Managerial Accounting Report

VerifiedAdded on 2020/12/09

|15

|3964

|400

Report

AI Summary

This report examines the importance of budgeting in business organizations, analyzing two articles that explore traditional and public sector budgeting. It highlights the similarities and differences between the approaches, emphasizing the role of management in achieving organizational goals. The report concludes that budgeting remains a crucial tool for planning, controlling, and achieving business objectives in today's dynamic environment.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGERIAL

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY ..................................................................................................................................1

Preparation of report on budgeting.........................................................................................1

A. Budgeting...........................................................................................................................1

B. Purpose of both article and research questions set out in them........................................3

C. Similarities and differences between findings from article..............................................4

D. Outcomes learned from both articles.................................................................................6

CONCLUSION ...............................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

MAIN BODY ..................................................................................................................................1

Preparation of report on budgeting.........................................................................................1

A. Budgeting...........................................................................................................................1

B. Purpose of both article and research questions set out in them........................................3

C. Similarities and differences between findings from article..............................................4

D. Outcomes learned from both articles.................................................................................6

CONCLUSION ...............................................................................................................................7

REFERENCES................................................................................................................................8

EXECUTIVE SUMMERY

Managerial accounting, also known as cost accounting; is a process of determination of

significant information, its analysis and evaluation to provide mangers of the organisation with

relevant data for attainment of business goals. The process involves development of a effective

plan in order to ensure efficient utilisation of resources. A plan ca not work ll alone so controllin

is also required to monitor maximum utilisation of resources. The purpose of study 1 is that there

are several controversies regarding the use of traditional budgeting in business organisation be

public or private. The main purpose of study 2 is reviewing the administration, management and

contribution of accounting in current budgeting theories. The focus of Study 1 was on the

planning of income and expenditure. Main objective is to provide with certain tools and

techniques to define how income generated must be allocated for existing expenditure, so a part

of it can be left as savings.

Managerial accounting, also known as cost accounting; is a process of determination of

significant information, its analysis and evaluation to provide mangers of the organisation with

relevant data for attainment of business goals. The process involves development of a effective

plan in order to ensure efficient utilisation of resources. A plan ca not work ll alone so controllin

is also required to monitor maximum utilisation of resources. The purpose of study 1 is that there

are several controversies regarding the use of traditional budgeting in business organisation be

public or private. The main purpose of study 2 is reviewing the administration, management and

contribution of accounting in current budgeting theories. The focus of Study 1 was on the

planning of income and expenditure. Main objective is to provide with certain tools and

techniques to define how income generated must be allocated for existing expenditure, so a part

of it can be left as savings.

INTRODUCTION

Managerial accounting, also termed as cost accounting is one of the most important and

integral part of account system of an organisation. It can be defined as a process of identifying,

measuring, analysing, interpreting financial information and communicating it to management

of firm to achieve business goals. In the present report management accounting tool Budgeting

is chosen and its details and relevance in an enterprise is discussed. This report is based on study

of two articles related with relevance and significance of budgeting in organisation. In this

implication and use of traditional budgeting method in present time is discussed with reflecting

the changes over years.

MAIN BODY

Preparation of report on budgeting

A. Budgeting

Money and time are two important resources of an organisation. This is a process related

with formulation of a plan for use of these resources effectively and efficiently. Planning all

alone cannot serve the purpose of effective utilisation hence, controlling is also very crucial for

efficient implementation of plan (Van der Stede, 2015). Budgets is a tool which is used by

manager for planning and controlling of limited resources available with the organisation. A

budget reflects objectives of the company and how management will proceed to achieve those

goals of firm.

Budgeting for activities of a business generally includes

Formulation of approximate computation of future sales

preparation of estimate of future cash collection and disbursement

planning for computation of future day to day activities of organisation

summarizing these calculations into an income statement and balance sheet.

Budgeting is a process which is chronological in nature and it comprises different

budgets. All of them are prepared and classified as per methods and techniques used for

generation and disbursement of money in the organisation. Some budgets are concerned with

sales, purchase, factory cost etc. while some are prepared for directing matters related with

investment and forecasting productivity and performance of company. In budgeting; budget

holds a very important part as they are the first step of planning in process.

1

Managerial accounting, also termed as cost accounting is one of the most important and

integral part of account system of an organisation. It can be defined as a process of identifying,

measuring, analysing, interpreting financial information and communicating it to management

of firm to achieve business goals. In the present report management accounting tool Budgeting

is chosen and its details and relevance in an enterprise is discussed. This report is based on study

of two articles related with relevance and significance of budgeting in organisation. In this

implication and use of traditional budgeting method in present time is discussed with reflecting

the changes over years.

MAIN BODY

Preparation of report on budgeting

A. Budgeting

Money and time are two important resources of an organisation. This is a process related

with formulation of a plan for use of these resources effectively and efficiently. Planning all

alone cannot serve the purpose of effective utilisation hence, controlling is also very crucial for

efficient implementation of plan (Van der Stede, 2015). Budgets is a tool which is used by

manager for planning and controlling of limited resources available with the organisation. A

budget reflects objectives of the company and how management will proceed to achieve those

goals of firm.

Budgeting for activities of a business generally includes

Formulation of approximate computation of future sales

preparation of estimate of future cash collection and disbursement

planning for computation of future day to day activities of organisation

summarizing these calculations into an income statement and balance sheet.

Budgeting is a process which is chronological in nature and it comprises different

budgets. All of them are prepared and classified as per methods and techniques used for

generation and disbursement of money in the organisation. Some budgets are concerned with

sales, purchase, factory cost etc. while some are prepared for directing matters related with

investment and forecasting productivity and performance of company. In budgeting; budget

holds a very important part as they are the first step of planning in process.

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

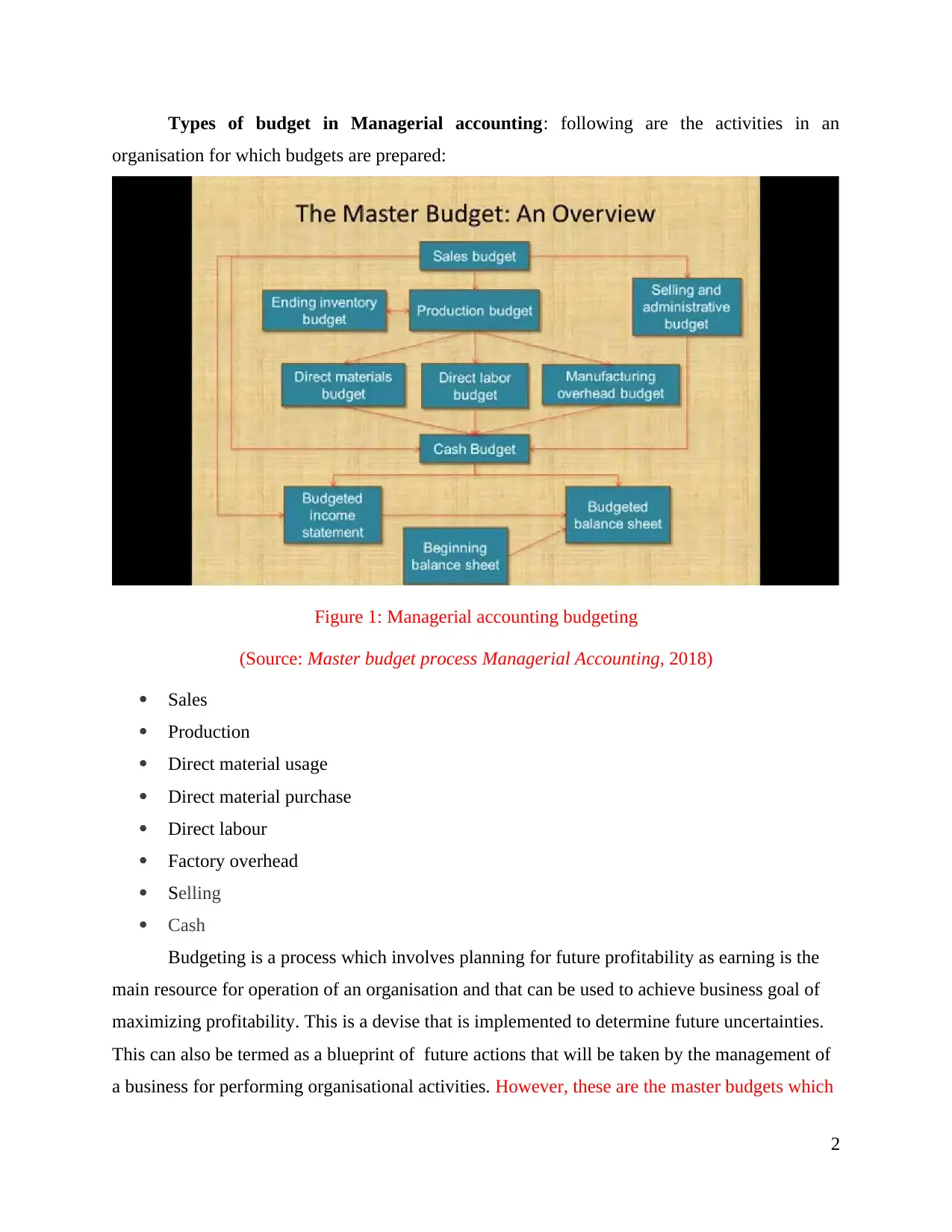

Types of budget in Managerial accounting: following are the activities in an

organisation for which budgets are prepared:

Figure 1: Managerial accounting budgeting

(Source: Master budget process Managerial Accounting, 2018)

Sales

Production

Direct material usage

Direct material purchase

Direct labour

Factory overhead

Selling

Cash

Budgeting is a process which involves planning for future profitability as earning is the

main resource for operation of an organisation and that can be used to achieve business goal of

maximizing profitability. This is a devise that is implemented to determine future uncertainties.

This can also be termed as a blueprint of future actions that will be taken by the management of

a business for performing organisational activities. However, these are the master budgets which

2

organisation for which budgets are prepared:

Figure 1: Managerial accounting budgeting

(Source: Master budget process Managerial Accounting, 2018)

Sales

Production

Direct material usage

Direct material purchase

Direct labour

Factory overhead

Selling

Cash

Budgeting is a process which involves planning for future profitability as earning is the

main resource for operation of an organisation and that can be used to achieve business goal of

maximizing profitability. This is a devise that is implemented to determine future uncertainties.

This can also be termed as a blueprint of future actions that will be taken by the management of

a business for performing organisational activities. However, these are the master budgets which

2

will be helpful in predicting expenses that will be incurred in the future. Level of funds that

will be required by business for meeting such costs. Thus, it benefits the organisation in making

pre-planned development tactics to resolve future risks. Hence, sales, cash and various relevant

budgetary techniques will be assistive for enhancing the internal efficiencies of an entity.

Importance of budgets

1. operating plans for the coming periods for managers: how activities will be carried out

and implementation plans will be done.

2. Preparation of management’s plans in quantitative terms: the level of activities it want to

achieve with ethical and moral approach (Savic, Vasiljevic and Popovic, 2016).

3. forces all levels of management to think about future performances, anticipate results,

take action and measures to correct possible poor results; and

4. motivating individuals and employees to strive to achieve pre-determined business goals.

Functions of budgeting:

1. Forecasting: the main task of budgeting is to forecast future performances. These are the

targets set, that an organisation think it should achieve. Forecasting is a complex exercise

that requires to take into consideration many factors related with firm. This can be

defined as ascertainment of future task that business is required to achieve in order to

ensure growth and profitability along with long run sustainability.

2. Planning: it depends on forecasting that has been done in past for making future

decisions (Budgeting: what are the functions of budgeting, 2018). Under this data

generated under forecasting are used to make plans so that set target can be achieved

through a proper planning. Planning is done on the basis of data which is forecasted by

the management as formulation of a path through which the data so determined under

forecasting can be attained.

3. Communication: this can be bifurcated into two parts :- one gathering of information

about competitors and activities and another dissemination of information when budgets

are not acted upon. Information related with competitor is very importance as through

this their future approach and present performance can be determined which ultimately

help in development of strategies.

4. Motivation: this is a driving force which encourages people to run toweards achievement

of organisational goals. Budgeting facilitates this through determination of two facts,

3

will be required by business for meeting such costs. Thus, it benefits the organisation in making

pre-planned development tactics to resolve future risks. Hence, sales, cash and various relevant

budgetary techniques will be assistive for enhancing the internal efficiencies of an entity.

Importance of budgets

1. operating plans for the coming periods for managers: how activities will be carried out

and implementation plans will be done.

2. Preparation of management’s plans in quantitative terms: the level of activities it want to

achieve with ethical and moral approach (Savic, Vasiljevic and Popovic, 2016).

3. forces all levels of management to think about future performances, anticipate results,

take action and measures to correct possible poor results; and

4. motivating individuals and employees to strive to achieve pre-determined business goals.

Functions of budgeting:

1. Forecasting: the main task of budgeting is to forecast future performances. These are the

targets set, that an organisation think it should achieve. Forecasting is a complex exercise

that requires to take into consideration many factors related with firm. This can be

defined as ascertainment of future task that business is required to achieve in order to

ensure growth and profitability along with long run sustainability.

2. Planning: it depends on forecasting that has been done in past for making future

decisions (Budgeting: what are the functions of budgeting, 2018). Under this data

generated under forecasting are used to make plans so that set target can be achieved

through a proper planning. Planning is done on the basis of data which is forecasted by

the management as formulation of a path through which the data so determined under

forecasting can be attained.

3. Communication: this can be bifurcated into two parts :- one gathering of information

about competitors and activities and another dissemination of information when budgets

are not acted upon. Information related with competitor is very importance as through

this their future approach and present performance can be determined which ultimately

help in development of strategies.

4. Motivation: this is a driving force which encourages people to run toweards achievement

of organisational goals. Budgeting facilitates this through determination of two facts,

3

one; how to make employees follow budgets and second; setting the difficulty level of

budgeting.

5. Evaluation: this means to compare something with a set standard of that thing. In

budgets target performances are set down and they are compared with actual performance

of the business (Smith, 2015). Through it can be easily found out that whether targets

have been achieved or not, and if not, reasons for the same are also determined.

6. Controlling and coordination: this simply means that there is proper communication

among different departments of the organisation and all are well informed about goals

and targets to be achieved. Controlling is done through timely evaluation of performances

and set goals and level of difference in performance is determined. Measures are applied

so that goals can be achieved on time.

7. Authorisation: through budgeting mispronunciation is minimized and mangers are made

more responsible about amount and place of their spending related with business. Manges

are made more responsible for their actions taken in relation to organisation, this ensures

that every act undertaken is for benefit and development of the business.

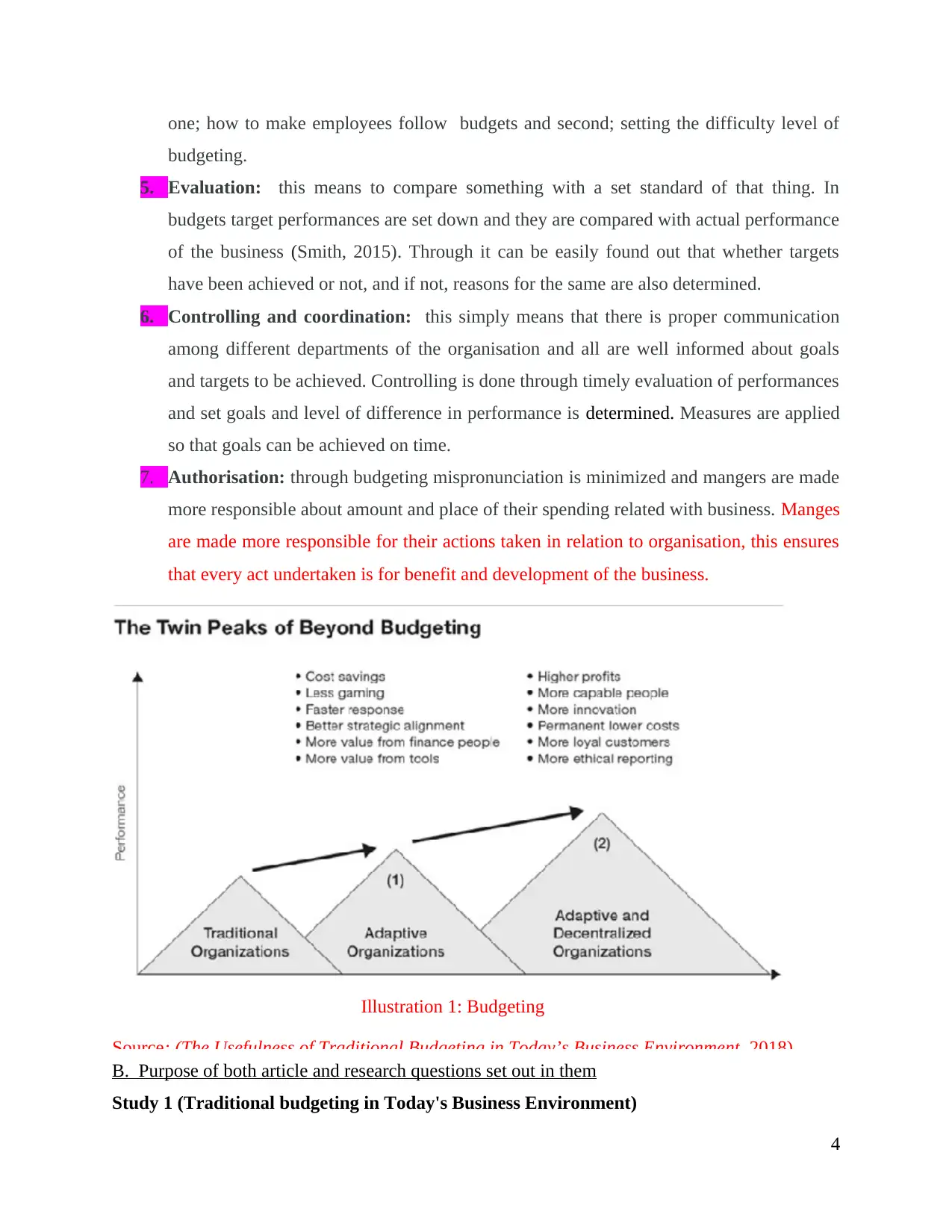

Illustration 1: Budgeting

Source: (The Usefulness of Traditional Budgeting in Today’s Business Environment, 2018)

B. Purpose of both article and research questions set out in them

Study 1 (Traditional budgeting in Today's Business Environment)

4

budgeting.

5. Evaluation: this means to compare something with a set standard of that thing. In

budgets target performances are set down and they are compared with actual performance

of the business (Smith, 2015). Through it can be easily found out that whether targets

have been achieved or not, and if not, reasons for the same are also determined.

6. Controlling and coordination: this simply means that there is proper communication

among different departments of the organisation and all are well informed about goals

and targets to be achieved. Controlling is done through timely evaluation of performances

and set goals and level of difference in performance is determined. Measures are applied

so that goals can be achieved on time.

7. Authorisation: through budgeting mispronunciation is minimized and mangers are made

more responsible about amount and place of their spending related with business. Manges

are made more responsible for their actions taken in relation to organisation, this ensures

that every act undertaken is for benefit and development of the business.

Illustration 1: Budgeting

Source: (The Usefulness of Traditional Budgeting in Today’s Business Environment, 2018)

B. Purpose of both article and research questions set out in them

Study 1 (Traditional budgeting in Today's Business Environment)

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The purpose of this study is that there are several controversies regarding the use of

traditional budgeting in business organisation be public or private. Study provides in depth

conceptual meaning of traditional budgeting with examination of income and expenditure for

developing framework to provide an understanding of it. This study focuses purely on following

the traditional methods of budgeting used in organisation and its relevance in present times. It is

given that in traditional approach business organisation put more emphasis on the allocation of

income generated to the expenses and cost incurred in business activities.

Study 2 (Public sector budgeting: A European review of

accounting and public management journals)

In public organisation budgeting is of central importance. Reason behind choosing this

topic for study is that the subject is multifaceted and provides a wide scope of research. This

requires a profound assessment of changes in institutional and socio economic landscape related

with roles and features in accounting study (Anessi-Pessina and et.al., 2016). The main purpose

of this study is reviewing the administration, management and contribution of accounting in

current budgeting theories and its use. Proposals are presented on how this can contribute in the

future. This study kept its focus on the fact that budgeting is not limited to allocation rather it

involves role of management in this process. Managers of a business organisation play a vital

role in attainment of set objectives.

Research questions stated in studies are:

Study 1

1. Determination of importance of traditional budgeting in present time?

2. Conceptual development of functional frame work of budgeting.

3. Presentation of alternatives to traditional budgeting.

4. Impact and influence of traditional budgeting on organisational culture.

Study 2

1. An investigation is set out for reviewing public budgeting as a tool to regulate relation in

the organisation.

2. Different roles of budgeting in an organisation is determined with identification of its

accountability function.

3. Methods employed in budgeting research

4. To find out gaps and future research approaches

5

traditional budgeting in business organisation be public or private. Study provides in depth

conceptual meaning of traditional budgeting with examination of income and expenditure for

developing framework to provide an understanding of it. This study focuses purely on following

the traditional methods of budgeting used in organisation and its relevance in present times. It is

given that in traditional approach business organisation put more emphasis on the allocation of

income generated to the expenses and cost incurred in business activities.

Study 2 (Public sector budgeting: A European review of

accounting and public management journals)

In public organisation budgeting is of central importance. Reason behind choosing this

topic for study is that the subject is multifaceted and provides a wide scope of research. This

requires a profound assessment of changes in institutional and socio economic landscape related

with roles and features in accounting study (Anessi-Pessina and et.al., 2016). The main purpose

of this study is reviewing the administration, management and contribution of accounting in

current budgeting theories and its use. Proposals are presented on how this can contribute in the

future. This study kept its focus on the fact that budgeting is not limited to allocation rather it

involves role of management in this process. Managers of a business organisation play a vital

role in attainment of set objectives.

Research questions stated in studies are:

Study 1

1. Determination of importance of traditional budgeting in present time?

2. Conceptual development of functional frame work of budgeting.

3. Presentation of alternatives to traditional budgeting.

4. Impact and influence of traditional budgeting on organisational culture.

Study 2

1. An investigation is set out for reviewing public budgeting as a tool to regulate relation in

the organisation.

2. Different roles of budgeting in an organisation is determined with identification of its

accountability function.

3. Methods employed in budgeting research

4. To find out gaps and future research approaches

5

C. Similarities and differences between findings from article

Similarities between two studies

Budgeting is so far considered as crucial in every organisation. The focus of Study 1 was

on the planning of income and expenditure (Public sector budgeting: a European review

ofaccounting and public management journal, 2018). Main aim was to provide with certain tools

and techniques to define how income generated must be allocated for existing expenditure, so a

part of it can be left as savings. Study 2 also share same view as study 1 that budging plays a

crucial role in a public as well as private organisation. Traditionally, budgeting has been a

process of deciding how much to spend and on what along with determining limit of expenses

with available income.

As per this study 1 Budgets preparation is very common for all business organisation as

it facilitates achievement of business goals. These are of key importance for a firm to ensure its

survival from development of budgets to the stage of its effective implementation. This was

supported by views presented in study 2 that budgeting has an extended role to perform roles and

functions which enforces managerial responsibilities and assertion of external accountability.

Traditional budgeting is significant for business as it provides a link of communication between

management and other departments in firm where revenue and cost related with future operations

and activities are planned and forecasted. Interpretive approaches in study 2 conversely defines

budgeting as accounting systems, far from being neutral and objective processes and tools. It

belongs to the organizational and

societal reality reflection and are affected by institutional variables and, in turn, effect them,

contributing to rationalization and legitimation processes.

According to study 1 budging in traditional way includes 3 steps in its processes stated as

creation, follow up and analysis. It clearly creates opportunities for development and growth of

staff and provides a firm base for quick decision making processes. The same thing is

represented in study 2 just in different words, according to it budgeting plays different roles as

classification of allocative, managerial and accounting functions so that management carry out

its actions significantly.

Frame work of budgeting is defined in study 1 as organisational planning, performance

evaluation, goal communication and formation of strategy. All these together provides a map to

how budgeting must be formulated and implemented in organisation. As stated in study 2

6

Similarities between two studies

Budgeting is so far considered as crucial in every organisation. The focus of Study 1 was

on the planning of income and expenditure (Public sector budgeting: a European review

ofaccounting and public management journal, 2018). Main aim was to provide with certain tools

and techniques to define how income generated must be allocated for existing expenditure, so a

part of it can be left as savings. Study 2 also share same view as study 1 that budging plays a

crucial role in a public as well as private organisation. Traditionally, budgeting has been a

process of deciding how much to spend and on what along with determining limit of expenses

with available income.

As per this study 1 Budgets preparation is very common for all business organisation as

it facilitates achievement of business goals. These are of key importance for a firm to ensure its

survival from development of budgets to the stage of its effective implementation. This was

supported by views presented in study 2 that budgeting has an extended role to perform roles and

functions which enforces managerial responsibilities and assertion of external accountability.

Traditional budgeting is significant for business as it provides a link of communication between

management and other departments in firm where revenue and cost related with future operations

and activities are planned and forecasted. Interpretive approaches in study 2 conversely defines

budgeting as accounting systems, far from being neutral and objective processes and tools. It

belongs to the organizational and

societal reality reflection and are affected by institutional variables and, in turn, effect them,

contributing to rationalization and legitimation processes.

According to study 1 budging in traditional way includes 3 steps in its processes stated as

creation, follow up and analysis. It clearly creates opportunities for development and growth of

staff and provides a firm base for quick decision making processes. The same thing is

represented in study 2 just in different words, according to it budgeting plays different roles as

classification of allocative, managerial and accounting functions so that management carry out

its actions significantly.

Frame work of budgeting is defined in study 1 as organisational planning, performance

evaluation, goal communication and formation of strategy. All these together provides a map to

how budgeting must be formulated and implemented in organisation. As stated in study 2

6

allocative budgets set out overall spending, managerial functions are related with assignment of

task and objectives and are made accountable for attainment of the same.

In study 1 budgeting is considered as a key component of management accounting in

most organisations. Regardless of many criticisms, stating that it is mere waste of time it is still

adopted and used religiously by many business as it facilitates planning, implementation and

execution of firm's objective. In study 2, for further understanding of application of budgeting in

organisation two more categories are added with allocative and managerial and accounting

functions, they are explicit theoretical and hybrid framework.

Further, both study 1 and 2, emphasis on the fact that budgeting is very important for an

organisation in attainment of business goals. Bot defied budgeting vital for attainment of set

objectives through planning and allocation of business resources along with implementation of

controlling activities.

Difference between two studies

Study 1 reflects use and application of traditional budgeting methods in an organisation

along with explaining the techniques used while study 2 considers budgeting allocations of costs

and delegation of responsibilities to mangers and making them accountable for achievement of

the set targets.

The focus of study 2 was on inter organisational aspects of budgeting emphasizing on its

managerial and allocative functions (Traditional Budgeting in Today’s Business Environment,

2018). It either adopte theoretical approach or donot consider it at all, rather rely on quantitative

analysis. In this study budgeting in organisation is not given much emphasized with respect to

its importance and significance in achievement of goals and targets pre-determined by firm. As

far as study one is concerned it purely considers budgeting as important part of the organisation

in its absolute manner.

Study 1 clearly specifies that traditional budgeting is related with determination of

income generated and allocation of expense from that financial gain. While, study 2 states that

with allocation of cost and the management becomes responsible for attainment of accounting

goals laid down in the budgets.

Moreover, it can be stated that traditional approach of budgeting kept its focus on

income, expense and it allocation, rather as per study two, in budgeting managers are held more

responsible for achievement of organisational goals. As per study 1, planing is carried out for

7

task and objectives and are made accountable for attainment of the same.

In study 1 budgeting is considered as a key component of management accounting in

most organisations. Regardless of many criticisms, stating that it is mere waste of time it is still

adopted and used religiously by many business as it facilitates planning, implementation and

execution of firm's objective. In study 2, for further understanding of application of budgeting in

organisation two more categories are added with allocative and managerial and accounting

functions, they are explicit theoretical and hybrid framework.

Further, both study 1 and 2, emphasis on the fact that budgeting is very important for an

organisation in attainment of business goals. Bot defied budgeting vital for attainment of set

objectives through planning and allocation of business resources along with implementation of

controlling activities.

Difference between two studies

Study 1 reflects use and application of traditional budgeting methods in an organisation

along with explaining the techniques used while study 2 considers budgeting allocations of costs

and delegation of responsibilities to mangers and making them accountable for achievement of

the set targets.

The focus of study 2 was on inter organisational aspects of budgeting emphasizing on its

managerial and allocative functions (Traditional Budgeting in Today’s Business Environment,

2018). It either adopte theoretical approach or donot consider it at all, rather rely on quantitative

analysis. In this study budgeting in organisation is not given much emphasized with respect to

its importance and significance in achievement of goals and targets pre-determined by firm. As

far as study one is concerned it purely considers budgeting as important part of the organisation

in its absolute manner.

Study 1 clearly specifies that traditional budgeting is related with determination of

income generated and allocation of expense from that financial gain. While, study 2 states that

with allocation of cost and the management becomes responsible for attainment of accounting

goals laid down in the budgets.

Moreover, it can be stated that traditional approach of budgeting kept its focus on

income, expense and it allocation, rather as per study two, in budgeting managers are held more

responsible for achievement of organisational goals. As per study 1, planing is carried out for

7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

allocation of limited resource and according to study 2, along with allocation management

control is also considered as important aspect.

Traditional budgeting European review

Focus on income and expenditure plan Focus on managerial and allocative functions.

Limited to traditional tools and techniques of

budgeting.

Expects budgeting to perform further role and

functions enforcing managerial responsibilities

and discharging external accountability.

Lacks flexibility and adaptability of

behavioural weakness of employees and

management of organisation.

Purely considers it as responsibility of

mangers to achieve organisational goals.

D. Outcomes learned from both articles

Outcomes

Study 1

1. The first outcome that can be abstracted from study one is that, traditional budgeting

cannot be taken as obsolete, broken, gratuitous that cannot be intensely supported. This is

supported with the argument that traditional budgeting is a base for establishment of control as

this builds extensive planning, coordination and motivation that encourages effective work

performance leading to achievement of business goals. This can be concluded from study 1 that,

budgeting is understood as a planning tool for attainment of organisational goal. For this, budgets

are prepared and implemented in organisation along with their evaluation. budgets are prepared

for major activities which are undertaken in business such as sales, purchases, inventory etc. As

discussed above in the report overall organisation planning is done with setting out of objectives

which are linked with future expectations. For example: - sales of a firm is forecasted at a level

higher than current year's sale. This means that units of product are estimated to be sold in the

period for which budgets is made. After this performance is evaluated and margin of deviation is

seen, means actual sales are compared with budgeted. Any discrepancy is measured and then

strategies are formulated to attain target goals.

2. Second learning from this study can be stated as budgeting is core of an organisation

and a measure for success of management. For every business this is highly recommended as it

8

control is also considered as important aspect.

Traditional budgeting European review

Focus on income and expenditure plan Focus on managerial and allocative functions.

Limited to traditional tools and techniques of

budgeting.

Expects budgeting to perform further role and

functions enforcing managerial responsibilities

and discharging external accountability.

Lacks flexibility and adaptability of

behavioural weakness of employees and

management of organisation.

Purely considers it as responsibility of

mangers to achieve organisational goals.

D. Outcomes learned from both articles

Outcomes

Study 1

1. The first outcome that can be abstracted from study one is that, traditional budgeting

cannot be taken as obsolete, broken, gratuitous that cannot be intensely supported. This is

supported with the argument that traditional budgeting is a base for establishment of control as

this builds extensive planning, coordination and motivation that encourages effective work

performance leading to achievement of business goals. This can be concluded from study 1 that,

budgeting is understood as a planning tool for attainment of organisational goal. For this, budgets

are prepared and implemented in organisation along with their evaluation. budgets are prepared

for major activities which are undertaken in business such as sales, purchases, inventory etc. As

discussed above in the report overall organisation planning is done with setting out of objectives

which are linked with future expectations. For example: - sales of a firm is forecasted at a level

higher than current year's sale. This means that units of product are estimated to be sold in the

period for which budgets is made. After this performance is evaluated and margin of deviation is

seen, means actual sales are compared with budgeted. Any discrepancy is measured and then

strategies are formulated to attain target goals.

2. Second learning from this study can be stated as budgeting is core of an organisation

and a measure for success of management. For every business this is highly recommended as it

8

defines goals and keep its focus on achievement of the targets. It is crucial to success,

development and growth of an enterprise. As budgets forecast future goals that organisation need

to attain, and in this process proper planning, implantation, analysis and selection of all activities

is done. Overall organisation face a scrutiny and its growth is ensured as budgets are set at

higher level as compared to current position and in case of discrepancy, reasons for the same are

found out and they are eliminated with application of controlling measure for attaining those set

targets.

Study 2

1. One outcome from this study is that budgeting is understudied and not many

researches are done in respect of focusing on the role of management in budgeting. Budgeting

is vital for an organisation and for point of research it is extremely multifaceted. As per this

study budgeting is remarkably under researched and under theorized. The main research of this

study was based on qualitative explanation. This study suggested that traditional budgeting

approaches are important and must be considered along with modern techniques. All the

approaches used in this article were based on theories stating that budgeting plays an important

role in development of a business but this topic have been not explored to a great extent. This

study stated that both modern and traditional approaches are equally important for business in

attainment of organisational goals. But relevance of both topics with each other have not yet

explored to a grate extent and it is under researched.

2. Another outcome from this study is that an interpretive background with a prevalence

of qualitative-explanatory studies; and to focus on the

managerial role of budgeting and making them accountable for attainment of organisational

goal. In this study it was concluded that with a qualitative approach mangers of the organisation

are held responsible for making budgets and to attain target goals of business. Allocation of cost

means determination of expenses related with each activity within organisation and preparation

of budgets for same. For achievement of the same managers are held accountable and

responsible to accomplish the budgeted targets. Managers are held responsible for their acts

taken under business operation and that must be in favour and benefit of the organisation. In ca

of any diversification from their business aim, they are the one who will be blamed as it is their

duty to endure attainment of set goals of firm.

9

development and growth of an enterprise. As budgets forecast future goals that organisation need

to attain, and in this process proper planning, implantation, analysis and selection of all activities

is done. Overall organisation face a scrutiny and its growth is ensured as budgets are set at

higher level as compared to current position and in case of discrepancy, reasons for the same are

found out and they are eliminated with application of controlling measure for attaining those set

targets.

Study 2

1. One outcome from this study is that budgeting is understudied and not many

researches are done in respect of focusing on the role of management in budgeting. Budgeting

is vital for an organisation and for point of research it is extremely multifaceted. As per this

study budgeting is remarkably under researched and under theorized. The main research of this

study was based on qualitative explanation. This study suggested that traditional budgeting

approaches are important and must be considered along with modern techniques. All the

approaches used in this article were based on theories stating that budgeting plays an important

role in development of a business but this topic have been not explored to a great extent. This

study stated that both modern and traditional approaches are equally important for business in

attainment of organisational goals. But relevance of both topics with each other have not yet

explored to a grate extent and it is under researched.

2. Another outcome from this study is that an interpretive background with a prevalence

of qualitative-explanatory studies; and to focus on the

managerial role of budgeting and making them accountable for attainment of organisational

goal. In this study it was concluded that with a qualitative approach mangers of the organisation

are held responsible for making budgets and to attain target goals of business. Allocation of cost

means determination of expenses related with each activity within organisation and preparation

of budgets for same. For achievement of the same managers are held accountable and

responsible to accomplish the budgeted targets. Managers are held responsible for their acts

taken under business operation and that must be in favour and benefit of the organisation. In ca

of any diversification from their business aim, they are the one who will be blamed as it is their

duty to endure attainment of set goals of firm.

9

CONCLUSION

From the above report it can be concluded that budgeting is an integral part of a business

organisation that can bot be separated from it. Budgeting process in a business can be referred as

quantifying objective of a firm that is achieved through preparation of various budgets. Further it

can be interpreted that for all activities undertaken in an organisation different budgets are

prepared and in this future performance targets are set out. In addition, it was also determined

that as per two articles both emphasize on importance of budgeting but study one is more

theatrical in nature and study two is more focused on qualitative approach that is responsibility

are given to mangers for achievement of goals. Lastly, report can be finished with statement, in

present world, budgeting tool can be used in most of the organisation irrespective of their size.

With implementation of this tool overall performance of organisation gets evaluated and

controlling measures can be applied for timely achievement of the goals.

10

From the above report it can be concluded that budgeting is an integral part of a business

organisation that can bot be separated from it. Budgeting process in a business can be referred as

quantifying objective of a firm that is achieved through preparation of various budgets. Further it

can be interpreted that for all activities undertaken in an organisation different budgets are

prepared and in this future performance targets are set out. In addition, it was also determined

that as per two articles both emphasize on importance of budgeting but study one is more

theatrical in nature and study two is more focused on qualitative approach that is responsibility

are given to mangers for achievement of goals. Lastly, report can be finished with statement, in

present world, budgeting tool can be used in most of the organisation irrespective of their size.

With implementation of this tool overall performance of organisation gets evaluated and

controlling measures can be applied for timely achievement of the goals.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Book and Journals:

Anessi-Pessina, E and et.al., 2016. Public sector budgeting: a European review of accounting

and public management journals. Accounting, Auditing & Accountability Journal. 29(3).

pp.491-519.

Savic, B., Vasiljevic, Z. and Popovic, N., 2016. THE ROLE AND IMPORTANCE OF

STRATEGIC BUDGETING FOR COMPETITIVENESS OF THE AGRIBUSINESS

SUPPLY CHAIN 1. Ekonomika Poljoprivrede. 63(1). p.295.

Smith, R. W., 2015. Budgeting: Ethics of. In Encyclopedia of Public Administration and Public

Policy-5 Volume Set. (pp. 1-7). Routledge.

Van der Stede, W. A., 2015. Budgeting and management control. Wiley Encyclopedia of

Management. pp.1-7.

Online:

Traditional Budgeting in Today’s Business Environment. 2018. [Pdf]. Available

through

:<https://search.proquest.com/business/docview/1898424070/6CC81E03AB8D4428PQ/1?

accountid=30552>.

Public sector budgeting: a European review of accounting and public management journals.

2018. [Pdf]. Available through

:<https://search.proquest.com/business/docview/2076271311/291666EFD2FB4E91PQ/1?

accountid=30552>.

Budgeting: what are the functions of budgeting. 2018. [Online]. Available through :<.

https://www.accountantnextdoor.com/budgeting-what-are-the-functions-of-budgeting/>

Master budget process Managerial Accounting. 2018. [Online]. Available through :<

https://www.youtube.com/watch?v=2Wbr7cScyOA >.

The Usefulness of Traditional Budgeting in Today’s Business Environment. 2018. [Online].

Available through :<http://www.turkishtaxnews.com/articles/the-usefulness-of-traditional-

budgeting-in-today-s-business-environment/

11

Book and Journals:

Anessi-Pessina, E and et.al., 2016. Public sector budgeting: a European review of accounting

and public management journals. Accounting, Auditing & Accountability Journal. 29(3).

pp.491-519.

Savic, B., Vasiljevic, Z. and Popovic, N., 2016. THE ROLE AND IMPORTANCE OF

STRATEGIC BUDGETING FOR COMPETITIVENESS OF THE AGRIBUSINESS

SUPPLY CHAIN 1. Ekonomika Poljoprivrede. 63(1). p.295.

Smith, R. W., 2015. Budgeting: Ethics of. In Encyclopedia of Public Administration and Public

Policy-5 Volume Set. (pp. 1-7). Routledge.

Van der Stede, W. A., 2015. Budgeting and management control. Wiley Encyclopedia of

Management. pp.1-7.

Online:

Traditional Budgeting in Today’s Business Environment. 2018. [Pdf]. Available

through

:<https://search.proquest.com/business/docview/1898424070/6CC81E03AB8D4428PQ/1?

accountid=30552>.

Public sector budgeting: a European review of accounting and public management journals.

2018. [Pdf]. Available through

:<https://search.proquest.com/business/docview/2076271311/291666EFD2FB4E91PQ/1?

accountid=30552>.

Budgeting: what are the functions of budgeting. 2018. [Online]. Available through :<.

https://www.accountantnextdoor.com/budgeting-what-are-the-functions-of-budgeting/>

Master budget process Managerial Accounting. 2018. [Online]. Available through :<

https://www.youtube.com/watch?v=2Wbr7cScyOA >.

The Usefulness of Traditional Budgeting in Today’s Business Environment. 2018. [Online].

Available through :<http://www.turkishtaxnews.com/articles/the-usefulness-of-traditional-

budgeting-in-today-s-business-environment/

11

12

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.