Dell Laptop Plant Project: Financial Analysis and Recommendations

VerifiedAdded on 2023/03/17

|8

|1222

|92

Report

AI Summary

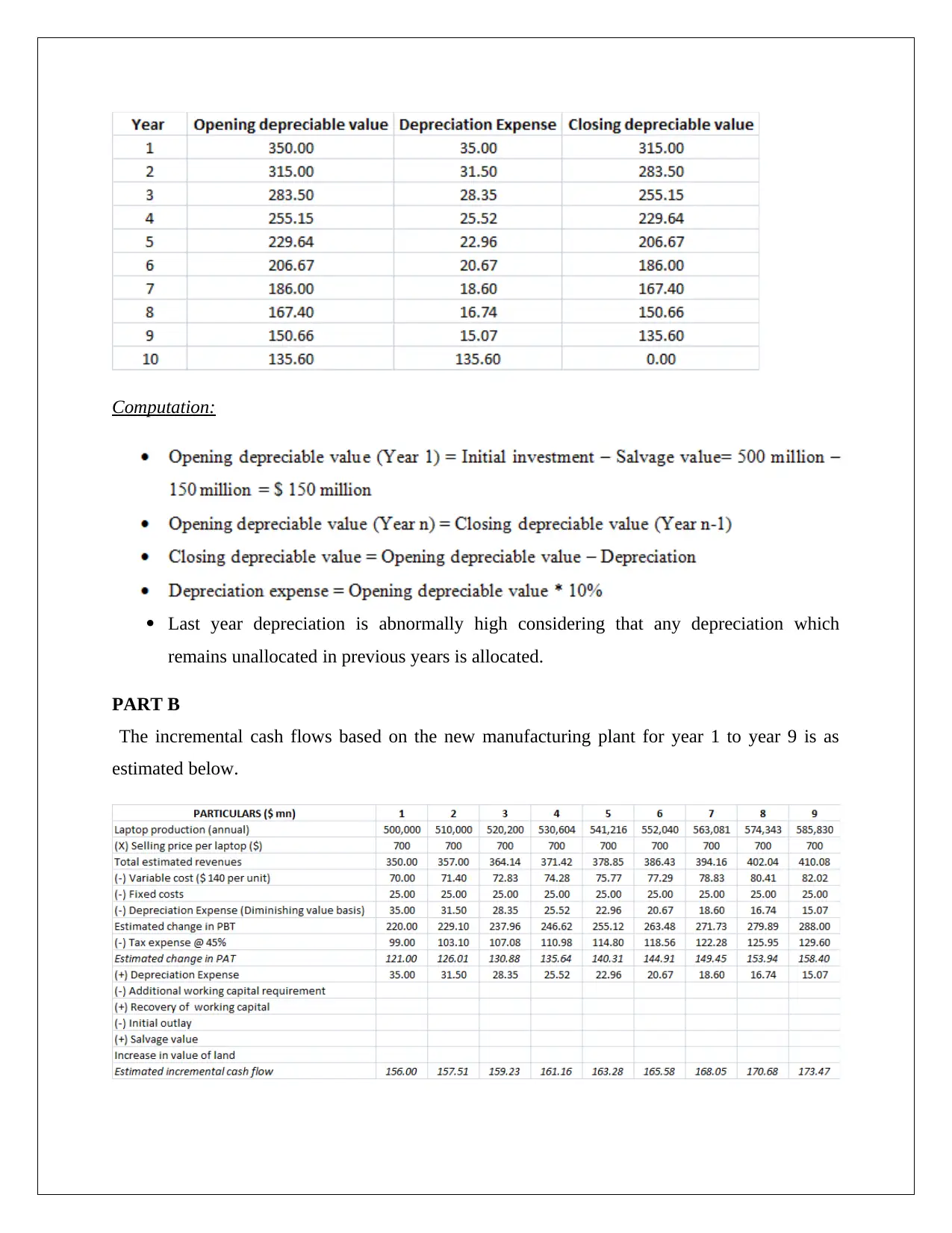

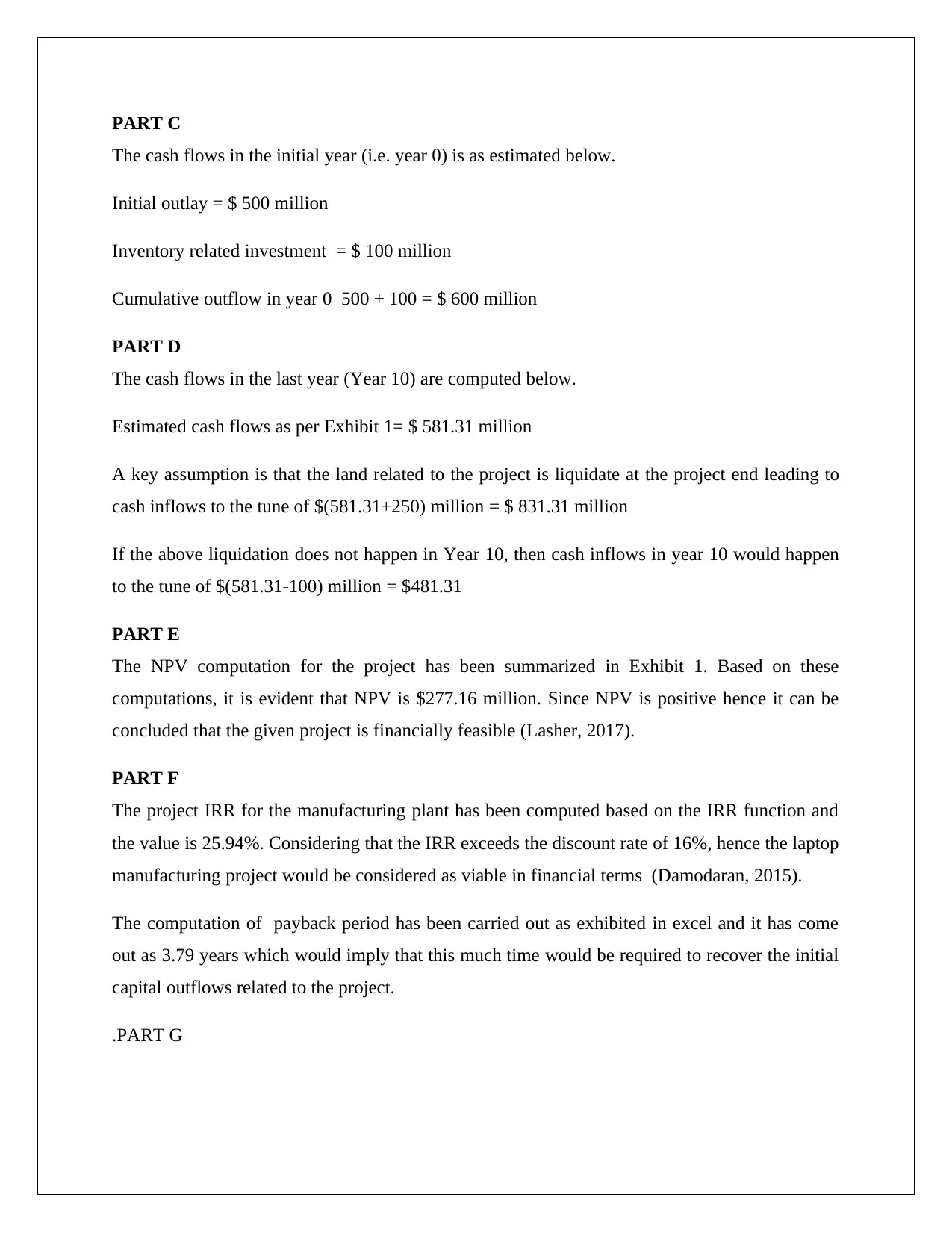

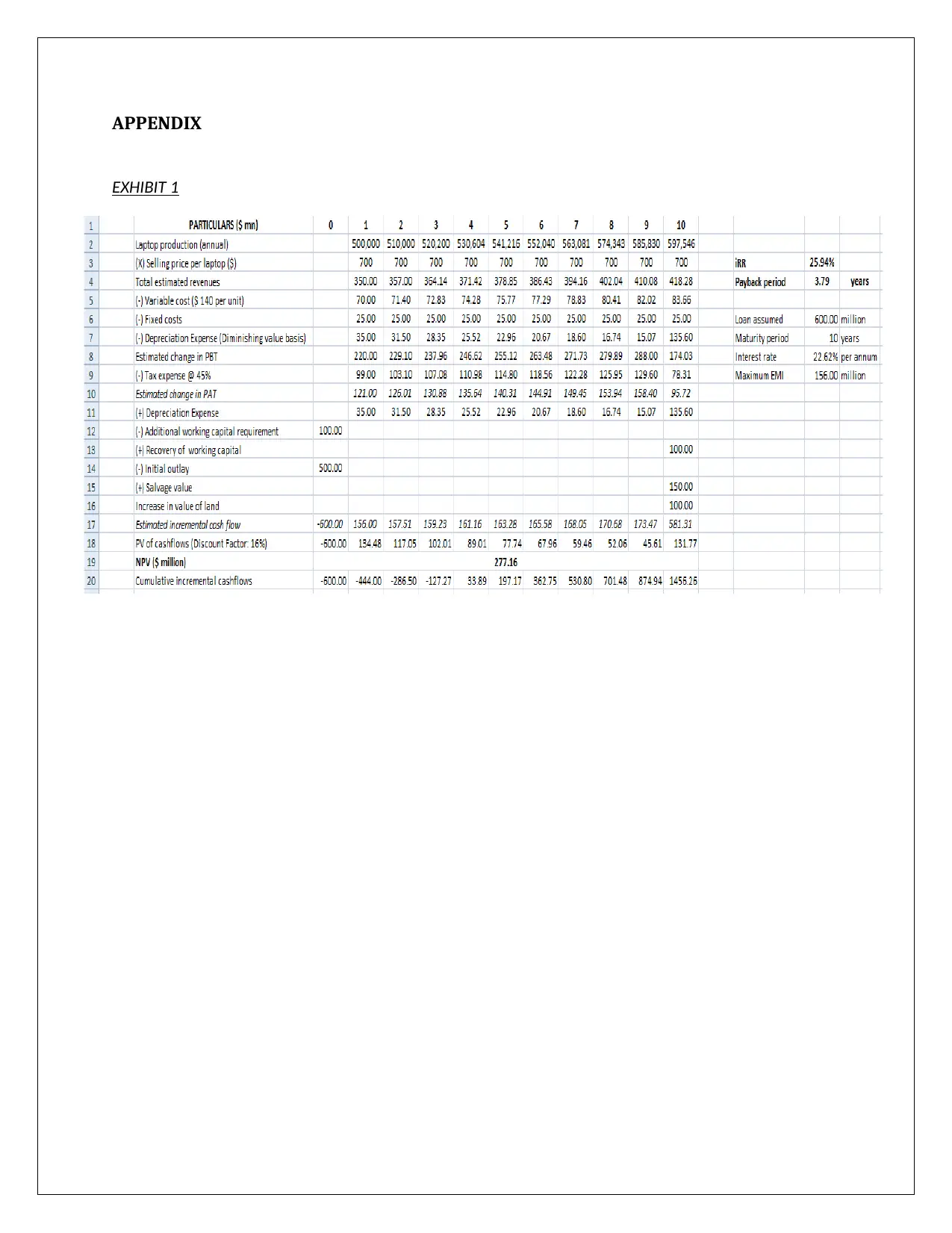

This report presents a financial analysis of a proposed laptop manufacturing plant for Dell, evaluating its feasibility using capital budgeting techniques. The analysis includes calculations for depreciation, incremental cash flows, and initial investments, leading to the computation of Net Present Value (NPV), Internal Rate of Return (IRR), and payback period. The report finds the project financially viable based on a positive NPV and an IRR exceeding the discount rate. The report also assesses the impact of debt financing and the company's current approach to the cost of capital. It concludes with recommendations to adjust the cost of capital based on risk and relax the CEO's stringent debt servicing requirement to maximize shareholder wealth. References to academic sources are also provided.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.