BA 620: Managerial Finance Project - GM and Toyota Motors Analysis

VerifiedAdded on 2022/11/14

|13

|2752

|271

Project

AI Summary

This project presents a comparative financial analysis of General Motors (GM) and Toyota Motors, evaluating their performance through ratio analysis and capital budgeting techniques. Part I focuses on ratio analysis, including liquidity, profitability, solvency, and activity ratios, comparing GM and Toyota's financial health. The analysis reveals GM's strengths in profitability and efficiency, while Toyota excels in liquidity. The report offers strategies to improve GM's liquidity. Part II delves into a capital budgeting project, assessing the viability of a new business line for Adams, Incorporated. The analysis includes calculations for initial outlay, depreciation, sales projections, and after-tax cash flows. It utilizes metrics like payback period, net present value (NPV), internal rate of return (IRR), and profitability index to evaluate the project's feasibility. The project concludes with recommendations and a comprehensive overview of both companies' financial positions and investment potential.

Running head: MANAGERIAL FINANCE

MANAGERIAL FINANCE

(GENERAL MOTORS VS TOYOTA MOTORS)

MANAGERIAL FINANCE

(GENERAL MOTORS VS TOYOTA MOTORS)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running head: MANAGERIAL FINANCE

Table of Contents

Overview..........................................................................................................................................3

Part I.................................................................................................................................................3

Ratio Analysis..................................................................................................................................3

Liquidity..........................................................................................................................................3

Profitability......................................................................................................................................4

Solvency..........................................................................................................................................5

Activity ratios..................................................................................................................................6

Part II...............................................................................................................................................8

References......................................................................................................................................12

Table of Contents

Overview..........................................................................................................................................3

Part I.................................................................................................................................................3

Ratio Analysis..................................................................................................................................3

Liquidity..........................................................................................................................................3

Profitability......................................................................................................................................4

Solvency..........................................................................................................................................5

Activity ratios..................................................................................................................................6

Part II...............................................................................................................................................8

References......................................................................................................................................12

Running head: MANAGERIAL FINANCE

Overview

In the concept of the financial statements it is important for the accountants to prepare the correct

financial statements as then they are available for the comparison. For the purpose of the in-

depth communication and the understanding the company adopts some kind of the techniques in

order to give a detailed insight to the users of the financial statements as well. In this report a

detailed analysis has been undertaken to evaluate the overall performance of the General Motors

and the Toyota Group. Both the companies belong to the same industry and are involved in the

manufacturing of the automobiles (Robinson, Henry, Pirie & Broihahn, 2015).

Part I

Ratio Analysis

The ratio analysis is the analysis which is undertaken with an aim to find out the overall financial

performance of the companies. This technique makes use of the different ratios of the different

categories such as profitability, efficiency, solvency and the overall liquidity position of the

company (Boyas & Teeter, 2017). The ratio analysis can be conducted either on the basis of the

industry benchmarks or on the basis of the comparison with the other company belonging to the

same industry. In this report the detailed ratio analysis is undertaken for the two renowned

companies namely GENERAL MOTORS AND TOYOTA GROUP.

Liquidity

The liquidity ratios are the ratios that are used to measure the performance of the enterprise with

respect to how well the company is able to pay back the short term and the contractual obligation

Overview

In the concept of the financial statements it is important for the accountants to prepare the correct

financial statements as then they are available for the comparison. For the purpose of the in-

depth communication and the understanding the company adopts some kind of the techniques in

order to give a detailed insight to the users of the financial statements as well. In this report a

detailed analysis has been undertaken to evaluate the overall performance of the General Motors

and the Toyota Group. Both the companies belong to the same industry and are involved in the

manufacturing of the automobiles (Robinson, Henry, Pirie & Broihahn, 2015).

Part I

Ratio Analysis

The ratio analysis is the analysis which is undertaken with an aim to find out the overall financial

performance of the companies. This technique makes use of the different ratios of the different

categories such as profitability, efficiency, solvency and the overall liquidity position of the

company (Boyas & Teeter, 2017). The ratio analysis can be conducted either on the basis of the

industry benchmarks or on the basis of the comparison with the other company belonging to the

same industry. In this report the detailed ratio analysis is undertaken for the two renowned

companies namely GENERAL MOTORS AND TOYOTA GROUP.

Liquidity

The liquidity ratios are the ratios that are used to measure the performance of the enterprise with

respect to how well the company is able to pay back the short term and the contractual obligation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running head: MANAGERIAL FINANCE

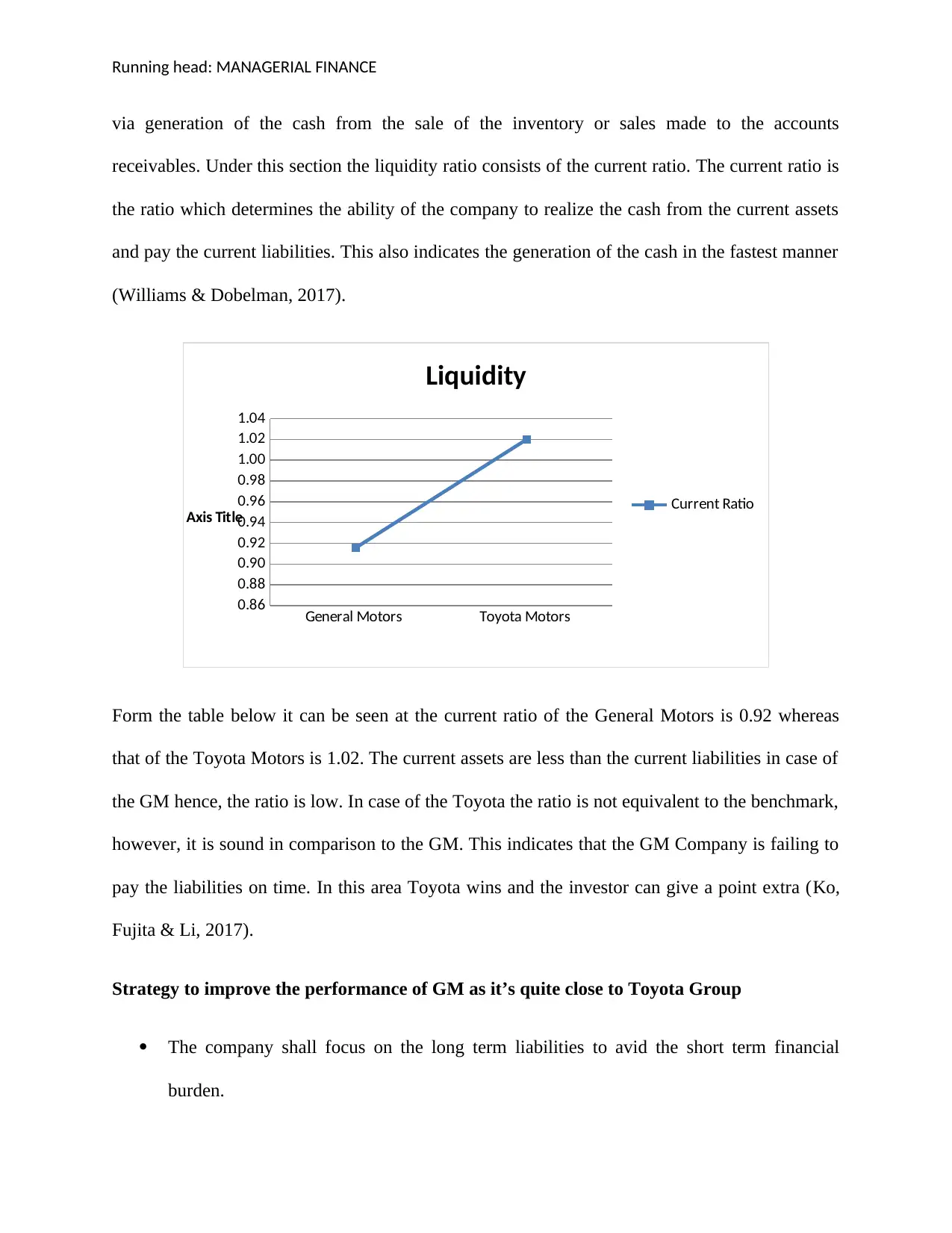

via generation of the cash from the sale of the inventory or sales made to the accounts

receivables. Under this section the liquidity ratio consists of the current ratio. The current ratio is

the ratio which determines the ability of the company to realize the cash from the current assets

and pay the current liabilities. This also indicates the generation of the cash in the fastest manner

(Williams & Dobelman, 2017).

General Motors Toyota Motors

0.86

0.88

0.90

0.92

0.94

0.96

0.98

1.00

1.02

1.04

Liquidity

Current Ratio

Axis Title

Form the table below it can be seen at the current ratio of the General Motors is 0.92 whereas

that of the Toyota Motors is 1.02. The current assets are less than the current liabilities in case of

the GM hence, the ratio is low. In case of the Toyota the ratio is not equivalent to the benchmark,

however, it is sound in comparison to the GM. This indicates that the GM Company is failing to

pay the liabilities on time. In this area Toyota wins and the investor can give a point extra (Ko,

Fujita & Li, 2017).

Strategy to improve the performance of GM as it’s quite close to Toyota Group

The company shall focus on the long term liabilities to avid the short term financial

burden.

via generation of the cash from the sale of the inventory or sales made to the accounts

receivables. Under this section the liquidity ratio consists of the current ratio. The current ratio is

the ratio which determines the ability of the company to realize the cash from the current assets

and pay the current liabilities. This also indicates the generation of the cash in the fastest manner

(Williams & Dobelman, 2017).

General Motors Toyota Motors

0.86

0.88

0.90

0.92

0.94

0.96

0.98

1.00

1.02

1.04

Liquidity

Current Ratio

Axis Title

Form the table below it can be seen at the current ratio of the General Motors is 0.92 whereas

that of the Toyota Motors is 1.02. The current assets are less than the current liabilities in case of

the GM hence, the ratio is low. In case of the Toyota the ratio is not equivalent to the benchmark,

however, it is sound in comparison to the GM. This indicates that the GM Company is failing to

pay the liabilities on time. In this area Toyota wins and the investor can give a point extra (Ko,

Fujita & Li, 2017).

Strategy to improve the performance of GM as it’s quite close to Toyota Group

The company shall focus on the long term liabilities to avid the short term financial

burden.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running head: MANAGERIAL FINANCE

Obsolete assets must be eliminated from the company so that the proper cash is

generated.

The assets shall be used to the fullest capacity and the smart manner.

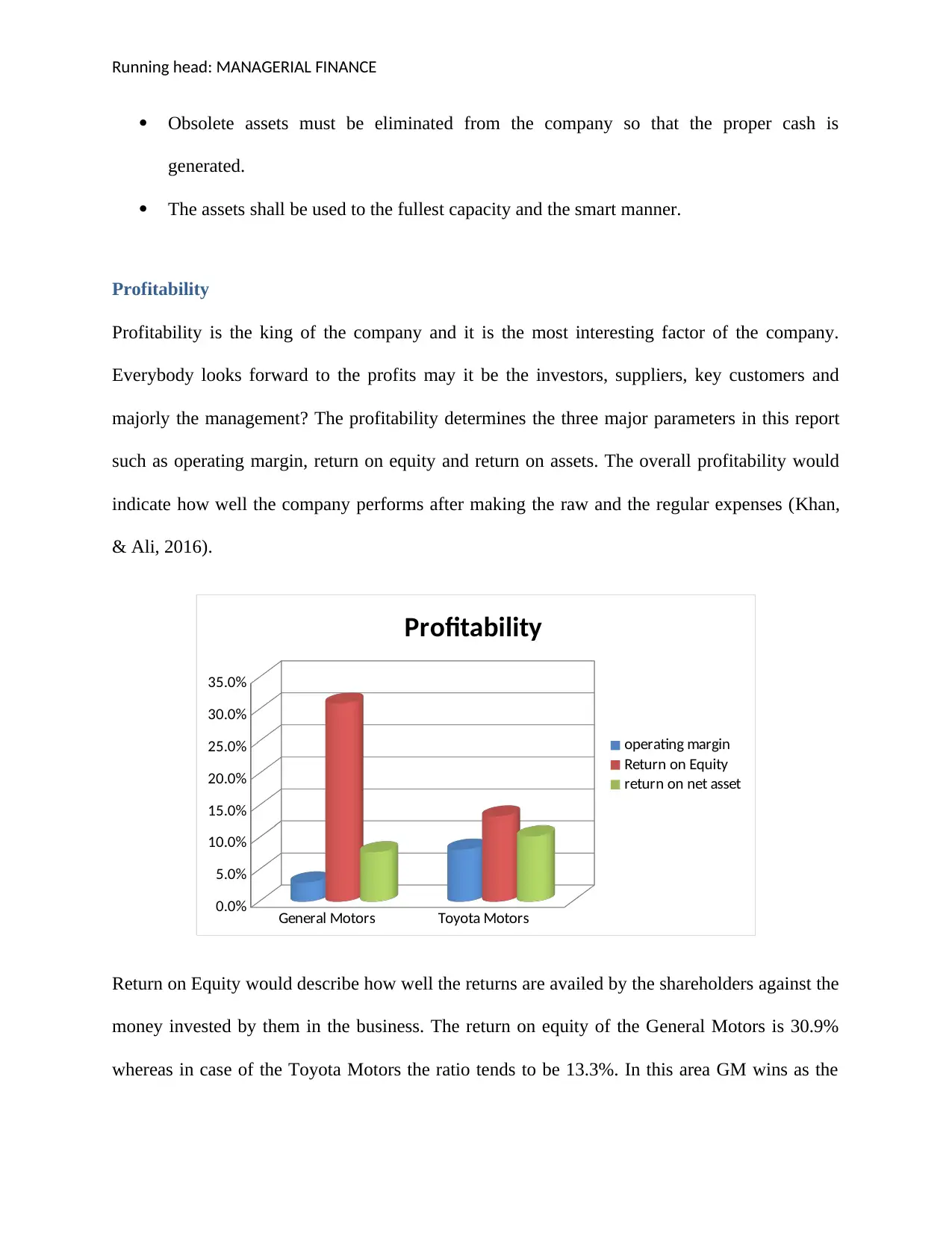

Profitability

Profitability is the king of the company and it is the most interesting factor of the company.

Everybody looks forward to the profits may it be the investors, suppliers, key customers and

majorly the management? The profitability determines the three major parameters in this report

such as operating margin, return on equity and return on assets. The overall profitability would

indicate how well the company performs after making the raw and the regular expenses (Khan,

& Ali, 2016).

General Motors Toyota Motors

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

Profitability

operating margin

Return on Equity

return on net asset

Return on Equity would describe how well the returns are availed by the shareholders against the

money invested by them in the business. The return on equity of the General Motors is 30.9%

whereas in case of the Toyota Motors the ratio tends to be 13.3%. In this area GM wins as the

Obsolete assets must be eliminated from the company so that the proper cash is

generated.

The assets shall be used to the fullest capacity and the smart manner.

Profitability

Profitability is the king of the company and it is the most interesting factor of the company.

Everybody looks forward to the profits may it be the investors, suppliers, key customers and

majorly the management? The profitability determines the three major parameters in this report

such as operating margin, return on equity and return on assets. The overall profitability would

indicate how well the company performs after making the raw and the regular expenses (Khan,

& Ali, 2016).

General Motors Toyota Motors

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

Profitability

operating margin

Return on Equity

return on net asset

Return on Equity would describe how well the returns are availed by the shareholders against the

money invested by them in the business. The return on equity of the General Motors is 30.9%

whereas in case of the Toyota Motors the ratio tends to be 13.3%. In this area GM wins as the

Running head: MANAGERIAL FINANCE

ratio of the net income in comparison to the equity invested by the investors is smooth. Almost

31% returns are being availed by the shareholders after the entire expenses have been entertained

(Edem, 2017).

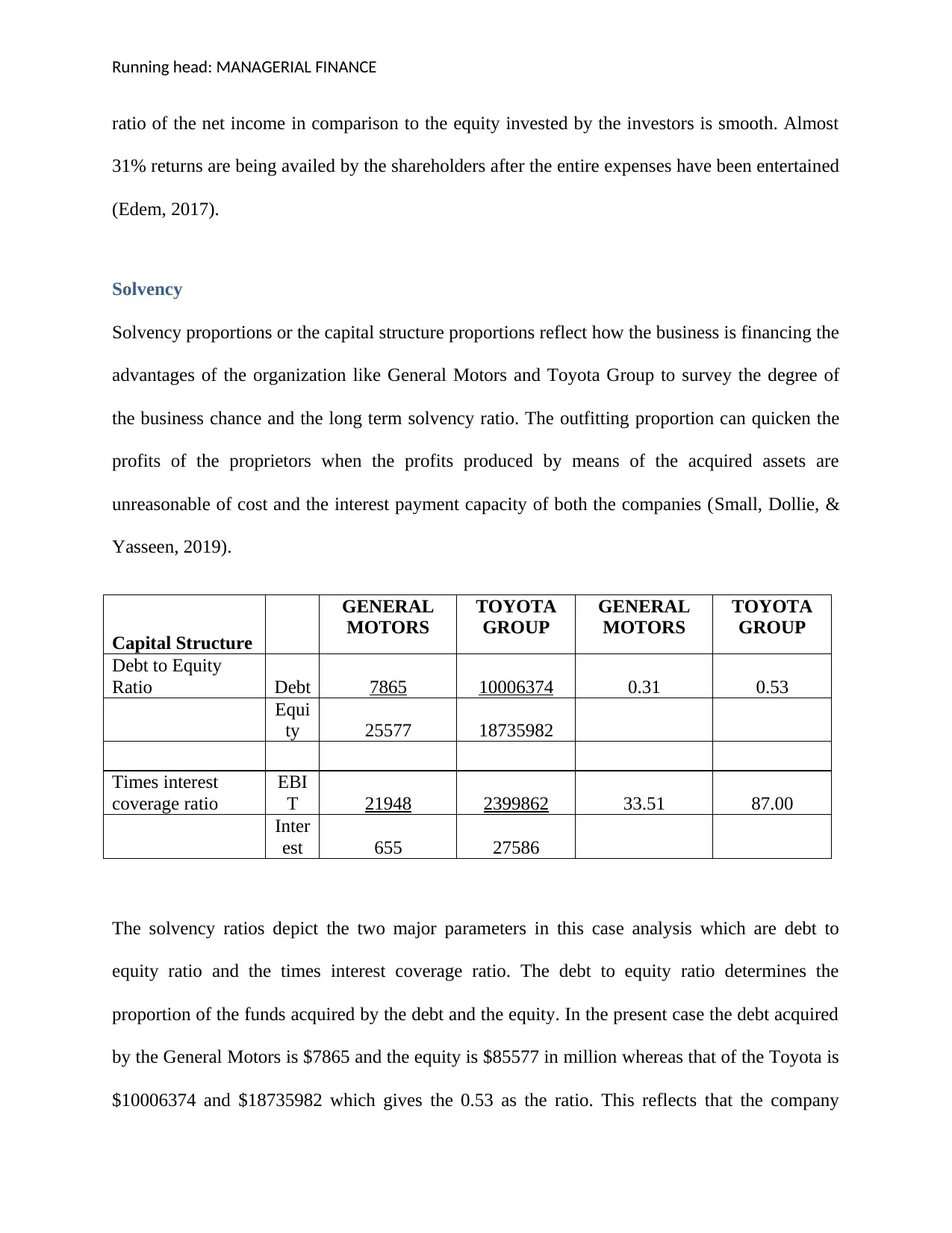

Solvency

Solvency proportions or the capital structure proportions reflect how the business is financing the

advantages of the organization like General Motors and Toyota Group to survey the degree of

the business chance and the long term solvency ratio. The outfitting proportion can quicken the

profits of the proprietors when the profits produced by means of the acquired assets are

unreasonable of cost and the interest payment capacity of both the companies (Small, Dollie, &

Yasseen, 2019).

Capital Structure

GENERAL

MOTORS

TOYOTA

GROUP

GENERAL

MOTORS

TOYOTA

GROUP

Debt to Equity

Ratio Debt 7865 10006374 0.31 0.53

Equi

ty 25577 18735982

Times interest

coverage ratio

EBI

T 21948 2399862 33.51 87.00

Inter

est 655 27586

The solvency ratios depict the two major parameters in this case analysis which are debt to

equity ratio and the times interest coverage ratio. The debt to equity ratio determines the

proportion of the funds acquired by the debt and the equity. In the present case the debt acquired

by the General Motors is $7865 and the equity is $85577 in million whereas that of the Toyota is

$10006374 and $18735982 which gives the 0.53 as the ratio. This reflects that the company

ratio of the net income in comparison to the equity invested by the investors is smooth. Almost

31% returns are being availed by the shareholders after the entire expenses have been entertained

(Edem, 2017).

Solvency

Solvency proportions or the capital structure proportions reflect how the business is financing the

advantages of the organization like General Motors and Toyota Group to survey the degree of

the business chance and the long term solvency ratio. The outfitting proportion can quicken the

profits of the proprietors when the profits produced by means of the acquired assets are

unreasonable of cost and the interest payment capacity of both the companies (Small, Dollie, &

Yasseen, 2019).

Capital Structure

GENERAL

MOTORS

TOYOTA

GROUP

GENERAL

MOTORS

TOYOTA

GROUP

Debt to Equity

Ratio Debt 7865 10006374 0.31 0.53

Equi

ty 25577 18735982

Times interest

coverage ratio

EBI

T 21948 2399862 33.51 87.00

Inter

est 655 27586

The solvency ratios depict the two major parameters in this case analysis which are debt to

equity ratio and the times interest coverage ratio. The debt to equity ratio determines the

proportion of the funds acquired by the debt and the equity. In the present case the debt acquired

by the General Motors is $7865 and the equity is $85577 in million whereas that of the Toyota is

$10006374 and $18735982 which gives the 0.53 as the ratio. This reflects that the company

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running head: MANAGERIAL FINANCE

makes use of the debt and the equity in almost equal manner. This is the reason the return on

equity was lower. In case of the general motors is 0.31 thus indicating the debt portion is lower

than the equity. Hence in this scenario the General Motors is one point ahead from the point of

view of the investment (Volpe & Banfi, 2017).

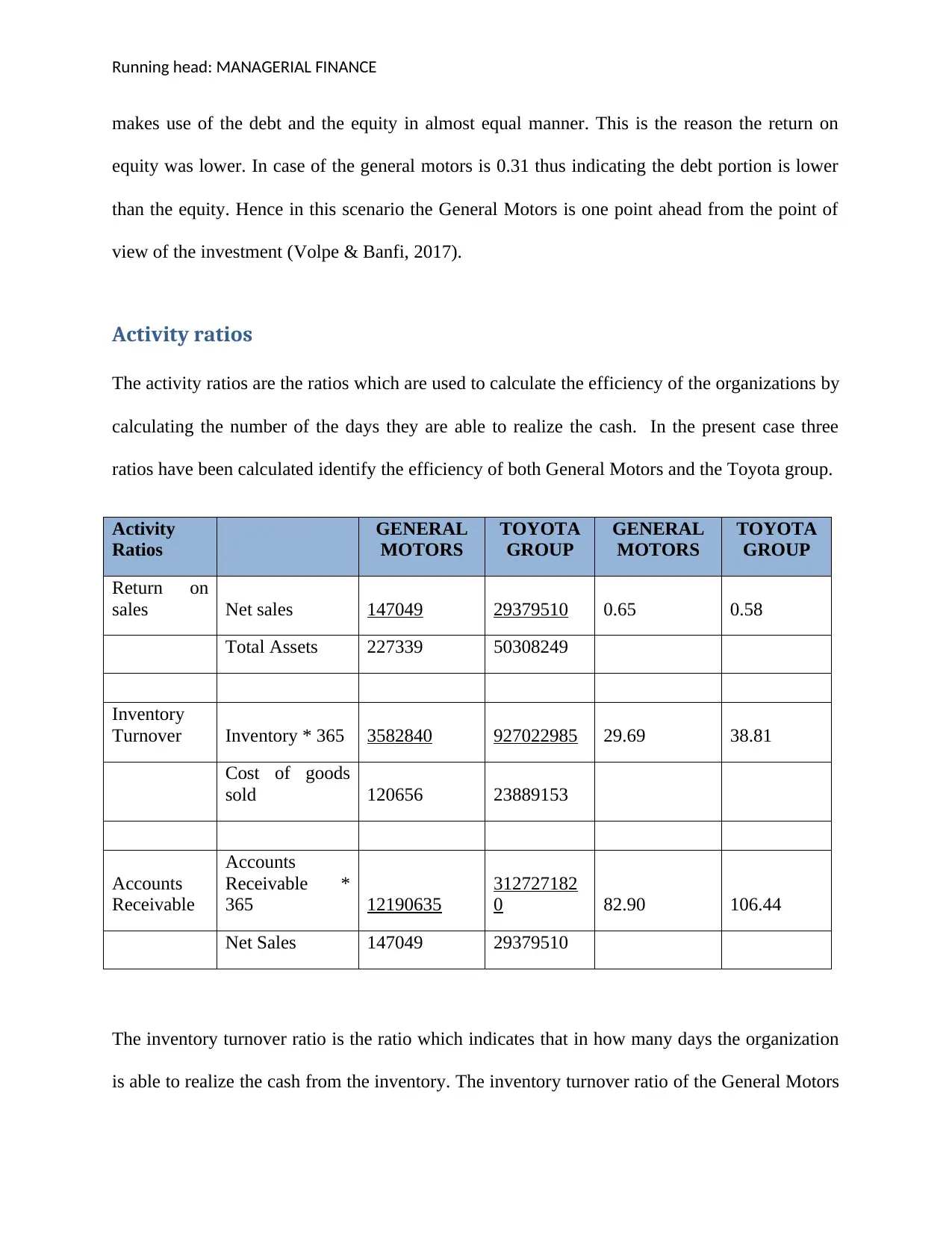

Activity ratios

The activity ratios are the ratios which are used to calculate the efficiency of the organizations by

calculating the number of the days they are able to realize the cash. In the present case three

ratios have been calculated identify the efficiency of both General Motors and the Toyota group.

Activity

Ratios

GENERAL

MOTORS

TOYOTA

GROUP

GENERAL

MOTORS

TOYOTA

GROUP

Return on

sales Net sales 147049 29379510 0.65 0.58

Total Assets 227339 50308249

Inventory

Turnover Inventory * 365 3582840 927022985 29.69 38.81

Cost of goods

sold 120656 23889153

Accounts

Receivable

Accounts

Receivable *

365 12190635

312727182

0 82.90 106.44

Net Sales 147049 29379510

The inventory turnover ratio is the ratio which indicates that in how many days the organization

is able to realize the cash from the inventory. The inventory turnover ratio of the General Motors

makes use of the debt and the equity in almost equal manner. This is the reason the return on

equity was lower. In case of the general motors is 0.31 thus indicating the debt portion is lower

than the equity. Hence in this scenario the General Motors is one point ahead from the point of

view of the investment (Volpe & Banfi, 2017).

Activity ratios

The activity ratios are the ratios which are used to calculate the efficiency of the organizations by

calculating the number of the days they are able to realize the cash. In the present case three

ratios have been calculated identify the efficiency of both General Motors and the Toyota group.

Activity

Ratios

GENERAL

MOTORS

TOYOTA

GROUP

GENERAL

MOTORS

TOYOTA

GROUP

Return on

sales Net sales 147049 29379510 0.65 0.58

Total Assets 227339 50308249

Inventory

Turnover Inventory * 365 3582840 927022985 29.69 38.81

Cost of goods

sold 120656 23889153

Accounts

Receivable

Accounts

Receivable *

365 12190635

312727182

0 82.90 106.44

Net Sales 147049 29379510

The inventory turnover ratio is the ratio which indicates that in how many days the organization

is able to realize the cash from the inventory. The inventory turnover ratio of the General Motors

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running head: MANAGERIAL FINANCE

is 29.6 whereas that of the Toyota Company is 38.81 days. The General Motors is able to realize

the cash easily as the cost of the goods is lower and the inventory is not piled up. In case of the

Toyota the company is taking more time to realize the cash from the market due to the wide

business operations and also due to the inventory in the warehouse. Further, the accounts

receivables of the General Motors are 82.9 days whereas that of the Toyota Group is 106.4 days

which is beyond the acceptable level. The company’s cash conversion cycle would see an impact

due to the low speed of the process (Olesen, Petersen & Podinovski, 2015). Lastly the return on

sales is also one of the ratios which determine how well the company has generated the net sales

with the use of the assets. The company is able to generate the sales efficiently and still ahead of

the Toyota Motors. From the point of the investment the investor shall choose General Motors.

The organization can begin by setting up the aging schedules to figure out for how much time the

receivables are extraordinary. The approach of the audit can be seen on the consistent premise to

recognize for the examples in the reprobate records.

Developing a technique to distinguish the feeble clients and the reprobate records can be

one of the arrangements to improve the delinquent of the clients.

The client will be given receipt as indicated by the significant timespan (Pratt, 2016).

The arrangement of presenting the client impetuses is one of the most significant factors

in deciding the brief installment techniques and the limits and the extra items.

From the overall analysis it can be stated that the General motors is performing well than the

Toyota Motors in all aspects except the liquidity position. Apart from that the profitability,

solvency as well as the efficiency the company is smooth and sound form the point of view of

is 29.6 whereas that of the Toyota Company is 38.81 days. The General Motors is able to realize

the cash easily as the cost of the goods is lower and the inventory is not piled up. In case of the

Toyota the company is taking more time to realize the cash from the market due to the wide

business operations and also due to the inventory in the warehouse. Further, the accounts

receivables of the General Motors are 82.9 days whereas that of the Toyota Group is 106.4 days

which is beyond the acceptable level. The company’s cash conversion cycle would see an impact

due to the low speed of the process (Olesen, Petersen & Podinovski, 2015). Lastly the return on

sales is also one of the ratios which determine how well the company has generated the net sales

with the use of the assets. The company is able to generate the sales efficiently and still ahead of

the Toyota Motors. From the point of the investment the investor shall choose General Motors.

The organization can begin by setting up the aging schedules to figure out for how much time the

receivables are extraordinary. The approach of the audit can be seen on the consistent premise to

recognize for the examples in the reprobate records.

Developing a technique to distinguish the feeble clients and the reprobate records can be

one of the arrangements to improve the delinquent of the clients.

The client will be given receipt as indicated by the significant timespan (Pratt, 2016).

The arrangement of presenting the client impetuses is one of the most significant factors

in deciding the brief installment techniques and the limits and the extra items.

From the overall analysis it can be stated that the General motors is performing well than the

Toyota Motors in all aspects except the liquidity position. Apart from that the profitability,

solvency as well as the efficiency the company is smooth and sound form the point of view of

Running head: MANAGERIAL FINANCE

the investors. Also, the recommendations have been provided for the purpose of the

improvement of the liquidity. Hence, the General Motors is the acceptable choice.

Part II

1. If the company spends $40000 the company shall not include in the cost of the initial

outlay as this cost is a variable cost or say one time investment which is bound to be

done. At times it may also happen that the company may not incur this cost in the later

years, henceforth this cost shall not be included in the cost of the outlay.

2. The depreciation of the machinery is charged on the overall cost of the machinery. The

overall cost does not include any shipping charges or installation charge. Hence the

purchase price which is $20000 and hence the depreciation amount is (200000-

25000)*7.41%. The reason behind taking the 7.41% is the use of the MACRS asset for

the period of the three years. The rate of the depreciation associated with the period of the

three years is 7.41% hence the value of the deprecation is 12968.

3. The annual sales are $250000 in the first year and thereafter there was an increase of the

3% annually. The cost of the sales is $125000 and thereafter they are increased by 3%

every year.

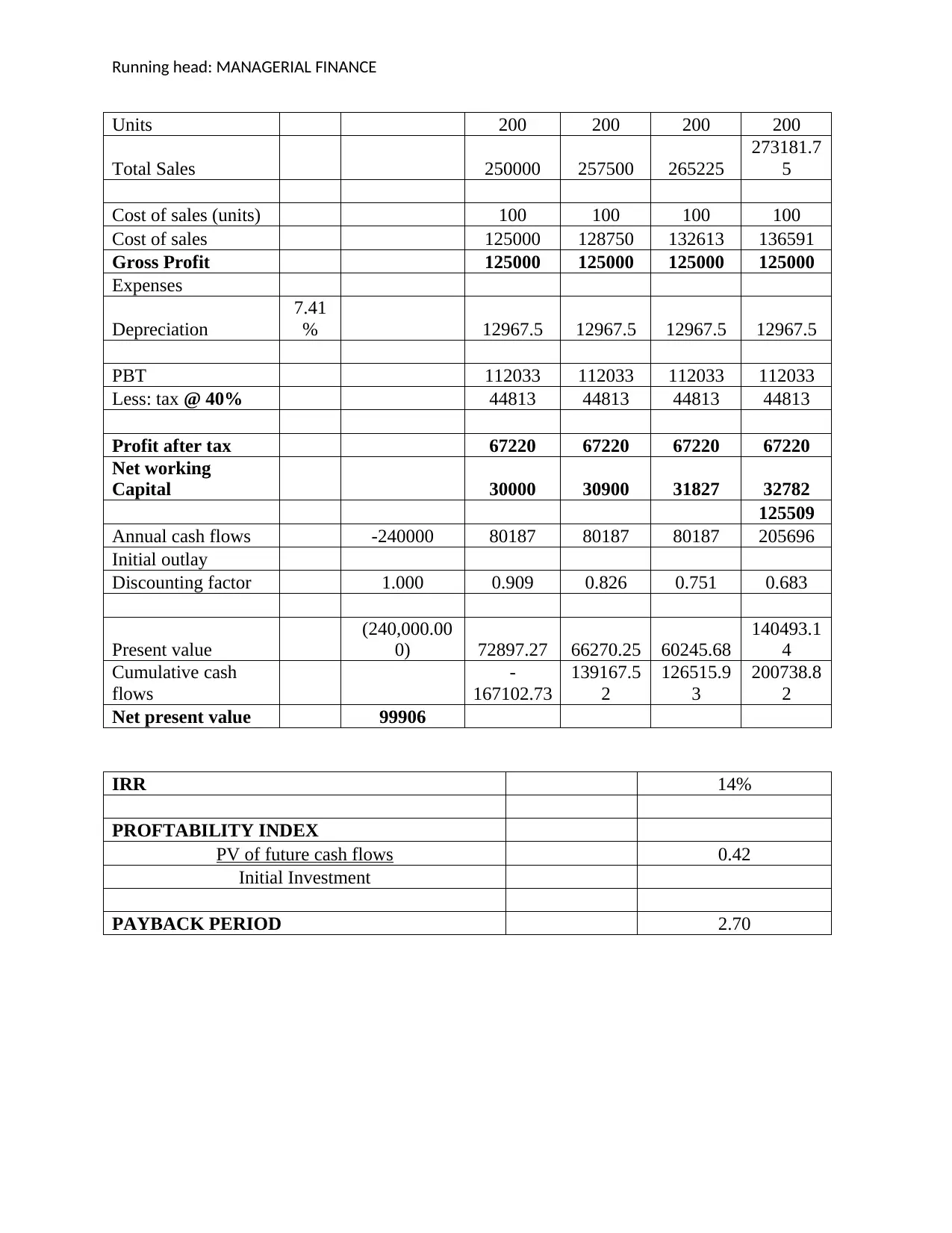

4. The calculations have been presented in the table below.

5. The net required working capital would be $125509 which is to be recovered at the end

of the 4th year.

6. The after tax cash flows has been calculated in the table below.

7. The calculations have been presented in the table below.

8. The methodology of the payback period alone is not sufficient to decide whether the

project shall be accepted or rejected. If the net present value comes to

the investors. Also, the recommendations have been provided for the purpose of the

improvement of the liquidity. Hence, the General Motors is the acceptable choice.

Part II

1. If the company spends $40000 the company shall not include in the cost of the initial

outlay as this cost is a variable cost or say one time investment which is bound to be

done. At times it may also happen that the company may not incur this cost in the later

years, henceforth this cost shall not be included in the cost of the outlay.

2. The depreciation of the machinery is charged on the overall cost of the machinery. The

overall cost does not include any shipping charges or installation charge. Hence the

purchase price which is $20000 and hence the depreciation amount is (200000-

25000)*7.41%. The reason behind taking the 7.41% is the use of the MACRS asset for

the period of the three years. The rate of the depreciation associated with the period of the

three years is 7.41% hence the value of the deprecation is 12968.

3. The annual sales are $250000 in the first year and thereafter there was an increase of the

3% annually. The cost of the sales is $125000 and thereafter they are increased by 3%

every year.

4. The calculations have been presented in the table below.

5. The net required working capital would be $125509 which is to be recovered at the end

of the 4th year.

6. The after tax cash flows has been calculated in the table below.

7. The calculations have been presented in the table below.

8. The methodology of the payback period alone is not sufficient to decide whether the

project shall be accepted or rejected. If the net present value comes to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running head: MANAGERIAL FINANCE

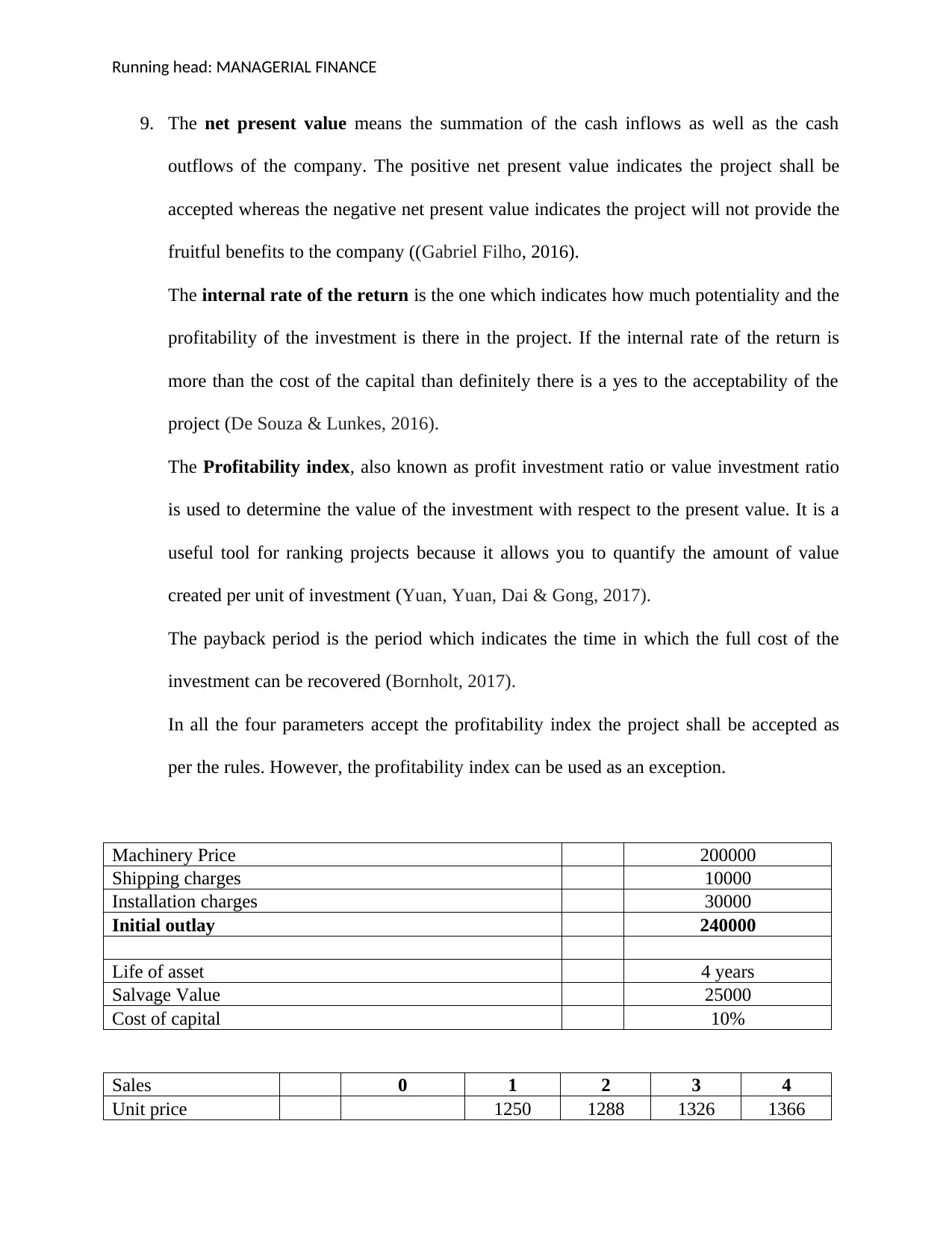

9. The net present value means the summation of the cash inflows as well as the cash

outflows of the company. The positive net present value indicates the project shall be

accepted whereas the negative net present value indicates the project will not provide the

fruitful benefits to the company ((Gabriel Filho, 2016).

The internal rate of the return is the one which indicates how much potentiality and the

profitability of the investment is there in the project. If the internal rate of the return is

more than the cost of the capital than definitely there is a yes to the acceptability of the

project (De Souza & Lunkes, 2016).

The Profitability index, also known as profit investment ratio or value investment ratio

is used to determine the value of the investment with respect to the present value. It is a

useful tool for ranking projects because it allows you to quantify the amount of value

created per unit of investment (Yuan, Yuan, Dai & Gong, 2017).

The payback period is the period which indicates the time in which the full cost of the

investment can be recovered (Bornholt, 2017).

In all the four parameters accept the profitability index the project shall be accepted as

per the rules. However, the profitability index can be used as an exception.

Machinery Price 200000

Shipping charges 10000

Installation charges 30000

Initial outlay 240000

Life of asset 4 years

Salvage Value 25000

Cost of capital 10%

Sales 0 1 2 3 4

Unit price 1250 1288 1326 1366

9. The net present value means the summation of the cash inflows as well as the cash

outflows of the company. The positive net present value indicates the project shall be

accepted whereas the negative net present value indicates the project will not provide the

fruitful benefits to the company ((Gabriel Filho, 2016).

The internal rate of the return is the one which indicates how much potentiality and the

profitability of the investment is there in the project. If the internal rate of the return is

more than the cost of the capital than definitely there is a yes to the acceptability of the

project (De Souza & Lunkes, 2016).

The Profitability index, also known as profit investment ratio or value investment ratio

is used to determine the value of the investment with respect to the present value. It is a

useful tool for ranking projects because it allows you to quantify the amount of value

created per unit of investment (Yuan, Yuan, Dai & Gong, 2017).

The payback period is the period which indicates the time in which the full cost of the

investment can be recovered (Bornholt, 2017).

In all the four parameters accept the profitability index the project shall be accepted as

per the rules. However, the profitability index can be used as an exception.

Machinery Price 200000

Shipping charges 10000

Installation charges 30000

Initial outlay 240000

Life of asset 4 years

Salvage Value 25000

Cost of capital 10%

Sales 0 1 2 3 4

Unit price 1250 1288 1326 1366

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running head: MANAGERIAL FINANCE

Units 200 200 200 200

Total Sales 250000 257500 265225

273181.7

5

Cost of sales (units) 100 100 100 100

Cost of sales 125000 128750 132613 136591

Gross Profit 125000 125000 125000 125000

Expenses

Depreciation

7.41

% 12967.5 12967.5 12967.5 12967.5

PBT 112033 112033 112033 112033

Less: tax @ 40% 44813 44813 44813 44813

Profit after tax 67220 67220 67220 67220

Net working

Capital 30000 30900 31827 32782

125509

Annual cash flows -240000 80187 80187 80187 205696

Initial outlay

Discounting factor 1.000 0.909 0.826 0.751 0.683

Present value

(240,000.00

0) 72897.27 66270.25 60245.68

140493.1

4

Cumulative cash

flows

-

167102.73

139167.5

2

126515.9

3

200738.8

2

Net present value 99906

IRR 14%

PROFTABILITY INDEX

PV of future cash flows 0.42

Initial Investment

PAYBACK PERIOD 2.70

Units 200 200 200 200

Total Sales 250000 257500 265225

273181.7

5

Cost of sales (units) 100 100 100 100

Cost of sales 125000 128750 132613 136591

Gross Profit 125000 125000 125000 125000

Expenses

Depreciation

7.41

% 12967.5 12967.5 12967.5 12967.5

PBT 112033 112033 112033 112033

Less: tax @ 40% 44813 44813 44813 44813

Profit after tax 67220 67220 67220 67220

Net working

Capital 30000 30900 31827 32782

125509

Annual cash flows -240000 80187 80187 80187 205696

Initial outlay

Discounting factor 1.000 0.909 0.826 0.751 0.683

Present value

(240,000.00

0) 72897.27 66270.25 60245.68

140493.1

4

Cumulative cash

flows

-

167102.73

139167.5

2

126515.9

3

200738.8

2

Net present value 99906

IRR 14%

PROFTABILITY INDEX

PV of future cash flows 0.42

Initial Investment

PAYBACK PERIOD 2.70

Running head: MANAGERIAL FINANCE

References

Bornholt, G. (2017). What is an Investment Project's Implied Rate of Return?. Abacus, 53(4),

513-526.

Boyas, E., & Teeter, R. (2017). Teaching Financial Ratio Analysis using XBRL. In

Developments in Business Simulation and Experiential Learning: Proceedings of the

Annual ABSEL conference (Vol. 44, No. 1).

De Souza, P., & Lunkes, R. J. (2016). Capital budgeting practices by large Brazilian

companies. Contaduría y Administración, 61(3), 514-534.

Edem, D. B. (2017). Liquidity Management and Performance of Deposit Money Banks in

Nigeria (1986–2011): An Investigation. International Journal of Economics, Finance and

Management Sciences, 5(3), 146-161.

Gabriel Filho, L. A., Cremasco, C. P., Putti, F. F., Goes, B. C., & Magalhaes, M. M. (2016).

Geometric Analysis of Net Present Value and Internal Rate of Return. Journal of Applied

Mathematics & Informatics, 34, 75-84.

Khan, R. A., & Ali, M. (2016). Impact of liquidity on profitability of commercial banks in

Pakistan: An analysis on banking sector in Pakistan. Global Journal of Management and

Business Research.

Ko, Y. C., Fujita, H., & Li, T. (2017). An evidential analysis of Altman Z-score for financial

predictions: Case study on solar energy companies. Applied Soft Computing, 52, 748-759.

References

Bornholt, G. (2017). What is an Investment Project's Implied Rate of Return?. Abacus, 53(4),

513-526.

Boyas, E., & Teeter, R. (2017). Teaching Financial Ratio Analysis using XBRL. In

Developments in Business Simulation and Experiential Learning: Proceedings of the

Annual ABSEL conference (Vol. 44, No. 1).

De Souza, P., & Lunkes, R. J. (2016). Capital budgeting practices by large Brazilian

companies. Contaduría y Administración, 61(3), 514-534.

Edem, D. B. (2017). Liquidity Management and Performance of Deposit Money Banks in

Nigeria (1986–2011): An Investigation. International Journal of Economics, Finance and

Management Sciences, 5(3), 146-161.

Gabriel Filho, L. A., Cremasco, C. P., Putti, F. F., Goes, B. C., & Magalhaes, M. M. (2016).

Geometric Analysis of Net Present Value and Internal Rate of Return. Journal of Applied

Mathematics & Informatics, 34, 75-84.

Khan, R. A., & Ali, M. (2016). Impact of liquidity on profitability of commercial banks in

Pakistan: An analysis on banking sector in Pakistan. Global Journal of Management and

Business Research.

Ko, Y. C., Fujita, H., & Li, T. (2017). An evidential analysis of Altman Z-score for financial

predictions: Case study on solar energy companies. Applied Soft Computing, 52, 748-759.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.