to this overloading of indirect cost unnecessary losses are mounting.

So manager these days have abandoned the practice of using ABC , instead they are

implementing by relying on Time Driven activity based costing which has helped managers to

make more flexible cost model to ease out the complication of the model.

According to CIMA(Chartered Institution of Management Accounting ) the TDABC

involves an time driven activity of analysing resource consumption and calculating the cost and

planning future activities (Chenhall and Smith, 2011).

Features of Time Driven Activity Based Costing

Estimation of cost per unit of capacity – Managers estimates the practical capacity of

resource supplies in place of surveying on employees time consumption.

Estimating unit time of activities – after successfully calculating the cost per unit time of

the following resources the role of manager is to allot employee and define the time

needed to complete that activity

calculation of cost-driven rates-they can be easily calculated by multiplying several input

variables once the standard rates are calculated the new policies for new ventures and

business are planned

identification of product and services – identification and elimination of services which

are unprofitable and fetching lower profits or overprices .

Manufacturing – it helps in better planning in manufacturing sectors having effective and

better promotional activities and increasing the sales

financial institution -like the manufacturing industries it also have variety of products

and services in financial sectors which can result in cross-product and cross customer

activities. The personal factors can also be attributed accurately

lean accounting – the time driven activity based can be successfully performed through

lean accounting practices which helps in easy calculation and planing of accounting,

controls and measure complete costing methods.

Applications of time driven activity based costing

2

allocate the resources to complete their tasks on time. It is very easy model to implement in

organisation as comparison to traditional costing systems.

2.Time driven activity based costing and its features

Activity– based costing is a method in which activities of an organisation are identified

and cost are assigned accordingly the evaluation which is based on allocation of resources to

product and services according to their consumption. In this method the indirect costs are

added to direct costs due to this overloading of indirect cost unnecessary losses are mounting.

So manager these days have abandoned the practice of using ABC , instead they are

implementing by relying on Time Driven activity based costing which has helped managers to

make more flexible cost model to ease out the complication of the model.

According to CIMA(Chartered Institution of Management Accounting ) the TDABC

involves an time driven activity of analysing resource consumption and calculating the cost and

planning future activities (Chenhall and Smith, 2011).

Features of Time Driven Activity Based Costing

Estimation of cost per unit of capacity – Managers estimates the practical capacity of

resource supplies in place of surveying on employees time consumption.

Estimating unit time of activities – after successfully calculating the cost per unit time of

the following resources the role of manager is to allot employee and define the time

needed to complete that activity

calculation of cost-driven rates-they can be easily calculated by multiplying several input

variables once the standard rates are calculated the new policies for new ventures and

business are planned

identification of product and services – identification and elimination of services which

are unprofitable and fetching lower profits or overprices .

Manufacturing – it helps in better planning in manufacturing sectors having effective and

better promotional activities and increasing the sales

financial institution -like the manufacturing industries it also have variety of products

and services in financial sectors which can result in cross-product and cross customer

activities. The personal factors can also be attributed accurately

lean accounting – the time driven activity based can be successfully performed through

lean accounting practices which helps in easy calculation and planing of accounting,

controls and measure complete costing methods.

Applications of time driven activity based costing

2

it is applicable through company costing and financing practices

they helps in full scope and parctical view of accounting practices

they helps in planning and allocating of resources effectively

help in control costs in product level and departmental level

it helps in identifying and eliminating unnecessary cost of product

Reasons for implementing TBABC

easy budget and performance measurement

cost accounting

evaluation and and estimation of budget for implementing new technologies

increase growth rate of company

data and surveys performance are easier to measure as many analysis through analytical

tools can be performed through analytical too

flexibility and accountability gets easier

it is easy to keep pace with management innovation tools like TQM and JIT systems.

Limitations

Treatment of fixed costs as variables sometimes leads to wrong assumption of data

analyse. It is some time very difficult to trace and differentiate between the indirect and direct

costs.

Public sector usage is very low sop people find it very difficult to understand the concept

of time driven activity

3. Difference between Time driven activity based costing and traditional costing systems

There is huge difference between the two models of costing which are Time driven

activity based costing and traditional costing systems. Both these methods are used for the

allocation of indirect cost to the different products. Such allocation of indirect cost helps in

identification of the estimated overhead cost accompanying to production of different products.

In spite of having the same functions, both the costing methods have large number of

differences. First difference which arise while using the both these costing methods is on

accuracy and complexity (Joseph, 2014).

Traditional costing system

It is the costing method which is used by the organisation in allocation of the indirect cost

to products on the basis of their planned overhead rates. It is the simple method to use but doesn't

provide accurate results in comparison to Time driven activity based costing systems. It is the

costing method, in which all overhead costs are treated as single bundle of indirect costs. This

method provides better results only in one condition when direct costs are more than indirect

3

they helps in full scope and parctical view of accounting practices

they helps in planning and allocating of resources effectively

help in control costs in product level and departmental level

it helps in identifying and eliminating unnecessary cost of product

Reasons for implementing TBABC

easy budget and performance measurement

cost accounting

evaluation and and estimation of budget for implementing new technologies

increase growth rate of company

data and surveys performance are easier to measure as many analysis through analytical

tools can be performed through analytical too

flexibility and accountability gets easier

it is easy to keep pace with management innovation tools like TQM and JIT systems.

Limitations

Treatment of fixed costs as variables sometimes leads to wrong assumption of data

analyse. It is some time very difficult to trace and differentiate between the indirect and direct

costs.

Public sector usage is very low sop people find it very difficult to understand the concept

of time driven activity

3. Difference between Time driven activity based costing and traditional costing systems

There is huge difference between the two models of costing which are Time driven

activity based costing and traditional costing systems. Both these methods are used for the

allocation of indirect cost to the different products. Such allocation of indirect cost helps in

identification of the estimated overhead cost accompanying to production of different products.

In spite of having the same functions, both the costing methods have large number of

differences. First difference which arise while using the both these costing methods is on

accuracy and complexity (Joseph, 2014).

Traditional costing system

It is the costing method which is used by the organisation in allocation of the indirect cost

to products on the basis of their planned overhead rates. It is the simple method to use but doesn't

provide accurate results in comparison to Time driven activity based costing systems. It is the

costing method, in which all overhead costs are treated as single bundle of indirect costs. This

method provides better results only in one condition when direct costs are more than indirect

3

cost. There are many steps are involved in the calculation of Traditional costing systems which

are define below:

The first step includes about the calculation of indirect cost while using this method of

costing

Second step includes about the process of approximation regarding indirect cost for

particular period

Third step includes about the determination of cost driver like labour hour, machine hours

etc.

Fourth step includes about approximation of the cost for such particular cost driver

Fifth step includes about, computation of planned overhead rate

Last step includes the process of assigning of overhead to products by using planned

overhead rate which is calculated above (Kaplan, 2011).

Time driven activity based costing system

It is the revised model of Activity based costing system which helps in allocation of the

time and determination of the demand of different resources required by each transaction,

product etc. This system helps the organisation to effectively manage the limited resources. Use

of this method reduces the need of information and approximate only two things which are

mentioned below:

Capacity of resources and their cost

Time required in performance and completion of transactional activities.

The major concepts which are include in the calculation of TDABC are:

To prepare effective time based module regarding one activity which is flexible to use

and applied on other plants and companies of same industry.

It is the easiest model which requires less time and resources to implement in

organisation. Also very easy to finding out the conclusion, for ex. It requires only two

persons and two days in a month to load, compute, report finding etc.

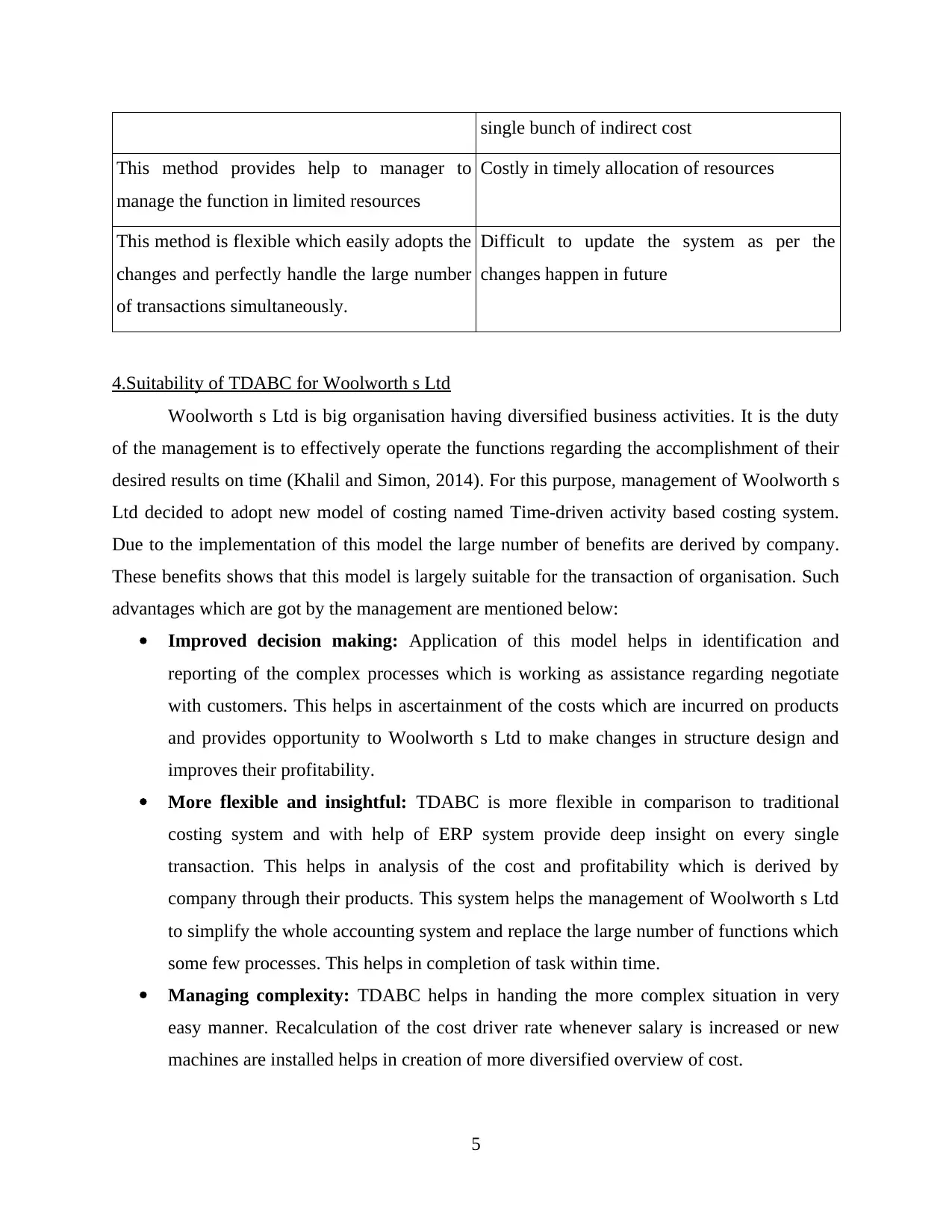

Difference between TDABC and Traditional costing system

Time driven activity based costing system Traditional costing system

It is the revised model which provides accurate

results

This method of does not provide accurate

result s because it assumes overhead cost as

4

are define below:

The first step includes about the calculation of indirect cost while using this method of

costing

Second step includes about the process of approximation regarding indirect cost for

particular period

Third step includes about the determination of cost driver like labour hour, machine hours

etc.

Fourth step includes about approximation of the cost for such particular cost driver

Fifth step includes about, computation of planned overhead rate

Last step includes the process of assigning of overhead to products by using planned

overhead rate which is calculated above (Kaplan, 2011).

Time driven activity based costing system

It is the revised model of Activity based costing system which helps in allocation of the

time and determination of the demand of different resources required by each transaction,

product etc. This system helps the organisation to effectively manage the limited resources. Use

of this method reduces the need of information and approximate only two things which are

mentioned below:

Capacity of resources and their cost

Time required in performance and completion of transactional activities.

The major concepts which are include in the calculation of TDABC are:

To prepare effective time based module regarding one activity which is flexible to use

and applied on other plants and companies of same industry.

It is the easiest model which requires less time and resources to implement in

organisation. Also very easy to finding out the conclusion, for ex. It requires only two

persons and two days in a month to load, compute, report finding etc.

Difference between TDABC and Traditional costing system

Time driven activity based costing system Traditional costing system

It is the revised model which provides accurate

results

This method of does not provide accurate

result s because it assumes overhead cost as

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

single bunch of indirect cost

This method provides help to manager to

manage the function in limited resources

Costly in timely allocation of resources

This method is flexible which easily adopts the

changes and perfectly handle the large number

of transactions simultaneously.

Difficult to update the system as per the

changes happen in future

4.Suitability of TDABC for Woolworth s Ltd

Woolworth s Ltd is big organisation having diversified business activities. It is the duty

of the management is to effectively operate the functions regarding the accomplishment of their

desired results on time (Khalil and Simon, 2014). For this purpose, management of Woolworth s

Ltd decided to adopt new model of costing named Time-driven activity based costing system.

Due to the implementation of this model the large number of benefits are derived by company.

These benefits shows that this model is largely suitable for the transaction of organisation. Such

advantages which are got by the management are mentioned below:

Improved decision making: Application of this model helps in identification and

reporting of the complex processes which is working as assistance regarding negotiate

with customers. This helps in ascertainment of the costs which are incurred on products

and provides opportunity to Woolworth s Ltd to make changes in structure design and

improves their profitability.

More flexible and insightful: TDABC is more flexible in comparison to traditional

costing system and with help of ERP system provide deep insight on every single

transaction. This helps in analysis of the cost and profitability which is derived by

company through their products. This system helps the management of Woolworth s Ltd

to simplify the whole accounting system and replace the large number of functions which

some few processes. This helps in completion of task within time.

Managing complexity: TDABC helps in handing the more complex situation in very

easy manner. Recalculation of the cost driver rate whenever salary is increased or new

machines are installed helps in creation of more diversified overview of cost.

5

This method provides help to manager to

manage the function in limited resources

Costly in timely allocation of resources

This method is flexible which easily adopts the

changes and perfectly handle the large number

of transactions simultaneously.

Difficult to update the system as per the

changes happen in future

4.Suitability of TDABC for Woolworth s Ltd

Woolworth s Ltd is big organisation having diversified business activities. It is the duty

of the management is to effectively operate the functions regarding the accomplishment of their

desired results on time (Khalil and Simon, 2014). For this purpose, management of Woolworth s

Ltd decided to adopt new model of costing named Time-driven activity based costing system.

Due to the implementation of this model the large number of benefits are derived by company.

These benefits shows that this model is largely suitable for the transaction of organisation. Such

advantages which are got by the management are mentioned below:

Improved decision making: Application of this model helps in identification and

reporting of the complex processes which is working as assistance regarding negotiate

with customers. This helps in ascertainment of the costs which are incurred on products

and provides opportunity to Woolworth s Ltd to make changes in structure design and

improves their profitability.

More flexible and insightful: TDABC is more flexible in comparison to traditional

costing system and with help of ERP system provide deep insight on every single

transaction. This helps in analysis of the cost and profitability which is derived by

company through their products. This system helps the management of Woolworth s Ltd

to simplify the whole accounting system and replace the large number of functions which

some few processes. This helps in completion of task within time.

Managing complexity: TDABC helps in handing the more complex situation in very

easy manner. Recalculation of the cost driver rate whenever salary is increased or new

machines are installed helps in creation of more diversified overview of cost.

5

Forecast budget:By the use of this model of costing Woolworth s Ltd are easily forecast

the demand of the resources which are required by different departments in preparation of

the products. This also helps in preparation of the budgets and allocation of the funds.

Flexibility: This model provides the flexibility to the management of Woolworth s Ltd as

they have the option to make the changes in the model whenever the change happen in

activities (Maher, Stickney and Weil, 2012). It is improved the decision making power

and provides lot more time to concentrate on other matter and improve their profitability

by effectively allocation of costs.

CONCLUSION

It has been concluded from the above report that, Time driven activity based costing

system is the effective model which helps in easy budgeting and management of performance,

improve the growth rate of Woolworth s Ltd. makes the accountability more easier and

effectively manage the transactions in limited resources. From the effective features of TDABC,

it is clear that this model of costing is highly suitable for Woolworth s Ltd. This is so because the

large number of benefits are derived by the management like forecast resource demand and

prepare budgets, easy to operate and not much expensive to adopt changes.

6

the demand of the resources which are required by different departments in preparation of

the products. This also helps in preparation of the budgets and allocation of the funds.

Flexibility: This model provides the flexibility to the management of Woolworth s Ltd as

they have the option to make the changes in the model whenever the change happen in

activities (Maher, Stickney and Weil, 2012). It is improved the decision making power

and provides lot more time to concentrate on other matter and improve their profitability

by effectively allocation of costs.

CONCLUSION

It has been concluded from the above report that, Time driven activity based costing

system is the effective model which helps in easy budgeting and management of performance,

improve the growth rate of Woolworth s Ltd. makes the accountability more easier and

effectively manage the transactions in limited resources. From the effective features of TDABC,

it is clear that this model of costing is highly suitable for Woolworth s Ltd. This is so because the

large number of benefits are derived by the management like forecast resource demand and

prepare budgets, easy to operate and not much expensive to adopt changes.

6

REFERENCES

Books and Journals

Anderson, L. K. and Sollenberger, H. M., 2011. Managerial accounting. Cincinnati, Ohio:

College Division, South-Western Pub. Co..

Chenhall, R. H. and Smith, D., 2011. A review of Australian management accounting research:

1980–2009. Accounting & Finance, 51(1). pp.173-206.

Joseph, M., 2014. Debt to Society: Accounting for Life under. University of Minnesota Press.

Kaplan, R. S., 2011. Accounting scholarship that advances professional knowledge and practice.

The Accounting Review, 86(2). pp.367-383.

Khalil, M. and Simon, J., 2014. Efficient contracting, earnings smoothing and managerial

accounting discretion. Journal of Applied Accounting Research, 15(1). pp.100-123.

Maher, M. W., Stickney, C. P. and Weil, R. L., 2012. Managerial accounting: An introduction

to concepts, methods and uses. Cengage Learning.

Park, K. and Jang, S., 2014. Hospitality finance and managerial accounting research: Suggesting

an interdisciplinary research agenda. International Journal of Contemporary Hospitality

Management, 26(5).pp.751-777.

Russo, C. J., Mertins, L. and Ray, M., 2013. Psychological type and academic performance in

the managerial accounting course. Journal of Education for Business, 88(4). pp.210-

215.

Songini, L., Gnan, L. and Malmi, T., 2013. The role and impact of accounting in family

business. Journal of Family Business Strategy, 4(2). pp.71-83.

Wall, F. and Greiling, D., 2011. Accounting information for managerial decision-making in

shareholder management versus stakeholder management. Review of Managerial

Science, 5(2-3), pp.91-135.

Online:

The Advantages and Disadvantages of Budgeting. 2017.[Online]. Available

through:<http://www.bifa.org/library/freight-management/finance/budgeting/the-

advantages-and-disadvantages-of-budgeting> .

7

Books and Journals

Anderson, L. K. and Sollenberger, H. M., 2011. Managerial accounting. Cincinnati, Ohio:

College Division, South-Western Pub. Co..

Chenhall, R. H. and Smith, D., 2011. A review of Australian management accounting research:

1980–2009. Accounting & Finance, 51(1). pp.173-206.

Joseph, M., 2014. Debt to Society: Accounting for Life under. University of Minnesota Press.

Kaplan, R. S., 2011. Accounting scholarship that advances professional knowledge and practice.

The Accounting Review, 86(2). pp.367-383.

Khalil, M. and Simon, J., 2014. Efficient contracting, earnings smoothing and managerial

accounting discretion. Journal of Applied Accounting Research, 15(1). pp.100-123.

Maher, M. W., Stickney, C. P. and Weil, R. L., 2012. Managerial accounting: An introduction

to concepts, methods and uses. Cengage Learning.

Park, K. and Jang, S., 2014. Hospitality finance and managerial accounting research: Suggesting

an interdisciplinary research agenda. International Journal of Contemporary Hospitality

Management, 26(5).pp.751-777.

Russo, C. J., Mertins, L. and Ray, M., 2013. Psychological type and academic performance in

the managerial accounting course. Journal of Education for Business, 88(4). pp.210-

215.

Songini, L., Gnan, L. and Malmi, T., 2013. The role and impact of accounting in family

business. Journal of Family Business Strategy, 4(2). pp.71-83.

Wall, F. and Greiling, D., 2011. Accounting information for managerial decision-making in

shareholder management versus stakeholder management. Review of Managerial

Science, 5(2-3), pp.91-135.

Online:

The Advantages and Disadvantages of Budgeting. 2017.[Online]. Available

through:<http://www.bifa.org/library/freight-management/finance/budgeting/the-

advantages-and-disadvantages-of-budgeting> .

7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

8

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.