Managerial Accounting: Financial Analysis & Floppy Disc Inc. Report

VerifiedAdded on 2023/06/08

|11

|1403

|496

Report

AI Summary

This document presents a detailed solution to a managerial accounting assignment, encompassing several key areas of financial analysis. It includes an income statement for Floppy Disc Inc., segmented by product lines (DVD and Blu-Ray), utilizing a contribution format to assess profitability. The a...

Running Head: Managerial Accounting

Financial Analysis

Financial Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Accounting 1

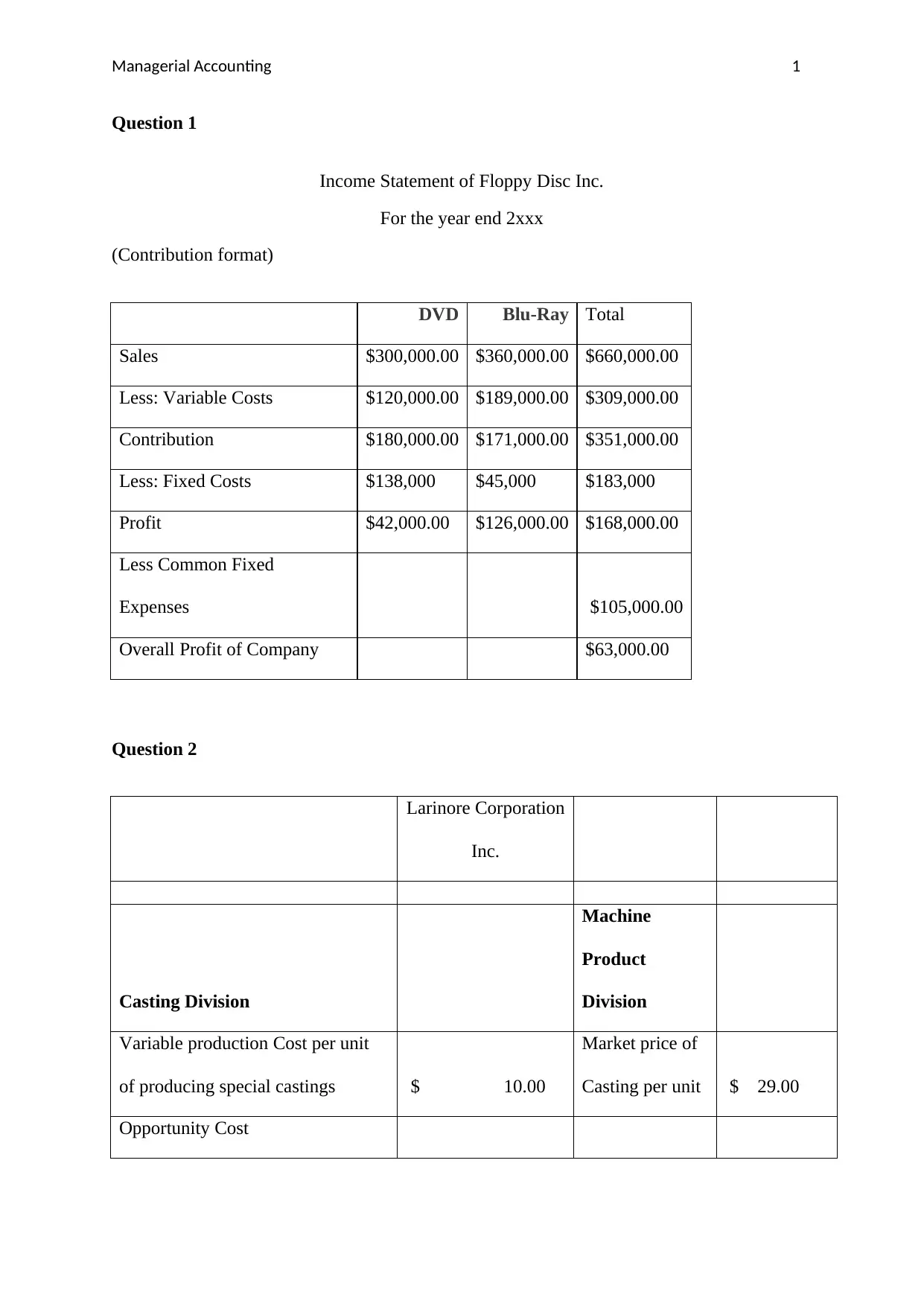

Question 1

Income Statement of Floppy Disc Inc.

For the year end 2xxx

(Contribution format)

DVD Blu-Ray Total

Sales $300,000.00 $360,000.00 $660,000.00

Less: Variable Costs $120,000.00 $189,000.00 $309,000.00

Contribution $180,000.00 $171,000.00 $351,000.00

Less: Fixed Costs $138,000 $45,000 $183,000

Profit $42,000.00 $126,000.00 $168,000.00

Less Common Fixed

Expenses $105,000.00

Overall Profit of Company $63,000.00

Question 2

Larinore Corporation

Inc.

Casting Division

Machine

Product

Division

Variable production Cost per unit

of producing special castings $ 10.00

Market price of

Casting per unit $ 29.00

Opportunity Cost

Question 1

Income Statement of Floppy Disc Inc.

For the year end 2xxx

(Contribution format)

DVD Blu-Ray Total

Sales $300,000.00 $360,000.00 $660,000.00

Less: Variable Costs $120,000.00 $189,000.00 $309,000.00

Contribution $180,000.00 $171,000.00 $351,000.00

Less: Fixed Costs $138,000 $45,000 $183,000

Profit $42,000.00 $126,000.00 $168,000.00

Less Common Fixed

Expenses $105,000.00

Overall Profit of Company $63,000.00

Question 2

Larinore Corporation

Inc.

Casting Division

Machine

Product

Division

Variable production Cost per unit

of producing special castings $ 10.00

Market price of

Casting per unit $ 29.00

Opportunity Cost

Managerial Accounting 2

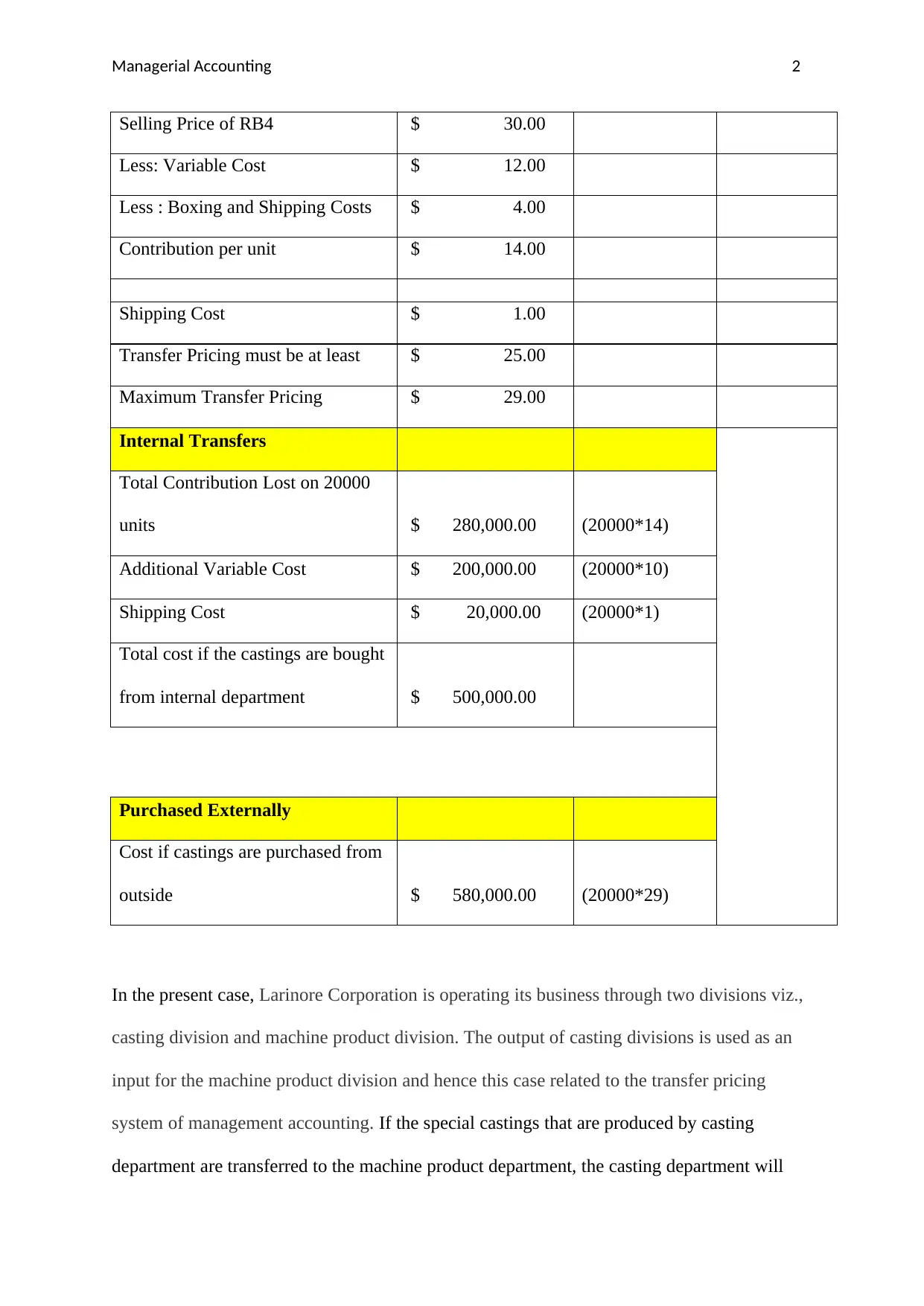

Selling Price of RB4 $ 30.00

Less: Variable Cost $ 12.00

Less : Boxing and Shipping Costs $ 4.00

Contribution per unit $ 14.00

Shipping Cost $ 1.00

Transfer Pricing must be at least $ 25.00

Maximum Transfer Pricing $ 29.00

Internal Transfers

Total Contribution Lost on 20000

units $ 280,000.00 (20000*14)

Additional Variable Cost $ 200,000.00 (20000*10)

Shipping Cost $ 20,000.00 (20000*1)

Total cost if the castings are bought

from internal department $ 500,000.00

Purchased Externally

Cost if castings are purchased from

outside $ 580,000.00 (20000*29)

In the present case, Larinore Corporation is operating its business through two divisions viz.,

casting division and machine product division. The output of casting divisions is used as an

input for the machine product division and hence this case related to the transfer pricing

system of management accounting. If the special castings that are produced by casting

department are transferred to the machine product department, the casting department will

Selling Price of RB4 $ 30.00

Less: Variable Cost $ 12.00

Less : Boxing and Shipping Costs $ 4.00

Contribution per unit $ 14.00

Shipping Cost $ 1.00

Transfer Pricing must be at least $ 25.00

Maximum Transfer Pricing $ 29.00

Internal Transfers

Total Contribution Lost on 20000

units $ 280,000.00 (20000*14)

Additional Variable Cost $ 200,000.00 (20000*10)

Shipping Cost $ 20,000.00 (20000*1)

Total cost if the castings are bought

from internal department $ 500,000.00

Purchased Externally

Cost if castings are purchased from

outside $ 580,000.00 (20000*29)

In the present case, Larinore Corporation is operating its business through two divisions viz.,

casting division and machine product division. The output of casting divisions is used as an

input for the machine product division and hence this case related to the transfer pricing

system of management accounting. If the special castings that are produced by casting

department are transferred to the machine product department, the casting department will

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managerial Accounting 3

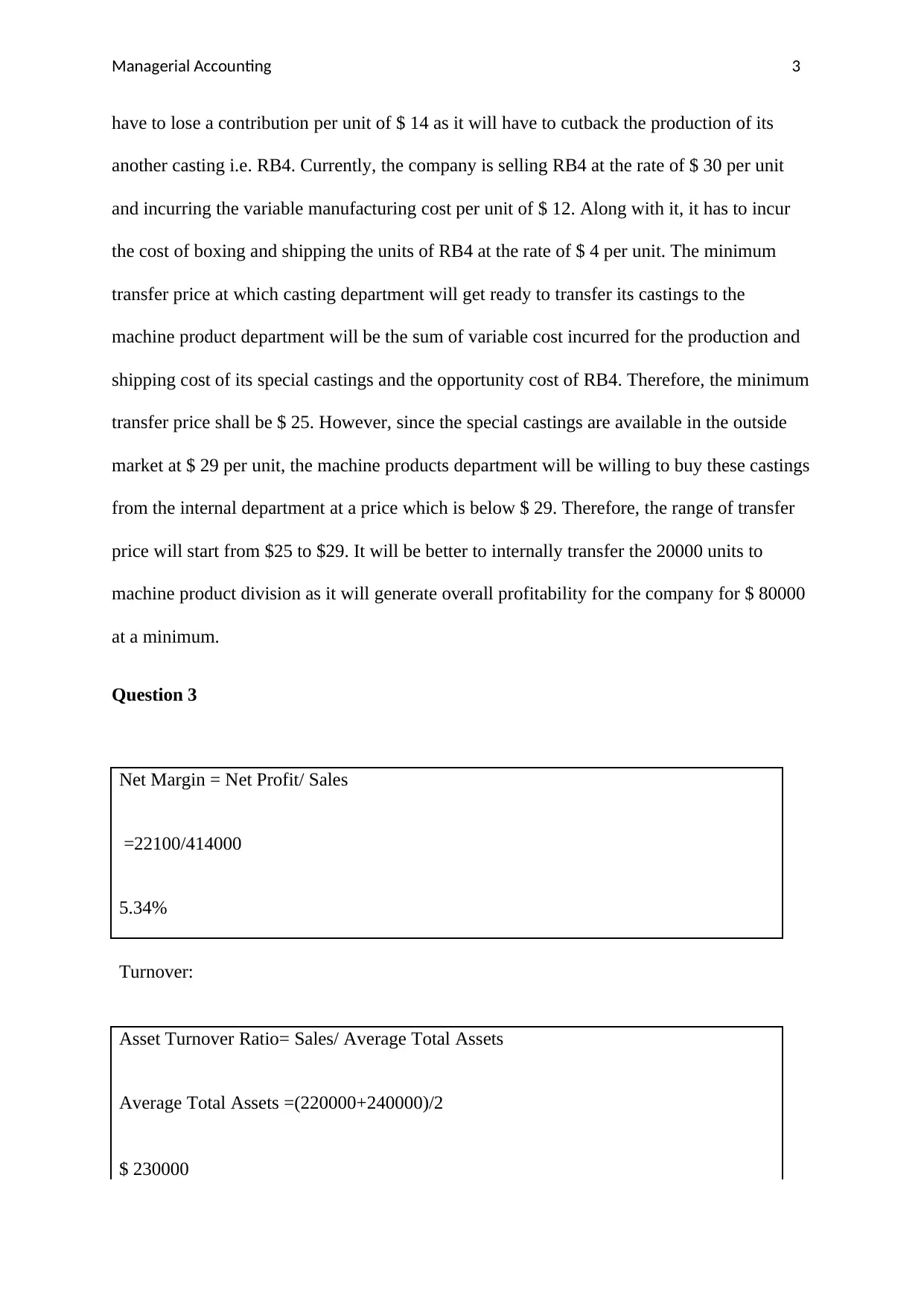

have to lose a contribution per unit of $ 14 as it will have to cutback the production of its

another casting i.e. RB4. Currently, the company is selling RB4 at the rate of $ 30 per unit

and incurring the variable manufacturing cost per unit of $ 12. Along with it, it has to incur

the cost of boxing and shipping the units of RB4 at the rate of $ 4 per unit. The minimum

transfer price at which casting department will get ready to transfer its castings to the

machine product department will be the sum of variable cost incurred for the production and

shipping cost of its special castings and the opportunity cost of RB4. Therefore, the minimum

transfer price shall be $ 25. However, since the special castings are available in the outside

market at $ 29 per unit, the machine products department will be willing to buy these castings

from the internal department at a price which is below $ 29. Therefore, the range of transfer

price will start from $25 to $29. It will be better to internally transfer the 20000 units to

machine product division as it will generate overall profitability for the company for $ 80000

at a minimum.

Question 3

Net Margin = Net Profit/ Sales

=22100/414000

5.34%

Turnover:

Asset Turnover Ratio= Sales/ Average Total Assets

Average Total Assets =(220000+240000)/2

$ 230000

have to lose a contribution per unit of $ 14 as it will have to cutback the production of its

another casting i.e. RB4. Currently, the company is selling RB4 at the rate of $ 30 per unit

and incurring the variable manufacturing cost per unit of $ 12. Along with it, it has to incur

the cost of boxing and shipping the units of RB4 at the rate of $ 4 per unit. The minimum

transfer price at which casting department will get ready to transfer its castings to the

machine product department will be the sum of variable cost incurred for the production and

shipping cost of its special castings and the opportunity cost of RB4. Therefore, the minimum

transfer price shall be $ 25. However, since the special castings are available in the outside

market at $ 29 per unit, the machine products department will be willing to buy these castings

from the internal department at a price which is below $ 29. Therefore, the range of transfer

price will start from $25 to $29. It will be better to internally transfer the 20000 units to

machine product division as it will generate overall profitability for the company for $ 80000

at a minimum.

Question 3

Net Margin = Net Profit/ Sales

=22100/414000

5.34%

Turnover:

Asset Turnover Ratio= Sales/ Average Total Assets

Average Total Assets =(220000+240000)/2

$ 230000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Accounting 4

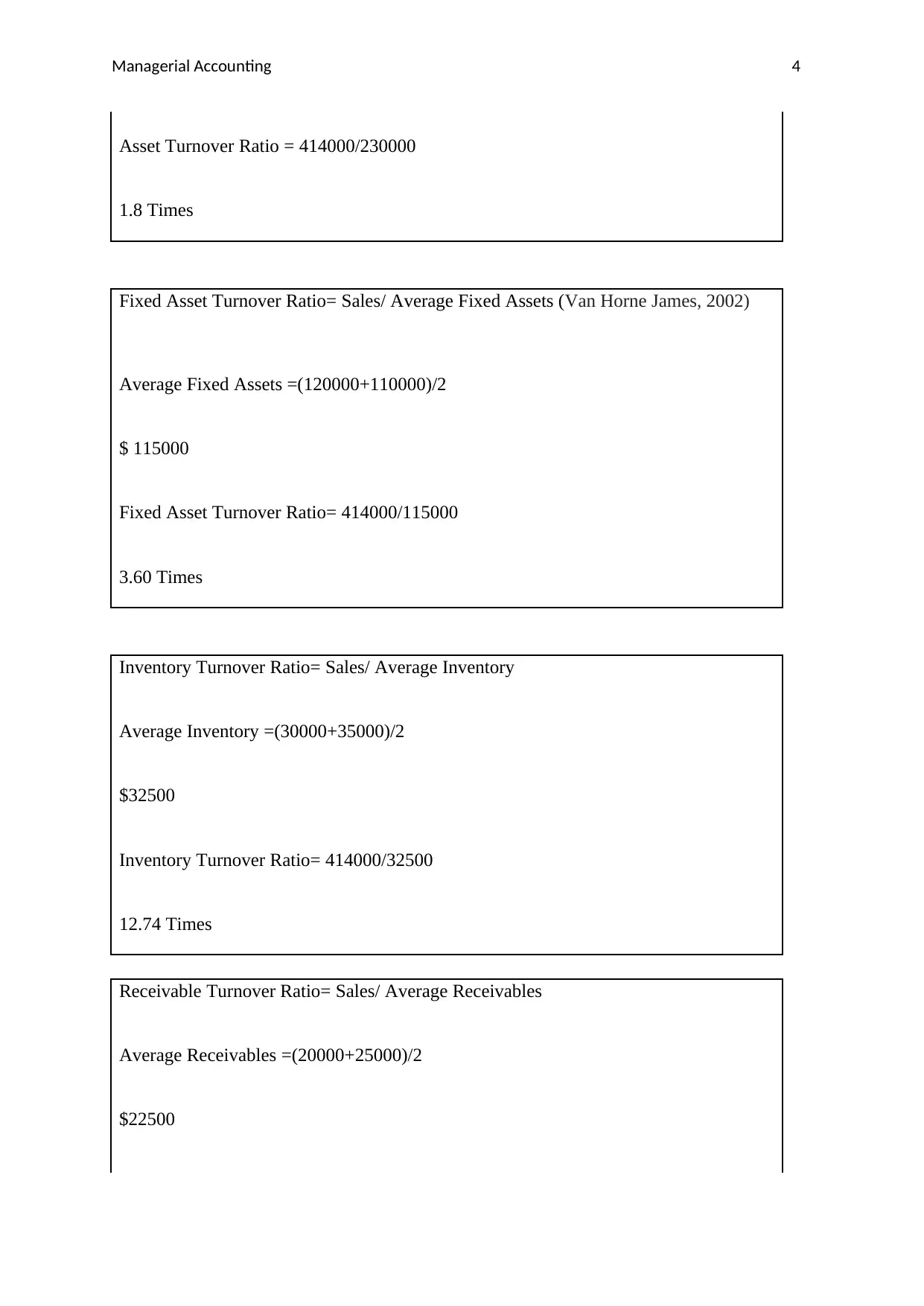

Asset Turnover Ratio = 414000/230000

1.8 Times

Fixed Asset Turnover Ratio= Sales/ Average Fixed Assets (Van Horne James, 2002)

Average Fixed Assets =(120000+110000)/2

$ 115000

Fixed Asset Turnover Ratio= 414000/115000

3.60 Times

Inventory Turnover Ratio= Sales/ Average Inventory

Average Inventory =(30000+35000)/2

$32500

Inventory Turnover Ratio= 414000/32500

12.74 Times

Receivable Turnover Ratio= Sales/ Average Receivables

Average Receivables =(20000+25000)/2

$22500

Asset Turnover Ratio = 414000/230000

1.8 Times

Fixed Asset Turnover Ratio= Sales/ Average Fixed Assets (Van Horne James, 2002)

Average Fixed Assets =(120000+110000)/2

$ 115000

Fixed Asset Turnover Ratio= 414000/115000

3.60 Times

Inventory Turnover Ratio= Sales/ Average Inventory

Average Inventory =(30000+35000)/2

$32500

Inventory Turnover Ratio= 414000/32500

12.74 Times

Receivable Turnover Ratio= Sales/ Average Receivables

Average Receivables =(20000+25000)/2

$22500

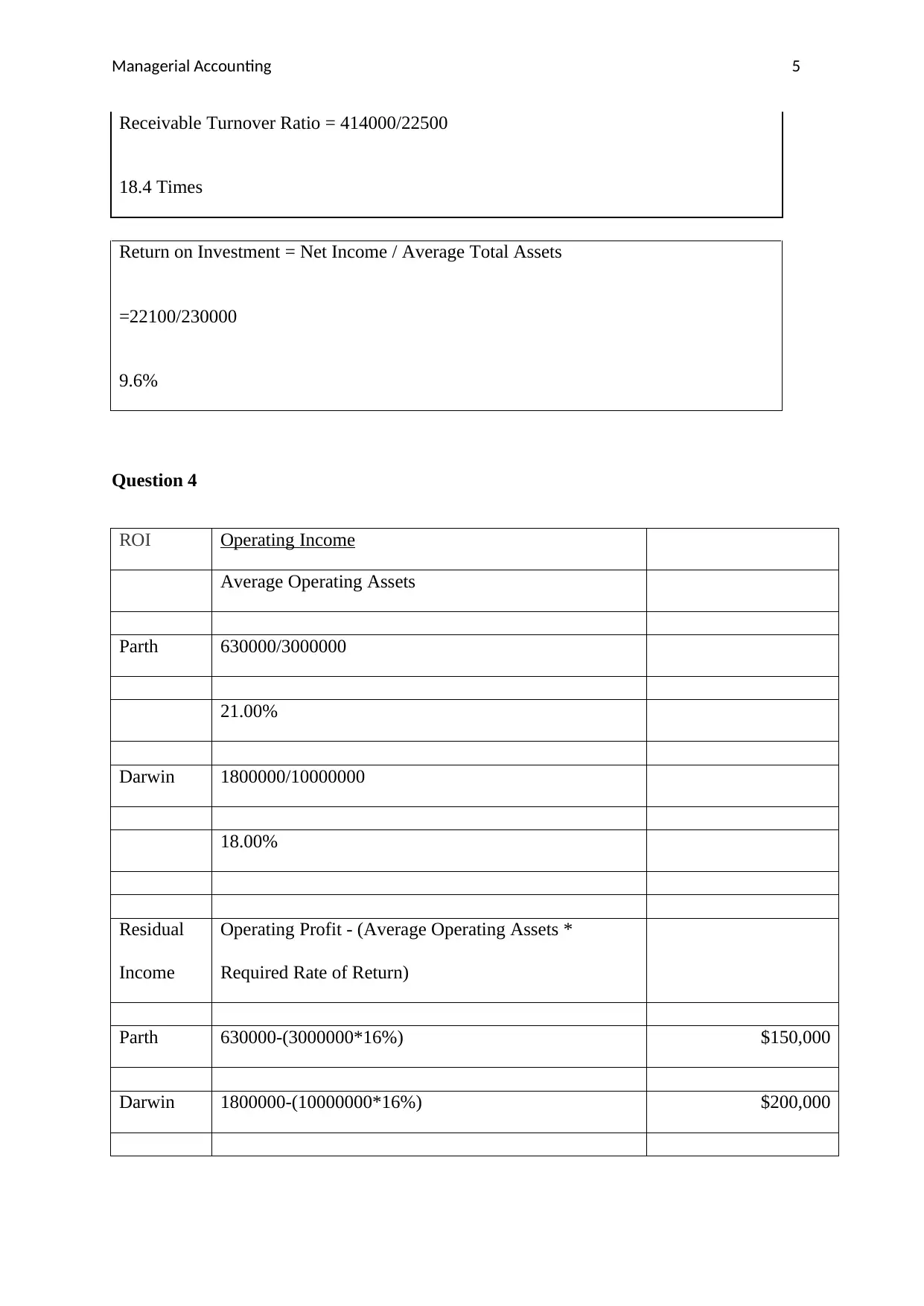

Managerial Accounting 5

Receivable Turnover Ratio = 414000/22500

18.4 Times

Return on Investment = Net Income / Average Total Assets

=22100/230000

9.6%

Question 4

ROI Operating Income

Average Operating Assets

Parth 630000/3000000

21.00%

Darwin 1800000/10000000

18.00%

Residual

Income

Operating Profit - (Average Operating Assets *

Required Rate of Return)

Parth 630000-(3000000*16%) $150,000

Darwin 1800000-(10000000*16%) $200,000

Receivable Turnover Ratio = 414000/22500

18.4 Times

Return on Investment = Net Income / Average Total Assets

=22100/230000

9.6%

Question 4

ROI Operating Income

Average Operating Assets

Parth 630000/3000000

21.00%

Darwin 1800000/10000000

18.00%

Residual

Income

Operating Profit - (Average Operating Assets *

Required Rate of Return)

Parth 630000-(3000000*16%) $150,000

Darwin 1800000-(10000000*16%) $200,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

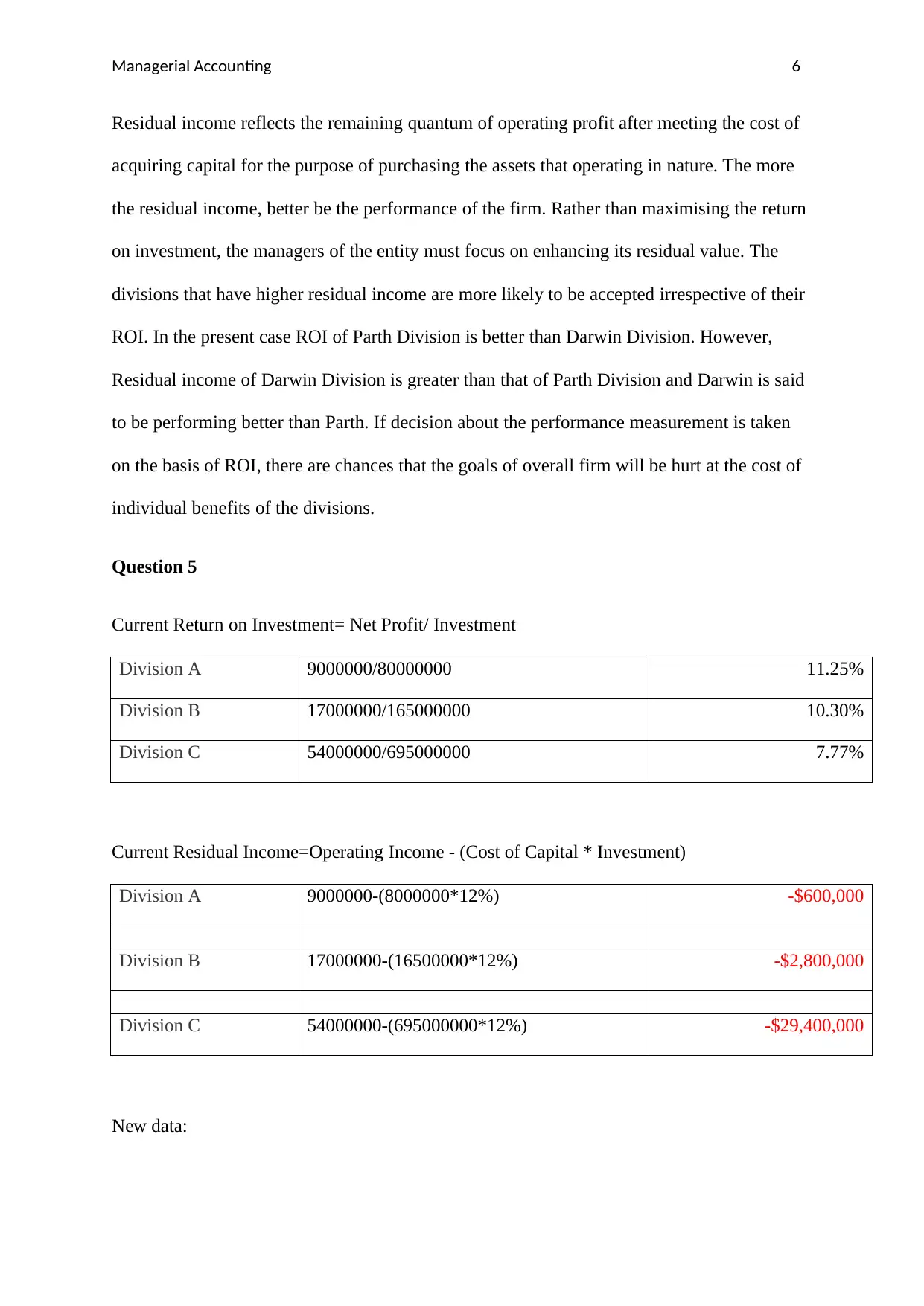

Managerial Accounting 6

Residual income reflects the remaining quantum of operating profit after meeting the cost of

acquiring capital for the purpose of purchasing the assets that operating in nature. The more

the residual income, better be the performance of the firm. Rather than maximising the return

on investment, the managers of the entity must focus on enhancing its residual value. The

divisions that have higher residual income are more likely to be accepted irrespective of their

ROI. In the present case ROI of Parth Division is better than Darwin Division. However,

Residual income of Darwin Division is greater than that of Parth Division and Darwin is said

to be performing better than Parth. If decision about the performance measurement is taken

on the basis of ROI, there are chances that the goals of overall firm will be hurt at the cost of

individual benefits of the divisions.

Question 5

Current Return on Investment= Net Profit/ Investment

Division A 9000000/80000000 11.25%

Division B 17000000/165000000 10.30%

Division C 54000000/695000000 7.77%

Current Residual Income=Operating Income - (Cost of Capital * Investment)

Division A 9000000-(8000000*12%) -$600,000

Division B 17000000-(16500000*12%) -$2,800,000

Division C 54000000-(695000000*12%) -$29,400,000

New data:

Residual income reflects the remaining quantum of operating profit after meeting the cost of

acquiring capital for the purpose of purchasing the assets that operating in nature. The more

the residual income, better be the performance of the firm. Rather than maximising the return

on investment, the managers of the entity must focus on enhancing its residual value. The

divisions that have higher residual income are more likely to be accepted irrespective of their

ROI. In the present case ROI of Parth Division is better than Darwin Division. However,

Residual income of Darwin Division is greater than that of Parth Division and Darwin is said

to be performing better than Parth. If decision about the performance measurement is taken

on the basis of ROI, there are chances that the goals of overall firm will be hurt at the cost of

individual benefits of the divisions.

Question 5

Current Return on Investment= Net Profit/ Investment

Division A 9000000/80000000 11.25%

Division B 17000000/165000000 10.30%

Division C 54000000/695000000 7.77%

Current Residual Income=Operating Income - (Cost of Capital * Investment)

Division A 9000000-(8000000*12%) -$600,000

Division B 17000000-(16500000*12%) -$2,800,000

Division C 54000000-(695000000*12%) -$29,400,000

New data:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

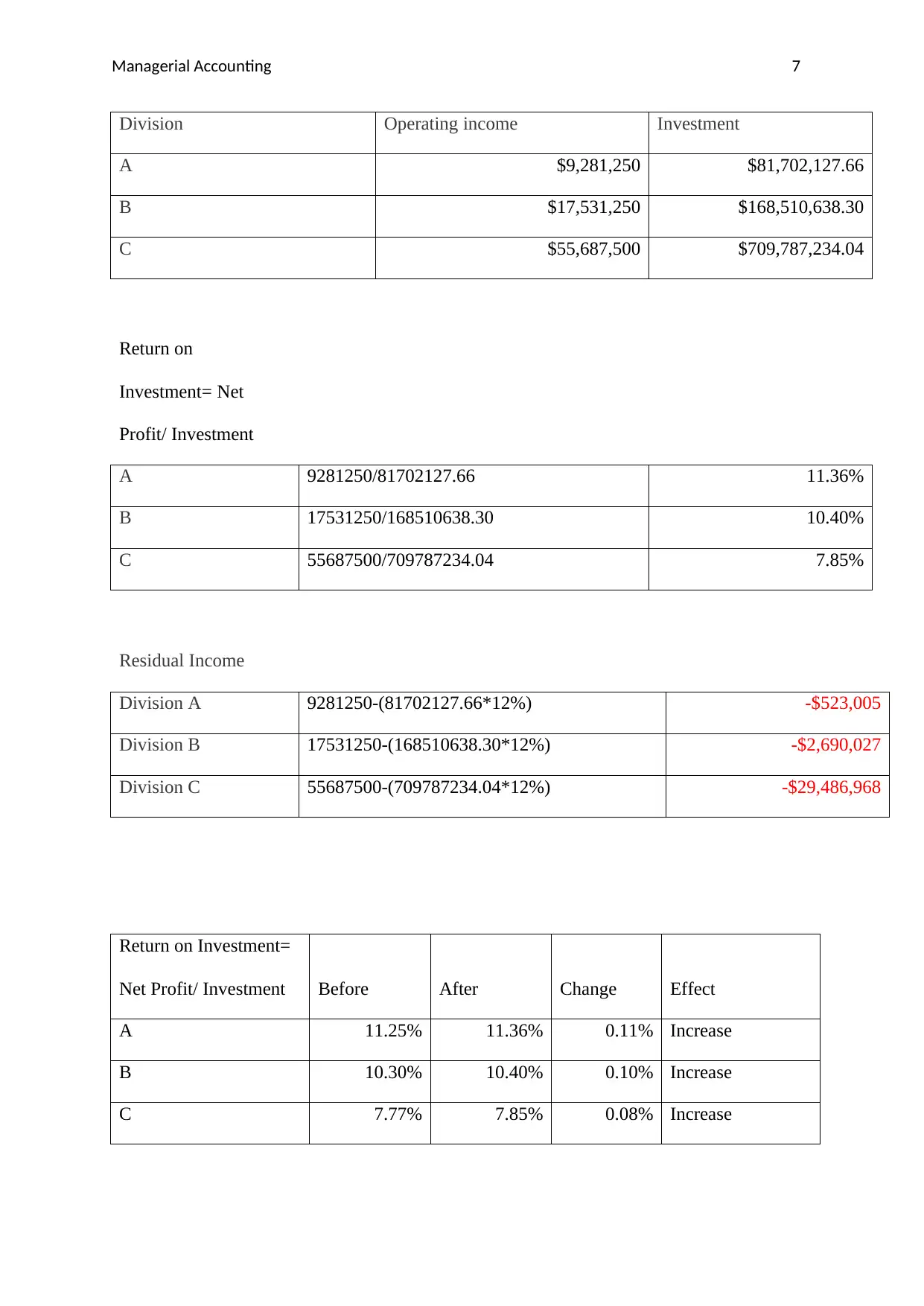

Managerial Accounting 7

Division Operating income Investment

A $9,281,250 $81,702,127.66

B $17,531,250 $168,510,638.30

C $55,687,500 $709,787,234.04

Return on

Investment= Net

Profit/ Investment

A 9281250/81702127.66 11.36%

B 17531250/168510638.30 10.40%

C 55687500/709787234.04 7.85%

Residual Income

Division A 9281250-(81702127.66*12%) -$523,005

Division B 17531250-(168510638.30*12%) -$2,690,027

Division C 55687500-(709787234.04*12%) -$29,486,968

Return on Investment=

Net Profit/ Investment Before After Change Effect

A 11.25% 11.36% 0.11% Increase

B 10.30% 10.40% 0.10% Increase

C 7.77% 7.85% 0.08% Increase

Division Operating income Investment

A $9,281,250 $81,702,127.66

B $17,531,250 $168,510,638.30

C $55,687,500 $709,787,234.04

Return on

Investment= Net

Profit/ Investment

A 9281250/81702127.66 11.36%

B 17531250/168510638.30 10.40%

C 55687500/709787234.04 7.85%

Residual Income

Division A 9281250-(81702127.66*12%) -$523,005

Division B 17531250-(168510638.30*12%) -$2,690,027

Division C 55687500-(709787234.04*12%) -$29,486,968

Return on Investment=

Net Profit/ Investment Before After Change Effect

A 11.25% 11.36% 0.11% Increase

B 10.30% 10.40% 0.10% Increase

C 7.77% 7.85% 0.08% Increase

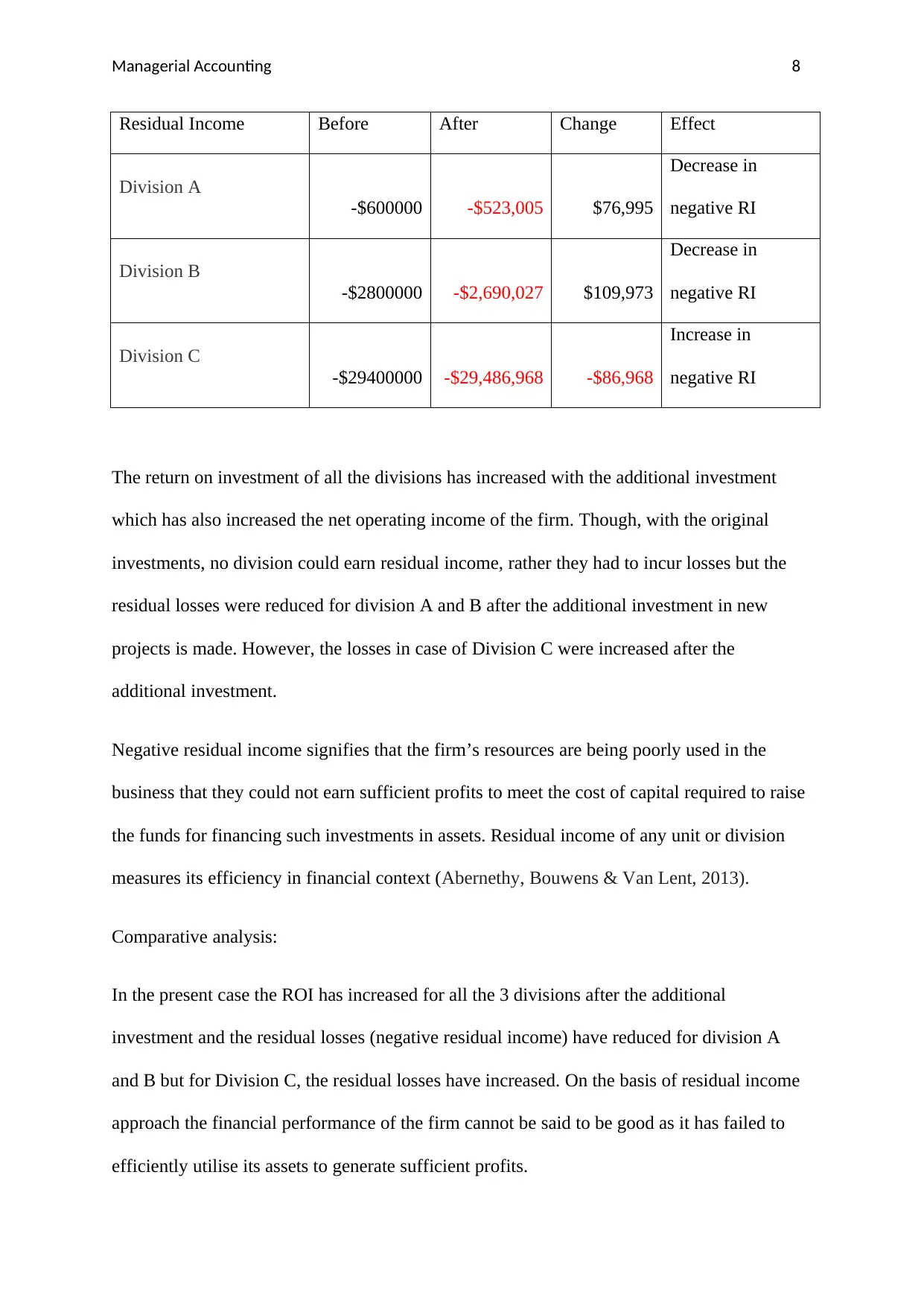

Managerial Accounting 8

Residual Income Before After Change Effect

Division A

-$600000 -$523,005 $76,995

Decrease in

negative RI

Division B

-$2800000 -$2,690,027 $109,973

Decrease in

negative RI

Division C

-$29400000 -$29,486,968 -$86,968

Increase in

negative RI

The return on investment of all the divisions has increased with the additional investment

which has also increased the net operating income of the firm. Though, with the original

investments, no division could earn residual income, rather they had to incur losses but the

residual losses were reduced for division A and B after the additional investment in new

projects is made. However, the losses in case of Division C were increased after the

additional investment.

Negative residual income signifies that the firm’s resources are being poorly used in the

business that they could not earn sufficient profits to meet the cost of capital required to raise

the funds for financing such investments in assets. Residual income of any unit or division

measures its efficiency in financial context (Abernethy, Bouwens & Van Lent, 2013).

Comparative analysis:

In the present case the ROI has increased for all the 3 divisions after the additional

investment and the residual losses (negative residual income) have reduced for division A

and B but for Division C, the residual losses have increased. On the basis of residual income

approach the financial performance of the firm cannot be said to be good as it has failed to

efficiently utilise its assets to generate sufficient profits.

Residual Income Before After Change Effect

Division A

-$600000 -$523,005 $76,995

Decrease in

negative RI

Division B

-$2800000 -$2,690,027 $109,973

Decrease in

negative RI

Division C

-$29400000 -$29,486,968 -$86,968

Increase in

negative RI

The return on investment of all the divisions has increased with the additional investment

which has also increased the net operating income of the firm. Though, with the original

investments, no division could earn residual income, rather they had to incur losses but the

residual losses were reduced for division A and B after the additional investment in new

projects is made. However, the losses in case of Division C were increased after the

additional investment.

Negative residual income signifies that the firm’s resources are being poorly used in the

business that they could not earn sufficient profits to meet the cost of capital required to raise

the funds for financing such investments in assets. Residual income of any unit or division

measures its efficiency in financial context (Abernethy, Bouwens & Van Lent, 2013).

Comparative analysis:

In the present case the ROI has increased for all the 3 divisions after the additional

investment and the residual losses (negative residual income) have reduced for division A

and B but for Division C, the residual losses have increased. On the basis of residual income

approach the financial performance of the firm cannot be said to be good as it has failed to

efficiently utilise its assets to generate sufficient profits.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managerial Accounting 9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Accounting 10

References:

Abernethy, M. A., Bouwens, J., & Van Lent, L. (2013). The role of performance measures in

the intertemporal decisions of business unit managers. Contemporary Accounting

Research, 30(3), 925-961.

Van Horne James, C. (2002). Financial Management & Policy, 12/E. Pearson Education

India.

References:

Abernethy, M. A., Bouwens, J., & Van Lent, L. (2013). The role of performance measures in

the intertemporal decisions of business unit managers. Contemporary Accounting

Research, 30(3), 925-961.

Van Horne James, C. (2002). Financial Management & Policy, 12/E. Pearson Education

India.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.