ACC511 - Managerial Finance: Project Evaluation for Dell Inc.

VerifiedAdded on 2022/11/14

|9

|1857

|331

Report

AI Summary

This report provides a comprehensive financial analysis of a proposed manufacturing plant project by Dell Inc. The report evaluates the project's feasibility using Net Present Value (NPV), Internal Rate of Return (IRR), and payback period methods. It includes detailed calculations for cash flows, depreciation, and discount rates to determine the project's profitability and investment viability. The report also considers a new financial discipline adopted by the company and assesses the maximum interest rate the company can afford. Furthermore, the report presents the pros and cons of the new financial requirements. The analysis concludes with recommendations on whether Dell should proceed with the project, based on the financial metrics and the new financial discipline.

Running head: MANAGERIAL FINANCE

Managerial finance

Name of the student

Name of the university

Student ID

Author note

Managerial finance

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGERIAL FINANCE

Executive summary

Aim of the report is to analyse one manufacturing project that is planned by Dell to be started

in near future. However, the company wants to evaluate the project in context of its

profitability before investing the amount. Different methods those will be used for the

project’s analysis are NPV approach, IRR and payback period. In addition to that the project

will be evaluated based on the new financial discipline adopted by it.

Executive summary

Aim of the report is to analyse one manufacturing project that is planned by Dell to be started

in near future. However, the company wants to evaluate the project in context of its

profitability before investing the amount. Different methods those will be used for the

project’s analysis are NPV approach, IRR and payback period. In addition to that the project

will be evaluated based on the new financial discipline adopted by it.

2MANAGERIAL FINANCE

Table of Contents

Introduction................................................................................................................................3

Question 1..................................................................................................................................3

(a) Expenses for yearly depreciation.................................................................................3

(b) Year 1 to 9 – yearly cash flows...................................................................................3

(c) Year 0 – cash flow.......................................................................................................4

(d) Year 10 – cash flows...................................................................................................4

(e) Calculation of NPV and interpretation........................................................................4

(f) Payback period and IRR and interpretation................................................................5

(g) Applying same discount rate for all the projects.........................................................6

Question 2..................................................................................................................................6

(a) Maximum rate of interest............................................................................................6

(b) Pros and cons of new requirement...............................................................................6

Conclusion and recommendation...............................................................................................7

Reference....................................................................................................................................8

Table of Contents

Introduction................................................................................................................................3

Question 1..................................................................................................................................3

(a) Expenses for yearly depreciation.................................................................................3

(b) Year 1 to 9 – yearly cash flows...................................................................................3

(c) Year 0 – cash flow.......................................................................................................4

(d) Year 10 – cash flows...................................................................................................4

(e) Calculation of NPV and interpretation........................................................................4

(f) Payback period and IRR and interpretation................................................................5

(g) Applying same discount rate for all the projects.........................................................6

Question 2..................................................................................................................................6

(a) Maximum rate of interest............................................................................................6

(b) Pros and cons of new requirement...............................................................................6

Conclusion and recommendation...............................................................................................7

Reference....................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGERIAL FINANCE

Introduction

The report will majorly focus on the proposed manufacturing plant that will be set-up

by Dell Inc. however, before taking the final decision regarding setting up of the plant Dell

will conduct the feasibility test for the project through various techniques those are generally

used to evaluate any investment. Based on the projected cash flow from the project the report

in the 2nd part will consider the bank loan and capability regarding whether the project will be

able to bear the interest on loan along with principal repayment. Taking both the aspects in

consideration it will be recommended whether the project is acceptable or not (Levy 2015)

Question 1

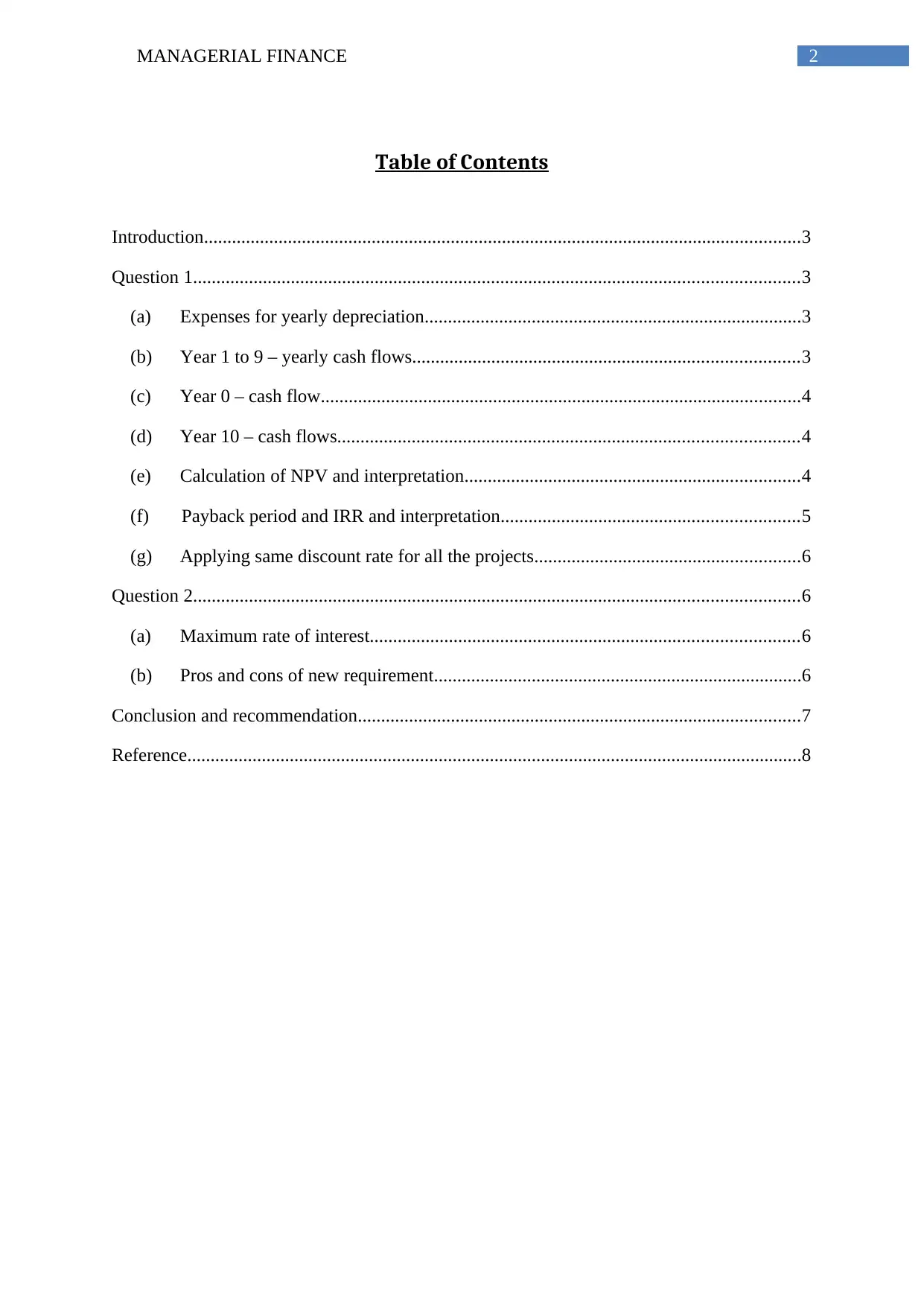

(a) Expenses for yearly depreciation

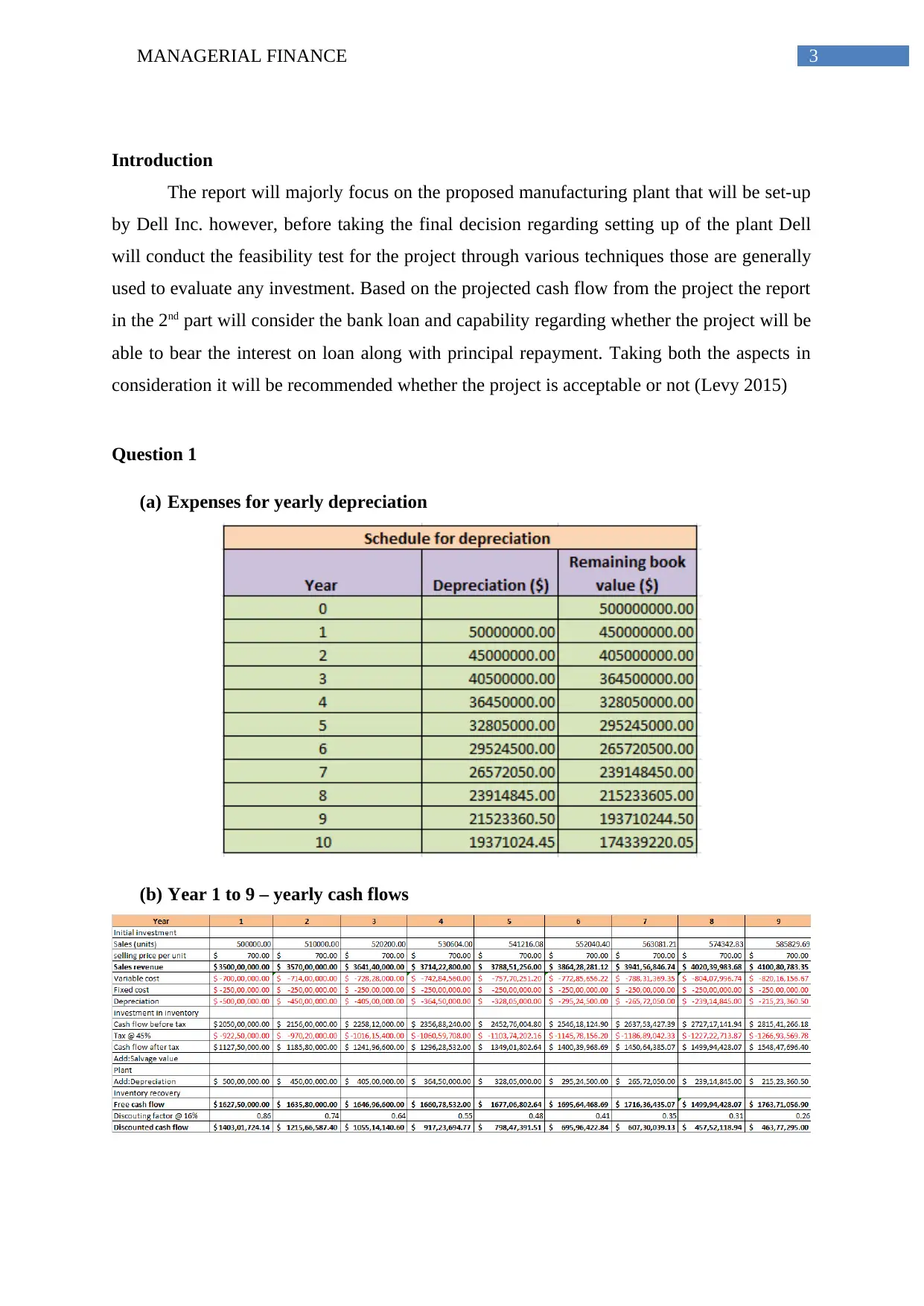

(b) Year 1 to 9 – yearly cash flows

Introduction

The report will majorly focus on the proposed manufacturing plant that will be set-up

by Dell Inc. however, before taking the final decision regarding setting up of the plant Dell

will conduct the feasibility test for the project through various techniques those are generally

used to evaluate any investment. Based on the projected cash flow from the project the report

in the 2nd part will consider the bank loan and capability regarding whether the project will be

able to bear the interest on loan along with principal repayment. Taking both the aspects in

consideration it will be recommended whether the project is acceptable or not (Levy 2015)

Question 1

(a) Expenses for yearly depreciation

(b) Year 1 to 9 – yearly cash flows

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGERIAL FINANCE

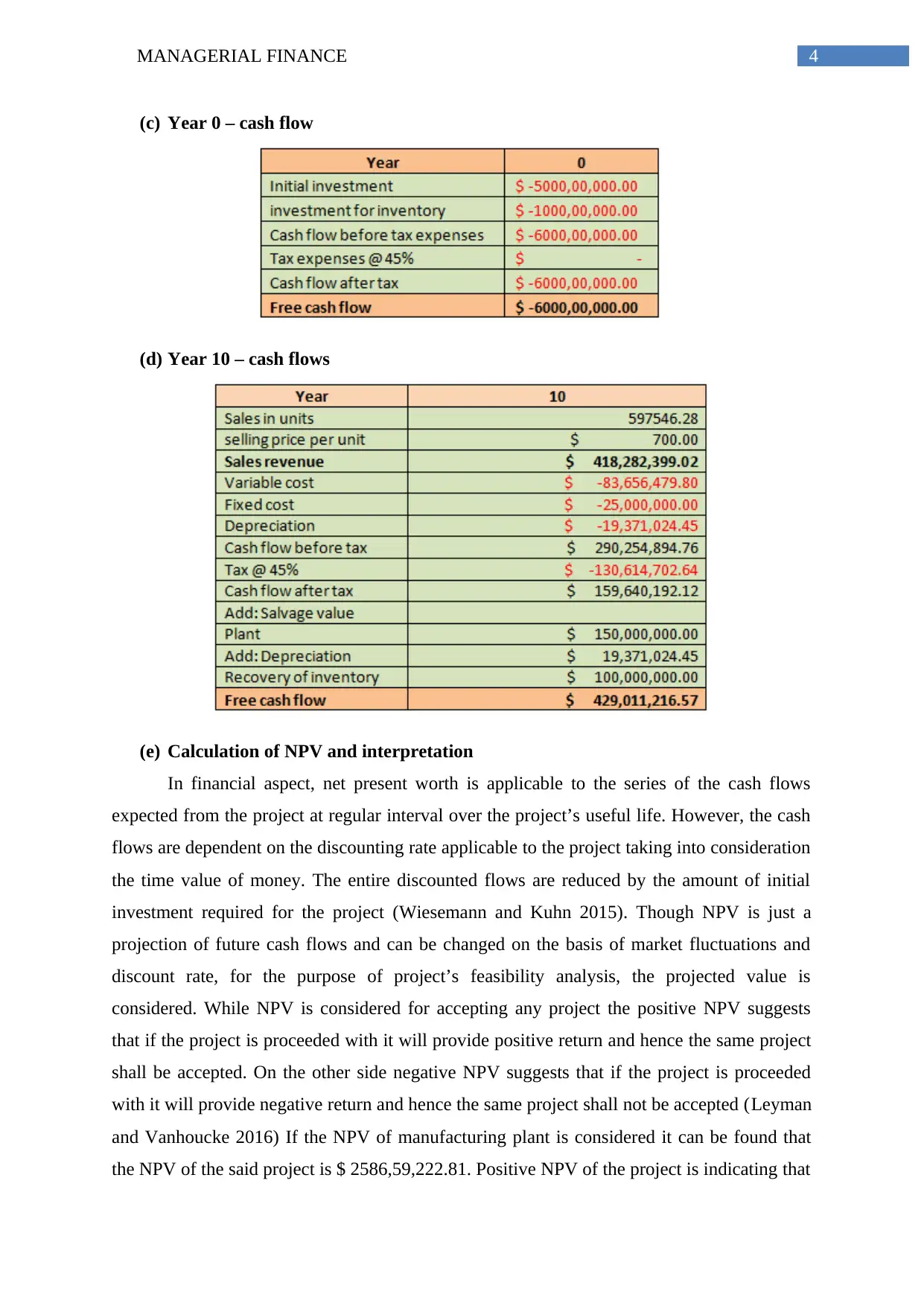

(c) Year 0 – cash flow

(d) Year 10 – cash flows

(e) Calculation of NPV and interpretation

In financial aspect, net present worth is applicable to the series of the cash flows

expected from the project at regular interval over the project’s useful life. However, the cash

flows are dependent on the discounting rate applicable to the project taking into consideration

the time value of money. The entire discounted flows are reduced by the amount of initial

investment required for the project (Wiesemann and Kuhn 2015). Though NPV is just a

projection of future cash flows and can be changed on the basis of market fluctuations and

discount rate, for the purpose of project’s feasibility analysis, the projected value is

considered. While NPV is considered for accepting any project the positive NPV suggests

that if the project is proceeded with it will provide positive return and hence the same project

shall be accepted. On the other side negative NPV suggests that if the project is proceeded

with it will provide negative return and hence the same project shall not be accepted (Leyman

and Vanhoucke 2016) If the NPV of manufacturing plant is considered it can be found that

the NPV of the said project is $ 2586,59,222.81. Positive NPV of the project is indicating that

(c) Year 0 – cash flow

(d) Year 10 – cash flows

(e) Calculation of NPV and interpretation

In financial aspect, net present worth is applicable to the series of the cash flows

expected from the project at regular interval over the project’s useful life. However, the cash

flows are dependent on the discounting rate applicable to the project taking into consideration

the time value of money. The entire discounted flows are reduced by the amount of initial

investment required for the project (Wiesemann and Kuhn 2015). Though NPV is just a

projection of future cash flows and can be changed on the basis of market fluctuations and

discount rate, for the purpose of project’s feasibility analysis, the projected value is

considered. While NPV is considered for accepting any project the positive NPV suggests

that if the project is proceeded with it will provide positive return and hence the same project

shall be accepted. On the other side negative NPV suggests that if the project is proceeded

with it will provide negative return and hence the same project shall not be accepted (Leyman

and Vanhoucke 2016) If the NPV of manufacturing plant is considered it can be found that

the NPV of the said project is $ 2586,59,222.81. Positive NPV of the project is indicating that

5MANAGERIAL FINANCE

if the project is proceeded with it will provide positive return and hence the same project shall

be accepted.

(f) Payback period and IRR and interpretation

Payback period assumes the time that will be taken by the project to recover the

initial capital outlay made by the entity for project acquisition. As the cash flows for the near

future is comparatively more accurate as compared to the cash flow for the distant period, the

payback period also indicates the inherent risk with the project. However the major drawback

of this approach it does not consider the cash flows generated by the project after the payback

period that is after the initial amount of investment is recovered. While considering payback

period the project with larger cash flows in the initial period of the project are considered as

better as compared to the project with larger cash flows at later period (Qiu, Wang and Wang

2015). Similarly, the project with longer payback period is involved with higher risk. While

payback period is the deciding factor for any project’s acceptability the project with the

payback period of lower than its useful life is considered acceptable. On the other side, if the

project’s initial investment cannot be recovered within the useful life of the project, it is

rejected as it indicates that the project is not able to recover the initial investment amount

(Gorshkov et al. 2018). If the payback period of manufacturing plant is considered it can be

found that the simple payback period of the said project is 3.66 years and discounted payback

period is 5.88 years. Payback period of less than the lifetime of the project is indicating that if

the project is proceeded with it will be able to recover the initial investment within its lifetime

and hence the same project shall be accepted.

IRR is the minimum rate of discount that is used by the management for identifying

what will be yielded by the project in future and whether the return will be acceptable as well

as worth to pursue. It is the particular rate that is equates NPV of the future cash flows of the

project to nil. To be more specific, if the PV of future cash flow is projected through using of

internal rate as discounting rate and the initial investment is deducted from that, NPV of the

project will be zero. While IRR is used for measuring the feasibility of the project, the project

is accepted if IRR is more than cost of capital and conversely the project is not accepted if he

IRR is lower than the capital cost (Magni, C.A., 2016). It can be found from the computation

that the IRR of the project is 26% that is more than the capital cost of 16% and hence the

same project shall be accepted.

if the project is proceeded with it will provide positive return and hence the same project shall

be accepted.

(f) Payback period and IRR and interpretation

Payback period assumes the time that will be taken by the project to recover the

initial capital outlay made by the entity for project acquisition. As the cash flows for the near

future is comparatively more accurate as compared to the cash flow for the distant period, the

payback period also indicates the inherent risk with the project. However the major drawback

of this approach it does not consider the cash flows generated by the project after the payback

period that is after the initial amount of investment is recovered. While considering payback

period the project with larger cash flows in the initial period of the project are considered as

better as compared to the project with larger cash flows at later period (Qiu, Wang and Wang

2015). Similarly, the project with longer payback period is involved with higher risk. While

payback period is the deciding factor for any project’s acceptability the project with the

payback period of lower than its useful life is considered acceptable. On the other side, if the

project’s initial investment cannot be recovered within the useful life of the project, it is

rejected as it indicates that the project is not able to recover the initial investment amount

(Gorshkov et al. 2018). If the payback period of manufacturing plant is considered it can be

found that the simple payback period of the said project is 3.66 years and discounted payback

period is 5.88 years. Payback period of less than the lifetime of the project is indicating that if

the project is proceeded with it will be able to recover the initial investment within its lifetime

and hence the same project shall be accepted.

IRR is the minimum rate of discount that is used by the management for identifying

what will be yielded by the project in future and whether the return will be acceptable as well

as worth to pursue. It is the particular rate that is equates NPV of the future cash flows of the

project to nil. To be more specific, if the PV of future cash flow is projected through using of

internal rate as discounting rate and the initial investment is deducted from that, NPV of the

project will be zero. While IRR is used for measuring the feasibility of the project, the project

is accepted if IRR is more than cost of capital and conversely the project is not accepted if he

IRR is lower than the capital cost (Magni, C.A., 2016). It can be found from the computation

that the IRR of the project is 26% that is more than the capital cost of 16% and hence the

same project shall be accepted.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGERIAL FINANCE

(g) Applying same discount rate for all the projects

Discounting rate has 2 components – uncertainty risk and time value of money those

in combination form theoretical basis for rate of discount. Higher rate of discount signifies

higher risk and uncertainty and lower PV for the future cash flows. Hence, the discount rate

for each of the project shall be different based on the risk involved, duration and timing of

cash flows. Further, the discount rate is also become different based on the uncertainty

involved with the project in context of inflation, market condition and profitability (Campani

2014). Hence, risk as well as uncertainty both shall be adjusted while applying the discount

rate which is different for individual project. Hence, the company’s approach is not

appropriate.

Question 2

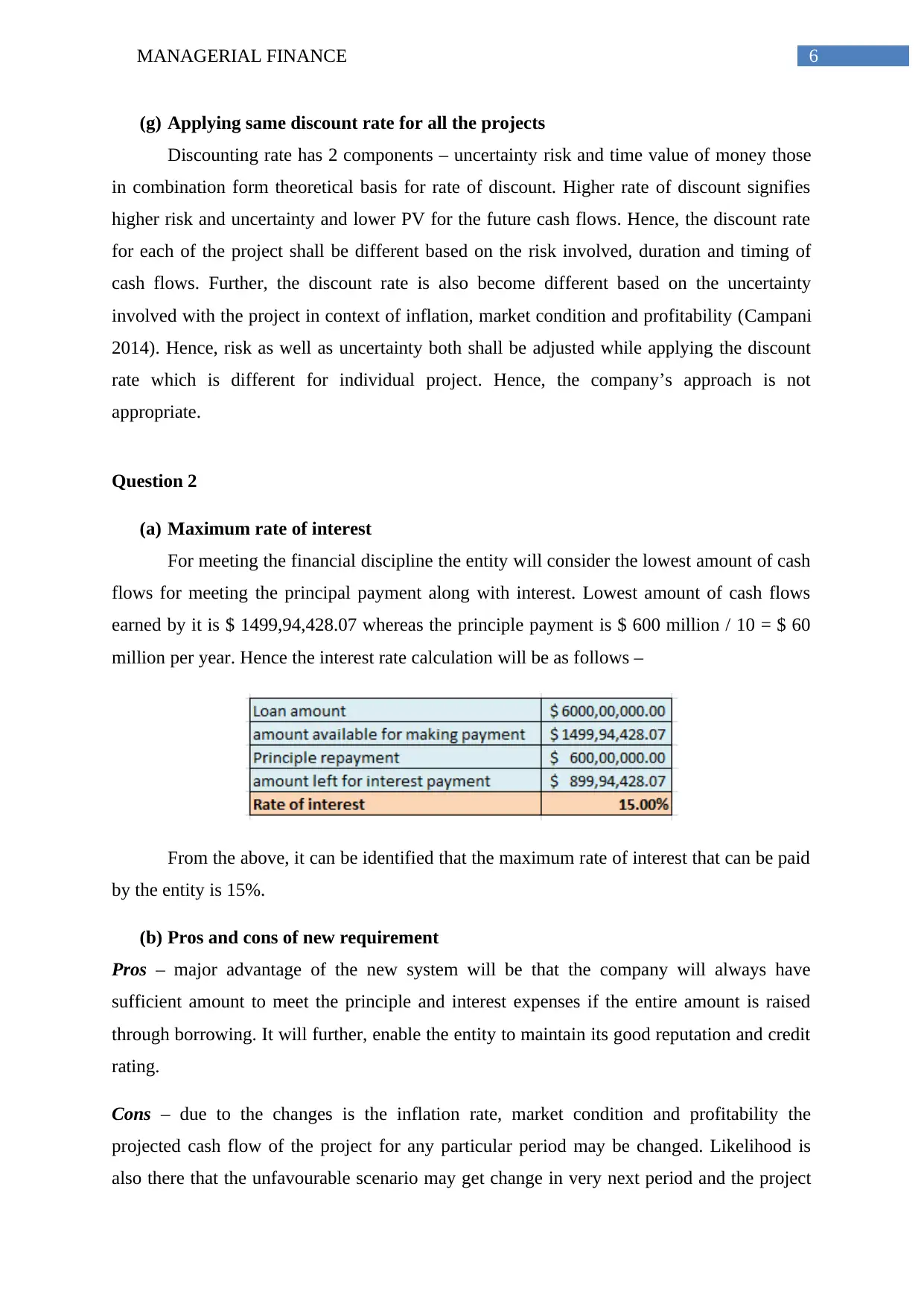

(a) Maximum rate of interest

For meeting the financial discipline the entity will consider the lowest amount of cash

flows for meeting the principal payment along with interest. Lowest amount of cash flows

earned by it is $ 1499,94,428.07 whereas the principle payment is $ 600 million / 10 = $ 60

million per year. Hence the interest rate calculation will be as follows –

From the above, it can be identified that the maximum rate of interest that can be paid

by the entity is 15%.

(b) Pros and cons of new requirement

Pros – major advantage of the new system will be that the company will always have

sufficient amount to meet the principle and interest expenses if the entire amount is raised

through borrowing. It will further, enable the entity to maintain its good reputation and credit

rating.

Cons – due to the changes is the inflation rate, market condition and profitability the

projected cash flow of the project for any particular period may be changed. Likelihood is

also there that the unfavourable scenario may get change in very next period and the project

(g) Applying same discount rate for all the projects

Discounting rate has 2 components – uncertainty risk and time value of money those

in combination form theoretical basis for rate of discount. Higher rate of discount signifies

higher risk and uncertainty and lower PV for the future cash flows. Hence, the discount rate

for each of the project shall be different based on the risk involved, duration and timing of

cash flows. Further, the discount rate is also become different based on the uncertainty

involved with the project in context of inflation, market condition and profitability (Campani

2014). Hence, risk as well as uncertainty both shall be adjusted while applying the discount

rate which is different for individual project. Hence, the company’s approach is not

appropriate.

Question 2

(a) Maximum rate of interest

For meeting the financial discipline the entity will consider the lowest amount of cash

flows for meeting the principal payment along with interest. Lowest amount of cash flows

earned by it is $ 1499,94,428.07 whereas the principle payment is $ 600 million / 10 = $ 60

million per year. Hence the interest rate calculation will be as follows –

From the above, it can be identified that the maximum rate of interest that can be paid

by the entity is 15%.

(b) Pros and cons of new requirement

Pros – major advantage of the new system will be that the company will always have

sufficient amount to meet the principle and interest expenses if the entire amount is raised

through borrowing. It will further, enable the entity to maintain its good reputation and credit

rating.

Cons – due to the changes is the inflation rate, market condition and profitability the

projected cash flow of the project for any particular period may be changed. Likelihood is

also there that the unfavourable scenario may get change in very next period and the project

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL FINANCE

will earn the expected amount. Hence, with changes in the scenario the company may suffer

short of liquidity and may not be in a position to meet the interest expenses (El Tahir and El

Otaibi 2014)

Conclusion and recommendation

It can be concluded that the project’s analysis is revealing that it is fulfilling all the

criteria those are considered for acceptability of the same. For instance, the project has

positive NPV, IRR greater than cost of capital and payback period shorter than useful life of

the project. Hence, it can be recommended that the project shall be accepted as it will

generate profit for the entity. Regarding new financial discipline of the entity it can be

recommended that based on only the projection the decision for raising such big amount

through debt shall not be made. It shall consider the market scenario, its liquidity position,

leverage position and past periods profitability.

will earn the expected amount. Hence, with changes in the scenario the company may suffer

short of liquidity and may not be in a position to meet the interest expenses (El Tahir and El

Otaibi 2014)

Conclusion and recommendation

It can be concluded that the project’s analysis is revealing that it is fulfilling all the

criteria those are considered for acceptability of the same. For instance, the project has

positive NPV, IRR greater than cost of capital and payback period shorter than useful life of

the project. Hence, it can be recommended that the project shall be accepted as it will

generate profit for the entity. Regarding new financial discipline of the entity it can be

recommended that based on only the projection the decision for raising such big amount

through debt shall not be made. It shall consider the market scenario, its liquidity position,

leverage position and past periods profitability.

8MANAGERIAL FINANCE

Reference

Campani, C.H., 2014. On the Rate of Return and Valuation of Non-Conventional

Projects. Business and Management Review, 3(12), pp.01-06.

El Tahir, Y. and El Otaibi, D., 2014. Internal Rate of Return: A suggested alternative formula

and its macroeconomics implications. Journal of American Science, 10(11), pp.216-221.

Gorshkov, A.S., Vatin, N.I., Rymkevich, P.P. and Kydrevich, O.O., 2018. Payback period of

investments in energy saving. Magazine of Civil Engineering, 78(2).

Hopkinson, M., 2017. Net Present value and risk modelling for projects. Routledge.

Levy, H., 2015. Stochastic dominance: Investment decision making under uncertainty.

Springer.

Leyman, P. and Vanhoucke, M., 2016. Payment models and net present value optimization

for resource-constrained project scheduling. Computers & Industrial Engineering, 91,

pp.139-153.

Magni, C.A., 2016. Capital depreciation and the underdetermination of rate of return: A

unifying perspective. Journal of Mathematical Economics, 67, pp.54-79.

Qiu, Y., Wang, Y.D. and Wang, J., 2015. Implied discount rate and payback threshold of

energy efficiency investment in the industrial sector. Applied Economics, 47(21), pp.2218-

2233.

Wiesemann, W. and Kuhn, D., 2015. The stochastic time-constrained net present value

problem. In Handbook on project management and scheduling vol. 2 (pp. 753-780). Springer,

Cham.

Reference

Campani, C.H., 2014. On the Rate of Return and Valuation of Non-Conventional

Projects. Business and Management Review, 3(12), pp.01-06.

El Tahir, Y. and El Otaibi, D., 2014. Internal Rate of Return: A suggested alternative formula

and its macroeconomics implications. Journal of American Science, 10(11), pp.216-221.

Gorshkov, A.S., Vatin, N.I., Rymkevich, P.P. and Kydrevich, O.O., 2018. Payback period of

investments in energy saving. Magazine of Civil Engineering, 78(2).

Hopkinson, M., 2017. Net Present value and risk modelling for projects. Routledge.

Levy, H., 2015. Stochastic dominance: Investment decision making under uncertainty.

Springer.

Leyman, P. and Vanhoucke, M., 2016. Payment models and net present value optimization

for resource-constrained project scheduling. Computers & Industrial Engineering, 91,

pp.139-153.

Magni, C.A., 2016. Capital depreciation and the underdetermination of rate of return: A

unifying perspective. Journal of Mathematical Economics, 67, pp.54-79.

Qiu, Y., Wang, Y.D. and Wang, J., 2015. Implied discount rate and payback threshold of

energy efficiency investment in the industrial sector. Applied Economics, 47(21), pp.2218-

2233.

Wiesemann, W. and Kuhn, D., 2015. The stochastic time-constrained net present value

problem. In Handbook on project management and scheduling vol. 2 (pp. 753-780). Springer,

Cham.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.