Managerial Accounting Report: Cost Analysis and Decision Making

VerifiedAdded on 2020/10/23

|13

|3952

|162

Report

AI Summary

This report delves into the core concepts of managerial accounting, emphasizing cost analysis, decision-making, and innovation. Part A examines different cost types (fixed, variable, opportunity), relevant and irrelevant information for appliance purchase decisions, and calculations for various options, including employing additional staff. Detailed calculations and interpretations are provided to guide decisions on appliance purchases, employee hiring, and the optimal number of children to accommodate. Part B explores the components of a management accounting system and its contribution to innovation, drawing on journal articles. The report highlights the importance of managerial accounting in achieving organizational goals, offering a practical application of its principles through case studies and calculations. The report concludes with a synthesis of findings, providing a comprehensive understanding of managerial accounting's role in business operations and strategic planning.

MANAGERIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

1. Different types of costs discusses in the unit with example....................................................1

2. Relevant information to decision for purchasing the appliance?.............................................2

3. Calculation of cost to be incurred by Franks as to choose different options...........................2

4. Calculation and interpretation of additional cost to be incurred by Franks for employing

additional employees for taking decision regarding whether to employ additional employees or

not................................................................................................................................................3

5. Calculation to be used to take decision regarding number of children to be accepted and

number of employee to be hired..................................................................................................4

PART B............................................................................................................................................5

1. Identification of components of management accounting system...........................................5

2.Explanation of how management accounting contributes to the innovation process...............6

3. Findings from the journal articles that could management accountant...................................7

CONCLUSION ...............................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

1. Different types of costs discusses in the unit with example....................................................1

2. Relevant information to decision for purchasing the appliance?.............................................2

3. Calculation of cost to be incurred by Franks as to choose different options...........................2

4. Calculation and interpretation of additional cost to be incurred by Franks for employing

additional employees for taking decision regarding whether to employ additional employees or

not................................................................................................................................................3

5. Calculation to be used to take decision regarding number of children to be accepted and

number of employee to be hired..................................................................................................4

PART B............................................................................................................................................5

1. Identification of components of management accounting system...........................................5

2.Explanation of how management accounting contributes to the innovation process...............6

3. Findings from the journal articles that could management accountant...................................7

CONCLUSION ...............................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Managerial accounting, most commonly called as cost accounting is the systematic

process of identifying, measuring, examining & analysing, interpreting and communicating the

information to the business managers for the purpose of attainment of organisational goals and

objectives. It is different from the financial accounting as the managerial accounting's main

motive is to help the internal management in its decision making while financial accounting is

more concerned with reporting and communicating the financial information to outside

stakeholders (Chovancova, Krejza and Vankova, 2019).

The present project report will highlight the different types of costs, relevancy and

irrelevancy regarding the purchase decision related to appliance, decision regarding hiring of

new employee. In the other section of the report, it will cover the critical evaluation of role of

management accounting and the provisions and components of the management accounting in

the innovation process of the two different companies based on a journal article.

PART A

1. Different types of costs discusses in the unit with example

Cost can be categorized in different types like fixed costs, variable cost, period cost,

product cost, sunk cost, etc. the present unit includes the following types of costs:

Fixed cost: Fixed cost can be defined as a cost which is incurred by a business

organisation. In management accounting, these costs does not change with increase or

decrease in the production volume. Although, these remains constant over the period. To

break even the fixed cost, more revenue is needed to generate by the business so that per

unit of fixed cost could be lower down. This is done by the way of economies of scale

(Latan and et.al., 2018).

In the present unit, utility cost of daycare i.e. $ 50 per month can be consider as a fixed cost. This

cost is to be incurred by the Franks on monthly basis rather than on the basis of number of child

cared by them. Therefore it would be consider as a periodic cost or the fixed cost.

Variable cost: Variable cost are those that keeps changing with the change in number of

volume of production or number of services provided by a company. These cost remains

constant on per unit basis (Horton and de Araujo Wanderley, 2018).

In the present case the cost of meal can be consider as variable cost. The Franks need to incur

$3.2 per child per day on meal. The change in cost would be based on number of child served by

1

Managerial accounting, most commonly called as cost accounting is the systematic

process of identifying, measuring, examining & analysing, interpreting and communicating the

information to the business managers for the purpose of attainment of organisational goals and

objectives. It is different from the financial accounting as the managerial accounting's main

motive is to help the internal management in its decision making while financial accounting is

more concerned with reporting and communicating the financial information to outside

stakeholders (Chovancova, Krejza and Vankova, 2019).

The present project report will highlight the different types of costs, relevancy and

irrelevancy regarding the purchase decision related to appliance, decision regarding hiring of

new employee. In the other section of the report, it will cover the critical evaluation of role of

management accounting and the provisions and components of the management accounting in

the innovation process of the two different companies based on a journal article.

PART A

1. Different types of costs discusses in the unit with example

Cost can be categorized in different types like fixed costs, variable cost, period cost,

product cost, sunk cost, etc. the present unit includes the following types of costs:

Fixed cost: Fixed cost can be defined as a cost which is incurred by a business

organisation. In management accounting, these costs does not change with increase or

decrease in the production volume. Although, these remains constant over the period. To

break even the fixed cost, more revenue is needed to generate by the business so that per

unit of fixed cost could be lower down. This is done by the way of economies of scale

(Latan and et.al., 2018).

In the present unit, utility cost of daycare i.e. $ 50 per month can be consider as a fixed cost. This

cost is to be incurred by the Franks on monthly basis rather than on the basis of number of child

cared by them. Therefore it would be consider as a periodic cost or the fixed cost.

Variable cost: Variable cost are those that keeps changing with the change in number of

volume of production or number of services provided by a company. These cost remains

constant on per unit basis (Horton and de Araujo Wanderley, 2018).

In the present case the cost of meal can be consider as variable cost. The Franks need to incur

$3.2 per child per day on meal. The change in cost would be based on number of child served by

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

them. Further, it would remain unchanged on per child basis. Therefore, these will be consider as

variable cost.

Opportunity cost: Opportunity cost refers to the cost that would need to be incurred by

a business if it chooses the second best alternative. These costs are not actually incurred

by a business. Rather, they would have been incurred if it selects the next best

alternative (Rikhardsson and Yigitbasioglu, 2018).

In the present unit, Franks have 3 options, whether to purchase the equipment, or to select

Red Oak for laundering the clothes or to select Landmark for self laundering the cloths. The cost

of third best alternative would be consider as opportunity cost for Franks. Like if the Frank

chooses option 1 , it would cost 52 for which it will have to forego the benefit of choosing option

2 &3. In all the three cases, the third option seemed to be the most cost effective option as it

would cost the Frank only 31.24 as against the option 2 in which it would cost it 50.39.

2. Relevant information to decision for purchasing the appliance?

Relevant information: Relevant information can be defined as a material information

that are needed to be consider in order to take any decision. In the present unit, information

regarding cost of old washer and dryer, cost to be incurred for launder the cloths through Red

oak, each cost that would needed to be incurred for self service laundering like convenience cost,

cost of purchasing laundry supplies, purchase, installation and energy cost of washer and dryers,

etc. would be relevant cost as they would be taken into account while taking decision about

whether to purchase the appliance or not.

Irrelevant information: Irrelevant information are all those information that would not

be consider while taking any specific decision in a business organisation. These can also be

consider as immaterial information for a specific decision making process (Bedford and Speklé,

2018).

In the present unit for the purpose of taking decision regarding purchase of appliance all

information other than cost to be incurred in various alternatives of purchasing like cost of meal,

purchasing cost of home, information regarding increase in cost, information of annual

subscription fee of license, etc. are irrelevant information regarding the decision making process

of purchasing the appliances.

3. Calculation of cost to be incurred by Franks as to choose different options

Option 1 launder the cloths by Red Oak company

2

variable cost.

Opportunity cost: Opportunity cost refers to the cost that would need to be incurred by

a business if it chooses the second best alternative. These costs are not actually incurred

by a business. Rather, they would have been incurred if it selects the next best

alternative (Rikhardsson and Yigitbasioglu, 2018).

In the present unit, Franks have 3 options, whether to purchase the equipment, or to select

Red Oak for laundering the clothes or to select Landmark for self laundering the cloths. The cost

of third best alternative would be consider as opportunity cost for Franks. Like if the Frank

chooses option 1 , it would cost 52 for which it will have to forego the benefit of choosing option

2 &3. In all the three cases, the third option seemed to be the most cost effective option as it

would cost the Frank only 31.24 as against the option 2 in which it would cost it 50.39.

2. Relevant information to decision for purchasing the appliance?

Relevant information: Relevant information can be defined as a material information

that are needed to be consider in order to take any decision. In the present unit, information

regarding cost of old washer and dryer, cost to be incurred for launder the cloths through Red

oak, each cost that would needed to be incurred for self service laundering like convenience cost,

cost of purchasing laundry supplies, purchase, installation and energy cost of washer and dryers,

etc. would be relevant cost as they would be taken into account while taking decision about

whether to purchase the appliance or not.

Irrelevant information: Irrelevant information are all those information that would not

be consider while taking any specific decision in a business organisation. These can also be

consider as immaterial information for a specific decision making process (Bedford and Speklé,

2018).

In the present unit for the purpose of taking decision regarding purchase of appliance all

information other than cost to be incurred in various alternatives of purchasing like cost of meal,

purchasing cost of home, information regarding increase in cost, information of annual

subscription fee of license, etc. are irrelevant information regarding the decision making process

of purchasing the appliances.

3. Calculation of cost to be incurred by Franks as to choose different options

Option 1 launder the cloths by Red Oak company

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

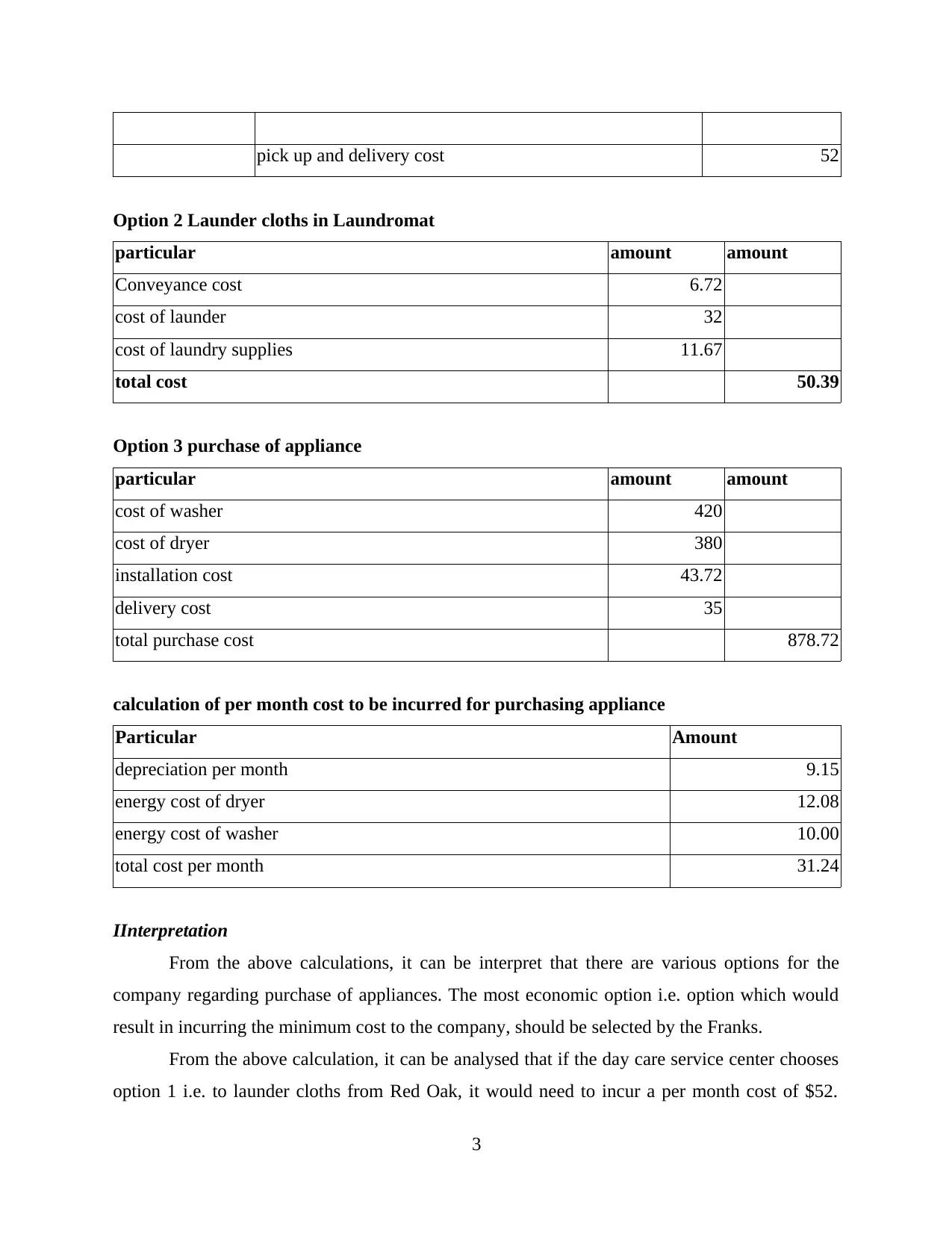

pick up and delivery cost 52

Option 2 Launder cloths in Laundromat

particular amount amount

Conveyance cost 6.72

cost of launder 32

cost of laundry supplies 11.67

total cost 50.39

Option 3 purchase of appliance

particular amount amount

cost of washer 420

cost of dryer 380

installation cost 43.72

delivery cost 35

total purchase cost 878.72

calculation of per month cost to be incurred for purchasing appliance

Particular Amount

depreciation per month 9.15

energy cost of dryer 12.08

energy cost of washer 10.00

total cost per month 31.24

IInterpretation

From the above calculations, it can be interpret that there are various options for the

company regarding purchase of appliances. The most economic option i.e. option which would

result in incurring the minimum cost to the company, should be selected by the Franks.

From the above calculation, it can be analysed that if the day care service center chooses

option 1 i.e. to launder cloths from Red Oak, it would need to incur a per month cost of $52.

3

Option 2 Launder cloths in Laundromat

particular amount amount

Conveyance cost 6.72

cost of launder 32

cost of laundry supplies 11.67

total cost 50.39

Option 3 purchase of appliance

particular amount amount

cost of washer 420

cost of dryer 380

installation cost 43.72

delivery cost 35

total purchase cost 878.72

calculation of per month cost to be incurred for purchasing appliance

Particular Amount

depreciation per month 9.15

energy cost of dryer 12.08

energy cost of washer 10.00

total cost per month 31.24

IInterpretation

From the above calculations, it can be interpret that there are various options for the

company regarding purchase of appliances. The most economic option i.e. option which would

result in incurring the minimum cost to the company, should be selected by the Franks.

From the above calculation, it can be analysed that if the day care service center chooses

option 1 i.e. to launder cloths from Red Oak, it would need to incur a per month cost of $52.

3

further, it would need to incur a cost of $50.39 per month if they choose to self launder the cloths

at laundromat. In addition, if they decides to purchase both washer and dryer, they would need to

incur a cost of $31.24 per month.

As the purchase of appliances would result in incurring a minimum amount of cost by the

Franks, it should decide to purchase the appliance rather than launder from Red Oak or

Laundromat.

4. Calculation and interpretation of additional cost to be incurred by Franks for employing

additional employees for taking decision regarding whether to employ additional

employees or not

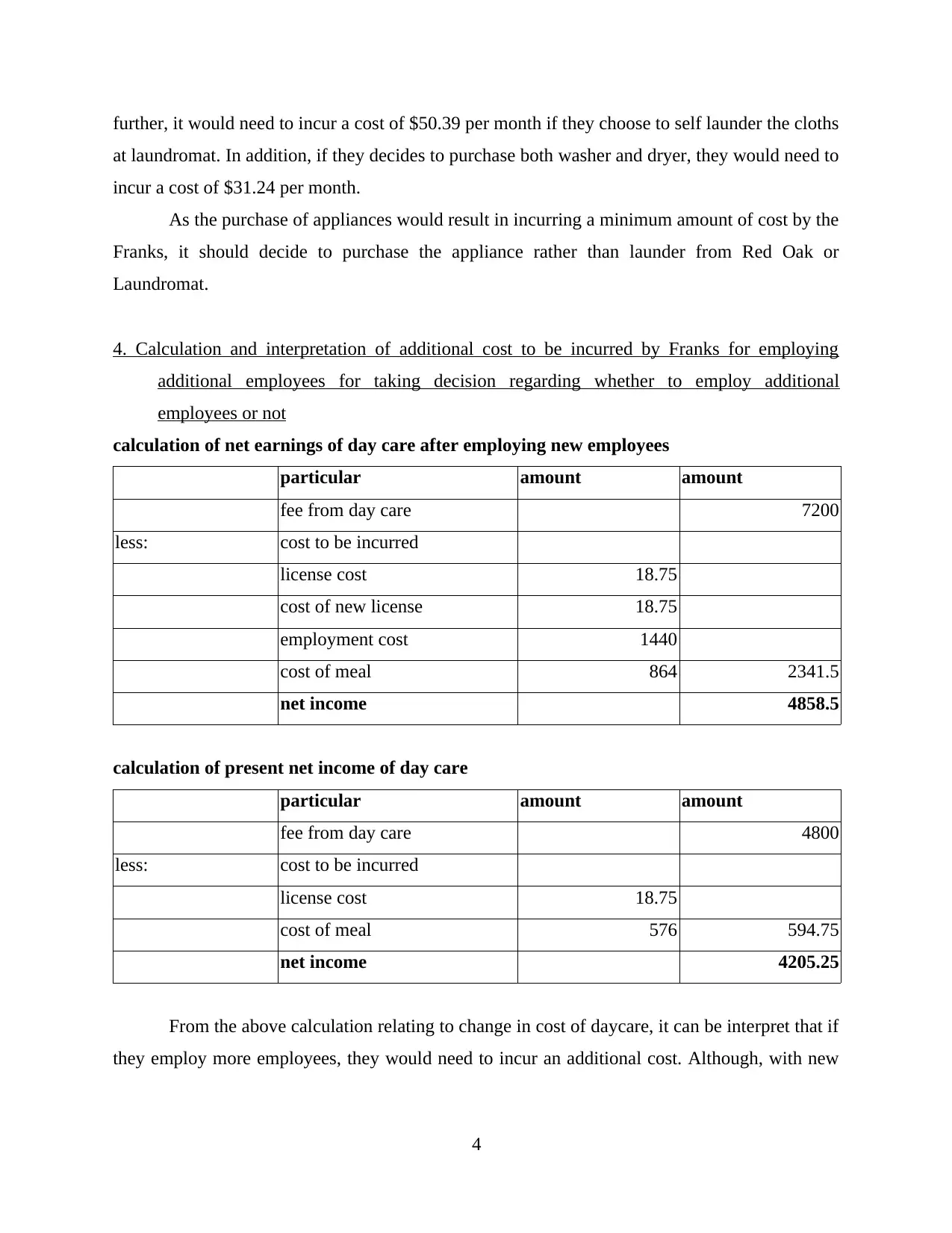

calculation of net earnings of day care after employing new employees

particular amount amount

fee from day care 7200

less: cost to be incurred

license cost 18.75

cost of new license 18.75

employment cost 1440

cost of meal 864 2341.5

net income 4858.5

calculation of present net income of day care

particular amount amount

fee from day care 4800

less: cost to be incurred

license cost 18.75

cost of meal 576 594.75

net income 4205.25

From the above calculation relating to change in cost of daycare, it can be interpret that if

they employ more employees, they would need to incur an additional cost. Although, with new

4

at laundromat. In addition, if they decides to purchase both washer and dryer, they would need to

incur a cost of $31.24 per month.

As the purchase of appliances would result in incurring a minimum amount of cost by the

Franks, it should decide to purchase the appliance rather than launder from Red Oak or

Laundromat.

4. Calculation and interpretation of additional cost to be incurred by Franks for employing

additional employees for taking decision regarding whether to employ additional

employees or not

calculation of net earnings of day care after employing new employees

particular amount amount

fee from day care 7200

less: cost to be incurred

license cost 18.75

cost of new license 18.75

employment cost 1440

cost of meal 864 2341.5

net income 4858.5

calculation of present net income of day care

particular amount amount

fee from day care 4800

less: cost to be incurred

license cost 18.75

cost of meal 576 594.75

net income 4205.25

From the above calculation relating to change in cost of daycare, it can be interpret that if

they employ more employees, they would need to incur an additional cost. Although, with new

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

employees, Franks would be able to serve more children, with the same context, it would

increase a license cost of the company.

Furthermore, by netting all the additional incomes and expenses, it can be interpret that

Franks should employ the new employees as it would result in enhancement of total income of

the Franks

5. Calculation to be used to take decision regarding number of children to be accepted and

number of employee to be hired

calculation of net earnings of day care if they cares 6 children

particular amount amount

fee from day care 7200

less: cost to be incurred

license cost 18.75

cost of new license 18.75

employment cost 1440

cost of meal 864

insurance 320 2661.5

net income 4538.5

calculation of present net income of day care if they care for 9 child

particular amount amount

fee from day care 4800

less: cost to be incurred

license cost 18.75

cost of meal 576 594.75

net income 4205.25

calculation of net earnings of day care by caring for 14 children

particular amount amount

fee from day care 11200

5

increase a license cost of the company.

Furthermore, by netting all the additional incomes and expenses, it can be interpret that

Franks should employ the new employees as it would result in enhancement of total income of

the Franks

5. Calculation to be used to take decision regarding number of children to be accepted and

number of employee to be hired

calculation of net earnings of day care if they cares 6 children

particular amount amount

fee from day care 7200

less: cost to be incurred

license cost 18.75

cost of new license 18.75

employment cost 1440

cost of meal 864

insurance 320 2661.5

net income 4538.5

calculation of present net income of day care if they care for 9 child

particular amount amount

fee from day care 4800

less: cost to be incurred

license cost 18.75

cost of meal 576 594.75

net income 4205.25

calculation of net earnings of day care by caring for 14 children

particular amount amount

fee from day care 11200

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

less: cost to be incurred

license cost 18.75

cost of new license 37.5

employment cost 4320

cost of meal 864

utility cost 125

rent 650

insurance 416.66 6431.91

net income 4768.08

Interpretation:

From the interpretation of the above calculation, it can be interpret that with the change

in number of children to be served by the day care, all the variable costs will be change. Further,

with the increase in number of child, the company would need to incur several extra costs like,

cost of employing extra employees, cost of rent, in case, they serves 14 children, cost of taking

more license, etc. further, it would also result in earning extra income from the serving fee of

children. From the interpretation of above calculation, it can be interpret that, the Frank would

earn the maximum income by serving 14 children.

Further, the in case if they serves 14 children, they would need to employ 3 more

employees. In addition, it would also need to incur additional rental expenses and insurance

expenses as well.

PART B

1. Identification of components of management accounting system

Managerial accounting primarily revolves around three basic components that are:

planning,

controlling

decision making

Almost all the companies around the world have their requirement based on these

components right from the very beginning (Nartey, 2018). The Cannon applied the components

of managerial accounting it decided to venture into different business other then camera industry

which was mini copier machines. For example, the top management of the company consisted

6

license cost 18.75

cost of new license 37.5

employment cost 4320

cost of meal 864

utility cost 125

rent 650

insurance 416.66 6431.91

net income 4768.08

Interpretation:

From the interpretation of the above calculation, it can be interpret that with the change

in number of children to be served by the day care, all the variable costs will be change. Further,

with the increase in number of child, the company would need to incur several extra costs like,

cost of employing extra employees, cost of rent, in case, they serves 14 children, cost of taking

more license, etc. further, it would also result in earning extra income from the serving fee of

children. From the interpretation of above calculation, it can be interpret that, the Frank would

earn the maximum income by serving 14 children.

Further, the in case if they serves 14 children, they would need to employ 3 more

employees. In addition, it would also need to incur additional rental expenses and insurance

expenses as well.

PART B

1. Identification of components of management accounting system

Managerial accounting primarily revolves around three basic components that are:

planning,

controlling

decision making

Almost all the companies around the world have their requirement based on these

components right from the very beginning (Nartey, 2018). The Cannon applied the components

of managerial accounting it decided to venture into different business other then camera industry

which was mini copier machines. For example, the top management of the company consisted

6

a team of 8 people belonging to different department for determining the cost and reliability

relationship of mini copier. At this stage, management accounting helped the company in

deciding what would be the best process of producing and designing the mini copier which is

cost effective, requires less service and maintenance. Management accounting helped it in

undertaking its one of the most revolutionised program called as cost reliability improvement

which has made the organisation as one of the most popular innovator of all time.

Another company Apple Computer, Inc. after the failures of its two products Lisa and

Apple II , it came with a product called as Macintosh, a low cost personal computer for the

public. Although, the company did not use completely original technology for the new product

but it made the product available to the public at insanely lower prices. This was achieved with

the help of management accounting within the organization. The cost accounting helped the

company in analysing and interpreting the cost and benefits of producing personal computer at

the most competitive prices and selling them in the market. This made Apple extremely popular

in the world and is now of the big 4 technology company of the world (Towards a new theory of

innovation management: A case study comparing Canon, Inc. and Apple Computer, Inc., 1991).

According to Kothari (2019) management accounting is based on the intuitive decision

making and is subject to personal bias of the managers. This means that analysis and

interpretation of the information depends completely upon the capability of interpreted and

business analyst which could affect the effectiveness of the management accounting as a

decision making tool. For example, Steve jobs took decisions based on personal bias when he

decided against providing the expansion slots on the Mac- original which would have allowed

third party vendors to develop an add on equipment.

2.Explanation of how management accounting contributes to the innovation process

In the article, innovation has been described as the information creation process that

develops due to the social interactions. Management accounting is of utmost significance to the

innovation process because whenever a new process or product is developed or any idea has

been conceived of developing new product, then various costs are incurred related to research,

designing, feasibilities studies, etc., for which budgets are prepared and according to which the

activities are undertaken.

Above all, the problem solving and decision making is done by the help of management

accounting. This field of accounting helps an organisation in determining what amount of

7

relationship of mini copier. At this stage, management accounting helped the company in

deciding what would be the best process of producing and designing the mini copier which is

cost effective, requires less service and maintenance. Management accounting helped it in

undertaking its one of the most revolutionised program called as cost reliability improvement

which has made the organisation as one of the most popular innovator of all time.

Another company Apple Computer, Inc. after the failures of its two products Lisa and

Apple II , it came with a product called as Macintosh, a low cost personal computer for the

public. Although, the company did not use completely original technology for the new product

but it made the product available to the public at insanely lower prices. This was achieved with

the help of management accounting within the organization. The cost accounting helped the

company in analysing and interpreting the cost and benefits of producing personal computer at

the most competitive prices and selling them in the market. This made Apple extremely popular

in the world and is now of the big 4 technology company of the world (Towards a new theory of

innovation management: A case study comparing Canon, Inc. and Apple Computer, Inc., 1991).

According to Kothari (2019) management accounting is based on the intuitive decision

making and is subject to personal bias of the managers. This means that analysis and

interpretation of the information depends completely upon the capability of interpreted and

business analyst which could affect the effectiveness of the management accounting as a

decision making tool. For example, Steve jobs took decisions based on personal bias when he

decided against providing the expansion slots on the Mac- original which would have allowed

third party vendors to develop an add on equipment.

2.Explanation of how management accounting contributes to the innovation process

In the article, innovation has been described as the information creation process that

develops due to the social interactions. Management accounting is of utmost significance to the

innovation process because whenever a new process or product is developed or any idea has

been conceived of developing new product, then various costs are incurred related to research,

designing, feasibilities studies, etc., for which budgets are prepared and according to which the

activities are undertaken.

Above all, the problem solving and decision making is done by the help of management

accounting. This field of accounting helps an organisation in determining what amount of

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

resources should be funnelled in a particular project. Innovation by the both the companies

along with the application of management accounting which helped them in surviving for so

long in the market. The decisions regarding the production and selling of mini copier and

Macintosh personal computers was formed explicitly by considering their costs and profits that

would be generated by incurring those costs. For example, Apple's CEO decided that most of its

resources should be put into development and production of Macintosh while the top

management of Cannon were of view that homogeneous structure should be maintained in

organisation. The innovation in Cannon in the form of new version of established product for a

larger market whereas Apple took forward the technology in terms of personal computers.

Thus, it can be said that management accounting helped both the company in taking

rationale decisions for their respective businesses which in turn made them cost effective and

cost efficient. Management accounting helps managers right from the planning stage of

developing new product till the controlling stage where it is monitored by the way of estimated

figures and budgets.

According to Quinn and Hiebl, (2018) undertaking innovation process is not as smooth

as it seems. It involves great expenditure for conducting decisions, various studies are to be

conducted, numerous trial and errors occur before mangers decides to launch a new process or

product. The information creating process is insanely time consuming process which could have

serious effects on the other core operations of an organisation. It may result into vanishing up

scare resources for developing something which could not be sell in the market. Business risk

and financial risk are two things which are kept at stake for producing new innovative products.

3. Findings from the journal articles that could management accountant

One thing that management accountant can learn from the Apple company is that clear

and well defined leadership of Steve Jobs who had the vision of creating something insanely

new. The CEO was convinced and analysed the market the situations perfectly which allowed

him to invest more of company's resources in Mac project.

This quality could be adopted by the management accountant while analysing and

interpreting the cost related data with more precision which could help it in drawing more

effective conclusions. This means that reports communicated by the management accountant

would help the management in taking more rationale and optimum decisions for the business.

8

along with the application of management accounting which helped them in surviving for so

long in the market. The decisions regarding the production and selling of mini copier and

Macintosh personal computers was formed explicitly by considering their costs and profits that

would be generated by incurring those costs. For example, Apple's CEO decided that most of its

resources should be put into development and production of Macintosh while the top

management of Cannon were of view that homogeneous structure should be maintained in

organisation. The innovation in Cannon in the form of new version of established product for a

larger market whereas Apple took forward the technology in terms of personal computers.

Thus, it can be said that management accounting helped both the company in taking

rationale decisions for their respective businesses which in turn made them cost effective and

cost efficient. Management accounting helps managers right from the planning stage of

developing new product till the controlling stage where it is monitored by the way of estimated

figures and budgets.

According to Quinn and Hiebl, (2018) undertaking innovation process is not as smooth

as it seems. It involves great expenditure for conducting decisions, various studies are to be

conducted, numerous trial and errors occur before mangers decides to launch a new process or

product. The information creating process is insanely time consuming process which could have

serious effects on the other core operations of an organisation. It may result into vanishing up

scare resources for developing something which could not be sell in the market. Business risk

and financial risk are two things which are kept at stake for producing new innovative products.

3. Findings from the journal articles that could management accountant

One thing that management accountant can learn from the Apple company is that clear

and well defined leadership of Steve Jobs who had the vision of creating something insanely

new. The CEO was convinced and analysed the market the situations perfectly which allowed

him to invest more of company's resources in Mac project.

This quality could be adopted by the management accountant while analysing and

interpreting the cost related data with more precision which could help it in drawing more

effective conclusions. This means that reports communicated by the management accountant

would help the management in taking more rationale and optimum decisions for the business.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Another lesson that could help a management accountant is to avoid personal biasses

while taking decisions. Apple's former CEO Steve Jobs when decided against providing

expansion slots in his products which could allow other to produce an add on equipment. Thus, a

management accountant should not allow its personal judgement and biasses that could affect the

decisions adversely as such actions can significantly affect the growth of the business (Towards

a new theory of innovation management: A case study comparing Canon, Inc. and Apple

Computer, Inc. 1991).

There are certain things from he Cannon which could help a management accountant in

its professional life. One of the thing is Cannon's top management was more concerned with the

clear and well defined structure should prevail in the organisation. This is necessary for effective

communication within the company as well such well defined structure increases the efficiency

of operations of firm.

Another impressive thing that Cannon applied while undertaking the project of Mini

Copier MC is its comprehensive problem solving approach. For producing a cost effective MC it

formed a team of 8 people belonging to different department from the inputs of which , the

company was able take more rationale decision. The problem of producing the MC with lowest

cost was able to be solved when the inputs were taken in which it was said that entire drum could

be discarded. This thought was processed further by design team which helped the company in

producing inexpensive MC.

From this, two things can be learned by a management accountant. First, is that it should

always use different ways of solving the problem by involving people from different level in the

department so that better decision could be taken by the management accountant. Another thing

which could be learned by the management accountant is that it should be creative in its

approach as well as it should promote the same while working with the people in an

organisation. The ability to work in a team could be learned by the management accountant by

watching how Cannon's top management involved people in their decision making regarding the

development of new product called as Mini Copier.

CONCLUSION

From the above project report, it can be summarised as that management accounting is

the system where managers uses the accounting information to facilitate themselves for the better

decision making. The main objective of management accounting is to help the managers in

9

while taking decisions. Apple's former CEO Steve Jobs when decided against providing

expansion slots in his products which could allow other to produce an add on equipment. Thus, a

management accountant should not allow its personal judgement and biasses that could affect the

decisions adversely as such actions can significantly affect the growth of the business (Towards

a new theory of innovation management: A case study comparing Canon, Inc. and Apple

Computer, Inc. 1991).

There are certain things from he Cannon which could help a management accountant in

its professional life. One of the thing is Cannon's top management was more concerned with the

clear and well defined structure should prevail in the organisation. This is necessary for effective

communication within the company as well such well defined structure increases the efficiency

of operations of firm.

Another impressive thing that Cannon applied while undertaking the project of Mini

Copier MC is its comprehensive problem solving approach. For producing a cost effective MC it

formed a team of 8 people belonging to different department from the inputs of which , the

company was able take more rationale decision. The problem of producing the MC with lowest

cost was able to be solved when the inputs were taken in which it was said that entire drum could

be discarded. This thought was processed further by design team which helped the company in

producing inexpensive MC.

From this, two things can be learned by a management accountant. First, is that it should

always use different ways of solving the problem by involving people from different level in the

department so that better decision could be taken by the management accountant. Another thing

which could be learned by the management accountant is that it should be creative in its

approach as well as it should promote the same while working with the people in an

organisation. The ability to work in a team could be learned by the management accountant by

watching how Cannon's top management involved people in their decision making regarding the

development of new product called as Mini Copier.

CONCLUSION

From the above project report, it can be summarised as that management accounting is

the system where managers uses the accounting information to facilitate themselves for the better

decision making. The main objective of management accounting is to help the managers in

9

planning, decision making and controlling by identifying early signs of problems. The report

also concluded that there are different types of costs in a business such as fixed costs, variable

costs, opportunity cost which means the cost of next best possible alternative, direct and indirect

costs. All these costs are taken into consideration while forming a rationale decisions for the

business. Further, in the report it was also concluded that there are some information which is

relevant and some which is irrelevant. Irrelevant information should be ignored for reaching

more effective conclusions. In other section of the report, it was summarised that management

accountant shall have problem solving skills, it must analyse and interprets cost related data with

highest precision, shall avoid personal biasses in taking decisions.

10

also concluded that there are different types of costs in a business such as fixed costs, variable

costs, opportunity cost which means the cost of next best possible alternative, direct and indirect

costs. All these costs are taken into consideration while forming a rationale decisions for the

business. Further, in the report it was also concluded that there are some information which is

relevant and some which is irrelevant. Irrelevant information should be ignored for reaching

more effective conclusions. In other section of the report, it was summarised that management

accountant shall have problem solving skills, it must analyse and interprets cost related data with

highest precision, shall avoid personal biasses in taking decisions.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.