HI5017 Managerial Accounting: Case Studies & Journal Article Critique

VerifiedAdded on 2023/03/31

|11

|3524

|342

Case Study

AI Summary

This assignment provides a comprehensive analysis of managerial accounting principles through a case study and a journal article critique. The case study involves identifying different types of costs (fixed, variable, incremental, and sunk) and their relevance in decision-making, specifically concerning the purchase of appliances and the expansion of a daycare business. It evaluates various alternatives using incremental analysis and provides recommendations based on financial outcomes. The journal article critique focuses on the application of managerial accounting in innovation management, comparing Canon Inc. and Apple Computer Inc., and highlighting the importance of information sharing and effective management in achieving business goals. The assignment concludes with detailed calculations and recommendations for optimizing profitability and strategic decision-making.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student

Name of the University

Author’s Note

Managerial Accounting

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGERIAL ACCOUNTING

Table of Contents

Part A: Case Study Analysis....................................................................................................................2

Answer to 1.......................................................................................................................................2

Answer to 2.......................................................................................................................................2

Answer to 3.......................................................................................................................................3

Answer to 4.......................................................................................................................................3

Answer to 5.......................................................................................................................................4

Part B: Journal Article Critique...............................................................................................................5

Answer to 1.......................................................................................................................................5

Answer to 2.......................................................................................................................................6

Answer to 3.......................................................................................................................................7

References.............................................................................................................................................9

Table of Contents

Part A: Case Study Analysis....................................................................................................................2

Answer to 1.......................................................................................................................................2

Answer to 2.......................................................................................................................................2

Answer to 3.......................................................................................................................................3

Answer to 4.......................................................................................................................................3

Answer to 5.......................................................................................................................................4

Part B: Journal Article Critique...............................................................................................................5

Answer to 1.......................................................................................................................................5

Answer to 2.......................................................................................................................................6

Answer to 3.......................................................................................................................................7

References.............................................................................................................................................9

2MANAGERIAL ACCOUNTING

Part A: Case Study Analysis

Answer to 1

It can be seen from the provided scenario that there are examples of four

types of costs; they are fixed cost, variable cost, and incremental cost and sunk cost.

However, it needs to be mentioned that it is not needed to consider the sunk costs

due to the fact that these costs are not included at the time to make decisions. Fixed

costs are considered as those costs that do not changes with the fluctuation in the

number of products or proceeded services or sold. After that, variable costs are

considered as those costs that increases or decreases on the basis of the increase

or decrease in the production volume. After that, incremental costs are considered

as those costs that the managers use at the time of the analysis of business

planning in order gain an insight about the company’s additional costs when they

undertake a specific action (Hilton and Platt 2013). The following table shows the

examples of the above-discussed costs from the provided case study.

Example

Fixed Costs The annual licence fee of $225 can be considered as an

example of fixed cost. The main reason is that there would

not be any change in this fee due to the actions of the couple

Variable Costs The collected total amount at a rate of $800 per child for the

purpose of child care is the example of variable cost because

of the variation of this cost in accordance with the number of

students

Incremental

Costs

The increase in cost of utilities that is $50 is a fixed cost.

Provided information states that this would increase in each

month due to day care and children’s number is not an issue.

Thus, this is an incremental cost that can be adjusted

because of the change in utilities (Kaplan and Atkinson

2015).

Answer to 2

There is a major necessity for differentiating the costs that are relevant or

irrelevant to the decision related to the purchase of appliance. The presence of two

inherent issues can be seen in this case; first, whether the cost would be incurred on

the basis of future undertaken decision, and second, one can differentiate the cost

from the available alternatives. It is needed to consider the cost as relevant after it

satisfies particular criteria (Brewer, Garrison and Noreen 2015). For this reason, in

case Franks takes the decision of purchasing the appliances, following are the

relevant costs then:

1. Cost of new appliance

2. Cost for delivering the new appliance

3. Cost of installation of the new appliance

4. Added utility cost

It is required for Frank for the effective consideration of the differences in the

costs of the available alternatives if he takes the decision of the investigation of all

the available alternatives. For this reason, some additional costs would be relevant

for Frank; they are as below:

1. Cost of delivery as well as the delivery of the laundry services

2. Self-service laundry expenditures such as detergent, laundering and others

Part A: Case Study Analysis

Answer to 1

It can be seen from the provided scenario that there are examples of four

types of costs; they are fixed cost, variable cost, and incremental cost and sunk cost.

However, it needs to be mentioned that it is not needed to consider the sunk costs

due to the fact that these costs are not included at the time to make decisions. Fixed

costs are considered as those costs that do not changes with the fluctuation in the

number of products or proceeded services or sold. After that, variable costs are

considered as those costs that increases or decreases on the basis of the increase

or decrease in the production volume. After that, incremental costs are considered

as those costs that the managers use at the time of the analysis of business

planning in order gain an insight about the company’s additional costs when they

undertake a specific action (Hilton and Platt 2013). The following table shows the

examples of the above-discussed costs from the provided case study.

Example

Fixed Costs The annual licence fee of $225 can be considered as an

example of fixed cost. The main reason is that there would

not be any change in this fee due to the actions of the couple

Variable Costs The collected total amount at a rate of $800 per child for the

purpose of child care is the example of variable cost because

of the variation of this cost in accordance with the number of

students

Incremental

Costs

The increase in cost of utilities that is $50 is a fixed cost.

Provided information states that this would increase in each

month due to day care and children’s number is not an issue.

Thus, this is an incremental cost that can be adjusted

because of the change in utilities (Kaplan and Atkinson

2015).

Answer to 2

There is a major necessity for differentiating the costs that are relevant or

irrelevant to the decision related to the purchase of appliance. The presence of two

inherent issues can be seen in this case; first, whether the cost would be incurred on

the basis of future undertaken decision, and second, one can differentiate the cost

from the available alternatives. It is needed to consider the cost as relevant after it

satisfies particular criteria (Brewer, Garrison and Noreen 2015). For this reason, in

case Franks takes the decision of purchasing the appliances, following are the

relevant costs then:

1. Cost of new appliance

2. Cost for delivering the new appliance

3. Cost of installation of the new appliance

4. Added utility cost

It is required for Frank for the effective consideration of the differences in the

costs of the available alternatives if he takes the decision of the investigation of all

the available alternatives. For this reason, some additional costs would be relevant

for Frank; they are as below:

1. Cost of delivery as well as the delivery of the laundry services

2. Self-service laundry expenditures such as detergent, laundering and others

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGERIAL ACCOUNTING

There is a major necessity for gaining understanding about the costs that are

already incurred which do not have relevancy with the future decisions. Thus, there

are some costs that can be considered as irrelevant to the appliance purchase

related decisions and they are as follows:

1. Cost of old appliance

2. Cost of detergent in case the available options do not consider the series like

delivery and pick-up (Needles, Powers and Crosson 2013).

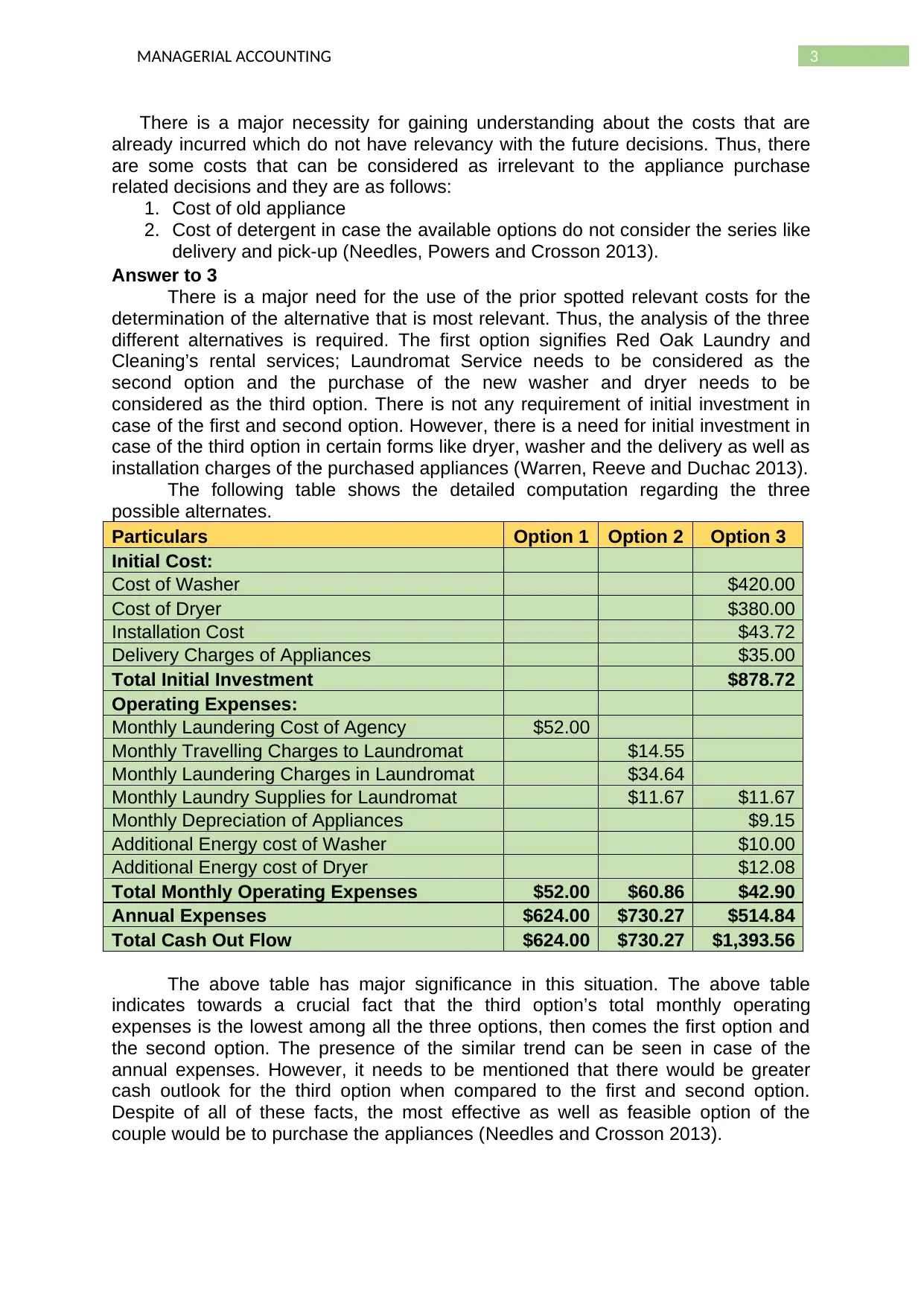

Answer to 3

There is a major need for the use of the prior spotted relevant costs for the

determination of the alternative that is most relevant. Thus, the analysis of the three

different alternatives is required. The first option signifies Red Oak Laundry and

Cleaning’s rental services; Laundromat Service needs to be considered as the

second option and the purchase of the new washer and dryer needs to be

considered as the third option. There is not any requirement of initial investment in

case of the first and second option. However, there is a need for initial investment in

case of the third option in certain forms like dryer, washer and the delivery as well as

installation charges of the purchased appliances (Warren, Reeve and Duchac 2013).

The following table shows the detailed computation regarding the three

possible alternates.

Particulars Option 1 Option 2 Option 3

Initial Cost:

Cost of Washer $420.00

Cost of Dryer $380.00

Installation Cost $43.72

Delivery Charges of Appliances $35.00

Total Initial Investment $878.72

Operating Expenses:

Monthly Laundering Cost of Agency $52.00

Monthly Travelling Charges to Laundromat $14.55

Monthly Laundering Charges in Laundromat $34.64

Monthly Laundry Supplies for Laundromat $11.67 $11.67

Monthly Depreciation of Appliances $9.15

Additional Energy cost of Washer $10.00

Additional Energy cost of Dryer $12.08

Total Monthly Operating Expenses $52.00 $60.86 $42.90

Annual Expenses $624.00 $730.27 $514.84

Total Cash Out Flow $624.00 $730.27 $1,393.56

The above table has major significance in this situation. The above table

indicates towards a crucial fact that the third option’s total monthly operating

expenses is the lowest among all the three options, then comes the first option and

the second option. The presence of the similar trend can be seen in case of the

annual expenses. However, it needs to be mentioned that there would be greater

cash outlook for the third option when compared to the first and second option.

Despite of all of these facts, the most effective as well as feasible option of the

couple would be to purchase the appliances (Needles and Crosson 2013).

There is a major necessity for gaining understanding about the costs that are

already incurred which do not have relevancy with the future decisions. Thus, there

are some costs that can be considered as irrelevant to the appliance purchase

related decisions and they are as follows:

1. Cost of old appliance

2. Cost of detergent in case the available options do not consider the series like

delivery and pick-up (Needles, Powers and Crosson 2013).

Answer to 3

There is a major need for the use of the prior spotted relevant costs for the

determination of the alternative that is most relevant. Thus, the analysis of the three

different alternatives is required. The first option signifies Red Oak Laundry and

Cleaning’s rental services; Laundromat Service needs to be considered as the

second option and the purchase of the new washer and dryer needs to be

considered as the third option. There is not any requirement of initial investment in

case of the first and second option. However, there is a need for initial investment in

case of the third option in certain forms like dryer, washer and the delivery as well as

installation charges of the purchased appliances (Warren, Reeve and Duchac 2013).

The following table shows the detailed computation regarding the three

possible alternates.

Particulars Option 1 Option 2 Option 3

Initial Cost:

Cost of Washer $420.00

Cost of Dryer $380.00

Installation Cost $43.72

Delivery Charges of Appliances $35.00

Total Initial Investment $878.72

Operating Expenses:

Monthly Laundering Cost of Agency $52.00

Monthly Travelling Charges to Laundromat $14.55

Monthly Laundering Charges in Laundromat $34.64

Monthly Laundry Supplies for Laundromat $11.67 $11.67

Monthly Depreciation of Appliances $9.15

Additional Energy cost of Washer $10.00

Additional Energy cost of Dryer $12.08

Total Monthly Operating Expenses $52.00 $60.86 $42.90

Annual Expenses $624.00 $730.27 $514.84

Total Cash Out Flow $624.00 $730.27 $1,393.56

The above table has major significance in this situation. The above table

indicates towards a crucial fact that the third option’s total monthly operating

expenses is the lowest among all the three options, then comes the first option and

the second option. The presence of the similar trend can be seen in case of the

annual expenses. However, it needs to be mentioned that there would be greater

cash outlook for the third option when compared to the first and second option.

Despite of all of these facts, the most effective as well as feasible option of the

couple would be to purchase the appliances (Needles and Crosson 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGERIAL ACCOUNTING

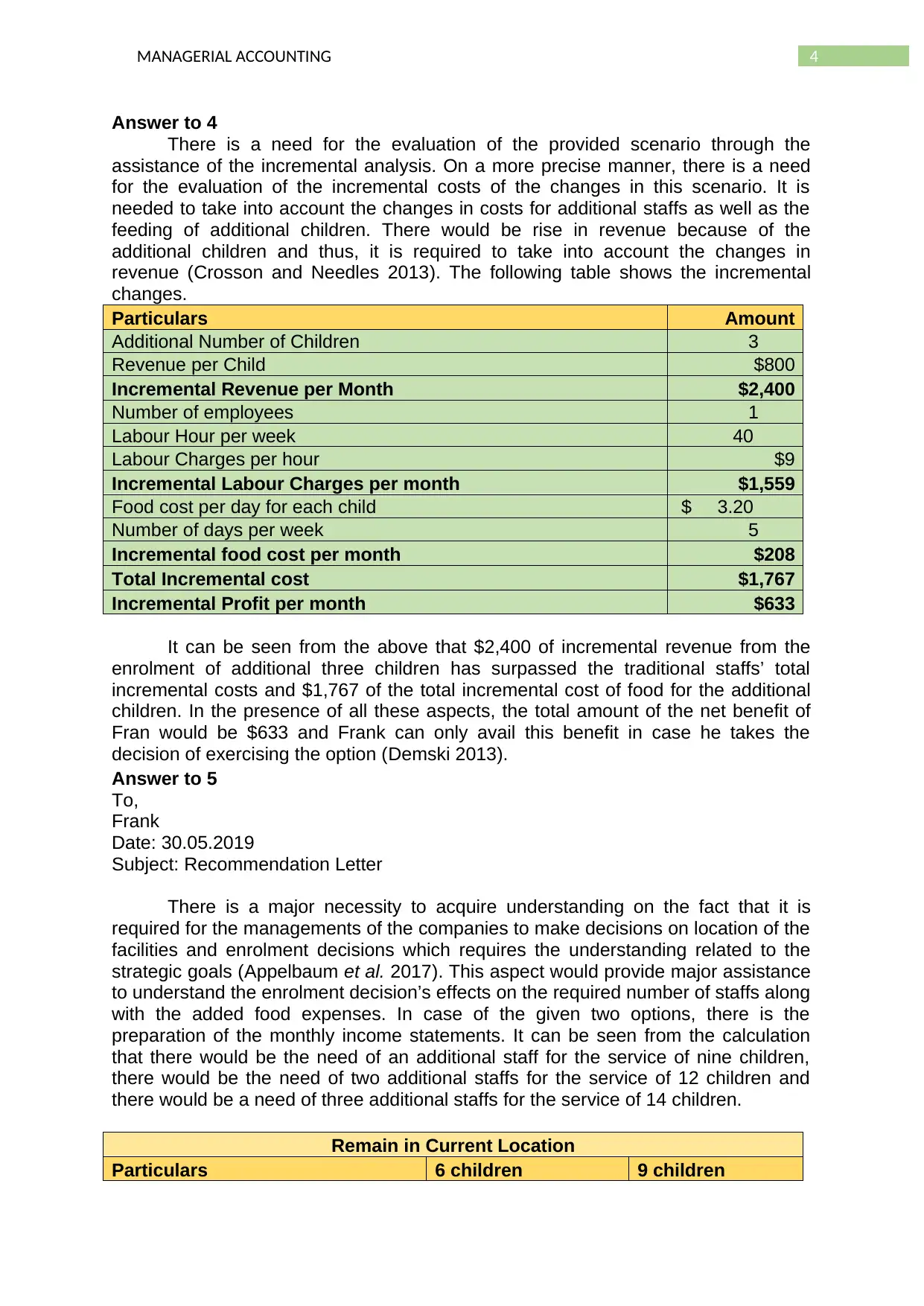

Answer to 4

There is a need for the evaluation of the provided scenario through the

assistance of the incremental analysis. On a more precise manner, there is a need

for the evaluation of the incremental costs of the changes in this scenario. It is

needed to take into account the changes in costs for additional staffs as well as the

feeding of additional children. There would be rise in revenue because of the

additional children and thus, it is required to take into account the changes in

revenue (Crosson and Needles 2013). The following table shows the incremental

changes.

Particulars Amount

Additional Number of Children 3

Revenue per Child $800

Incremental Revenue per Month $2,400

Number of employees 1

Labour Hour per week 40

Labour Charges per hour $9

Incremental Labour Charges per month $1,559

Food cost per day for each child $ 3.20

Number of days per week 5

Incremental food cost per month $208

Total Incremental cost $1,767

Incremental Profit per month $633

It can be seen from the above that $2,400 of incremental revenue from the

enrolment of additional three children has surpassed the traditional staffs’ total

incremental costs and $1,767 of the total incremental cost of food for the additional

children. In the presence of all these aspects, the total amount of the net benefit of

Fran would be $633 and Frank can only avail this benefit in case he takes the

decision of exercising the option (Demski 2013).

Answer to 5

To,

Frank

Date: 30.05.2019

Subject: Recommendation Letter

There is a major necessity to acquire understanding on the fact that it is

required for the managements of the companies to make decisions on location of the

facilities and enrolment decisions which requires the understanding related to the

strategic goals (Appelbaum et al. 2017). This aspect would provide major assistance

to understand the enrolment decision’s effects on the required number of staffs along

with the added food expenses. In case of the given two options, there is the

preparation of the monthly income statements. It can be seen from the calculation

that there would be the need of an additional staff for the service of nine children,

there would be the need of two additional staffs for the service of 12 children and

there would be a need of three additional staffs for the service of 14 children.

Remain in Current Location

Particulars 6 children 9 children

Answer to 4

There is a need for the evaluation of the provided scenario through the

assistance of the incremental analysis. On a more precise manner, there is a need

for the evaluation of the incremental costs of the changes in this scenario. It is

needed to take into account the changes in costs for additional staffs as well as the

feeding of additional children. There would be rise in revenue because of the

additional children and thus, it is required to take into account the changes in

revenue (Crosson and Needles 2013). The following table shows the incremental

changes.

Particulars Amount

Additional Number of Children 3

Revenue per Child $800

Incremental Revenue per Month $2,400

Number of employees 1

Labour Hour per week 40

Labour Charges per hour $9

Incremental Labour Charges per month $1,559

Food cost per day for each child $ 3.20

Number of days per week 5

Incremental food cost per month $208

Total Incremental cost $1,767

Incremental Profit per month $633

It can be seen from the above that $2,400 of incremental revenue from the

enrolment of additional three children has surpassed the traditional staffs’ total

incremental costs and $1,767 of the total incremental cost of food for the additional

children. In the presence of all these aspects, the total amount of the net benefit of

Fran would be $633 and Frank can only avail this benefit in case he takes the

decision of exercising the option (Demski 2013).

Answer to 5

To,

Frank

Date: 30.05.2019

Subject: Recommendation Letter

There is a major necessity to acquire understanding on the fact that it is

required for the managements of the companies to make decisions on location of the

facilities and enrolment decisions which requires the understanding related to the

strategic goals (Appelbaum et al. 2017). This aspect would provide major assistance

to understand the enrolment decision’s effects on the required number of staffs along

with the added food expenses. In case of the given two options, there is the

preparation of the monthly income statements. It can be seen from the calculation

that there would be the need of an additional staff for the service of nine children,

there would be the need of two additional staffs for the service of 12 children and

there would be a need of three additional staffs for the service of 14 children.

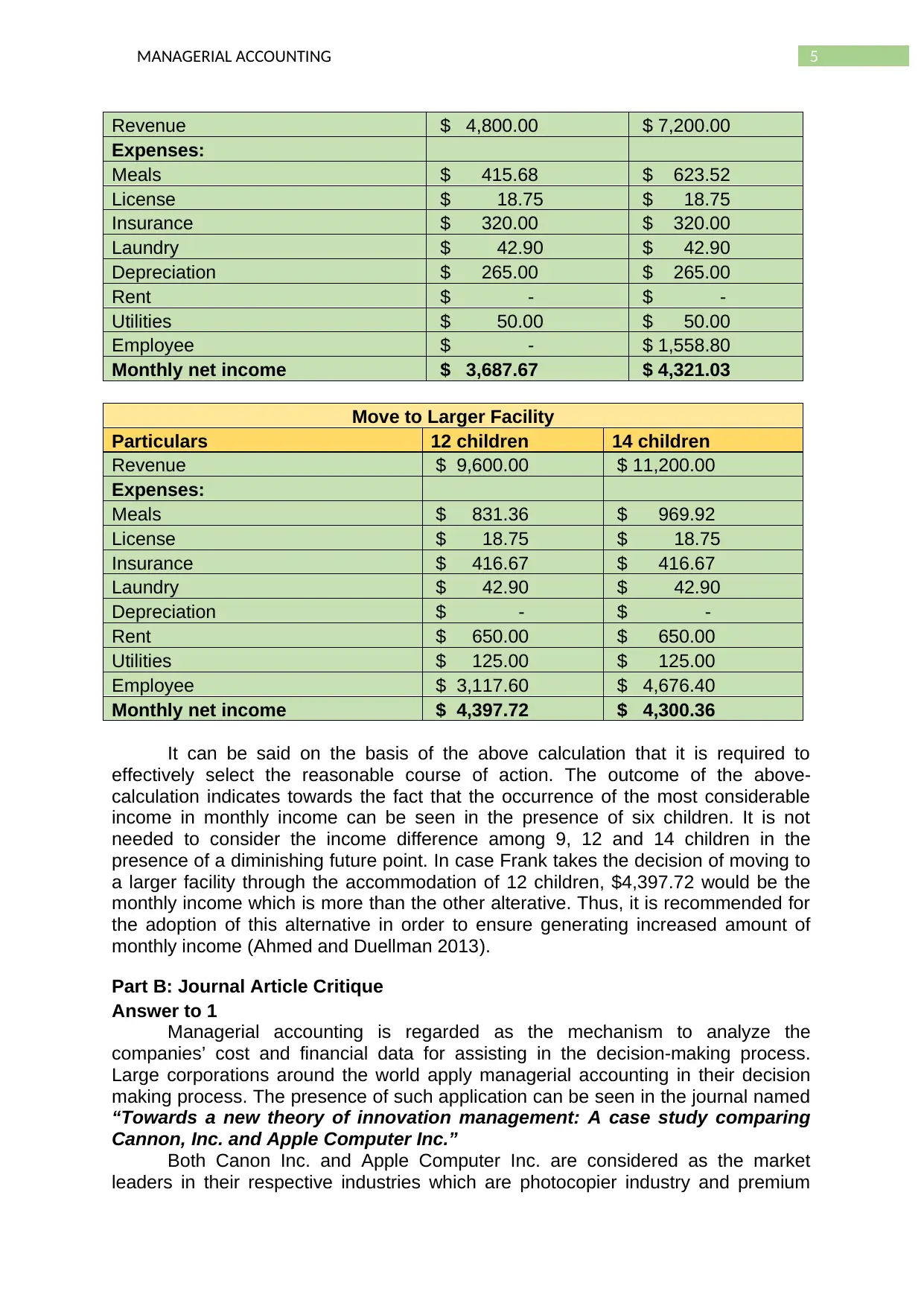

Remain in Current Location

Particulars 6 children 9 children

5MANAGERIAL ACCOUNTING

Revenue $ 4,800.00 $ 7,200.00

Expenses:

Meals $ 415.68 $ 623.52

License $ 18.75 $ 18.75

Insurance $ 320.00 $ 320.00

Laundry $ 42.90 $ 42.90

Depreciation $ 265.00 $ 265.00

Rent $ - $ -

Utilities $ 50.00 $ 50.00

Employee $ - $ 1,558.80

Monthly net income $ 3,687.67 $ 4,321.03

Move to Larger Facility

Particulars 12 children 14 children

Revenue $ 9,600.00 $ 11,200.00

Expenses:

Meals $ 831.36 $ 969.92

License $ 18.75 $ 18.75

Insurance $ 416.67 $ 416.67

Laundry $ 42.90 $ 42.90

Depreciation $ - $ -

Rent $ 650.00 $ 650.00

Utilities $ 125.00 $ 125.00

Employee $ 3,117.60 $ 4,676.40

Monthly net income $ 4,397.72 $ 4,300.36

It can be said on the basis of the above calculation that it is required to

effectively select the reasonable course of action. The outcome of the above-

calculation indicates towards the fact that the occurrence of the most considerable

income in monthly income can be seen in the presence of six children. It is not

needed to consider the income difference among 9, 12 and 14 children in the

presence of a diminishing future point. In case Frank takes the decision of moving to

a larger facility through the accommodation of 12 children, $4,397.72 would be the

monthly income which is more than the other alterative. Thus, it is recommended for

the adoption of this alternative in order to ensure generating increased amount of

monthly income (Ahmed and Duellman 2013).

Part B: Journal Article Critique

Answer to 1

Managerial accounting is regarded as the mechanism to analyze the

companies’ cost and financial data for assisting in the decision-making process.

Large corporations around the world apply managerial accounting in their decision

making process. The presence of such application can be seen in the journal named

“Towards a new theory of innovation management: A case study comparing

Cannon, Inc. and Apple Computer Inc.”

Both Canon Inc. and Apple Computer Inc. are considered as the market

leaders in their respective industries which are photocopier industry and premium

Revenue $ 4,800.00 $ 7,200.00

Expenses:

Meals $ 415.68 $ 623.52

License $ 18.75 $ 18.75

Insurance $ 320.00 $ 320.00

Laundry $ 42.90 $ 42.90

Depreciation $ 265.00 $ 265.00

Rent $ - $ -

Utilities $ 50.00 $ 50.00

Employee $ - $ 1,558.80

Monthly net income $ 3,687.67 $ 4,321.03

Move to Larger Facility

Particulars 12 children 14 children

Revenue $ 9,600.00 $ 11,200.00

Expenses:

Meals $ 831.36 $ 969.92

License $ 18.75 $ 18.75

Insurance $ 416.67 $ 416.67

Laundry $ 42.90 $ 42.90

Depreciation $ - $ -

Rent $ 650.00 $ 650.00

Utilities $ 125.00 $ 125.00

Employee $ 3,117.60 $ 4,676.40

Monthly net income $ 4,397.72 $ 4,300.36

It can be said on the basis of the above calculation that it is required to

effectively select the reasonable course of action. The outcome of the above-

calculation indicates towards the fact that the occurrence of the most considerable

income in monthly income can be seen in the presence of six children. It is not

needed to consider the income difference among 9, 12 and 14 children in the

presence of a diminishing future point. In case Frank takes the decision of moving to

a larger facility through the accommodation of 12 children, $4,397.72 would be the

monthly income which is more than the other alterative. Thus, it is recommended for

the adoption of this alternative in order to ensure generating increased amount of

monthly income (Ahmed and Duellman 2013).

Part B: Journal Article Critique

Answer to 1

Managerial accounting is regarded as the mechanism to analyze the

companies’ cost and financial data for assisting in the decision-making process.

Large corporations around the world apply managerial accounting in their decision

making process. The presence of such application can be seen in the journal named

“Towards a new theory of innovation management: A case study comparing

Cannon, Inc. and Apple Computer Inc.”

Both Canon Inc. and Apple Computer Inc. are considered as the market

leaders in their respective industries which are photocopier industry and premium

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGERIAL ACCOUNTING

computer manufacturer respectively. Success is regarded as a competitive situation

which has reliance of effective ground management and certain core competencies

of the companies. Companies are required to be innovative in their product offerings

as well as in cost management due to the massive technology changes. Effective

management is needed for fighting the hurdles in markets in order to be superior in

the industry (Butler and Ghosh 2015). It can be seen in the provided journal that the

processes of information creation and sharing have been given major emphasis

since it is essential in managerial accounting (Nonala and Kenney 1991). As per the

case of Canon, through the inclusion of employees from different departments, the

firm conducted certain feasibility study of their new product, a mini copier. The

strategy was to make effective decision in the presence of senior executive from

every department (Otley and Emmanuel 2013). Everyone knows about the struggle

of Steve Jobs for building Apple Mac PC and the success that came after it, but the

main reason for the success of the firm is their effective and efficient management.

As mentioned in the article, Apple has a strong management team and they

maintained a continuous interaction among them in order to make the management

stronger (Nonala and Kenney 1991). The application of effective management

accounting tools and techniques made them able in grabbing the market

opportunities in order to make their products more innovative as well as cost

effective. Moreover, it can also be seen that these companies have been working

with their executives, engineers and managers in order to make complete

harmonization so that collaboratively they can develop innovative products in their

respective industries (Weygandt et al. 2018).

It can be said on the basis of the above discussion that the effective and

efficient application of managerial accounting tools and techniques assists the

companies to improve their process of decision-making for the overall success of the

business.

Answer to 2

Managerial accounting as well as the process of management accounting is a

continuous organizational process that assists in bringing innovation in management

system s that effective business decisions can be made. The provided journal article

summarizes innovation in the management system of a company as the process of

creation of innovation along with effective sharing of that information. This is a

majorly true proposition because of its presence of many companies where the

analysis as well as use of different financial and non-financial information can be

seen in the management processes. Thus, it can be said that the managements of

the firms create and share this useful information for various purposes (Otley and

Emmanuel 2013).

Management executives stay at the top of the organizational structure and

they are involved in the use of financial and non-financial information the business

for the analysis of different business activities and then make business decisions on

the basis of the analysis. It is noteworthy to mention that business success largely

depends on the correct use of information and correct business decisions. Thus, the

presence of effective business information system is paramount for the companies

where effective decision making relies on the correct use of significant and efficient

decision along with the innovation of management information system (Mihăilă

2014).

In the provided journal article, major emphasis is provided on the information

system innovation (Nonala and Kenney 1991). Innovation needs to be there in the

information creation as well as sharing system because of the use of financial and

computer manufacturer respectively. Success is regarded as a competitive situation

which has reliance of effective ground management and certain core competencies

of the companies. Companies are required to be innovative in their product offerings

as well as in cost management due to the massive technology changes. Effective

management is needed for fighting the hurdles in markets in order to be superior in

the industry (Butler and Ghosh 2015). It can be seen in the provided journal that the

processes of information creation and sharing have been given major emphasis

since it is essential in managerial accounting (Nonala and Kenney 1991). As per the

case of Canon, through the inclusion of employees from different departments, the

firm conducted certain feasibility study of their new product, a mini copier. The

strategy was to make effective decision in the presence of senior executive from

every department (Otley and Emmanuel 2013). Everyone knows about the struggle

of Steve Jobs for building Apple Mac PC and the success that came after it, but the

main reason for the success of the firm is their effective and efficient management.

As mentioned in the article, Apple has a strong management team and they

maintained a continuous interaction among them in order to make the management

stronger (Nonala and Kenney 1991). The application of effective management

accounting tools and techniques made them able in grabbing the market

opportunities in order to make their products more innovative as well as cost

effective. Moreover, it can also be seen that these companies have been working

with their executives, engineers and managers in order to make complete

harmonization so that collaboratively they can develop innovative products in their

respective industries (Weygandt et al. 2018).

It can be said on the basis of the above discussion that the effective and

efficient application of managerial accounting tools and techniques assists the

companies to improve their process of decision-making for the overall success of the

business.

Answer to 2

Managerial accounting as well as the process of management accounting is a

continuous organizational process that assists in bringing innovation in management

system s that effective business decisions can be made. The provided journal article

summarizes innovation in the management system of a company as the process of

creation of innovation along with effective sharing of that information. This is a

majorly true proposition because of its presence of many companies where the

analysis as well as use of different financial and non-financial information can be

seen in the management processes. Thus, it can be said that the managements of

the firms create and share this useful information for various purposes (Otley and

Emmanuel 2013).

Management executives stay at the top of the organizational structure and

they are involved in the use of financial and non-financial information the business

for the analysis of different business activities and then make business decisions on

the basis of the analysis. It is noteworthy to mention that business success largely

depends on the correct use of information and correct business decisions. Thus, the

presence of effective business information system is paramount for the companies

where effective decision making relies on the correct use of significant and efficient

decision along with the innovation of management information system (Mihăilă

2014).

In the provided journal article, major emphasis is provided on the information

system innovation (Nonala and Kenney 1991). Innovation needs to be there in the

information creation as well as sharing system because of the use of financial and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL ACCOUNTING

non-financial information by the management. It can be seen from the case study of

Apple Inc. in the provided journal article that the management executives of the

company worked together for the analysis of managerial issues in order to make

correct decisions. It has been possible to bring innovation in the information creation

and sharing process due to the effective interrelation among the managers,

executives and engineers. It provided them major assistance to solve the managerial

issues efficiently. For instance, the management of Apple Inc. utilized their effective

and efficient information creation and analysis system for making decision during the

development of Apple Mac Book (Greenberg and Wilner 2015).

The management team of Canon Inc. also utilized their management

information system for making effective business decisions. They have brought

innovation in the managerial level process of information creation. It can be seen that

the managerial approach of Canon Inc. to approach the organizational problems and

decision-making process is different from that of Apple Inc. They tried to solve the

issues in the presence of all managerial executives along with the assistance of their

efficiency information system. The use of different traditional management processes

can be seen by the making management decisions. For example, the use of certain

traditional managerial procedures could be seen by the management of Canon Inc.

along with the innovative technologically advanced processes for the development of

the mini copier (Bobryshev et al. 2015).

Thus, it can be seen from the above discussion that there is a major necessity

of innovation on the information creation as well sharing process in order to bring

improvement in the management processes and managerial decision-making

process.

Answer to 3

Management is considered as the backbone of every business because of the

fact that it assists in organizing the necessary components for smooth running of

business through the effective utilization of available resources so that the overall

business objectives can be achieved. Making decisions regarding the effective

management of organizational resources is considered as one of the most crucial

functions of the management. Effective decision-making perspective is considered

as the main pillar for organizational success. The presence of innovation in the

products and services helps the firms in competing with their competitors in the

highly competitive markets. Management is considered as the main part of the

business organizations which always try hard for the achievement of the long-term

as well as short-term business objectives and goals (Narayanaswamy 2017).

The significant of the information provided by the management information

system cannot be ignored the success of the decision-making process of the

companies. The effective management teams of the firms significantly contribute to

the success of the decision-making process of the firms so that the companies can

achieve their long and short-term business goals. The application of different types

of managerial tools and management decision-making processes can be seen within

the organizations in order to solve various types of organizational as well as

managerial problems (Songini, Gnan and Malmi 2013).

The provided journal article involves in the comparison of the case studies of

two companies that are Canon Inc. and Apple Inc. and both of these companies

belong to the technology industry (Nonala and Kenney 1991). Due to the continuous

changes in technology that brings different kinds of innovations, businesses

organization are entering into the market with innovative products and services in

each and every day which is making the competition more intense. In order to

non-financial information by the management. It can be seen from the case study of

Apple Inc. in the provided journal article that the management executives of the

company worked together for the analysis of managerial issues in order to make

correct decisions. It has been possible to bring innovation in the information creation

and sharing process due to the effective interrelation among the managers,

executives and engineers. It provided them major assistance to solve the managerial

issues efficiently. For instance, the management of Apple Inc. utilized their effective

and efficient information creation and analysis system for making decision during the

development of Apple Mac Book (Greenberg and Wilner 2015).

The management team of Canon Inc. also utilized their management

information system for making effective business decisions. They have brought

innovation in the managerial level process of information creation. It can be seen that

the managerial approach of Canon Inc. to approach the organizational problems and

decision-making process is different from that of Apple Inc. They tried to solve the

issues in the presence of all managerial executives along with the assistance of their

efficiency information system. The use of different traditional management processes

can be seen by the making management decisions. For example, the use of certain

traditional managerial procedures could be seen by the management of Canon Inc.

along with the innovative technologically advanced processes for the development of

the mini copier (Bobryshev et al. 2015).

Thus, it can be seen from the above discussion that there is a major necessity

of innovation on the information creation as well sharing process in order to bring

improvement in the management processes and managerial decision-making

process.

Answer to 3

Management is considered as the backbone of every business because of the

fact that it assists in organizing the necessary components for smooth running of

business through the effective utilization of available resources so that the overall

business objectives can be achieved. Making decisions regarding the effective

management of organizational resources is considered as one of the most crucial

functions of the management. Effective decision-making perspective is considered

as the main pillar for organizational success. The presence of innovation in the

products and services helps the firms in competing with their competitors in the

highly competitive markets. Management is considered as the main part of the

business organizations which always try hard for the achievement of the long-term

as well as short-term business objectives and goals (Narayanaswamy 2017).

The significant of the information provided by the management information

system cannot be ignored the success of the decision-making process of the

companies. The effective management teams of the firms significantly contribute to

the success of the decision-making process of the firms so that the companies can

achieve their long and short-term business goals. The application of different types

of managerial tools and management decision-making processes can be seen within

the organizations in order to solve various types of organizational as well as

managerial problems (Songini, Gnan and Malmi 2013).

The provided journal article involves in the comparison of the case studies of

two companies that are Canon Inc. and Apple Inc. and both of these companies

belong to the technology industry (Nonala and Kenney 1991). Due to the continuous

changes in technology that brings different kinds of innovations, businesses

organization are entering into the market with innovative products and services in

each and every day which is making the competition more intense. In order to

8MANAGERIAL ACCOUNTING

ensure survival in this market along with to be successful, every company is needed

to ensure the adoption of activities that help them in bringing innovative products in

the market. They are needed to analyze their competitors for the purpose of

decision-making process so that the tough challenge can be effectively faced

(Baiman 2014).

For this reason, it is essential to ensure the presence of information creation

as well as sharing system in the organizational decision-making process. Innovation

in the information creation process refers to the creation of more significant financial

and non-financial information for effective decision-making process. At the same

time, information sharing system refers to the process to make all managerial

information available to the higher management executives having involvement in

the decision-making process as well as implementation of the decisions. The

information sharing system also consists of the process to collect information from

different segments and departments of the firms for making effective contribution

towards the decision-making process (Krstevski and Mancheski 2016).

It can be said based on the above discussion that it is not enough for the

companies to have a management information system for the decision-making

process unless there is innovation in the processes of information creation and

information sharing in efficient manner. Thus, the presence of improved and efficient

management information system assists the companies in making better decisions.

ensure survival in this market along with to be successful, every company is needed

to ensure the adoption of activities that help them in bringing innovative products in

the market. They are needed to analyze their competitors for the purpose of

decision-making process so that the tough challenge can be effectively faced

(Baiman 2014).

For this reason, it is essential to ensure the presence of information creation

as well as sharing system in the organizational decision-making process. Innovation

in the information creation process refers to the creation of more significant financial

and non-financial information for effective decision-making process. At the same

time, information sharing system refers to the process to make all managerial

information available to the higher management executives having involvement in

the decision-making process as well as implementation of the decisions. The

information sharing system also consists of the process to collect information from

different segments and departments of the firms for making effective contribution

towards the decision-making process (Krstevski and Mancheski 2016).

It can be said based on the above discussion that it is not enough for the

companies to have a management information system for the decision-making

process unless there is innovation in the processes of information creation and

information sharing in efficient manner. Thus, the presence of improved and efficient

management information system assists the companies in making better decisions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGERIAL ACCOUNTING

References

Ahmed, A.S. and Duellman, S., 2013. Managerial overconfidence and accounting

conservatism. Journal of Accounting Research, 51(1), pp.1-30.

Appelbaum, D., Kogan, A., Vasarhelyi, M. and Yan, Z., 2017. Impact of business

analytics and enterprise systems on managerial accounting. International Journal of

Accounting Information Systems, 25, pp.29-44.

Baiman, S., 2014. Some ideas for further research in managerial accounting. Journal

of Management Accounting Research, 26(2), pp.119-121.

Bobryshev, A.N., Tatarinova, M.N., Grishanova, S.V. and Frolov, A.V.E., 2015.

Management accounting in Russia: problems of theoretical study and practical

application in the economic crisis. Journal of Advanced Research in Law and

Economics, 6(3 (13)), p.511.

Brewer, P.C., Garrison, R.H. and Noreen, E.W., 2015. Introduction to managerial

accounting. McGraw-Hill Education.

Butler, S.A. and Ghosh, D., 2015. Individual differences in managerial accounting

judgments and decision making. The British Accounting Review, 47(1), pp.33-45.

Crosson, S.V. and Needles, B.E., 2013. Managerial accounting. Cengage Learning.

Demski, J., 2013. Managerial uses of accounting information. Springer Science &

Business Media.

Greenberg, R.K. and Wilner, N.A., 2015. Using concept maps to provide an

integrative framework for teaching the cost or managerial accounting course. Journal

of Accounting Education, 33(1), pp.16-35.

Hilton, R.W. and Platt, D.E., 2013. Managerial accounting: creating value in a

dynamic business environment. McGraw-Hill Education.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI

Learning.

Krstevski, D. and Mancheski, G., 2016. Managerial accounting: Modeling customer

lifetime value-An application in the telecommunication industry. European Journal of

Business and Social Sciences, 5(01), pp.64-77.

Mihăilă, M., 2014. Managerial accounting and decision making, in energy

industry. Procedia-Social and Behavioral Sciences, 109, pp.1199-1202.

Narayanaswamy, R., 2017. Financial accounting: a managerial perspective. PHI

Learning Pvt. Ltd..

Needles, B. and Crosson, S., 2013. Managerial accounting. Cengage Learning.

Needles, B.E., Powers, M. and Crosson, S.V., 2013. Financial and managerial

accounting. Nelson Education.

Nonala, I. and Kenney, M., 1991. Towards a new theory of innovation management:

A case study comparing Canon, Inc. and Apple Computer, Inc. Journal of

Engineering and Technology Management, 8(1), pp.67-83.

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for management

control. Springer.

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for management

control. Springer.

Songini, L., Gnan, L. and Malmi, T., 2013. The role and impact of accounting in

family business. Journal of Family Business Strategy, 4(2), pp.71-83.

Warren, C., Reeve, J.M. and Duchac, J., 2013. Financial & managerial accounting.

Cengage Learning.

References

Ahmed, A.S. and Duellman, S., 2013. Managerial overconfidence and accounting

conservatism. Journal of Accounting Research, 51(1), pp.1-30.

Appelbaum, D., Kogan, A., Vasarhelyi, M. and Yan, Z., 2017. Impact of business

analytics and enterprise systems on managerial accounting. International Journal of

Accounting Information Systems, 25, pp.29-44.

Baiman, S., 2014. Some ideas for further research in managerial accounting. Journal

of Management Accounting Research, 26(2), pp.119-121.

Bobryshev, A.N., Tatarinova, M.N., Grishanova, S.V. and Frolov, A.V.E., 2015.

Management accounting in Russia: problems of theoretical study and practical

application in the economic crisis. Journal of Advanced Research in Law and

Economics, 6(3 (13)), p.511.

Brewer, P.C., Garrison, R.H. and Noreen, E.W., 2015. Introduction to managerial

accounting. McGraw-Hill Education.

Butler, S.A. and Ghosh, D., 2015. Individual differences in managerial accounting

judgments and decision making. The British Accounting Review, 47(1), pp.33-45.

Crosson, S.V. and Needles, B.E., 2013. Managerial accounting. Cengage Learning.

Demski, J., 2013. Managerial uses of accounting information. Springer Science &

Business Media.

Greenberg, R.K. and Wilner, N.A., 2015. Using concept maps to provide an

integrative framework for teaching the cost or managerial accounting course. Journal

of Accounting Education, 33(1), pp.16-35.

Hilton, R.W. and Platt, D.E., 2013. Managerial accounting: creating value in a

dynamic business environment. McGraw-Hill Education.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI

Learning.

Krstevski, D. and Mancheski, G., 2016. Managerial accounting: Modeling customer

lifetime value-An application in the telecommunication industry. European Journal of

Business and Social Sciences, 5(01), pp.64-77.

Mihăilă, M., 2014. Managerial accounting and decision making, in energy

industry. Procedia-Social and Behavioral Sciences, 109, pp.1199-1202.

Narayanaswamy, R., 2017. Financial accounting: a managerial perspective. PHI

Learning Pvt. Ltd..

Needles, B. and Crosson, S., 2013. Managerial accounting. Cengage Learning.

Needles, B.E., Powers, M. and Crosson, S.V., 2013. Financial and managerial

accounting. Nelson Education.

Nonala, I. and Kenney, M., 1991. Towards a new theory of innovation management:

A case study comparing Canon, Inc. and Apple Computer, Inc. Journal of

Engineering and Technology Management, 8(1), pp.67-83.

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for management

control. Springer.

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for management

control. Springer.

Songini, L., Gnan, L. and Malmi, T., 2013. The role and impact of accounting in

family business. Journal of Family Business Strategy, 4(2), pp.71-83.

Warren, C., Reeve, J.M. and Duchac, J., 2013. Financial & managerial accounting.

Cengage Learning.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGERIAL ACCOUNTING

Weygandt, J.J., Kieso, D.E., Kimmel, P.D. and Aly, I.M., 2018. Managerial

Accounting: Tools for Business Decision-making. John Wiley & Sons Canada,

Limited.

Weygandt, J.J., Kieso, D.E., Kimmel, P.D. and Aly, I.M., 2018. Managerial

Accounting: Tools for Business Decision-making. John Wiley & Sons Canada,

Limited.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.