Financial Ratio Analysis of Sports Direct vs JD Sports Fashion

VerifiedAdded on 2023/01/11

|27

|4025

|26

Report

AI Summary

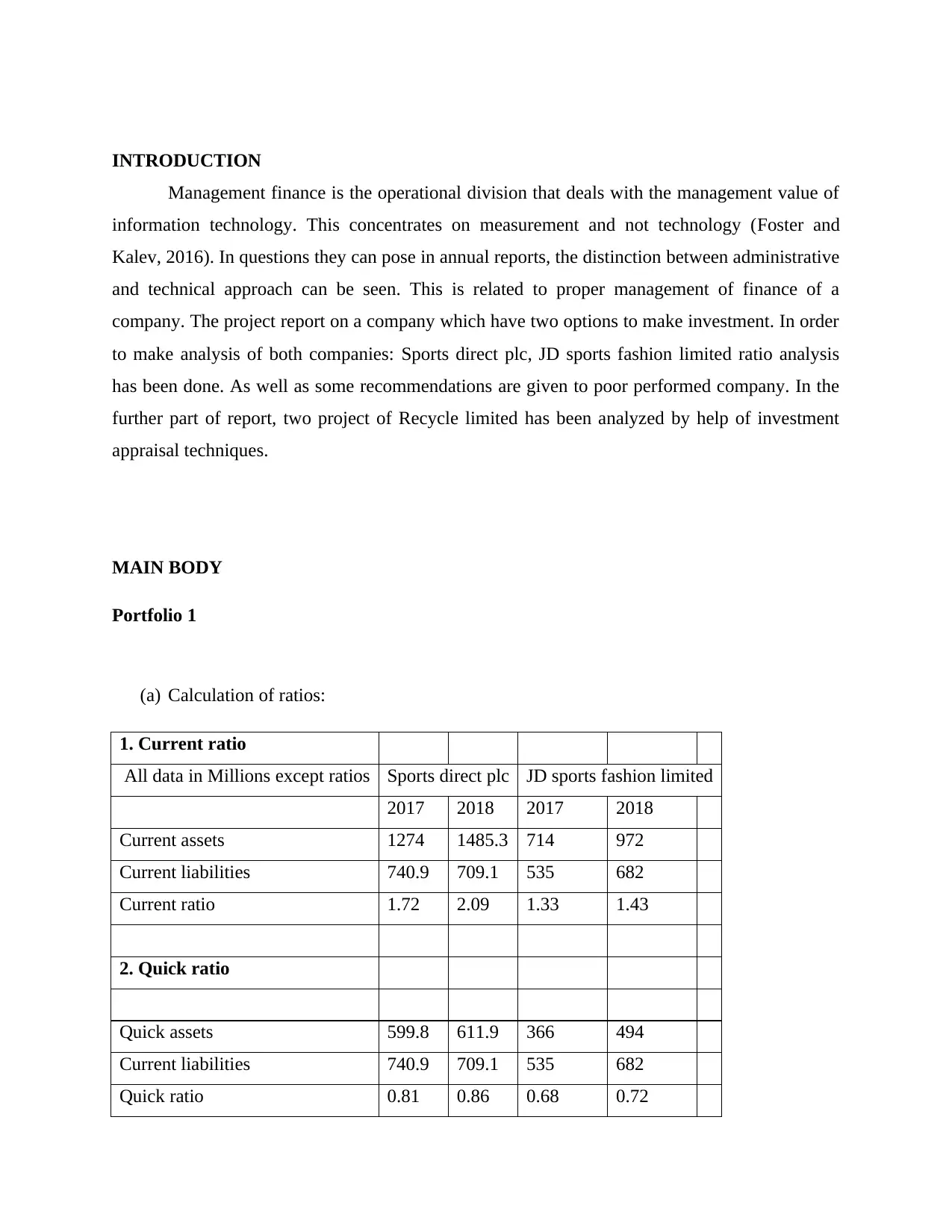

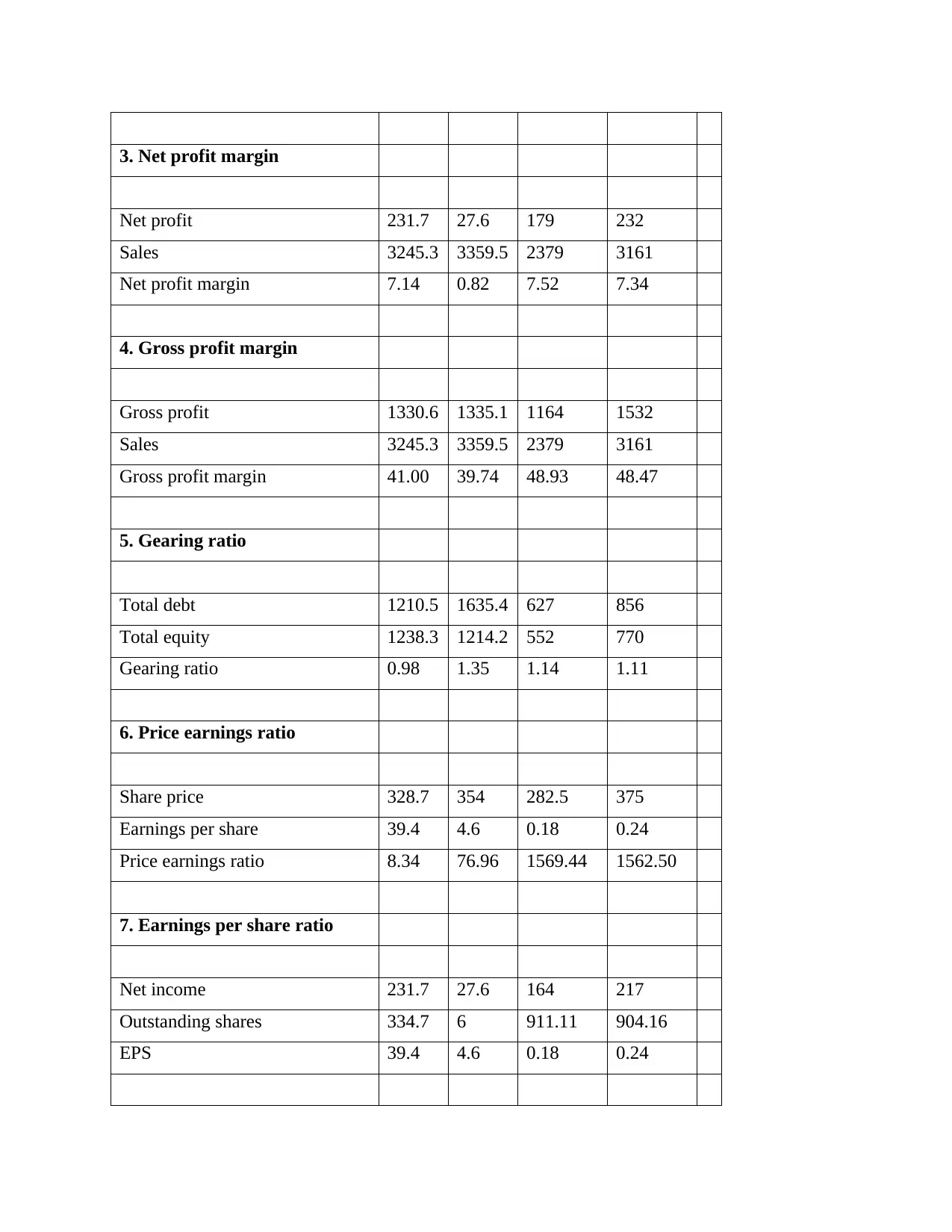

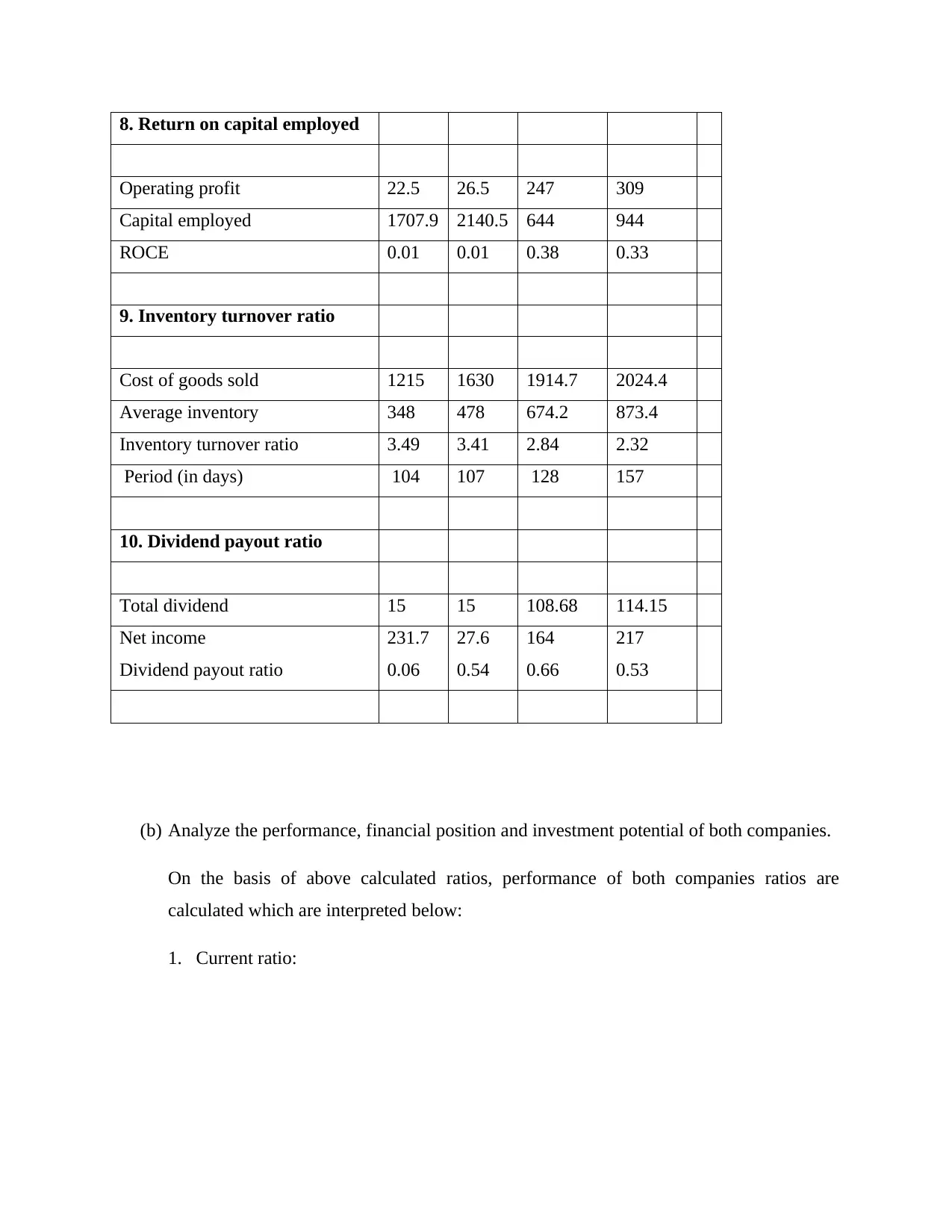

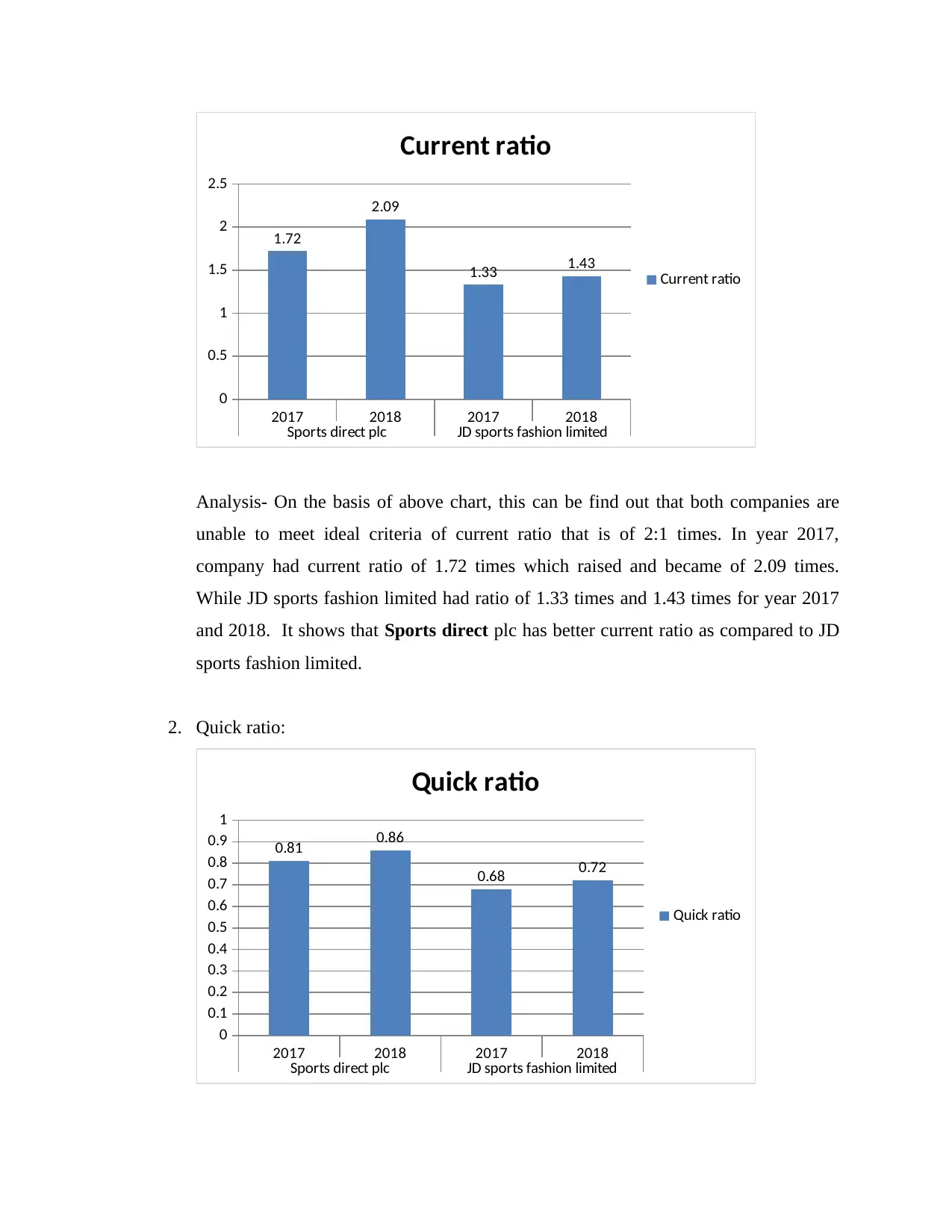

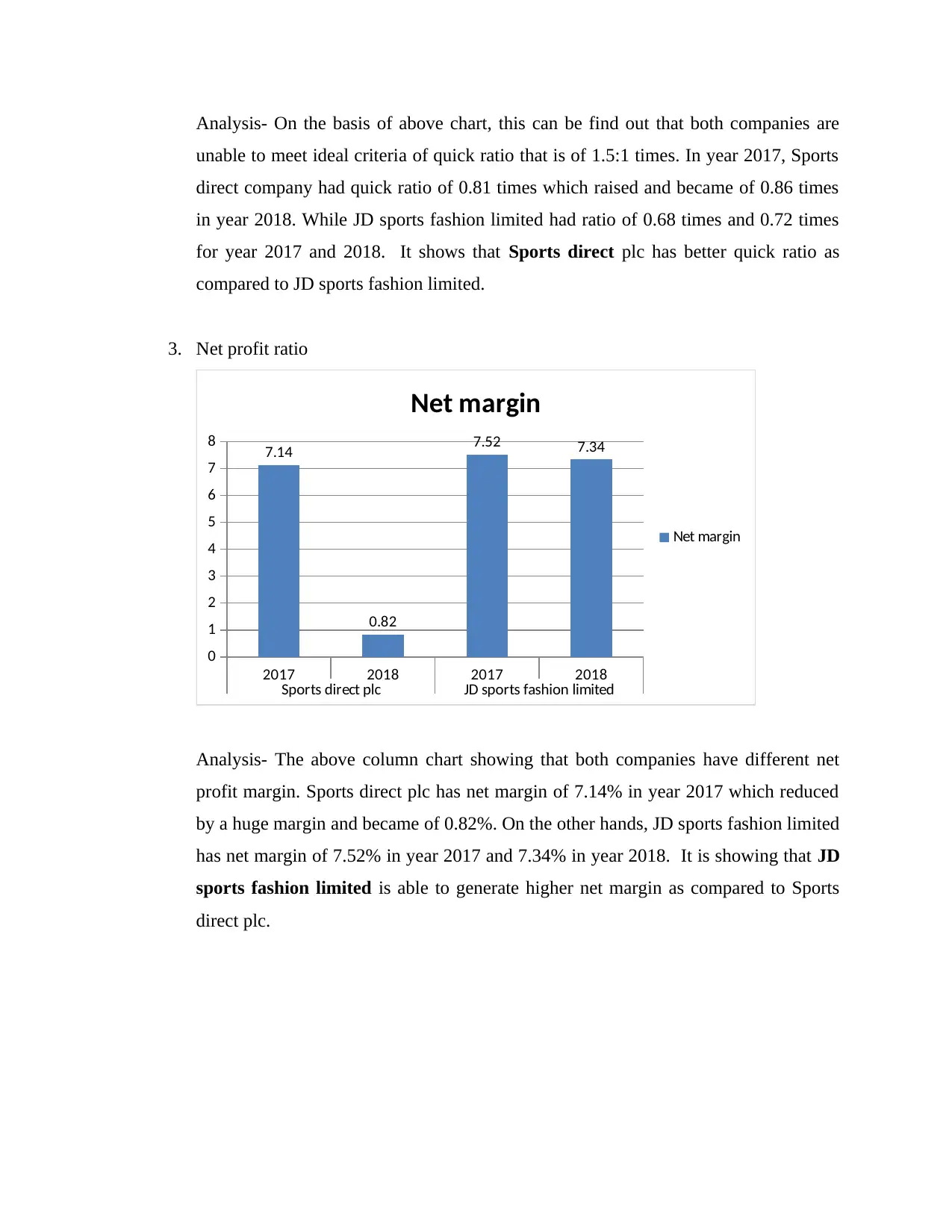

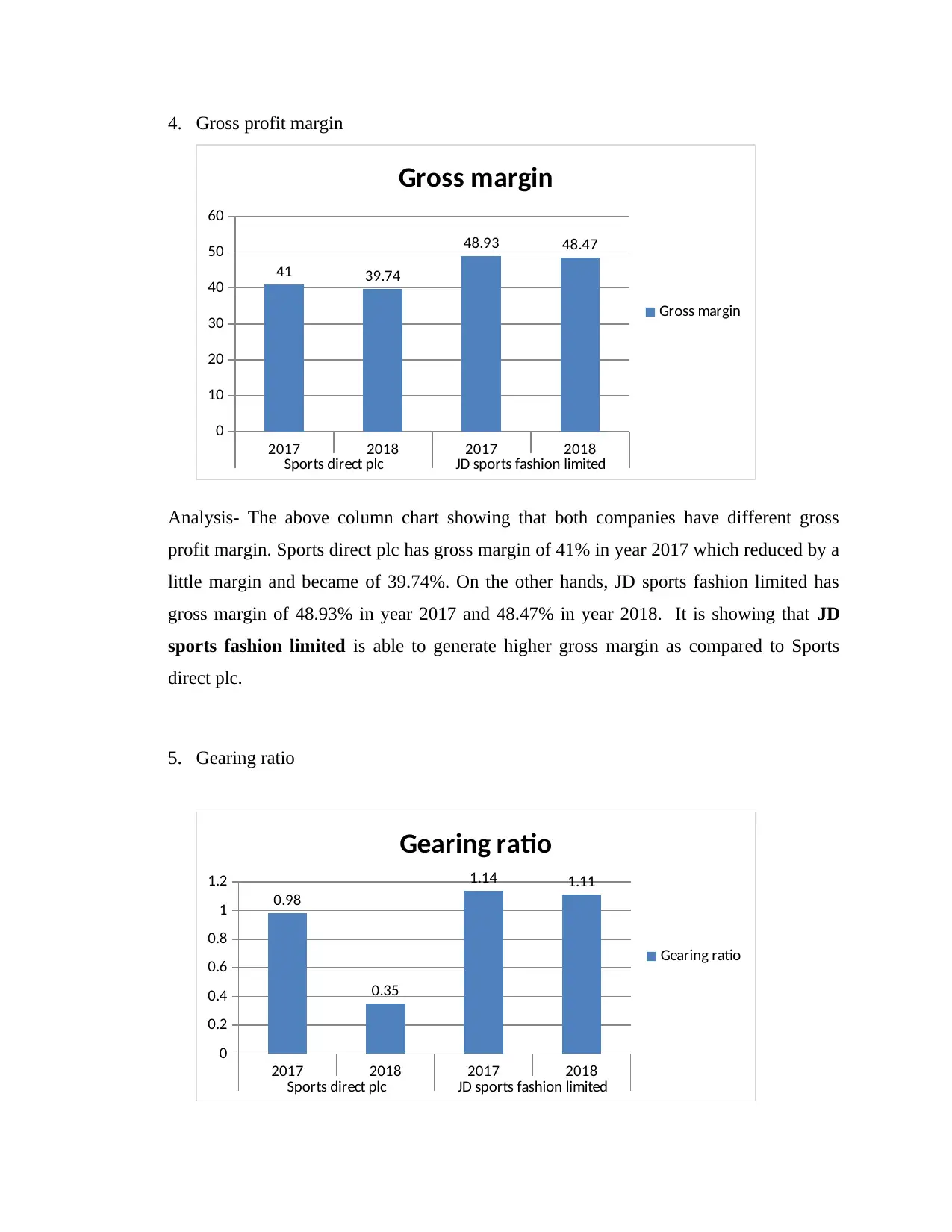

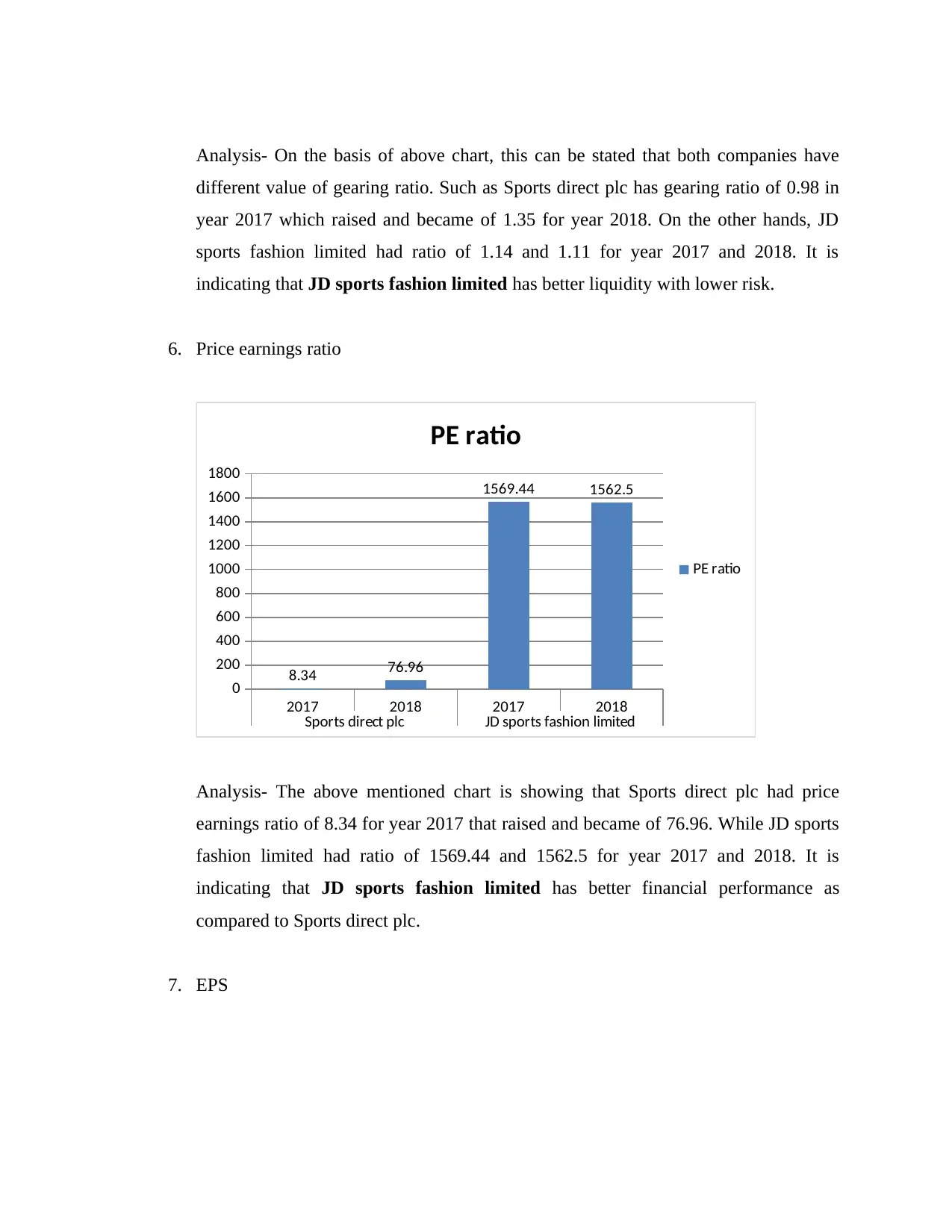

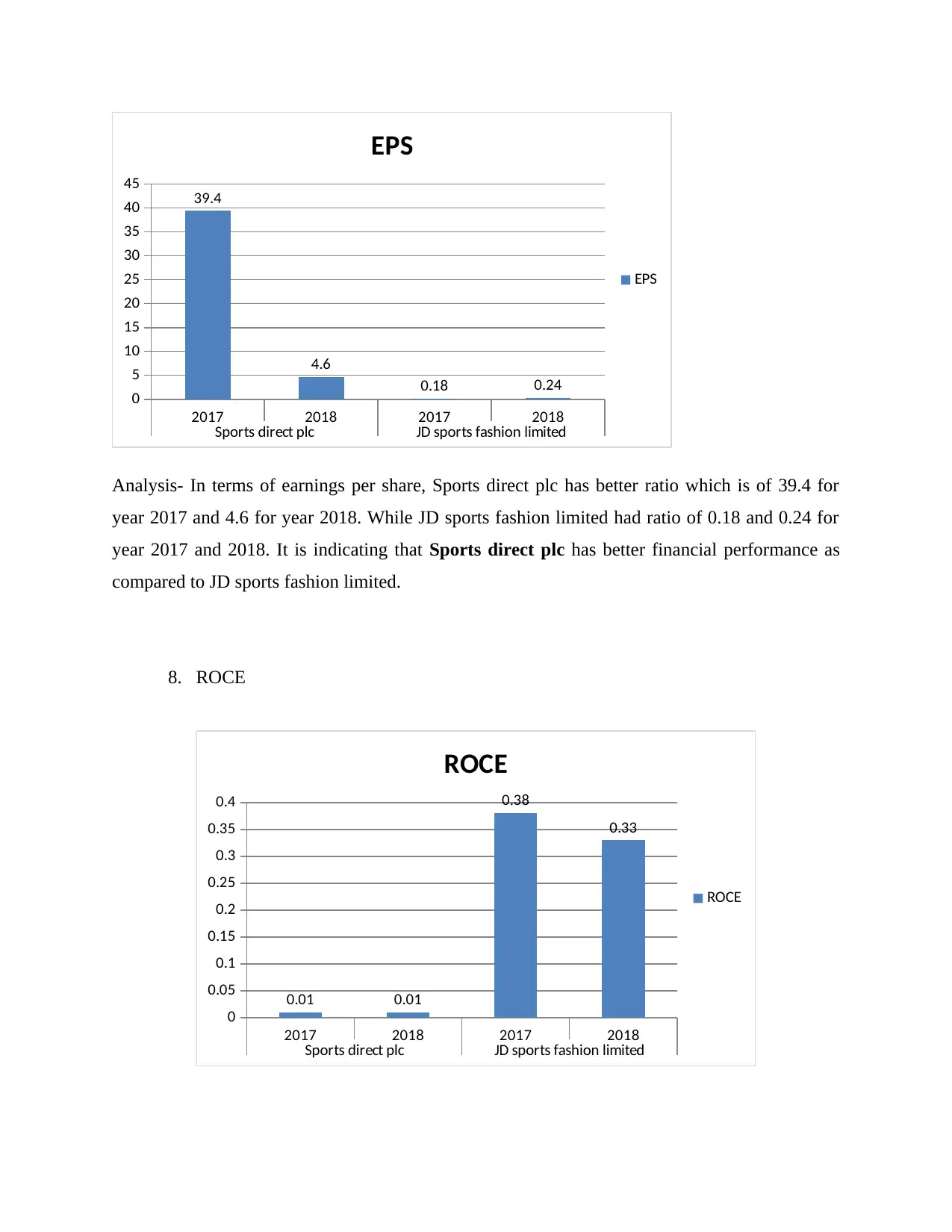

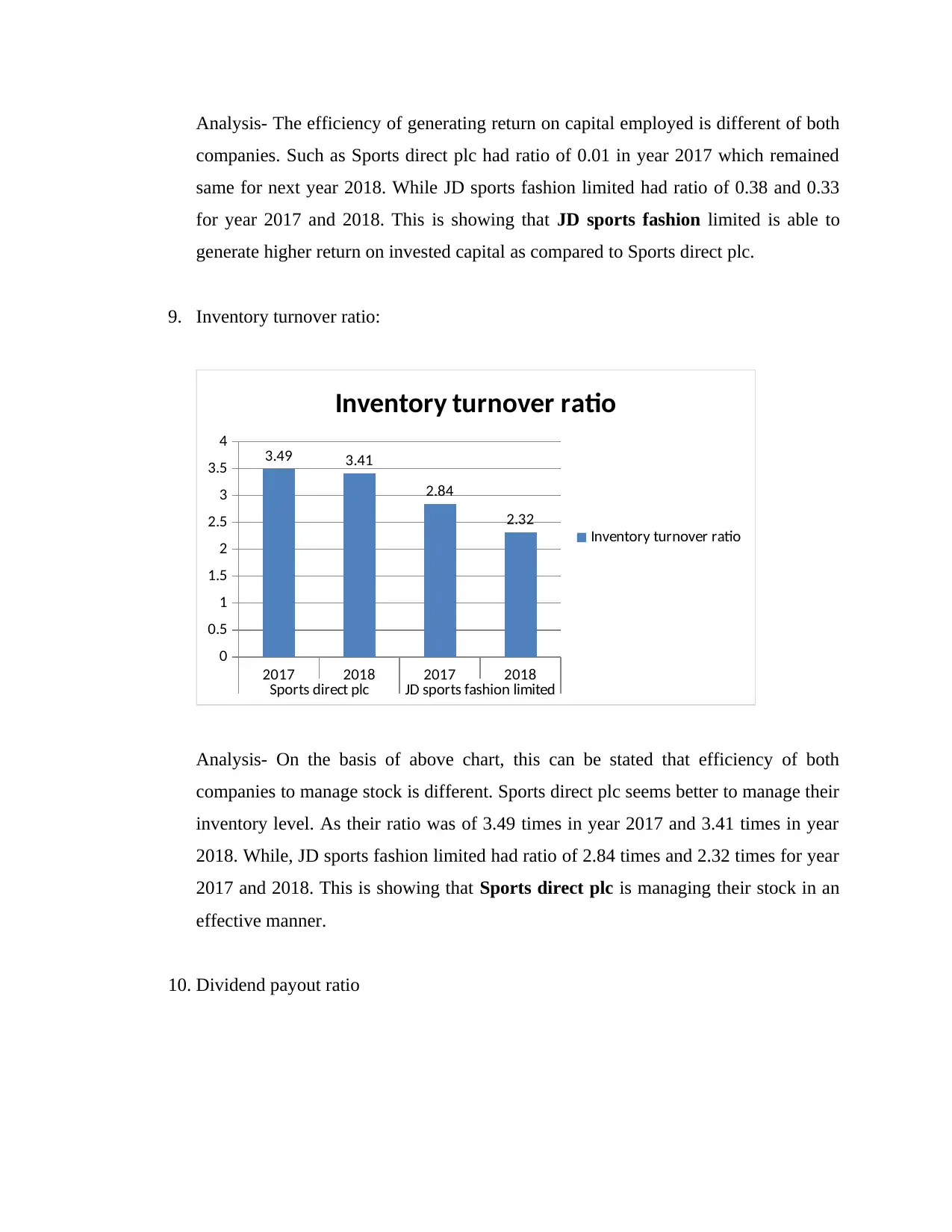

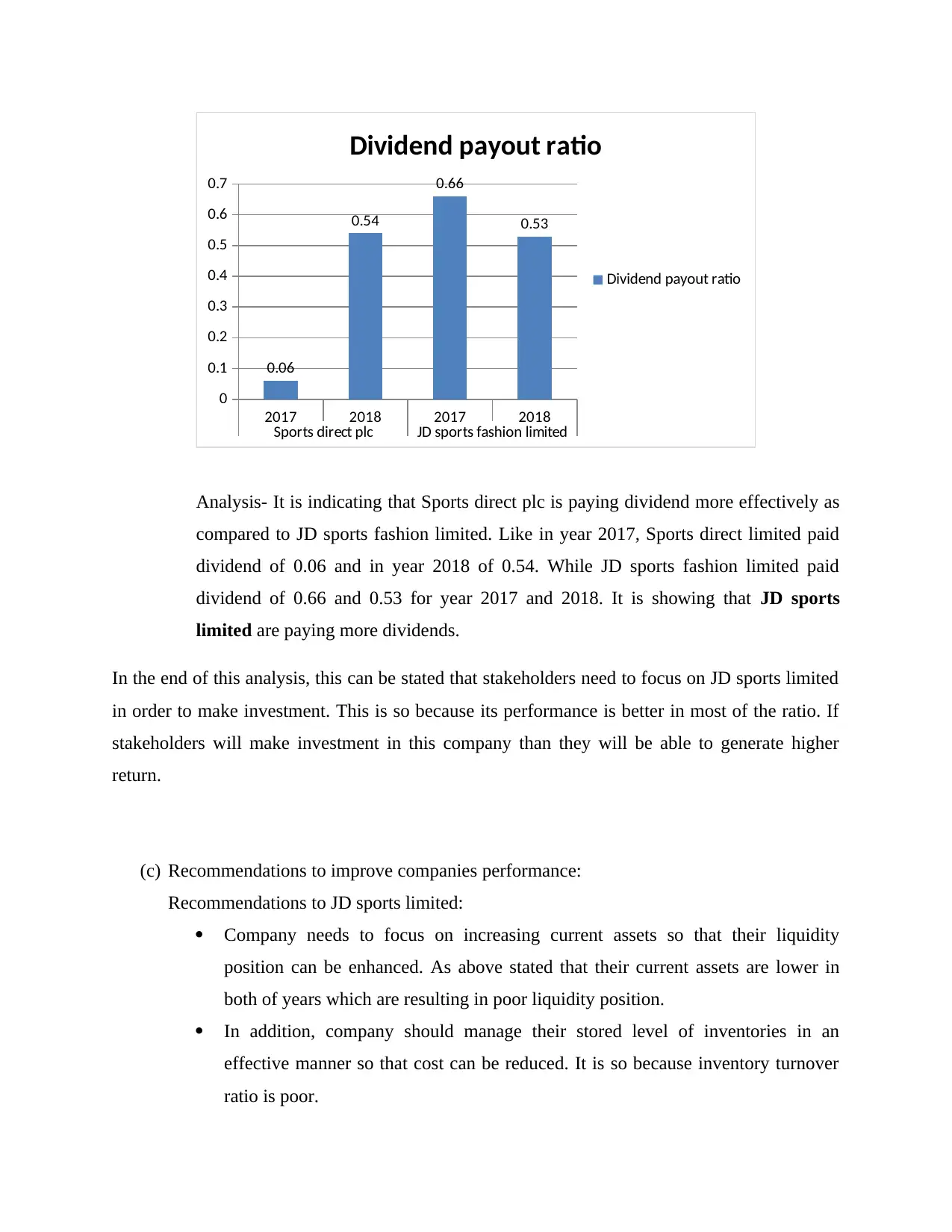

This report presents a comprehensive financial analysis of Sports Direct plc and JD Sports Fashion Limited, focusing on their performance, financial position, and investment potential. The analysis employs various financial ratios, including current ratio, quick ratio, net profit margin, gross profit margin, gearing ratio, price-earnings ratio, earnings per share, return on capital employed, inventory turnover ratio, and dividend payout ratio. The report compares the two companies across these metrics for the years 2017 and 2018, highlighting their strengths and weaknesses. Recommendations are provided to improve the performance of each company, focusing on enhancing profitability, managing inventory, and optimizing share value. Additionally, the report discusses the limitations of relying solely on financial ratios for interpreting a company's performance, considering factors like historical data, inflation, accounting policy changes, and potential financial statement manipulation. The conclusion emphasizes the importance of a holistic approach to financial analysis, considering both quantitative and qualitative factors.

1 out of 27

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.