Complete Solution: Managerial Accounting and Finance Assignment

VerifiedAdded on 2023/06/07

|9

|1634

|185

Homework Assignment

AI Summary

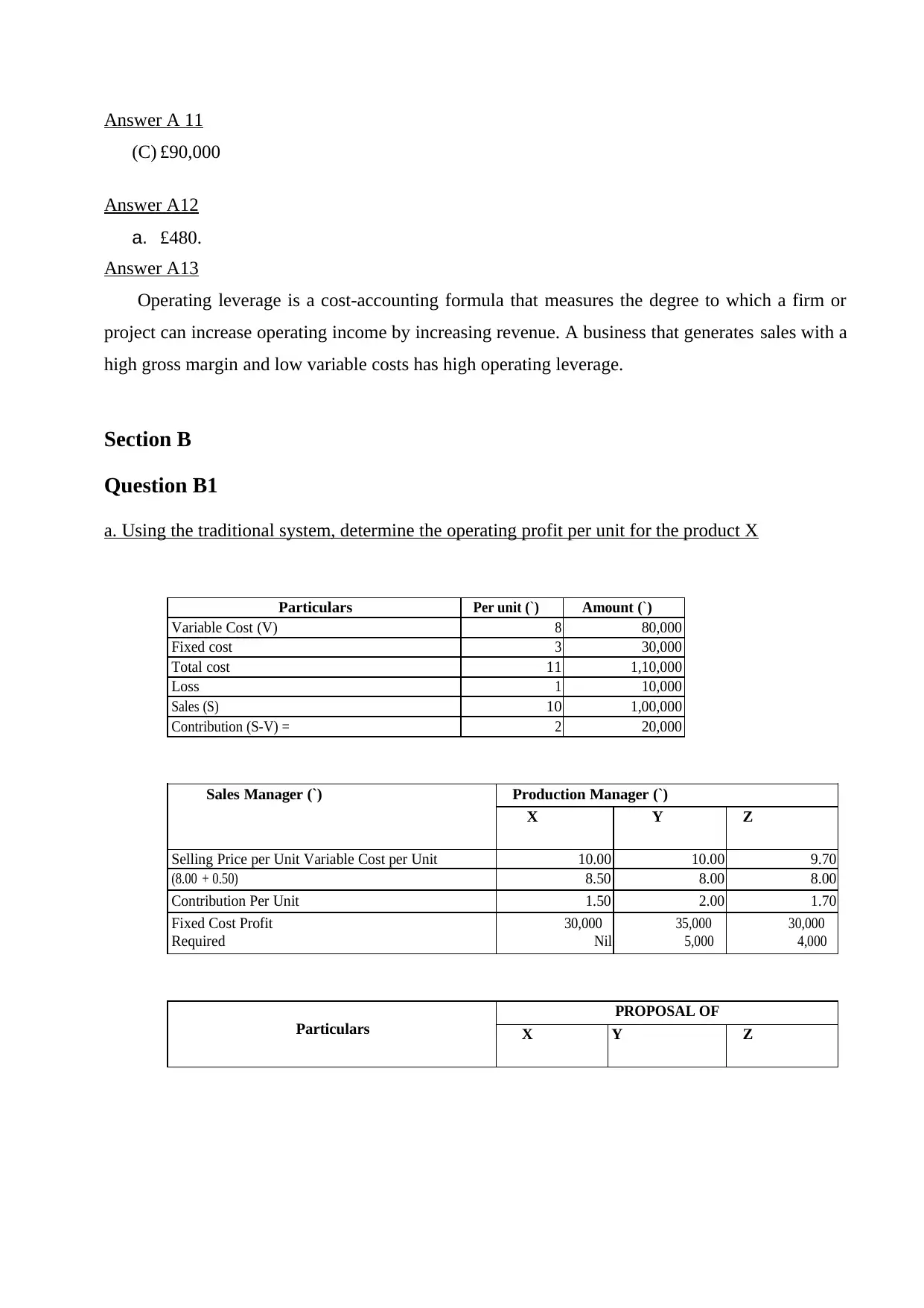

This document presents a comprehensive solution to a Managerial Accounting and Finance assignment, covering key areas such as cost accounting, budgeting, and investment appraisal. The solution includes answers to multiple-choice questions related to fundamental concepts like cost behavior and financial statement analysis. Additionally, it addresses practical problems involving activity-based costing (ABC), comparing it with traditional absorption costing methods. Furthermore, the assignment delves into investment decision-making, calculating payback periods and net present values (NPV) for different projects, ultimately recommending the most financially beneficial option based on these analyses. The document also discusses the advantages and disadvantages of using NPV and internal rate of return (IRR) methods for project evaluation, providing a well-rounded overview of essential managerial accounting and finance principles. Desklib provides a platform for students to access similar solved assignments and past papers for effective learning.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.