Managerial Accounting Report: Triton Corporation Performance Analysis

VerifiedAdded on 2020/10/22

|14

|4195

|129

Report

AI Summary

This report provides a comprehensive managerial accounting analysis of Triton Corporation, focusing on evaluating the performance of its various product divisions, including electrical products, floor boards, car accessories, industrial services, bathroom accessories, and pipes. It assesses their revenue, operating profit, and operating profit margin to identify strengths and weaknesses. The report delves into the implications of low-value-added items and their impact on financial returns and profitability, particularly for divisions like pipes and electrical products. It critically analyzes the arguments for selling the bathroom and pipes divisions, considering market share and operating profit margins. Furthermore, it explores strategies for reducing financial gearing and introduces a decentralization program to improve decision-making. The report uses financial ratios and budgetary control tools to identify potential risks and suggest improvements. The analysis aims to offer insights into working capital investment, cost control, and strategic decisions for maximizing financial performance.

MANAGERIAL

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION ..........................................................................................................................1

A. Drafting report to managing director.....................................................................................1

(a) Assessing each product divisions..........................................................................................1

(b) Implications of low value added items in context of financial returns and profitability.......4

B. Critical analysis of arguments of selling bathroom division and pipes division....................5

C Reducing the financial gearing................................................................................................7

D. Introduction of decentralisation programme which will be beneficial and decision making 9

CONCLUSION .............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION ..........................................................................................................................1

A. Drafting report to managing director.....................................................................................1

(a) Assessing each product divisions..........................................................................................1

(b) Implications of low value added items in context of financial returns and profitability.......4

B. Critical analysis of arguments of selling bathroom division and pipes division....................5

C Reducing the financial gearing................................................................................................7

D. Introduction of decentralisation programme which will be beneficial and decision making 9

CONCLUSION .............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

In the recent times, managers of business unit lay high level of emphasis on undertaking

accounting tools and techniques for evaluating performance. Moreover, accounting tools enables

manager to make evaluation of monetary aspects and take suitable decisions for the upcoming

time period. In addition to this, investment appraisal tools also provide assistance to the manager

in assessing whether proposed investment will contribute in the organizational success or not.

The present report is based on the case situation of Triton Corporation which comes under

manufacturing sector. In this, report will provide deeper insight about the manner through which

manager of firm can take decision about working capital investment and other matters pertaining

to the operations. Further, report also depicts the reasons due to which company prefers to reduce

the level of gearing. Along with this, report also entails how financial ratios and budgetary

control tools assists in identifying possible risk areas and give indications for improvements.

A. Drafting report to managing director

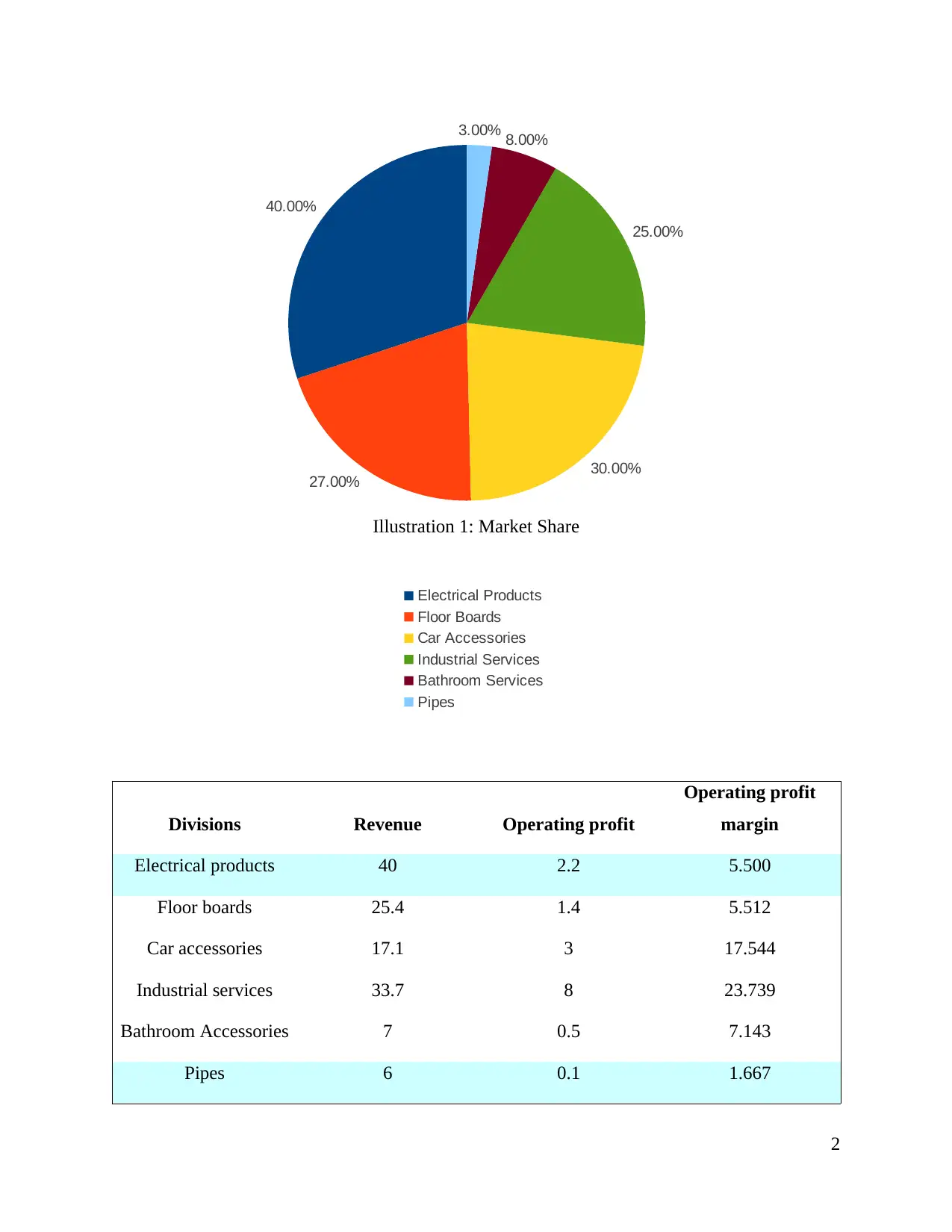

(a) Assessing each product divisions

While evaluating the divisions in light of competition which is growing day by day. The

organization consists of six operating divisions such as electrical products, Floor Boards, Car

Accessories, Industrial services, bathroom services and Pipes. In last year Triton Corporation is

generating huge sales of all electrical products followed up by Industrial services (Weygandt,

Kimmel and Kieso, 2015). For floor board cost of sales is in large proportion as compared to

other six divisions profit. In the context of salaries and wages highest has been consumed by

industrial services but it is generating profit not like pipes which is consuming seconding highest

of wages but its market share is least along with profit (Cost Controlling techniques, 2018).

1

In the recent times, managers of business unit lay high level of emphasis on undertaking

accounting tools and techniques for evaluating performance. Moreover, accounting tools enables

manager to make evaluation of monetary aspects and take suitable decisions for the upcoming

time period. In addition to this, investment appraisal tools also provide assistance to the manager

in assessing whether proposed investment will contribute in the organizational success or not.

The present report is based on the case situation of Triton Corporation which comes under

manufacturing sector. In this, report will provide deeper insight about the manner through which

manager of firm can take decision about working capital investment and other matters pertaining

to the operations. Further, report also depicts the reasons due to which company prefers to reduce

the level of gearing. Along with this, report also entails how financial ratios and budgetary

control tools assists in identifying possible risk areas and give indications for improvements.

A. Drafting report to managing director

(a) Assessing each product divisions

While evaluating the divisions in light of competition which is growing day by day. The

organization consists of six operating divisions such as electrical products, Floor Boards, Car

Accessories, Industrial services, bathroom services and Pipes. In last year Triton Corporation is

generating huge sales of all electrical products followed up by Industrial services (Weygandt,

Kimmel and Kieso, 2015). For floor board cost of sales is in large proportion as compared to

other six divisions profit. In the context of salaries and wages highest has been consumed by

industrial services but it is generating profit not like pipes which is consuming seconding highest

of wages but its market share is least along with profit (Cost Controlling techniques, 2018).

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

40.00%

27.00% 30.00%

25.00%

8.00%

3.00%

Illustration 1: Market Share

Electrical Products

Floor Boards

Car Accessories

Industrial Services

Bathroom Services

Pipes

Divisions Revenue Operating profit

Operating profit

margin

Electrical products 40 2.2 5.500

Floor boards 25.4 1.4 5.512

Car accessories 17.1 3 17.544

Industrial services 33.7 8 23.739

Bathroom Accessories 7 0.5 7.143

Pipes 6 0.1 1.667

2

27.00% 30.00%

25.00%

8.00%

3.00%

Illustration 1: Market Share

Electrical Products

Floor Boards

Car Accessories

Industrial Services

Bathroom Services

Pipes

Divisions Revenue Operating profit

Operating profit

margin

Electrical products 40 2.2 5.500

Floor boards 25.4 1.4 5.512

Car accessories 17.1 3 17.544

Industrial services 33.7 8 23.739

Bathroom Accessories 7 0.5 7.143

Pipes 6 0.1 1.667

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5.500

5.512

17.544 23.739

7.143

1.667

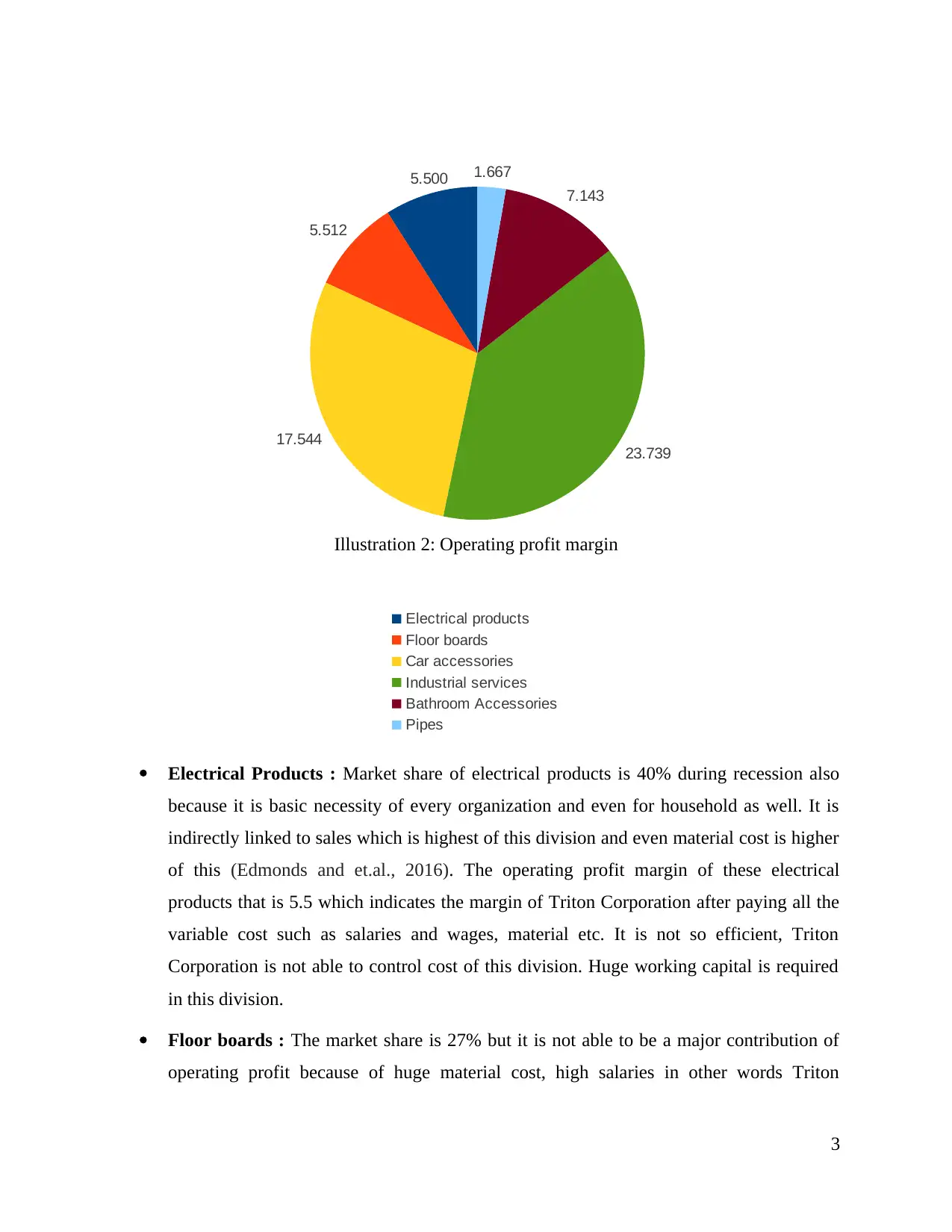

Illustration 2: Operating profit margin

Electrical products

Floor boards

Car accessories

Industrial services

Bathroom Accessories

Pipes

Electrical Products : Market share of electrical products is 40% during recession also

because it is basic necessity of every organization and even for household as well. It is

indirectly linked to sales which is highest of this division and even material cost is higher

of this (Edmonds and et.al., 2016). The operating profit margin of these electrical

products that is 5.5 which indicates the margin of Triton Corporation after paying all the

variable cost such as salaries and wages, material etc. It is not so efficient, Triton

Corporation is not able to control cost of this division. Huge working capital is required

in this division.

Floor boards : The market share is 27% but it is not able to be a major contribution of

operating profit because of huge material cost, high salaries in other words Triton

3

5.512

17.544 23.739

7.143

1.667

Illustration 2: Operating profit margin

Electrical products

Floor boards

Car accessories

Industrial services

Bathroom Accessories

Pipes

Electrical Products : Market share of electrical products is 40% during recession also

because it is basic necessity of every organization and even for household as well. It is

indirectly linked to sales which is highest of this division and even material cost is higher

of this (Edmonds and et.al., 2016). The operating profit margin of these electrical

products that is 5.5 which indicates the margin of Triton Corporation after paying all the

variable cost such as salaries and wages, material etc. It is not so efficient, Triton

Corporation is not able to control cost of this division. Huge working capital is required

in this division.

Floor boards : The market share is 27% but it is not able to be a major contribution of

operating profit because of huge material cost, high salaries in other words Triton

3

Corporation is not having capability to control its variable cost. Huge working capital is

required in this division (Butler and Ghosh, 2015).

Car Accessories : The sale of car accessories is not appropriate according to other

division but due to less variable cost that is material cost, salaries and other is

controllable by Triton Corporation so it is contributing huge proportion of 17.54 that is

second highest in all divisions with great market share.

Industrial services : The aspect of industrial services given the best example for

operating profit margin, in which it has maintained sales instead of controlling its

variable cost. In the proportion of sales and variable cost both are not equal so this leads

to huge market share along with the highest operating profit margin (Epure, 2016).

Bathroom accessories : It is the division which is less contributing in sales but while

generating sales it is controlling its variable cost i.e. low salaries and wages leads to less

market share but it is generating profit margin through operations is of 7.14 which is

highest than electrical products and floor brands.

Pipes : The division which consists of less sales, operating profit margin and even market

share as well. As its sales are of 6 m but its variable cost is of 5.9, it clearly depicts that it

is not even reaching to break even (Kim, Schmidgall and Damitio, 2017). The Triton

Corporation has huge working capital requirement in this division.

(b) Implications of low value added items in context of financial returns and profitability

In the context of financial returns and profitability, the highest operating profit is of

industrial services and followed up by car accessories but at average is of bathroom services

(Ionescu, 2017). The Triton Corporation must track on sales of these accessories along with

variable cost. According to operating profit margin most low value added services are considered

as :

Pipes with 1.67 operating margin

Electrical products with 5.5 operating margin

Floor Boards with 5.5 operating margin.

With the context of pipes, there is requirement of huge working capital so they should

work on that. For basis of electrical products Triton Corporation must check on its material cost

4

required in this division (Butler and Ghosh, 2015).

Car Accessories : The sale of car accessories is not appropriate according to other

division but due to less variable cost that is material cost, salaries and other is

controllable by Triton Corporation so it is contributing huge proportion of 17.54 that is

second highest in all divisions with great market share.

Industrial services : The aspect of industrial services given the best example for

operating profit margin, in which it has maintained sales instead of controlling its

variable cost. In the proportion of sales and variable cost both are not equal so this leads

to huge market share along with the highest operating profit margin (Epure, 2016).

Bathroom accessories : It is the division which is less contributing in sales but while

generating sales it is controlling its variable cost i.e. low salaries and wages leads to less

market share but it is generating profit margin through operations is of 7.14 which is

highest than electrical products and floor brands.

Pipes : The division which consists of less sales, operating profit margin and even market

share as well. As its sales are of 6 m but its variable cost is of 5.9, it clearly depicts that it

is not even reaching to break even (Kim, Schmidgall and Damitio, 2017). The Triton

Corporation has huge working capital requirement in this division.

(b) Implications of low value added items in context of financial returns and profitability

In the context of financial returns and profitability, the highest operating profit is of

industrial services and followed up by car accessories but at average is of bathroom services

(Ionescu, 2017). The Triton Corporation must track on sales of these accessories along with

variable cost. According to operating profit margin most low value added services are considered

as :

Pipes with 1.67 operating margin

Electrical products with 5.5 operating margin

Floor Boards with 5.5 operating margin.

With the context of pipes, there is requirement of huge working capital so they should

work on that. For basis of electrical products Triton Corporation must check on its material cost

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

which should be controllable because this is directly linked to margin. Whether it is generating

huge sales but they should implement some efficient techniques which will be controlling there

cost. They should use techniques like EOQ analysis and all for controlling the variable cost.

With the perspective of floor boards, sales is average but major proportion is used in material

cost so similar to electrical products they should apply some techniques which will be effective

for both divisions and even they should be promoted very well so this will lead to generate more

sales and they should try to control the variable cost. The bathroom accessories are at average

position (Bernardi and Collins, 2018), they should keep track of there sales by applying effective

techniques for promoting and for best reach to consumers. Bathroom services are considered as

most essentials for every human so they should use effective tools for promotions by satisfying

there existing customer and to make new target group.

B. Critical analysis of arguments of selling bathroom division and pipes division

Bathroom accessories Pipes

Sales 7 6

Variable cost 6.5 5.9

Operating profit 0.5 0.1

Operating profit margin 7.14 1.67

Market share 8 3

The present era is very competitive in nature as all the divisions of same Triton

Corporation are competing with itself for revenue and profit margin. According to long term

viability strategic decision has to be undertaken in context of Triton Corporation for both

division such as bathroom accessories and Pipes. In the context of sales they are somewhat

similar and both has huge requirement of huge working capital or capital expenditure for

improving the level of efficiency (Yousefi, and et.al., 2018). Both the division can be sold of for

making it more competitive by selling them. As there is need of more capital for generating more

profit but in the same context market share of bathroom accessories is of 8 but division of pipe

has very less market share. Bathroom accessories are very profitable in both purpose that is

household and for corporates as well. Even, while observing the operating profit margin of this is

5

huge sales but they should implement some efficient techniques which will be controlling there

cost. They should use techniques like EOQ analysis and all for controlling the variable cost.

With the perspective of floor boards, sales is average but major proportion is used in material

cost so similar to electrical products they should apply some techniques which will be effective

for both divisions and even they should be promoted very well so this will lead to generate more

sales and they should try to control the variable cost. The bathroom accessories are at average

position (Bernardi and Collins, 2018), they should keep track of there sales by applying effective

techniques for promoting and for best reach to consumers. Bathroom services are considered as

most essentials for every human so they should use effective tools for promotions by satisfying

there existing customer and to make new target group.

B. Critical analysis of arguments of selling bathroom division and pipes division

Bathroom accessories Pipes

Sales 7 6

Variable cost 6.5 5.9

Operating profit 0.5 0.1

Operating profit margin 7.14 1.67

Market share 8 3

The present era is very competitive in nature as all the divisions of same Triton

Corporation are competing with itself for revenue and profit margin. According to long term

viability strategic decision has to be undertaken in context of Triton Corporation for both

division such as bathroom accessories and Pipes. In the context of sales they are somewhat

similar and both has huge requirement of huge working capital or capital expenditure for

improving the level of efficiency (Yousefi, and et.al., 2018). Both the division can be sold of for

making it more competitive by selling them. As there is need of more capital for generating more

profit but in the same context market share of bathroom accessories is of 8 but division of pipe

has very less market share. Bathroom accessories are very profitable in both purpose that is

household and for corporates as well. Even, while observing the operating profit margin of this is

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7.14 which is recommendable to the organization in all aspects. They should work on division of

bathroom by controlling variable cost in proportion of sales.

For increasing sales they should use various promotional techniques such as advertising

cost, satisfying existing customer which will lead to word of mouth. They can create strong

online presence by creating blogs of there employees and quality team. There search engine

optimisation should be attracted to various people such as creating great content and viral it

through online. In the same series they might launch social media presence as it is interlinked to

search engine optimization (Tyler and et.al., 2018). Even they can use social media such as

Twitter and all. For increasing sale they might explore opportunities into new market overseas.

There is requirement of extensive research for finding new potential.

In the same context for bathroom accessories it is contributing good in operating profit

margin but for generating more margin it should be able to control variable cost such as material

cost, Labour cost control and even it should be able to control the cost of overhead by various

techniques. For controlling the cost of material they should try to get the best possible price and

they must reduce or even eliminating cost. They might check with various suppliers and they

should get best manufacturing material in best price (Dang, Hoang and Tran, 2017). The material

should be purchased in specific quantity according to space of inventory, there should be not

over inventory and it should not be very less. The inventory should be according to capital and

waste should be controlled by tracing mistakes and forming strategies such as use of every piece

of cloth, metal etc.

Even they can control variable cost by controlling labour cost and on contrary they

should make there worker very efficient. There operations of each product must be tracked by

senior management that from where it is coming and its expenditure (Weygandt, Kimmel and

Kieso, 2015). Staffing arrangements must be observed according to scheduling of labour within

specific duration. In same series variable overhead cost must be controlled which will lead to

great contribution in aspect of operating profit margin. Energy use must be audited and there

should be proper use of machines and lights. Thus, division of Bathroom must not be sold

because it will generate huge profit to the Triton Corporation but on contrary side if it is sold

then it will be improving the final margin of Triton Corporation at the end of year. Its variable

6

bathroom by controlling variable cost in proportion of sales.

For increasing sales they should use various promotional techniques such as advertising

cost, satisfying existing customer which will lead to word of mouth. They can create strong

online presence by creating blogs of there employees and quality team. There search engine

optimisation should be attracted to various people such as creating great content and viral it

through online. In the same series they might launch social media presence as it is interlinked to

search engine optimization (Tyler and et.al., 2018). Even they can use social media such as

Twitter and all. For increasing sale they might explore opportunities into new market overseas.

There is requirement of extensive research for finding new potential.

In the same context for bathroom accessories it is contributing good in operating profit

margin but for generating more margin it should be able to control variable cost such as material

cost, Labour cost control and even it should be able to control the cost of overhead by various

techniques. For controlling the cost of material they should try to get the best possible price and

they must reduce or even eliminating cost. They might check with various suppliers and they

should get best manufacturing material in best price (Dang, Hoang and Tran, 2017). The material

should be purchased in specific quantity according to space of inventory, there should be not

over inventory and it should not be very less. The inventory should be according to capital and

waste should be controlled by tracing mistakes and forming strategies such as use of every piece

of cloth, metal etc.

Even they can control variable cost by controlling labour cost and on contrary they

should make there worker very efficient. There operations of each product must be tracked by

senior management that from where it is coming and its expenditure (Weygandt, Kimmel and

Kieso, 2015). Staffing arrangements must be observed according to scheduling of labour within

specific duration. In same series variable overhead cost must be controlled which will lead to

great contribution in aspect of operating profit margin. Energy use must be audited and there

should be proper use of machines and lights. Thus, division of Bathroom must not be sold

because it will generate huge profit to the Triton Corporation but on contrary side if it is sold

then it will be improving the final margin of Triton Corporation at the end of year. Its variable

6

cost to the Triton Corporation is of 6.5 but its operating profit margin is 7.11, so this will

indirectly increase margin of Triton Corporation without incurring any variable cost.

The division of pipe is generating sales of 6 million with its variable cost of 5.9 which is

clearly giving picture of less profit before interest and tax and after paying its tax and interest it

will directly incur loss to the Triton Corporation. But this scene is hypothetical, tax structure is

not known. So according to operating profit margin it is giving 1.67 and its market share is of 3%

which is very low as compared to other division (Edmonds and et.al., 2016). Division of pipe is

not contributing too much and indirectly it is generating cost to Triton Corporation instead of

generating profit. Accordance with its market share, if it is sold to the organization who is only

dealing with pipes then it will not generate cost but it will be referred as margin to Triton. So it

should concentrate on margin instead of cost.

C Reducing the financial gearing

In terms with analysis operational gains of Triton Corporation in due period there will be

various techniques which are needed to be considered by business professionals such as reducing

costs of assets. Similarly, the professionals are planning to improve the sum of capital for

equipment replacement and modernisation programmes (Butler and Ghosh, 2015). Firm

approaches towards reducing financial gearing in the due period which will be effective and

helpful as per meeting financial goals. Requirement of financial capital in the operational

activities are the main areas of concerning in a business unit. Therefore, there have been

increment in debt securities which are by selling marketable securities among investors of firm.

On the other side, they have also considered factors which increase profitability for all products

which are being produces and marketed in environment. If comprised with analysing the

activators which will be used on managing profitably of entity such as Payback period.

1. Identification of influential factors which will be used for building long term payback

period:

For making appropriate project palliating and administration of the operations which will

require suitable changes in the operations. Therefore, to improve the probability of the period

which will be consideration by making effective changes in the operating in each activities. In

Accordance with the electrical products of the firm in the due period they have made the highest

revenue of 40 million (Epure, 2016). The costs incurred in production are for material it was

7

indirectly increase margin of Triton Corporation without incurring any variable cost.

The division of pipe is generating sales of 6 million with its variable cost of 5.9 which is

clearly giving picture of less profit before interest and tax and after paying its tax and interest it

will directly incur loss to the Triton Corporation. But this scene is hypothetical, tax structure is

not known. So according to operating profit margin it is giving 1.67 and its market share is of 3%

which is very low as compared to other division (Edmonds and et.al., 2016). Division of pipe is

not contributing too much and indirectly it is generating cost to Triton Corporation instead of

generating profit. Accordance with its market share, if it is sold to the organization who is only

dealing with pipes then it will not generate cost but it will be referred as margin to Triton. So it

should concentrate on margin instead of cost.

C Reducing the financial gearing

In terms with analysis operational gains of Triton Corporation in due period there will be

various techniques which are needed to be considered by business professionals such as reducing

costs of assets. Similarly, the professionals are planning to improve the sum of capital for

equipment replacement and modernisation programmes (Butler and Ghosh, 2015). Firm

approaches towards reducing financial gearing in the due period which will be effective and

helpful as per meeting financial goals. Requirement of financial capital in the operational

activities are the main areas of concerning in a business unit. Therefore, there have been

increment in debt securities which are by selling marketable securities among investors of firm.

On the other side, they have also considered factors which increase profitability for all products

which are being produces and marketed in environment. If comprised with analysing the

activators which will be used on managing profitably of entity such as Payback period.

1. Identification of influential factors which will be used for building long term payback

period:

For making appropriate project palliating and administration of the operations which will

require suitable changes in the operations. Therefore, to improve the probability of the period

which will be consideration by making effective changes in the operating in each activities. In

Accordance with the electrical products of the firm in the due period they have made the highest

revenue of 40 million (Epure, 2016). The costs incurred in production are for material it was

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

34.5, for salaries it was 1.2 and the other relevant costs are of 2.1. Therefore, in relation with

such analysis it can be said that the firm is making fewer payments to the employees in the

manufacturing the Electricity products. Considering the period of recession which insist that

there will be fruitful changes in the operational practices of the firm which in turn will have

effective revenue generation as well as profitable gains at the same time. The highest revenue

rented by electric products of Triton Corporation which has the negative impacts as the salaries

payable to the employees are lower than other product line of firm.

Concerning revenue generated by other departments of business such as floor boards,

cars accessories etc. on which Pipes and Bathroom Accessories are having poor performance as

they are contributing lower income gains to business. Thus, the highest salaries is being payable

by the firm in industrial services in due period. Therefore, to concern the wealth of individual as

well as firm it can be said that they have to balance the operations as well as pay employees as

per their efficiencies and ability to operate activities (Kim, Schmidgall and Damitio, 2017).

Thus, concerning the lower income retained by the other department on which it can be said that

there is needed to have satisfactory improvements in sales as well as reduction in the costs.

Moreover, it has been planned by Triton Corporation to make investments in operational

activities of firm on which they will have effective rise in revenue and operations.

2. Strategies for reducing gearing:

Triton corporation can take major steps for reducing gearing and for improving debt to

capital ratio. These strategies can be applied for raising the profitability of sales, restructuring the

debt and for managing inventory in very efficient manner (Ionescu, 2017). It will be representing

the total financial soundness of Tritorn corporation and even it will reveal appropriate proportion

of equity and even for financing debts. In gearing, 0.5 is considered as ideal ratio or less than it.

Any organization who is representing gearing 1 or more than that it is considered as insolvent

technically.

One of the most common and logical way for reducing debt to capital ratio then it should

be capable for raising sales revenue and profitability. This can be attained by increasing prices,

sales or even by decreasing costs. The cash which is extra used for paying in context of existing

debt. Gearing can be also reduced by managing inventory in most effective pattern. Unnecessary

inventory should not be managed because it is blocking money or it is referred as waste of cash

8

such analysis it can be said that the firm is making fewer payments to the employees in the

manufacturing the Electricity products. Considering the period of recession which insist that

there will be fruitful changes in the operational practices of the firm which in turn will have

effective revenue generation as well as profitable gains at the same time. The highest revenue

rented by electric products of Triton Corporation which has the negative impacts as the salaries

payable to the employees are lower than other product line of firm.

Concerning revenue generated by other departments of business such as floor boards,

cars accessories etc. on which Pipes and Bathroom Accessories are having poor performance as

they are contributing lower income gains to business. Thus, the highest salaries is being payable

by the firm in industrial services in due period. Therefore, to concern the wealth of individual as

well as firm it can be said that they have to balance the operations as well as pay employees as

per their efficiencies and ability to operate activities (Kim, Schmidgall and Damitio, 2017).

Thus, concerning the lower income retained by the other department on which it can be said that

there is needed to have satisfactory improvements in sales as well as reduction in the costs.

Moreover, it has been planned by Triton Corporation to make investments in operational

activities of firm on which they will have effective rise in revenue and operations.

2. Strategies for reducing gearing:

Triton corporation can take major steps for reducing gearing and for improving debt to

capital ratio. These strategies can be applied for raising the profitability of sales, restructuring the

debt and for managing inventory in very efficient manner (Ionescu, 2017). It will be representing

the total financial soundness of Tritorn corporation and even it will reveal appropriate proportion

of equity and even for financing debts. In gearing, 0.5 is considered as ideal ratio or less than it.

Any organization who is representing gearing 1 or more than that it is considered as insolvent

technically.

One of the most common and logical way for reducing debt to capital ratio then it should

be capable for raising sales revenue and profitability. This can be attained by increasing prices,

sales or even by decreasing costs. The cash which is extra used for paying in context of existing

debt. Gearing can be also reduced by managing inventory in most effective pattern. Unnecessary

inventory should not be managed because it is blocking money or it is referred as waste of cash

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

flow (Bernardi and Collins, 2018). The most logical way for raising capital is to restructuring

debt and it will lead to decrease debt to capital ratio. If Triton Corporation will be financing at

huge interest rate, and present interest rate is simultaneously lower so organization can attain

refinance to its own existing debt at lower rates. So this will directly decrease the expenses of

interest and monthly payments which leads for raising bottom line of Triton and cash flow.

D. Introduction of decentralisation programme which will be beneficial and decision making

1. Advises to the managing directors:

On the basis of given case situation, Triton Corporation is planning to cut staff from 48 to

20. Given scenario presents that managing director believes effectual control can be exerted on

financial aspects through using ratio and variance analysis technique (Yousefi, and et.al., 2018).

In the context of Triton Corporation both such techniques are highly effectual which in turn

gives clear indication in relation to undertaking strategic actions for improvement.

Ratio analysis may be served as the most effectual technique which assists in evaluating

financial performance under different areas such as profitability, liquidity, solvency and

efficiency. Hence, using the tool of ratio analysis Triton Corporation’s manager can evaluate

financial performance over the years and compare the same with rivals (Tyler and et.al., 2018).

Hence, by performing ratio analysis firm can assess its weak areas and thereby become able to

take measure for performance enhancement. In the context of Triton Corporation, by taking into

account final accounts following ratios have been calculated.

Liquidity ratio analysis

Particulars Formula Figures

Current assets 35

Current liabilities 20

Current ratio Current assets / current

liabilities

1.75:1

Interpretation: Outcome of ratio analysis presents that Triton Corporation has maintained

enough current assets for meeting obligations. From assessment, it has identified that ideal

current ratio accounts for 2:1. On the basis of this, firm must have 2 current assets for meeting 1

obligation. Hence, by taking into account overall evaluation it can be presented that business unit

is able to meet obligations from current assets prominently.

Solvency ratio analysis

9

debt and it will lead to decrease debt to capital ratio. If Triton Corporation will be financing at

huge interest rate, and present interest rate is simultaneously lower so organization can attain

refinance to its own existing debt at lower rates. So this will directly decrease the expenses of

interest and monthly payments which leads for raising bottom line of Triton and cash flow.

D. Introduction of decentralisation programme which will be beneficial and decision making

1. Advises to the managing directors:

On the basis of given case situation, Triton Corporation is planning to cut staff from 48 to

20. Given scenario presents that managing director believes effectual control can be exerted on

financial aspects through using ratio and variance analysis technique (Yousefi, and et.al., 2018).

In the context of Triton Corporation both such techniques are highly effectual which in turn

gives clear indication in relation to undertaking strategic actions for improvement.

Ratio analysis may be served as the most effectual technique which assists in evaluating

financial performance under different areas such as profitability, liquidity, solvency and

efficiency. Hence, using the tool of ratio analysis Triton Corporation’s manager can evaluate

financial performance over the years and compare the same with rivals (Tyler and et.al., 2018).

Hence, by performing ratio analysis firm can assess its weak areas and thereby become able to

take measure for performance enhancement. In the context of Triton Corporation, by taking into

account final accounts following ratios have been calculated.

Liquidity ratio analysis

Particulars Formula Figures

Current assets 35

Current liabilities 20

Current ratio Current assets / current

liabilities

1.75:1

Interpretation: Outcome of ratio analysis presents that Triton Corporation has maintained

enough current assets for meeting obligations. From assessment, it has identified that ideal

current ratio accounts for 2:1. On the basis of this, firm must have 2 current assets for meeting 1

obligation. Hence, by taking into account overall evaluation it can be presented that business unit

is able to meet obligations from current assets prominently.

Solvency ratio analysis

9

Particulars Formula Figures

Loan 48

Total shareholders’ equity

(Share capital + reserves)

22

Debt-equity ratio Loan / shareholder’s equity 2.18

Interpretation: Tabular presentation shows that debt-equity ratio implies for 2.2:1

respectively. In the context of Triton Corporation, solvency position can said to be sound when

debt-equity ratio accounts for .5:1. It presents that firm should 2 equities over 1 debt. Currently,

Triton Corporation has maintained high debt over equities which in turn considered as not a good

indicator. The reason behind this, in the case of debt, firm has to make interest payment

irrespective of profit generation. On the other side, under equities, firm offer dividend to the

shareholders only when it generates enough margin during the concerned period. Hence, it can

be mentioned that higher debt level imposes financial burden and impacts firm’s profitability.

Thus, at the time of raising funds Triton Corporation should keep in mind ideal ratio such

as .5:1.

2.Critical analysis over fruitful needs of management accounting techniques in business

practices:

Impacts of managerial accounting techniques in business operations which will be helpful

as it creates the appropriate internal analysis over the operations. It consists of preparing all the

reports such as income statements, financial statements, budgets as well as various accounts of

the different operations incurred in the business (Dang, Hoang and Tran, 2017). Moreover, the

main motive of preparing such reports is that it will be a helpful tool which initiates the internal

auditing of the venturi. Derived outcomes from the operations of firm will have effective control

over business gains and profits of the entity. Budgeting and various costing use in management

accounting methods benefits in organising the operational activities. Thus, it provokes the

managerial professionals as well as accounting personal to undertake the research through

financial of firm as well as generate the new ideas which will have impacts on managing

operations of entity (Weygandt, Kimmel and Kieso, 2015). Ideas and the decisions made bay

professionals are in relation with improving the operational activities as well as managing the

profitable gains of firm in the right time. Reduction in costs and expenses will be effective as it

10

Loan 48

Total shareholders’ equity

(Share capital + reserves)

22

Debt-equity ratio Loan / shareholder’s equity 2.18

Interpretation: Tabular presentation shows that debt-equity ratio implies for 2.2:1

respectively. In the context of Triton Corporation, solvency position can said to be sound when

debt-equity ratio accounts for .5:1. It presents that firm should 2 equities over 1 debt. Currently,

Triton Corporation has maintained high debt over equities which in turn considered as not a good

indicator. The reason behind this, in the case of debt, firm has to make interest payment

irrespective of profit generation. On the other side, under equities, firm offer dividend to the

shareholders only when it generates enough margin during the concerned period. Hence, it can

be mentioned that higher debt level imposes financial burden and impacts firm’s profitability.

Thus, at the time of raising funds Triton Corporation should keep in mind ideal ratio such

as .5:1.

2.Critical analysis over fruitful needs of management accounting techniques in business

practices:

Impacts of managerial accounting techniques in business operations which will be helpful

as it creates the appropriate internal analysis over the operations. It consists of preparing all the

reports such as income statements, financial statements, budgets as well as various accounts of

the different operations incurred in the business (Dang, Hoang and Tran, 2017). Moreover, the

main motive of preparing such reports is that it will be a helpful tool which initiates the internal

auditing of the venturi. Derived outcomes from the operations of firm will have effective control

over business gains and profits of the entity. Budgeting and various costing use in management

accounting methods benefits in organising the operational activities. Thus, it provokes the

managerial professionals as well as accounting personal to undertake the research through

financial of firm as well as generate the new ideas which will have impacts on managing

operations of entity (Weygandt, Kimmel and Kieso, 2015). Ideas and the decisions made bay

professionals are in relation with improving the operational activities as well as managing the

profitable gains of firm in the right time. Reduction in costs and expenses will be effective as it

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.