LSBM203 - Managerial Finance: Ratio Analysis and Investment Appraisal

VerifiedAdded on 2023/06/15

|14

|3807

|295

Report

AI Summary

This report provides a managerial finance analysis, dividing into two portfolios: ratio analysis of B&M and Morrison, and investment appraisal techniques. Portfolio 1 assesses growth, profitability, and financial ratios, highlighting areas where Morrison underperforms compared to B&M, particularly in liquidity, profit margins, and gearing ratios. Recommendations suggest Morrison needs significant improvements. The report also acknowledges the limitations of financial ratios. Portfolio 2 focuses on capital investment appraisal techniques and their limitations. Desklib offers this and similar resources to aid students in their studies.

Managerial Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

Portfolio 1........................................................................................................................................1

Summary......................................................................................................................................1

Recommendation.........................................................................................................................7

Limitations of Financial Ratios...................................................................................................7

Portfolio 2........................................................................................................................................8

Capital investment Appraisal Techniques...................................................................................8

Limitation of Investment appraisal techniques............................................................................9

Limitations of Investment Appraisal Techniques......................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

Portfolio 1........................................................................................................................................1

Summary......................................................................................................................................1

Recommendation.........................................................................................................................7

Limitations of Financial Ratios...................................................................................................7

Portfolio 2........................................................................................................................................8

Capital investment Appraisal Techniques...................................................................................8

Limitation of Investment appraisal techniques............................................................................9

Limitations of Investment Appraisal Techniques......................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Managerial finance is an important aspect as it is related with the funds of the company

which can be used in an impactful manner so as to add value to the company in the long run so

that it can achieve its goals and objectives that are made in the starting as a whole (Akhigbe,

Newman and Whyte, 2017). The below report is divided into 2 parts that is portfolio 1 and

portfolio 2 and both the portfolios carries a lot of value in the long run for the firm. In the first

part there is an evaluation of the company’s ratios that is B&M and Morrison while in the part 2

there is an analysis of the techniques used is done so that the firm can take appropriate decisions

on the investing part of the firm.

Portfolio 1

Summary

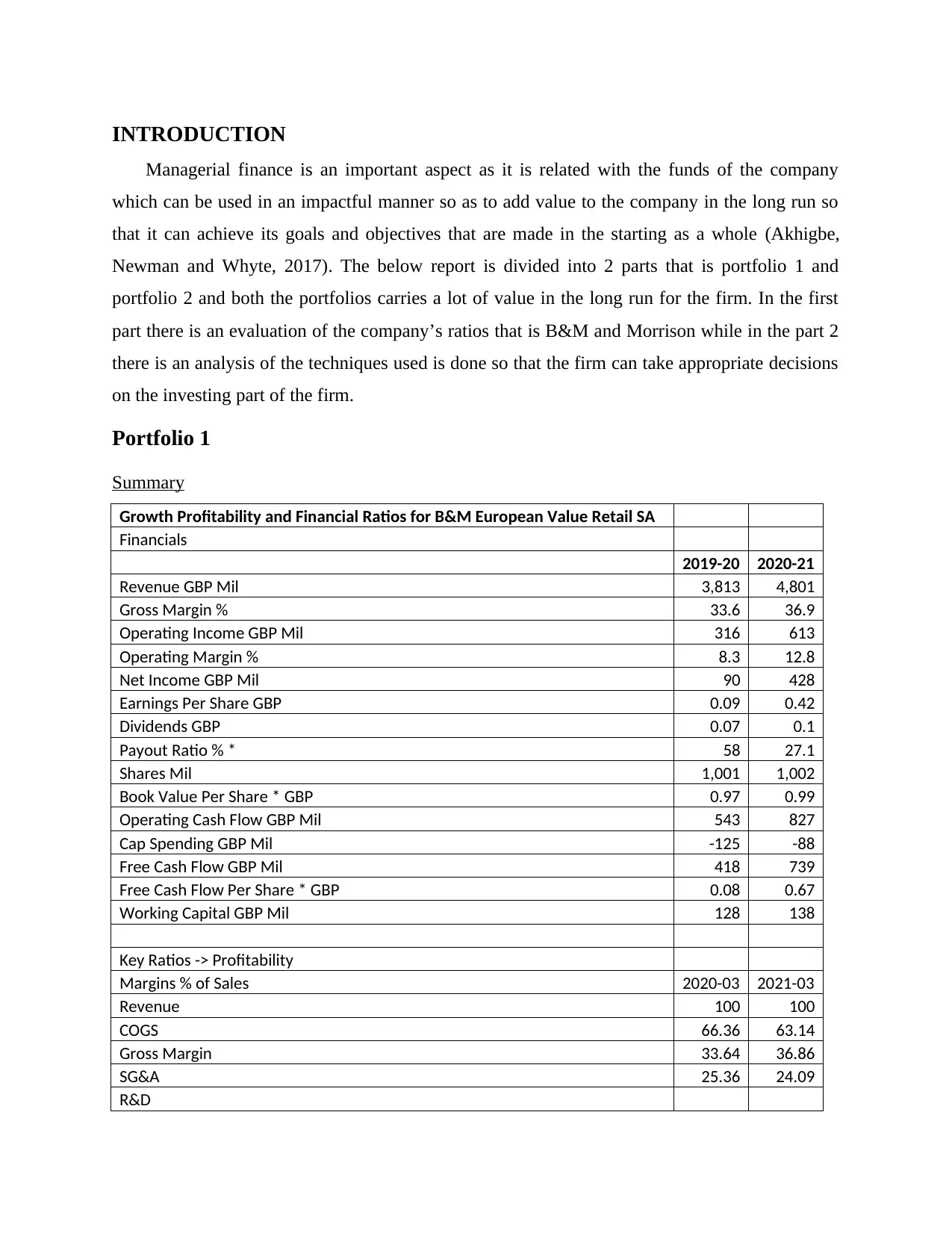

Growth Profitability and Financial Ratios for B&M European Value Retail SA

Financials

2019-20 2020-21

Revenue GBP Mil 3,813 4,801

Gross Margin % 33.6 36.9

Operating Income GBP Mil 316 613

Operating Margin % 8.3 12.8

Net Income GBP Mil 90 428

Earnings Per Share GBP 0.09 0.42

Dividends GBP 0.07 0.1

Payout Ratio % * 58 27.1

Shares Mil 1,001 1,002

Book Value Per Share * GBP 0.97 0.99

Operating Cash Flow GBP Mil 543 827

Cap Spending GBP Mil -125 -88

Free Cash Flow GBP Mil 418 739

Free Cash Flow Per Share * GBP 0.08 0.67

Working Capital GBP Mil 128 138

Key Ratios -> Profitability

Margins % of Sales 2020-03 2021-03

Revenue 100 100

COGS 66.36 63.14

Gross Margin 33.64 36.86

SG&A 25.36 24.09

R&D

Managerial finance is an important aspect as it is related with the funds of the company

which can be used in an impactful manner so as to add value to the company in the long run so

that it can achieve its goals and objectives that are made in the starting as a whole (Akhigbe,

Newman and Whyte, 2017). The below report is divided into 2 parts that is portfolio 1 and

portfolio 2 and both the portfolios carries a lot of value in the long run for the firm. In the first

part there is an evaluation of the company’s ratios that is B&M and Morrison while in the part 2

there is an analysis of the techniques used is done so that the firm can take appropriate decisions

on the investing part of the firm.

Portfolio 1

Summary

Growth Profitability and Financial Ratios for B&M European Value Retail SA

Financials

2019-20 2020-21

Revenue GBP Mil 3,813 4,801

Gross Margin % 33.6 36.9

Operating Income GBP Mil 316 613

Operating Margin % 8.3 12.8

Net Income GBP Mil 90 428

Earnings Per Share GBP 0.09 0.42

Dividends GBP 0.07 0.1

Payout Ratio % * 58 27.1

Shares Mil 1,001 1,002

Book Value Per Share * GBP 0.97 0.99

Operating Cash Flow GBP Mil 543 827

Cap Spending GBP Mil -125 -88

Free Cash Flow GBP Mil 418 739

Free Cash Flow Per Share * GBP 0.08 0.67

Working Capital GBP Mil 128 138

Key Ratios -> Profitability

Margins % of Sales 2020-03 2021-03

Revenue 100 100

COGS 66.36 63.14

Gross Margin 33.64 36.86

SG&A 25.36 24.09

R&D

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Other

Operating Margin 8.28 12.78

Net Int Inc & Other -1.67 -1.83

EBT Margin 6.61 10.94

Profitability 2020-03 2021-03

Tax Rate % 22.71 18.52

Net Margin % 2.36 8.92

Asset Turnover (Average) 1.29 1.38

Return on Assets % 3.05 12.36

Financial Leverage (Average) 4.12 4.58

Return on Equity % 9.35 53.5

Return on Invested Capital % 6.46 17.41

Interest Coverage 4.15 7.26

Key Ratios -> Growth

2020-03 2021-03

Revenue %

Year over Year 9.38 25.91

3-Year Average 16.2 16.59

5-Year Average 18.29 18.73

10-Year Average

Operating Income %

Year over Year 19.48 94.19

3-Year Average 15.6 36.76

5-Year Average 15.01 27.67

10-Year Average

Net Income %

Year over Year -56.12 375.53

3-Year Average -14.28 32.06

5-Year Average 18.43 28.01

10-Year Average

EPS %

Year over Year -56.1 374.44

3-Year Average -14.3 31.92

5-Year Average 21.49 28.06

10-Year Average

Key Ratios -> Cash Flow

Cash Flow Ratios 2020-03 2021-03

Operating Cash Flow Growth % YOY 155.81 52.3

Free Cash Flow Growth % YOY 294.95 76.67

Cap Ex as a % of Sales 3.27 1.83

Operating Margin 8.28 12.78

Net Int Inc & Other -1.67 -1.83

EBT Margin 6.61 10.94

Profitability 2020-03 2021-03

Tax Rate % 22.71 18.52

Net Margin % 2.36 8.92

Asset Turnover (Average) 1.29 1.38

Return on Assets % 3.05 12.36

Financial Leverage (Average) 4.12 4.58

Return on Equity % 9.35 53.5

Return on Invested Capital % 6.46 17.41

Interest Coverage 4.15 7.26

Key Ratios -> Growth

2020-03 2021-03

Revenue %

Year over Year 9.38 25.91

3-Year Average 16.2 16.59

5-Year Average 18.29 18.73

10-Year Average

Operating Income %

Year over Year 19.48 94.19

3-Year Average 15.6 36.76

5-Year Average 15.01 27.67

10-Year Average

Net Income %

Year over Year -56.12 375.53

3-Year Average -14.28 32.06

5-Year Average 18.43 28.01

10-Year Average

EPS %

Year over Year -56.1 374.44

3-Year Average -14.3 31.92

5-Year Average 21.49 28.06

10-Year Average

Key Ratios -> Cash Flow

Cash Flow Ratios 2020-03 2021-03

Operating Cash Flow Growth % YOY 155.81 52.3

Free Cash Flow Growth % YOY 294.95 76.67

Cap Ex as a % of Sales 3.27 1.83

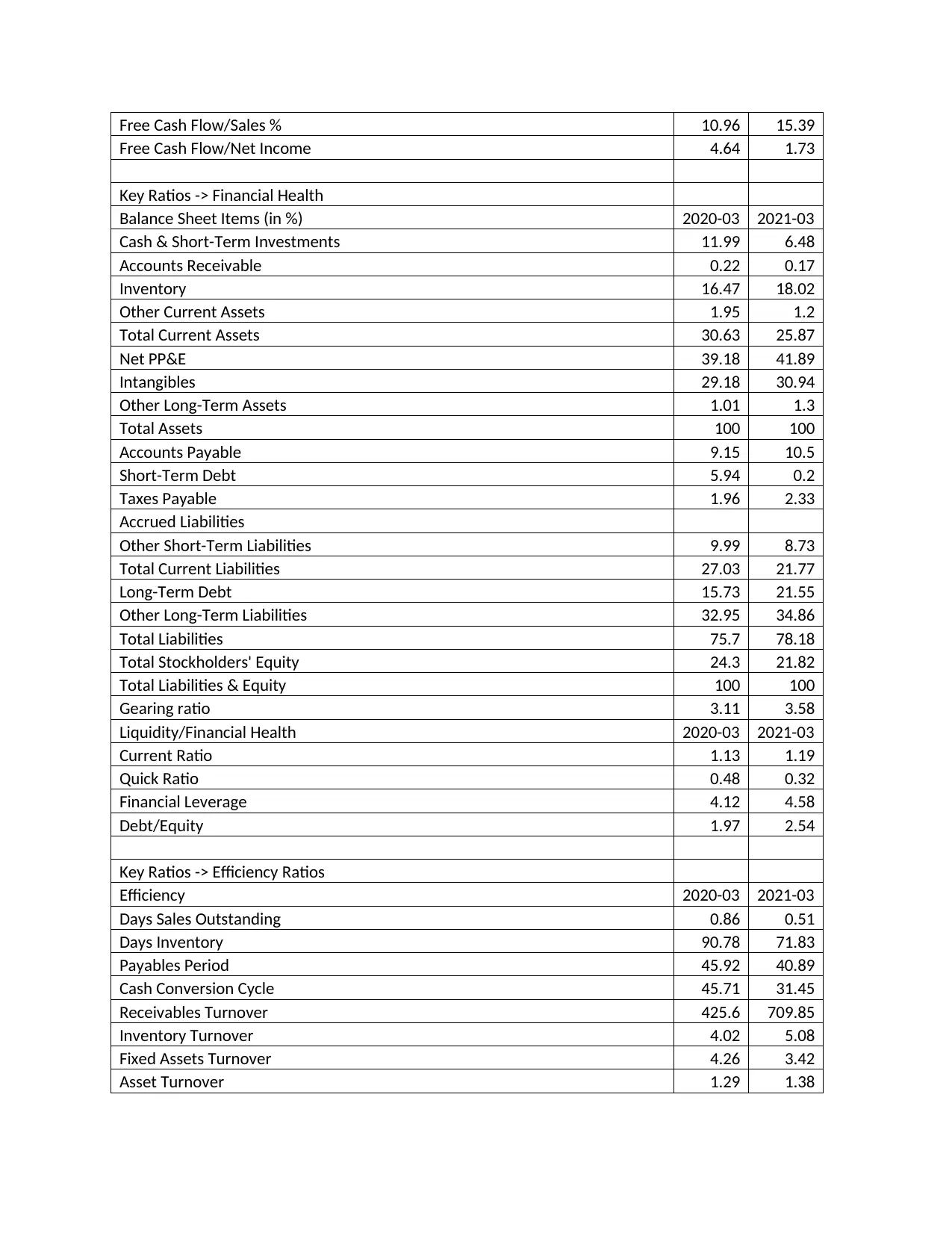

Free Cash Flow/Sales % 10.96 15.39

Free Cash Flow/Net Income 4.64 1.73

Key Ratios -> Financial Health

Balance Sheet Items (in %) 2020-03 2021-03

Cash & Short-Term Investments 11.99 6.48

Accounts Receivable 0.22 0.17

Inventory 16.47 18.02

Other Current Assets 1.95 1.2

Total Current Assets 30.63 25.87

Net PP&E 39.18 41.89

Intangibles 29.18 30.94

Other Long-Term Assets 1.01 1.3

Total Assets 100 100

Accounts Payable 9.15 10.5

Short-Term Debt 5.94 0.2

Taxes Payable 1.96 2.33

Accrued Liabilities

Other Short-Term Liabilities 9.99 8.73

Total Current Liabilities 27.03 21.77

Long-Term Debt 15.73 21.55

Other Long-Term Liabilities 32.95 34.86

Total Liabilities 75.7 78.18

Total Stockholders' Equity 24.3 21.82

Total Liabilities & Equity 100 100

Gearing ratio 3.11 3.58

Liquidity/Financial Health 2020-03 2021-03

Current Ratio 1.13 1.19

Quick Ratio 0.48 0.32

Financial Leverage 4.12 4.58

Debt/Equity 1.97 2.54

Key Ratios -> Efficiency Ratios

Efficiency 2020-03 2021-03

Days Sales Outstanding 0.86 0.51

Days Inventory 90.78 71.83

Payables Period 45.92 40.89

Cash Conversion Cycle 45.71 31.45

Receivables Turnover 425.6 709.85

Inventory Turnover 4.02 5.08

Fixed Assets Turnover 4.26 3.42

Asset Turnover 1.29 1.38

Free Cash Flow/Net Income 4.64 1.73

Key Ratios -> Financial Health

Balance Sheet Items (in %) 2020-03 2021-03

Cash & Short-Term Investments 11.99 6.48

Accounts Receivable 0.22 0.17

Inventory 16.47 18.02

Other Current Assets 1.95 1.2

Total Current Assets 30.63 25.87

Net PP&E 39.18 41.89

Intangibles 29.18 30.94

Other Long-Term Assets 1.01 1.3

Total Assets 100 100

Accounts Payable 9.15 10.5

Short-Term Debt 5.94 0.2

Taxes Payable 1.96 2.33

Accrued Liabilities

Other Short-Term Liabilities 9.99 8.73

Total Current Liabilities 27.03 21.77

Long-Term Debt 15.73 21.55

Other Long-Term Liabilities 32.95 34.86

Total Liabilities 75.7 78.18

Total Stockholders' Equity 24.3 21.82

Total Liabilities & Equity 100 100

Gearing ratio 3.11 3.58

Liquidity/Financial Health 2020-03 2021-03

Current Ratio 1.13 1.19

Quick Ratio 0.48 0.32

Financial Leverage 4.12 4.58

Debt/Equity 1.97 2.54

Key Ratios -> Efficiency Ratios

Efficiency 2020-03 2021-03

Days Sales Outstanding 0.86 0.51

Days Inventory 90.78 71.83

Payables Period 45.92 40.89

Cash Conversion Cycle 45.71 31.45

Receivables Turnover 425.6 709.85

Inventory Turnover 4.02 5.08

Fixed Assets Turnover 4.26 3.42

Asset Turnover 1.29 1.38

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

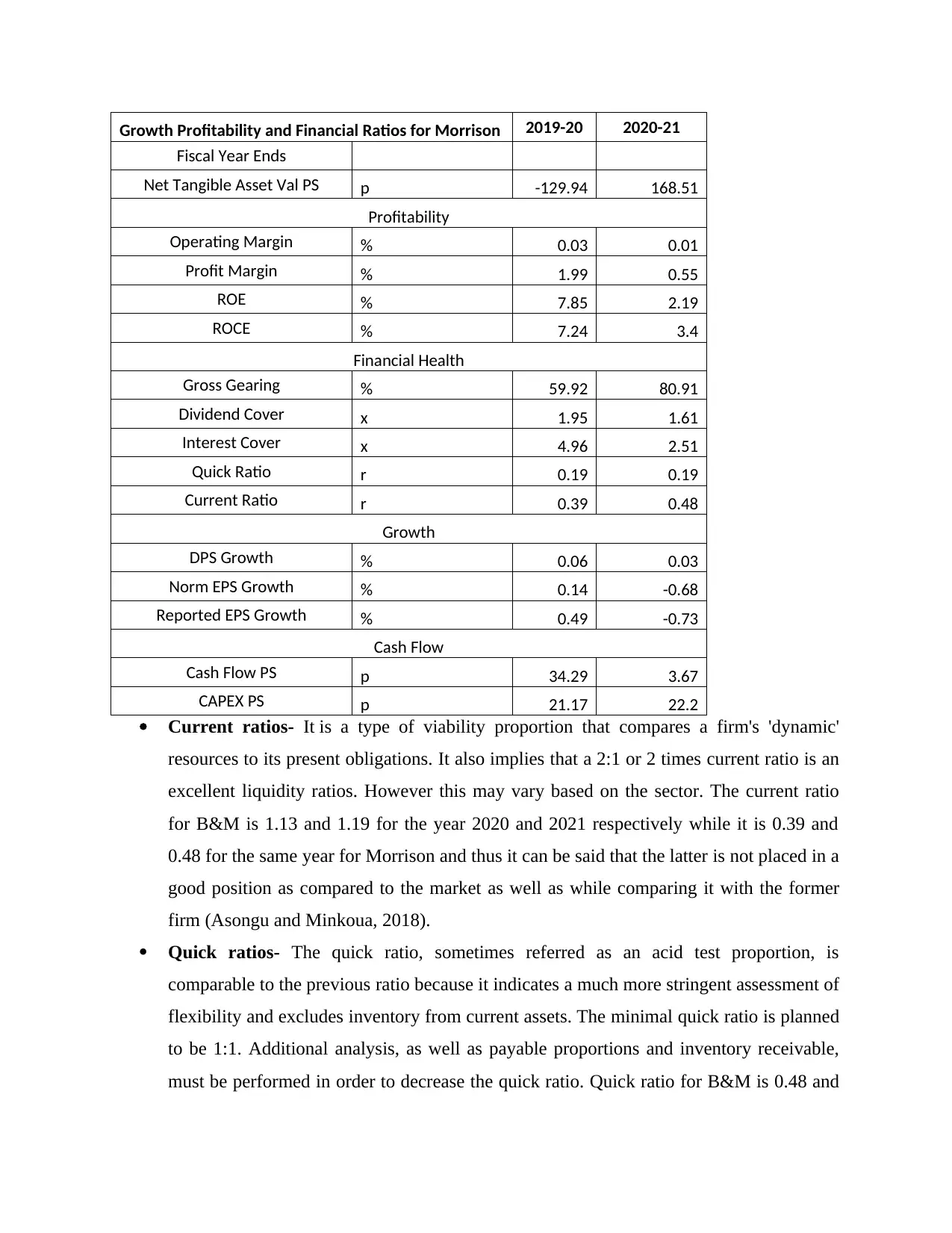

Growth Profitability and Financial Ratios for Morrison 2019-20 2020-21

Fiscal Year Ends

Net Tangible Asset Val PS p -129.94 168.51

Profitability

Operating Margin % 0.03 0.01

Profit Margin % 1.99 0.55

ROE % 7.85 2.19

ROCE % 7.24 3.4

Financial Health

Gross Gearing % 59.92 80.91

Dividend Cover x 1.95 1.61

Interest Cover x 4.96 2.51

Quick Ratio r 0.19 0.19

Current Ratio r 0.39 0.48

Growth

DPS Growth % 0.06 0.03

Norm EPS Growth % 0.14 -0.68

Reported EPS Growth % 0.49 -0.73

Cash Flow

Cash Flow PS p 34.29 3.67

CAPEX PS p 21.17 22.2

Current ratios- It is a type of viability proportion that compares a firm's 'dynamic'

resources to its present obligations. It also implies that a 2:1 or 2 times current ratio is an

excellent liquidity ratios. However this may vary based on the sector. The current ratio

for B&M is 1.13 and 1.19 for the year 2020 and 2021 respectively while it is 0.39 and

0.48 for the same year for Morrison and thus it can be said that the latter is not placed in a

good position as compared to the market as well as while comparing it with the former

firm (Asongu and Minkoua, 2018).

Quick ratios- The quick ratio, sometimes referred as an acid test proportion, is

comparable to the previous ratio because it indicates a much more stringent assessment of

flexibility and excludes inventory from current assets. The minimal quick ratio is planned

to be 1:1. Additional analysis, as well as payable proportions and inventory receivable,

must be performed in order to decrease the quick ratio. Quick ratio for B&M is 0.48 and

Fiscal Year Ends

Net Tangible Asset Val PS p -129.94 168.51

Profitability

Operating Margin % 0.03 0.01

Profit Margin % 1.99 0.55

ROE % 7.85 2.19

ROCE % 7.24 3.4

Financial Health

Gross Gearing % 59.92 80.91

Dividend Cover x 1.95 1.61

Interest Cover x 4.96 2.51

Quick Ratio r 0.19 0.19

Current Ratio r 0.39 0.48

Growth

DPS Growth % 0.06 0.03

Norm EPS Growth % 0.14 -0.68

Reported EPS Growth % 0.49 -0.73

Cash Flow

Cash Flow PS p 34.29 3.67

CAPEX PS p 21.17 22.2

Current ratios- It is a type of viability proportion that compares a firm's 'dynamic'

resources to its present obligations. It also implies that a 2:1 or 2 times current ratio is an

excellent liquidity ratios. However this may vary based on the sector. The current ratio

for B&M is 1.13 and 1.19 for the year 2020 and 2021 respectively while it is 0.39 and

0.48 for the same year for Morrison and thus it can be said that the latter is not placed in a

good position as compared to the market as well as while comparing it with the former

firm (Asongu and Minkoua, 2018).

Quick ratios- The quick ratio, sometimes referred as an acid test proportion, is

comparable to the previous ratio because it indicates a much more stringent assessment of

flexibility and excludes inventory from current assets. The minimal quick ratio is planned

to be 1:1. Additional analysis, as well as payable proportions and inventory receivable,

must be performed in order to decrease the quick ratio. Quick ratio for B&M is 0.48 and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

0.32 for the year 2020 and 2021 respectively while it is 0.19 and 0.19 for the same year

for Morrison so it can be said that yet again Morrison is not placed at a good position and

thus has to retrospect its operation and that too in a detailed manner (Balteș and

Minculete, 2016).

Operating profit margin- The net profit margins proportion is a type of productivity

statistic that shows that much of the income made is transformed into revenue. A

company with a better income relation or one which is the similar as the prior season may

also be a sign indicating it is performing effectively. This ratio stands at 8.3 and 12.8 for

the year 2020 and 2021 for B&M while for the same year for Morrison it stands at 3 and

1 respectively and hence it can be said that there are a number of aspects that the firm has

to look upon so that it can survive in the market for a longer time period.

Gross Profit margin- The gross margin is a metric which can be utilized to assess a

corporation's general personal and economic sustainability. It also promises to be able to

assist analysts in determining whether a business is able to supply a services or

manufacturing an item, and if so, whether it will do so effectively than its rivals. This

ratio stands at 33.6 and 36.9 for B&M while it is 19.9 and 5.5 for Morrison for the year

2020 and 2021 and thus yet again the latter company is not performing well in this aspect

and thus immediate measures has to be taken so that it can help the company in the long

run (Caselli and Roitman, 2019).

Gearing ratios- The gearing ratio calculates a corporation's fiscal exposure by

comparing the quantity of outstanding cash to the shareholders ownership. Furthermore,

it indicates that a GR of more than 50% may indicate heightened fiscal vulnerability,

whereas anywhere within 25% and 50% might be regarded acceptable. This ratio stands

at 31.1, 35.8 and 59.92, 80.91 for the year 2020 and 2021 for the companies B&M and

Morrison and thus the ratio gives a view that Morrison is not performing well in the

market.

Earnings per share- Price/Earnings ratio is a monetary proportion utilized for

evaluation. Researchers and traders utilize it to calculate the equivalent worth of a

corporation's stock in like-to-like assessments. When the P/E concentration is greater,

buyers can anticipate higher profits in the long term, and whenever the P/E level is lower,

buyers can anticipate lower returns. This ratio is not in a very good position for both the

for Morrison so it can be said that yet again Morrison is not placed at a good position and

thus has to retrospect its operation and that too in a detailed manner (Balteș and

Minculete, 2016).

Operating profit margin- The net profit margins proportion is a type of productivity

statistic that shows that much of the income made is transformed into revenue. A

company with a better income relation or one which is the similar as the prior season may

also be a sign indicating it is performing effectively. This ratio stands at 8.3 and 12.8 for

the year 2020 and 2021 for B&M while for the same year for Morrison it stands at 3 and

1 respectively and hence it can be said that there are a number of aspects that the firm has

to look upon so that it can survive in the market for a longer time period.

Gross Profit margin- The gross margin is a metric which can be utilized to assess a

corporation's general personal and economic sustainability. It also promises to be able to

assist analysts in determining whether a business is able to supply a services or

manufacturing an item, and if so, whether it will do so effectively than its rivals. This

ratio stands at 33.6 and 36.9 for B&M while it is 19.9 and 5.5 for Morrison for the year

2020 and 2021 and thus yet again the latter company is not performing well in this aspect

and thus immediate measures has to be taken so that it can help the company in the long

run (Caselli and Roitman, 2019).

Gearing ratios- The gearing ratio calculates a corporation's fiscal exposure by

comparing the quantity of outstanding cash to the shareholders ownership. Furthermore,

it indicates that a GR of more than 50% may indicate heightened fiscal vulnerability,

whereas anywhere within 25% and 50% might be regarded acceptable. This ratio stands

at 31.1, 35.8 and 59.92, 80.91 for the year 2020 and 2021 for the companies B&M and

Morrison and thus the ratio gives a view that Morrison is not performing well in the

market.

Earnings per share- Price/Earnings ratio is a monetary proportion utilized for

evaluation. Researchers and traders utilize it to calculate the equivalent worth of a

corporation's stock in like-to-like assessments. When the P/E concentration is greater,

buyers can anticipate higher profits in the long term, and whenever the P/E level is lower,

buyers can anticipate lower returns. This ratio is not in a very good position for both the

companies as it is 0.09, 0.42 and 0.14, -0.68 for B&M and Morrison for 2020 and 2021

respectively so it can be said that B&M is still in a good position (Cumming and

Zambelli, 2017).

Return on capital employed- Returns on Capital Employed (ROCE) is a monetary

measure which measures a company's fiscal performance as well as the effectiveness of

its investment. Moreover, it states that this proportion is crucial since buyers evaluate it

while considering investing selections. Whenever that proportion is less than the

frequency where a company repays its debt, it may indicate bad productivity. This ratio

stands at 6.46, 17.41 and 7.24, 3.4 for B&M and Morrison for the year 2020 and 2021

respectively and thus it can be seen that B&M firm is placed at a good stance as

compared to other company..

Average inventories turnover period- The average inventory turnover duration is a

statistic which gauges an operational productivity by assessing how quickly stockpiles

can be converted into ultimate marketable item services. For every sector, the AITP that

is deemed standard may vary. This ratio is at 4.02, 5.08 and 4.96, 2.51 for B&M and

Morrison for 2020 and 2021 and thus it can be seen yet again that B&M is placed at a

good position as contrasted to the other (Dikau and Volz, 2020).

Debtors’ days- Consumers are frequently given a term of grace on purchases,

particularly when making large purchases. The duration it takes to collect overdue

accounts from every borrower, on the other hand, has a significant impact on the

company's total profitability. And the receivables outstanding turnover proportion shows

us just this. The volume of occasions a company recovers its average trade receivables

each year is known as trade receivables turnover ratio. The proportion is utilized to assess

an organization's capacity to effectively extend loans to consumers and recover cash from

clients on schedule. The concept of turnover in the trade receivables relies mostly on

borrowing transactions. Since monetary transactions don't really generate

trade receivables, the emphasis is solely on borrowing purchases. This ratio stands at

425.6, 709.85 and 889.5, 1005.6 for B&M and Morrison for 2020 and 2021 and thus it

can be said that B&M is performing well in the industry (Ehrlich and Guilbault, 2017).

Creditor’s days- The trade payable turnover proportion is a financial measure which

determines total credited acquisitions to average trade payable over a time to illustrate a

respectively so it can be said that B&M is still in a good position (Cumming and

Zambelli, 2017).

Return on capital employed- Returns on Capital Employed (ROCE) is a monetary

measure which measures a company's fiscal performance as well as the effectiveness of

its investment. Moreover, it states that this proportion is crucial since buyers evaluate it

while considering investing selections. Whenever that proportion is less than the

frequency where a company repays its debt, it may indicate bad productivity. This ratio

stands at 6.46, 17.41 and 7.24, 3.4 for B&M and Morrison for the year 2020 and 2021

respectively and thus it can be seen that B&M firm is placed at a good stance as

compared to other company..

Average inventories turnover period- The average inventory turnover duration is a

statistic which gauges an operational productivity by assessing how quickly stockpiles

can be converted into ultimate marketable item services. For every sector, the AITP that

is deemed standard may vary. This ratio is at 4.02, 5.08 and 4.96, 2.51 for B&M and

Morrison for 2020 and 2021 and thus it can be seen yet again that B&M is placed at a

good position as contrasted to the other (Dikau and Volz, 2020).

Debtors’ days- Consumers are frequently given a term of grace on purchases,

particularly when making large purchases. The duration it takes to collect overdue

accounts from every borrower, on the other hand, has a significant impact on the

company's total profitability. And the receivables outstanding turnover proportion shows

us just this. The volume of occasions a company recovers its average trade receivables

each year is known as trade receivables turnover ratio. The proportion is utilized to assess

an organization's capacity to effectively extend loans to consumers and recover cash from

clients on schedule. The concept of turnover in the trade receivables relies mostly on

borrowing transactions. Since monetary transactions don't really generate

trade receivables, the emphasis is solely on borrowing purchases. This ratio stands at

425.6, 709.85 and 889.5, 1005.6 for B&M and Morrison for 2020 and 2021 and thus it

can be said that B&M is performing well in the industry (Ehrlich and Guilbault, 2017).

Creditor’s days- The trade payable turnover proportion is a financial measure which

determines total credited acquisitions to average trade payable over a time to illustrate a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

firm's capacity to repay off its trade payable. To put it another way, the trade payment

turnover margin is the number of instances a firm could clear off its typical trade payable

amount each year. This proportion aids financiers in determining a business's viability by

determining how readily a firm could repay its present providers and subcontractors.

Businesses which could clear off suppliers on a constant schedule year round demonstrate

to creditors that they'll be capable of making periodic interests and original repayments.

This percentage is often used by suppliers while deciding whether or not to create an

independent term of debt or leasing proposal for a prospective client. This ratio stands at

45.92, 40.89 and 30.5, 25.6 for B&M and Morrison for 2020 and 2021 so it can be seen

that B&M is performing well in the sector (Gabor and Brooks, 2017).

Recommendation

It can be recommend from the above that B&M is performing satisfactory while Morrison

is doing not well at all in the market and thus it can be said that serious measures must be taken

by the firm to improve its stance so that it can add value to the firm in the long run.

Limitations of Financial Ratios

During the fiscal metrics examination, a multitude of flaws were discovered. Statistical data

is a constraint because the material utilized to calculate the proportions is based on previous

outcomes which have been provided by the company and cannot forecast upcoming events

(Gomber, Koch and Siering, 2017). Additional issue is that organisations may report financial

transactions that are the equivalent but in an unique manner owing to various accountancy

practises. For instance, one corporation may well have utilised straight-line amortization whereas

another might well have employed expedited amortization. Moreover, fiscal comparisons

research is dependent on fiscal account material supplied by the business, which may be

modified to represent higher than real profitability. As a consequence, the research could be

deceptive. Furthermore, several argue that 'understanding' is a major restriction of profitability

metrics, as determining the specific rationale for the proportion outcome can be difficult. For

instance, a corporation would possess a CR of 2:1 as a consequence of certain previous

initiatives that the corporation has undertaken in attempt to increase its working capital. This

implies that the CR number may only be transitory, as it may fall in the ahead. Other constraints

include the state of the economy, hyperinflation, and the firm's plan. They would not be

described in ability to remain under the character count.

turnover margin is the number of instances a firm could clear off its typical trade payable

amount each year. This proportion aids financiers in determining a business's viability by

determining how readily a firm could repay its present providers and subcontractors.

Businesses which could clear off suppliers on a constant schedule year round demonstrate

to creditors that they'll be capable of making periodic interests and original repayments.

This percentage is often used by suppliers while deciding whether or not to create an

independent term of debt or leasing proposal for a prospective client. This ratio stands at

45.92, 40.89 and 30.5, 25.6 for B&M and Morrison for 2020 and 2021 so it can be seen

that B&M is performing well in the sector (Gabor and Brooks, 2017).

Recommendation

It can be recommend from the above that B&M is performing satisfactory while Morrison

is doing not well at all in the market and thus it can be said that serious measures must be taken

by the firm to improve its stance so that it can add value to the firm in the long run.

Limitations of Financial Ratios

During the fiscal metrics examination, a multitude of flaws were discovered. Statistical data

is a constraint because the material utilized to calculate the proportions is based on previous

outcomes which have been provided by the company and cannot forecast upcoming events

(Gomber, Koch and Siering, 2017). Additional issue is that organisations may report financial

transactions that are the equivalent but in an unique manner owing to various accountancy

practises. For instance, one corporation may well have utilised straight-line amortization whereas

another might well have employed expedited amortization. Moreover, fiscal comparisons

research is dependent on fiscal account material supplied by the business, which may be

modified to represent higher than real profitability. As a consequence, the research could be

deceptive. Furthermore, several argue that 'understanding' is a major restriction of profitability

metrics, as determining the specific rationale for the proportion outcome can be difficult. For

instance, a corporation would possess a CR of 2:1 as a consequence of certain previous

initiatives that the corporation has undertaken in attempt to increase its working capital. This

implies that the CR number may only be transitory, as it may fall in the ahead. Other constraints

include the state of the economy, hyperinflation, and the firm's plan. They would not be

described in ability to remain under the character count.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Portfolio 2

Capital investment Appraisal Techniques

According to the discounted cash flow method, corporate leadership must choose Project A

since it has a larger net present value (NPV) than Project B. (without considering taxation on

depreciation)

Instead, if we estimate a 50% rate of taxation, the NPV could be determined by subtracting

the amortization savings from the total tax savings.

Net Present Value of project can be calculated as =Initial Investment-Discounted present

value of Cash inflow@16%-Discounted present value of depreciation.

Net Present Value of project A

=£78000-£35000*0.862+£36,000*0.743+£38,000*0.641+£29,000*0.552+£28,000*0.476+

£22,000*0.410=-£41632

Present value discount factor= Cost of capital@16%

Depreciation= £78000/6=£13000 per year

Present value Annuity factor for 6 y..r@16%=3.685

Present value of depreciation for 6 years =£13000*3.685(PVAIF)=£47905

Because the tax percentage is not specified in the query, this one has been omitted as a source of

amortization savings.

Net Present Value of project A

=£78000-£12000*0.862+£16,000*0.743+£21,000*0.641+£35,000*0.552+£46,000*0.476+

£48,000*0.410+£10000*0.410=£-22689

Present value discount factor= Cost of capital@16%

Depreciation= £78000-£10000/6=£76333.33 per year

Present value Annuity factor for 6 y..r@16%=3.685

Present value of depreciation for 6 years =£76333.33*3.685(PVAIF)=£ 281288.32

According to the discounted cash flow method, upper leadership must choose Project A

since it has a larger net present value (NPV) than Project B. (without considering taxation on

depreciation)

However, if we estimate a rate of tax of 50%, the NPV could be computed by factoring in

amortization savings as a tax savings.

Capital investment Appraisal Techniques

According to the discounted cash flow method, corporate leadership must choose Project A

since it has a larger net present value (NPV) than Project B. (without considering taxation on

depreciation)

Instead, if we estimate a 50% rate of taxation, the NPV could be determined by subtracting

the amortization savings from the total tax savings.

Net Present Value of project can be calculated as =Initial Investment-Discounted present

value of Cash inflow@16%-Discounted present value of depreciation.

Net Present Value of project A

=£78000-£35000*0.862+£36,000*0.743+£38,000*0.641+£29,000*0.552+£28,000*0.476+

£22,000*0.410=-£41632

Present value discount factor= Cost of capital@16%

Depreciation= £78000/6=£13000 per year

Present value Annuity factor for 6 y..r@16%=3.685

Present value of depreciation for 6 years =£13000*3.685(PVAIF)=£47905

Because the tax percentage is not specified in the query, this one has been omitted as a source of

amortization savings.

Net Present Value of project A

=£78000-£12000*0.862+£16,000*0.743+£21,000*0.641+£35,000*0.552+£46,000*0.476+

£48,000*0.410+£10000*0.410=£-22689

Present value discount factor= Cost of capital@16%

Depreciation= £78000-£10000/6=£76333.33 per year

Present value Annuity factor for 6 y..r@16%=3.685

Present value of depreciation for 6 years =£76333.33*3.685(PVAIF)=£ 281288.32

According to the discounted cash flow method, upper leadership must choose Project A

since it has a larger net present value (NPV) than Project B. (without considering taxation on

depreciation)

However, if we estimate a rate of tax of 50%, the NPV could be computed by factoring in

amortization savings as a tax savings.

Limitation of Investment appraisal techniques

High-tech initiatives since the advantages connected with elevated initiatives might well

be optimised in the big scheme of things; this may be hard to assess advantages in the

forthcoming years, causing complexity in decision-making in the big scheme of things

(Kassim and Manap, 2017).

Cost of investment assessment is problematic even though there are various other hazards

that are not reflected in return on equipment for discounted reasons, such as financial

contagion, systemic threat, and hyperinflation hazards. As a result, in long-term decision-

making, accurate prediction is not attainable to the degree that it is required for outcome.

Additional limitations of capital assessment methodologies include the failure to include

potential expenses in outcome and disproportionate short-term expenditure, among

others.

Working Capital after Tax Disparity whenever there is a difference between the working

capital after taxation in the first season and the working capital after taxation in the

second season, a venture with a high beginning CFAT relative to the second year would

produce contradicting outcomes for long-term planning process.

Investing evaluation approaches do not even have a capital maximisation goal in the

sense that they do not reflect the temporal worth of currency in diverse situations while

generating decisions.

Similar repayment duration if 2 activities possess the similar return duration, it will be

hard to identify them for judgement call purposes.

The selection of group's cut-off repayment time is discretionary in character and

contributes to competing outcome (Mian and Sufi, 2018).

Early Expenditure Disparity it would've been hard to ascertain 2 necessarily incompatible

initiatives in long-term choice selection if the program sizes were dissimilar in level of

finance invested.

Where there has been a variation in program lifespan or discrepancy in program lifetime,

in long-term planning process, contradicting results might well be reached.

Outlet trend whenever a money runoff sequence happens at various times, asset

assessment procedures are ineffective in establishing long-term decisions.

High-tech initiatives since the advantages connected with elevated initiatives might well

be optimised in the big scheme of things; this may be hard to assess advantages in the

forthcoming years, causing complexity in decision-making in the big scheme of things

(Kassim and Manap, 2017).

Cost of investment assessment is problematic even though there are various other hazards

that are not reflected in return on equipment for discounted reasons, such as financial

contagion, systemic threat, and hyperinflation hazards. As a result, in long-term decision-

making, accurate prediction is not attainable to the degree that it is required for outcome.

Additional limitations of capital assessment methodologies include the failure to include

potential expenses in outcome and disproportionate short-term expenditure, among

others.

Working Capital after Tax Disparity whenever there is a difference between the working

capital after taxation in the first season and the working capital after taxation in the

second season, a venture with a high beginning CFAT relative to the second year would

produce contradicting outcomes for long-term planning process.

Investing evaluation approaches do not even have a capital maximisation goal in the

sense that they do not reflect the temporal worth of currency in diverse situations while

generating decisions.

Similar repayment duration if 2 activities possess the similar return duration, it will be

hard to identify them for judgement call purposes.

The selection of group's cut-off repayment time is discretionary in character and

contributes to competing outcome (Mian and Sufi, 2018).

Early Expenditure Disparity it would've been hard to ascertain 2 necessarily incompatible

initiatives in long-term choice selection if the program sizes were dissimilar in level of

finance invested.

Where there has been a variation in program lifespan or discrepancy in program lifetime,

in long-term planning process, contradicting results might well be reached.

Outlet trend whenever a money runoff sequence happens at various times, asset

assessment procedures are ineffective in establishing long-term decisions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.