Financial Analysis of Sports Retail Firms

VerifiedAdded on 2020/06/06

|20

|4942

|34

AI Summary

This assignment focuses on the financial analysis of two sports retail firms: JD Sports Fashion Plc and Sports Direct International Plc. It requires students to utilize various financial ratios to evaluate the firms' performance, profitability, liquidity, and solvency. The assignment also delves into the concept of capital budgeting, examining its importance in investment decisions for these companies. Students will analyze the advantages and disadvantages of different capital budgeting methods and apply them to real-world scenarios within the sports retail industry.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGERIAL FINANCE

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

PORTFOLIO 1.................................................................................................................................1

Question 1...............................................................................................................................1

A) Calculating financial ratios of two companies for two accounting periods i.e. 2015 and

2016........................................................................................................................................1

B) Analysing performance, financial condition and investment potential of Sports Direct and

JD Sports firms.......................................................................................................................4

C) Providing appropriate suggestions to the firm which has poor financial performance...11

D) Discussing drawbacks of financial ratios which used to analyse firm's performance....11

PORTFOLIO 2...............................................................................................................................12

Question 2.............................................................................................................................12

A) Use of basic investment appraisal methods and suggestions to management of a local

manufacturing enterprise......................................................................................................12

B) Discussing limitations associated with investment appraisal technique for taking long-term

decisions...............................................................................................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................1

PORTFOLIO 1.................................................................................................................................1

Question 1...............................................................................................................................1

A) Calculating financial ratios of two companies for two accounting periods i.e. 2015 and

2016........................................................................................................................................1

B) Analysing performance, financial condition and investment potential of Sports Direct and

JD Sports firms.......................................................................................................................4

C) Providing appropriate suggestions to the firm which has poor financial performance...11

D) Discussing drawbacks of financial ratios which used to analyse firm's performance....11

PORTFOLIO 2...............................................................................................................................12

Question 2.............................................................................................................................12

A) Use of basic investment appraisal methods and suggestions to management of a local

manufacturing enterprise......................................................................................................12

B) Discussing limitations associated with investment appraisal technique for taking long-term

decisions...............................................................................................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Finance is considered as blood for every organisation because it helps to exist and operate

in the industry. Due to unavailability of financial resources, an entrepreneur unable to establish

its business in the market and sale products and services. The present project reflects about some

methods which help to assess financial information and make profitable investments. For

measuring the business performance, two companies are taken into consideration i.e. Sports

Direct International Plc. and JD Sports Fashion Plc. Both these firms operate in apparel industry

and have a huge market presence. Further, using some financial ratios, financial condition,

performance as well as investment potential are analysed. Under the second part of present

assignment, investment appraisal methods i.e. NPV, ARR and payback period are calculated for

local manufacturing company. On the basis of these tools, suggestions to the management for

making fruitful investment are to be given.

PORTFOLIO 1

Question 1

A) Calculating financial ratios of two companies for two accounting periods i.e. 2015 and 2016

2015 2016

Name of

financial ratios Formula

Sports Direct

International

Plc.

JD Sports

Fashion Plc.

Sports Direct

International

Plc.

JD Sports

Fashion

Plc.

Current assets

(CA) 878297 400259 1311437 510695

Current liabilities

(CL) 382621 326748 540608 348154

Current ratios

(CR) CA / CL 2.30 1.22 2.43 1.47

Current assets

(CA) 878297 400259 1311437 510695

1

Finance is considered as blood for every organisation because it helps to exist and operate

in the industry. Due to unavailability of financial resources, an entrepreneur unable to establish

its business in the market and sale products and services. The present project reflects about some

methods which help to assess financial information and make profitable investments. For

measuring the business performance, two companies are taken into consideration i.e. Sports

Direct International Plc. and JD Sports Fashion Plc. Both these firms operate in apparel industry

and have a huge market presence. Further, using some financial ratios, financial condition,

performance as well as investment potential are analysed. Under the second part of present

assignment, investment appraisal methods i.e. NPV, ARR and payback period are calculated for

local manufacturing company. On the basis of these tools, suggestions to the management for

making fruitful investment are to be given.

PORTFOLIO 1

Question 1

A) Calculating financial ratios of two companies for two accounting periods i.e. 2015 and 2016

2015 2016

Name of

financial ratios Formula

Sports Direct

International

Plc.

JD Sports

Fashion Plc.

Sports Direct

International

Plc.

JD Sports

Fashion

Plc.

Current assets

(CA) 878297 400259 1311437 510695

Current liabilities

(CL) 382621 326748 540608 348154

Current ratios

(CR) CA / CL 2.30 1.22 2.43 1.47

Current assets

(CA) 878297 400259 1311437 510695

1

Current liabilities

(CL) 382621 326748 540608 348154

Stock 517054 91024 702158 106336

Prepaid expenses 0 0 0 0

Quick ratios

(QR)

CA – (stock +

prepaid

expenses) / CL 0.94 0.53 1.13 0.78

Gross profit (GP) 1240812 739550 1284644 884221

Net sales 2832560 1522253 2904325 1821652

Gross profit

ratio

GP / net sales *

100 43.81% 48.58% 44.23% 48.54%

Operating profit

(OP) 8345 92646 11137 133406

Net sales 2832560 1522253 2904325 1821652

Operating profit

ratio

OP / net sales *

100 10.44% 6.09% 7.68% 7.32%

Net profit (NP) 241353 53971 278981 100630

Net sales 2832560 1522253 2904325 1821652

Net profit ratio

NP / net sales *

100 8.52% 3.55% 9.61% 5.52%

Debt 136849 -374 333063 -247

2

(CL) 382621 326748 540608 348154

Stock 517054 91024 702158 106336

Prepaid expenses 0 0 0 0

Quick ratios

(QR)

CA – (stock +

prepaid

expenses) / CL 0.94 0.53 1.13 0.78

Gross profit (GP) 1240812 739550 1284644 884221

Net sales 2832560 1522253 2904325 1821652

Gross profit

ratio

GP / net sales *

100 43.81% 48.58% 44.23% 48.54%

Operating profit

(OP) 8345 92646 11137 133406

Net sales 2832560 1522253 2904325 1821652

Operating profit

ratio

OP / net sales *

100 10.44% 6.09% 7.68% 7.32%

Net profit (NP) 241353 53971 278981 100630

Net sales 2832560 1522253 2904325 1821652

Net profit ratio

NP / net sales *

100 8.52% 3.55% 9.61% 5.52%

Debt 136849 -374 333063 -247

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

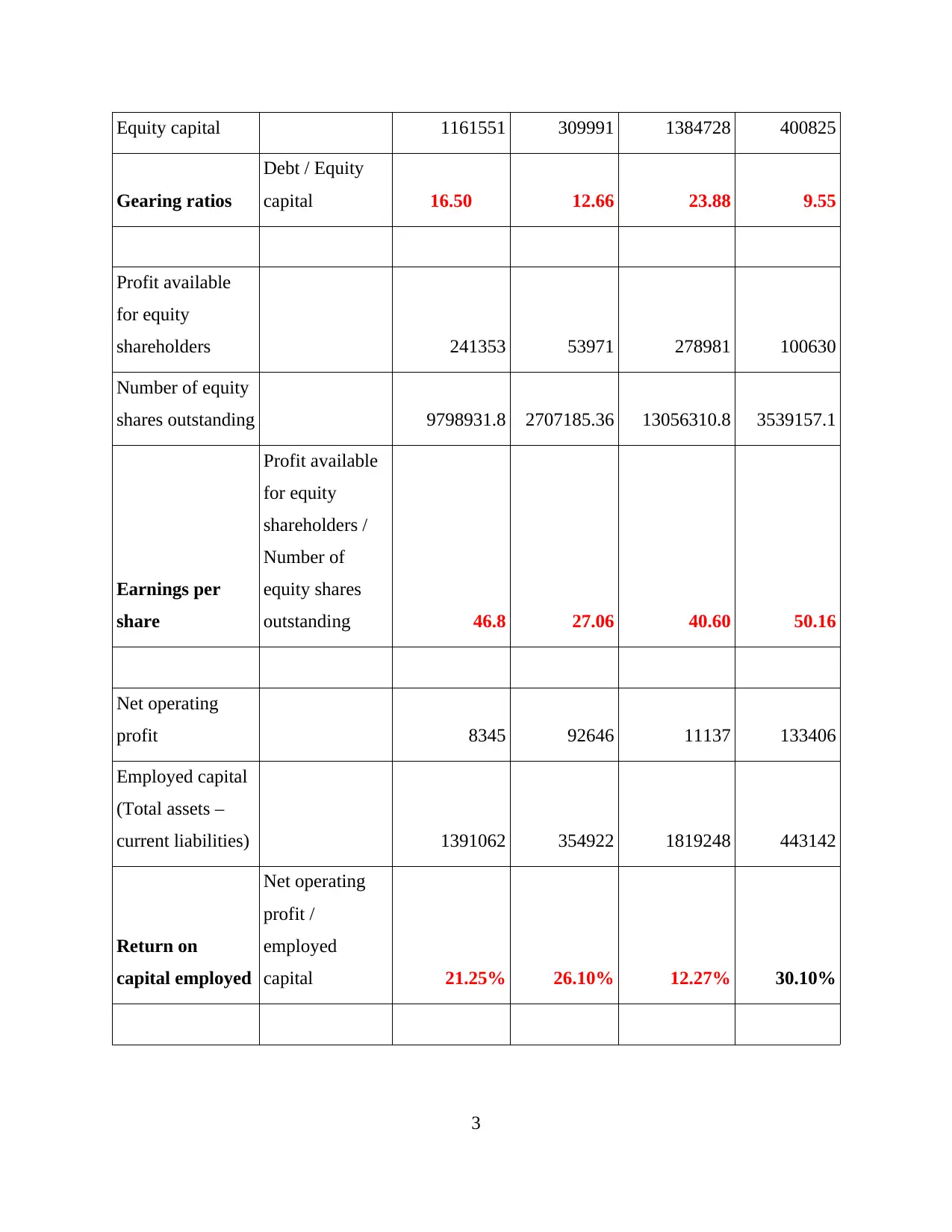

Equity capital 1161551 309991 1384728 400825

Gearing ratios

Debt / Equity

capital 16.50 12.66 23.88 9.55

Profit available

for equity

shareholders 241353 53971 278981 100630

Number of equity

shares outstanding 9798931.8 2707185.36 13056310.8 3539157.1

Earnings per

share

Profit available

for equity

shareholders /

Number of

equity shares

outstanding 46.8 27.06 40.60 50.16

Net operating

profit 8345 92646 11137 133406

Employed capital

(Total assets –

current liabilities) 1391062 354922 1819248 443142

Return on

capital employed

Net operating

profit /

employed

capital 21.25% 26.10% 12.27% 30.10%

3

Gearing ratios

Debt / Equity

capital 16.50 12.66 23.88 9.55

Profit available

for equity

shareholders 241353 53971 278981 100630

Number of equity

shares outstanding 9798931.8 2707185.36 13056310.8 3539157.1

Earnings per

share

Profit available

for equity

shareholders /

Number of

equity shares

outstanding 46.8 27.06 40.60 50.16

Net operating

profit 8345 92646 11137 133406

Employed capital

(Total assets –

current liabilities) 1391062 354922 1819248 443142

Return on

capital employed

Net operating

profit /

employed

capital 21.25% 26.10% 12.27% 30.10%

3

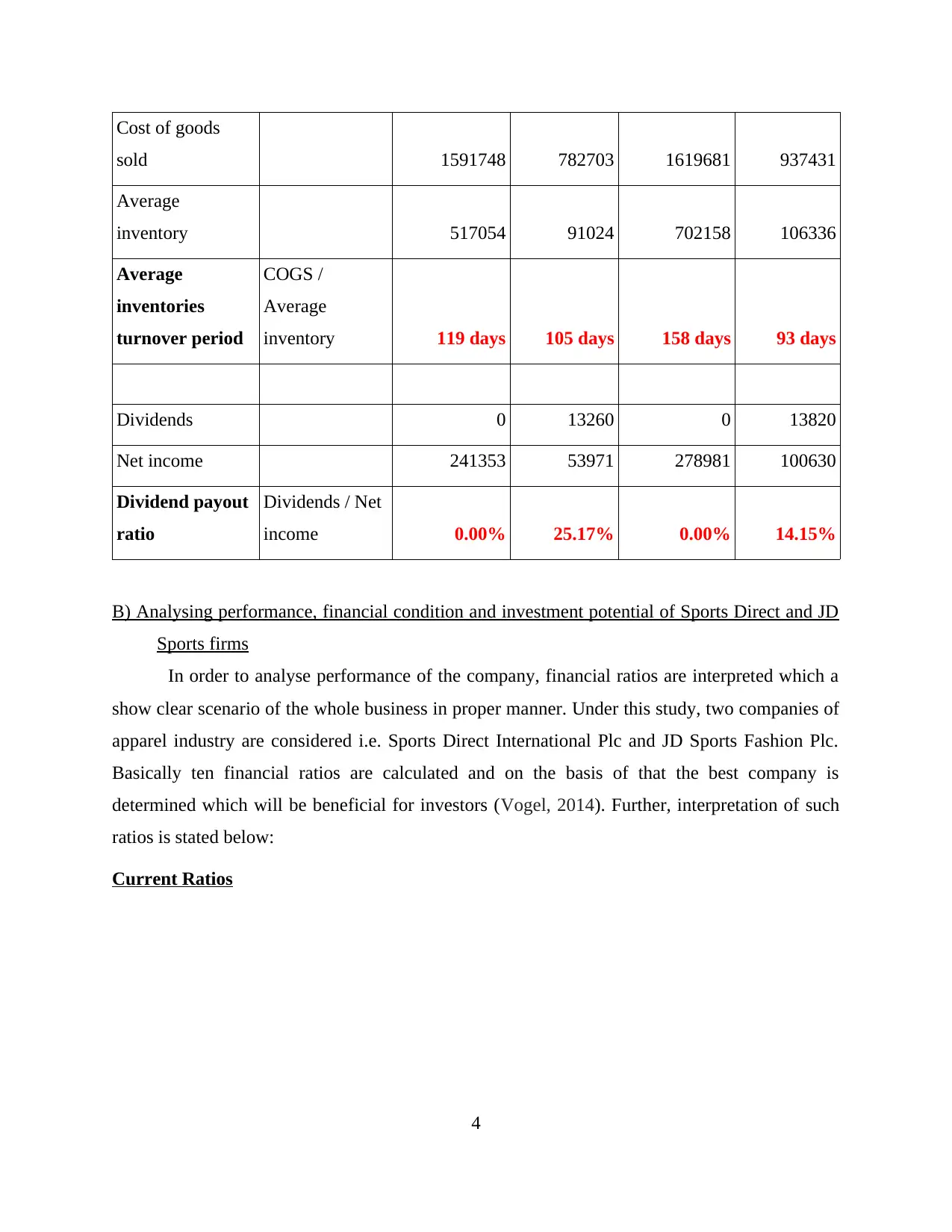

Cost of goods

sold 1591748 782703 1619681 937431

Average

inventory 517054 91024 702158 106336

Average

inventories

turnover period

COGS /

Average

inventory 119 days 105 days 158 days 93 days

Dividends 0 13260 0 13820

Net income 241353 53971 278981 100630

Dividend payout

ratio

Dividends / Net

income 0.00% 25.17% 0.00% 14.15%

B) Analysing performance, financial condition and investment potential of Sports Direct and JD

Sports firms

In order to analyse performance of the company, financial ratios are interpreted which a

show clear scenario of the whole business in proper manner. Under this study, two companies of

apparel industry are considered i.e. Sports Direct International Plc and JD Sports Fashion Plc.

Basically ten financial ratios are calculated and on the basis of that the best company is

determined which will be beneficial for investors (Vogel, 2014). Further, interpretation of such

ratios is stated below:

Current Ratios

4

sold 1591748 782703 1619681 937431

Average

inventory 517054 91024 702158 106336

Average

inventories

turnover period

COGS /

Average

inventory 119 days 105 days 158 days 93 days

Dividends 0 13260 0 13820

Net income 241353 53971 278981 100630

Dividend payout

ratio

Dividends / Net

income 0.00% 25.17% 0.00% 14.15%

B) Analysing performance, financial condition and investment potential of Sports Direct and JD

Sports firms

In order to analyse performance of the company, financial ratios are interpreted which a

show clear scenario of the whole business in proper manner. Under this study, two companies of

apparel industry are considered i.e. Sports Direct International Plc and JD Sports Fashion Plc.

Basically ten financial ratios are calculated and on the basis of that the best company is

determined which will be beneficial for investors (Vogel, 2014). Further, interpretation of such

ratios is stated below:

Current Ratios

4

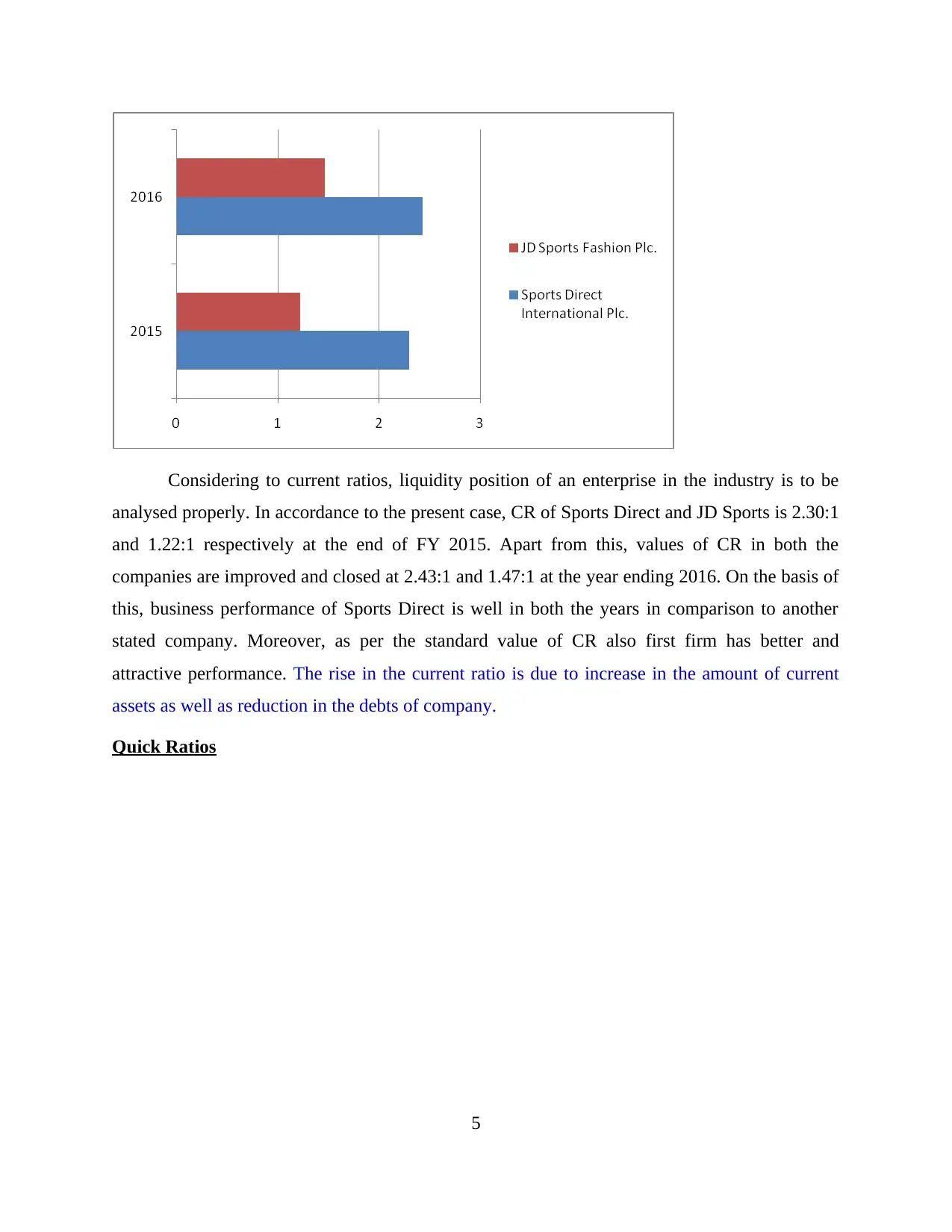

Considering to current ratios, liquidity position of an enterprise in the industry is to be

analysed properly. In accordance to the present case, CR of Sports Direct and JD Sports is 2.30:1

and 1.22:1 respectively at the end of FY 2015. Apart from this, values of CR in both the

companies are improved and closed at 2.43:1 and 1.47:1 at the year ending 2016. On the basis of

this, business performance of Sports Direct is well in both the years in comparison to another

stated company. Moreover, as per the standard value of CR also first firm has better and

attractive performance. The rise in the current ratio is due to increase in the amount of current

assets as well as reduction in the debts of company.

Quick Ratios

5

analysed properly. In accordance to the present case, CR of Sports Direct and JD Sports is 2.30:1

and 1.22:1 respectively at the end of FY 2015. Apart from this, values of CR in both the

companies are improved and closed at 2.43:1 and 1.47:1 at the year ending 2016. On the basis of

this, business performance of Sports Direct is well in both the years in comparison to another

stated company. Moreover, as per the standard value of CR also first firm has better and

attractive performance. The rise in the current ratio is due to increase in the amount of current

assets as well as reduction in the debts of company.

Quick Ratios

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

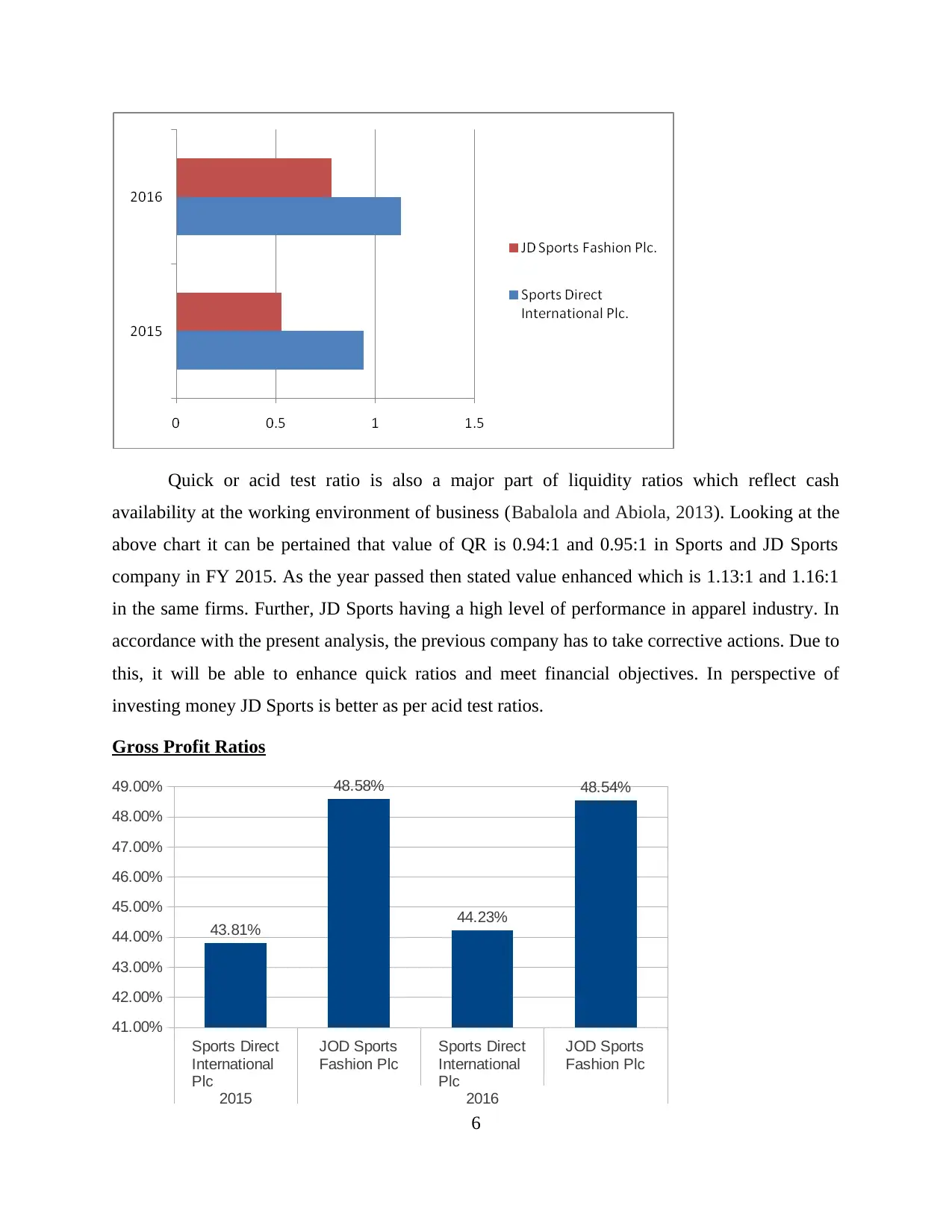

Quick or acid test ratio is also a major part of liquidity ratios which reflect cash

availability at the working environment of business (Babalola and Abiola, 2013). Looking at the

above chart it can be pertained that value of QR is 0.94:1 and 0.95:1 in Sports and JD Sports

company in FY 2015. As the year passed then stated value enhanced which is 1.13:1 and 1.16:1

in the same firms. Further, JD Sports having a high level of performance in apparel industry. In

accordance with the present analysis, the previous company has to take corrective actions. Due to

this, it will be able to enhance quick ratios and meet financial objectives. In perspective of

investing money JD Sports is better as per acid test ratios.

Gross Profit Ratios

Sports Direct

International

Plc

JOD Sports

Fashion Plc

Sports Direct

International

Plc

JOD Sports

Fashion Plc

2015 2016

41.00%

42.00%

43.00%

44.00%

45.00%

46.00%

47.00%

48.00%

49.00%

43.81%

48.58%

44.23%

48.54%

6

availability at the working environment of business (Babalola and Abiola, 2013). Looking at the

above chart it can be pertained that value of QR is 0.94:1 and 0.95:1 in Sports and JD Sports

company in FY 2015. As the year passed then stated value enhanced which is 1.13:1 and 1.16:1

in the same firms. Further, JD Sports having a high level of performance in apparel industry. In

accordance with the present analysis, the previous company has to take corrective actions. Due to

this, it will be able to enhance quick ratios and meet financial objectives. In perspective of

investing money JD Sports is better as per acid test ratios.

Gross Profit Ratios

Sports Direct

International

Plc

JOD Sports

Fashion Plc

Sports Direct

International

Plc

JOD Sports

Fashion Plc

2015 2016

41.00%

42.00%

43.00%

44.00%

45.00%

46.00%

47.00%

48.00%

49.00%

43.81%

48.58%

44.23%

48.54%

6

This is a part of profitability ratios where company can determine gross profit generated

at the end of accounting period. Higher the value of this tool is one of the profitable for company

and investors both (Delen, Kuzey and Uyar, 2013). At the end of fiscal year 2015, GP ratio of

Sports and JD Sports was 43.81% and 48.58% respectively which enhanced up to 44.23% and

48.54% in the year 2016. This value clearly shows that, profit generation capacity of JD Sports is

well as compared to its competitor. Moreover, it is highly able to manage and reduce cost of

goods sales which are unproductive and create unnecessary burden on the management.

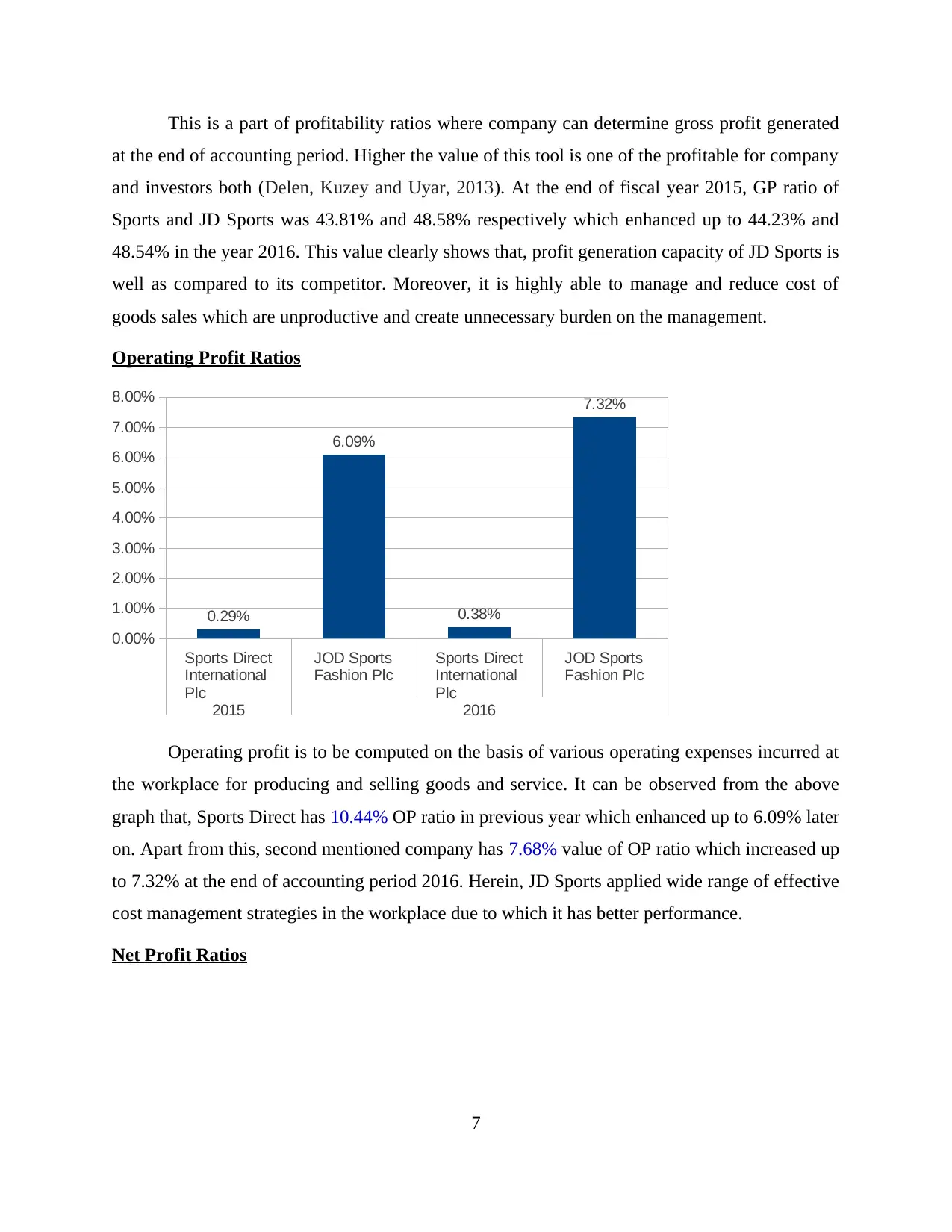

Operating Profit Ratios

Sports Direct

International

Plc

JOD Sports

Fashion Plc

Sports Direct

International

Plc

JOD Sports

Fashion Plc

2015 2016

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

0.29%

6.09%

0.38%

7.32%

Operating profit is to be computed on the basis of various operating expenses incurred at

the workplace for producing and selling goods and service. It can be observed from the above

graph that, Sports Direct has 10.44% OP ratio in previous year which enhanced up to 6.09% later

on. Apart from this, second mentioned company has 7.68% value of OP ratio which increased up

to 7.32% at the end of accounting period 2016. Herein, JD Sports applied wide range of effective

cost management strategies in the workplace due to which it has better performance.

Net Profit Ratios

7

at the end of accounting period. Higher the value of this tool is one of the profitable for company

and investors both (Delen, Kuzey and Uyar, 2013). At the end of fiscal year 2015, GP ratio of

Sports and JD Sports was 43.81% and 48.58% respectively which enhanced up to 44.23% and

48.54% in the year 2016. This value clearly shows that, profit generation capacity of JD Sports is

well as compared to its competitor. Moreover, it is highly able to manage and reduce cost of

goods sales which are unproductive and create unnecessary burden on the management.

Operating Profit Ratios

Sports Direct

International

Plc

JOD Sports

Fashion Plc

Sports Direct

International

Plc

JOD Sports

Fashion Plc

2015 2016

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

0.29%

6.09%

0.38%

7.32%

Operating profit is to be computed on the basis of various operating expenses incurred at

the workplace for producing and selling goods and service. It can be observed from the above

graph that, Sports Direct has 10.44% OP ratio in previous year which enhanced up to 6.09% later

on. Apart from this, second mentioned company has 7.68% value of OP ratio which increased up

to 7.32% at the end of accounting period 2016. Herein, JD Sports applied wide range of effective

cost management strategies in the workplace due to which it has better performance.

Net Profit Ratios

7

Sports Direct

International

Plc

JOD Sports

Fashion Plc

Sports Direct

International

Plc

JOD Sports

Fashion Plc

2015 2016

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

8.52%

3.55%

9.61%

5.52%

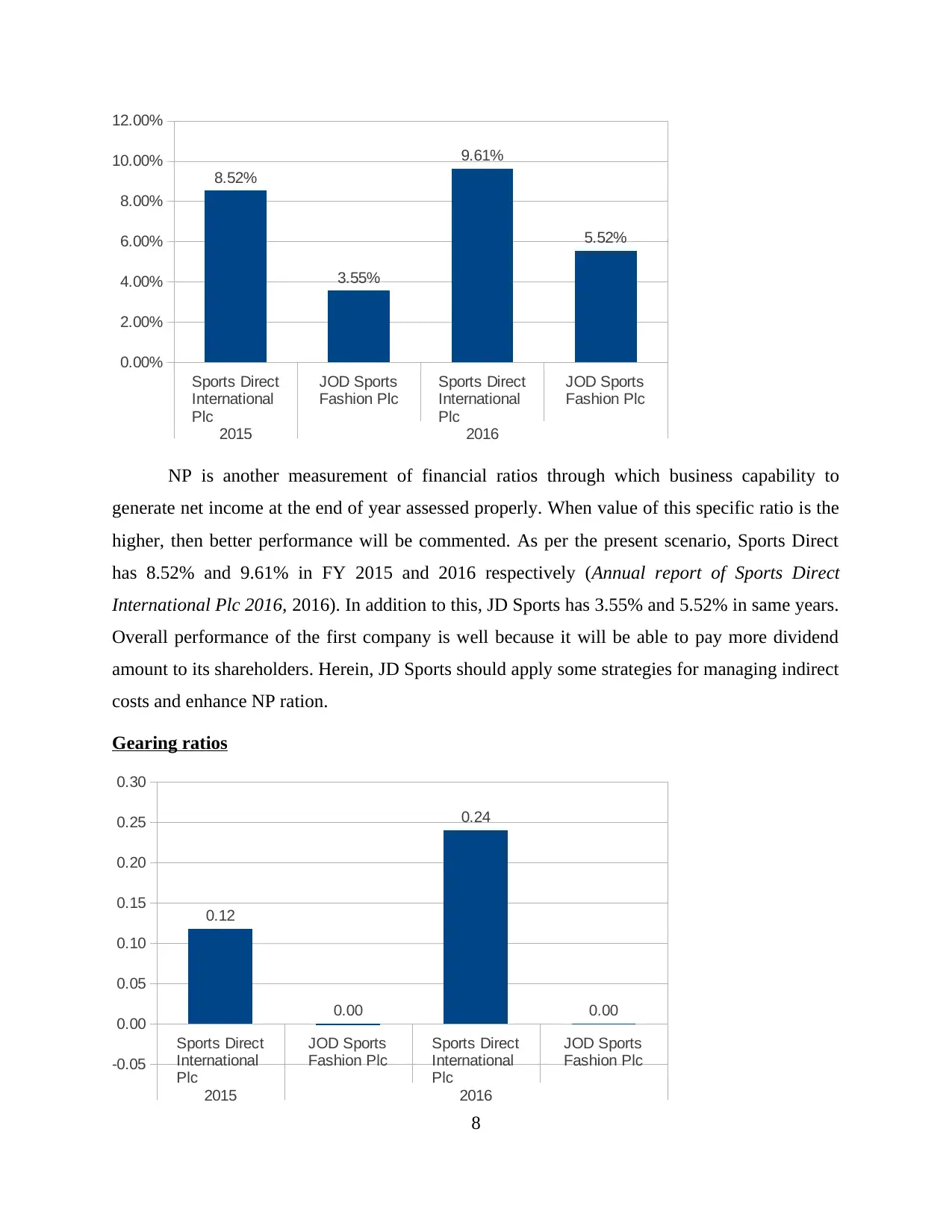

NP is another measurement of financial ratios through which business capability to

generate net income at the end of year assessed properly. When value of this specific ratio is the

higher, then better performance will be commented. As per the present scenario, Sports Direct

has 8.52% and 9.61% in FY 2015 and 2016 respectively (Annual report of Sports Direct

International Plc 2016, 2016). In addition to this, JD Sports has 3.55% and 5.52% in same years.

Overall performance of the first company is well because it will be able to pay more dividend

amount to its shareholders. Herein, JD Sports should apply some strategies for managing indirect

costs and enhance NP ration.

Gearing ratios

Sports Direct

International

Plc

JOD Sports

Fashion Plc

Sports Direct

International

Plc

JOD Sports

Fashion Plc

2015 2016

-0.05

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.12

0.00

0.24

0.00

8

International

Plc

JOD Sports

Fashion Plc

Sports Direct

International

Plc

JOD Sports

Fashion Plc

2015 2016

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

8.52%

3.55%

9.61%

5.52%

NP is another measurement of financial ratios through which business capability to

generate net income at the end of year assessed properly. When value of this specific ratio is the

higher, then better performance will be commented. As per the present scenario, Sports Direct

has 8.52% and 9.61% in FY 2015 and 2016 respectively (Annual report of Sports Direct

International Plc 2016, 2016). In addition to this, JD Sports has 3.55% and 5.52% in same years.

Overall performance of the first company is well because it will be able to pay more dividend

amount to its shareholders. Herein, JD Sports should apply some strategies for managing indirect

costs and enhance NP ration.

Gearing ratios

Sports Direct

International

Plc

JOD Sports

Fashion Plc

Sports Direct

International

Plc

JOD Sports

Fashion Plc

2015 2016

-0.05

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.12

0.00

0.24

0.00

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

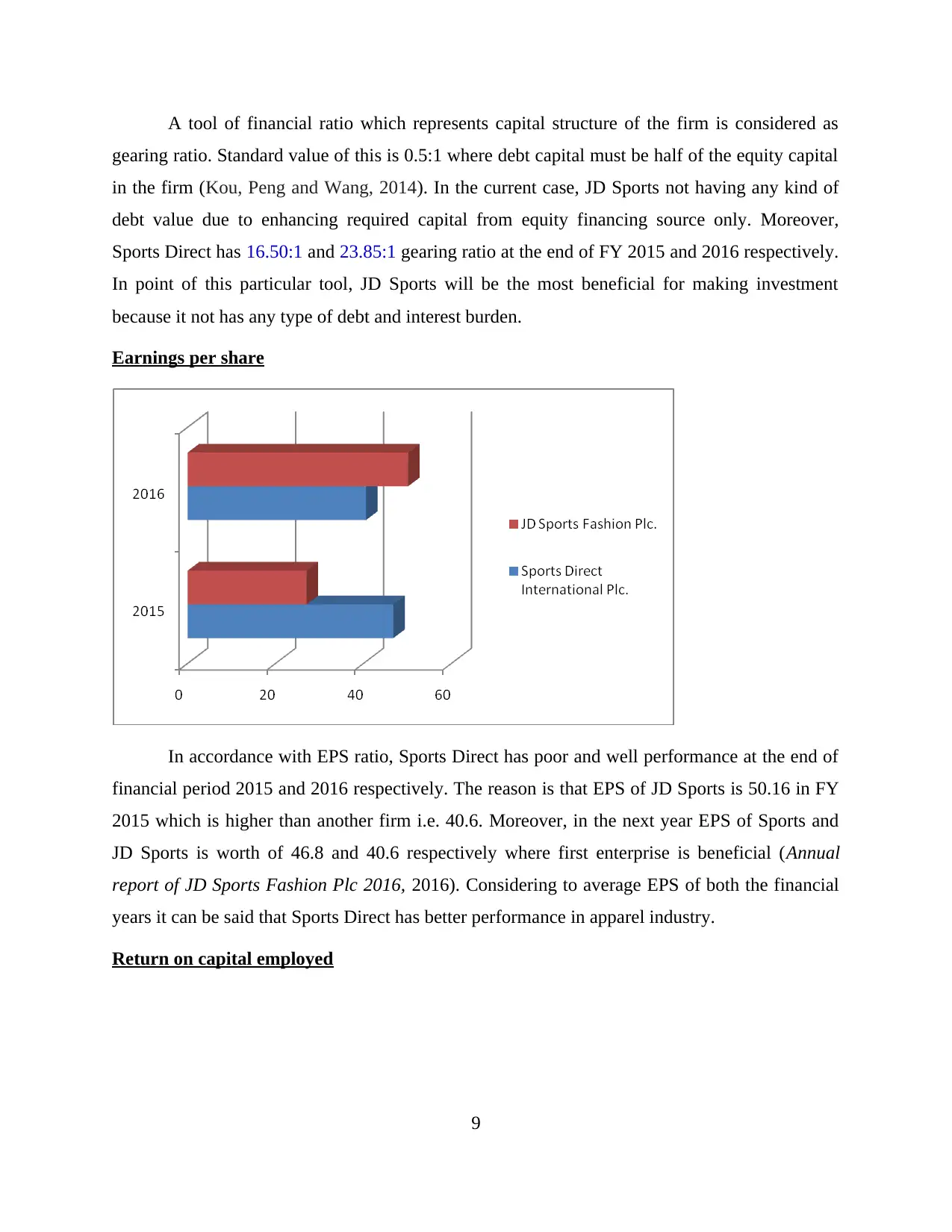

A tool of financial ratio which represents capital structure of the firm is considered as

gearing ratio. Standard value of this is 0.5:1 where debt capital must be half of the equity capital

in the firm (Kou, Peng and Wang, 2014). In the current case, JD Sports not having any kind of

debt value due to enhancing required capital from equity financing source only. Moreover,

Sports Direct has 16.50:1 and 23.85:1 gearing ratio at the end of FY 2015 and 2016 respectively.

In point of this particular tool, JD Sports will be the most beneficial for making investment

because it not has any type of debt and interest burden.

Earnings per share

In accordance with EPS ratio, Sports Direct has poor and well performance at the end of

financial period 2015 and 2016 respectively. The reason is that EPS of JD Sports is 50.16 in FY

2015 which is higher than another firm i.e. 40.6. Moreover, in the next year EPS of Sports and

JD Sports is worth of 46.8 and 40.6 respectively where first enterprise is beneficial (Annual

report of JD Sports Fashion Plc 2016, 2016). Considering to average EPS of both the financial

years it can be said that Sports Direct has better performance in apparel industry.

Return on capital employed

9

gearing ratio. Standard value of this is 0.5:1 where debt capital must be half of the equity capital

in the firm (Kou, Peng and Wang, 2014). In the current case, JD Sports not having any kind of

debt value due to enhancing required capital from equity financing source only. Moreover,

Sports Direct has 16.50:1 and 23.85:1 gearing ratio at the end of FY 2015 and 2016 respectively.

In point of this particular tool, JD Sports will be the most beneficial for making investment

because it not has any type of debt and interest burden.

Earnings per share

In accordance with EPS ratio, Sports Direct has poor and well performance at the end of

financial period 2015 and 2016 respectively. The reason is that EPS of JD Sports is 50.16 in FY

2015 which is higher than another firm i.e. 40.6. Moreover, in the next year EPS of Sports and

JD Sports is worth of 46.8 and 40.6 respectively where first enterprise is beneficial (Annual

report of JD Sports Fashion Plc 2016, 2016). Considering to average EPS of both the financial

years it can be said that Sports Direct has better performance in apparel industry.

Return on capital employed

9

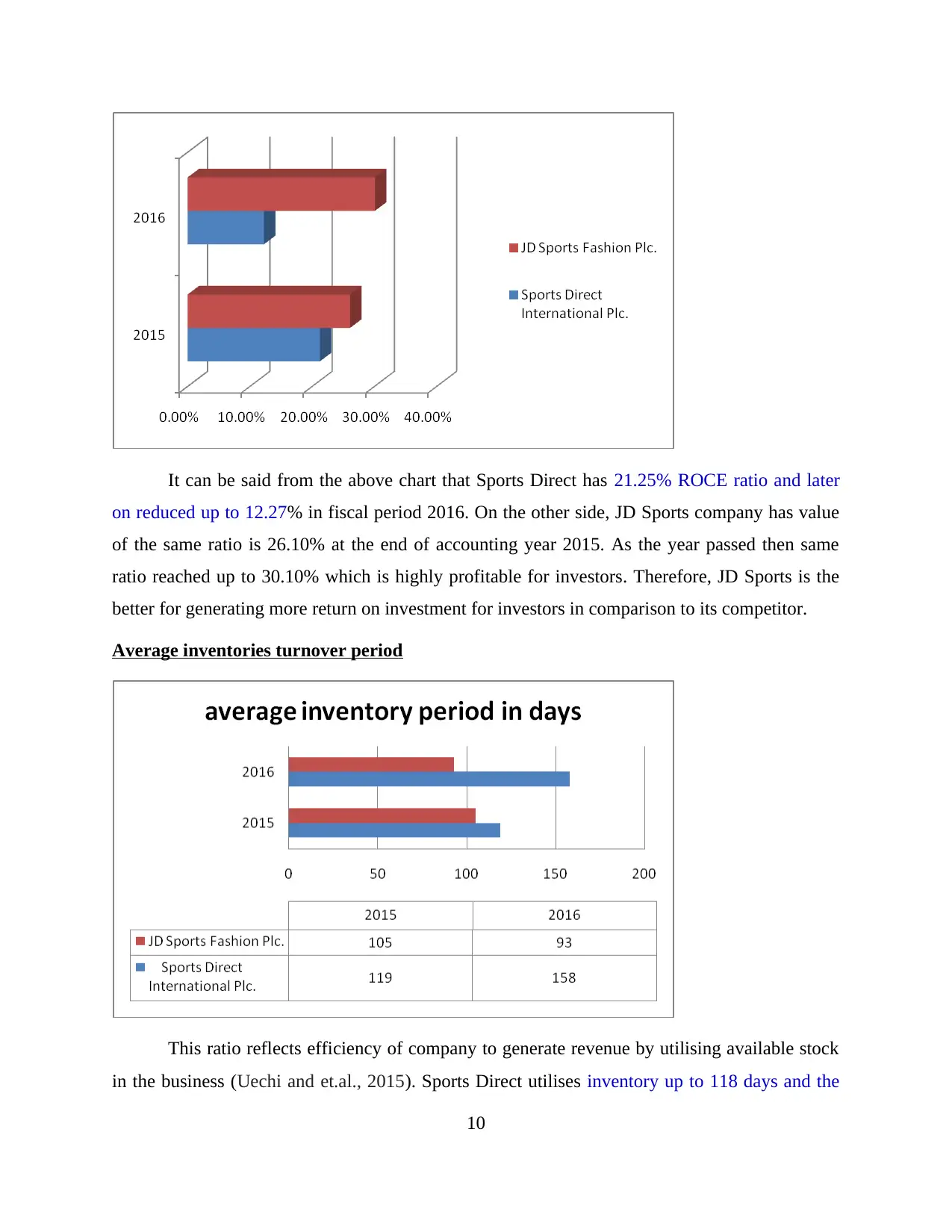

It can be said from the above chart that Sports Direct has 21.25% ROCE ratio and later

on reduced up to 12.27% in fiscal period 2016. On the other side, JD Sports company has value

of the same ratio is 26.10% at the end of accounting year 2015. As the year passed then same

ratio reached up to 30.10% which is highly profitable for investors. Therefore, JD Sports is the

better for generating more return on investment for investors in comparison to its competitor.

Average inventories turnover period

This ratio reflects efficiency of company to generate revenue by utilising available stock

in the business (Uechi and et.al., 2015). Sports Direct utilises inventory up to 118 days and the

10

on reduced up to 12.27% in fiscal period 2016. On the other side, JD Sports company has value

of the same ratio is 26.10% at the end of accounting year 2015. As the year passed then same

ratio reached up to 30.10% which is highly profitable for investors. Therefore, JD Sports is the

better for generating more return on investment for investors in comparison to its competitor.

Average inventories turnover period

This ratio reflects efficiency of company to generate revenue by utilising available stock

in the business (Uechi and et.al., 2015). Sports Direct utilises inventory up to 118 days and the

10

same value within JD Sports is 105 days in previous year. When looking at the next accounting

period then it can be seen that, Sports Direct uses stock up to 158 days and the same in second

firm is 93 days. As per decision rule that higher the average stock turnover ratio is better, JD

Sports performing well in the apparel industry. As per this, the second firm the most beneficial

for investing money.

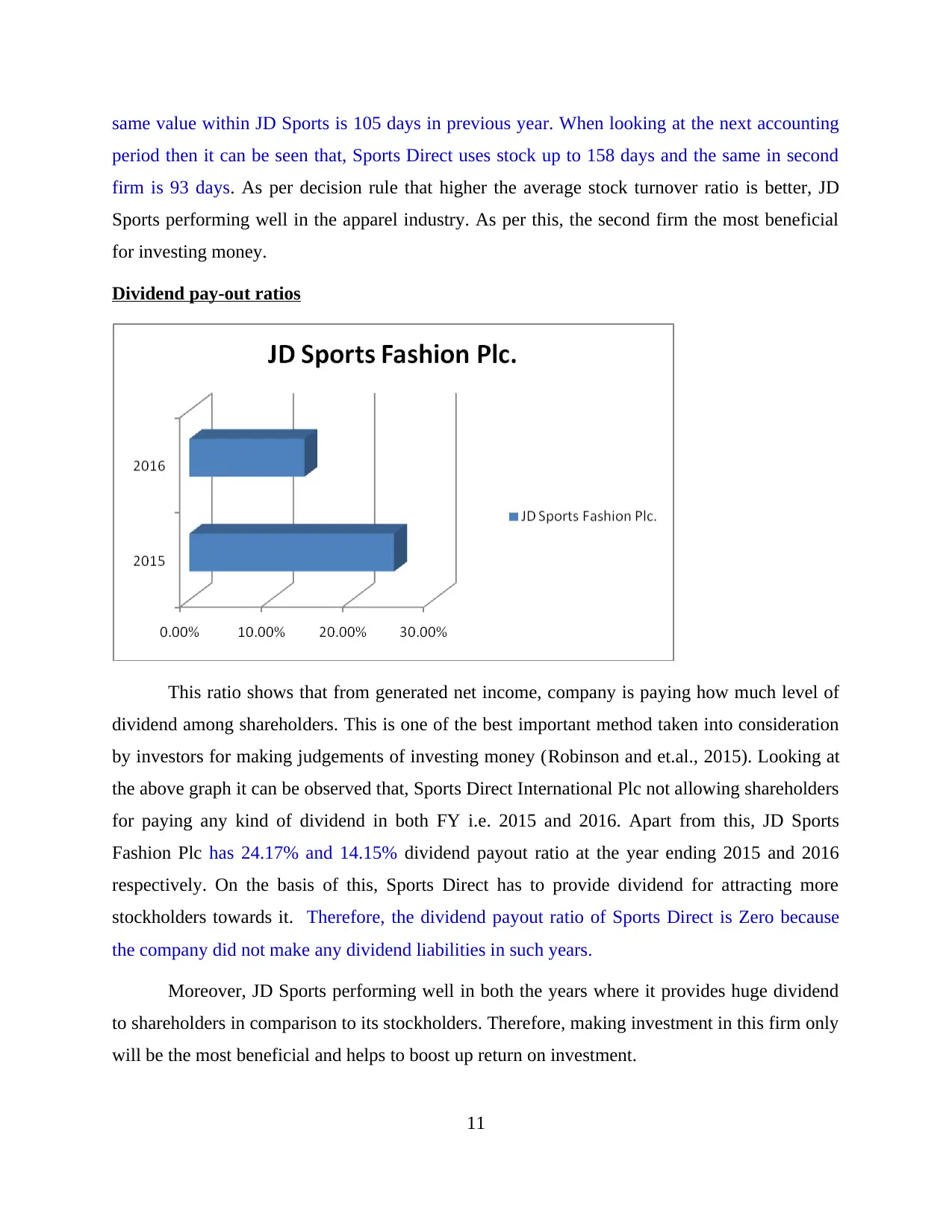

Dividend pay-out ratios

This ratio shows that from generated net income, company is paying how much level of

dividend among shareholders. This is one of the best important method taken into consideration

by investors for making judgements of investing money (Robinson and et.al., 2015). Looking at

the above graph it can be observed that, Sports Direct International Plc not allowing shareholders

for paying any kind of dividend in both FY i.e. 2015 and 2016. Apart from this, JD Sports

Fashion Plc has 24.17% and 14.15% dividend payout ratio at the year ending 2015 and 2016

respectively. On the basis of this, Sports Direct has to provide dividend for attracting more

stockholders towards it. Therefore, the dividend payout ratio of Sports Direct is Zero because

the company did not make any dividend liabilities in such years.

Moreover, JD Sports performing well in both the years where it provides huge dividend

to shareholders in comparison to its stockholders. Therefore, making investment in this firm only

will be the most beneficial and helps to boost up return on investment.

11

period then it can be seen that, Sports Direct uses stock up to 158 days and the same in second

firm is 93 days. As per decision rule that higher the average stock turnover ratio is better, JD

Sports performing well in the apparel industry. As per this, the second firm the most beneficial

for investing money.

Dividend pay-out ratios

This ratio shows that from generated net income, company is paying how much level of

dividend among shareholders. This is one of the best important method taken into consideration

by investors for making judgements of investing money (Robinson and et.al., 2015). Looking at

the above graph it can be observed that, Sports Direct International Plc not allowing shareholders

for paying any kind of dividend in both FY i.e. 2015 and 2016. Apart from this, JD Sports

Fashion Plc has 24.17% and 14.15% dividend payout ratio at the year ending 2015 and 2016

respectively. On the basis of this, Sports Direct has to provide dividend for attracting more

stockholders towards it. Therefore, the dividend payout ratio of Sports Direct is Zero because

the company did not make any dividend liabilities in such years.

Moreover, JD Sports performing well in both the years where it provides huge dividend

to shareholders in comparison to its stockholders. Therefore, making investment in this firm only

will be the most beneficial and helps to boost up return on investment.

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

C) Providing appropriate suggestions to the firm which has poor financial performance

From the above financial ratios it can be analysed that Sports Direct has poor

performance and its rival performing well in apparel sector. For resolving poor condition and

enhancing it some strategies are suggested below:

Sports Direct needs to generate capital for any business project from equity financing

rather than debt. On the basis of this, it will become able for declining interest burden and

gearing ratio both in the industry.

Apart from this, it has to enhance operating profit by using some strategies for reducing

operating expenses. This particular tactic will support to Sports Direct for increasing

return on capital employed ratio which is one of the attraction point of shareholders.

It requires giving training to the workforce about ways for utilising stock in an optimum

direction. Due to this, it able to boost up average inventory turnover times at the end of

upcoming accounting period.

At the last, management of Sports Direct provide dividend among shareholders at the end

of year. On the basis of this, stockholders will attract towards it for purchasing shares.

Further, JD Sports needs to manage indirect costs incurred at the workplace which will

support to enhance NP ratio at the end of next accounting period and make it financially

sound.

D) Discussing drawbacks of financial ratios which used to analyse firm's performance

Despite various kinds of advantages, the financial ratios have some drawbacks which will

affect to the business organisation. Further, some limitations of this stated below:

Main problem associated with financial ratios is that, it considers only quantitative

measures for analysing business performance. Further, it ignores those aspects which

come into consideration under qualitative (Peavler, 2017).

It shows that company is performing whether well or poor in the industry only. Reasons

due to which performance changes at the workplace are not reflected by financial ratio

analysis.

12

From the above financial ratios it can be analysed that Sports Direct has poor

performance and its rival performing well in apparel sector. For resolving poor condition and

enhancing it some strategies are suggested below:

Sports Direct needs to generate capital for any business project from equity financing

rather than debt. On the basis of this, it will become able for declining interest burden and

gearing ratio both in the industry.

Apart from this, it has to enhance operating profit by using some strategies for reducing

operating expenses. This particular tactic will support to Sports Direct for increasing

return on capital employed ratio which is one of the attraction point of shareholders.

It requires giving training to the workforce about ways for utilising stock in an optimum

direction. Due to this, it able to boost up average inventory turnover times at the end of

upcoming accounting period.

At the last, management of Sports Direct provide dividend among shareholders at the end

of year. On the basis of this, stockholders will attract towards it for purchasing shares.

Further, JD Sports needs to manage indirect costs incurred at the workplace which will

support to enhance NP ratio at the end of next accounting period and make it financially

sound.

D) Discussing drawbacks of financial ratios which used to analyse firm's performance

Despite various kinds of advantages, the financial ratios have some drawbacks which will

affect to the business organisation. Further, some limitations of this stated below:

Main problem associated with financial ratios is that, it considers only quantitative

measures for analysing business performance. Further, it ignores those aspects which

come into consideration under qualitative (Peavler, 2017).

It shows that company is performing whether well or poor in the industry only. Reasons

due to which performance changes at the workplace are not reflected by financial ratio

analysis.

12

When two or more companies consider different accounting standards and principles for

preparing financial statements then proper comparison cannot be made among the firms.

The tools of ratio analysis help to measure and analyse only historical data and

information. On the basis of these, management of selected two firms cannot make

effectual as well as fruitful predictions.

The financial ratios not considering impact of inflation rate on various information. Due

to this particular situation, company unable to analyse and predict performance properly

(The limitations of ratio analysis, 2011).

Apart from this, only one of two kinds of ratios are not enough for analysing business

performance in the industry. Requirement of calculating several ratios is there for

knowing performance of the firms in appropriate direction.

PORTFOLIO 2

Question 2

A) Use of basic investment appraisal methods and suggestions to management of a local

manufacturing enterprise

A method through which viability of one project among two or more simultaneous

alternatives is analysed is known as capital budgeting. Further, it is basically used to make

investment in one specific alternative among two or more at the workplace. Due to this particular

nature, it is called as an investment appraisal technique. There is a wide range of tools involved

in this which are like NPV, IRR, ARR, payback period, profitability index, etc (Abor, 2017). In

the present case scenario, a local manufacturing company has two options in order to purchase

machines i.e. A and B. Further, investment decisions are to be made with the help of basic three

techniques which involve NPV, payback and ARR. Calculations and suggestions are given as

below:

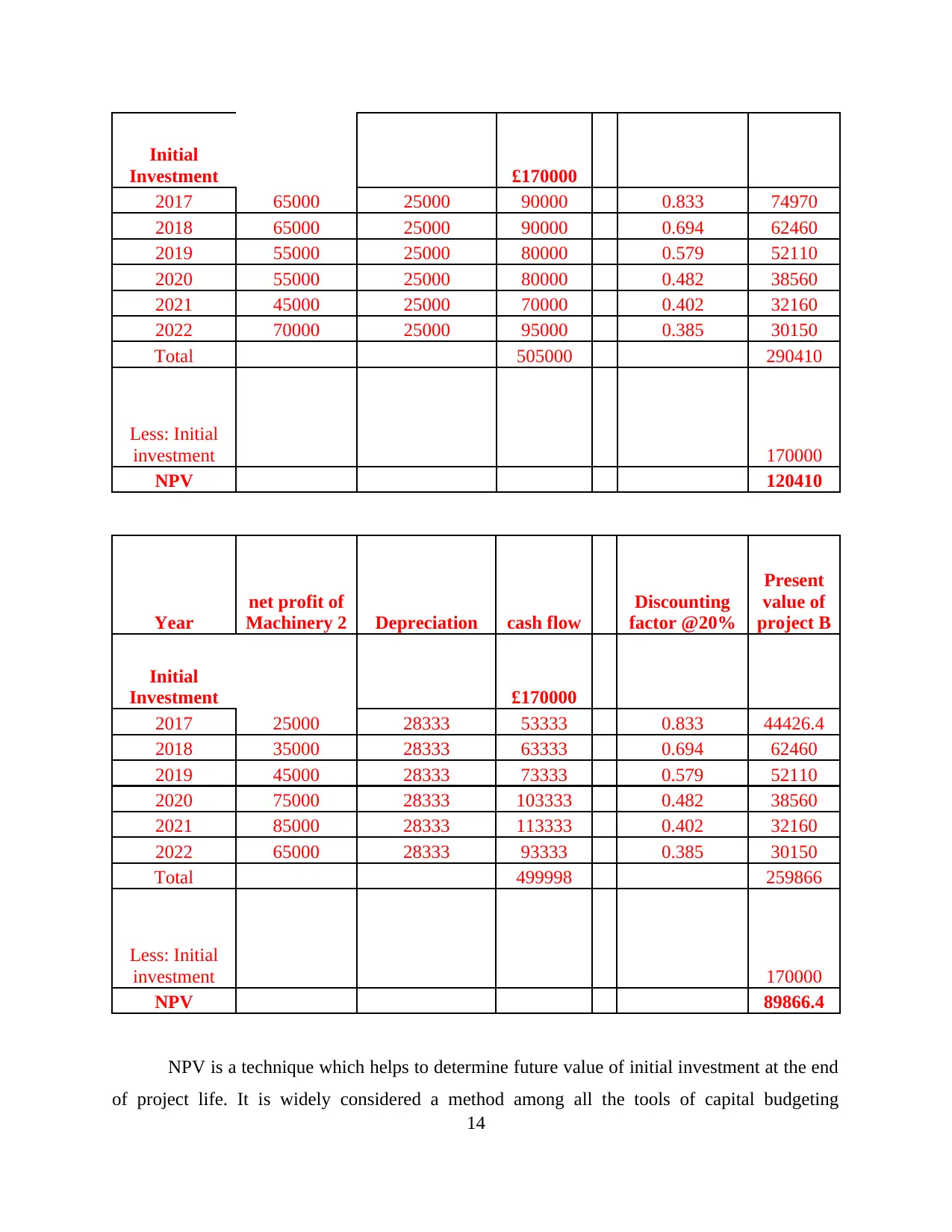

Net Present Value

Year

net profit of

Machinery 1 Depreciation cash flow

Discounting

factor @20%

Present

value of

project B

13

preparing financial statements then proper comparison cannot be made among the firms.

The tools of ratio analysis help to measure and analyse only historical data and

information. On the basis of these, management of selected two firms cannot make

effectual as well as fruitful predictions.

The financial ratios not considering impact of inflation rate on various information. Due

to this particular situation, company unable to analyse and predict performance properly

(The limitations of ratio analysis, 2011).

Apart from this, only one of two kinds of ratios are not enough for analysing business

performance in the industry. Requirement of calculating several ratios is there for

knowing performance of the firms in appropriate direction.

PORTFOLIO 2

Question 2

A) Use of basic investment appraisal methods and suggestions to management of a local

manufacturing enterprise

A method through which viability of one project among two or more simultaneous

alternatives is analysed is known as capital budgeting. Further, it is basically used to make

investment in one specific alternative among two or more at the workplace. Due to this particular

nature, it is called as an investment appraisal technique. There is a wide range of tools involved

in this which are like NPV, IRR, ARR, payback period, profitability index, etc (Abor, 2017). In

the present case scenario, a local manufacturing company has two options in order to purchase

machines i.e. A and B. Further, investment decisions are to be made with the help of basic three

techniques which involve NPV, payback and ARR. Calculations and suggestions are given as

below:

Net Present Value

Year

net profit of

Machinery 1 Depreciation cash flow

Discounting

factor @20%

Present

value of

project B

13

Initial

Investment £170000

2017 65000 25000 90000 0.833 74970

2018 65000 25000 90000 0.694 62460

2019 55000 25000 80000 0.579 52110

2020 55000 25000 80000 0.482 38560

2021 45000 25000 70000 0.402 32160

2022 70000 25000 95000 0.385 30150

Total 505000 290410

Less: Initial

investment 170000

NPV 120410

Year

net profit of

Machinery 2 Depreciation cash flow

Discounting

factor @20%

Present

value of

project B

Initial

Investment £170000

2017 25000 28333 53333 0.833 44426.4

2018 35000 28333 63333 0.694 62460

2019 45000 28333 73333 0.579 52110

2020 75000 28333 103333 0.482 38560

2021 85000 28333 113333 0.402 32160

2022 65000 28333 93333 0.385 30150

Total 499998 259866

Less: Initial

investment 170000

NPV 89866.4

NPV is a technique which helps to determine future value of initial investment at the end

of project life. It is widely considered a method among all the tools of capital budgeting

14

Investment £170000

2017 65000 25000 90000 0.833 74970

2018 65000 25000 90000 0.694 62460

2019 55000 25000 80000 0.579 52110

2020 55000 25000 80000 0.482 38560

2021 45000 25000 70000 0.402 32160

2022 70000 25000 95000 0.385 30150

Total 505000 290410

Less: Initial

investment 170000

NPV 120410

Year

net profit of

Machinery 2 Depreciation cash flow

Discounting

factor @20%

Present

value of

project B

Initial

Investment £170000

2017 25000 28333 53333 0.833 44426.4

2018 35000 28333 63333 0.694 62460

2019 45000 28333 73333 0.579 52110

2020 75000 28333 103333 0.482 38560

2021 85000 28333 113333 0.402 32160

2022 65000 28333 93333 0.385 30150

Total 499998 259866

Less: Initial

investment 170000

NPV 89866.4

NPV is a technique which helps to determine future value of initial investment at the end

of project life. It is widely considered a method among all the tools of capital budgeting

14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

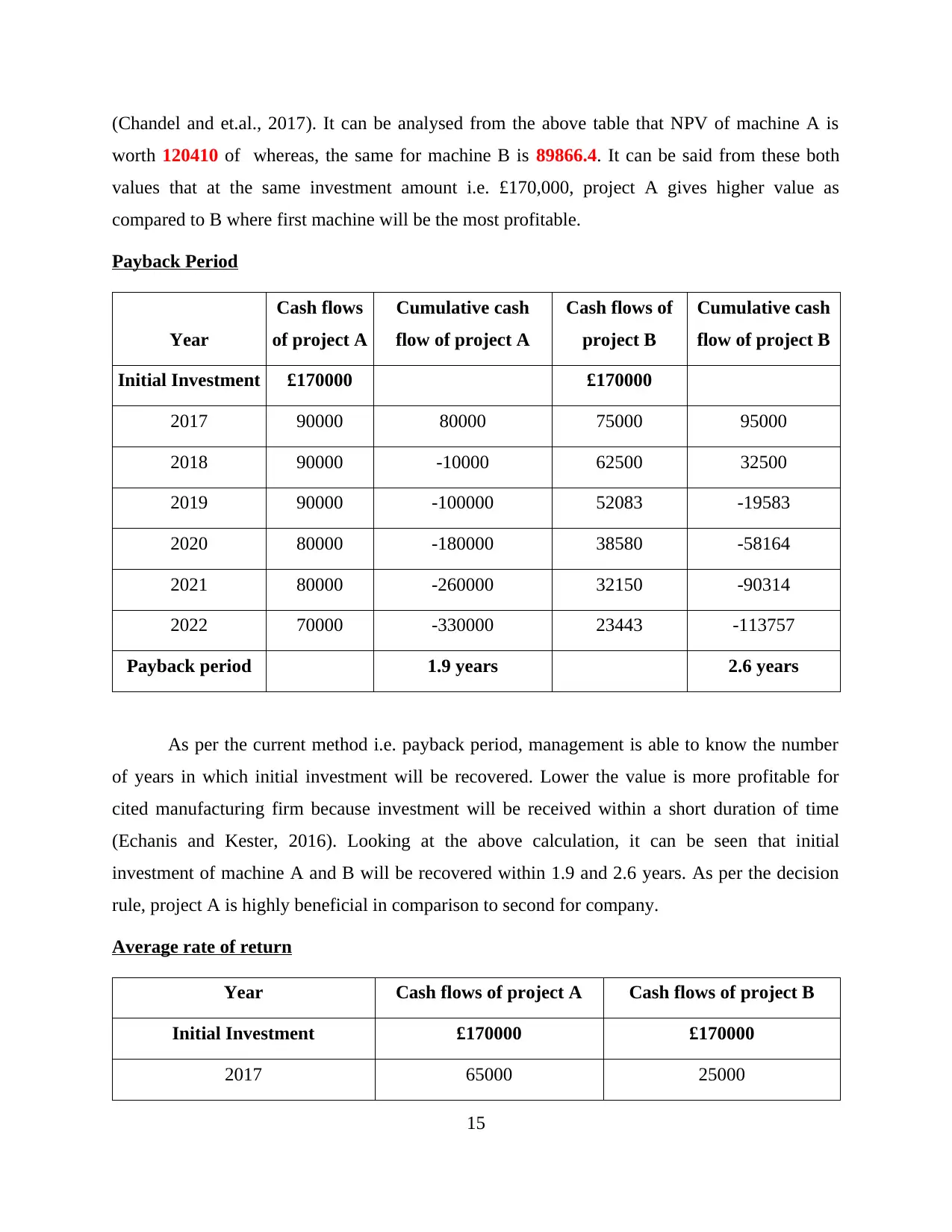

(Chandel and et.al., 2017). It can be analysed from the above table that NPV of machine A is

worth 120410 of whereas, the same for machine B is 89866.4. It can be said from these both

values that at the same investment amount i.e. £170,000, project A gives higher value as

compared to B where first machine will be the most profitable.

Payback Period

Year

Cash flows

of project A

Cumulative cash

flow of project A

Cash flows of

project B

Cumulative cash

flow of project B

Initial Investment £170000 £170000

2017 90000 80000 75000 95000

2018 90000 -10000 62500 32500

2019 90000 -100000 52083 -19583

2020 80000 -180000 38580 -58164

2021 80000 -260000 32150 -90314

2022 70000 -330000 23443 -113757

Payback period 1.9 years 2.6 years

As per the current method i.e. payback period, management is able to know the number

of years in which initial investment will be recovered. Lower the value is more profitable for

cited manufacturing firm because investment will be received within a short duration of time

(Echanis and Kester, 2016). Looking at the above calculation, it can be seen that initial

investment of machine A and B will be recovered within 1.9 and 2.6 years. As per the decision

rule, project A is highly beneficial in comparison to second for company.

Average rate of return

Year Cash flows of project A Cash flows of project B

Initial Investment £170000 £170000

2017 65000 25000

15

worth 120410 of whereas, the same for machine B is 89866.4. It can be said from these both

values that at the same investment amount i.e. £170,000, project A gives higher value as

compared to B where first machine will be the most profitable.

Payback Period

Year

Cash flows

of project A

Cumulative cash

flow of project A

Cash flows of

project B

Cumulative cash

flow of project B

Initial Investment £170000 £170000

2017 90000 80000 75000 95000

2018 90000 -10000 62500 32500

2019 90000 -100000 52083 -19583

2020 80000 -180000 38580 -58164

2021 80000 -260000 32150 -90314

2022 70000 -330000 23443 -113757

Payback period 1.9 years 2.6 years

As per the current method i.e. payback period, management is able to know the number

of years in which initial investment will be recovered. Lower the value is more profitable for

cited manufacturing firm because investment will be received within a short duration of time

(Echanis and Kester, 2016). Looking at the above calculation, it can be seen that initial

investment of machine A and B will be recovered within 1.9 and 2.6 years. As per the decision

rule, project A is highly beneficial in comparison to second for company.

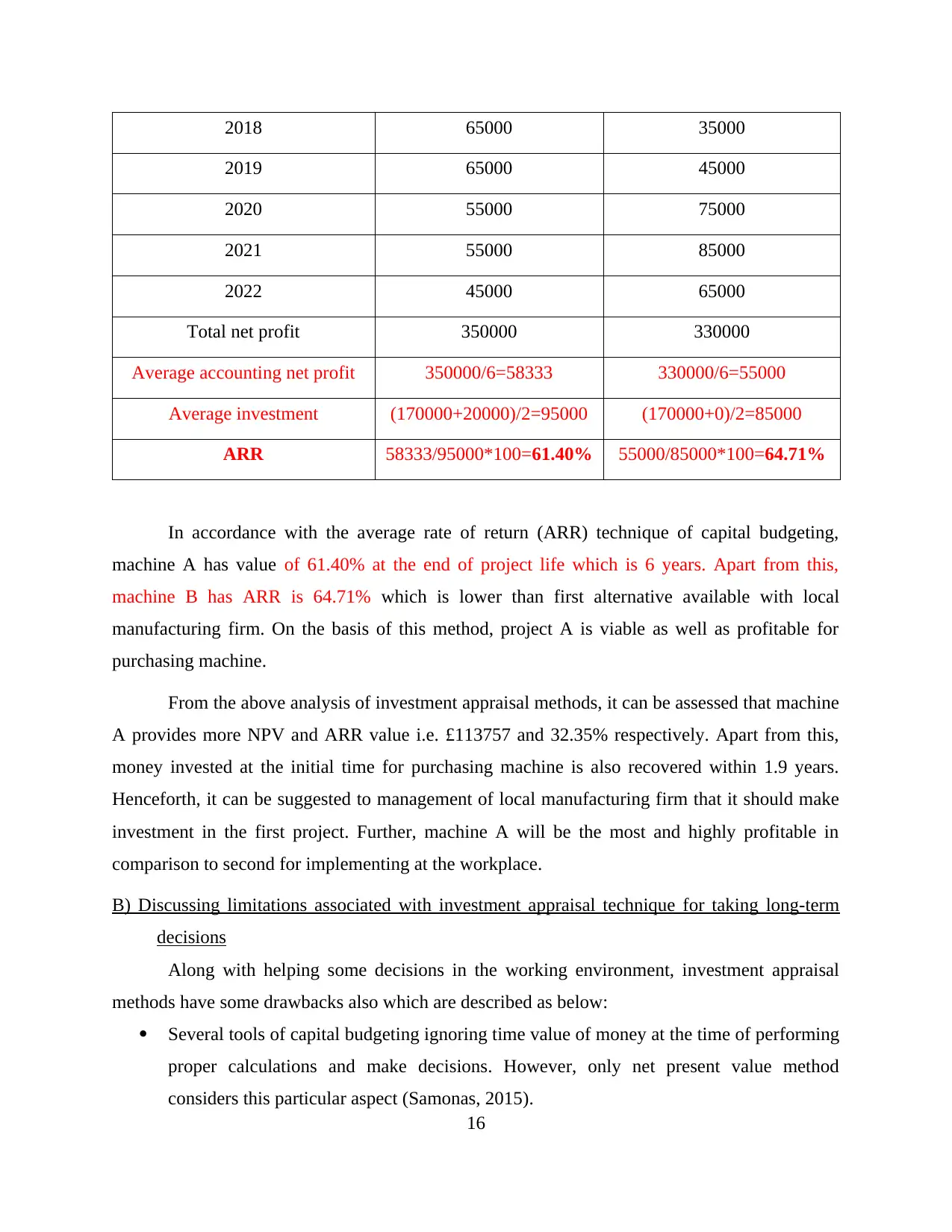

Average rate of return

Year Cash flows of project A Cash flows of project B

Initial Investment £170000 £170000

2017 65000 25000

15

2018 65000 35000

2019 65000 45000

2020 55000 75000

2021 55000 85000

2022 45000 65000

Total net profit 350000 330000

Average accounting net profit 350000/6=58333 330000/6=55000

Average investment (170000+20000)/2=95000 (170000+0)/2=85000

ARR 58333/95000*100=61.40% 55000/85000*100=64.71%

In accordance with the average rate of return (ARR) technique of capital budgeting,

machine A has value of 61.40% at the end of project life which is 6 years. Apart from this,

machine B has ARR is 64.71% which is lower than first alternative available with local

manufacturing firm. On the basis of this method, project A is viable as well as profitable for

purchasing machine.

From the above analysis of investment appraisal methods, it can be assessed that machine

A provides more NPV and ARR value i.e. £113757 and 32.35% respectively. Apart from this,

money invested at the initial time for purchasing machine is also recovered within 1.9 years.

Henceforth, it can be suggested to management of local manufacturing firm that it should make

investment in the first project. Further, machine A will be the most and highly profitable in

comparison to second for implementing at the workplace.

B) Discussing limitations associated with investment appraisal technique for taking long-term

decisions

Along with helping some decisions in the working environment, investment appraisal

methods have some drawbacks also which are described as below:

Several tools of capital budgeting ignoring time value of money at the time of performing

proper calculations and make decisions. However, only net present value method

considers this particular aspect (Samonas, 2015).

16

2019 65000 45000

2020 55000 75000

2021 55000 85000

2022 45000 65000

Total net profit 350000 330000

Average accounting net profit 350000/6=58333 330000/6=55000

Average investment (170000+20000)/2=95000 (170000+0)/2=85000

ARR 58333/95000*100=61.40% 55000/85000*100=64.71%

In accordance with the average rate of return (ARR) technique of capital budgeting,

machine A has value of 61.40% at the end of project life which is 6 years. Apart from this,

machine B has ARR is 64.71% which is lower than first alternative available with local

manufacturing firm. On the basis of this method, project A is viable as well as profitable for

purchasing machine.

From the above analysis of investment appraisal methods, it can be assessed that machine

A provides more NPV and ARR value i.e. £113757 and 32.35% respectively. Apart from this,

money invested at the initial time for purchasing machine is also recovered within 1.9 years.

Henceforth, it can be suggested to management of local manufacturing firm that it should make

investment in the first project. Further, machine A will be the most and highly profitable in

comparison to second for implementing at the workplace.

B) Discussing limitations associated with investment appraisal technique for taking long-term

decisions

Along with helping some decisions in the working environment, investment appraisal

methods have some drawbacks also which are described as below:

Several tools of capital budgeting ignoring time value of money at the time of performing

proper calculations and make decisions. However, only net present value method

considers this particular aspect (Samonas, 2015).

16

This is not useful for taking those investment decisions which are for short period of time

at the workplace. Further, these techniques are of the irreversible nature at most of the

times in the business environment.

Calculation of capital budgeting tools are based on various assumptions as well as

estimations. Further, situation of the future market are uncertain where company cannot

predict for long term.

This technique remains introspective in its nature due to which profitable kind of

investment decisions cannot be made. The reason behind this is that, risk and discounting

both the factors remain unchanged for the project life while performing calculations.

Apart from this, wrong investment appraisal decisions can create negative impact on long

term durability of the business (Capital Budgeting – Advantages and Disadvantages,

2016). Therefore, highly talented as well as skilled professional of the financials is

required to hire in the company.

Limitations of ARR:

This technique is helpful in analysing the returns a business will going to acquire from

the cost of investments made in new operations. The limitation lies over it as it only considers

the practice aspects as it ignores the time value of money. Therefore, it is been unhealthy for the

financial stability.

Limitations of NPV:

This method will help in analysis the present value of future investments but it did not

help in improving the profitability of firm.

Limitations of payback period:

This technique is used to determine the time over which the firm will going to have that

must gains that they have invested in the project. It also does not bring adequate profitability or

helps in decision making.

CONCLUSION

Hereby, it can be articulated that when financial resources are managed effectively in the

business then company able to boost up its financial performance in the industry. As per the ratio

17

at the workplace. Further, these techniques are of the irreversible nature at most of the

times in the business environment.

Calculation of capital budgeting tools are based on various assumptions as well as

estimations. Further, situation of the future market are uncertain where company cannot

predict for long term.

This technique remains introspective in its nature due to which profitable kind of

investment decisions cannot be made. The reason behind this is that, risk and discounting

both the factors remain unchanged for the project life while performing calculations.

Apart from this, wrong investment appraisal decisions can create negative impact on long

term durability of the business (Capital Budgeting – Advantages and Disadvantages,

2016). Therefore, highly talented as well as skilled professional of the financials is

required to hire in the company.

Limitations of ARR:

This technique is helpful in analysing the returns a business will going to acquire from

the cost of investments made in new operations. The limitation lies over it as it only considers

the practice aspects as it ignores the time value of money. Therefore, it is been unhealthy for the

financial stability.

Limitations of NPV:

This method will help in analysis the present value of future investments but it did not

help in improving the profitability of firm.

Limitations of payback period:

This technique is used to determine the time over which the firm will going to have that

must gains that they have invested in the project. It also does not bring adequate profitability or

helps in decision making.

CONCLUSION

Hereby, it can be articulated that when financial resources are managed effectively in the

business then company able to boost up its financial performance in the industry. As per the ratio

17

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

analysis it can be said that, Sports Direct International Plc performing poor in comparison to JD

Sports Fashion Plc at the end of financial year 2015 and 2016 both. However, in terms of net

profit and current ratio only Sports Direct perform better. From the second part it can be

summarised that, machine A generates higher NPV and ARR as well as lower payback period at

as compared to machine B. Hence, management of local manufacturing firm needs to invest

money in project A which will be the most beneficial.

18

Sports Fashion Plc at the end of financial year 2015 and 2016 both. However, in terms of net

profit and current ratio only Sports Direct perform better. From the second part it can be

summarised that, machine A generates higher NPV and ARR as well as lower payback period at

as compared to machine B. Hence, management of local manufacturing firm needs to invest

money in project A which will be the most beneficial.

18

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.