A Detailed Analysis of Executive Remuneration at QBE Insurance Company

VerifiedAdded on 2019/11/08

|6

|1266

|415

Report

AI Summary

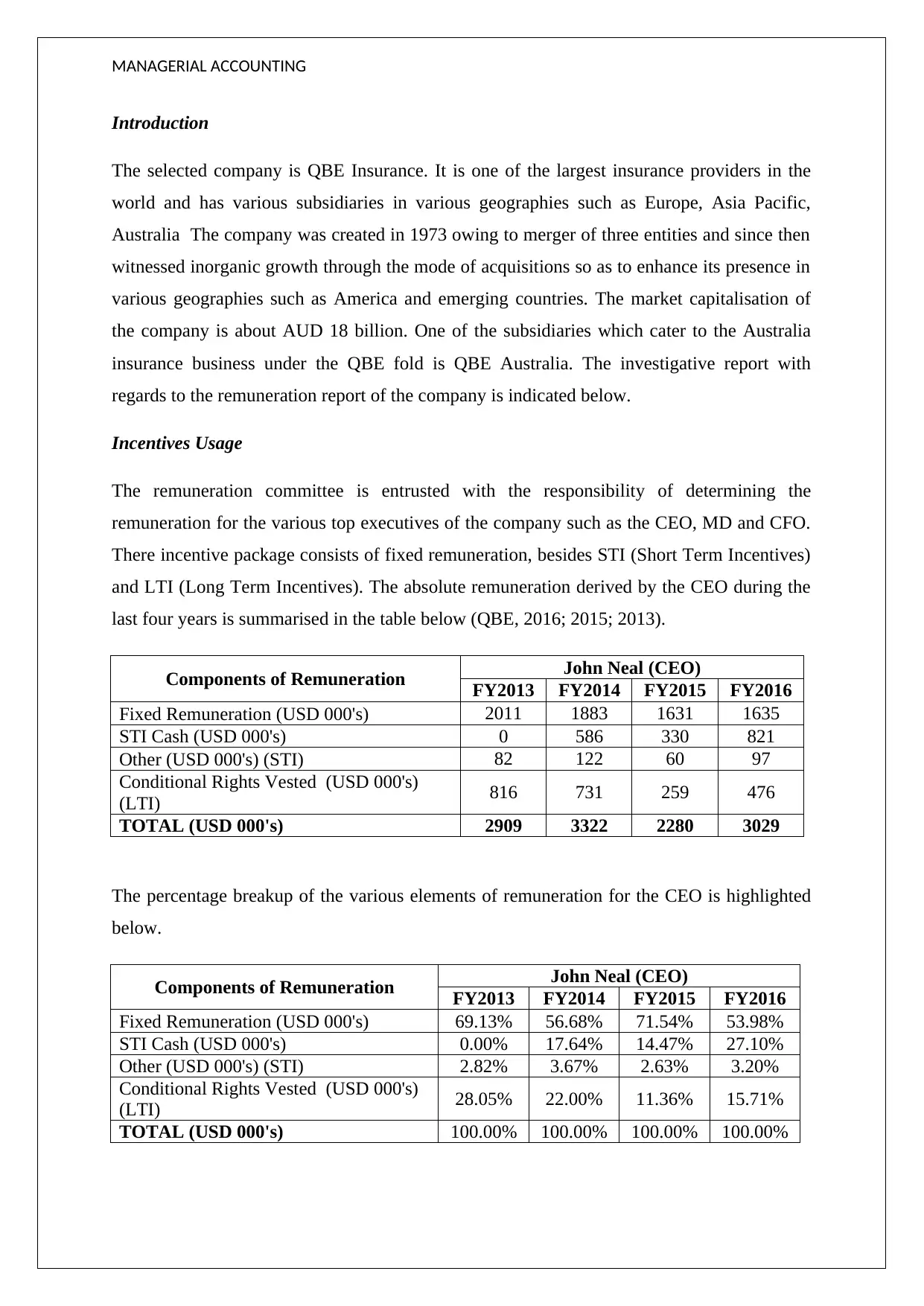

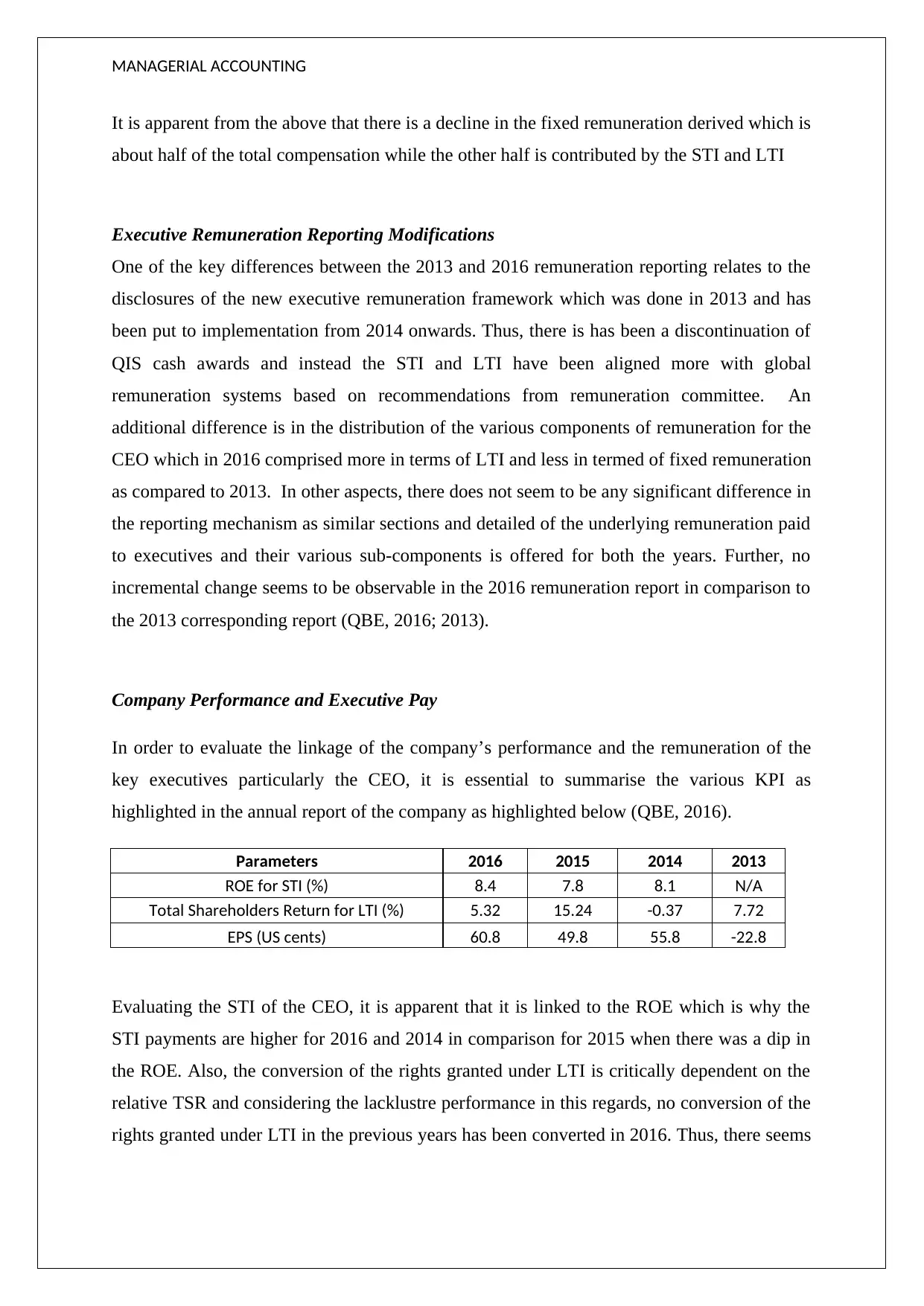

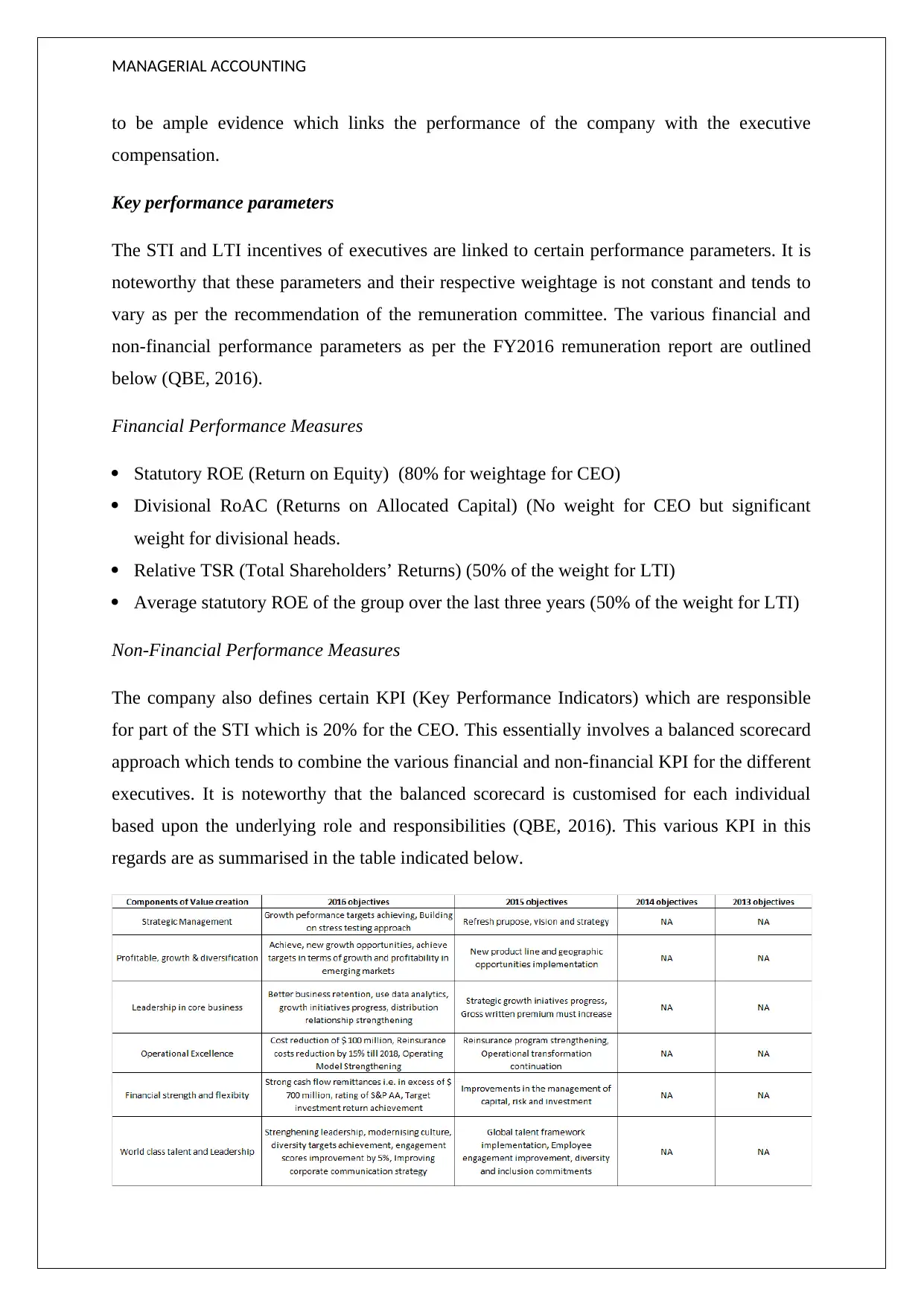

This report provides an in-depth analysis of the executive remuneration at QBE Insurance, focusing on the period from 2013 to 2016. It examines the components of the CEO's compensation, including fixed remuneration, Short-Term Incentives (STI), and Long-Term Incentives (LTI), and their respective percentages over the years. The report highlights the changes in the remuneration reporting framework, such as the introduction of a new executive remuneration framework and the alignment of STI and LTI with global systems. It also evaluates the linkage between the company's financial performance, measured by metrics like ROE and TSR, and the executive pay, demonstrating how STI and LTI are tied to specific performance parameters. The report also discusses the key performance indicators (KPIs), both financial and non-financial, used to determine executive incentives, and recommends increasing the weightage of the balanced scorecard for STI determination to incentivize management to focus on shareholder wealth creation. References to QBE's annual reports from 2013, 2014, and 2016 are provided.

1 out of 6

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.