Managerial Finance Report: Ratio Analysis and Capital Budgeting

VerifiedAdded on 2022/12/30

FINANCE

Paraphrase This Document

INTRODUCTION...........................................................................................................................3

PORTFOLIO 1.................................................................................................................................3

A Calculation related with financial ratio...................................................................................3

B. Explanation of assessment of financial performance of Tesco & Sainsbury.........................5

C Explanation of main cause of poor performance of organization...........................................8

D. Limitation of financial ratio technique for measures performance of organization...............8

PORTFOLIO 2.................................................................................................................................9

A. Use of various types of investment appraisal technique for investment decision..................9

B. Limitation of capital budgeting techniques..........................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................12

.......................................................................................................................................................12

Managerial finance is define as essential branch of finance which help in create value of

organizations performance and its agility. To understand this concept this report has been

formulate. It divided into two parts. The first part is related with the relevance of ratio analysis as

essential tool of managerial finance. This define how manager use ratio to measure or compare

performance of Tesco & Sainsbury. It also define he limitations of this tool. In another portfolio

the relevance of managerial finance technique for determine or take decision has been mention

specifically. This report define how technique of capital budgeting calculated and their use for

take decision and limitation of theses techniques. All these information are define in systematic

manner.

PORTFOLIO 1

A Calculation related with financial ratio.

Ratio: In practical life the term ratio , define as tool which use for measure or define

quantitative relation between 2 elements. By using ratio person can evaluate the number of times

one item contains another in particular statement. Generally business organizations use ratio for

measure financial performance of their business transactions or activities within given time

period. This will help in determine impact of organizations activities on performance and earning

gain for the organization.

Tesco & Saisbury are run their business in supermarket sector, both are considers

multinational organization which contribute toward economy of UK. Theses entities use ratio

tool for measure financial performance .The main reason of use this tool to compare the

performance of each other by identifying performance in quantitative terms.

Following are calculation of some ratio through which manager can easily recognize and

compare performance of rival companies (Ahuja and Kalra, 2020).

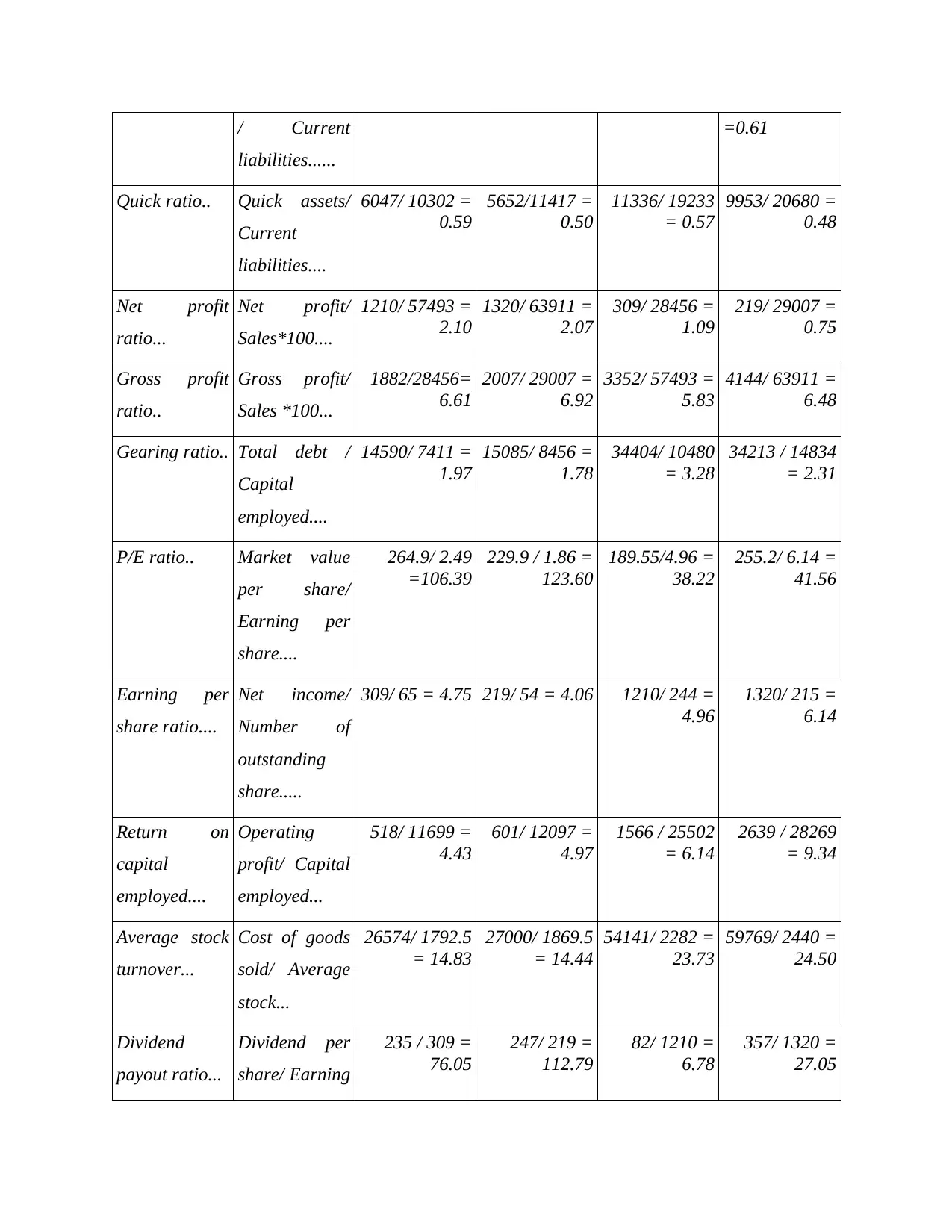

Particular Formula Sainsbury

2018 2019

Tesco

2018 2019

Current ratio.. Current assets 7857/ 10302 =

0.76

7581 / 11417

= 0.66

13600/ 19233

=0.71

12570/20980

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

liabilities......

=0.61

Quick ratio.. Quick assets/

Current

liabilities....

6047/ 10302 =

0.59

5652/11417 =

0.50

11336/ 19233

= 0.57

9953/ 20680 =

0.48

Net profit

ratio...

Net profit/

Sales*100....

1210/ 57493 =

2.10

1320/ 63911 =

2.07

309/ 28456 =

1.09

219/ 29007 =

0.75

Gross profit

ratio..

Gross profit/

Sales *100...

1882/28456=

6.61

2007/ 29007 =

6.92

3352/ 57493 =

5.83

4144/ 63911 =

6.48

Gearing ratio.. Total debt /

Capital

employed....

14590/ 7411 =

1.97

15085/ 8456 =

1.78

34404/ 10480

= 3.28

34213 / 14834

= 2.31

P/E ratio.. Market value

per share/

Earning per

share....

264.9/ 2.49

=106.39

229.9 / 1.86 =

123.60

189.55/4.96 =

38.22

255.2/ 6.14 =

41.56

Earning per

share ratio....

Net income/

Number of

outstanding

share.....

309/ 65 = 4.75 219/ 54 = 4.06 1210/ 244 =

4.96

1320/ 215 =

6.14

Return on

capital

employed....

Operating

profit/ Capital

employed...

518/ 11699 =

4.43

601/ 12097 =

4.97

1566 / 25502

= 6.14

2639 / 28269

= 9.34

Average stock

turnover...

Cost of goods

sold/ Average

stock...

26574/ 1792.5

= 14.83

27000/ 1869.5

= 14.44

54141/ 2282 =

23.73

59769/ 2440 =

24.50

Dividend

payout ratio...

Dividend per

share/ Earning

235 / 309 =

76.05

247/ 219 =

112.79

82/ 1210 =

6.78

357/ 1320 =

27.05

Paraphrase This Document

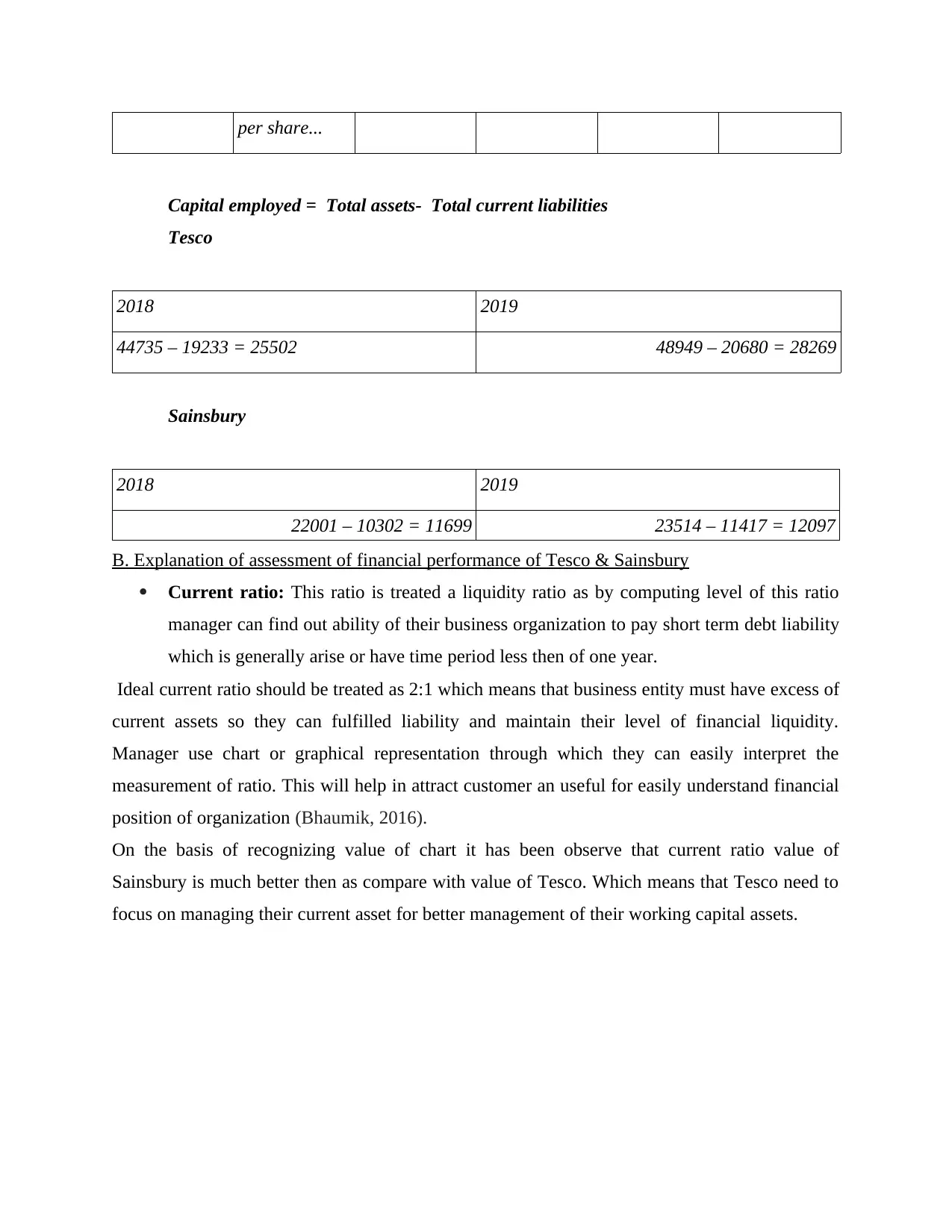

Capital employed = Total assets- Total current liabilities

Tesco

2018 2019

44735 – 19233 = 25502 48949 – 20680 = 28269

Sainsbury

2018 2019

22001 – 10302 = 11699 23514 – 11417 = 12097

B. Explanation of assessment of financial performance of Tesco & Sainsbury

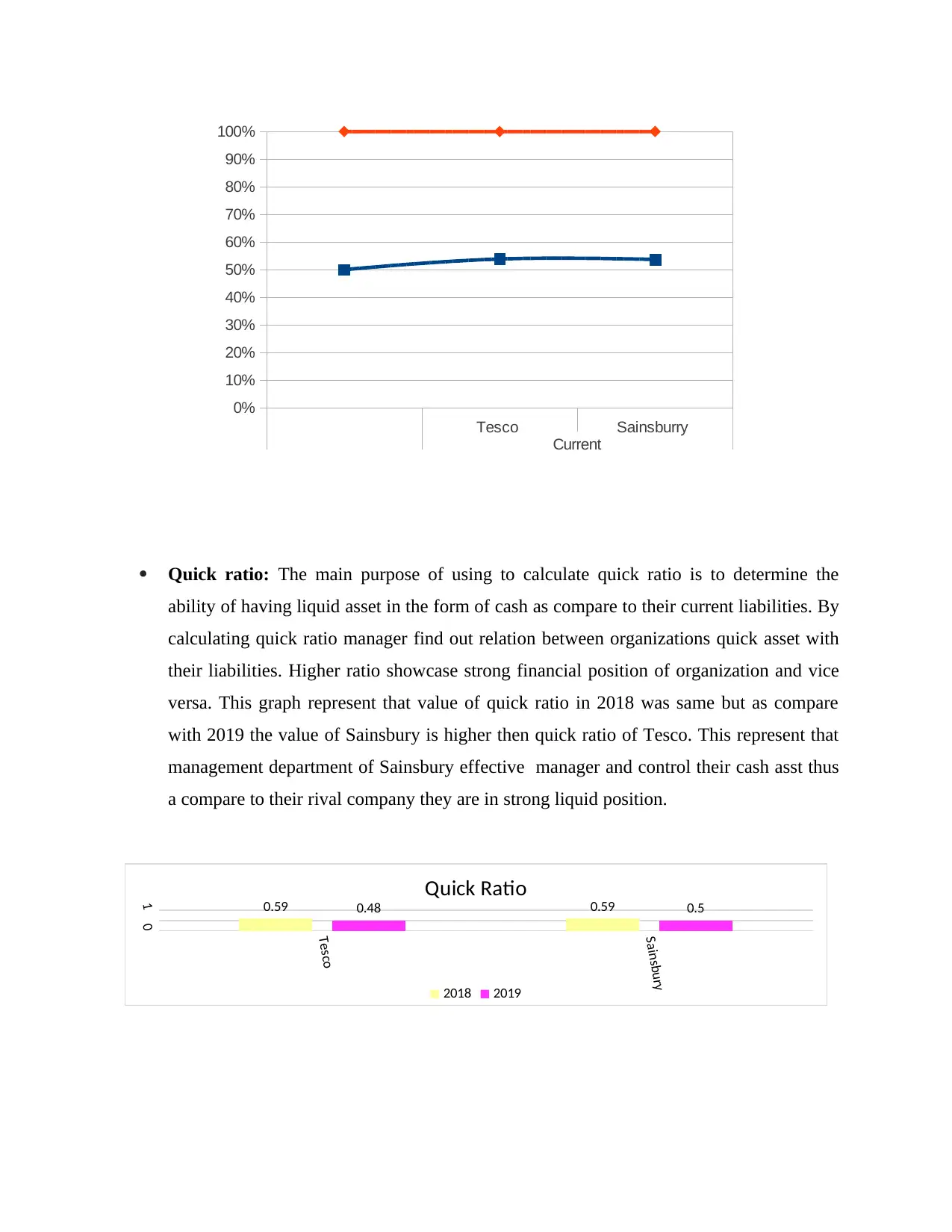

Current ratio: This ratio is treated a liquidity ratio as by computing level of this ratio

manager can find out ability of their business organization to pay short term debt liability

which is generally arise or have time period less then of one year.

Ideal current ratio should be treated as 2:1 which means that business entity must have excess of

current assets so they can fulfilled liability and maintain their level of financial liquidity.

Manager use chart or graphical representation through which they can easily interpret the

measurement of ratio. This will help in attract customer an useful for easily understand financial

position of organization (Bhaumik, 2016).

On the basis of recognizing value of chart it has been observe that current ratio value of

Sainsbury is much better then as compare with value of Tesco. Which means that Tesco need to

focus on managing their current asset for better management of their working capital assets.

ability of having liquid asset in the form of cash as compare to their current liabilities. By

calculating quick ratio manager find out relation between organizations quick asset with

their liabilities. Higher ratio showcase strong financial position of organization and vice

versa. This graph represent that value of quick ratio in 2018 was same but as compare

with 2019 the value of Sainsbury is higher then quick ratio of Tesco. This represent that

management department of Sainsbury effective manager and control their cash asst thus

a compare to their rival company they are in strong liquid position.

Tesco Sainsburry

Current

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Tesco

Sainsbury

01 0.59 0.590.48 0.5

Quick Ratio

2018 2019

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

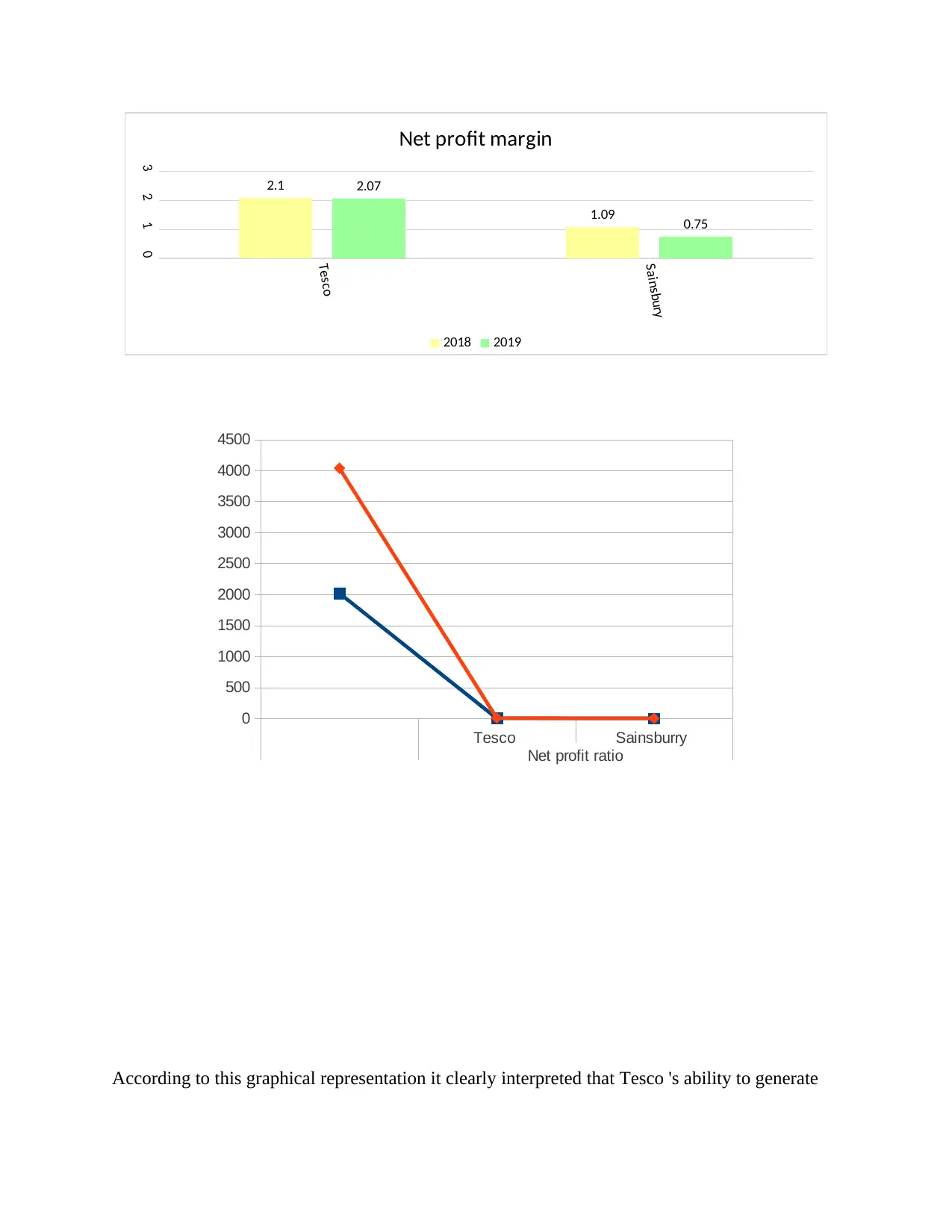

sales. The main purpose of this ratio is to determine ability of organization to generate

profit or revenue by selling their products. To understand the potion of net profit ratio

manager need to use graphs through which the can easily determine value ((Bu, 2020).

Tesco Sainsburry

Liquid

0

500

1000

1500

2000

2500

3000

3500

4000

4500

Paraphrase This Document

Tesco

Sainsbury

0123

2.1

1.09

2.07

0.75

Net profit margin

2018 2019

Tesco Sainsburry

Net profit ratio

0

500

1000

1500

2000

2500

3000

3500

4000

4500

ratio was 2.1 and in 2019 it was determine at 2.07 on the other side Sainsbur only generate 1.09

in 2018 and its profit value decliner 0.75.Which means that Tesco able to attain more profit as

compare to Sainsubry.

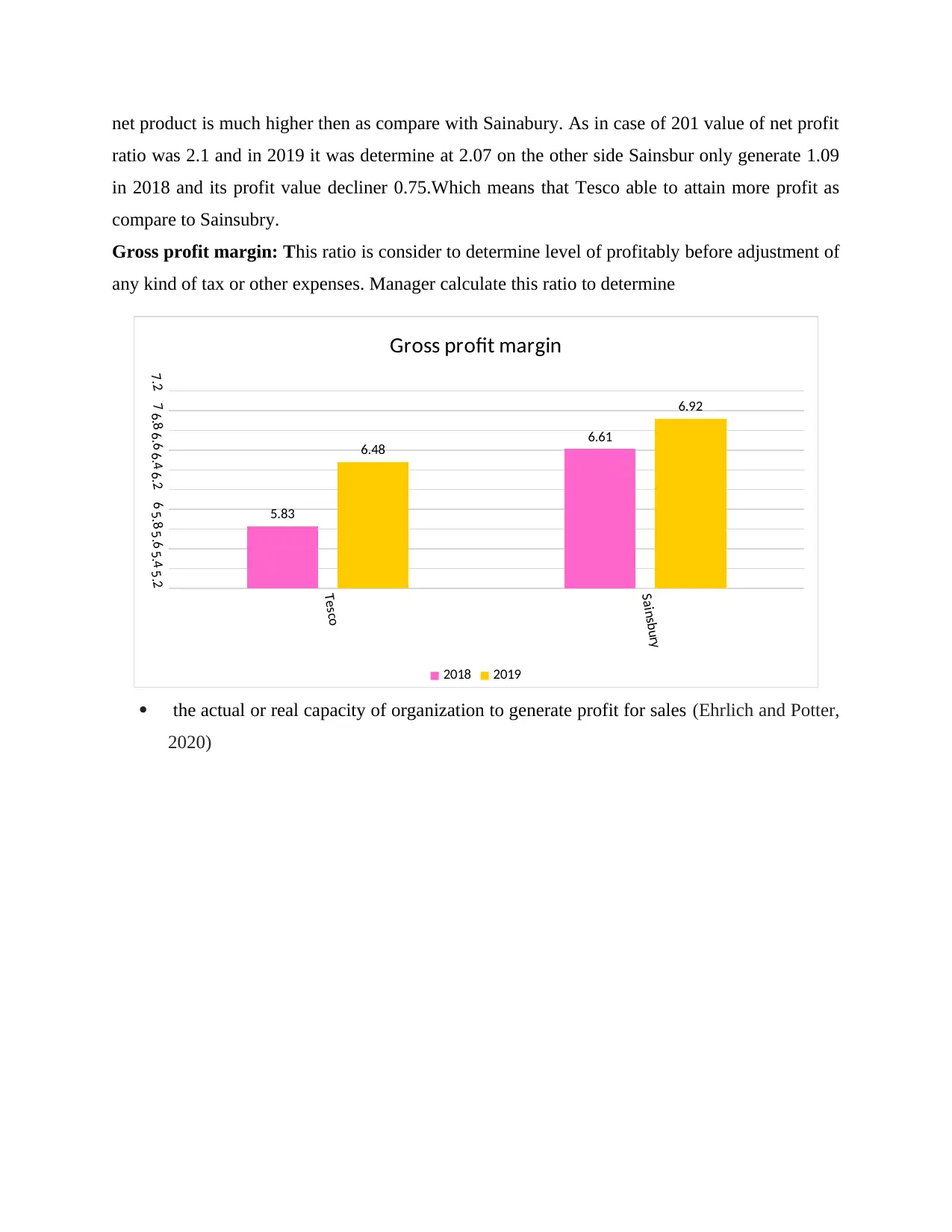

Gross profit margin: This ratio is consider to determine level of profitably before adjustment of

any kind of tax or other expenses. Manager calculate this ratio to determine

the actual or real capacity of organization to generate profit for sales (Ehrlich and Potter,

2020)

Tesco

Sainsbury

5.25.45.65.866.26.46.66.877.2

5.83

6.61

6.48

6.92

Gross profit margin

2018 2019

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

value of Sainsbury is higher . This means that the revenue rate of Sainsbury is better then Tesco

but due to their selling expenses it is not able to generate more profit as compare to their rival

industries.

Gearing ratio:The main purpose of determining this ratio is to identify value of financial

leverage by calculating or measuring value of equity and business liabilities. The main

purpose of determining this ratio to evaluate that business corporation must have

sufficient external source which will help in measuring or providing tax benefits. To

evaluate gearing ratio of Tesco and Sainsbury chart has been formulated.

Tesco Sainsburry

Gross profit ratio

0

500

1000

1500

2000

2500

3000

3500

4000

4500

Paraphrase This Document

Sainsbury

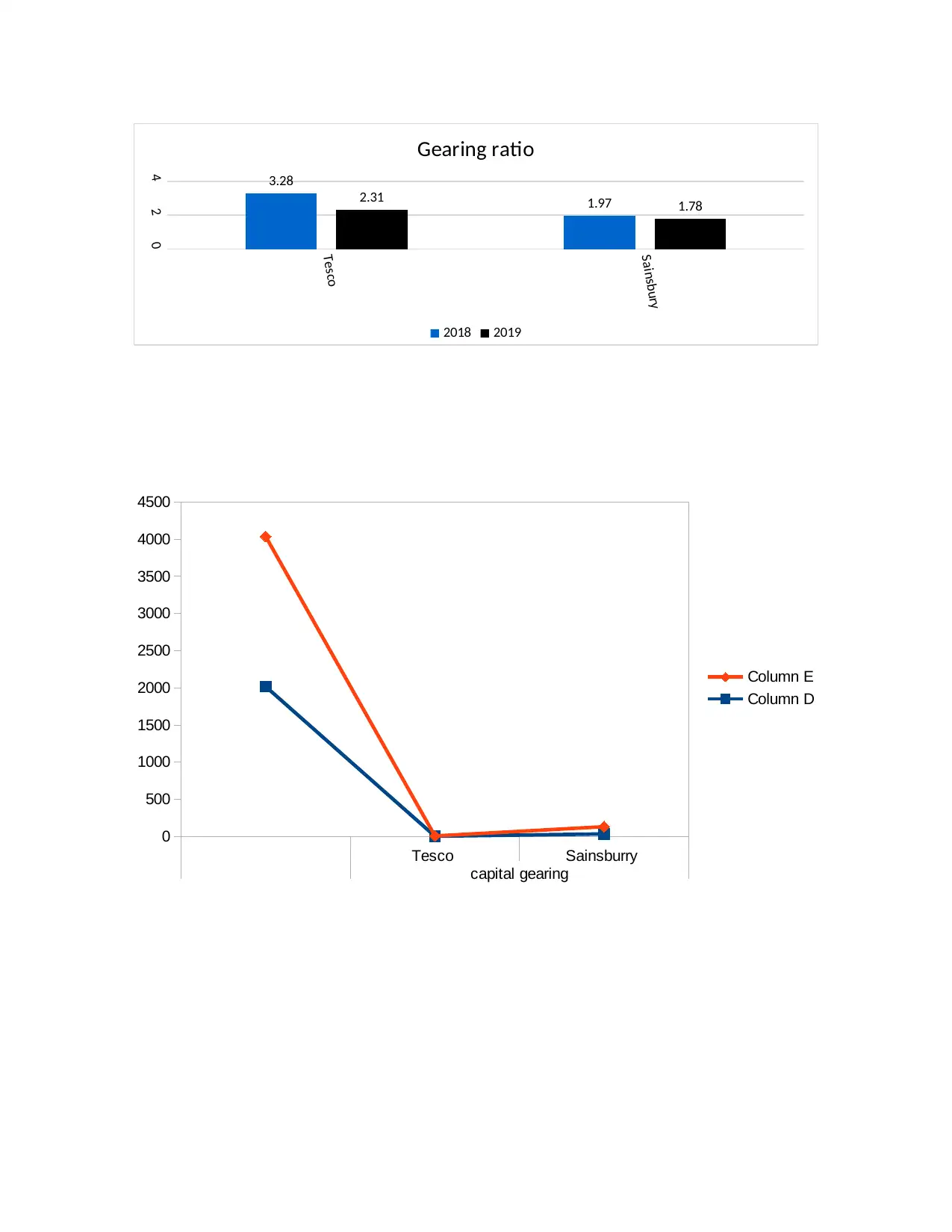

024 3.28

1.972.31 1.78

Gearing ratio

2018 2019

Tesco Sainsburry

capital gearing

0

500

1000

1500

2000

2500

3000

3500

4000

4500

Column E

Column D

which means that this organization use or formulate strategies which help in managing their

extent funds in effective way as compare with Sainsbury.

Price earnings ratio: This ratio is calculated by only listed organization. The main

purpose of calculating this ratio is to determine whether organization is under or

overvalued as per the norms of accounting standard. They on the basis of calculating

price earning ratio organization able to found the rate of revenue investor gain upon each

share. Higher ratio of price earning showcase high exception of investors regarding with

earnings (Jaisinghani, Kaur and Inamdar, 2019).

On the basis of calculating value from chart it define hat Sainsbury market price and value of

earnings much better then Tesco.

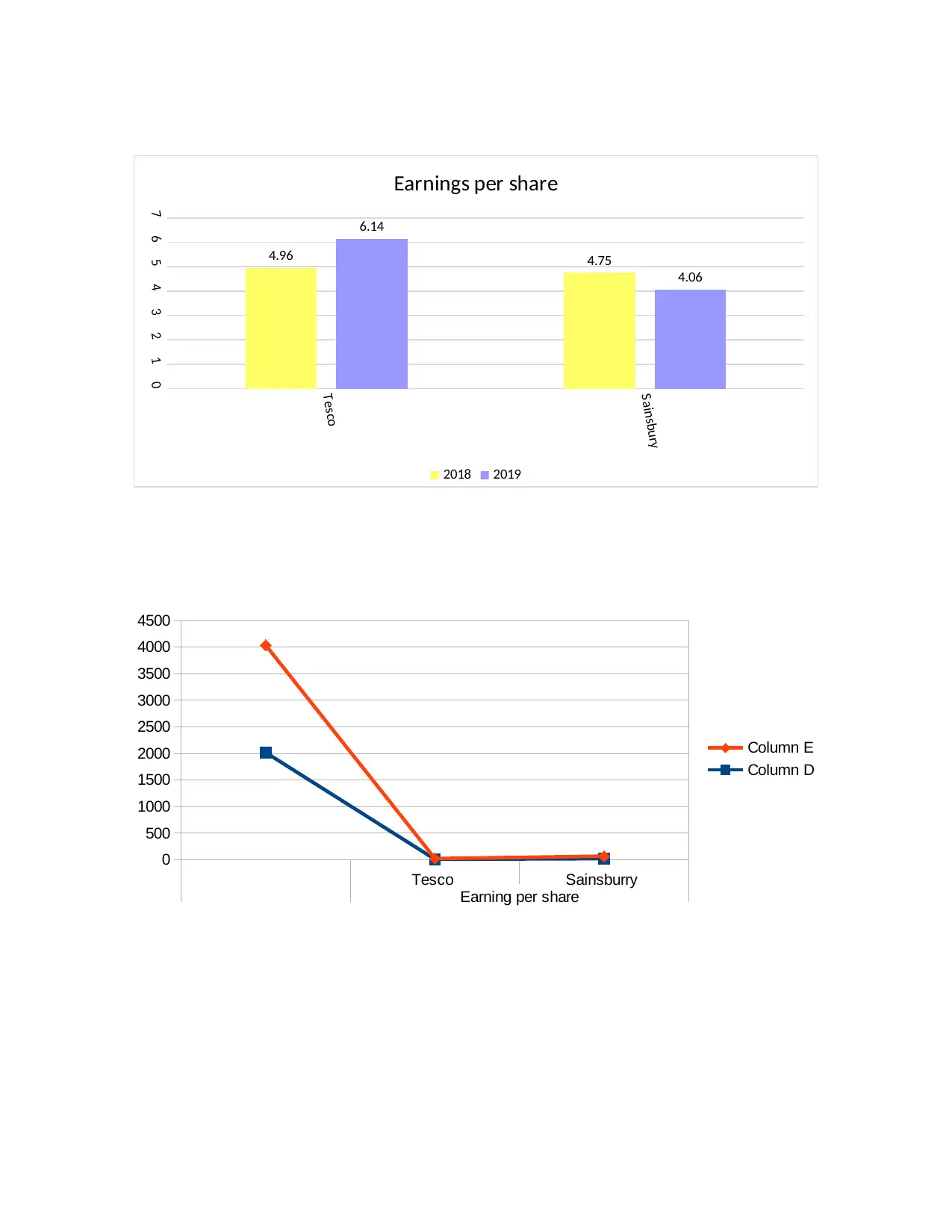

Earnings per share: This ratio is also part of profitability ratio. It is calculated by

recognize profit with number of shares organization have. On the basis of that manager

measure the rate of profit of organization. For measure the comparison between theses

two companies chart has been formulated (Kwon, 2018).

Tesco

Sainsbury

050100150

38.22

106.39

41.56

123.6

Price earnings ratio

2018 2019

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sainsbury

01234567

4.96 4.75

6.14

4.06

Earnings per share

2018 2019

Tesco Sainsburry

Earning per share

0

500

1000

1500

2000

2500

3000

3500

4000

4500

Column E

Column D

Paraphrase This Document

per share price is much better then its rival industry.

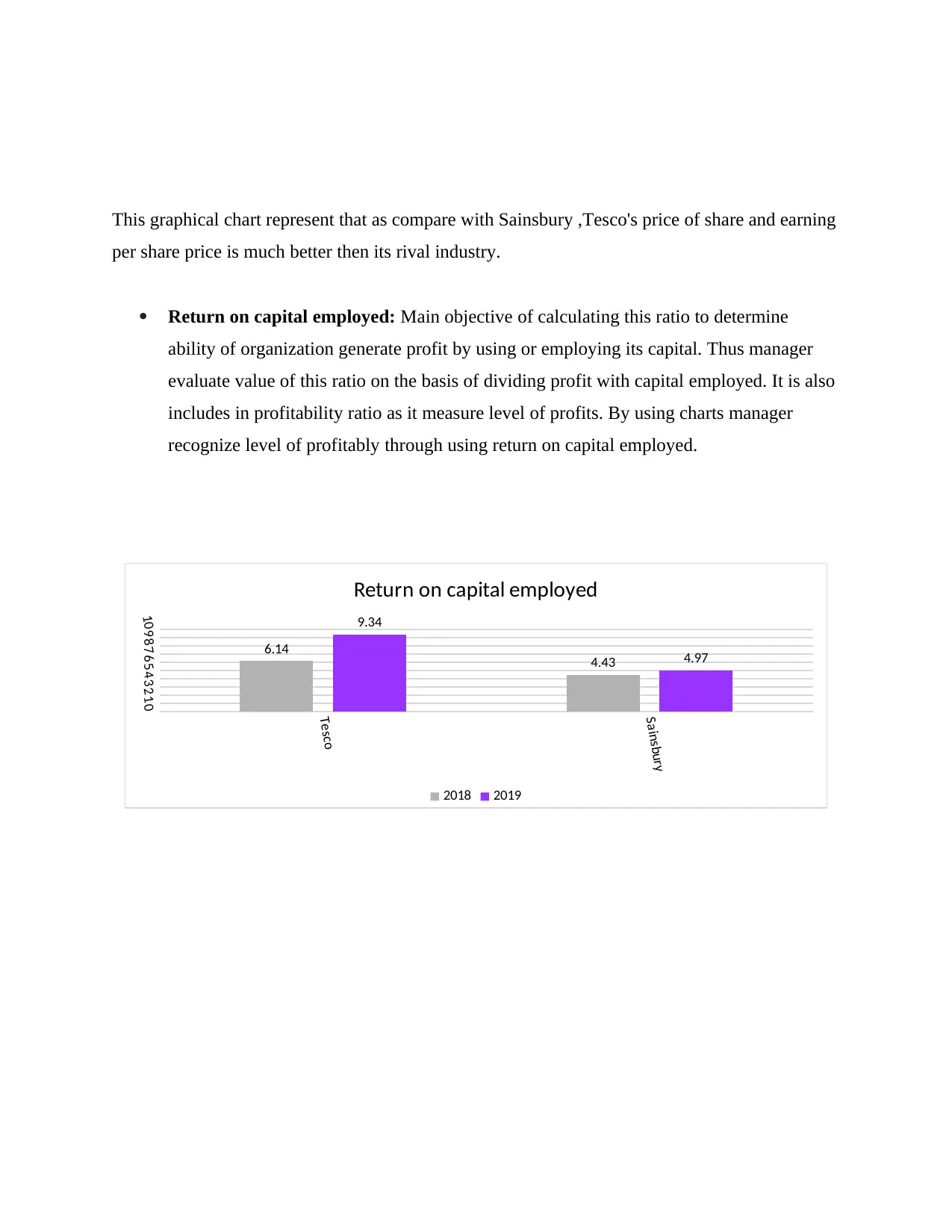

Return on capital employed: Main objective of calculating this ratio to determine

ability of organization generate profit by using or employing its capital. Thus manager

evaluate value of this ratio on the basis of dividing profit with capital employed. It is also

includes in profitability ratio as it measure level of profits. By using charts manager

recognize level of profitably through using return on capital employed.

Tesco

Sainsbury

012345678910

6.14 4.43

9.34

4.97

Return on capital employed

2018 2019

manage their asset and capital in effective manner as compare to its rival company.

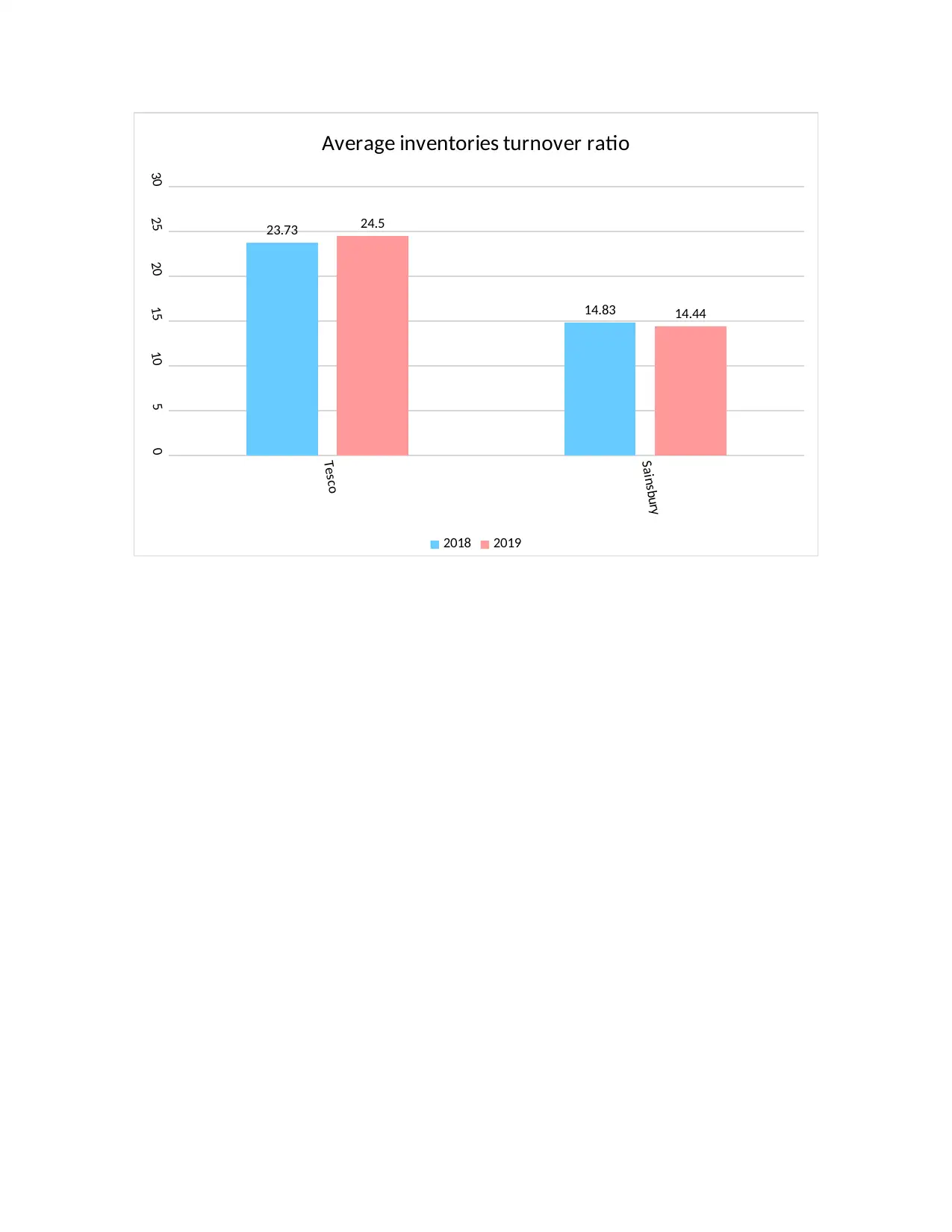

Stock turnover ratio: This ratio is used to evaluate the rate at which stock has been

replace and sell within the market . Higher stock turnover ratio showcase long time

require to compete the operating cycle for goods. This ratio is define by measuring

performance of two organizations. It is showcase efficiency level of organization fr

particular time period (Meng and Wang, 2019).

Tesco Sainsburry

returm on capital

0

500

1000

1500

2000

2500

3000

3500

4000

4500

Column E

Column D

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sainsbury

0

5

10

15

20

25

30

23.73

14.83

24.5

14.44

Average inventories turnover ratio

2018 2019

Paraphrase This Document

material and run the operating cycle and as compare with this Tesco took more time for running

or compete their stock turnover cycle. This means that management department of Sainsbury

effective formulate ad control their stock management strategy.

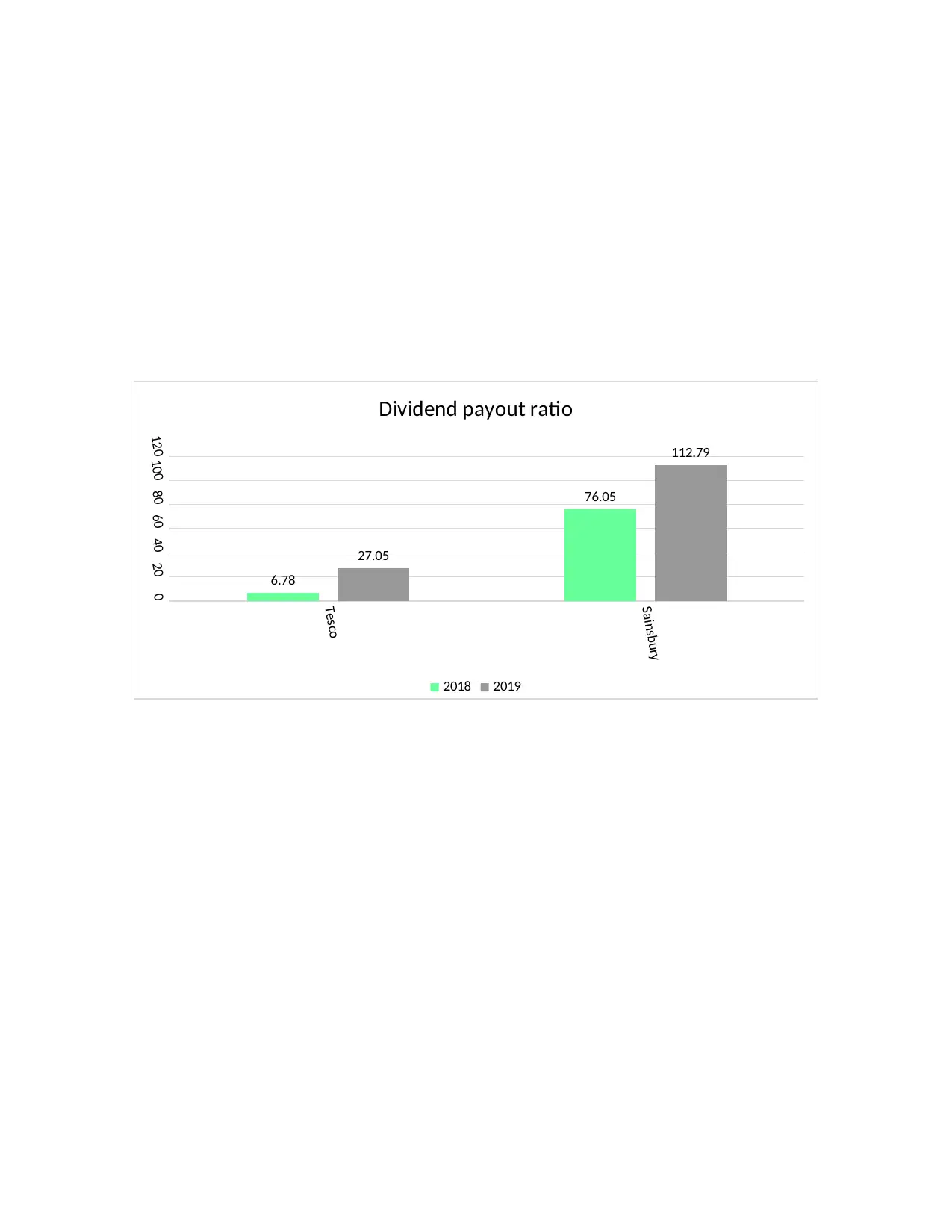

Dividend pay-out ratio: By calculating dividend pay out ratio customers able to find out

value of dividend or rate which organization pay to their relevant shareholder. Higher dividend

pay out ratio show case positive relation between profit and dividend which means that

organization offer high rate of dividend. By formulating chart

Tesco Sainsburry

inventory

0

500

1000

1500

2000

2500

3000

3500

4000

4500

Column E

Column D

Sainsbury

020406080100120

6.78

76.05

27.05

112.79

Dividend payout ratio

2018 2019

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

as compare to this Tesco only distribute 40 percentage of their dividend to shareholder. Which

mean that price of dividend of Sainsbury is much better, which represent that shareholder must

ned to invest in this organization as compare to Tesco (Musumeci and O’Brien, 2019).

C Explanation of main cause of poor performance of organization.

On the basis of analysing performance of each company, it recognized that even though

the value of ratio of both organization has been increase their performance has been enhance as

compare to 2018 but in case of comparison the performance of Sainsbury is far better then

Tesco.

Even though the net profit, earning per share ratio has been higher of Tesco then

Sainsbury however due to using effective stock management technique and offering higher rate

Tesco Sainsburry

dividend

0

500

1000

1500

2000

2500

3000

3500

4000

4500

Column E

Column D

Paraphrase This Document

then Tesco.

The main reason of decrement in the performance of Tesco is that their management

department is not formulator stock control management strategies, their value of cash assets is

also comparatively low. Which means that the not able to collect funds from debtors and

manage their financial funds.

Tesco due to investing in new market segment not able to generate much profit a

compare to its rival industries (Nikbakht, Shahrokhi and Corriette, 2019).

Their management department also not utilized resource and formulate budget or wok in

ethical ,systemic manner thus they are not available of beat their rivals company.

D. Limitation of financial ratio technique for measures performance of organization.

Business organization use ratio for measuring and compare their financial performance

with other companies. This may consider as appropriate tool of measurement of financial

management however there will be some of limitation of this technique which mention below

The result generate or calculate ratio are not accurate or reliable as organization belongs

from different countries use different accounting practices.

Ratio also nor define measurement of financial performance in qualitative terms.

Seasonal variation impact on the result of this ratio.

Financial ratio does not consider changes in price value. It neglect many of essential

factors.

PORTFOLIO 2

A. Use of various types of investment appraisal technique for investment decision.

Investment appraisal technique: Theses are part of financial management which

business organization use to evaluate or recognize value or performance of each alternative. On

the basis of that manager took decision which alternative provides them more benefits or which

is beneficial for attaining economic profits. Thee will be many techniques through which

manager recognize the time period and rate of profits. Following are some of them are define

below

Pay back period: This period has been calculated to identified the time required for an

alternative to cover up all the initial cost which manager use to invest during the time of project

up their cost (Panda and Kumar, 2020).

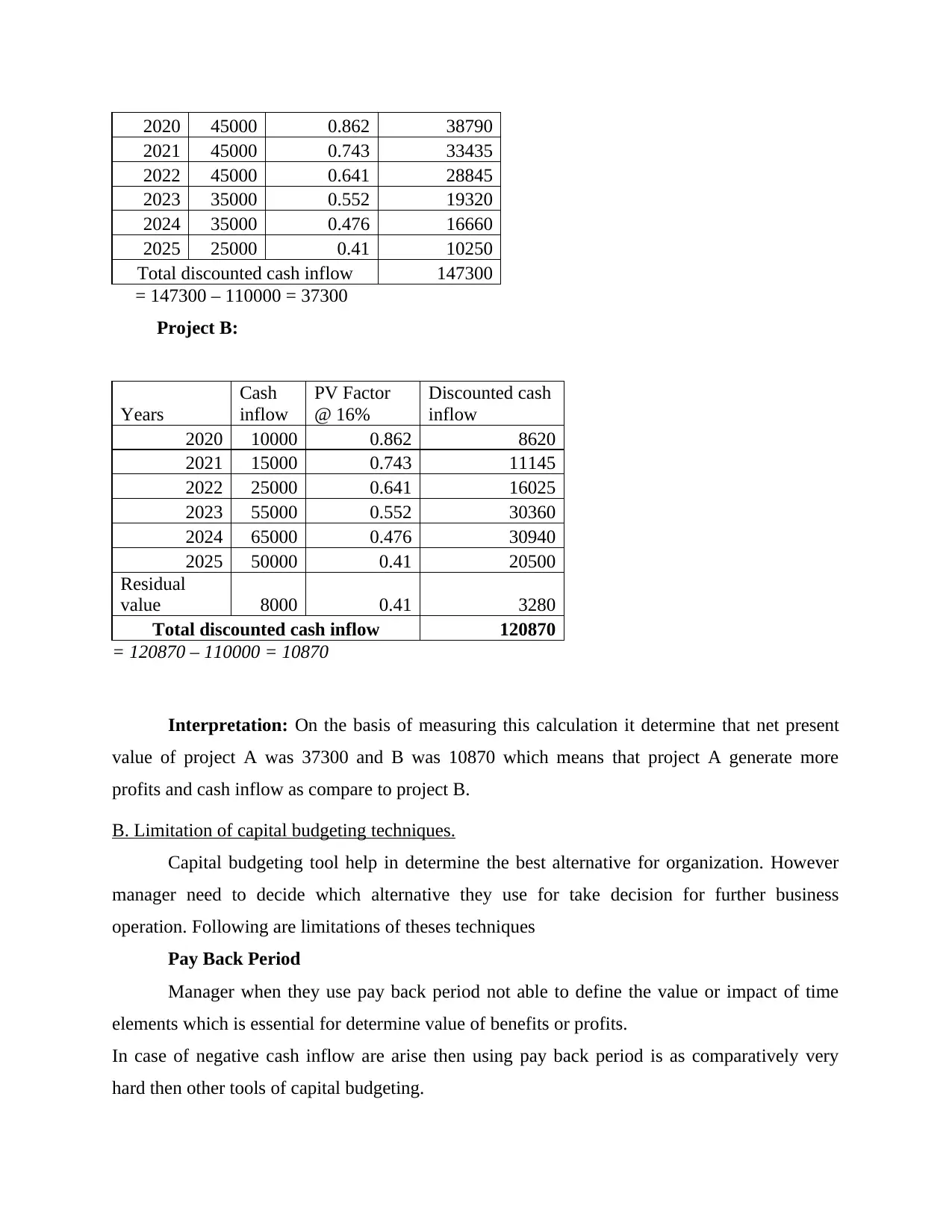

Calculation of pay back period for project A

Formula: Completed years + (Cost of project - Cumulative cash inflow in the completed year) /

cash inflow of next year

Year

Cash

inflow

Cumulative

cash inflow

2020 45000 45000

2021 45000 90000

2022 45000 135000

2023 35000 170000

2024 35000 205000

2025 25000 230000

= 2 + (110000 – 90000 / 45000 = 2.44 years

Project B

Years

Cash

inflow

Cumulative

cash inflow

2020 10000 10000

2021 15000 25000

2022 25000 50000

2023 55000 105000

2024 65000 170000

2025 50000 220000

= 4 + (110000 – 105000) / 65000 = 4.08 years

Interpretation: On their basis of calculating value of pay back period it has been

considers that as compare to project B , project A is much beneficial for organization. As it just

took only 2. 44 years to cover up initial cost when manager choose project A over project B.

Ne present value: This tool is also part of investment appraisal method. Manager on the

basis of calculating net present value can determine which project gives them higher rate of

return and more beneficial for company (Waemustafa, 2018).

Project A:

Years

Cash

inflow

PV Factor

@ 16%

Discounted

cash inflow

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2021 45000 0.743 33435

2022 45000 0.641 28845

2023 35000 0.552 19320

2024 35000 0.476 16660

2025 25000 0.41 10250

Total discounted cash inflow 147300

= 147300 – 110000 = 37300

Project B:

Years

Cash

inflow

PV Factor

@ 16%

Discounted cash

inflow

2020 10000 0.862 8620

2021 15000 0.743 11145

2022 25000 0.641 16025

2023 55000 0.552 30360

2024 65000 0.476 30940

2025 50000 0.41 20500

Residual

value 8000 0.41 3280

Total discounted cash inflow 120870

= 120870 – 110000 = 10870

Interpretation: On the basis of measuring this calculation it determine that net present

value of project A was 37300 and B was 10870 which means that project A generate more

profits and cash inflow as compare to project B.

B. Limitation of capital budgeting techniques.

Capital budgeting tool help in determine the best alternative for organization. However

manager need to decide which alternative they use for take decision for further business

operation. Following are limitations of theses techniques

Pay Back Period

Manager when they use pay back period not able to define the value or impact of time

elements which is essential for determine value of benefits or profits.

In case of negative cash inflow are arise then using pay back period is as comparatively very

hard then other tools of capital budgeting.

Paraphrase This Document

it is not include essential elements which directly impact on the profitability level of

organization.

Limitations of net present value

Net present value may consider time factor but when manager use this technique for

calculating their value of alternative they not define or represent clear image of investment

elements. Manager not able to identify wherever organization attain profit or loss.

By using net present value to find out best alternative , organization need to hire person who

have knowledge regarding he field of account and they also have degree . This is time

consuming and complex procedure (Young and Wu, 2017).

The rate of arriving accuracy result of this method is depend on the finance manager as they use

this tool for measuring performance.

Net present value is not able to determine or find the value and worth of shareholder. Thus it is

not consider as accurate formulate or statement of using capital decision.

The biggest limitation of using net present value is that it does not use or evaluate sunk

cost during the time of calculate value of cash inflow thus the rate of accurate results compare to

other alternative.

This method also not use proper cash inflow thus it s not relevant for using or take decision

regarding business operations and future projects.

CONCLUSION

From the above analysis it has been concluded that organizations need to use tools of

financial management through which they can mage their financial assets. by using ratio analysis

they can easily evaluate and measure Fianna performance for specific time period. On the basis

of that manager formulate policies to overcome their limitation by comparing it with other

organization's financial statements. They also use net present value or pay back period or other

tools of capital budgeting through which they can easily evaluate rate of cash inflow and on the

basis of tat they find out which alternative given them high rate of economic benefits.

Managerial finance in took decision by managing all the asset special financial in effective and

systematic way by controlling wastage use of theses resource.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Books and journals

Ahuja, B. R. and Kalra, R., 2020. Impact of macroeconomic variables on corporate capital

structure: a case of India. Managerial Finance.

Bhaumik, P. K., 2016. An appropriate risk addendum for risky projects. Managerial Finance.

Bu, Q., 2020. Mutual Fund Alpha: Is It Managerial or Emotional?. Journal of Behavioral

Finance, pp.1-10.

Ehrlich, J. A. and Potter, J. M., 2020. Is offense worth more than defense and pitching? Marginal

revenue product and revenue sharing in major league baseball. Managerial Finance.

Jaisinghani, D., Kaur, M. and Inamdar, M. M., 2019. Analyzing seasonal anomalies for Israel:

evidence from pre-and post-global financial crisis. Managerial Finance.

Kwon, G. J., 2018. Comparative value relevance of accounting information among Asian

countries. Managerial Finance.

Meng, Y. and Wang, X., 2019. Do institutional investors have homogeneous influence on

corporate social responsibility? Evidence from investor investment horizon. Managerial

Finance.

Musumeci, J. and O’Brien, T., 2019. Lease vs buy: clarifying the impact of tax and borrowing

rates. Managerial Finance.

Nikbakht, E., Shahrokhi, M. and Corriette, A., 2019. Blockchain & distributed financial data.

Managerial Finance.

Panda, B. and Kumar, G., 2020. What matters to ownership structure? Evidence from pre-and

post-global financial crisis in an emerging market. Managerial Finance.

Waemustafa, W., 2018. The paradox of managerial ownership and financial decisions of the

textile sector: An Asian market perspective. Journal of Social Sciences Research. (4).

pp.184-190.

Young, W. and Wu, C. C., 2017. Abnormal investment, changes in institutional ownership, and

SEO long-run performance. Managerial Finance

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.