Managerial Finance Report: Financial Performance Analysis

VerifiedAdded on 2022/11/24

|19

|4171

|50

Report

AI Summary

This report delves into managerial finance, examining the financial performance, position, and investment potential of Tesco PLC and Sainsbury PLC. It employs ratio analysis to evaluate profitability, liquidity, and gearing, comparing the companies' performance in 2018 and 2019. The report also explores investment appraisal techniques and their limitations in long-term decision-making. It provides recommendations for improving financial performance and highlights the shortcomings of relying solely on financial ratios. The analysis includes current ratio, quick ratio, net profit margin, gross profit margin, gearing ratio, price to earnings ratio, earnings per share, return on capital employed, average inventory turnover period, and dividend payout ratio. The report provides a comprehensive overview of financial analysis and investment strategies.

Managerial Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

PORTFOLIO 1................................................................................................................................3

Ratio analysis...............................................................................................................................3

Analysis of financial performance, position and investment potential of both companies.........5

Recommendations on improving financial performance of poorly performing business.........11

Limitations of relying on financial ratios..................................................................................11

PORTFOLIO 2..............................................................................................................................13

Investment Appraisal techniques...............................................................................................13

Limitations of using investment appraisal techniques in long term decision making...............14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

PORTFOLIO 1................................................................................................................................3

Ratio analysis...............................................................................................................................3

Analysis of financial performance, position and investment potential of both companies.........5

Recommendations on improving financial performance of poorly performing business.........11

Limitations of relying on financial ratios..................................................................................11

PORTFOLIO 2..............................................................................................................................13

Investment Appraisal techniques...............................................................................................13

Limitations of using investment appraisal techniques in long term decision making...............14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Finance is the backbone of solid management, profitability, and development in a firm,

therefore business decision is important. It entails making prudent judgments about the capital

structure and condition. This study examines two firms' business decision from the perspective

of investors, as well as investing assessment methodologies from the perspective of management.

It's split into two halves (Salehi, Daemi and Akbari, 2020). The first portfolio uses ratio analysis

to examine Sainsbury PLC and Tesco PLC's profitability, positioning, and future value. Ratio

analysis' shortcomings in assessing a company's success are also highlighted. There are also

suggestions for enhancing the competitiveness of underperforming firms. The second portfolio

examines capital investment assessment methodologies and their limits in establishing long -

term business decisions.

PORTFOLIO 1

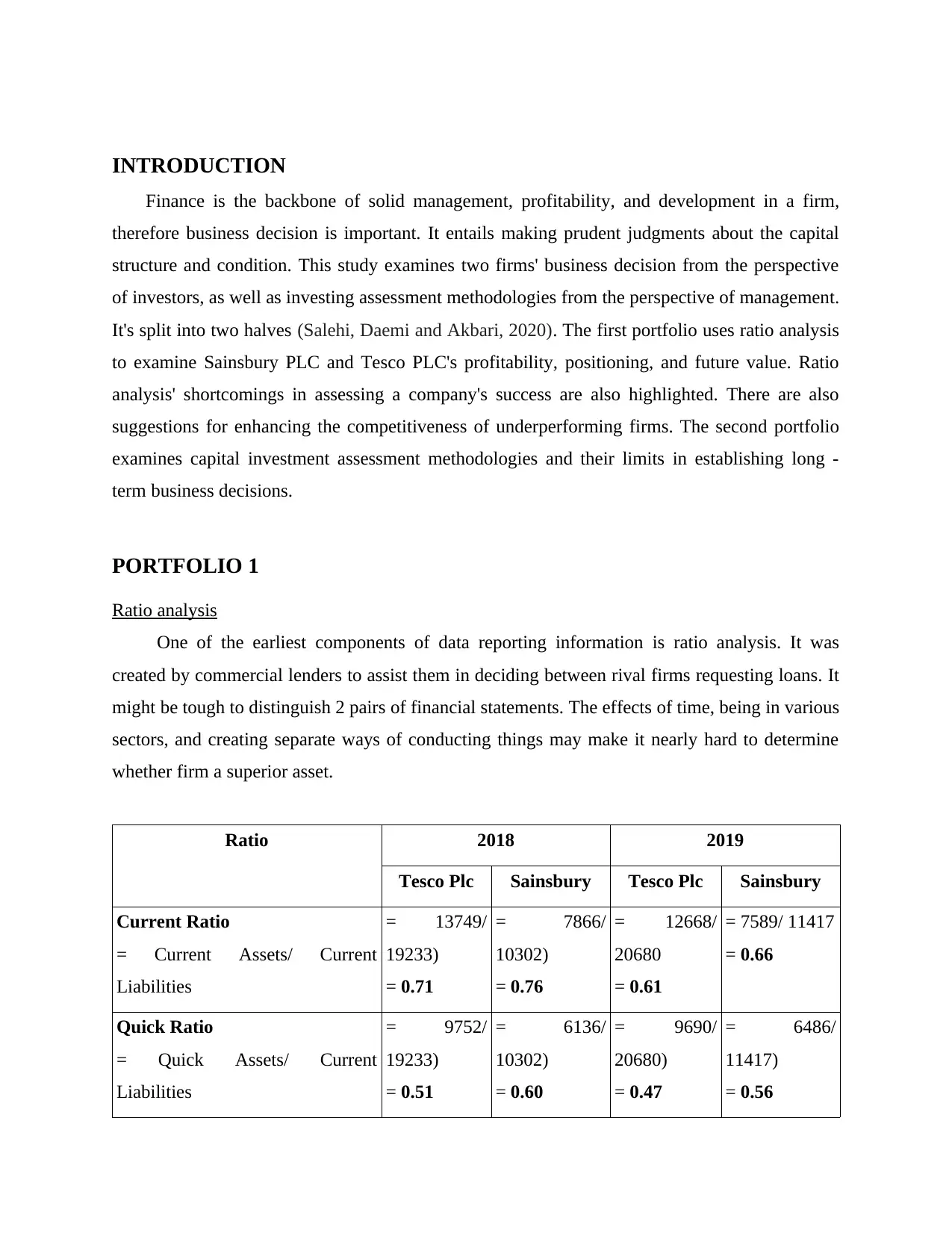

Ratio analysis

One of the earliest components of data reporting information is ratio analysis. It was

created by commercial lenders to assist them in deciding between rival firms requesting loans. It

might be tough to distinguish 2 pairs of financial statements. The effects of time, being in various

sectors, and creating separate ways of conducting things may make it nearly hard to determine

whether firm a superior asset.

Ratio 2018 2019

Tesco Plc Sainsbury Tesco Plc Sainsbury

Current Ratio

= Current Assets/ Current

Liabilities

= 13749/

19233)

= 0.71

= 7866/

10302)

= 0.76

= 12668/

20680

= 0.61

= 7589/ 11417

= 0.66

Quick Ratio

= Quick Assets/ Current

Liabilities

= 9752/

19233)

= 0.51

= 6136/

10302)

= 0.60

= 9690/

20680)

= 0.47

= 6486/

11417)

= 0.56

Finance is the backbone of solid management, profitability, and development in a firm,

therefore business decision is important. It entails making prudent judgments about the capital

structure and condition. This study examines two firms' business decision from the perspective

of investors, as well as investing assessment methodologies from the perspective of management.

It's split into two halves (Salehi, Daemi and Akbari, 2020). The first portfolio uses ratio analysis

to examine Sainsbury PLC and Tesco PLC's profitability, positioning, and future value. Ratio

analysis' shortcomings in assessing a company's success are also highlighted. There are also

suggestions for enhancing the competitiveness of underperforming firms. The second portfolio

examines capital investment assessment methodologies and their limits in establishing long -

term business decisions.

PORTFOLIO 1

Ratio analysis

One of the earliest components of data reporting information is ratio analysis. It was

created by commercial lenders to assist them in deciding between rival firms requesting loans. It

might be tough to distinguish 2 pairs of financial statements. The effects of time, being in various

sectors, and creating separate ways of conducting things may make it nearly hard to determine

whether firm a superior asset.

Ratio 2018 2019

Tesco Plc Sainsbury Tesco Plc Sainsbury

Current Ratio

= Current Assets/ Current

Liabilities

= 13749/

19233)

= 0.71

= 7866/

10302)

= 0.76

= 12668/

20680

= 0.61

= 7589/ 11417

= 0.66

Quick Ratio

= Quick Assets/ Current

Liabilities

= 9752/

19233)

= 0.51

= 6136/

10302)

= 0.60

= 9690/

20680)

= 0.47

= 6486/

11417)

= 0.56

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

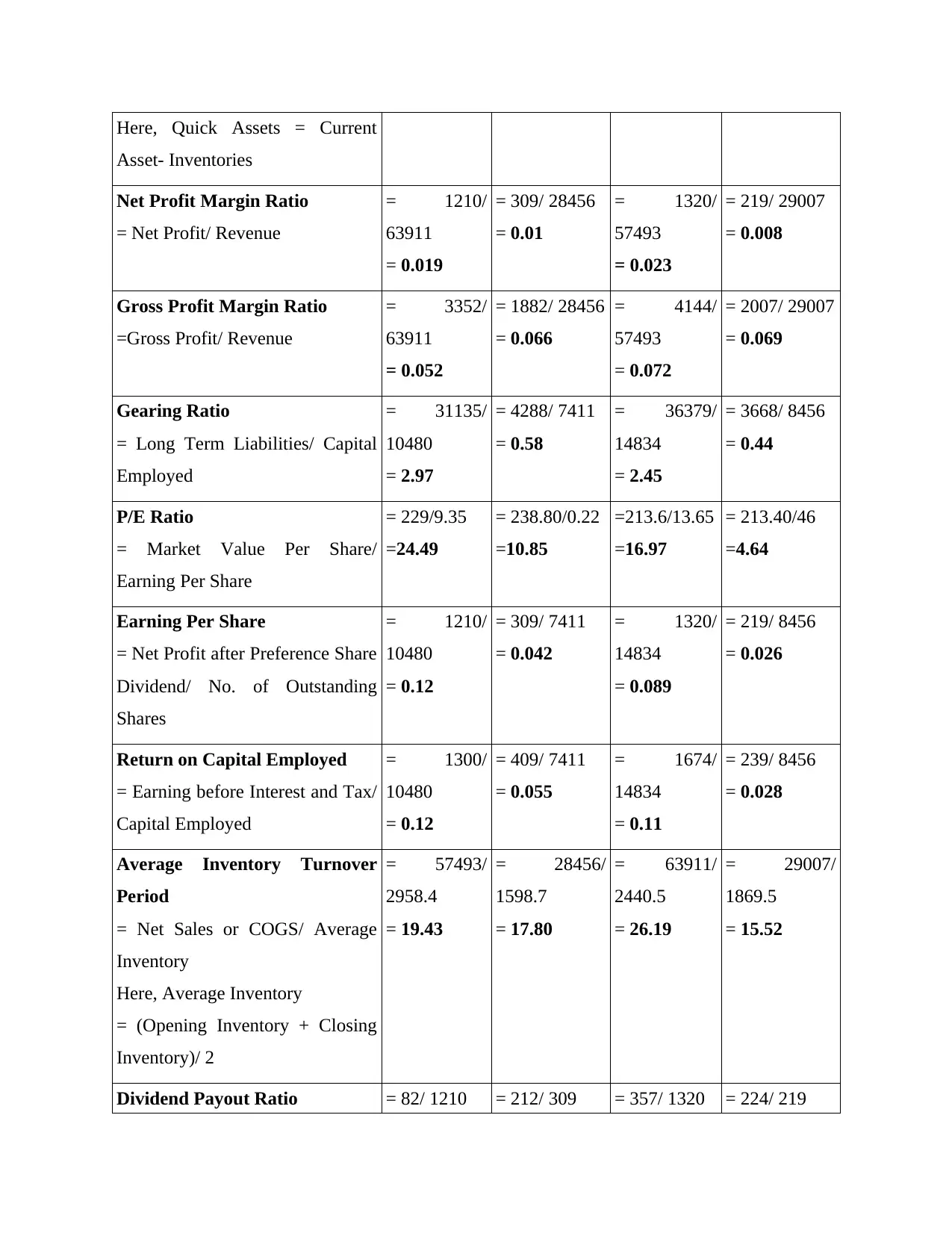

Here, Quick Assets = Current

Asset- Inventories

Net Profit Margin Ratio

= Net Profit/ Revenue

= 1210/

63911

= 0.019

= 309/ 28456

= 0.01

= 1320/

57493

= 0.023

= 219/ 29007

= 0.008

Gross Profit Margin Ratio

=Gross Profit/ Revenue

= 3352/

63911

= 0.052

= 1882/ 28456

= 0.066

= 4144/

57493

= 0.072

= 2007/ 29007

= 0.069

Gearing Ratio

= Long Term Liabilities/ Capital

Employed

= 31135/

10480

= 2.97

= 4288/ 7411

= 0.58

= 36379/

14834

= 2.45

= 3668/ 8456

= 0.44

P/E Ratio

= Market Value Per Share/

Earning Per Share

= 229/9.35

=24.49

= 238.80/0.22

=10.85

=213.6/13.65

=16.97

= 213.40/46

=4.64

Earning Per Share

= Net Profit after Preference Share

Dividend/ No. of Outstanding

Shares

= 1210/

10480

= 0.12

= 309/ 7411

= 0.042

= 1320/

14834

= 0.089

= 219/ 8456

= 0.026

Return on Capital Employed

= Earning before Interest and Tax/

Capital Employed

= 1300/

10480

= 0.12

= 409/ 7411

= 0.055

= 1674/

14834

= 0.11

= 239/ 8456

= 0.028

Average Inventory Turnover

Period

= Net Sales or COGS/ Average

Inventory

Here, Average Inventory

= (Opening Inventory + Closing

Inventory)/ 2

= 57493/

2958.4

= 19.43

= 28456/

1598.7

= 17.80

= 63911/

2440.5

= 26.19

= 29007/

1869.5

= 15.52

Dividend Payout Ratio = 82/ 1210 = 212/ 309 = 357/ 1320 = 224/ 219

Asset- Inventories

Net Profit Margin Ratio

= Net Profit/ Revenue

= 1210/

63911

= 0.019

= 309/ 28456

= 0.01

= 1320/

57493

= 0.023

= 219/ 29007

= 0.008

Gross Profit Margin Ratio

=Gross Profit/ Revenue

= 3352/

63911

= 0.052

= 1882/ 28456

= 0.066

= 4144/

57493

= 0.072

= 2007/ 29007

= 0.069

Gearing Ratio

= Long Term Liabilities/ Capital

Employed

= 31135/

10480

= 2.97

= 4288/ 7411

= 0.58

= 36379/

14834

= 2.45

= 3668/ 8456

= 0.44

P/E Ratio

= Market Value Per Share/

Earning Per Share

= 229/9.35

=24.49

= 238.80/0.22

=10.85

=213.6/13.65

=16.97

= 213.40/46

=4.64

Earning Per Share

= Net Profit after Preference Share

Dividend/ No. of Outstanding

Shares

= 1210/

10480

= 0.12

= 309/ 7411

= 0.042

= 1320/

14834

= 0.089

= 219/ 8456

= 0.026

Return on Capital Employed

= Earning before Interest and Tax/

Capital Employed

= 1300/

10480

= 0.12

= 409/ 7411

= 0.055

= 1674/

14834

= 0.11

= 239/ 8456

= 0.028

Average Inventory Turnover

Period

= Net Sales or COGS/ Average

Inventory

Here, Average Inventory

= (Opening Inventory + Closing

Inventory)/ 2

= 57493/

2958.4

= 19.43

= 28456/

1598.7

= 17.80

= 63911/

2440.5

= 26.19

= 29007/

1869.5

= 15.52

Dividend Payout Ratio = 82/ 1210 = 212/ 309 = 357/ 1320 = 224/ 219

= Dividend Paid/ Net Income = 0.068 = 0.69

= 0.27

= 1.02

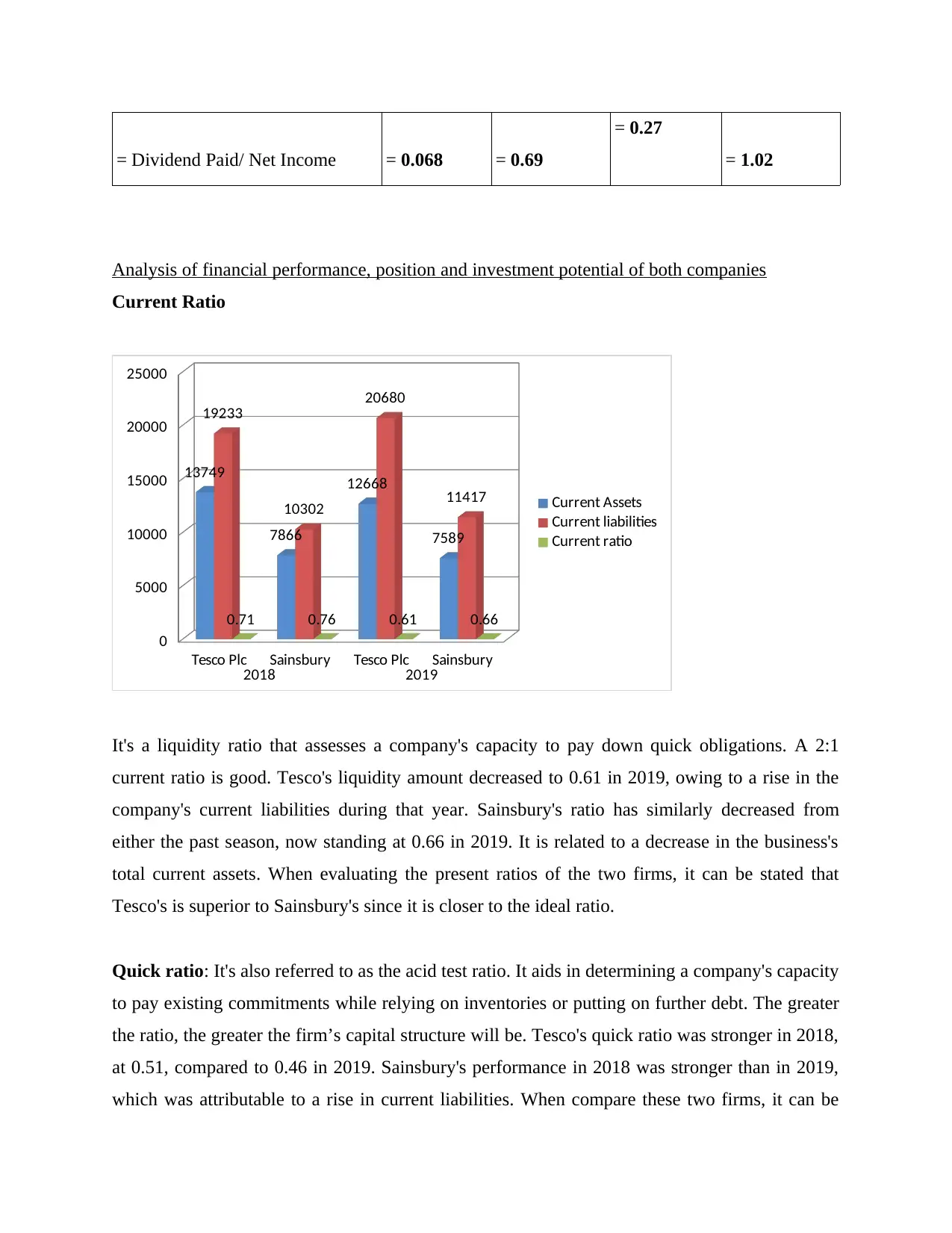

Analysis of financial performance, position and investment potential of both companies

Current Ratio

Tesco Plc Sainsbury Tesco Plc Sainsbury

2018 2019

0

5000

10000

15000

20000

25000

13749

7866

12668

7589

19233

10302

20680

11417

0.71 0.76 0.61 0.66

Current Assets

Current liabilities

Current ratio

It's a liquidity ratio that assesses a company's capacity to pay down quick obligations. A 2:1

current ratio is good. Tesco's liquidity amount decreased to 0.61 in 2019, owing to a rise in the

company's current liabilities during that year. Sainsbury's ratio has similarly decreased from

either the past season, now standing at 0.66 in 2019. It is related to a decrease in the business's

total current assets. When evaluating the present ratios of the two firms, it can be stated that

Tesco's is superior to Sainsbury's since it is closer to the ideal ratio.

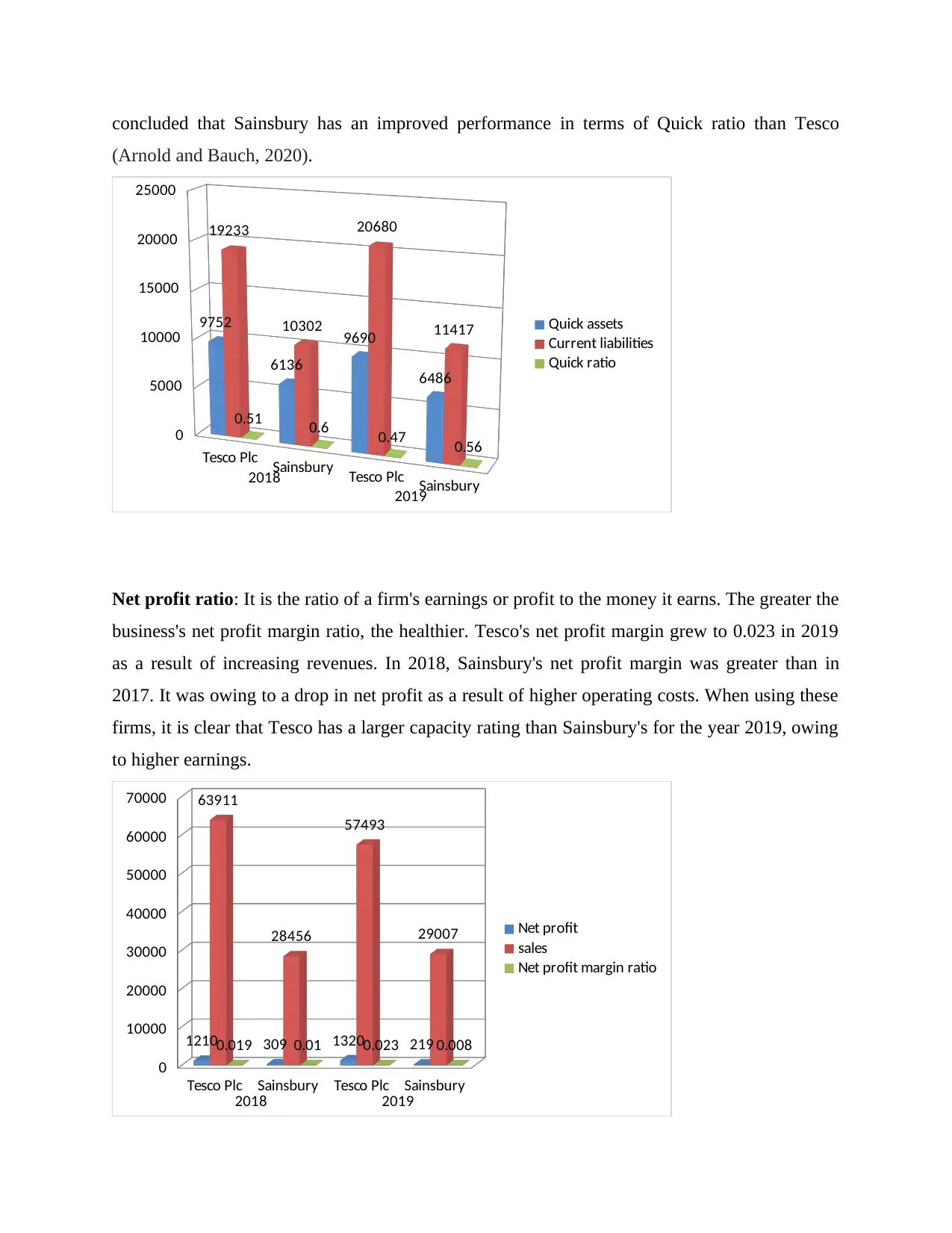

Quick ratio: It's also referred to as the acid test ratio. It aids in determining a company's capacity

to pay existing commitments while relying on inventories or putting on further debt. The greater

the ratio, the greater the firm’s capital structure will be. Tesco's quick ratio was stronger in 2018,

at 0.51, compared to 0.46 in 2019. Sainsbury's performance in 2018 was stronger than in 2019,

which was attributable to a rise in current liabilities. When compare these two firms, it can be

= 0.27

= 1.02

Analysis of financial performance, position and investment potential of both companies

Current Ratio

Tesco Plc Sainsbury Tesco Plc Sainsbury

2018 2019

0

5000

10000

15000

20000

25000

13749

7866

12668

7589

19233

10302

20680

11417

0.71 0.76 0.61 0.66

Current Assets

Current liabilities

Current ratio

It's a liquidity ratio that assesses a company's capacity to pay down quick obligations. A 2:1

current ratio is good. Tesco's liquidity amount decreased to 0.61 in 2019, owing to a rise in the

company's current liabilities during that year. Sainsbury's ratio has similarly decreased from

either the past season, now standing at 0.66 in 2019. It is related to a decrease in the business's

total current assets. When evaluating the present ratios of the two firms, it can be stated that

Tesco's is superior to Sainsbury's since it is closer to the ideal ratio.

Quick ratio: It's also referred to as the acid test ratio. It aids in determining a company's capacity

to pay existing commitments while relying on inventories or putting on further debt. The greater

the ratio, the greater the firm’s capital structure will be. Tesco's quick ratio was stronger in 2018,

at 0.51, compared to 0.46 in 2019. Sainsbury's performance in 2018 was stronger than in 2019,

which was attributable to a rise in current liabilities. When compare these two firms, it can be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

concluded that Sainsbury has an improved performance in terms of Quick ratio than Tesco

(Arnold and Bauch, 2020).

Tesco Plc Sainsbury Tesco Plc Sainsbury

2018

2019

0

5000

10000

15000

20000

25000

9752

6136

9690

6486

19233

10302

20680

11417

0.51 0.6 0.47 0.56

Quick assets

Current liabilities

Quick ratio

Net profit ratio: It is the ratio of a firm's earnings or profit to the money it earns. The greater the

business's net profit margin ratio, the healthier. Tesco's net profit margin grew to 0.023 in 2019

as a result of increasing revenues. In 2018, Sainsbury's net profit margin was greater than in

2017. It was owing to a drop in net profit as a result of higher operating costs. When using these

firms, it is clear that Tesco has a larger capacity rating than Sainsbury's for the year 2019, owing

to higher earnings.

Tesco Plc Sainsbury Tesco Plc Sainsbury

2018 2019

0

10000

20000

30000

40000

50000

60000

70000

1210 309 1320 219

63911

28456

57493

29007

0.019 0.01 0.023 0.008

Net profit

sales

Net profit margin ratio

(Arnold and Bauch, 2020).

Tesco Plc Sainsbury Tesco Plc Sainsbury

2018

2019

0

5000

10000

15000

20000

25000

9752

6136

9690

6486

19233

10302

20680

11417

0.51 0.6 0.47 0.56

Quick assets

Current liabilities

Quick ratio

Net profit ratio: It is the ratio of a firm's earnings or profit to the money it earns. The greater the

business's net profit margin ratio, the healthier. Tesco's net profit margin grew to 0.023 in 2019

as a result of increasing revenues. In 2018, Sainsbury's net profit margin was greater than in

2017. It was owing to a drop in net profit as a result of higher operating costs. When using these

firms, it is clear that Tesco has a larger capacity rating than Sainsbury's for the year 2019, owing

to higher earnings.

Tesco Plc Sainsbury Tesco Plc Sainsbury

2018 2019

0

10000

20000

30000

40000

50000

60000

70000

1210 309 1320 219

63911

28456

57493

29007

0.019 0.01 0.023 0.008

Net profit

sales

Net profit margin ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

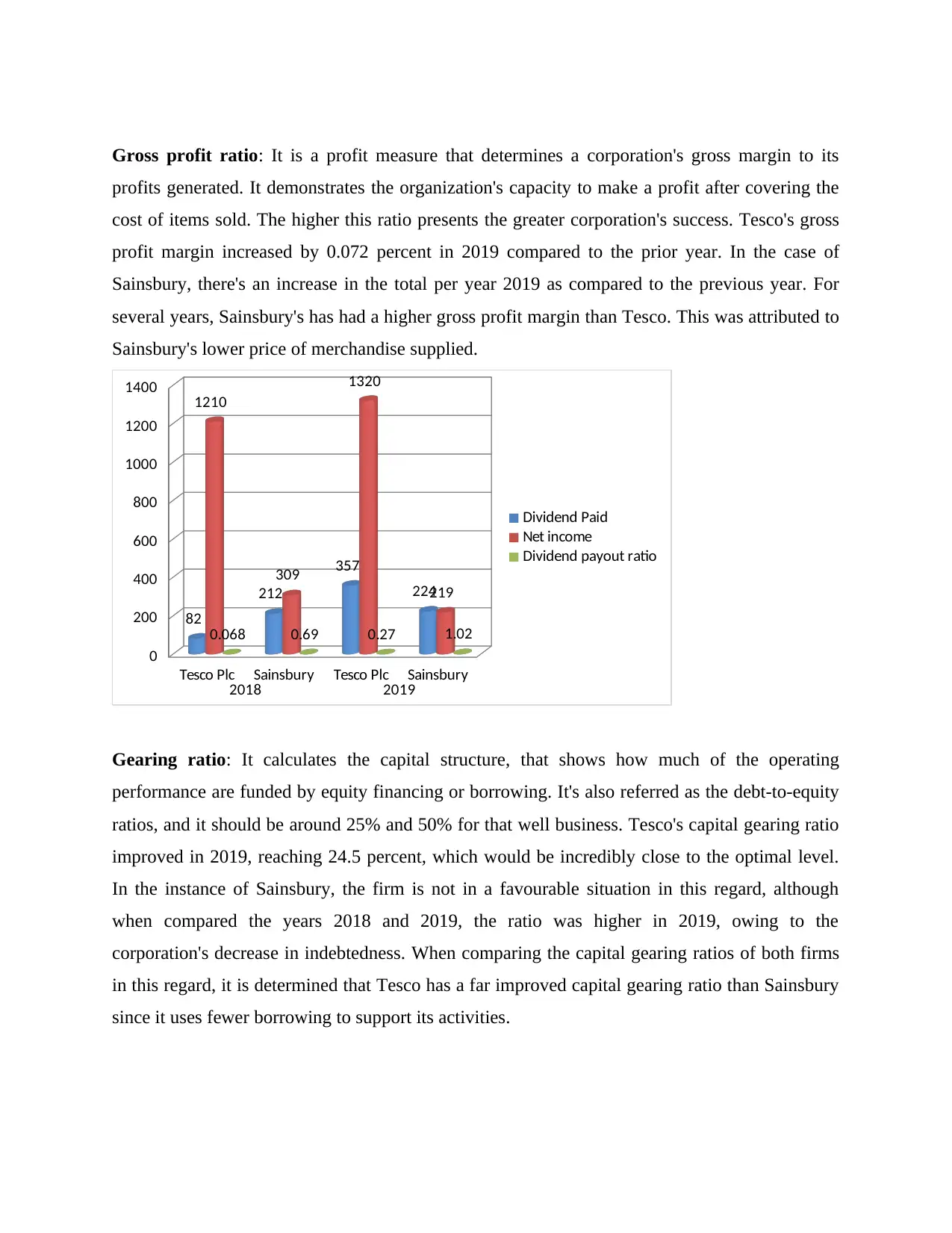

Gross profit ratio: It is a profit measure that determines a corporation's gross margin to its

profits generated. It demonstrates the organization's capacity to make a profit after covering the

cost of items sold. The higher this ratio presents the greater corporation's success. Tesco's gross

profit margin increased by 0.072 percent in 2019 compared to the prior year. In the case of

Sainsbury, there's an increase in the total per year 2019 as compared to the previous year. For

several years, Sainsbury's has had a higher gross profit margin than Tesco. This was attributed to

Sainsbury's lower price of merchandise supplied.

Tesco Plc Sainsbury Tesco Plc Sainsbury

2018 2019

0

200

400

600

800

1000

1200

1400

82

212

357

224

1210

309

1320

219

0.068 0.69 0.27 1.02

Dividend Paid

Net income

Dividend payout ratio

Gearing ratio: It calculates the capital structure, that shows how much of the operating

performance are funded by equity financing or borrowing. It's also referred as the debt-to-equity

ratios, and it should be around 25% and 50% for that well business. Tesco's capital gearing ratio

improved in 2019, reaching 24.5 percent, which would be incredibly close to the optimal level.

In the instance of Sainsbury, the firm is not in a favourable situation in this regard, although

when compared the years 2018 and 2019, the ratio was higher in 2019, owing to the

corporation's decrease in indebtedness. When comparing the capital gearing ratios of both firms

in this regard, it is determined that Tesco has a far improved capital gearing ratio than Sainsbury

since it uses fewer borrowing to support its activities.

profits generated. It demonstrates the organization's capacity to make a profit after covering the

cost of items sold. The higher this ratio presents the greater corporation's success. Tesco's gross

profit margin increased by 0.072 percent in 2019 compared to the prior year. In the case of

Sainsbury, there's an increase in the total per year 2019 as compared to the previous year. For

several years, Sainsbury's has had a higher gross profit margin than Tesco. This was attributed to

Sainsbury's lower price of merchandise supplied.

Tesco Plc Sainsbury Tesco Plc Sainsbury

2018 2019

0

200

400

600

800

1000

1200

1400

82

212

357

224

1210

309

1320

219

0.068 0.69 0.27 1.02

Dividend Paid

Net income

Dividend payout ratio

Gearing ratio: It calculates the capital structure, that shows how much of the operating

performance are funded by equity financing or borrowing. It's also referred as the debt-to-equity

ratios, and it should be around 25% and 50% for that well business. Tesco's capital gearing ratio

improved in 2019, reaching 24.5 percent, which would be incredibly close to the optimal level.

In the instance of Sainsbury, the firm is not in a favourable situation in this regard, although

when compared the years 2018 and 2019, the ratio was higher in 2019, owing to the

corporation's decrease in indebtedness. When comparing the capital gearing ratios of both firms

in this regard, it is determined that Tesco has a far improved capital gearing ratio than Sainsbury

since it uses fewer borrowing to support its activities.

Tesco Plc Sainsbury Tesco Plc Sainsbury

2018 2019

0

5000

10000

15000

20000

25000

30000

35000

40000

31135

4288

36379

3668

10480

7411

14834

8456

Long term liabilities

Capital em[ployed

Gearing ratio

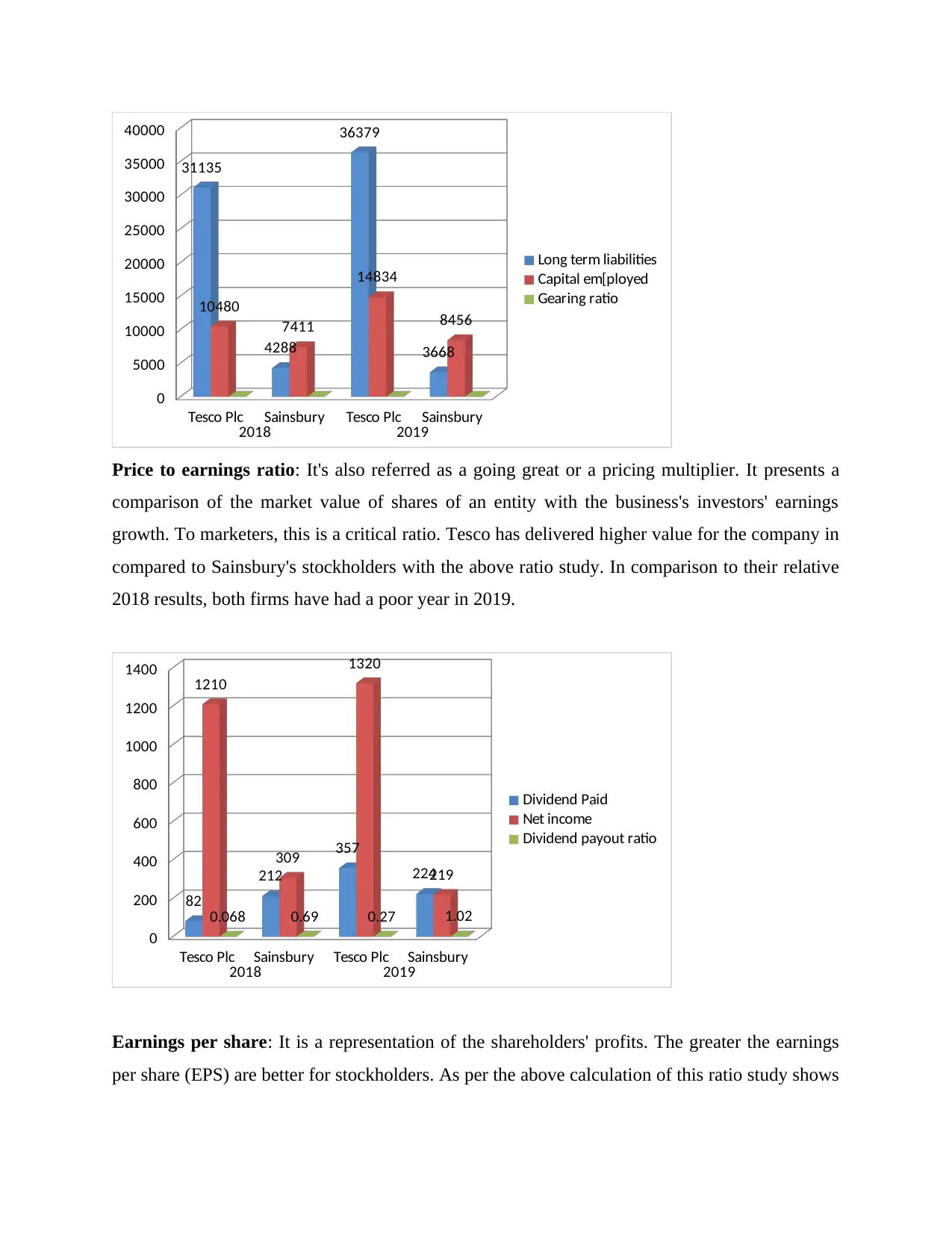

Price to earnings ratio: It's also referred as a going great or a pricing multiplier. It presents a

comparison of the market value of shares of an entity with the business's investors' earnings

growth. To marketers, this is a critical ratio. Tesco has delivered higher value for the company in

compared to Sainsbury's stockholders with the above ratio study. In comparison to their relative

2018 results, both firms have had a poor year in 2019.

Tesco Plc Sainsbury Tesco Plc Sainsbury

2018 2019

0

200

400

600

800

1000

1200

1400

82

212

357

224

1210

309

1320

219

0.068 0.69 0.27 1.02

Dividend Paid

Net income

Dividend payout ratio

Earnings per share: It is a representation of the shareholders' profits. The greater the earnings

per share (EPS) are better for stockholders. As per the above calculation of this ratio study shows

2018 2019

0

5000

10000

15000

20000

25000

30000

35000

40000

31135

4288

36379

3668

10480

7411

14834

8456

Long term liabilities

Capital em[ployed

Gearing ratio

Price to earnings ratio: It's also referred as a going great or a pricing multiplier. It presents a

comparison of the market value of shares of an entity with the business's investors' earnings

growth. To marketers, this is a critical ratio. Tesco has delivered higher value for the company in

compared to Sainsbury's stockholders with the above ratio study. In comparison to their relative

2018 results, both firms have had a poor year in 2019.

Tesco Plc Sainsbury Tesco Plc Sainsbury

2018 2019

0

200

400

600

800

1000

1200

1400

82

212

357

224

1210

309

1320

219

0.068 0.69 0.27 1.02

Dividend Paid

Net income

Dividend payout ratio

Earnings per share: It is a representation of the shareholders' profits. The greater the earnings

per share (EPS) are better for stockholders. As per the above calculation of this ratio study shows

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

that Tesco's EPS is higher than Sainsbury's. In comparison to their relative 2018 results, both

firms have had a poor year in 2019.

Tesco Plc Sainsbury Tesco Plc Sainsbury

2018 2019

0

200

400

600

800

1000

1200

1400

82

212

357

224

1210

309

1320

219

0.068 0.69 0.27 1.02

Dividend Paid

Net income

Dividend payout ratio

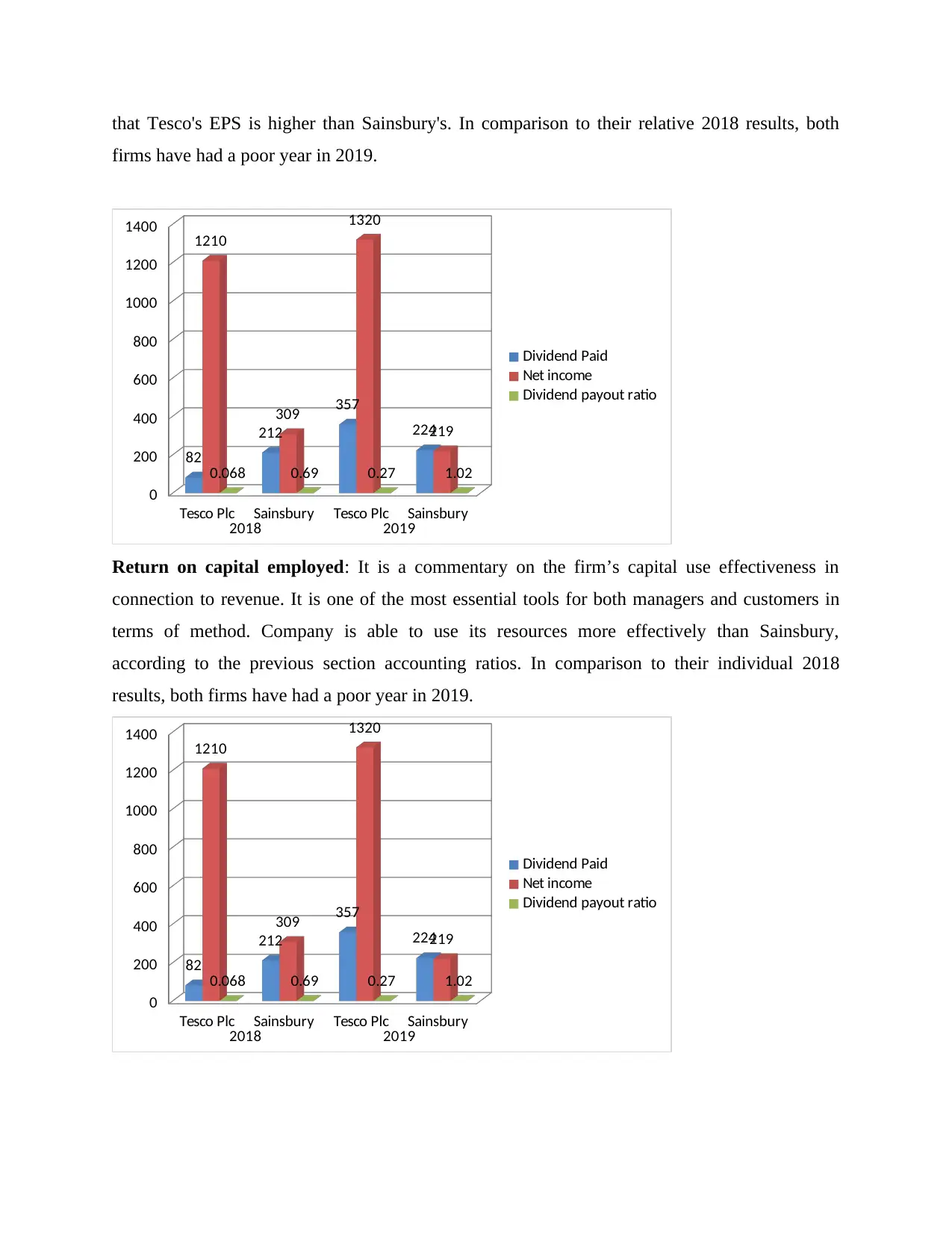

Return on capital employed: It is a commentary on the firm’s capital use effectiveness in

connection to revenue. It is one of the most essential tools for both managers and customers in

terms of method. Company is able to use its resources more effectively than Sainsbury,

according to the previous section accounting ratios. In comparison to their individual 2018

results, both firms have had a poor year in 2019.

Tesco Plc Sainsbury Tesco Plc Sainsbury

2018 2019

0

200

400

600

800

1000

1200

1400

82

212

357

224

1210

309

1320

219

0.068 0.69 0.27 1.02

Dividend Paid

Net income

Dividend payout ratio

firms have had a poor year in 2019.

Tesco Plc Sainsbury Tesco Plc Sainsbury

2018 2019

0

200

400

600

800

1000

1200

1400

82

212

357

224

1210

309

1320

219

0.068 0.69 0.27 1.02

Dividend Paid

Net income

Dividend payout ratio

Return on capital employed: It is a commentary on the firm’s capital use effectiveness in

connection to revenue. It is one of the most essential tools for both managers and customers in

terms of method. Company is able to use its resources more effectively than Sainsbury,

according to the previous section accounting ratios. In comparison to their individual 2018

results, both firms have had a poor year in 2019.

Tesco Plc Sainsbury Tesco Plc Sainsbury

2018 2019

0

200

400

600

800

1000

1200

1400

82

212

357

224

1210

309

1320

219

0.068 0.69 0.27 1.02

Dividend Paid

Net income

Dividend payout ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

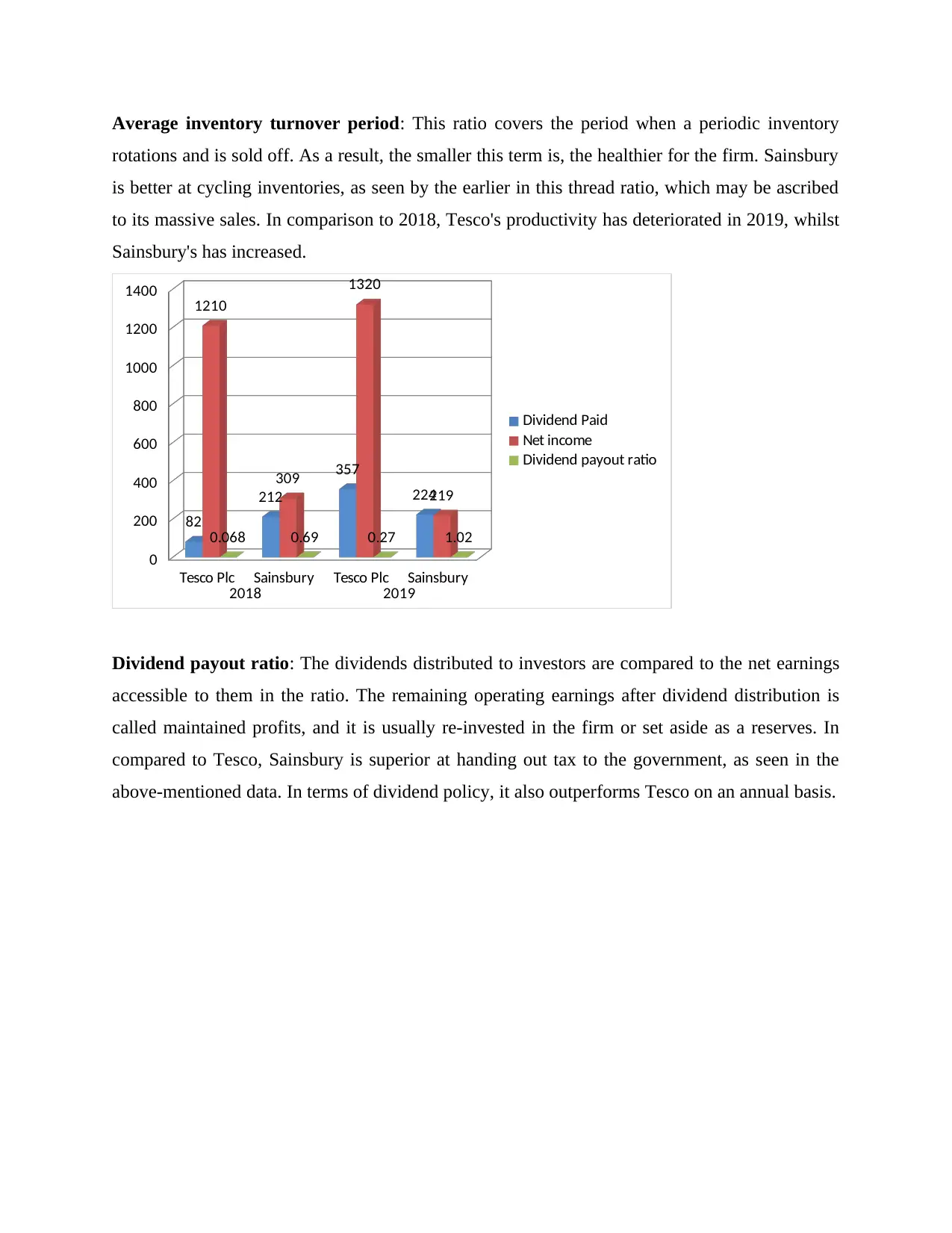

Average inventory turnover period: This ratio covers the period when a periodic inventory

rotations and is sold off. As a result, the smaller this term is, the healthier for the firm. Sainsbury

is better at cycling inventories, as seen by the earlier in this thread ratio, which may be ascribed

to its massive sales. In comparison to 2018, Tesco's productivity has deteriorated in 2019, whilst

Sainsbury's has increased.

Tesco Plc Sainsbury Tesco Plc Sainsbury

2018 2019

0

200

400

600

800

1000

1200

1400

82

212

357

224

1210

309

1320

219

0.068 0.69 0.27 1.02

Dividend Paid

Net income

Dividend payout ratio

Dividend payout ratio: The dividends distributed to investors are compared to the net earnings

accessible to them in the ratio. The remaining operating earnings after dividend distribution is

called maintained profits, and it is usually re-invested in the firm or set aside as a reserves. In

compared to Tesco, Sainsbury is superior at handing out tax to the government, as seen in the

above-mentioned data. In terms of dividend policy, it also outperforms Tesco on an annual basis.

rotations and is sold off. As a result, the smaller this term is, the healthier for the firm. Sainsbury

is better at cycling inventories, as seen by the earlier in this thread ratio, which may be ascribed

to its massive sales. In comparison to 2018, Tesco's productivity has deteriorated in 2019, whilst

Sainsbury's has increased.

Tesco Plc Sainsbury Tesco Plc Sainsbury

2018 2019

0

200

400

600

800

1000

1200

1400

82

212

357

224

1210

309

1320

219

0.068 0.69 0.27 1.02

Dividend Paid

Net income

Dividend payout ratio

Dividend payout ratio: The dividends distributed to investors are compared to the net earnings

accessible to them in the ratio. The remaining operating earnings after dividend distribution is

called maintained profits, and it is usually re-invested in the firm or set aside as a reserves. In

compared to Tesco, Sainsbury is superior at handing out tax to the government, as seen in the

above-mentioned data. In terms of dividend policy, it also outperforms Tesco on an annual basis.

Tesco Plc Sainsbury Tesco Plc Sainsbury

2018 2019

0

200

400

600

800

1000

1200

1400

82

212

357

224

1210

309

1320

219

0.068 0.69 0.27 1.02

Dividend Paid

Net income

Dividend payout ratio

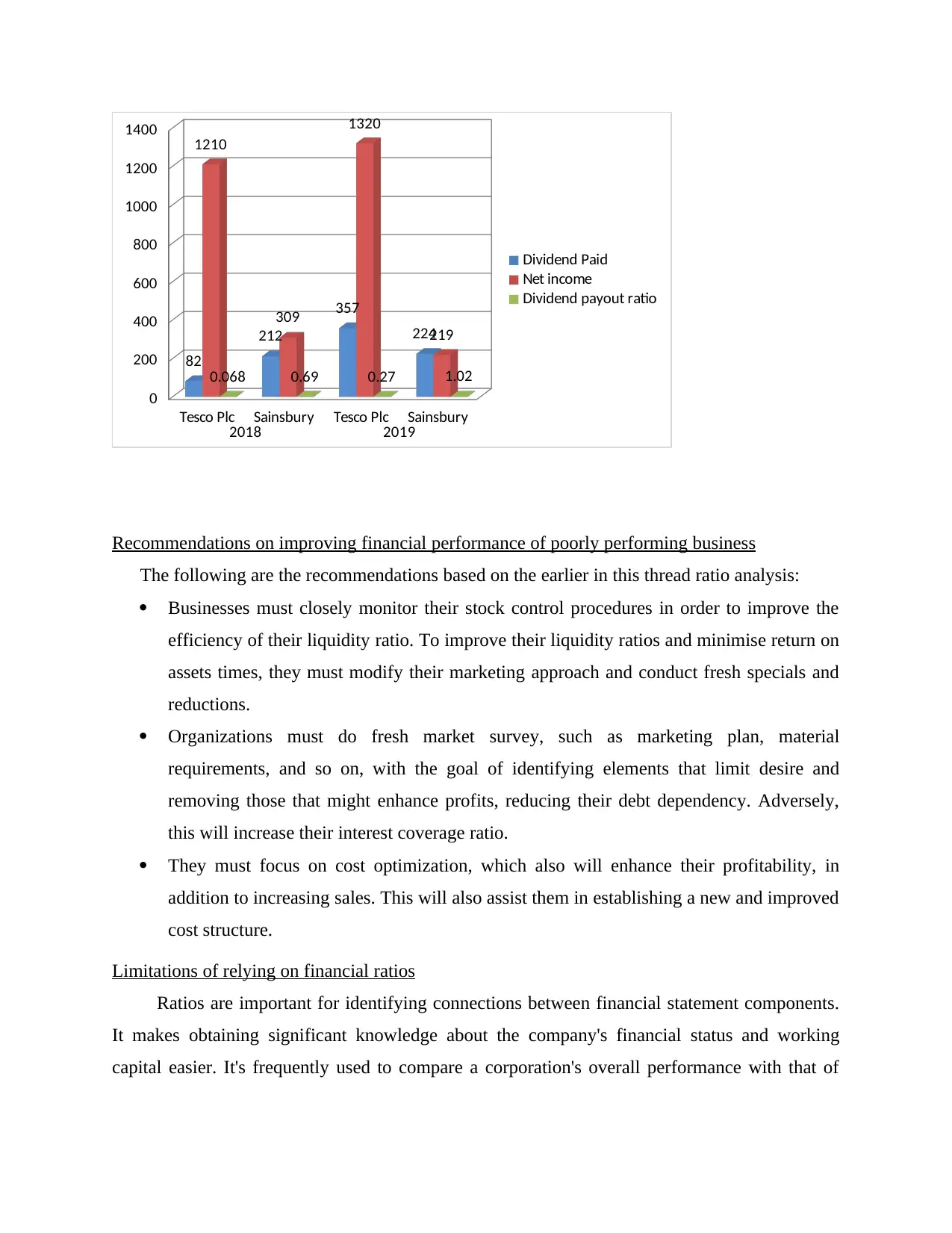

Recommendations on improving financial performance of poorly performing business

The following are the recommendations based on the earlier in this thread ratio analysis:

Businesses must closely monitor their stock control procedures in order to improve the

efficiency of their liquidity ratio. To improve their liquidity ratios and minimise return on

assets times, they must modify their marketing approach and conduct fresh specials and

reductions.

Organizations must do fresh market survey, such as marketing plan, material

requirements, and so on, with the goal of identifying elements that limit desire and

removing those that might enhance profits, reducing their debt dependency. Adversely,

this will increase their interest coverage ratio.

They must focus on cost optimization, which also will enhance their profitability, in

addition to increasing sales. This will also assist them in establishing a new and improved

cost structure.

Limitations of relying on financial ratios

Ratios are important for identifying connections between financial statement components.

It makes obtaining significant knowledge about the company's financial status and working

capital easier. It's frequently used to compare a corporation's overall performance with that of

2018 2019

0

200

400

600

800

1000

1200

1400

82

212

357

224

1210

309

1320

219

0.068 0.69 0.27 1.02

Dividend Paid

Net income

Dividend payout ratio

Recommendations on improving financial performance of poorly performing business

The following are the recommendations based on the earlier in this thread ratio analysis:

Businesses must closely monitor their stock control procedures in order to improve the

efficiency of their liquidity ratio. To improve their liquidity ratios and minimise return on

assets times, they must modify their marketing approach and conduct fresh specials and

reductions.

Organizations must do fresh market survey, such as marketing plan, material

requirements, and so on, with the goal of identifying elements that limit desire and

removing those that might enhance profits, reducing their debt dependency. Adversely,

this will increase their interest coverage ratio.

They must focus on cost optimization, which also will enhance their profitability, in

addition to increasing sales. This will also assist them in establishing a new and improved

cost structure.

Limitations of relying on financial ratios

Ratios are important for identifying connections between financial statement components.

It makes obtaining significant knowledge about the company's financial status and working

capital easier. It's frequently used to compare a corporation's overall performance with that of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.