Managerial Economics: Analyzing Market Forces and Elasticity

VerifiedAdded on 2023/04/25

|29

|5345

|61

Report

AI Summary

This report provides a comprehensive analysis of managerial economics principles, focusing on supply, demand, and elasticity. It begins by defining the supply schedule and exploring factors affecting supply, such as commodity price, prices of other goods, input costs, technology, and government policies. The report then discusses the concept of perfectly inelastic demand and its impact on market equilibrium, demonstrating how increased supply affects equilibrium price when demand remains constant. Further, it delves into the degrees of elasticity of demand, including perfectly elastic, perfectly inelastic, unitary elastic, elastic, and inelastic demand, supported by relevant diagrams. The point elasticity method is also explained, along with examples of goods with elastic and inelastic demand. Finally, the report applies these concepts to analyze specific market scenarios, such as the market for newspapers, St. Louis Rams T-shirts, bagels, and economics textbooks, providing a thorough understanding of market dynamics and elasticity in various contexts.

Running head: MANAGERIAL ECONOMICS

Managerial Economics

Name of the Student

Name of the University

Student ID

Managerial Economics

Name of the Student

Name of the University

Student ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGERIAL ECONOMICS

Table of Contents

Question 1..................................................................................................................................3

Question a...............................................................................................................................3

Question b..............................................................................................................................5

Question 2..................................................................................................................................6

Degrees of elasticity of demand.............................................................................................6

Point elasticity method.........................................................................................................11

Question 3................................................................................................................................13

Question a.............................................................................................................................13

Question b............................................................................................................................14

Question 4................................................................................................................................16

Question a.............................................................................................................................16

Question b............................................................................................................................17

Question 5................................................................................................................................18

Question a: market for newspaper in the town.....................................................................18

Question b: The market for St. Louis Rams cotton T-shirts................................................20

Question c: The market for bagels.......................................................................................21

Question d: The market for Krugman and Wells economics textbook................................23

Question 6................................................................................................................................24

Question a.............................................................................................................................24

Question b............................................................................................................................25

Question c.............................................................................................................................25

References................................................................................................................................26

Table of Contents

Question 1..................................................................................................................................3

Question a...............................................................................................................................3

Question b..............................................................................................................................5

Question 2..................................................................................................................................6

Degrees of elasticity of demand.............................................................................................6

Point elasticity method.........................................................................................................11

Question 3................................................................................................................................13

Question a.............................................................................................................................13

Question b............................................................................................................................14

Question 4................................................................................................................................16

Question a.............................................................................................................................16

Question b............................................................................................................................17

Question 5................................................................................................................................18

Question a: market for newspaper in the town.....................................................................18

Question b: The market for St. Louis Rams cotton T-shirts................................................20

Question c: The market for bagels.......................................................................................21

Question d: The market for Krugman and Wells economics textbook................................23

Question 6................................................................................................................................24

Question a.............................................................................................................................24

Question b............................................................................................................................25

Question c.............................................................................................................................25

References................................................................................................................................26

2MANAGERIAL ECONOMICS

Question 1

Question a

Supply schedule

Supply schedule is the presentation of quantity supplied corresponding to various

prices in a table form. The supply schedule shows various quantities of the supplied good at

different prices. It indicates relation between price and quantity supplied when all other non-

price factors remain constant. Supply schedules are of two kinds. These are individual supply

schedule and market supply schedule (Varian 2014). The individual supply schedule captures

the supply of an individual seller or firm in relation to own price. In contrast, market supply

schedule is the sum of individual supply schedules. It represents total supply in the market at

various prices.

Different factors affecting supply

In the market, there are different important factors that determine supply of a good.

Change in any of these factors lead to a corresponding change in supply of the good. Given

below are some of the important factors affecting supply of a commodity.

Price of the commodity

The most vital determinant of supply is the price. Following the law of supply, there

is a direct relation between price and supply of a good. That means with increase in price of a

good its supply increases and vice versa. This is because of the simple reason. As price of

good increases, producers have a higher possibility of making profit (Wetzstein 2013). It

encourages them to supply more in order to increase sale in the market.

Price of other goods

Question 1

Question a

Supply schedule

Supply schedule is the presentation of quantity supplied corresponding to various

prices in a table form. The supply schedule shows various quantities of the supplied good at

different prices. It indicates relation between price and quantity supplied when all other non-

price factors remain constant. Supply schedules are of two kinds. These are individual supply

schedule and market supply schedule (Varian 2014). The individual supply schedule captures

the supply of an individual seller or firm in relation to own price. In contrast, market supply

schedule is the sum of individual supply schedules. It represents total supply in the market at

various prices.

Different factors affecting supply

In the market, there are different important factors that determine supply of a good.

Change in any of these factors lead to a corresponding change in supply of the good. Given

below are some of the important factors affecting supply of a commodity.

Price of the commodity

The most vital determinant of supply is the price. Following the law of supply, there

is a direct relation between price and supply of a good. That means with increase in price of a

good its supply increases and vice versa. This is because of the simple reason. As price of

good increases, producers have a higher possibility of making profit (Wetzstein 2013). It

encourages them to supply more in order to increase sale in the market.

Price of other goods

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGERIAL ECONOMICS

Many resources have alternative uses. Because of this quantity supplied of a good

depends not only on its own price but also on price of other goods. If price of other god

increases, then it is more profitable to produce other goods in relation to the given

commodity. The firm then shifts the limited resources from production of concerned goods to

the production of more profitable alternatives. This results in a decline in supply of the given

commodity.

Price of inputs

If firms face a higher cost payable to the used factors of production and a higher cost

of inputs, there is a higher cost of production. Higher production cost implies a lower

profitability and hence, a decline in supply of the concerned commodity (Nicholson and

Snyder 2014). In contrast, a decline in factor prices or input price means a lower cost of

production. This results in an increase in supply of the product.

State of technology

Supply of a commodity varies with the state of technology. Adaption of innovative

and advanced technology lowers production cost and raises profitability of firms. The higher

profitability encourages producers to supply more. Outdate technology or technological

degradation on the other hand increase reduces profitability and hence, lowers supply.

Government policy

Government adapts several policies to intervene in the market. Such policies either

positively or negatively affects supply of a commodity. For example, if government increases

tax then there is a decline in profitability inducing firms to supply less (Banerjee 2014). The

policy tax concession or government subsidy on the other hand increases supply by lowering

effective cost of production.

Many resources have alternative uses. Because of this quantity supplied of a good

depends not only on its own price but also on price of other goods. If price of other god

increases, then it is more profitable to produce other goods in relation to the given

commodity. The firm then shifts the limited resources from production of concerned goods to

the production of more profitable alternatives. This results in a decline in supply of the given

commodity.

Price of inputs

If firms face a higher cost payable to the used factors of production and a higher cost

of inputs, there is a higher cost of production. Higher production cost implies a lower

profitability and hence, a decline in supply of the concerned commodity (Nicholson and

Snyder 2014). In contrast, a decline in factor prices or input price means a lower cost of

production. This results in an increase in supply of the product.

State of technology

Supply of a commodity varies with the state of technology. Adaption of innovative

and advanced technology lowers production cost and raises profitability of firms. The higher

profitability encourages producers to supply more. Outdate technology or technological

degradation on the other hand increase reduces profitability and hence, lowers supply.

Government policy

Government adapts several policies to intervene in the market. Such policies either

positively or negatively affects supply of a commodity. For example, if government increases

tax then there is a decline in profitability inducing firms to supply less (Banerjee 2014). The

policy tax concession or government subsidy on the other hand increases supply by lowering

effective cost of production.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGERIAL ECONOMICS

Objective of the firm

As stated by law of supply, supply of a commodity increases at a higher price as a

relatively higher price fulfills firms’ profit maximization goal. Some firms however might

agree to supply more at a lower price even if the price does not maximize profits. The goals

of such firms is to capture a higher share in the market in order to strengthen their position in

the market.

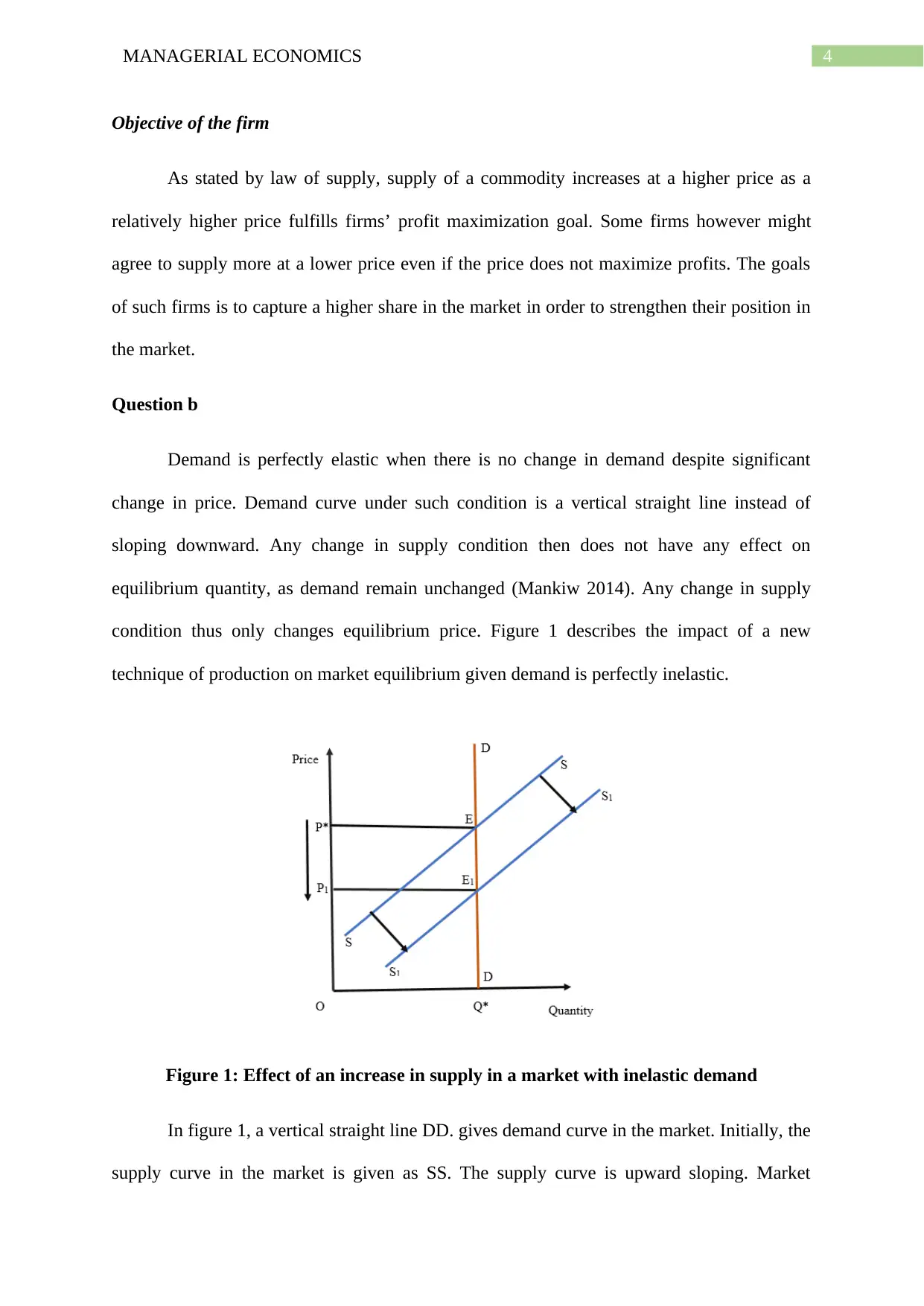

Question b

Demand is perfectly elastic when there is no change in demand despite significant

change in price. Demand curve under such condition is a vertical straight line instead of

sloping downward. Any change in supply condition then does not have any effect on

equilibrium quantity, as demand remain unchanged (Mankiw 2014). Any change in supply

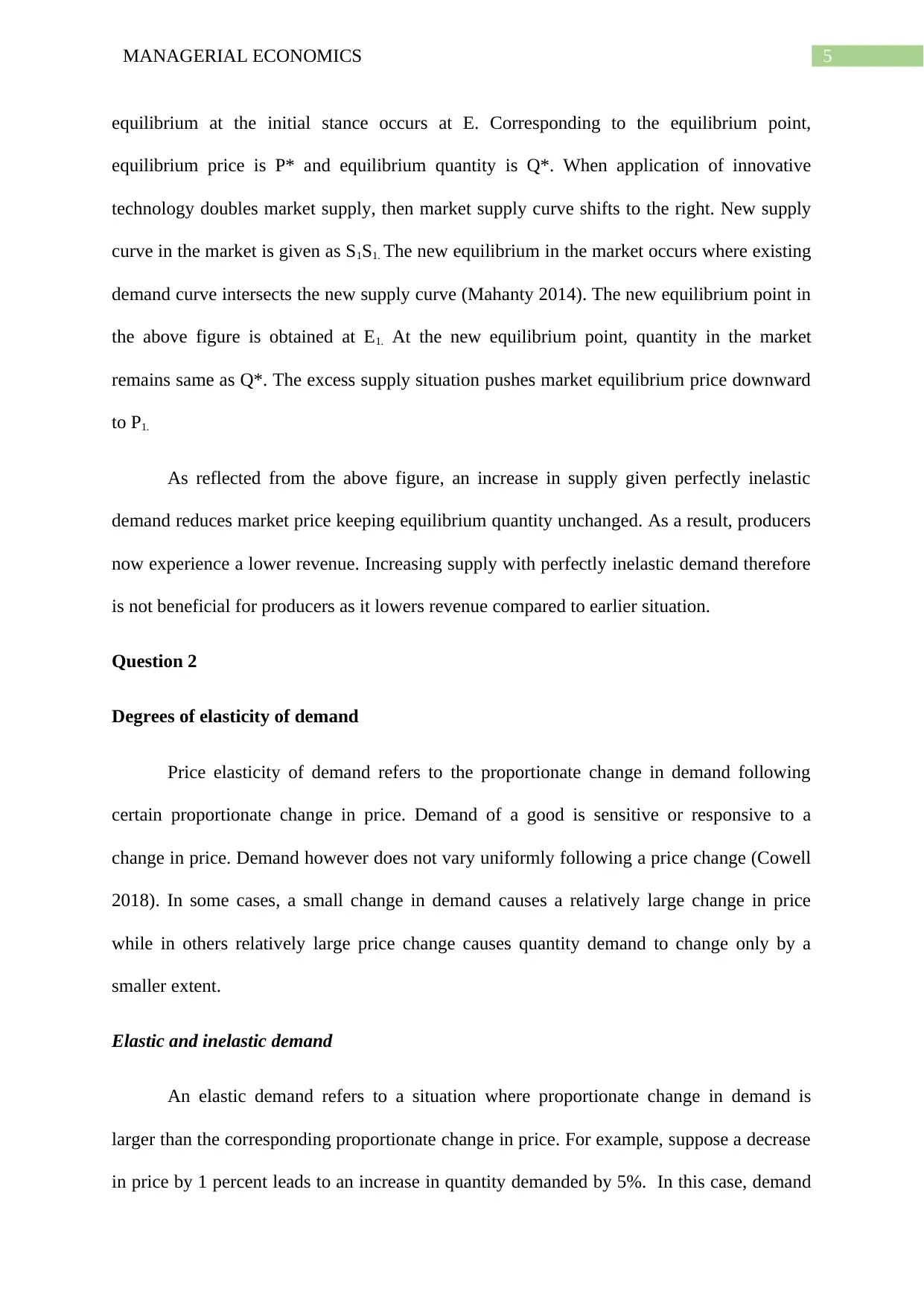

condition thus only changes equilibrium price. Figure 1 describes the impact of a new

technique of production on market equilibrium given demand is perfectly inelastic.

Figure 1: Effect of an increase in supply in a market with inelastic demand

In figure 1, a vertical straight line DD. gives demand curve in the market. Initially, the

supply curve in the market is given as SS. The supply curve is upward sloping. Market

Objective of the firm

As stated by law of supply, supply of a commodity increases at a higher price as a

relatively higher price fulfills firms’ profit maximization goal. Some firms however might

agree to supply more at a lower price even if the price does not maximize profits. The goals

of such firms is to capture a higher share in the market in order to strengthen their position in

the market.

Question b

Demand is perfectly elastic when there is no change in demand despite significant

change in price. Demand curve under such condition is a vertical straight line instead of

sloping downward. Any change in supply condition then does not have any effect on

equilibrium quantity, as demand remain unchanged (Mankiw 2014). Any change in supply

condition thus only changes equilibrium price. Figure 1 describes the impact of a new

technique of production on market equilibrium given demand is perfectly inelastic.

Figure 1: Effect of an increase in supply in a market with inelastic demand

In figure 1, a vertical straight line DD. gives demand curve in the market. Initially, the

supply curve in the market is given as SS. The supply curve is upward sloping. Market

5MANAGERIAL ECONOMICS

equilibrium at the initial stance occurs at E. Corresponding to the equilibrium point,

equilibrium price is P* and equilibrium quantity is Q*. When application of innovative

technology doubles market supply, then market supply curve shifts to the right. New supply

curve in the market is given as S1S1. The new equilibrium in the market occurs where existing

demand curve intersects the new supply curve (Mahanty 2014). The new equilibrium point in

the above figure is obtained at E1. At the new equilibrium point, quantity in the market

remains same as Q*. The excess supply situation pushes market equilibrium price downward

to P1.

As reflected from the above figure, an increase in supply given perfectly inelastic

demand reduces market price keeping equilibrium quantity unchanged. As a result, producers

now experience a lower revenue. Increasing supply with perfectly inelastic demand therefore

is not beneficial for producers as it lowers revenue compared to earlier situation.

Question 2

Degrees of elasticity of demand

Price elasticity of demand refers to the proportionate change in demand following

certain proportionate change in price. Demand of a good is sensitive or responsive to a

change in price. Demand however does not vary uniformly following a price change (Cowell

2018). In some cases, a small change in demand causes a relatively large change in price

while in others relatively large price change causes quantity demand to change only by a

smaller extent.

Elastic and inelastic demand

An elastic demand refers to a situation where proportionate change in demand is

larger than the corresponding proportionate change in price. For example, suppose a decrease

in price by 1 percent leads to an increase in quantity demanded by 5%. In this case, demand

equilibrium at the initial stance occurs at E. Corresponding to the equilibrium point,

equilibrium price is P* and equilibrium quantity is Q*. When application of innovative

technology doubles market supply, then market supply curve shifts to the right. New supply

curve in the market is given as S1S1. The new equilibrium in the market occurs where existing

demand curve intersects the new supply curve (Mahanty 2014). The new equilibrium point in

the above figure is obtained at E1. At the new equilibrium point, quantity in the market

remains same as Q*. The excess supply situation pushes market equilibrium price downward

to P1.

As reflected from the above figure, an increase in supply given perfectly inelastic

demand reduces market price keeping equilibrium quantity unchanged. As a result, producers

now experience a lower revenue. Increasing supply with perfectly inelastic demand therefore

is not beneficial for producers as it lowers revenue compared to earlier situation.

Question 2

Degrees of elasticity of demand

Price elasticity of demand refers to the proportionate change in demand following

certain proportionate change in price. Demand of a good is sensitive or responsive to a

change in price. Demand however does not vary uniformly following a price change (Cowell

2018). In some cases, a small change in demand causes a relatively large change in price

while in others relatively large price change causes quantity demand to change only by a

smaller extent.

Elastic and inelastic demand

An elastic demand refers to a situation where proportionate change in demand is

larger than the corresponding proportionate change in price. For example, suppose a decrease

in price by 1 percent leads to an increase in quantity demanded by 5%. In this case, demand

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGERIAL ECONOMICS

is considered as elastic demand. In contrast, there are products for which demand not very

much sensitive. For example, if a 5% increase in price causes demand to change by only 1%,

then demand is considered as inelastic (Labandeira, Labeaga and Lopez-Otero 2017).

The terms like elastic and inelastic do not completely capture the extent of responsiveness or

unresponsiveness of a quantity demanded of a product with respect to a change in price.

The degree of elasticity can be broadly categorized into five groups.

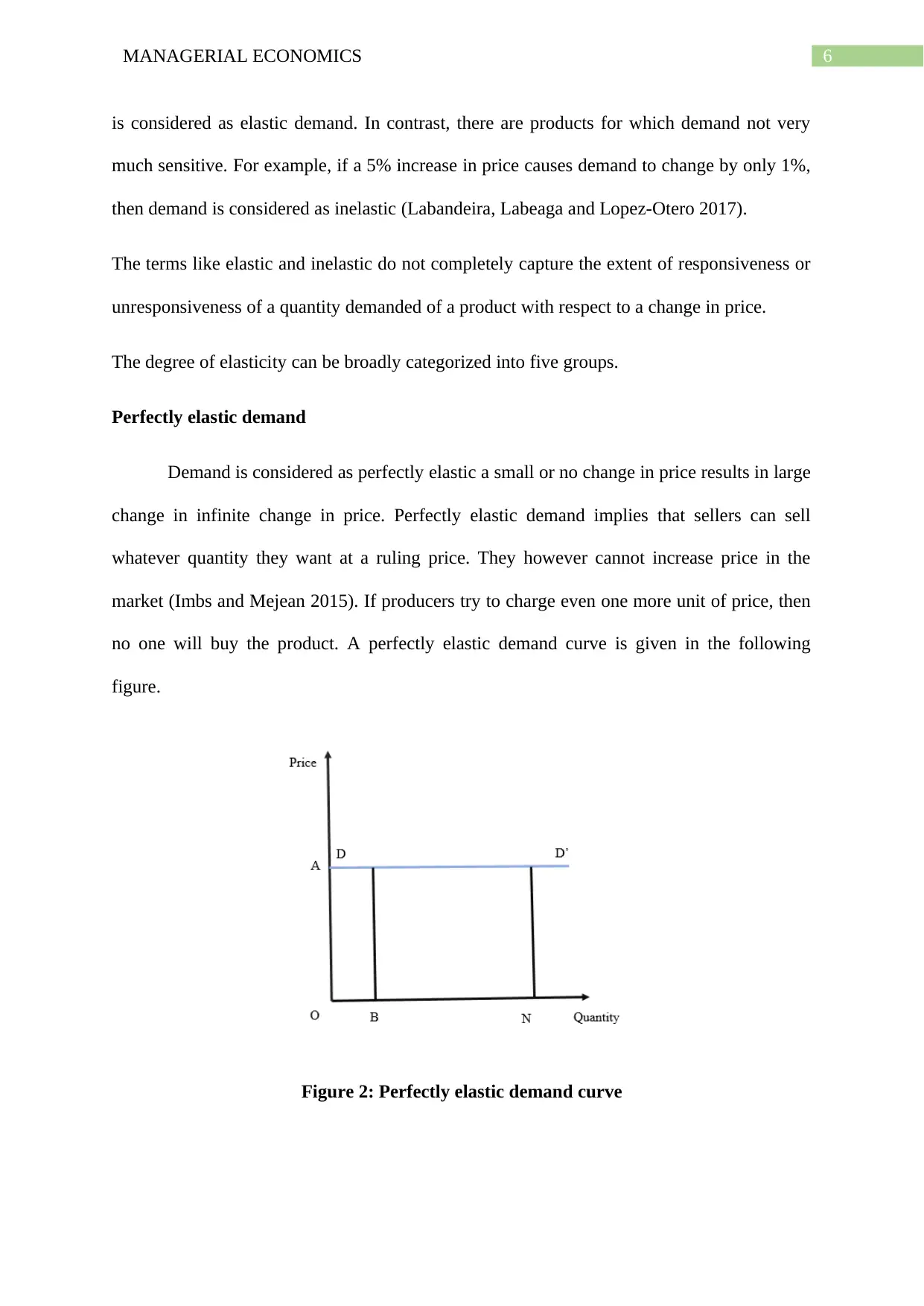

Perfectly elastic demand

Demand is considered as perfectly elastic a small or no change in price results in large

change in infinite change in price. Perfectly elastic demand implies that sellers can sell

whatever quantity they want at a ruling price. They however cannot increase price in the

market (Imbs and Mejean 2015). If producers try to charge even one more unit of price, then

no one will buy the product. A perfectly elastic demand curve is given in the following

figure.

Figure 2: Perfectly elastic demand curve

is considered as elastic demand. In contrast, there are products for which demand not very

much sensitive. For example, if a 5% increase in price causes demand to change by only 1%,

then demand is considered as inelastic (Labandeira, Labeaga and Lopez-Otero 2017).

The terms like elastic and inelastic do not completely capture the extent of responsiveness or

unresponsiveness of a quantity demanded of a product with respect to a change in price.

The degree of elasticity can be broadly categorized into five groups.

Perfectly elastic demand

Demand is considered as perfectly elastic a small or no change in price results in large

change in infinite change in price. Perfectly elastic demand implies that sellers can sell

whatever quantity they want at a ruling price. They however cannot increase price in the

market (Imbs and Mejean 2015). If producers try to charge even one more unit of price, then

no one will buy the product. A perfectly elastic demand curve is given in the following

figure.

Figure 2: Perfectly elastic demand curve

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL ECONOMICS

The above figure shows that the demand curve DD’ is a horizontal straight line

indicating that quantity demanded is highly responsiveness to change in price. The demand

curve DD’ is infinitely inelastic. The value of elasticity of demand in this case equals to

infinity.

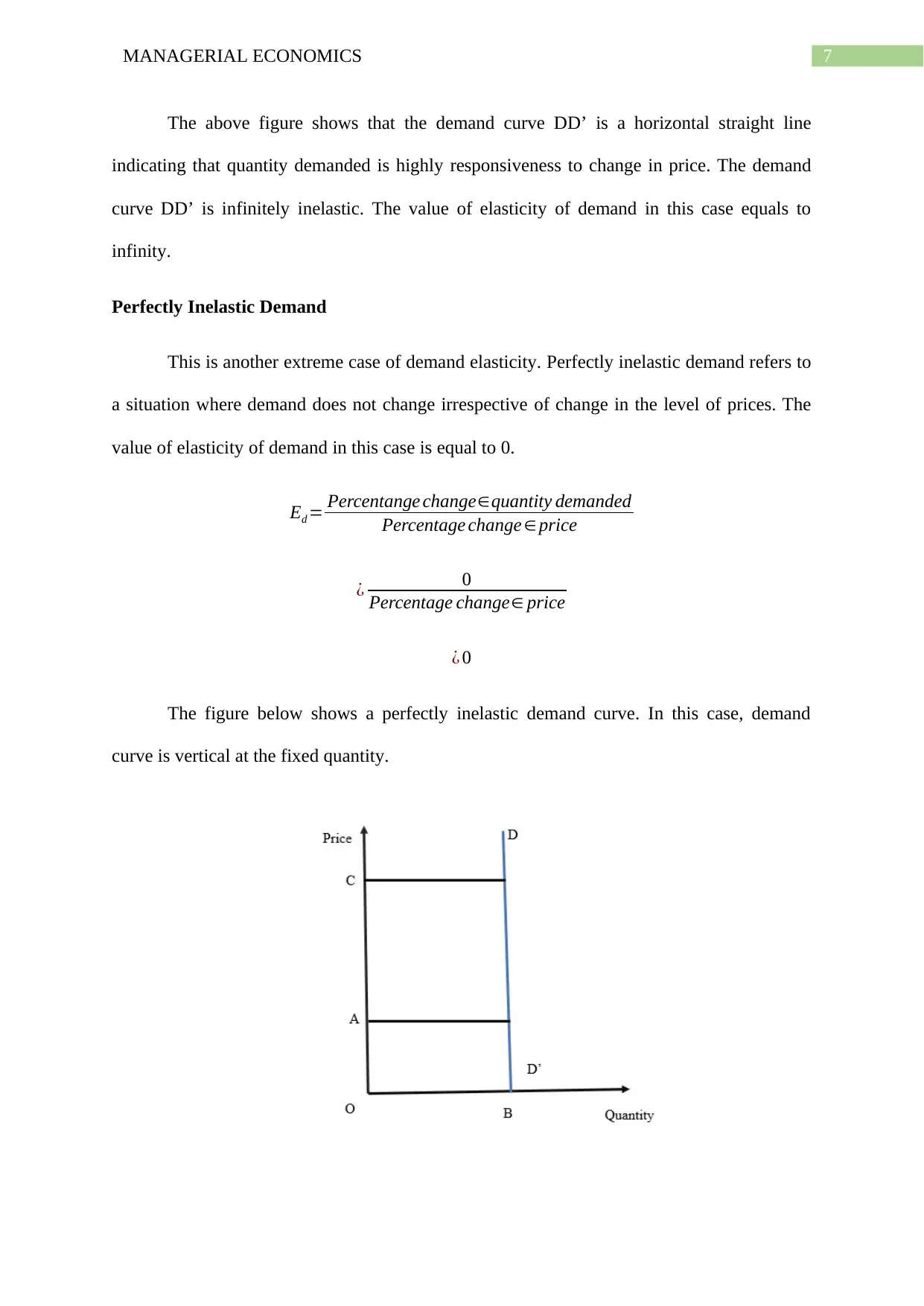

Perfectly Inelastic Demand

This is another extreme case of demand elasticity. Perfectly inelastic demand refers to

a situation where demand does not change irrespective of change in the level of prices. The

value of elasticity of demand in this case is equal to 0.

Ed = Percentange change∈quantity demanded

Percentage change ∈ price

¿ 0

Percentage change∈ price

¿ 0

The figure below shows a perfectly inelastic demand curve. In this case, demand

curve is vertical at the fixed quantity.

The above figure shows that the demand curve DD’ is a horizontal straight line

indicating that quantity demanded is highly responsiveness to change in price. The demand

curve DD’ is infinitely inelastic. The value of elasticity of demand in this case equals to

infinity.

Perfectly Inelastic Demand

This is another extreme case of demand elasticity. Perfectly inelastic demand refers to

a situation where demand does not change irrespective of change in the level of prices. The

value of elasticity of demand in this case is equal to 0.

Ed = Percentange change∈quantity demanded

Percentage change ∈ price

¿ 0

Percentage change∈ price

¿ 0

The figure below shows a perfectly inelastic demand curve. In this case, demand

curve is vertical at the fixed quantity.

8MANAGERIAL ECONOMICS

Figure 3: Perfectly inelastic demand

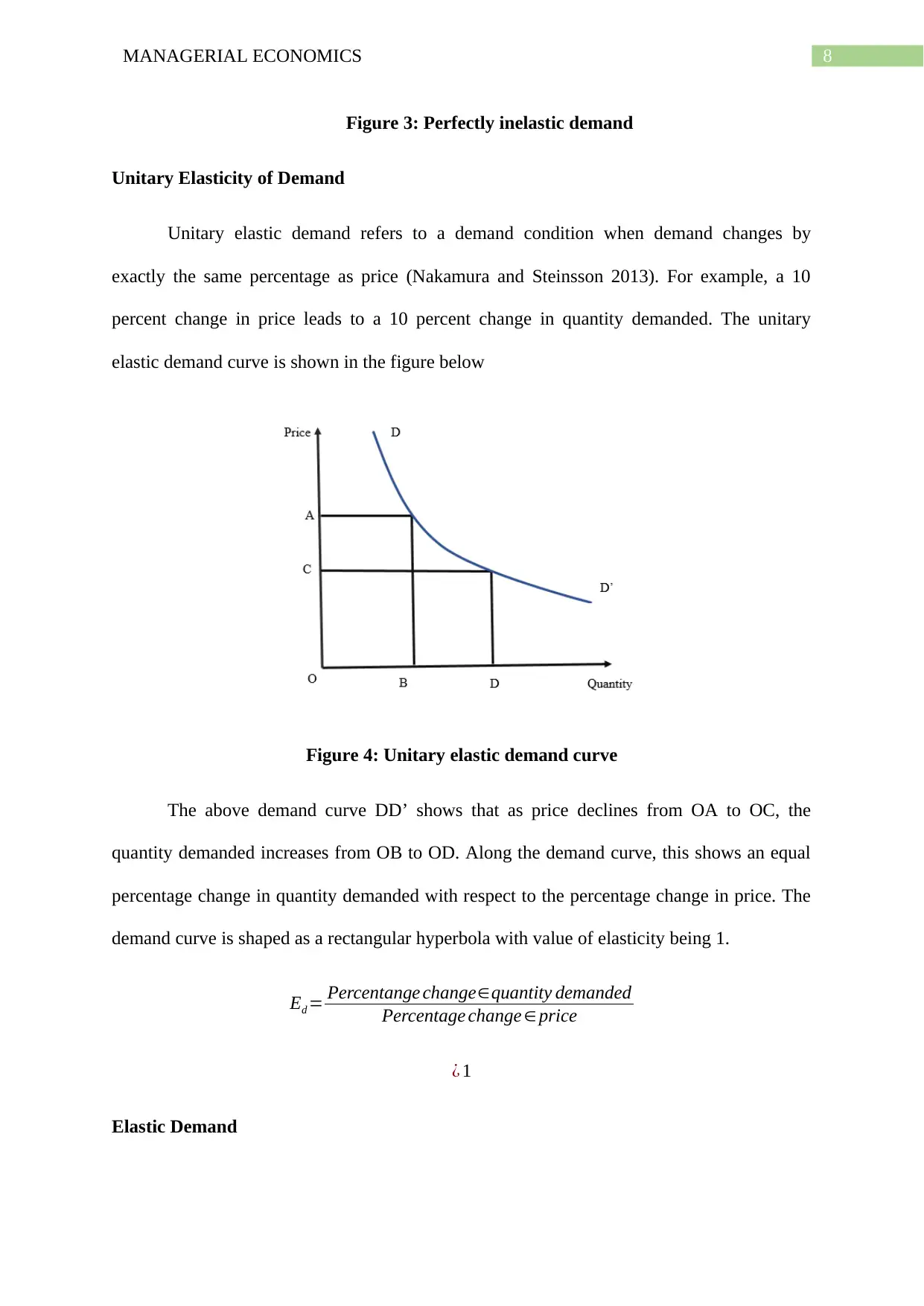

Unitary Elasticity of Demand

Unitary elastic demand refers to a demand condition when demand changes by

exactly the same percentage as price (Nakamura and Steinsson 2013). For example, a 10

percent change in price leads to a 10 percent change in quantity demanded. The unitary

elastic demand curve is shown in the figure below

Figure 4: Unitary elastic demand curve

The above demand curve DD’ shows that as price declines from OA to OC, the

quantity demanded increases from OB to OD. Along the demand curve, this shows an equal

percentage change in quantity demanded with respect to the percentage change in price. The

demand curve is shaped as a rectangular hyperbola with value of elasticity being 1.

Ed = Percentange change∈quantity demanded

Percentage change ∈ price

¿ 1

Elastic Demand

Figure 3: Perfectly inelastic demand

Unitary Elasticity of Demand

Unitary elastic demand refers to a demand condition when demand changes by

exactly the same percentage as price (Nakamura and Steinsson 2013). For example, a 10

percent change in price leads to a 10 percent change in quantity demanded. The unitary

elastic demand curve is shown in the figure below

Figure 4: Unitary elastic demand curve

The above demand curve DD’ shows that as price declines from OA to OC, the

quantity demanded increases from OB to OD. Along the demand curve, this shows an equal

percentage change in quantity demanded with respect to the percentage change in price. The

demand curve is shaped as a rectangular hyperbola with value of elasticity being 1.

Ed = Percentange change∈quantity demanded

Percentage change ∈ price

¿ 1

Elastic Demand

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGERIAL ECONOMICS

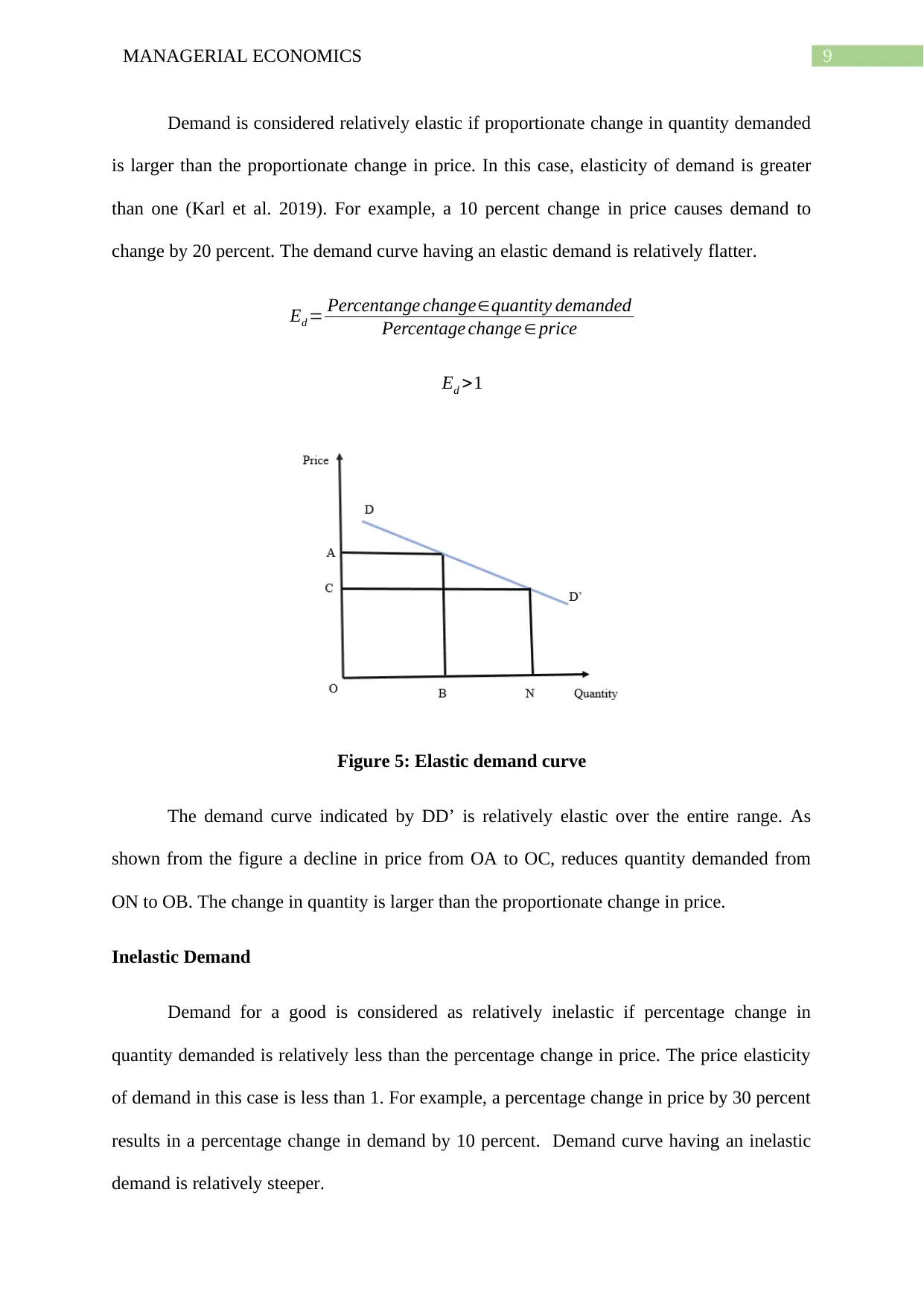

Demand is considered relatively elastic if proportionate change in quantity demanded

is larger than the proportionate change in price. In this case, elasticity of demand is greater

than one (Karl et al. 2019). For example, a 10 percent change in price causes demand to

change by 20 percent. The demand curve having an elastic demand is relatively flatter.

Ed = Percentange change∈quantity demanded

Percentage change ∈ price

Ed >1

Figure 5: Elastic demand curve

The demand curve indicated by DD’ is relatively elastic over the entire range. As

shown from the figure a decline in price from OA to OC, reduces quantity demanded from

ON to OB. The change in quantity is larger than the proportionate change in price.

Inelastic Demand

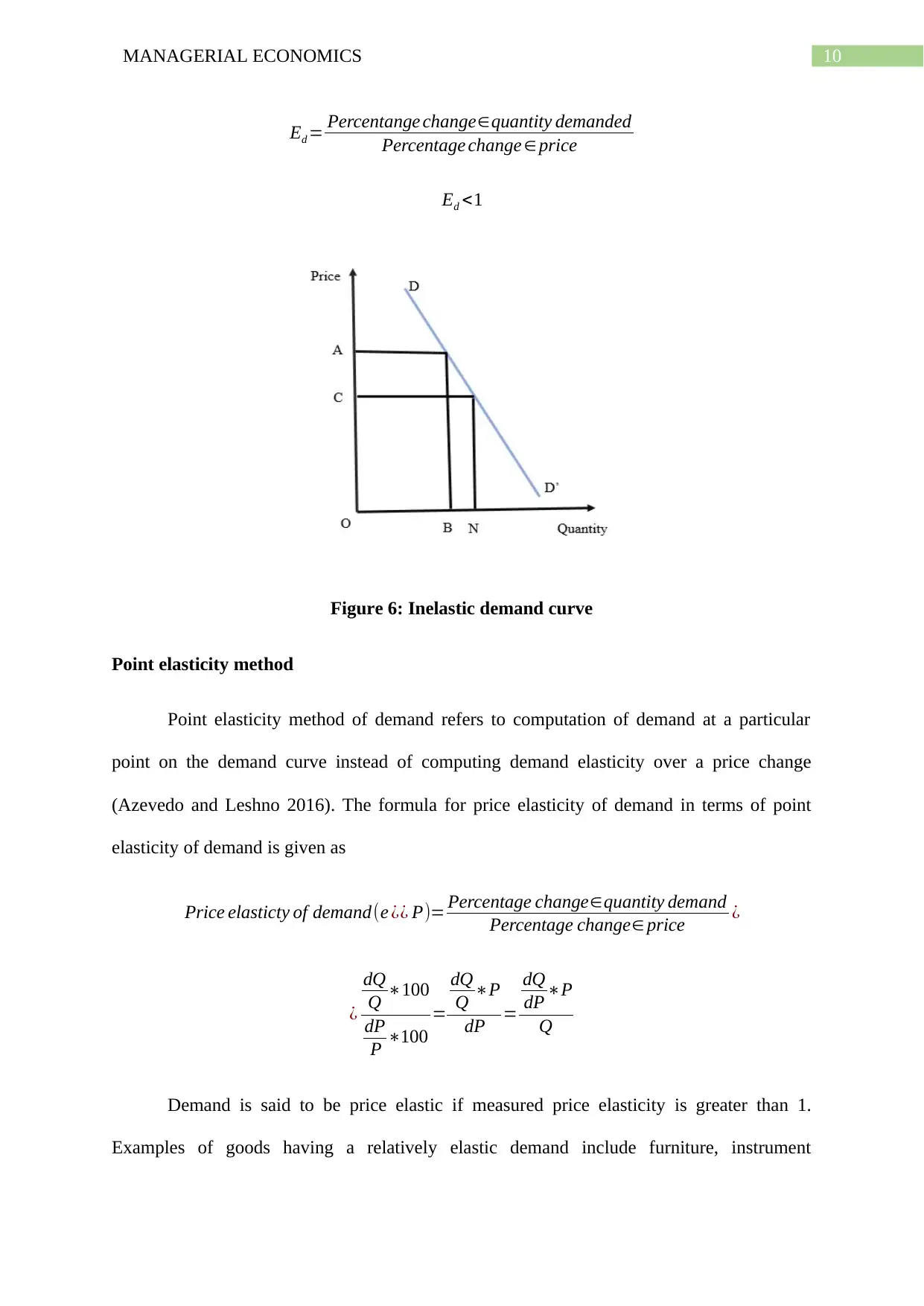

Demand for a good is considered as relatively inelastic if percentage change in

quantity demanded is relatively less than the percentage change in price. The price elasticity

of demand in this case is less than 1. For example, a percentage change in price by 30 percent

results in a percentage change in demand by 10 percent. Demand curve having an inelastic

demand is relatively steeper.

Demand is considered relatively elastic if proportionate change in quantity demanded

is larger than the proportionate change in price. In this case, elasticity of demand is greater

than one (Karl et al. 2019). For example, a 10 percent change in price causes demand to

change by 20 percent. The demand curve having an elastic demand is relatively flatter.

Ed = Percentange change∈quantity demanded

Percentage change ∈ price

Ed >1

Figure 5: Elastic demand curve

The demand curve indicated by DD’ is relatively elastic over the entire range. As

shown from the figure a decline in price from OA to OC, reduces quantity demanded from

ON to OB. The change in quantity is larger than the proportionate change in price.

Inelastic Demand

Demand for a good is considered as relatively inelastic if percentage change in

quantity demanded is relatively less than the percentage change in price. The price elasticity

of demand in this case is less than 1. For example, a percentage change in price by 30 percent

results in a percentage change in demand by 10 percent. Demand curve having an inelastic

demand is relatively steeper.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGERIAL ECONOMICS

Ed = Percentange change∈quantity demanded

Percentage change ∈ price

Ed <1

Figure 6: Inelastic demand curve

Point elasticity method

Point elasticity method of demand refers to computation of demand at a particular

point on the demand curve instead of computing demand elasticity over a price change

(Azevedo and Leshno 2016). The formula for price elasticity of demand in terms of point

elasticity of demand is given as

Price elasticty of demand(e ¿¿ P)= Percentage change∈quantity demand

Percentage change∈ price ¿

¿

dQ

Q ∗100

dP

P ∗100

=

dQ

Q ∗P

dP =

dQ

dP ∗P

Q

Demand is said to be price elastic if measured price elasticity is greater than 1.

Examples of goods having a relatively elastic demand include furniture, instrument

Ed = Percentange change∈quantity demanded

Percentage change ∈ price

Ed <1

Figure 6: Inelastic demand curve

Point elasticity method

Point elasticity method of demand refers to computation of demand at a particular

point on the demand curve instead of computing demand elasticity over a price change

(Azevedo and Leshno 2016). The formula for price elasticity of demand in terms of point

elasticity of demand is given as

Price elasticty of demand(e ¿¿ P)= Percentage change∈quantity demand

Percentage change∈ price ¿

¿

dQ

Q ∗100

dP

P ∗100

=

dQ

Q ∗P

dP =

dQ

dP ∗P

Q

Demand is said to be price elastic if measured price elasticity is greater than 1.

Examples of goods having a relatively elastic demand include furniture, instrument

11MANAGERIAL ECONOMICS

engineering product, motor vehicles, professional service, and such others. Demand is

considered as relatively inelastic if measured elasticity is less than 1 (Devine et al. 2018).

Examples of good having relatively inelastic demand include gasoline, oil, electricity, food

and other necessary items.

Income elasticty of demand( e¿¿ M )= Percentage change∈quantity demand

Percentage change∈income ¿

¿

dQ

Q ∗100

dM

M ∗100

¿

dQ

Q ∗M

dM

¿

dQ

dM ∗P

M

For normal goods, income elasticity is positive as demand increases with increase in

income. In case of inferior goods, income elasticity is negative, as people tend to decrease

demand with increase in income. For necessary goods like food, fuel income elasticity of

demand is greater than 1 and hence, demand is income inelastic (Yang and Ng 2015). In case

of luxury goods such as sports cars, jewellery income elasticity of demand is greater than 1

and therefore, demand of these goods are income elastic in nature.

Cross price elasticty of demand (e ¿¿ XY )= Percentage change∈quantity demand of good X

Percentage change∈ price of good Y ¿

d QX

QX

∗100

d PY

PY

∗100

engineering product, motor vehicles, professional service, and such others. Demand is

considered as relatively inelastic if measured elasticity is less than 1 (Devine et al. 2018).

Examples of good having relatively inelastic demand include gasoline, oil, electricity, food

and other necessary items.

Income elasticty of demand( e¿¿ M )= Percentage change∈quantity demand

Percentage change∈income ¿

¿

dQ

Q ∗100

dM

M ∗100

¿

dQ

Q ∗M

dM

¿

dQ

dM ∗P

M

For normal goods, income elasticity is positive as demand increases with increase in

income. In case of inferior goods, income elasticity is negative, as people tend to decrease

demand with increase in income. For necessary goods like food, fuel income elasticity of

demand is greater than 1 and hence, demand is income inelastic (Yang and Ng 2015). In case

of luxury goods such as sports cars, jewellery income elasticity of demand is greater than 1

and therefore, demand of these goods are income elastic in nature.

Cross price elasticty of demand (e ¿¿ XY )= Percentage change∈quantity demand of good X

Percentage change∈ price of good Y ¿

d QX

QX

∗100

d PY

PY

∗100

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 29

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.