ACC506 Task 2B: Investment Analysis and Capital Budgeting Report

VerifiedAdded on 2023/06/15

|12

|2128

|142

Report

AI Summary

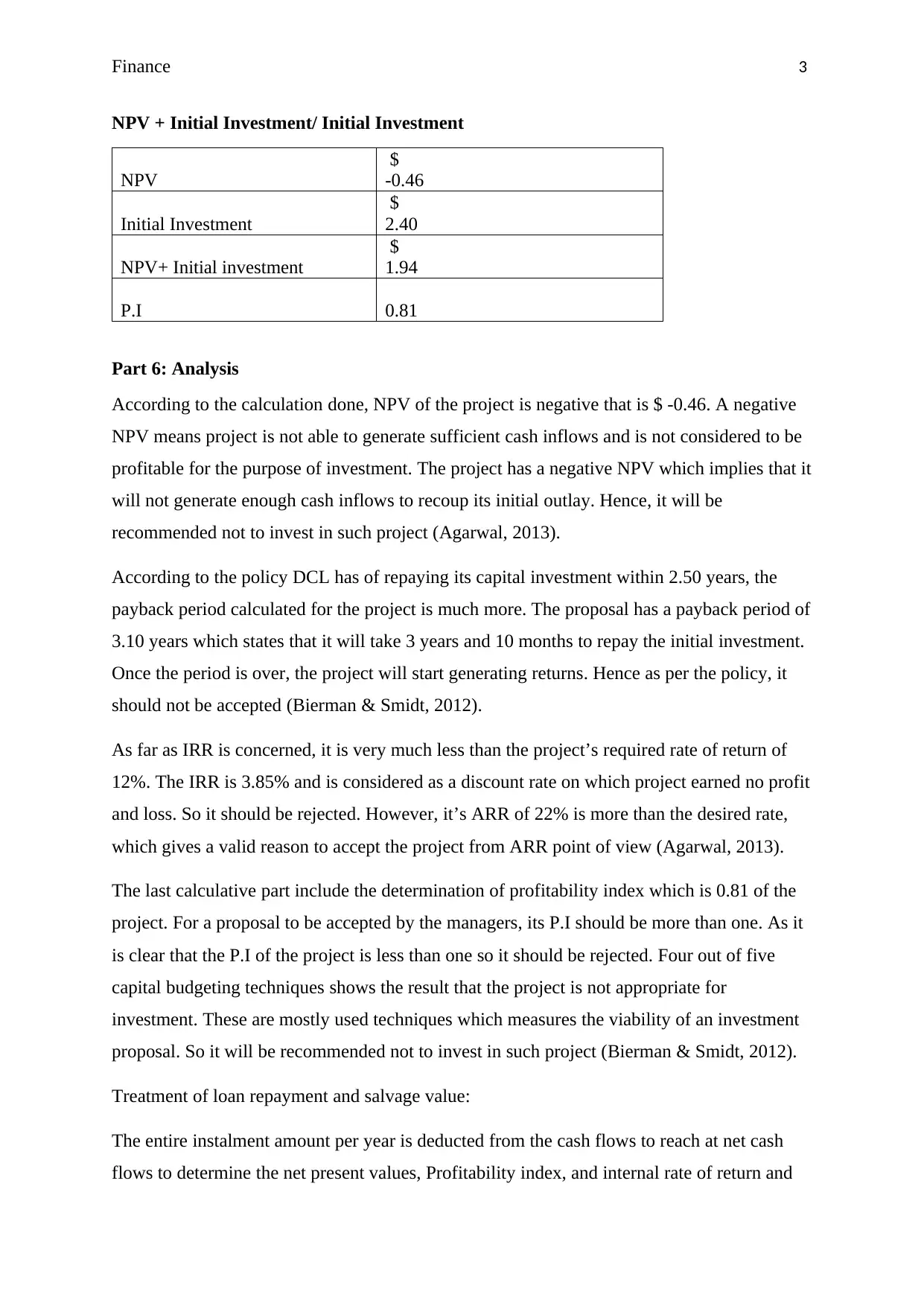

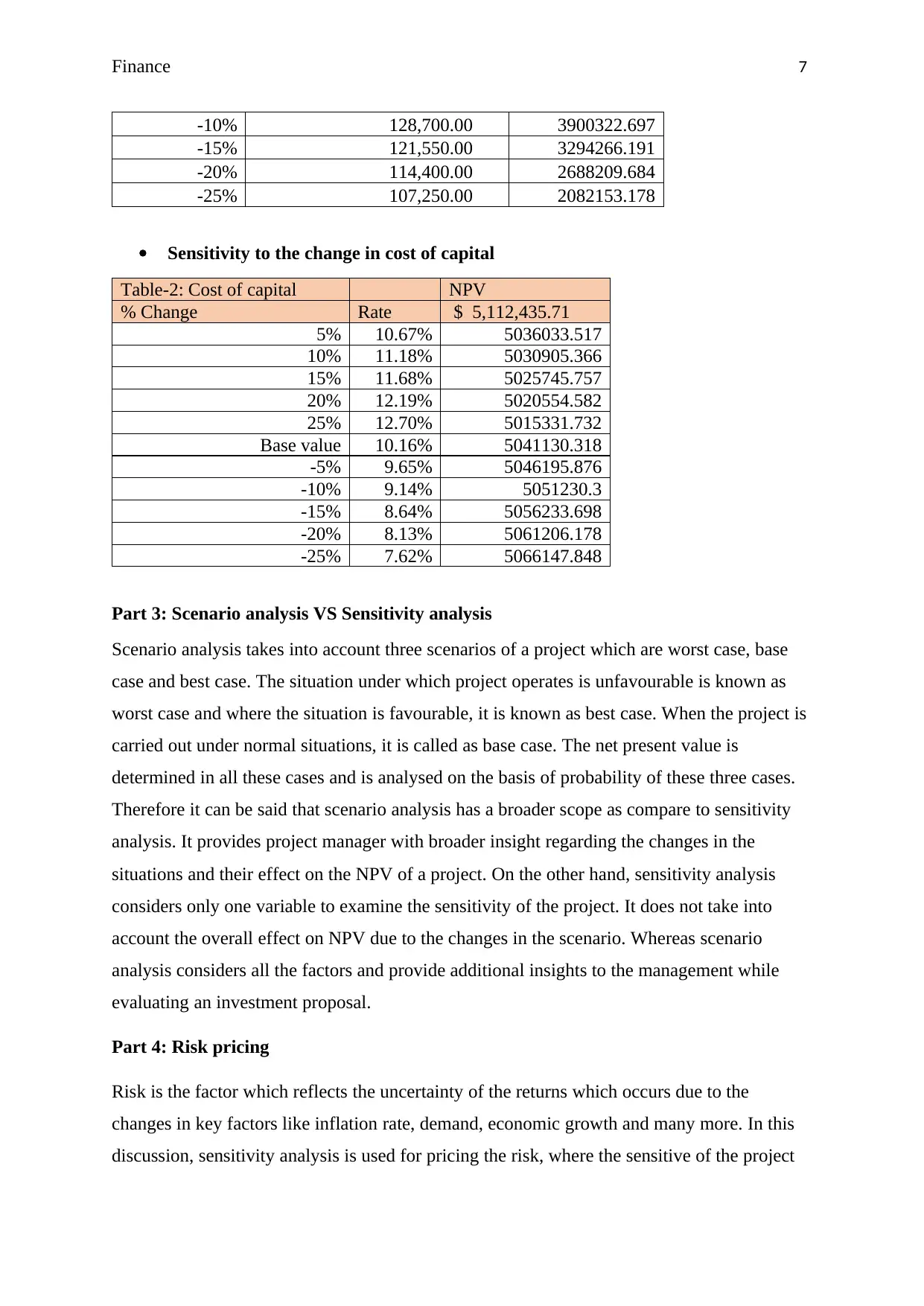

This report provides a detailed analysis of investment and capital budgeting techniques, including Net Present Value (NPV), Internal Rate of Return (IRR), Payback Period, Average Rate of Return (ARR), and Profitability Index (PI). It evaluates a project's financial viability using these methods, considering factors like cash flows, loan repayments, and salvage value. The report also includes a sensitivity analysis to assess the impact of changes in sales units and cost of capital on the project's NPV, along with a scenario analysis comparing worst-case, base-case, and best-case scenarios. The analysis concludes with a discussion on risk pricing and its relationship to the project's NPV. Additionally, the report addresses the treatment of loan repayments and salvage value in financial calculations. A second question examines the calculation of cash flows after tax and NPV evaluation along with sensitivity and scenario analysis.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.