Managerial Finance Report: Financial Analysis of Sports Retail Sector

VerifiedAdded on 2020/07/23

|25

|4524

|39

Report

AI Summary

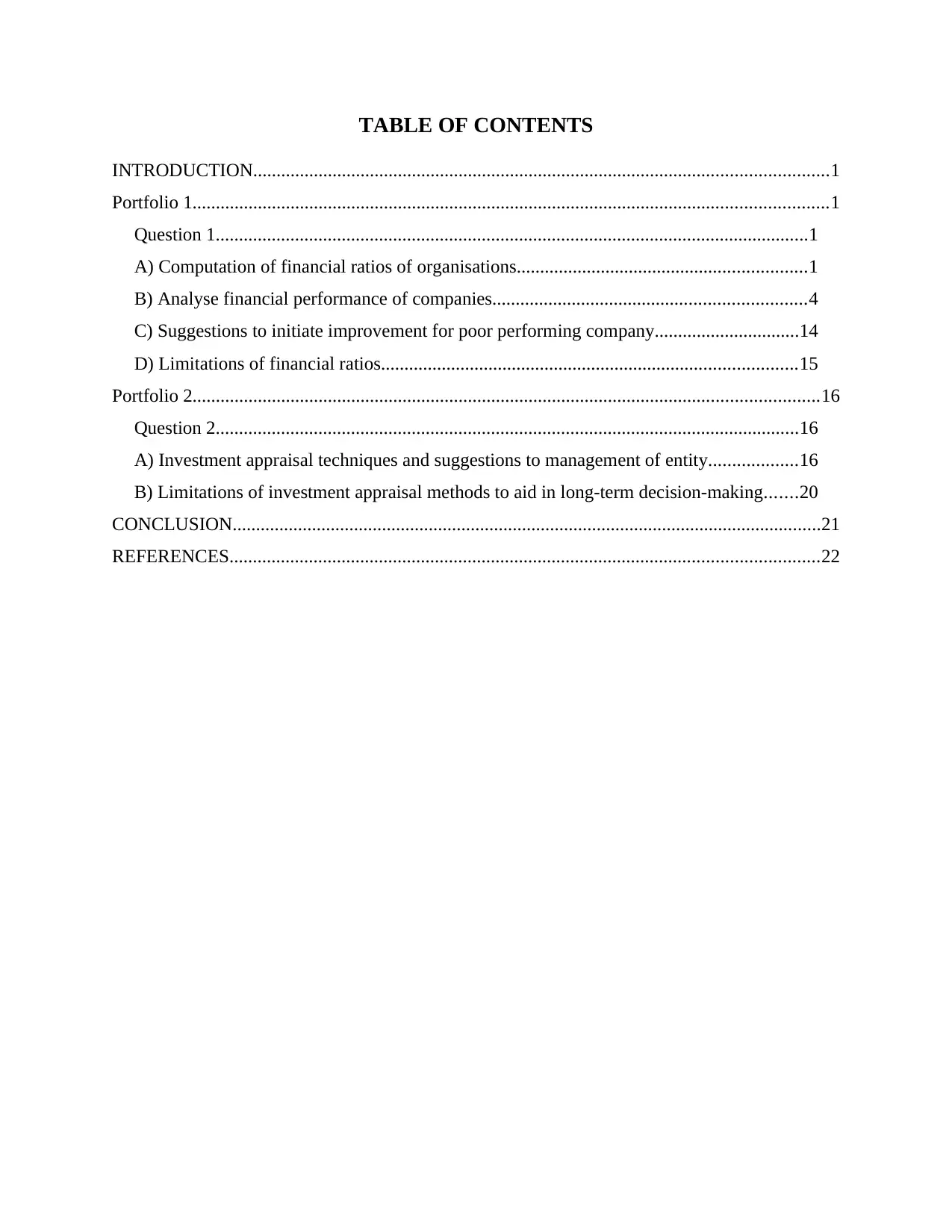

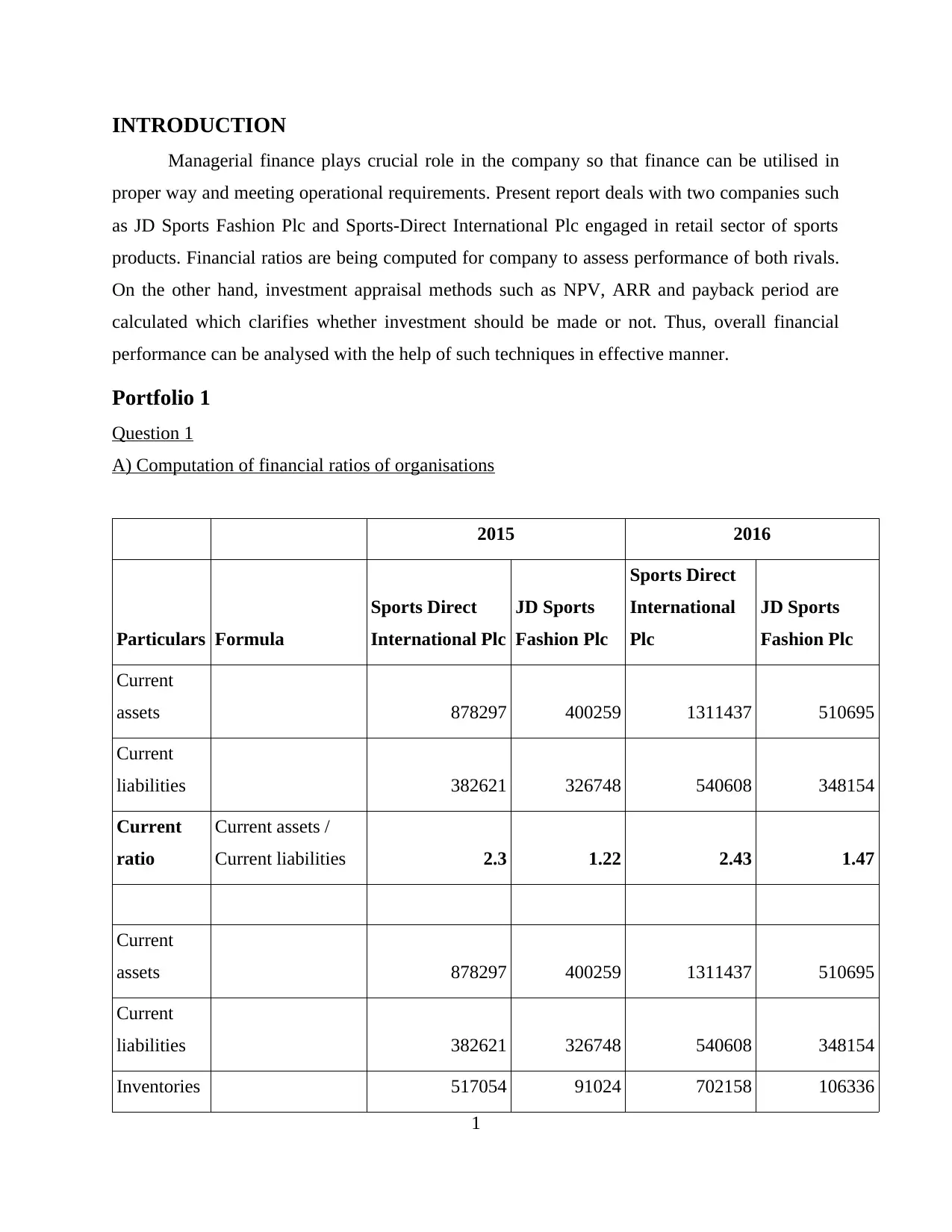

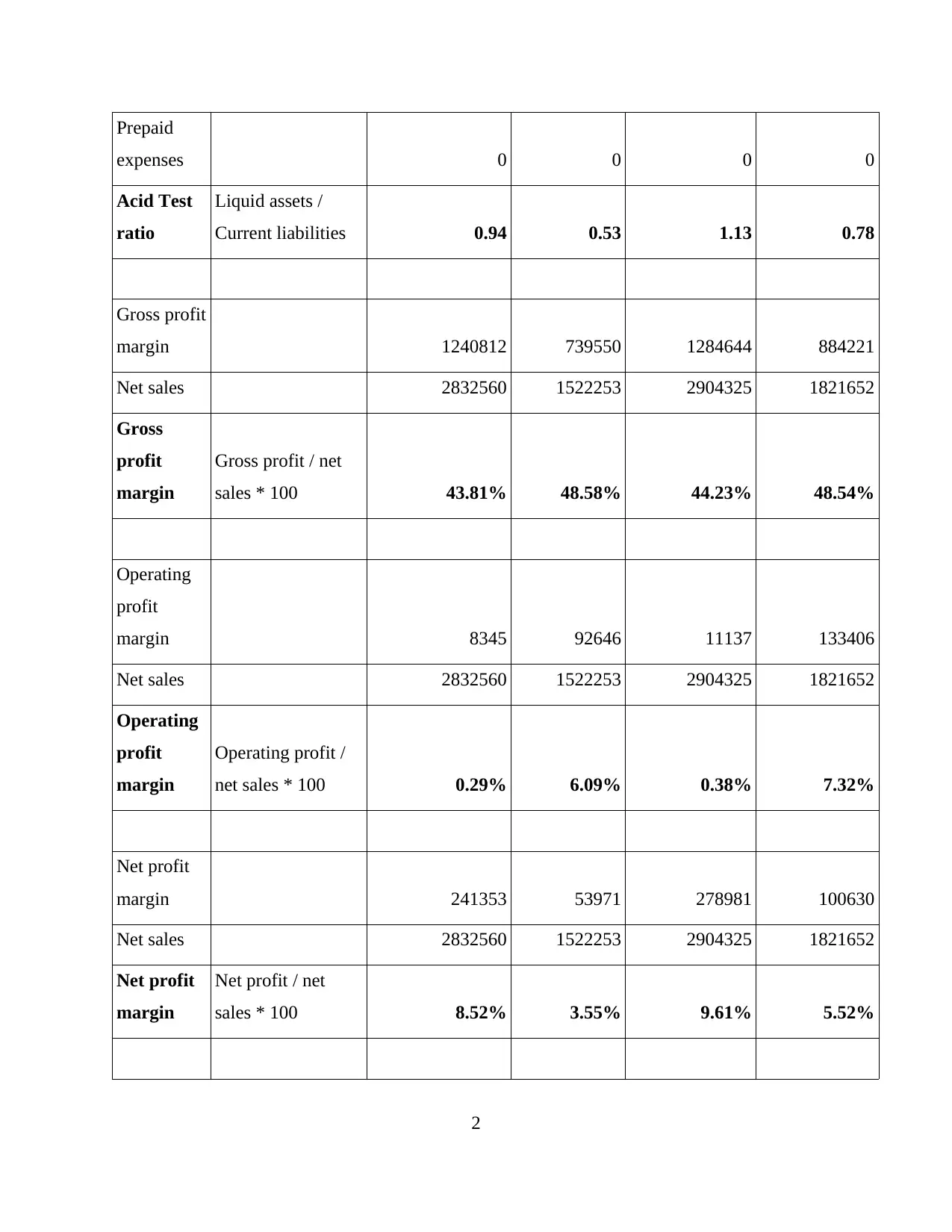

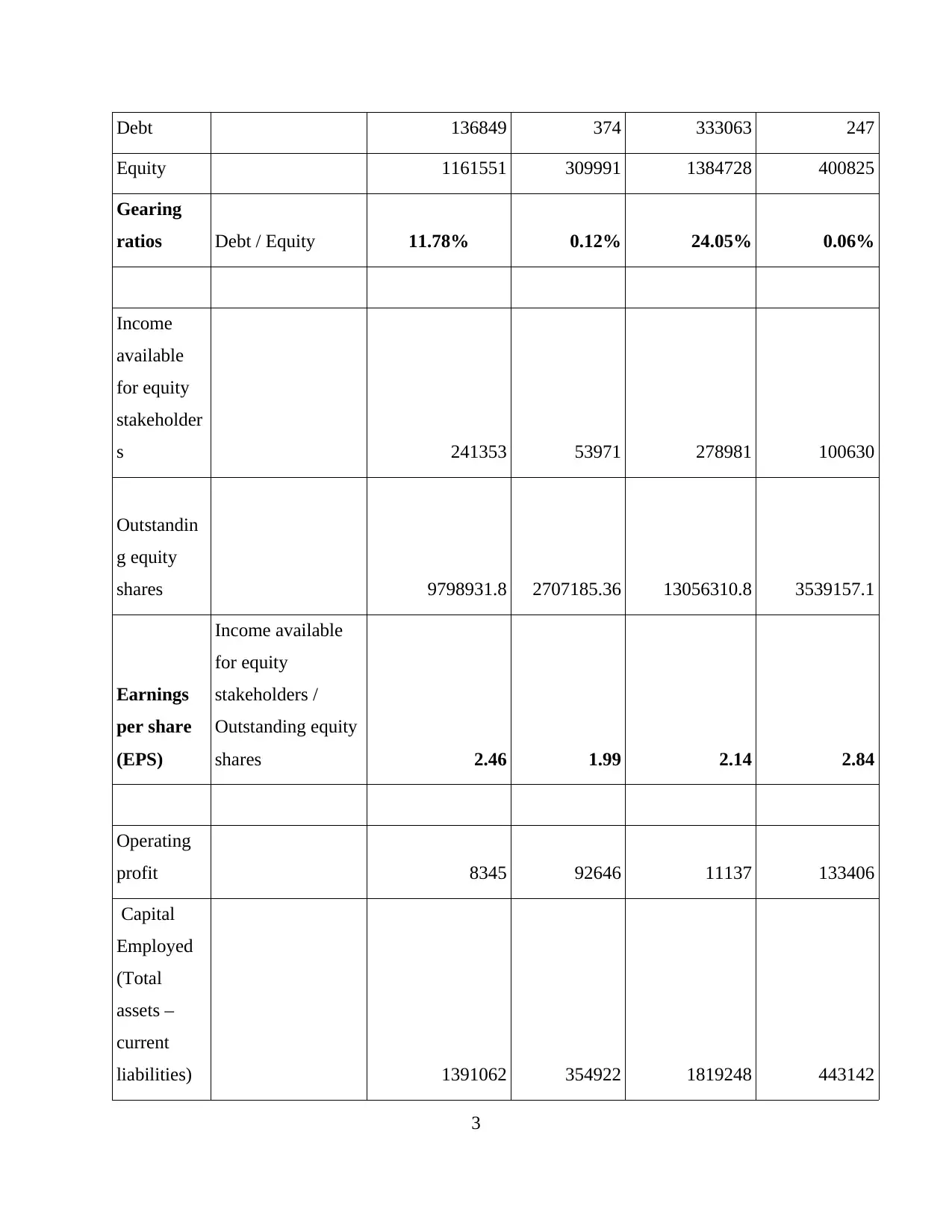

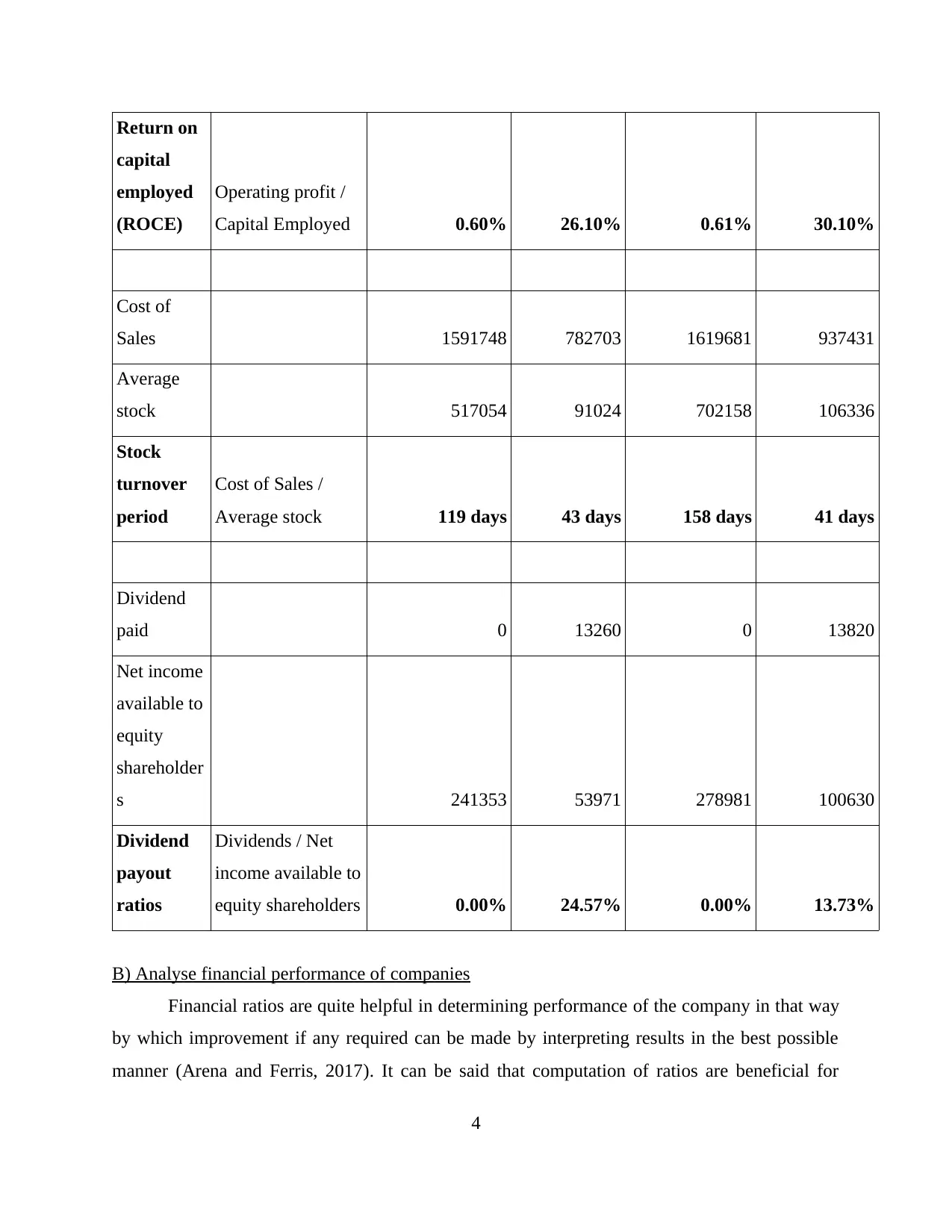

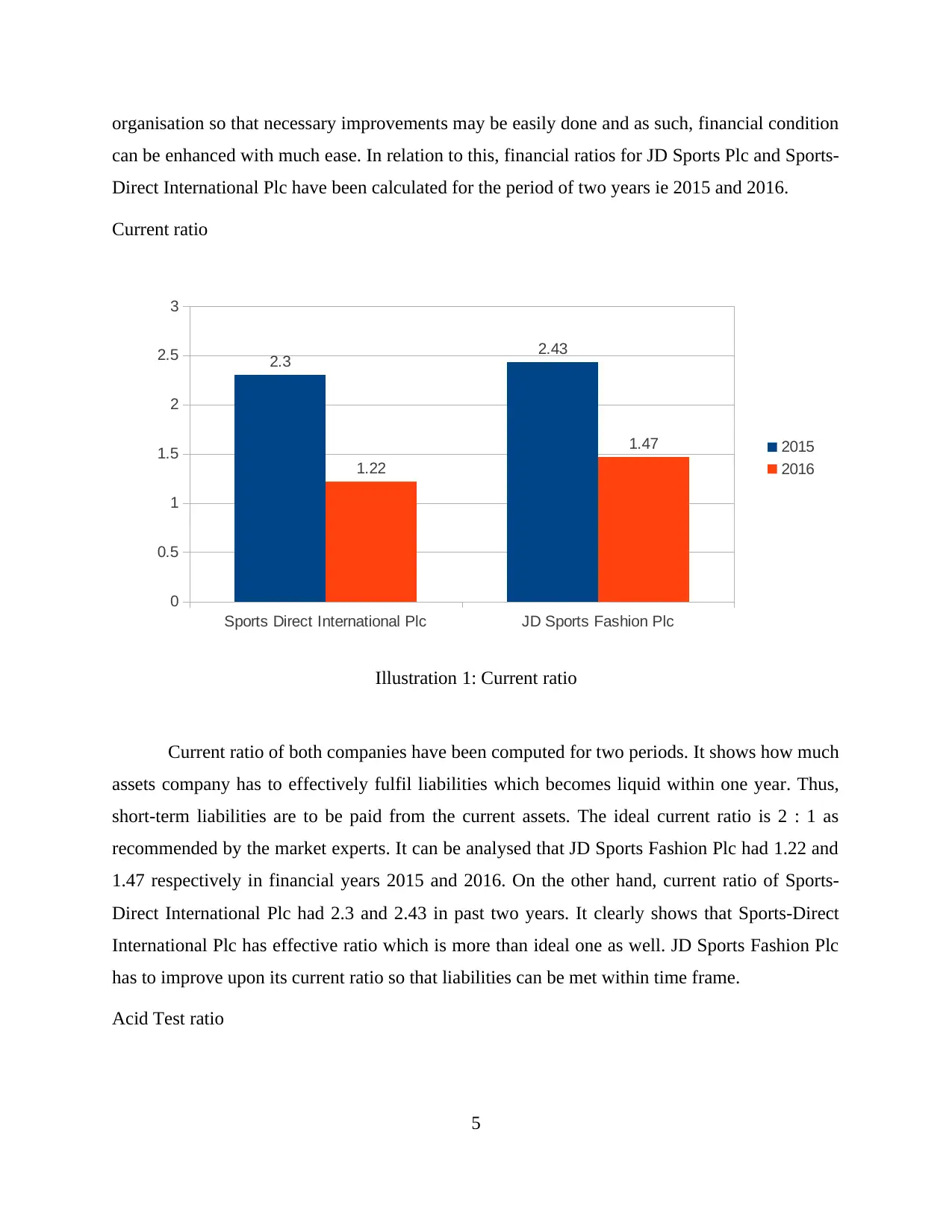

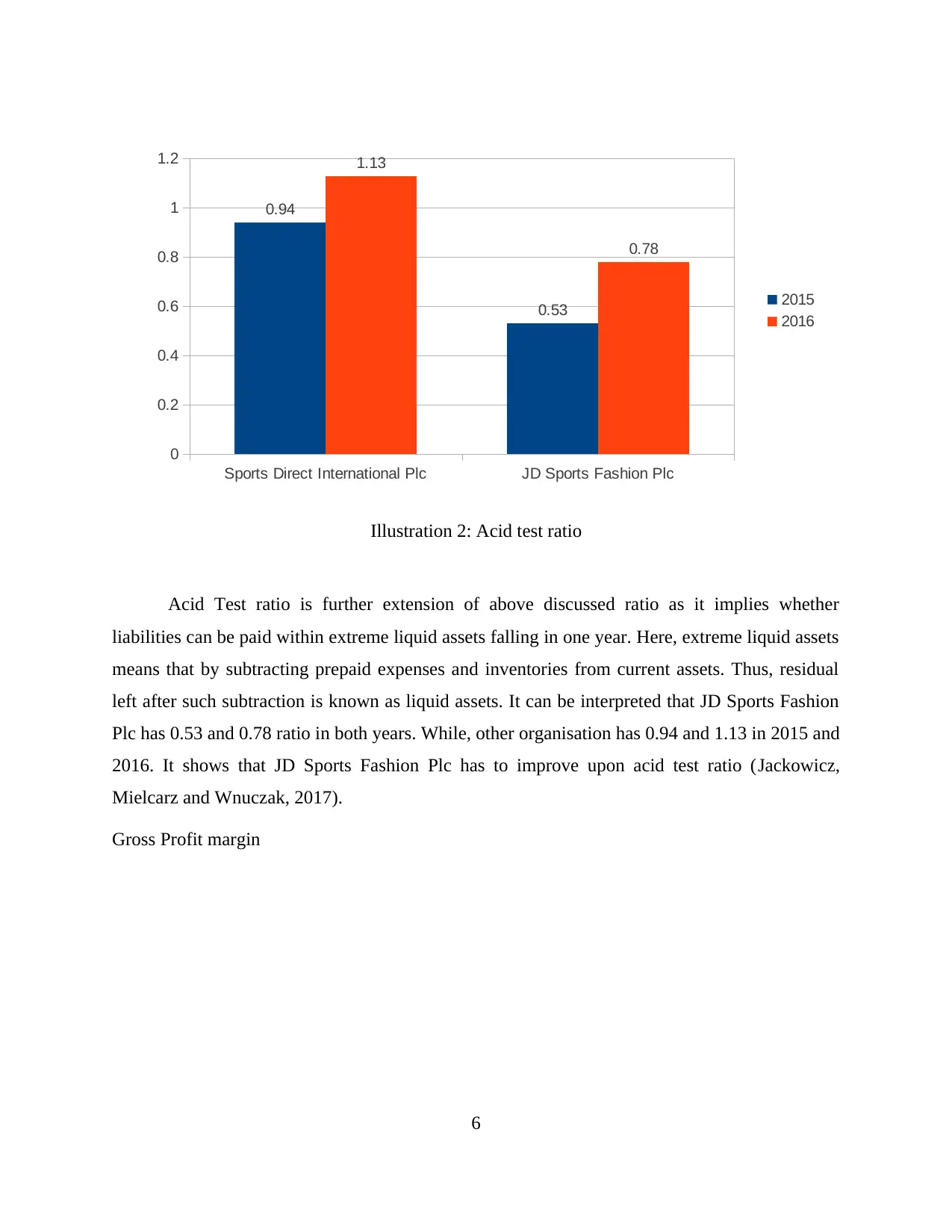

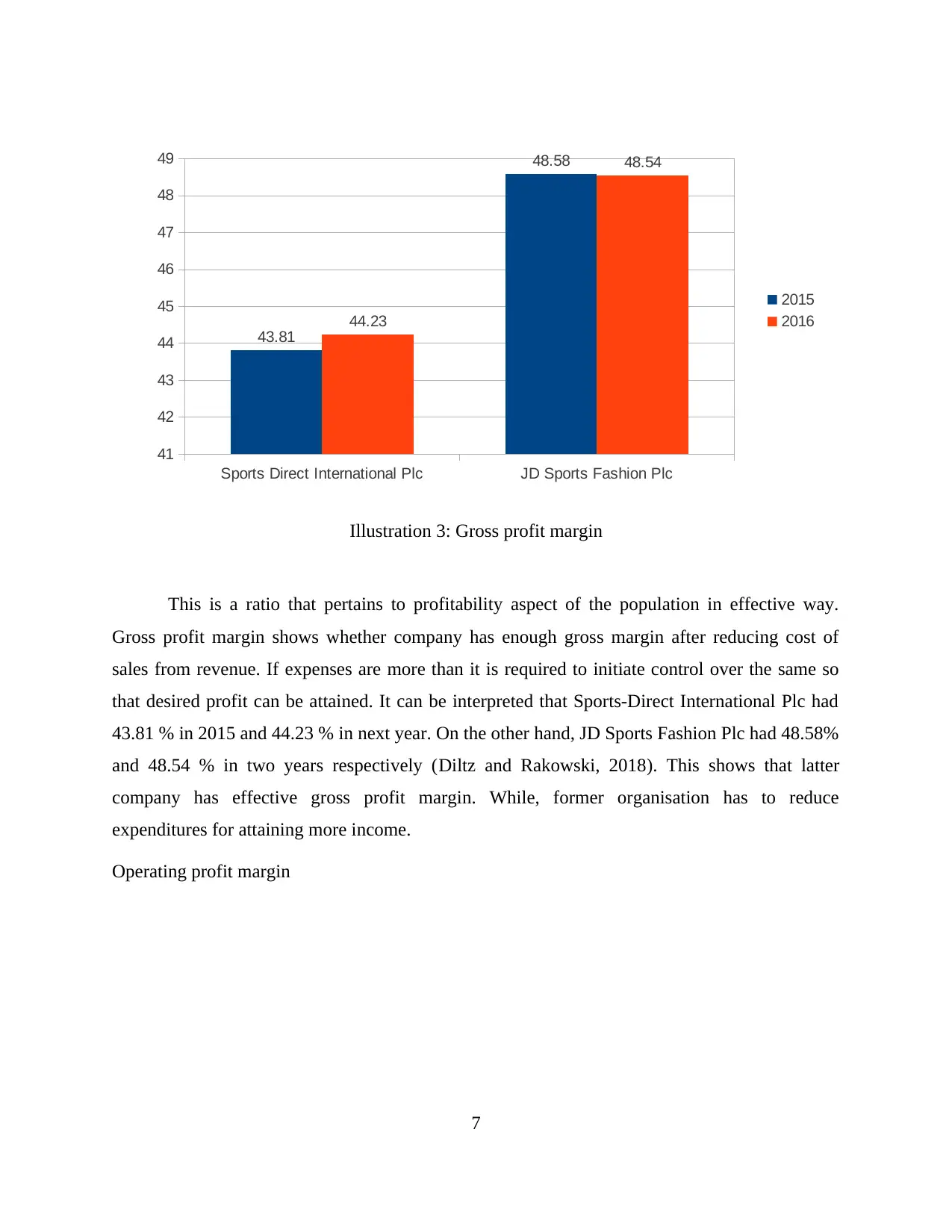

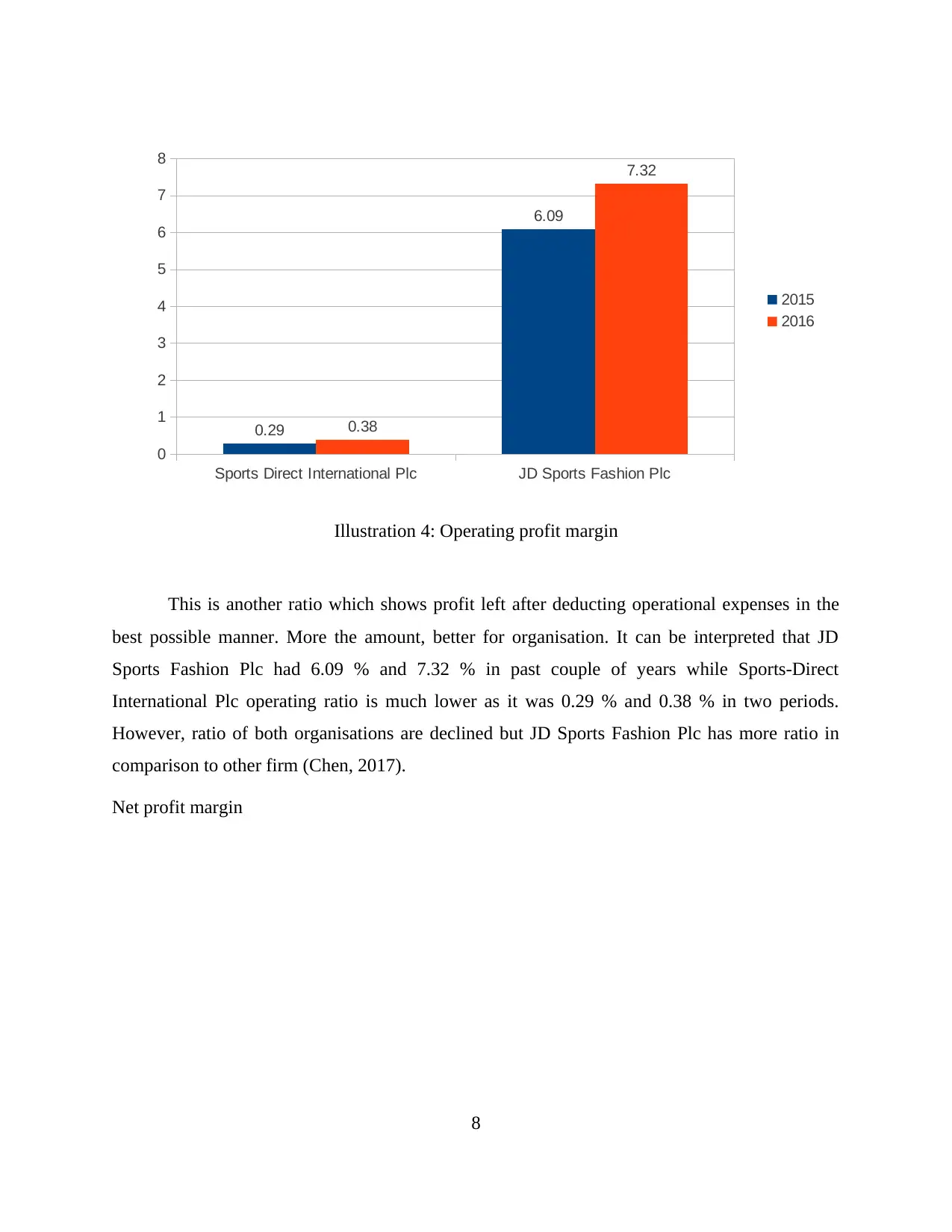

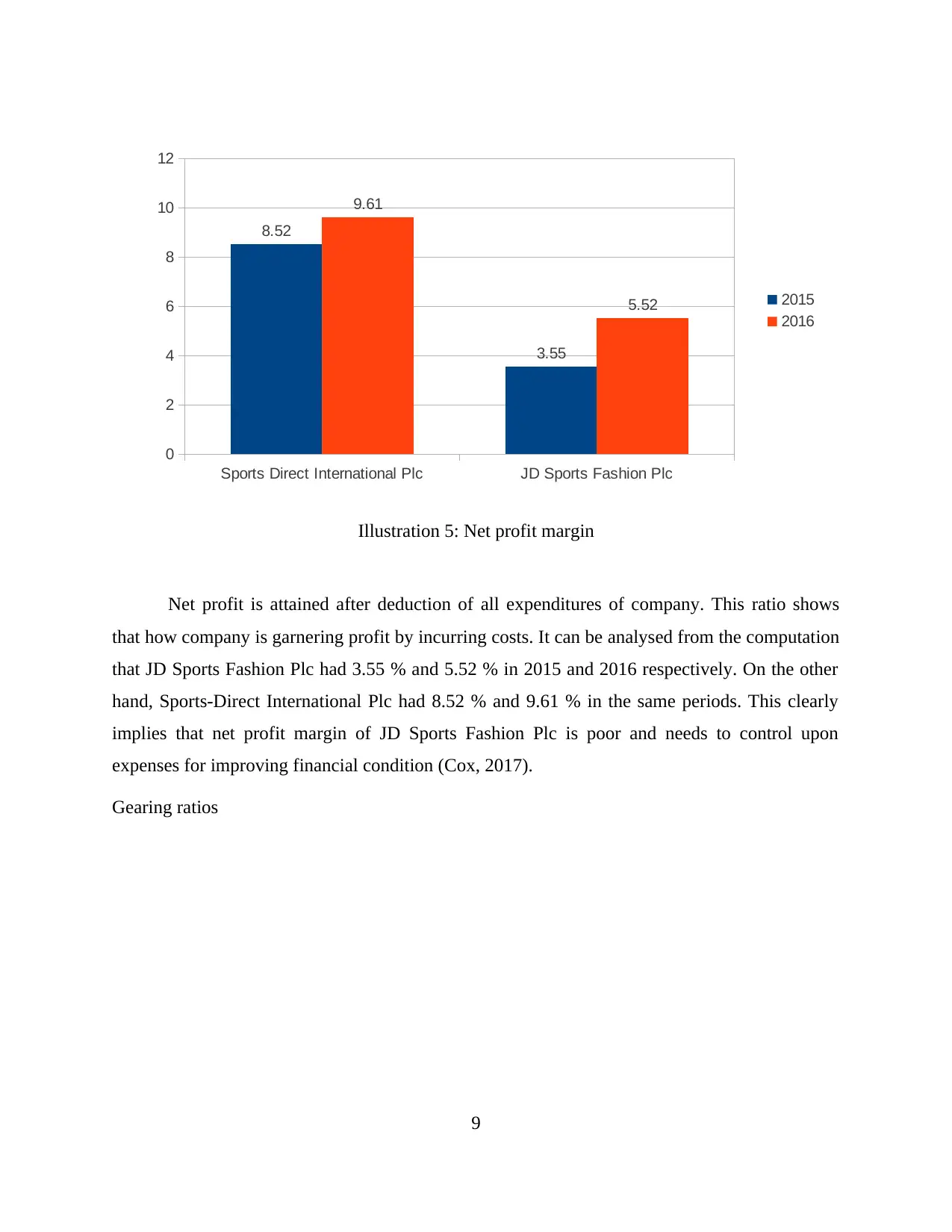

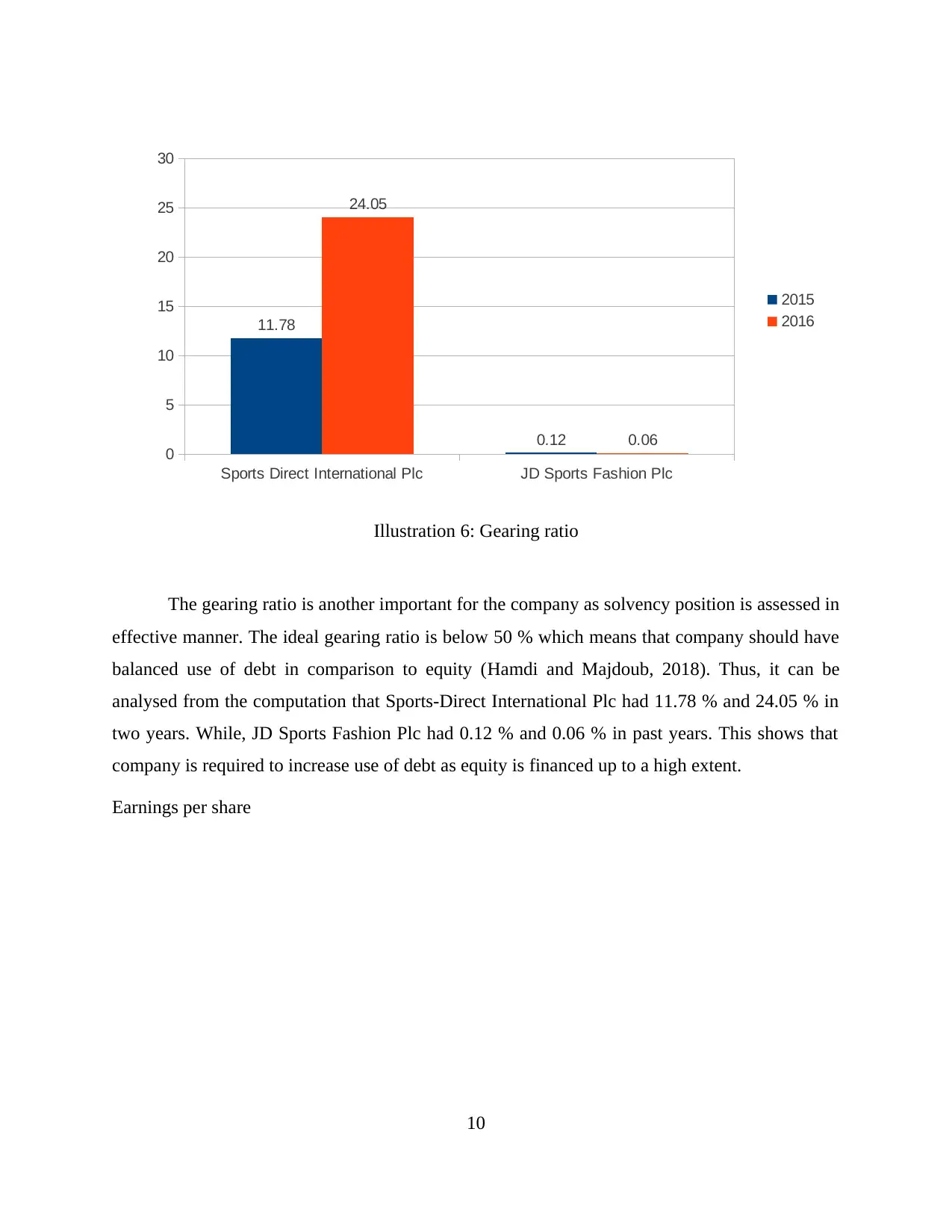

This report delves into managerial finance, focusing on the financial analysis of two prominent sports retail companies: JD Sports Fashion Plc and Sports-Direct International Plc. It begins with a detailed computation of various financial ratios, including current ratio, acid test ratio, gross profit margin, operating profit margin, net profit margin, gearing ratios, earnings per share (EPS), return on capital employed (ROCE), and stock turnover period, for both companies over two years (2015 and 2016). The analysis then interprets these ratios to assess the companies' financial performance, highlighting strengths and weaknesses. Furthermore, the report explores investment appraisal techniques such as Net Present Value (NPV), Average Rate of Return (ARR), and payback period, providing recommendations to management regarding investment decisions. Finally, it discusses the limitations of using financial ratios and investment appraisal methods for long-term decision-making, offering a comprehensive overview of financial analysis within the retail sector.

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.