HI5017 Managerial Accounting: Cost Analysis & Strategic Decisions

VerifiedAdded on 2023/04/03

|13

|3010

|200

Case Study

AI Summary

This assignment presents a comprehensive solution to a managerial accounting case study, focusing on cost analysis, decision-making, and strategic recommendations for a service-based company. Part A delves into various cost types, including utility, installation, and energy costs, and their relevance to business decisions, such as purchasing appliances and hiring employees. It advises the Franks on whether to operate their childcare business at home or in a rented space, providing detailed cost comparisons. Part B critically evaluates a journal article, analyzing the practical application of accounting information in real-life companies like Canon and Apple, highlighting the importance of risk management, performance management, and strategic management in achieving business goals and fostering innovation. The assignment concludes by emphasizing the role of management accounting in identifying risks, facilitating decision-making, and promoting innovation through the integration of economic trends and collaborative processes.

Managerial Accounting

1 | P a g e

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Part A...................................................................................................................................................................... 3

Part B......................................................................................................................................................................8

References............................................................................................................................................................11

2 | P a g e

Part A...................................................................................................................................................................... 3

Part B......................................................................................................................................................................8

References............................................................................................................................................................11

2 | P a g e

Part A

1. Cost

Cost is the monetary value that has been spent by every company in order to produce

services for their customers. It is one of the essential expenditures that must be made by the

company in order to run a business in an appropriate manner. Each production factor has an

associated cost (Kaplan and Atkinson, 2015).

Following there are different types of cost which are associated with the service based

company which are listed below:

1. Variable and fixed costs

2. Indirect and Direct costs

3. Period and Product costs

4. Opportunity and Incremental costs

5. Sunk costs

After considering the various different types of costs which are discussed in the stated

case, three types of costs are selected for further discussion which are mentioned

below:

a. Utility costs: Utility costs are all charges for utilities which have to be paid by the company

on the basis of usage. This cost is considered as a mixed cost in which both cost i.e. fixed

and variable are charged on a products or services based on actual usage (Haroun, 2015).

Some of the examples of utility costs are:

Heat (gas)

Water

Telephone and internet service

Sewer

The cost of utility follow the concept of accrual basis of accounting in which all costs which

are related to the utility are recorded on the basis of actual consumption.

b. Installation costs: The installation cost is part of the cost of the asset. But in installation

costs, there are still two component of costs are involved i.e. variable and fixed. For example,

Installation of Dryer and washer are the fixed costs whereas cost of improvement,

consumable material used in the teardown and the personnel costs in changing over period of

time is considered as variable costs (Schaltegger and Zvezdov, 2015).

c. Energy or Electricity costs: Energy costs are the costs which are incurred at the time of

using an electricity machine to manufacture some products or provide some services to the

3 | P a g e

1. Cost

Cost is the monetary value that has been spent by every company in order to produce

services for their customers. It is one of the essential expenditures that must be made by the

company in order to run a business in an appropriate manner. Each production factor has an

associated cost (Kaplan and Atkinson, 2015).

Following there are different types of cost which are associated with the service based

company which are listed below:

1. Variable and fixed costs

2. Indirect and Direct costs

3. Period and Product costs

4. Opportunity and Incremental costs

5. Sunk costs

After considering the various different types of costs which are discussed in the stated

case, three types of costs are selected for further discussion which are mentioned

below:

a. Utility costs: Utility costs are all charges for utilities which have to be paid by the company

on the basis of usage. This cost is considered as a mixed cost in which both cost i.e. fixed

and variable are charged on a products or services based on actual usage (Haroun, 2015).

Some of the examples of utility costs are:

Heat (gas)

Water

Telephone and internet service

Sewer

The cost of utility follow the concept of accrual basis of accounting in which all costs which

are related to the utility are recorded on the basis of actual consumption.

b. Installation costs: The installation cost is part of the cost of the asset. But in installation

costs, there are still two component of costs are involved i.e. variable and fixed. For example,

Installation of Dryer and washer are the fixed costs whereas cost of improvement,

consumable material used in the teardown and the personnel costs in changing over period of

time is considered as variable costs (Schaltegger and Zvezdov, 2015).

c. Energy or Electricity costs: Energy costs are the costs which are incurred at the time of

using an electricity machine to manufacture some products or provide some services to the

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

customers. Electricity costs are variable in nature and depend upon real consumption of

electricity. For example, the electricity costs depend upon the actual usage of Dryer and

Washer in washing the clothes (Klychova, et. al., 2015).

2. Decision

a. Relevant information to purchase the appliances

The costs of both appliances are:

For Dryer $380

For Washer $420

$800

Add: Installation cost $43.72

Delivery cost $35.00

$878.72

If Douglas and Pamela purchase the appliances they have to pay $878.72 and it also

provides benefits to them which are listed below:

1. It reduces the time and extra expenses.

2. One time investment and long-time benefit.

3. Reduces extra efforts of going here and there.

4. Safer, faster and easier to use.

b. Irrelevant information to purchase the appliances

While purchasing the new appliances following information are irrelevant which is mentioned

below:

1. Launder and dry clean the clothes from the Red Oak which charges $52 per month.

2. Self-service in which Franks wash the clothes to the Laundromat.

3. Purchasing laundry supplies in bulk from Mega Mart at a cost of $35 every quarter.

The above information is not useful while purchasing a new dryer and washer. The

information which influence the Franks decision is the price of the appliances and various

4 | P a g e

electricity. For example, the electricity costs depend upon the actual usage of Dryer and

Washer in washing the clothes (Klychova, et. al., 2015).

2. Decision

a. Relevant information to purchase the appliances

The costs of both appliances are:

For Dryer $380

For Washer $420

$800

Add: Installation cost $43.72

Delivery cost $35.00

$878.72

If Douglas and Pamela purchase the appliances they have to pay $878.72 and it also

provides benefits to them which are listed below:

1. It reduces the time and extra expenses.

2. One time investment and long-time benefit.

3. Reduces extra efforts of going here and there.

4. Safer, faster and easier to use.

b. Irrelevant information to purchase the appliances

While purchasing the new appliances following information are irrelevant which is mentioned

below:

1. Launder and dry clean the clothes from the Red Oak which charges $52 per month.

2. Self-service in which Franks wash the clothes to the Laundromat.

3. Purchasing laundry supplies in bulk from Mega Mart at a cost of $35 every quarter.

The above information is not useful while purchasing a new dryer and washer. The

information which influence the Franks decision is the price of the appliances and various

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

advantage provide by the both appliances in the future is important for couple ( Sakao and

Lindahl, 2015).

3. Cost to launder clothes

For calculation 4.33 weeks per month is taken

(a) Launder clothes to Red Oak Laundry and Dry Cleaning

Cost to launder clothes = $52*4.33=$225.16

(b) Launder clothes to Laundromat

Cost to launder clothes = 3*2*$0.56*$8 = $26.88

Add: Purchasing laundry supplies (converted into weeks) $35/12 = $2.917

Total cost = $26.88 + $2.917 =$29.797

While doing calculation in (a) and (b) part, it can be concluded that (b) option is suitable for

the Franks because the cost is low as compare to (a) part. The Franks should launder their

clothes to Laundromat.

4. For 3 children

Franks charge a fee for $800 per month for each child = $800*3 =$2400

Cost of hiring new employees = $9*40 = $360

Remaining profit = $2400 -$360 = $2040

Yes, the Franks should hire the additional employee how manages the extra children in an

appropriate manner. For hiring the new employees the extra expenses of $360 will be

incurred by the Franks. They should appoint at least 2 employees if they have already 3

employees.

5. Letter to the Franks advising them on their space options.

1/1/2019

To Franks,

Re: Advice regarding whether they operate child care business at home or space rent

in town.

5 | P a g e

Lindahl, 2015).

3. Cost to launder clothes

For calculation 4.33 weeks per month is taken

(a) Launder clothes to Red Oak Laundry and Dry Cleaning

Cost to launder clothes = $52*4.33=$225.16

(b) Launder clothes to Laundromat

Cost to launder clothes = 3*2*$0.56*$8 = $26.88

Add: Purchasing laundry supplies (converted into weeks) $35/12 = $2.917

Total cost = $26.88 + $2.917 =$29.797

While doing calculation in (a) and (b) part, it can be concluded that (b) option is suitable for

the Franks because the cost is low as compare to (a) part. The Franks should launder their

clothes to Laundromat.

4. For 3 children

Franks charge a fee for $800 per month for each child = $800*3 =$2400

Cost of hiring new employees = $9*40 = $360

Remaining profit = $2400 -$360 = $2040

Yes, the Franks should hire the additional employee how manages the extra children in an

appropriate manner. For hiring the new employees the extra expenses of $360 will be

incurred by the Franks. They should appoint at least 2 employees if they have already 3

employees.

5. Letter to the Franks advising them on their space options.

1/1/2019

To Franks,

Re: Advice regarding whether they operate child care business at home or space rent

in town.

5 | P a g e

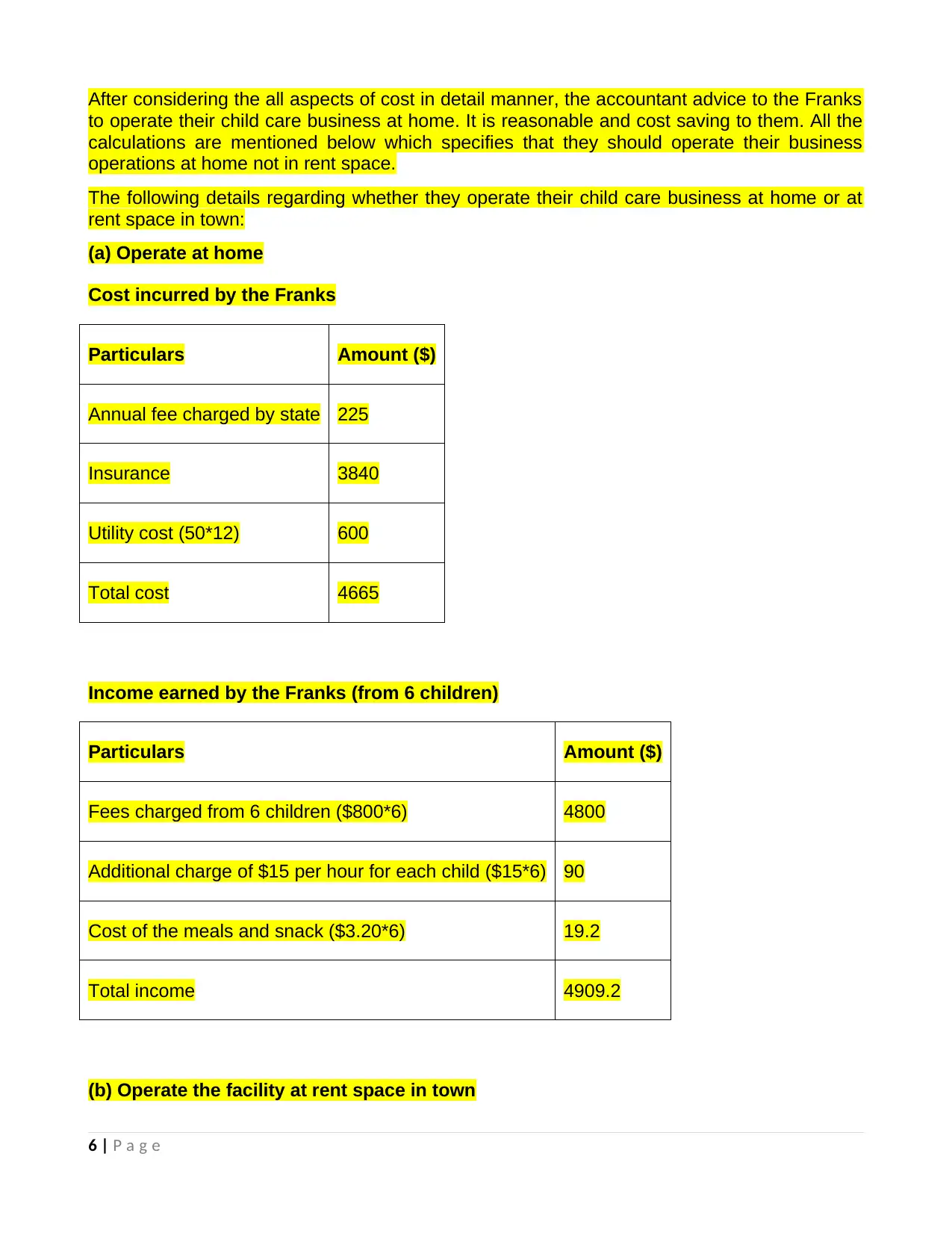

After considering the all aspects of cost in detail manner, the accountant advice to the Franks

to operate their child care business at home. It is reasonable and cost saving to them. All the

calculations are mentioned below which specifies that they should operate their business

operations at home not in rent space.

The following details regarding whether they operate their child care business at home or at

rent space in town:

(a) Operate at home

Cost incurred by the Franks

Particulars Amount ($)

Annual fee charged by state 225

Insurance 3840

Utility cost (50*12) 600

Total cost 4665

Income earned by the Franks (from 6 children)

Particulars Amount ($)

Fees charged from 6 children ($800*6) 4800

Additional charge of $15 per hour for each child ($15*6) 90

Cost of the meals and snack ($3.20*6) 19.2

Total income 4909.2

(b) Operate the facility at rent space in town

6 | P a g e

to operate their child care business at home. It is reasonable and cost saving to them. All the

calculations are mentioned below which specifies that they should operate their business

operations at home not in rent space.

The following details regarding whether they operate their child care business at home or at

rent space in town:

(a) Operate at home

Cost incurred by the Franks

Particulars Amount ($)

Annual fee charged by state 225

Insurance 3840

Utility cost (50*12) 600

Total cost 4665

Income earned by the Franks (from 6 children)

Particulars Amount ($)

Fees charged from 6 children ($800*6) 4800

Additional charge of $15 per hour for each child ($15*6) 90

Cost of the meals and snack ($3.20*6) 19.2

Total income 4909.2

(b) Operate the facility at rent space in town

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

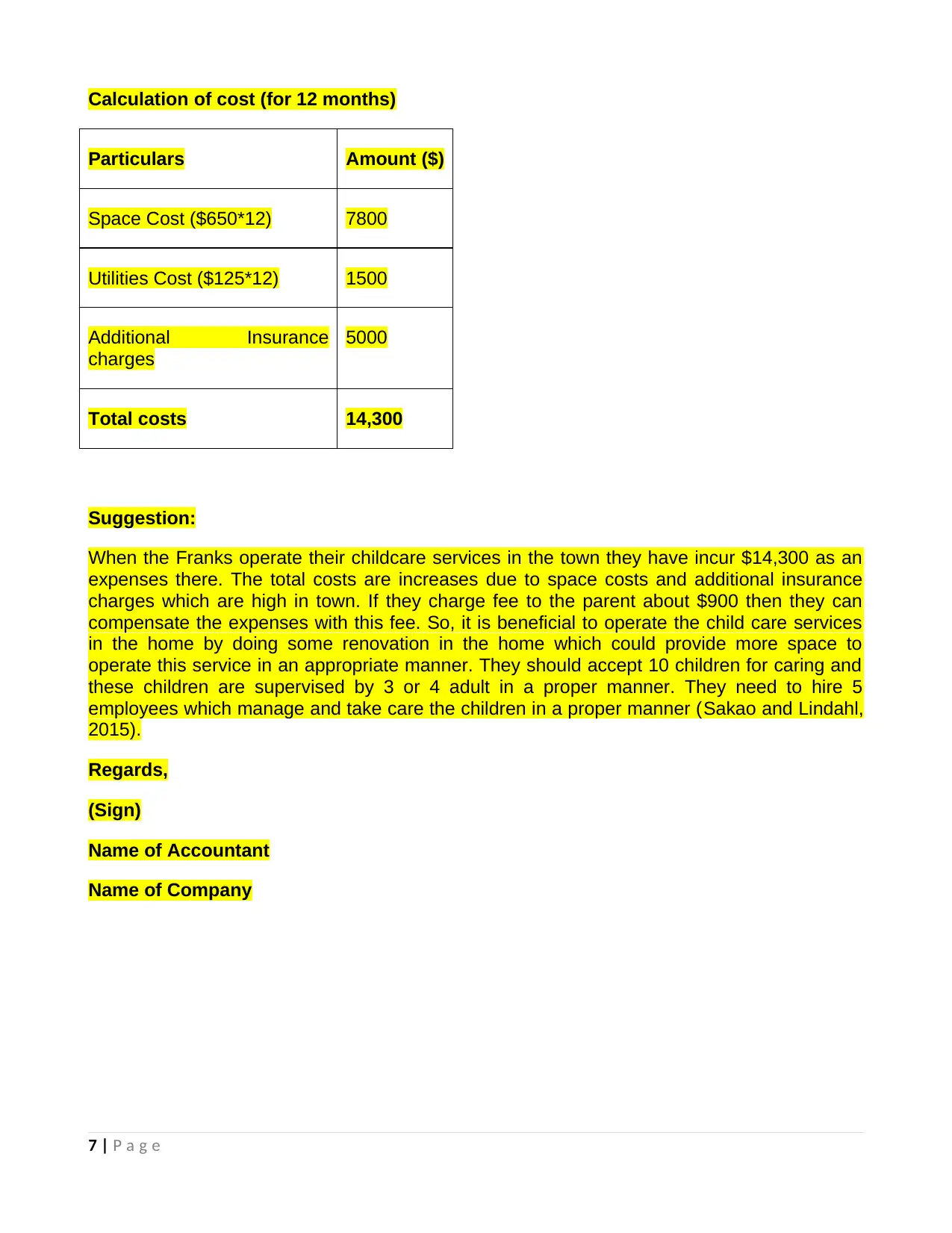

Calculation of cost (for 12 months)

Particulars Amount ($)

Space Cost ($650*12) 7800

Utilities Cost ($125*12) 1500

Additional Insurance

charges

5000

Total costs 14,300

Suggestion:

When the Franks operate their childcare services in the town they have incur $14,300 as an

expenses there. The total costs are increases due to space costs and additional insurance

charges which are high in town. If they charge fee to the parent about $900 then they can

compensate the expenses with this fee. So, it is beneficial to operate the child care services

in the home by doing some renovation in the home which could provide more space to

operate this service in an appropriate manner. They should accept 10 children for caring and

these children are supervised by 3 or 4 adult in a proper manner. They need to hire 5

employees which manage and take care the children in a proper manner (Sakao and Lindahl,

2015).

Regards,

(Sign)

Name of Accountant

Name of Company

7 | P a g e

Particulars Amount ($)

Space Cost ($650*12) 7800

Utilities Cost ($125*12) 1500

Additional Insurance

charges

5000

Total costs 14,300

Suggestion:

When the Franks operate their childcare services in the town they have incur $14,300 as an

expenses there. The total costs are increases due to space costs and additional insurance

charges which are high in town. If they charge fee to the parent about $900 then they can

compensate the expenses with this fee. So, it is beneficial to operate the child care services

in the home by doing some renovation in the home which could provide more space to

operate this service in an appropriate manner. They should accept 10 children for caring and

these children are supervised by 3 or 4 adult in a proper manner. They need to hire 5

employees which manage and take care the children in a proper manner (Sakao and Lindahl,

2015).

Regards,

(Sign)

Name of Accountant

Name of Company

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Part B

Question 1

The process of identifying, measuring, analyzing, interpreting and communicating information

to the managers of the organization is known as managerial accounting. The information

relating to managerial accounting and the data used in the managerial accounting helps the

managers of the firm for decision making (Cheng, et. al., 2015). The preparation of non-

financial accounts such as tax authorities and regulatory agencies are also included under

management accounting. The decisions taken by the managers are deeply affected by these

components; the components are briefly discussed below:

Risk management system:

The practices and preparations used to determine, managing, gauging and reporting risks for

attainment and achievement of the objectives and goals of the business. The determination of

risks or the barriers once done, it can gauge the risk (that is it can estimate the volume or

impact of the risk on the company), so that management according to that risk can be done

and it can be interpreted and communicated further to the managers for the process of

decision making (Weygandt, et. al., 2018). If the risks are identified on time and the data is

collected on the time it can let the company know about the barricades and thus a framework

can be prepared accordingly. Thus identification of risks in the business is a primary

component of the management accounting system. The identification of the problems

concerned within the drums of the machines associated with the identification of risks which

might disrupt the business and may be extraordinarily expensive within the long-term within

the case of Canon. Thus if the problem and risks of the canon are identified (Brewer,

Garrison, and Noreen, 2015). The framework and preparations can be done accordingly and

the disruption can be reduced or stopped (Collis and Hussey, 2017).

Performance management system:

It helps in decision making and manages the organization's performance. The organizational

goals are communicated to the employees individually, which allows the individual's tasks and

accountability towards the goals and achievement of objectives, thus this process also helps

in identifying and keeping track on the progress towards attainment of the goal (Gurcanli, Bilir,

and Sevim, 2015). This tool also helps in identifying the ability and performance of each and

every employee, which keeps a record and track of all the workers and employees in the

organization. The decision making is again and again practiced due to this tool. The manager

easily allocates their resources and subsequently track the results in the growth and

expansion of the organization. Canons performance was declining within

the early Seventies and it had been needed to bring one thing new the market to counter

growing threats from Xerox and conjointly at identical time long-faced matters of delivery one

thing which might be valuable for tiny offices and be more cost-effective (Tsai, et. al., 2014).

Each there was hardly any technology accessible thereto impact. This showed that the

management team of the corporate was thinking of the longer term performance and tried to

usher in one thing which might be able to alter the complete market structure for many years

to return within the kind of mini Copper copiers. This showed that the management leaders at

8 | P a g e

Question 1

The process of identifying, measuring, analyzing, interpreting and communicating information

to the managers of the organization is known as managerial accounting. The information

relating to managerial accounting and the data used in the managerial accounting helps the

managers of the firm for decision making (Cheng, et. al., 2015). The preparation of non-

financial accounts such as tax authorities and regulatory agencies are also included under

management accounting. The decisions taken by the managers are deeply affected by these

components; the components are briefly discussed below:

Risk management system:

The practices and preparations used to determine, managing, gauging and reporting risks for

attainment and achievement of the objectives and goals of the business. The determination of

risks or the barriers once done, it can gauge the risk (that is it can estimate the volume or

impact of the risk on the company), so that management according to that risk can be done

and it can be interpreted and communicated further to the managers for the process of

decision making (Weygandt, et. al., 2018). If the risks are identified on time and the data is

collected on the time it can let the company know about the barricades and thus a framework

can be prepared accordingly. Thus identification of risks in the business is a primary

component of the management accounting system. The identification of the problems

concerned within the drums of the machines associated with the identification of risks which

might disrupt the business and may be extraordinarily expensive within the long-term within

the case of Canon. Thus if the problem and risks of the canon are identified (Brewer,

Garrison, and Noreen, 2015). The framework and preparations can be done accordingly and

the disruption can be reduced or stopped (Collis and Hussey, 2017).

Performance management system:

It helps in decision making and manages the organization's performance. The organizational

goals are communicated to the employees individually, which allows the individual's tasks and

accountability towards the goals and achievement of objectives, thus this process also helps

in identifying and keeping track on the progress towards attainment of the goal (Gurcanli, Bilir,

and Sevim, 2015). This tool also helps in identifying the ability and performance of each and

every employee, which keeps a record and track of all the workers and employees in the

organization. The decision making is again and again practiced due to this tool. The manager

easily allocates their resources and subsequently track the results in the growth and

expansion of the organization. Canons performance was declining within

the early Seventies and it had been needed to bring one thing new the market to counter

growing threats from Xerox and conjointly at identical time long-faced matters of delivery one

thing which might be valuable for tiny offices and be more cost-effective (Tsai, et. al., 2014).

Each there was hardly any technology accessible thereto impact. This showed that the

management team of the corporate was thinking of the longer term performance and tried to

usher in one thing which might be able to alter the complete market structure for many years

to return within the kind of mini Copper copiers. This showed that the management leaders at

8 | P a g e

canon were committed to making a brand new performing arts system that matches their

long-run goals and vision (Fisher and Krumwiede, 2015).

Strategic management:

The process that includes continuous monitoring, planning, analyses and assessment to meet

the organizational goals and objectives is known as the strategic management. The strategies

that are created and applied by the companies are to be done quickly and make decisions

according to them so that the customers are attracted and the competition is also faced

accordingly. To remain successful and achieve the goals and objectives on time the

organization has to make good and competitive strategies. The tactical decisions will also

help the organizations to maintain the qualitative and quantitative features and aspects of the

firm (Otley, 2016). The development of low price in MAC computers project undertaken by

Apple was the associate degree instance of operating toward the accomplishment of a

visionary goal and transportation the low price universal computers to the plenty. The success

of the project can be stapled right down to not solely strategic vision displayed by the leaders

of the corporate however by a high level of commitment shown by the team members

engaged within the style and development method (Dale and Plunkett, 2017).

Question 2

In this case, the end result of social interaction which had created new information

regarding business was the example of innovation. Just because of the increment in

the social transactions all this innovation was possible. The contribution of

management accounting in this process is as follows:

It helps in identifying the risks before time and also helps in determining the barricades

of the firm.

As it helps in identifying the issues to the earliest, the preparations and framework can

also be done accordingly, the management is able to easily make decisions.

Economic trends are also included in these reports of management accounting which

would help the managers and the firm to get new and creative ideas for the firm

(Estrada and Romero, 2016).

The management accounting system will be required in the new interactive process of

developing ideas. Thus a decision is only based on these inputs.

The tech and new benchmarking would not be possible without the deep collaboration

of management accounting system. Hence the management accounting system helps

in giving innovative ideas and new idea generation (Cokins, Cherian, and Schwer,

2015).

Whether the innovation involves the design of the merchandise as within the case of

the canon or the event of a completely new product as incontestable within the case of

Apple, the management accounting system remains concerned at every step.

9 | P a g e

long-run goals and vision (Fisher and Krumwiede, 2015).

Strategic management:

The process that includes continuous monitoring, planning, analyses and assessment to meet

the organizational goals and objectives is known as the strategic management. The strategies

that are created and applied by the companies are to be done quickly and make decisions

according to them so that the customers are attracted and the competition is also faced

accordingly. To remain successful and achieve the goals and objectives on time the

organization has to make good and competitive strategies. The tactical decisions will also

help the organizations to maintain the qualitative and quantitative features and aspects of the

firm (Otley, 2016). The development of low price in MAC computers project undertaken by

Apple was the associate degree instance of operating toward the accomplishment of a

visionary goal and transportation the low price universal computers to the plenty. The success

of the project can be stapled right down to not solely strategic vision displayed by the leaders

of the corporate however by a high level of commitment shown by the team members

engaged within the style and development method (Dale and Plunkett, 2017).

Question 2

In this case, the end result of social interaction which had created new information

regarding business was the example of innovation. Just because of the increment in

the social transactions all this innovation was possible. The contribution of

management accounting in this process is as follows:

It helps in identifying the risks before time and also helps in determining the barricades

of the firm.

As it helps in identifying the issues to the earliest, the preparations and framework can

also be done accordingly, the management is able to easily make decisions.

Economic trends are also included in these reports of management accounting which

would help the managers and the firm to get new and creative ideas for the firm

(Estrada and Romero, 2016).

The management accounting system will be required in the new interactive process of

developing ideas. Thus a decision is only based on these inputs.

The tech and new benchmarking would not be possible without the deep collaboration

of management accounting system. Hence the management accounting system helps

in giving innovative ideas and new idea generation (Cokins, Cherian, and Schwer,

2015).

Whether the innovation involves the design of the merchandise as within the case of

the canon or the event of a completely new product as incontestable within the case of

Apple, the management accounting system remains concerned at every step.

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 3

Following points are useful for management accountants which help them in

improving their skills and knowledge and also improve the efficiency of the company

in an appropriate manner:

Before the Silicon Valley revolution took place the Japanese were leading in the

world and a profitable and good existence was already taken by them in the product

line. The new ideas were given preference and a renovation in the innovation was

needed by analysing thoroughly whether they make a business sense or not. There

were good discipline and uniformity in the manpower. The example of Canon shows

that if the aim is to get a better idea than the existing one, then even the chaos can

also become beneficial, the MC project put in practice is an example of increment in

effective research through social interaction (Bhimani and Willcocks, 2014).

However, it should be remembered that making chaos isn't the motive. This involves

putting in place of Associate in a Nursing setting within

which individuals will participate and it may be chaotic however an equivalent could

be a precursor to raised concepts. Concepts may be artistic and are available out of

arguments. Typically concepts may be a mixture of various concepts (Butler and

Ghosh, 2015). But the management and also the participants of the human

process would want to acknowledge the very fact that chaos can’t be allowed to

require precedence and the corporate management should have integrative ability to

convert these concepts into reality. Firms would want to figure wholeheartedly into

developing and giving the concepts a form. But if completely different

concepts square measure being worked upon by different groups then it should be

ensured they don’t overlap and if this not avoided an equivalent wouldn't end

in any kind of synergism (Maas, Schaltegger, and Crutzen, 2016).

Even in chaotic situations, the leaders come up where the management of the firm is

under high pressure. The leader is not allowed and not advised to action an

autocratic manner but in a catalyst way. The innovative ideas become a mandatory

part for the leader to be done. Even in the chaotic situation, a leader has to take

decisions which are crucial and critical for the organization. Hence the understanding

of the exact situation is very important for companies to come out of chaos such as

Canon (Bromwich and Scapens, 2016).

Companies would want to develop smaller however capable core teams which might

be needed to require half in intense social interactive sessions to bring out new

concepts and new meanings. They additionally ought to develop and demonstrate a

high level of commitment. Additionally, the most organization would even be needed

to self-organize. Self-organizing necessities terribly high in today's atmosphere as

their interactions would be a lot of emerging and that they would be ready to develop

new meanings from anything (Brands and Holtzblatt, 2015).

11 | P a g e

Following points are useful for management accountants which help them in

improving their skills and knowledge and also improve the efficiency of the company

in an appropriate manner:

Before the Silicon Valley revolution took place the Japanese were leading in the

world and a profitable and good existence was already taken by them in the product

line. The new ideas were given preference and a renovation in the innovation was

needed by analysing thoroughly whether they make a business sense or not. There

were good discipline and uniformity in the manpower. The example of Canon shows

that if the aim is to get a better idea than the existing one, then even the chaos can

also become beneficial, the MC project put in practice is an example of increment in

effective research through social interaction (Bhimani and Willcocks, 2014).

However, it should be remembered that making chaos isn't the motive. This involves

putting in place of Associate in a Nursing setting within

which individuals will participate and it may be chaotic however an equivalent could

be a precursor to raised concepts. Concepts may be artistic and are available out of

arguments. Typically concepts may be a mixture of various concepts (Butler and

Ghosh, 2015). But the management and also the participants of the human

process would want to acknowledge the very fact that chaos can’t be allowed to

require precedence and the corporate management should have integrative ability to

convert these concepts into reality. Firms would want to figure wholeheartedly into

developing and giving the concepts a form. But if completely different

concepts square measure being worked upon by different groups then it should be

ensured they don’t overlap and if this not avoided an equivalent wouldn't end

in any kind of synergism (Maas, Schaltegger, and Crutzen, 2016).

Even in chaotic situations, the leaders come up where the management of the firm is

under high pressure. The leader is not allowed and not advised to action an

autocratic manner but in a catalyst way. The innovative ideas become a mandatory

part for the leader to be done. Even in the chaotic situation, a leader has to take

decisions which are crucial and critical for the organization. Hence the understanding

of the exact situation is very important for companies to come out of chaos such as

Canon (Bromwich and Scapens, 2016).

Companies would want to develop smaller however capable core teams which might

be needed to require half in intense social interactive sessions to bring out new

concepts and new meanings. They additionally ought to develop and demonstrate a

high level of commitment. Additionally, the most organization would even be needed

to self-organize. Self-organizing necessities terribly high in today's atmosphere as

their interactions would be a lot of emerging and that they would be ready to develop

new meanings from anything (Brands and Holtzblatt, 2015).

11 | P a g e

References

Bhimani, A. and Willcocks, L., 2014. Digitisation,‘Big Data’and the transformation of

accounting information. Accounting and Business Research, 44(4), pp.469-490.

Brands, K. and Holtzblatt, M., 2015. Business Analytics: Transforming the Role of

Management Accountants. Management Accounting Quarterly, 16(3).

Brewer, P.C., Garrison, R.H. and Noreen, E.W., 2015. Introduction to managerial accounting.

McGraw-Hill Education.

Bromwich, M. and Scapens, R.W., 2016. Management accounting research: 25 years

on. Management Accounting Research, 31, pp.1-9.

Butler, S.A. and Ghosh, D., 2015. Individual differences in managerial accounting judgments

and decision making. The British Accounting Review, 47(1), pp.33-45.

Cheng, Y., Tao, F., Zhang, L. and Zuo, Y., 2015. Supply-demand matching of manufacturing

service in service-oriented manufacturing systems. Comput. Integr. Manuf. Syst, 21(7),

pp.1930-1940.

Cokins, G., Cherian, J. and Schwer, P., 2015. Don't be stuck in the last century! It's time for

management accountants to work with decision makers and give them the information they

need to do their jobs. Strategic Finance, 97(4), pp.26-34.

Collis, J. and Hussey, R., 2017. Cost and management accounting. Macmillan International

Higher Education.

Dale, B.G. and Plunkett, J.J., 2017. Quality costing. Routledge.

Estrada, A. and Romero, D., 2016. Towards a cost engineering method for product-service

systems based on a system cost uncertainty analysis. Procedia CIRP, 47, pp.84-89.

Fisher, J.G. and Krumwiede, K., 2015. Product costing systems: Finding the right

approach. Journal of Corporate Accounting & Finance, 26(4), pp.13-21.

Gurcanli, G.E., Bilir, S. and Sevim, M., 2015. Activity based risk assessment and safety cost

estimation for residential building construction projects. Safety science, 80, pp.1-12.

Haroun, A.E., 2015. Maintenance cost estimation: application of activity-based costing as a

fair estimate method. Journal of Quality in Maintenance Engineering, 21(3), pp.258-270.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Klychova, G.S., Zakirova, A.R., Zakirov, Z.R. and Valieva, G.R., 2015. Management aspects

of production cost accounting in horse breeding. Asian Social Science, 11(11), p.308.

12 | P a g e

Bhimani, A. and Willcocks, L., 2014. Digitisation,‘Big Data’and the transformation of

accounting information. Accounting and Business Research, 44(4), pp.469-490.

Brands, K. and Holtzblatt, M., 2015. Business Analytics: Transforming the Role of

Management Accountants. Management Accounting Quarterly, 16(3).

Brewer, P.C., Garrison, R.H. and Noreen, E.W., 2015. Introduction to managerial accounting.

McGraw-Hill Education.

Bromwich, M. and Scapens, R.W., 2016. Management accounting research: 25 years

on. Management Accounting Research, 31, pp.1-9.

Butler, S.A. and Ghosh, D., 2015. Individual differences in managerial accounting judgments

and decision making. The British Accounting Review, 47(1), pp.33-45.

Cheng, Y., Tao, F., Zhang, L. and Zuo, Y., 2015. Supply-demand matching of manufacturing

service in service-oriented manufacturing systems. Comput. Integr. Manuf. Syst, 21(7),

pp.1930-1940.

Cokins, G., Cherian, J. and Schwer, P., 2015. Don't be stuck in the last century! It's time for

management accountants to work with decision makers and give them the information they

need to do their jobs. Strategic Finance, 97(4), pp.26-34.

Collis, J. and Hussey, R., 2017. Cost and management accounting. Macmillan International

Higher Education.

Dale, B.G. and Plunkett, J.J., 2017. Quality costing. Routledge.

Estrada, A. and Romero, D., 2016. Towards a cost engineering method for product-service

systems based on a system cost uncertainty analysis. Procedia CIRP, 47, pp.84-89.

Fisher, J.G. and Krumwiede, K., 2015. Product costing systems: Finding the right

approach. Journal of Corporate Accounting & Finance, 26(4), pp.13-21.

Gurcanli, G.E., Bilir, S. and Sevim, M., 2015. Activity based risk assessment and safety cost

estimation for residential building construction projects. Safety science, 80, pp.1-12.

Haroun, A.E., 2015. Maintenance cost estimation: application of activity-based costing as a

fair estimate method. Journal of Quality in Maintenance Engineering, 21(3), pp.258-270.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Klychova, G.S., Zakirova, A.R., Zakirov, Z.R. and Valieva, G.R., 2015. Management aspects

of production cost accounting in horse breeding. Asian Social Science, 11(11), p.308.

12 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability

assessment, management accounting, control, and reporting. Journal of Cleaner

Production, 136, pp.237-248.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, pp.45-62.

Sakao, T. and Lindahl, M., 2015. A method to improve integrated product service offerings

based on life cycle costing. CIRP annals, 64(1), pp.33-36.

Schaltegger, S. and Zvezdov, D., 2015. Expanding material flow cost accounting. Framework,

review and potentials. Journal of Cleaner Production, 108, pp.1333-1341.

Tsai, W.H., Yang, C.H., Chang, J.C. and Lee, H.L., 2014. An activity-based costing decision

model for life cycle assessment in green building projects. European Journal of Operational

Research, 238(2), pp.607-619.

Weygandt, J.J., Kieso, D.E., Kimmel, P.D. and Aly, I.M., 2018. Managerial Accounting: Tools

for Business Decision-making. John Wiley & Sons Canada, Limited.

13 | P a g e

assessment, management accounting, control, and reporting. Journal of Cleaner

Production, 136, pp.237-248.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, pp.45-62.

Sakao, T. and Lindahl, M., 2015. A method to improve integrated product service offerings

based on life cycle costing. CIRP annals, 64(1), pp.33-36.

Schaltegger, S. and Zvezdov, D., 2015. Expanding material flow cost accounting. Framework,

review and potentials. Journal of Cleaner Production, 108, pp.1333-1341.

Tsai, W.H., Yang, C.H., Chang, J.C. and Lee, H.L., 2014. An activity-based costing decision

model for life cycle assessment in green building projects. European Journal of Operational

Research, 238(2), pp.607-619.

Weygandt, J.J., Kieso, D.E., Kimmel, P.D. and Aly, I.M., 2018. Managerial Accounting: Tools

for Business Decision-making. John Wiley & Sons Canada, Limited.

13 | P a g e

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.