Effective Planning Tools for Managing Accounts Part 2

VerifiedAdded on 2023/06/18

|19

|5920

|460

AI Summary

This report discusses management accounting, its role, methods, and planning tools. It also explains different types of management accounting systems like cost accounting, inventory management, job costing, and price optimizing systems. The report further explores costing systems like marginal and absorption costing and their benefits. Additionally, it examines monetary difficulties and the use of planned technology. The case study is based on Sollatek, UK, a manufacturing company dealing in tubes and valves.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

TABLE OF CONTENTS..............................................................................................................2

INTRODUCTION...........................................................................................................................3

Explain management accounting and give the essential requirements of different types of

management accounting systems................................................................................................3

Evaluating management accounting systems and management accounting reporting is

integrated within organizational processes.................................................................................4

Benefits of management accounting system...............................................................................4

Calculating costs using marginal and absorption costing and preparing income statement.......5

Monetary difficulties are examined............................................................................................8

The use of a planned technology...............................................................................................11

PART 2..........................................................................................................................................12

The benefits and drawbacks of different kinds of preparation instruments..............................12

Organizations are developing managerial accountancy systems in different approaches, as

seen through comparisons.........................................................................................................13

Assessment of a fiscal problem.................................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................17

TABLE OF CONTENTS..............................................................................................................2

INTRODUCTION...........................................................................................................................3

Explain management accounting and give the essential requirements of different types of

management accounting systems................................................................................................3

Evaluating management accounting systems and management accounting reporting is

integrated within organizational processes.................................................................................4

Benefits of management accounting system...............................................................................4

Calculating costs using marginal and absorption costing and preparing income statement.......5

Monetary difficulties are examined............................................................................................8

The use of a planned technology...............................................................................................11

PART 2..........................................................................................................................................12

The benefits and drawbacks of different kinds of preparation instruments..............................12

Organizations are developing managerial accountancy systems in different approaches, as

seen through comparisons.........................................................................................................13

Assessment of a fiscal problem.................................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................17

INTRODUCTION

Management accounting is the study of maintaining reports about business activities that

help the top-level management in order to make long term and short term business decisions. By

identifying business goals and strategies the managers of company make better and evidence

based strategic decisions. The case study will give detailed information about Sollatek, UK, the

manufacturing company deals in tubes and valves. The report will explore role, methods,

planning tools of management accounting systems. Further the case study will outline principles

and types of management accounting systems. In addition to this, the present report will give

types of managerial reports. Managerial accountancy is among the most efficient techniques for

assisting an enterprise in recording and summarising numerous monetary transactions which

occur inside a division (Andarwati, Nirwanto and Darsono, 2018). The major goal of accountants

and financial management is to gather numerous pieces of statistics from diverse suppliers in

order to ensure that finances are capable to satisfy the corporation's needs. It is carried out with

the intention of achieving an organization's short- and long-term aims and outcomes. There seem

to be a number of important factors to consider in order to maximise your yield in the coming

years. This method of production intends to provide important data regarding different aspects of

financial platforms, which are excellent resources for keeping track of important transactions in

the division. Aside from that, many forms of accountancy disclosure practices are considered

while analysing their advantages to the Sollatek organisation. In the same way, multiple pricing

strategies are employed to compute operating revenue. There are benefits and drawbacks to

employing a variety of preparatory techniques for budgeting process. Finally, a comparative with

other organisations is made to see how a managerial structure could deal with fiscal challenges

that develop in a company.

Explain management accounting and give the essential requirements of different types of

management accounting systems

Management accounting

It is the presentation of accounting related information to management of the company in

order to formulate the various business policies and assist in it daily business operations (An

overview of management accounting, 2021). It also means that it helps the managers to performs

all business related function including organizing, planning, controlling, budgeting. The main

Management accounting is the study of maintaining reports about business activities that

help the top-level management in order to make long term and short term business decisions. By

identifying business goals and strategies the managers of company make better and evidence

based strategic decisions. The case study will give detailed information about Sollatek, UK, the

manufacturing company deals in tubes and valves. The report will explore role, methods,

planning tools of management accounting systems. Further the case study will outline principles

and types of management accounting systems. In addition to this, the present report will give

types of managerial reports. Managerial accountancy is among the most efficient techniques for

assisting an enterprise in recording and summarising numerous monetary transactions which

occur inside a division (Andarwati, Nirwanto and Darsono, 2018). The major goal of accountants

and financial management is to gather numerous pieces of statistics from diverse suppliers in

order to ensure that finances are capable to satisfy the corporation's needs. It is carried out with

the intention of achieving an organization's short- and long-term aims and outcomes. There seem

to be a number of important factors to consider in order to maximise your yield in the coming

years. This method of production intends to provide important data regarding different aspects of

financial platforms, which are excellent resources for keeping track of important transactions in

the division. Aside from that, many forms of accountancy disclosure practices are considered

while analysing their advantages to the Sollatek organisation. In the same way, multiple pricing

strategies are employed to compute operating revenue. There are benefits and drawbacks to

employing a variety of preparatory techniques for budgeting process. Finally, a comparative with

other organisations is made to see how a managerial structure could deal with fiscal challenges

that develop in a company.

Explain management accounting and give the essential requirements of different types of

management accounting systems

Management accounting

It is the presentation of accounting related information to management of the company in

order to formulate the various business policies and assist in it daily business operations (An

overview of management accounting, 2021). It also means that it helps the managers to performs

all business related function including organizing, planning, controlling, budgeting. The main

objective is to avoid errors and minimize losses in order to make profit, it will ultimately

increase productivity.

Role of management accounting

The most important role is to analyse cost to determine the existing company expenses

and give relevant and proper suggestions for the future requirement and business activities

(Mahmoudian and et.al., 2021). After cost and budget analysis, the management team of the

company can make decisions which is beneficial for the firm. In order to direct financial

processes the managers of the company identifies past trends and predict future requirements for

decision-making process related to spending, budget, costs and sales.

Management accounting system and its role

The systematic process of control used by management team in order to influence

members to achieve business goals and objectives within the company (Massicotte and Henri,

2021). The company uses this system to save time and costs as it improve financial visibility and

develop asset and inventor management. A major importance of this system is that it gives high

flexibility and enhance decision-making process and minimizes various errors in terms of

accounting.

Role- This system plays a vital role in forecasting future business needs and for making plans

such as strategic management accounting and market study. With the help of this system, the

management team can analyse and maintain reports such as cash flow statements, liquidity and

others.

Evaluating management accounting systems and management accounting reporting is integrated

within organizational processes.

This system and process helps managers to make business decision with the help of

budgeting in order to control unnecessary control (NGUYEN and NGUYEN, 2021).

Comparing the budget to actual expenses to evaluate the financial information.

It provides brief information of company's resource flow and divides what is beneficial

and detects errors to form long term strategies to measure health of organization and on

the basis of that make effective production and budget decisions.

Benefits of management accounting system

Compiling and designing- In order to meet the requirements of business, the firm should

design and compile the accounting reports and statements with respect to past, present and future

increase productivity.

Role of management accounting

The most important role is to analyse cost to determine the existing company expenses

and give relevant and proper suggestions for the future requirement and business activities

(Mahmoudian and et.al., 2021). After cost and budget analysis, the management team of the

company can make decisions which is beneficial for the firm. In order to direct financial

processes the managers of the company identifies past trends and predict future requirements for

decision-making process related to spending, budget, costs and sales.

Management accounting system and its role

The systematic process of control used by management team in order to influence

members to achieve business goals and objectives within the company (Massicotte and Henri,

2021). The company uses this system to save time and costs as it improve financial visibility and

develop asset and inventor management. A major importance of this system is that it gives high

flexibility and enhance decision-making process and minimizes various errors in terms of

accounting.

Role- This system plays a vital role in forecasting future business needs and for making plans

such as strategic management accounting and market study. With the help of this system, the

management team can analyse and maintain reports such as cash flow statements, liquidity and

others.

Evaluating management accounting systems and management accounting reporting is integrated

within organizational processes.

This system and process helps managers to make business decision with the help of

budgeting in order to control unnecessary control (NGUYEN and NGUYEN, 2021).

Comparing the budget to actual expenses to evaluate the financial information.

It provides brief information of company's resource flow and divides what is beneficial

and detects errors to form long term strategies to measure health of organization and on

the basis of that make effective production and budget decisions.

Benefits of management accounting system

Compiling and designing- In order to meet the requirements of business, the firm should

design and compile the accounting reports and statements with respect to past, present and future

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

results (Maheshwari, Maheshwari and Maheshwari, 2021). The sollatek must design reports of

accounting in such a way including relevant business and cost data which can be modified in

order to meet the needs of organization.

Accounting for inflation- The company cannot earn profit unless capital is maintained in

real terms. So, it is important to measure the value of capital contributed by higher level

managers, owners and promoters in terms of real value of money. Therefore, in this way the rate

of inflation is taken into consideration by company in order to judge the performance and

potential of the business.

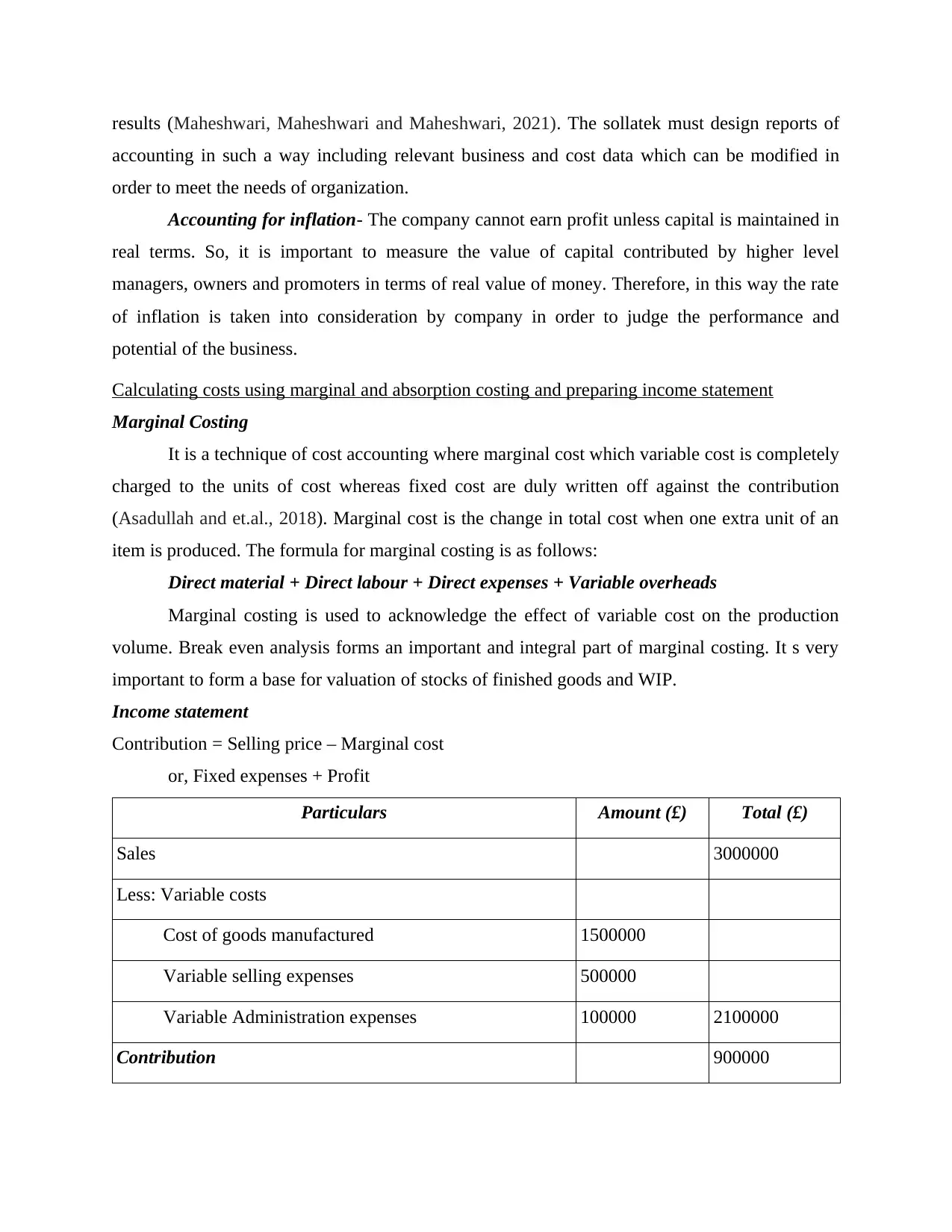

Calculating costs using marginal and absorption costing and preparing income statement

Marginal Costing

It is a technique of cost accounting where marginal cost which variable cost is completely

charged to the units of cost whereas fixed cost are duly written off against the contribution

(Asadullah and et.al., 2018). Marginal cost is the change in total cost when one extra unit of an

item is produced. The formula for marginal costing is as follows:

Direct material + Direct labour + Direct expenses + Variable overheads

Marginal costing is used to acknowledge the effect of variable cost on the production

volume. Break even analysis forms an important and integral part of marginal costing. It s very

important to form a base for valuation of stocks of finished goods and WIP.

Income statement

Contribution = Selling price – Marginal cost

or, Fixed expenses + Profit

Particulars Amount (£) Total (£)

Sales 3000000

Less: Variable costs

Cost of goods manufactured 1500000

Variable selling expenses 500000

Variable Administration expenses 100000 2100000

Contribution 900000

accounting in such a way including relevant business and cost data which can be modified in

order to meet the needs of organization.

Accounting for inflation- The company cannot earn profit unless capital is maintained in

real terms. So, it is important to measure the value of capital contributed by higher level

managers, owners and promoters in terms of real value of money. Therefore, in this way the rate

of inflation is taken into consideration by company in order to judge the performance and

potential of the business.

Calculating costs using marginal and absorption costing and preparing income statement

Marginal Costing

It is a technique of cost accounting where marginal cost which variable cost is completely

charged to the units of cost whereas fixed cost are duly written off against the contribution

(Asadullah and et.al., 2018). Marginal cost is the change in total cost when one extra unit of an

item is produced. The formula for marginal costing is as follows:

Direct material + Direct labour + Direct expenses + Variable overheads

Marginal costing is used to acknowledge the effect of variable cost on the production

volume. Break even analysis forms an important and integral part of marginal costing. It s very

important to form a base for valuation of stocks of finished goods and WIP.

Income statement

Contribution = Selling price – Marginal cost

or, Fixed expenses + Profit

Particulars Amount (£) Total (£)

Sales 3000000

Less: Variable costs

Cost of goods manufactured 1500000

Variable selling expenses 500000

Variable Administration expenses 100000 2100000

Contribution 900000

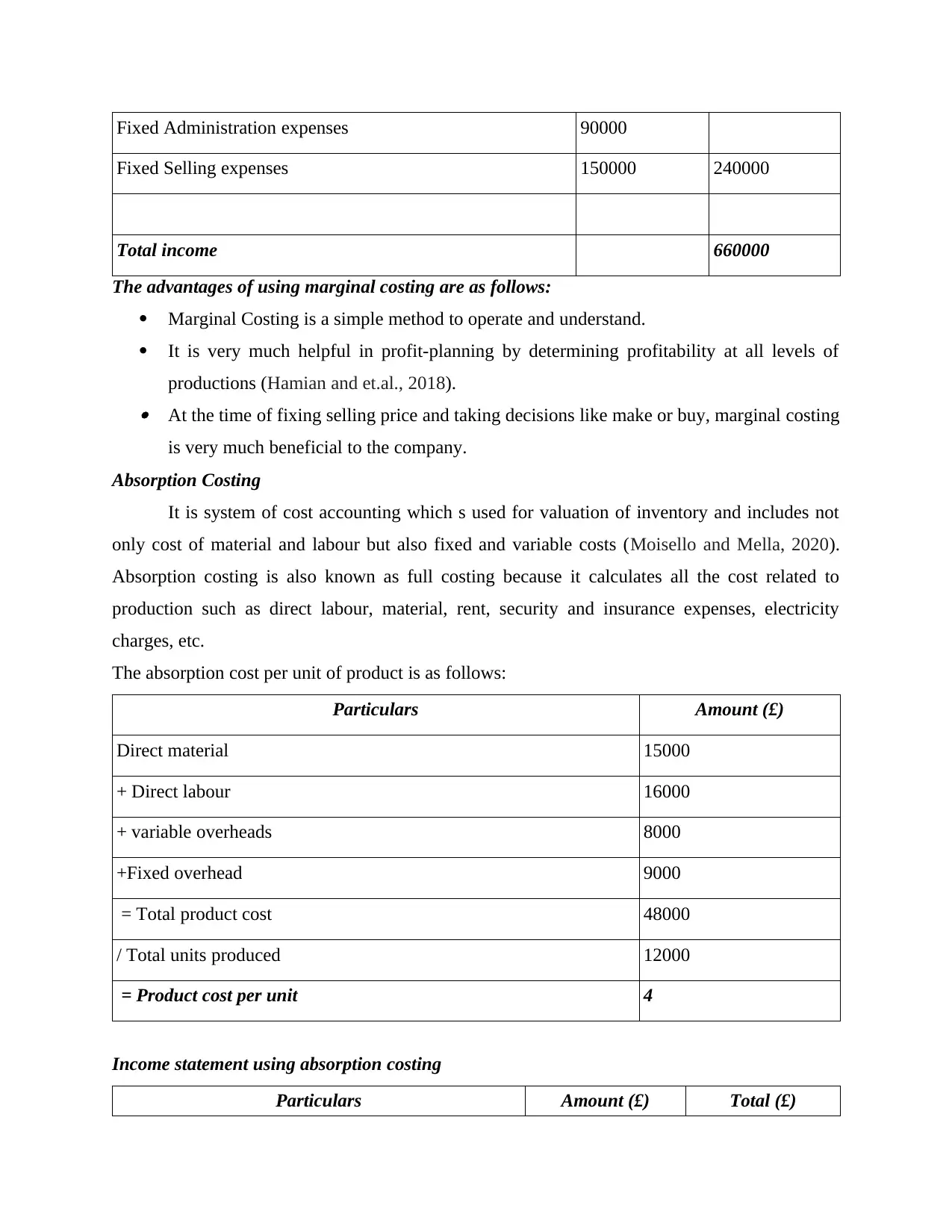

Fixed Administration expenses 90000

Fixed Selling expenses 150000 240000

Total income 660000

The advantages of using marginal costing are as follows:

Marginal Costing is a simple method to operate and understand.

It is very much helpful in profit-planning by determining profitability at all levels of

productions (Hamian and et.al., 2018). At the time of fixing selling price and taking decisions like make or buy, marginal costing

is very much beneficial to the company.

Absorption Costing

It is system of cost accounting which s used for valuation of inventory and includes not

only cost of material and labour but also fixed and variable costs (Moisello and Mella, 2020).

Absorption costing is also known as full costing because it calculates all the cost related to

production such as direct labour, material, rent, security and insurance expenses, electricity

charges, etc.

The absorption cost per unit of product is as follows:

Particulars Amount (£)

Direct material 15000

+ Direct labour 16000

+ variable overheads 8000

+Fixed overhead 9000

= Total product cost 48000

/ Total units produced 12000

= Product cost per unit 4

Income statement using absorption costing

Particulars Amount (£) Total (£)

Fixed Selling expenses 150000 240000

Total income 660000

The advantages of using marginal costing are as follows:

Marginal Costing is a simple method to operate and understand.

It is very much helpful in profit-planning by determining profitability at all levels of

productions (Hamian and et.al., 2018). At the time of fixing selling price and taking decisions like make or buy, marginal costing

is very much beneficial to the company.

Absorption Costing

It is system of cost accounting which s used for valuation of inventory and includes not

only cost of material and labour but also fixed and variable costs (Moisello and Mella, 2020).

Absorption costing is also known as full costing because it calculates all the cost related to

production such as direct labour, material, rent, security and insurance expenses, electricity

charges, etc.

The absorption cost per unit of product is as follows:

Particulars Amount (£)

Direct material 15000

+ Direct labour 16000

+ variable overheads 8000

+Fixed overhead 9000

= Total product cost 48000

/ Total units produced 12000

= Product cost per unit 4

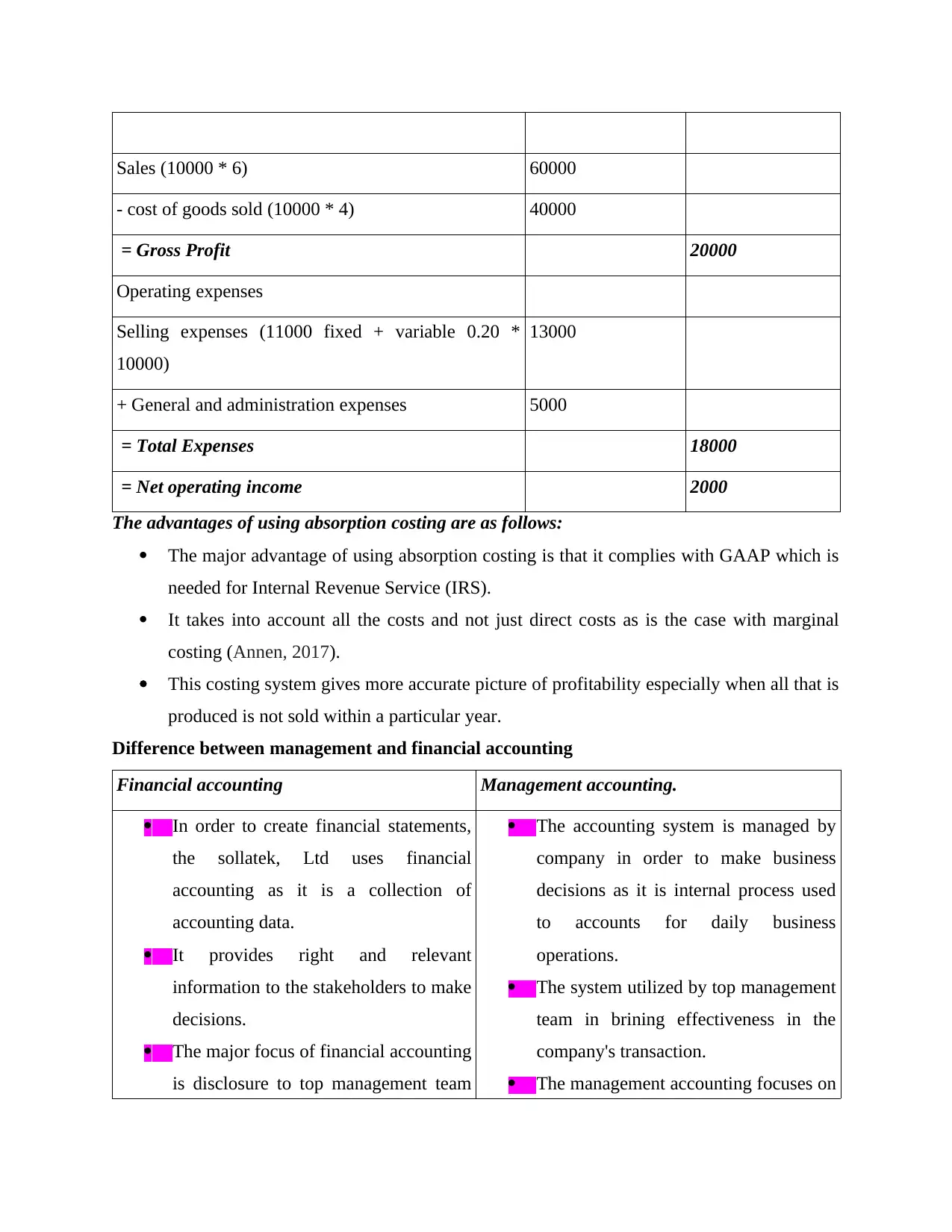

Income statement using absorption costing

Particulars Amount (£) Total (£)

Sales (10000 * 6) 60000

- cost of goods sold (10000 * 4) 40000

= Gross Profit 20000

Operating expenses

Selling expenses (11000 fixed + variable 0.20 *

10000)

13000

+ General and administration expenses 5000

= Total Expenses 18000

= Net operating income 2000

The advantages of using absorption costing are as follows:

The major advantage of using absorption costing is that it complies with GAAP which is

needed for Internal Revenue Service (IRS).

It takes into account all the costs and not just direct costs as is the case with marginal

costing (Annen, 2017).

This costing system gives more accurate picture of profitability especially when all that is

produced is not sold within a particular year.

Difference between management and financial accounting

Financial accounting Management accounting.

In order to create financial statements,

the sollatek, Ltd uses financial

accounting as it is a collection of

accounting data.

It provides right and relevant

information to the stakeholders to make

decisions.

The major focus of financial accounting

is disclosure to top management team

The accounting system is managed by

company in order to make business

decisions as it is internal process used

to accounts for daily business

operations.

The system utilized by top management

team in brining effectiveness in the

company's transaction.

The management accounting focuses on

- cost of goods sold (10000 * 4) 40000

= Gross Profit 20000

Operating expenses

Selling expenses (11000 fixed + variable 0.20 *

10000)

13000

+ General and administration expenses 5000

= Total Expenses 18000

= Net operating income 2000

The advantages of using absorption costing are as follows:

The major advantage of using absorption costing is that it complies with GAAP which is

needed for Internal Revenue Service (IRS).

It takes into account all the costs and not just direct costs as is the case with marginal

costing (Annen, 2017).

This costing system gives more accurate picture of profitability especially when all that is

produced is not sold within a particular year.

Difference between management and financial accounting

Financial accounting Management accounting.

In order to create financial statements,

the sollatek, Ltd uses financial

accounting as it is a collection of

accounting data.

It provides right and relevant

information to the stakeholders to make

decisions.

The major focus of financial accounting

is disclosure to top management team

The accounting system is managed by

company in order to make business

decisions as it is internal process used

to accounts for daily business

operations.

The system utilized by top management

team in brining effectiveness in the

company's transaction.

The management accounting focuses on

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

in the firm (Lee, 2020). The reports are

being prepared is useful to customers,

banks and suppliers etc.

Generally, the time horizon is past such

as one accounting year in financial

accounting.

Financial accounting systems provides

financial information which gives an

idea about health of business.

giving information about financial

health of business and providing

suggestion for necessary improvements.

The focus is on the future as it has no

specific time horizon for management

accounting.

The reports are being prepared is useful

to parties such as CEO, directors and

top-level managers, promoters.

It is being prepared for financial and

non-financial information which can be

used by management while making

decisions.

Monetary difficulties are examined

As a result of the aforementioned study, it has been determined that fiscal concerns and

administration are both characterized in this framework. As previously said, competitiveness and

effectiveness are two monetary factors which must be considered while creating an

organization's strategies and aspirations (Sledgianowski, Gomaa and Tan, 2017). To manage and

monitor all of such difficulties, the company employs a variety of technologies and tactics that

can help them grow their company while keeping it secure from harm. This one has been

observed that organisations that use outdated frameworks are unable to achieve organizational

goals and objectives. It has been determined that the great proportion of the firm's business

procedure is in need of improvement. It should have a huge impact on the business survival.

Someone could manage their day-to-day company risks by applying financial management and

quality arrangement indicators.

Types of management accounting systems

cost accounting systems- It is the system used to estimate the product costs for

profitability analysis, cost control and inventory valuation. The major role of cost accounting

system is to lower the cost of the business transaction in order to make profit. By controlling

relevant items in the company, will help to improve profit maximization. Sollatek ltd uses this

being prepared is useful to customers,

banks and suppliers etc.

Generally, the time horizon is past such

as one accounting year in financial

accounting.

Financial accounting systems provides

financial information which gives an

idea about health of business.

giving information about financial

health of business and providing

suggestion for necessary improvements.

The focus is on the future as it has no

specific time horizon for management

accounting.

The reports are being prepared is useful

to parties such as CEO, directors and

top-level managers, promoters.

It is being prepared for financial and

non-financial information which can be

used by management while making

decisions.

Monetary difficulties are examined

As a result of the aforementioned study, it has been determined that fiscal concerns and

administration are both characterized in this framework. As previously said, competitiveness and

effectiveness are two monetary factors which must be considered while creating an

organization's strategies and aspirations (Sledgianowski, Gomaa and Tan, 2017). To manage and

monitor all of such difficulties, the company employs a variety of technologies and tactics that

can help them grow their company while keeping it secure from harm. This one has been

observed that organisations that use outdated frameworks are unable to achieve organizational

goals and objectives. It has been determined that the great proportion of the firm's business

procedure is in need of improvement. It should have a huge impact on the business survival.

Someone could manage their day-to-day company risks by applying financial management and

quality arrangement indicators.

Types of management accounting systems

cost accounting systems- It is the system used to estimate the product costs for

profitability analysis, cost control and inventory valuation. The major role of cost accounting

system is to lower the cost of the business transaction in order to make profit. By controlling

relevant items in the company, will help to improve profit maximization. Sollatek ltd uses this

system to make good costing system by ensuring proper accounting for labour, overheads and

materials.

Benefits- using this system will benefit the company to minimize wastage and determine the

selling price of products (Mishra, Wu and Sarkar, 2021). Cost accounting system calculate the

profit and loss made on each product in the company in order to make profitability. It provides

data related to cost that helps in fixing prices of products and services.

Inventory management systems- It is the system in which the company keep track on

goods throughout their entire supply chain (Muller, 2019). It gives information about inventory

management approaches in the business. The process provides a real time view of inventory

across all selling channels in the company. Sollatek ltd uses ERP method of inventory

management that is enterprise resources planning which allows to manage all activities of their

business including finance, logistics and planning.

Benefits- it beneficial for company because it helps to manage multiple locations and stock outs,

keep proper records of stock (Wild, 2017). This system reduced risk of overselling to control

unnecessary expenditure. It improves business negotiation for cost savings while making

inventory related decisions. The system helps to minimize stock outs and excess stock in order to

simplify inventory management so that company can take inventory control decisions.

Job costing systems- This system is utilized by company to keep track on cost of

materials that are used during course of the job and provides information about them. The

sollatek ltd can use this process for determining if the job is profitable or not.

Benefits- The system provides analysis of the labour, overhead and materials for each job in the

company. It will be useful for accounting system in company because it can easily keep record

on all expenses on daily basis.

Price optimizing systems- This system gives proper understanding about how much

business the company obtain within profitability levels on the basis of how sensitive their

customer are to changes in prices of product (Liu and Sustik, 2021). It is mathematical process

that can calculate about the demand of products at different price levels. The company combine

that important data with inventory levels in order to suggest prices that will ultimately increase

profit margins.

materials.

Benefits- using this system will benefit the company to minimize wastage and determine the

selling price of products (Mishra, Wu and Sarkar, 2021). Cost accounting system calculate the

profit and loss made on each product in the company in order to make profitability. It provides

data related to cost that helps in fixing prices of products and services.

Inventory management systems- It is the system in which the company keep track on

goods throughout their entire supply chain (Muller, 2019). It gives information about inventory

management approaches in the business. The process provides a real time view of inventory

across all selling channels in the company. Sollatek ltd uses ERP method of inventory

management that is enterprise resources planning which allows to manage all activities of their

business including finance, logistics and planning.

Benefits- it beneficial for company because it helps to manage multiple locations and stock outs,

keep proper records of stock (Wild, 2017). This system reduced risk of overselling to control

unnecessary expenditure. It improves business negotiation for cost savings while making

inventory related decisions. The system helps to minimize stock outs and excess stock in order to

simplify inventory management so that company can take inventory control decisions.

Job costing systems- This system is utilized by company to keep track on cost of

materials that are used during course of the job and provides information about them. The

sollatek ltd can use this process for determining if the job is profitable or not.

Benefits- The system provides analysis of the labour, overhead and materials for each job in the

company. It will be useful for accounting system in company because it can easily keep record

on all expenses on daily basis.

Price optimizing systems- This system gives proper understanding about how much

business the company obtain within profitability levels on the basis of how sensitive their

customer are to changes in prices of product (Liu and Sustik, 2021). It is mathematical process

that can calculate about the demand of products at different price levels. The company combine

that important data with inventory levels in order to suggest prices that will ultimately increase

profit margins.

Benefits- customers are more attracted to pick up on products when they feel priced optimally

so, the company utilize this method to maximize its sales and profits. The best price of product

will allow company to achieve potential.

Presenting financial information-

It is important to provide financial and accounting information on time and accurate in

order to make business decisions (Ramachandran and Kakani, 2020). In the presence of

reliable information and details, organization can make better decisions, it will be able to

help other employees to make productive decisions.

The information provided in the financial accounting and management accounting must

be easily understandable and explicit by their users. The proper information must be

presented in effective way that the users do not get confused while making any relevant

decisions. Additionally, too much use of confusing statement must be avoided and easy

language must be used. In order to identify trends in performance the company can

compare with same information.

If the information provided in financial statements becomes complicated for the users and

unable to read properly, then the purpose of making business plans weakens. The

accounting information is reliable if it is free from material error and wrong details. In

addition to that, increasing the relevance of financial information includes maximizing

the confirmatory value so that any error can be avoided by the user.

Types of reports

Cost accounting report-This method includes information of provider such as data

utilization, charges and cost by centre. The report is helpful to keep the customer informed and

help them to control costs (Zhao, 2020). The report is utilized by firm to determine the cost per

equivalent unit in the project. Profit margins and unnecessary expenditure are estimated with the

help of cost report in the management accounting systems.

Budget report- In order to make proper list to know past estimated budget over a time

period the company utilizes this method. A company's budget report shows all the profit and loss

to measure the financial or actual position. If the company's budget report is well-designed then

it will be easy to achieve target (Loft, 2020). In the firm the budget report is also maintained to

provide incentives to employees that motivated them to achieve success. This method is used by

so, the company utilize this method to maximize its sales and profits. The best price of product

will allow company to achieve potential.

Presenting financial information-

It is important to provide financial and accounting information on time and accurate in

order to make business decisions (Ramachandran and Kakani, 2020). In the presence of

reliable information and details, organization can make better decisions, it will be able to

help other employees to make productive decisions.

The information provided in the financial accounting and management accounting must

be easily understandable and explicit by their users. The proper information must be

presented in effective way that the users do not get confused while making any relevant

decisions. Additionally, too much use of confusing statement must be avoided and easy

language must be used. In order to identify trends in performance the company can

compare with same information.

If the information provided in financial statements becomes complicated for the users and

unable to read properly, then the purpose of making business plans weakens. The

accounting information is reliable if it is free from material error and wrong details. In

addition to that, increasing the relevance of financial information includes maximizing

the confirmatory value so that any error can be avoided by the user.

Types of reports

Cost accounting report-This method includes information of provider such as data

utilization, charges and cost by centre. The report is helpful to keep the customer informed and

help them to control costs (Zhao, 2020). The report is utilized by firm to determine the cost per

equivalent unit in the project. Profit margins and unnecessary expenditure are estimated with the

help of cost report in the management accounting systems.

Budget report- In order to make proper list to know past estimated budget over a time

period the company utilizes this method. A company's budget report shows all the profit and loss

to measure the financial or actual position. If the company's budget report is well-designed then

it will be easy to achieve target (Loft, 2020). In the firm the budget report is also maintained to

provide incentives to employees that motivated them to achieve success. This method is used by

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

managers within the company to compare the estimations of budget with the accurate results

achieved during the business activities.

Account receivable Aging report - This method is adopted by sollatek ltd manager to

show the invoice balances which is unpaid with the time period they have been outstanding. The

firm can layout credit and selling practices within business activities. It keeps track on slow

paying clients for the business operations (Dutta, Paitya and Majumdar, 2020). The firm used

this method to attain detailed analysis of problems associated with company collection process.

The company is suggested to identify and measure irregularities in the report and improve

efficiencies.

Inventory report- This method used to know about how much stock the firm have, its

performance in the competitive market, the fastest selling products and also inventory

performance within the company (Inventory management systems, 2021). It is said by managers

of sollatek that manufacturing process can become more effective and efficient with the help of

this method. Additionally, the inventory report also shows comparison between different

assembly lines and find out the opportunities for development to attain required target and goals.

Proper and well-organized inventory reports can show over-ordering inventory to keep track

budget and control it in order to reduce uncertainty.

Performance report- This method is adopted by company which shows them overall

departmental reports to make strategic decisions (Al-Dmour, Zaidan and Al Natour, 2021). The

firm keeps an accurate measure of its financial strategy. In addition to that, management must

determine the evaluation of competitor analysis and its marketing strategy. To attain the most

effective financial decisions the company must have authentic managerial accounting report.

The use of a planned technology

Preparation techniques are auxiliary methods that assist practically any company,

especially Sollatek, in predicting upcoming occurrences. Prediction is being intended to

anticipate the upcoming occurrences, whereas contingencies preparation aids in the development

of preventive strategies and strategic preparation aids in the capture of various hypothetical

situations. A company utilizes such approaches to predict whether potential challenges might

arise. Budgeting management is perhaps the most integral function of such techniques, and

planned components aid in the preparation of various budgeting such as revenue and marketing

budgeting.

achieved during the business activities.

Account receivable Aging report - This method is adopted by sollatek ltd manager to

show the invoice balances which is unpaid with the time period they have been outstanding. The

firm can layout credit and selling practices within business activities. It keeps track on slow

paying clients for the business operations (Dutta, Paitya and Majumdar, 2020). The firm used

this method to attain detailed analysis of problems associated with company collection process.

The company is suggested to identify and measure irregularities in the report and improve

efficiencies.

Inventory report- This method used to know about how much stock the firm have, its

performance in the competitive market, the fastest selling products and also inventory

performance within the company (Inventory management systems, 2021). It is said by managers

of sollatek that manufacturing process can become more effective and efficient with the help of

this method. Additionally, the inventory report also shows comparison between different

assembly lines and find out the opportunities for development to attain required target and goals.

Proper and well-organized inventory reports can show over-ordering inventory to keep track

budget and control it in order to reduce uncertainty.

Performance report- This method is adopted by company which shows them overall

departmental reports to make strategic decisions (Al-Dmour, Zaidan and Al Natour, 2021). The

firm keeps an accurate measure of its financial strategy. In addition to that, management must

determine the evaluation of competitor analysis and its marketing strategy. To attain the most

effective financial decisions the company must have authentic managerial accounting report.

The use of a planned technology

Preparation techniques are auxiliary methods that assist practically any company,

especially Sollatek, in predicting upcoming occurrences. Prediction is being intended to

anticipate the upcoming occurrences, whereas contingencies preparation aids in the development

of preventive strategies and strategic preparation aids in the capture of various hypothetical

situations. A company utilizes such approaches to predict whether potential challenges might

arise. Budgeting management is perhaps the most integral function of such techniques, and

planned components aid in the preparation of various budgeting such as revenue and marketing

budgeting.

PART 2

The benefits and drawbacks of different kinds of preparation instruments

Budgeting management is the process of creating and managing amount of money in

attempt to prepare for the foreseeable. Such budgeting involves determining prospective

expenditures and revenue, which necessitates the usage of effective and strategic forecasting

technologies such that the company could forecast upcoming occurrences with near-perfect

accuracy. The following are some of those compromises:

Cash forecast: A liquid spending plan is a forecast of all monetary costs and revenues

that are projected to happen in the coming fiscal term (Bühler, Wallenburg and Wieland,

2016).

Sales forecast: A selling spending plan is a documentation that forecasts all potential

selling that are anticipated to happen in the prospective, depending on previous total

transactions, customer needs, and competitive effectiveness.

Scheduling is a procedure that entails the creation of clear proposals and regulations to

aid in the judgement call procedure. There are certain instruments that may be used to carry out

the preparation and implementation and aid in effective long term forecasting. The following are

the techniques:

Preparedness mechanism- A contingencies methodology is a preparation technique that

aids Sollatek in arranging specific preventative steps in the case of potential unforeseen events.

Those concerns could indeed be ecological or material; examples of ecological uncertainty

include floods, fires, and other weather events; examples of tangible risks include robbery,

protest, and shutdown (Glushchenko, Yarkova and Kucherova, 2017).

Benefits: The contingencies strategy is required for making a mitigation strategy that

serves as a backup method in the event of a crisis. This strategy reduces fear and disorder

in the workplace. Sollatek can use this technology to manage damage in unexpected

scenarios.

Drawbacks: Management and preparation consumes a considerable amount of effort and

resources because it takes highly experienced personnel to create it, but if none of the

unexpected events arise, all of the preparations are useless.

Predicting tools- Prediction is a management technique that uses methodologies including

market analysis, competition analysis, and reviewing previous encounters to anticipate major

The benefits and drawbacks of different kinds of preparation instruments

Budgeting management is the process of creating and managing amount of money in

attempt to prepare for the foreseeable. Such budgeting involves determining prospective

expenditures and revenue, which necessitates the usage of effective and strategic forecasting

technologies such that the company could forecast upcoming occurrences with near-perfect

accuracy. The following are some of those compromises:

Cash forecast: A liquid spending plan is a forecast of all monetary costs and revenues

that are projected to happen in the coming fiscal term (Bühler, Wallenburg and Wieland,

2016).

Sales forecast: A selling spending plan is a documentation that forecasts all potential

selling that are anticipated to happen in the prospective, depending on previous total

transactions, customer needs, and competitive effectiveness.

Scheduling is a procedure that entails the creation of clear proposals and regulations to

aid in the judgement call procedure. There are certain instruments that may be used to carry out

the preparation and implementation and aid in effective long term forecasting. The following are

the techniques:

Preparedness mechanism- A contingencies methodology is a preparation technique that

aids Sollatek in arranging specific preventative steps in the case of potential unforeseen events.

Those concerns could indeed be ecological or material; examples of ecological uncertainty

include floods, fires, and other weather events; examples of tangible risks include robbery,

protest, and shutdown (Glushchenko, Yarkova and Kucherova, 2017).

Benefits: The contingencies strategy is required for making a mitigation strategy that

serves as a backup method in the event of a crisis. This strategy reduces fear and disorder

in the workplace. Sollatek can use this technology to manage damage in unexpected

scenarios.

Drawbacks: Management and preparation consumes a considerable amount of effort and

resources because it takes highly experienced personnel to create it, but if none of the

unexpected events arise, all of the preparations are useless.

Predicting tools- Prediction is a management technique that uses methodologies including

market analysis, competition analysis, and reviewing previous encounters to anticipate major

developments. The main goal of utilizing such technology is to provide the most realistic

upcoming predictions possible. Smaller companies like Sollatek use prediction software to

anticipate upcoming occurrences such as selling and market share.

Benefits: Prediction aids Sollatek in predicting the upcoming patterns and consumer

attitudes, allowing the company to meet all of the requirements of potential clients and

accomplishing the people management aim of consumer gratification.

Drawbacks: Predicting incorporates ideas like assessment and forecasts that do not

provide any reliable information and are associated with a significant level of uncertainty

(Horvat and Mojzer, 2019).

Situation instrument- With a situation utility, an organization's management, such as

Sollatek, engages a strategy group to design several possible futures. This is a long term

management procedure in which a company captures a wide variety of options. For a more

effective decision-making procedure, pattern analytics and scenario analysis are used.

Benefits: Since it incorporates numerous new options, a simulation instrument aids a

company in being equipped for any potential problems or difficulties. It decreases the

number of disappointments for the company.

Drawbacks: Situation preparation takes a very long research and demands a higher level

of expertise, thus organisations like Sollatek have to pay a considerable amount of

money. However after incorporating all of those materials, this strategic scheme fails to

deliver correct outcomes. Thus, it is not a very good option for the firm as it can add up

to the cost of the company and thus making it run in a least impactful manner in the long

term and as compared to the other competitors that are operating in the similar market

situation (Kramer, Maas and Van Rinsum, 2016).

Organizations are developing managerial accountancy systems in different approaches, as seen

through comparisons

In the framework of a company, managerial accountancy is a critical part. In the

framework of an enterprise, there seem to be a variety of fiscal obstacles and concerns that

influence decision-making and long term development (Nkundabayanga, Tauringana and

Muhwezi, 2018). Managerial accountancy is an essential topic in the corporate environment

since it assists to identify the essential monetary components and difficulties that remained

related with evaluating the difficulties that lie ahead and anticipating the significant constraints.

upcoming predictions possible. Smaller companies like Sollatek use prediction software to

anticipate upcoming occurrences such as selling and market share.

Benefits: Prediction aids Sollatek in predicting the upcoming patterns and consumer

attitudes, allowing the company to meet all of the requirements of potential clients and

accomplishing the people management aim of consumer gratification.

Drawbacks: Predicting incorporates ideas like assessment and forecasts that do not

provide any reliable information and are associated with a significant level of uncertainty

(Horvat and Mojzer, 2019).

Situation instrument- With a situation utility, an organization's management, such as

Sollatek, engages a strategy group to design several possible futures. This is a long term

management procedure in which a company captures a wide variety of options. For a more

effective decision-making procedure, pattern analytics and scenario analysis are used.

Benefits: Since it incorporates numerous new options, a simulation instrument aids a

company in being equipped for any potential problems or difficulties. It decreases the

number of disappointments for the company.

Drawbacks: Situation preparation takes a very long research and demands a higher level

of expertise, thus organisations like Sollatek have to pay a considerable amount of

money. However after incorporating all of those materials, this strategic scheme fails to

deliver correct outcomes. Thus, it is not a very good option for the firm as it can add up

to the cost of the company and thus making it run in a least impactful manner in the long

term and as compared to the other competitors that are operating in the similar market

situation (Kramer, Maas and Van Rinsum, 2016).

Organizations are developing managerial accountancy systems in different approaches, as seen

through comparisons

In the framework of a company, managerial accountancy is a critical part. In the

framework of an enterprise, there seem to be a variety of fiscal obstacles and concerns that

influence decision-making and long term development (Nkundabayanga, Tauringana and

Muhwezi, 2018). Managerial accountancy is an essential topic in the corporate environment

since it assists to identify the essential monetary components and difficulties that remained

related with evaluating the difficulties that lie ahead and anticipating the significant constraints.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executives and accountants establish a variety of methods and initiatives as a result of

conducting a managerial accountancy process within the company. Whereas fiscal administration

and accountancy is a subset of managerial accountancy that is primarily concerned with

improving the effectiveness and efficiency of company administration and maintenance. The

only way to get the company to its intended outcome and target is to make the best utilization of

monetary assets and administration. Sollatek is a small-scale company, and the monetary

capabilities required by small-scale organisations are restricted at times and are debated in

numerous ways. In order to achieve high performance activities and administration, several

norms and guidelines have also been established. It is among the most crucial aspects of

effectively managing and operating monetary capacity. A leader's main purpose is to create

important adjustments in order to boost brief or medium term performance. In context of revenue

related difficulties, an institution's value is altered. Most of these are revenue related

commodities, financial instability, and current obligations. Certain corporate finance difficulties

are listed beneath, and they are controlled by managerial practises and finance performance

through the use of a managerial accountancy framework.

Merchandise and operation challenges as those are the problems that continue to be

related with improving item reliability and expanding an organization's production

capability. Every organisation must follow the management and orientation established

by the law. It could really aid individuals in determining the firm's stability and

effectiveness. It is critical for organisations to make much optimal use of their monetary

backing in the manufacturing operation so that successful involvement and strategies can

be implemented (Shil, Hoque and Akter, 2019).

The following are various examples of monetary methodologies:

Benchmarking: Establishing a goal or standard motivates people to perform incredibly

well and execute effectively enough in order to meet a deadline. Worker and business

outcomes would improve as a result of something like this. This is mostly suitable for

examining objectives and supply chain management in a proactive way, while the

company is primarily concerned with overseeing monetary issues and recommended

procedures, as well as establishing the function objectives connected with the accounting

division of a company.

conducting a managerial accountancy process within the company. Whereas fiscal administration

and accountancy is a subset of managerial accountancy that is primarily concerned with

improving the effectiveness and efficiency of company administration and maintenance. The

only way to get the company to its intended outcome and target is to make the best utilization of

monetary assets and administration. Sollatek is a small-scale company, and the monetary

capabilities required by small-scale organisations are restricted at times and are debated in

numerous ways. In order to achieve high performance activities and administration, several

norms and guidelines have also been established. It is among the most crucial aspects of

effectively managing and operating monetary capacity. A leader's main purpose is to create

important adjustments in order to boost brief or medium term performance. In context of revenue

related difficulties, an institution's value is altered. Most of these are revenue related

commodities, financial instability, and current obligations. Certain corporate finance difficulties

are listed beneath, and they are controlled by managerial practises and finance performance

through the use of a managerial accountancy framework.

Merchandise and operation challenges as those are the problems that continue to be

related with improving item reliability and expanding an organization's production

capability. Every organisation must follow the management and orientation established

by the law. It could really aid individuals in determining the firm's stability and

effectiveness. It is critical for organisations to make much optimal use of their monetary

backing in the manufacturing operation so that successful involvement and strategies can

be implemented (Shil, Hoque and Akter, 2019).

The following are various examples of monetary methodologies:

Benchmarking: Establishing a goal or standard motivates people to perform incredibly

well and execute effectively enough in order to meet a deadline. Worker and business

outcomes would improve as a result of something like this. This is mostly suitable for

examining objectives and supply chain management in a proactive way, while the

company is primarily concerned with overseeing monetary issues and recommended

procedures, as well as establishing the function objectives connected with the accounting

division of a company.

Key Performance Metrics: A KPI is a type of metric that is used to analyse and define

the important aspects that go into controlling a fiscal productivity of the company and

gaining a competitive edge. Among the most important tools for resolving financial

challenges in a company is a quality administration indicator. It is the method of

evaluating a firm's productivity to the prior year's achievement of the same or a separate

organization. The purpose of using this is to study and evaluate the performance of a

team and also an organisation over the year. This is a monetary instrument that explains

the procedures for doing corporate activities in a simple manner from a monetary point of

view.

Overview of the two companies and the manner in which managerial accountancy is being

adapted by businesses:

Sabble plc Sollatek company

This is a small scale corporate group that

manages electrical gadgets. It operates at a

central stage.

It's a large-scale organisation that deals with a

variety of things. They require a practical

accounting system which could handle

company day-to-day expenses.

This company uses critical performance

indicators to evaluate its operations as well as

collective displays.

Financial management and benchmarking tools

are used to address company budgeting

concerns in this situation.

Assessment of a fiscal problem

Funding accessibility, fiscal accounting, process improvement, and other fiscal issues

confront companies like Sollatek. These issues could be addressed and reduced by employing

approaches such as benchmarking and KPI that assist a company in establishing a series of

guidelines based on pattern and competition assessments, and then contrasting established

benchmarks to real outcomes.

CONCLUSION

To conclude, management accounting provides detailed information about finance and

resource flow so the company could meet its future requirements and make statistical decision on

time with the help of actual data. By separating benefits of using this system and detects flaws

the company can take long term approaches to measure its business standards. More importantly,

the important aspects that go into controlling a fiscal productivity of the company and

gaining a competitive edge. Among the most important tools for resolving financial

challenges in a company is a quality administration indicator. It is the method of

evaluating a firm's productivity to the prior year's achievement of the same or a separate

organization. The purpose of using this is to study and evaluate the performance of a

team and also an organisation over the year. This is a monetary instrument that explains

the procedures for doing corporate activities in a simple manner from a monetary point of

view.

Overview of the two companies and the manner in which managerial accountancy is being

adapted by businesses:

Sabble plc Sollatek company

This is a small scale corporate group that

manages electrical gadgets. It operates at a

central stage.

It's a large-scale organisation that deals with a

variety of things. They require a practical

accounting system which could handle

company day-to-day expenses.

This company uses critical performance

indicators to evaluate its operations as well as

collective displays.

Financial management and benchmarking tools

are used to address company budgeting

concerns in this situation.

Assessment of a fiscal problem

Funding accessibility, fiscal accounting, process improvement, and other fiscal issues

confront companies like Sollatek. These issues could be addressed and reduced by employing

approaches such as benchmarking and KPI that assist a company in establishing a series of

guidelines based on pattern and competition assessments, and then contrasting established

benchmarks to real outcomes.

CONCLUSION

To conclude, management accounting provides detailed information about finance and

resource flow so the company could meet its future requirements and make statistical decision on

time with the help of actual data. By separating benefits of using this system and detects flaws

the company can take long term approaches to measure its business standards. More importantly,

the company must focus on presenting financial information in such a way that it should be

reliable and accurate. With the present report, it is concluded that the company must focus on

inventory and budget management to avoid any unnecessary expenses and avoid excess stock to

maintain its budget. At last, the report summarized that company needs to compare budget to

actual expenditure happens in the company. The aforementioned study assessment indicated that

managerial accountancy is an important aspect of a firm because actions and strategy determine

its effectiveness and development in a highly dynamic environment. These decisions are taken

with the assistance of useful data obtained via the use of different managerial accountancy and

monitoring technologies. There seem to be a number of techniques that must be considered in

attempt to keep track of the expenditure and increase the odds of achieving a successful outcome.

Valuation techniques like KPIs, benchmarking, and corporation management assist a company in

resolving finance concerns and difficulties that encourage investment.

reliable and accurate. With the present report, it is concluded that the company must focus on

inventory and budget management to avoid any unnecessary expenses and avoid excess stock to

maintain its budget. At last, the report summarized that company needs to compare budget to

actual expenditure happens in the company. The aforementioned study assessment indicated that

managerial accountancy is an important aspect of a firm because actions and strategy determine

its effectiveness and development in a highly dynamic environment. These decisions are taken

with the assistance of useful data obtained via the use of different managerial accountancy and

monitoring technologies. There seem to be a number of techniques that must be considered in

attempt to keep track of the expenditure and increase the odds of achieving a successful outcome.

Valuation techniques like KPIs, benchmarking, and corporation management assist a company in

resolving finance concerns and difficulties that encourage investment.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals

Al-Dmour, A., Zaidan, H. and Al Natour, A. R., 2021. The impact knowledge management

processes on business performance via the role of accounting information quality as a

mediating factor. VINE Journal of Information and Knowledge Management Systems.

Annen, T., 2017. Renewal of the criticism regarding the use of absorption costing in farm

planning. Berichte über Landwirtschaft. 95(2).

Asadullah, M. and et.al., 2018. Low-cost base drag reduction technique. Int. J. Mech. Eng.

Robot. Res. 7(4). pp.428-432.

DUE, P. C., 2021. STATE PERFORMANCE PLAN/ANNUAL PERFORMANCE REPORT:

PART C.

Dutta, R., Paitya, N. and Majumdar, A., 2020. Ambipolar reduction methodology for SOI tunnel

FETs in low power applications: a performance report. Int J Recent Technol Eng. 8(5).

Hamian, M. and et.al., 2018. A framework to expedite joint energy-reserve payment cost

minimization using a custom-designed method based on mixed integer genetic

algorithm. Engineering Applications of Artificial Intelligence, 72, pp.203-212.

Lee, T. A., 2020. Financial accounting theory. In The Routledge companion to accounting

history (pp. 159-184). Routledge.

Liu, C. and Sustik, M. A., 2021. Elasticity Based Demand Forecasting and Price Optimization

for Online Retail. arXiv preprint arXiv:2106.08274.

Loft, A., 2020. Understanding accounting in its social and historical context: the case of cost

accounting in Britain, 1914-1925. Routledge.

Maheshwari, S. N., Maheshwari, S. K. and Maheshwari, M. S. K., 2021. Principles of

Management Accounting. Sultan Chand & Sons.

Mahmoudian, F. and et.al., 2021. Inter-and intra-organizational stakeholder arrangements in

carbon management accounting. The British Accounting Review. 53(1). p.100933.

Massicotte, S. and Henri, J. F., 2021. The use of management accounting information by boards

of directors to oversee strategy implementation. The British Accounting Review. 53(3).

p.100953.

Mishra, U., Wu, J. Z. and Sarkar, B., 2021. Optimum sustainable inventory management with

backorder and deterioration under controllable carbon emissions. Journal of Cleaner

Production. 279. p.123699.

Moisello, A. M. and Mella, P., 2020. Matching Revenues and Costs: The Counter-Intuitive

Rationality of Direct Costing. International Journal of Business and Management. 15(1).

pp.202-222.

Muller, M., 2019. Essentials of inventory management. HarperCollins Leadership.

Books and Journals

Al-Dmour, A., Zaidan, H. and Al Natour, A. R., 2021. The impact knowledge management

processes on business performance via the role of accounting information quality as a

mediating factor. VINE Journal of Information and Knowledge Management Systems.

Annen, T., 2017. Renewal of the criticism regarding the use of absorption costing in farm

planning. Berichte über Landwirtschaft. 95(2).

Asadullah, M. and et.al., 2018. Low-cost base drag reduction technique. Int. J. Mech. Eng.

Robot. Res. 7(4). pp.428-432.

DUE, P. C., 2021. STATE PERFORMANCE PLAN/ANNUAL PERFORMANCE REPORT:

PART C.

Dutta, R., Paitya, N. and Majumdar, A., 2020. Ambipolar reduction methodology for SOI tunnel

FETs in low power applications: a performance report. Int J Recent Technol Eng. 8(5).

Hamian, M. and et.al., 2018. A framework to expedite joint energy-reserve payment cost

minimization using a custom-designed method based on mixed integer genetic

algorithm. Engineering Applications of Artificial Intelligence, 72, pp.203-212.

Lee, T. A., 2020. Financial accounting theory. In The Routledge companion to accounting

history (pp. 159-184). Routledge.

Liu, C. and Sustik, M. A., 2021. Elasticity Based Demand Forecasting and Price Optimization

for Online Retail. arXiv preprint arXiv:2106.08274.

Loft, A., 2020. Understanding accounting in its social and historical context: the case of cost

accounting in Britain, 1914-1925. Routledge.

Maheshwari, S. N., Maheshwari, S. K. and Maheshwari, M. S. K., 2021. Principles of

Management Accounting. Sultan Chand & Sons.

Mahmoudian, F. and et.al., 2021. Inter-and intra-organizational stakeholder arrangements in

carbon management accounting. The British Accounting Review. 53(1). p.100933.

Massicotte, S. and Henri, J. F., 2021. The use of management accounting information by boards

of directors to oversee strategy implementation. The British Accounting Review. 53(3).

p.100953.

Mishra, U., Wu, J. Z. and Sarkar, B., 2021. Optimum sustainable inventory management with

backorder and deterioration under controllable carbon emissions. Journal of Cleaner

Production. 279. p.123699.

Moisello, A. M. and Mella, P., 2020. Matching Revenues and Costs: The Counter-Intuitive

Rationality of Direct Costing. International Journal of Business and Management. 15(1).

pp.202-222.

Muller, M., 2019. Essentials of inventory management. HarperCollins Leadership.

NGUYEN, T. M. and NGUYEN, T. T., 2021. The Application of Strategic Management

Accounting: Evidence from the Consumer Goods Industry in Vietnam. The Journal of

Asian Finance, Economics and Business. 8(10). pp.139-146.

Ramachandran, N. and Kakani, R. K., 2020. Financial Accounting For Management|. McGraw-

Hill Education.

Wild, T., 2017. Best practice in inventory management. Routledge.

Zhao, X., 2020. An Analysis of College Education Cost Accounting under the New Government

Accounting System. Frontiers in Educational Research. 3(14).

Andarwati, M., Nirwanto, N. and Darsono, J. T., 2018. Analysis of factors affecting the

successof accounting information systems based on information technology on SME

managementsas accounting informationend user. EJEFAS Journal. (98). pp.97-102.

Bühler, A., Wallenburg, C. M. and Wieland, A., 2016. Accounting for external turbulence of

logistics organizations via performance measurement systems. Supply Chain

Management: An International Journal.

Glushchenko, A. V., Yarkova, I. V. and Kucherova, Y. P., 2017, December. The Role of the

Ecologically-Oriented Accounting Systems from the Perspective of Minimizing the

Strategic Risks in Terms of Ecologizing the Production. In Perspectives on the use of

New Information and Communication Technology (ICT) in the Modern Economy (pp.

741-747). Springer, Cham.

Horvat, T. and Mojzer, J., 2019. Influence of Company Size on Accounting Information for

Decision-Making of Management. Naše gospodarstvo/Our economy. 65(2). pp.11-20.

Kramer, S., Maas, V. S. and Van Rinsum, M., 2016. Relative performance information, rank

ordering and employee performance: A research note. Management Accounting

Research. 33. pp.16-24.

Nkundabayanga, S., Tauringana, V. and Muhwezi, M., 2018. Management accounting practices,

governing boards and competitive advantage of Ugandan secondary schools. The

International Journal of Management Education. 32(6). pp.958-974.

Shil, N. C., Hoque, M. and Akter, M., 2019. Revisiting Management Accounting Practice Gap:

A Proposed PERAPPGAP Model. Journal of Accounting and Finance. 19(1). pp.135-

155.

Sledgianowski, D., Gomaa, M. and Tan, C., 2017. Toward integration of Big Data, technology

and information systems competencies into the accounting curriculum. Journal of

Accounting Education. 38. pp.81-93.

Online

An overview of management accounting. 2021. [Online]. Available through:

<https://www.accounting.com/careers/management-accounting/>

Inventory management systems. 2021. [Online]. Available through:

<https://www.unleashedsoftware.com/inventory-management-guide/inventory-

management-systems>

Accounting: Evidence from the Consumer Goods Industry in Vietnam. The Journal of

Asian Finance, Economics and Business. 8(10). pp.139-146.

Ramachandran, N. and Kakani, R. K., 2020. Financial Accounting For Management|. McGraw-

Hill Education.

Wild, T., 2017. Best practice in inventory management. Routledge.

Zhao, X., 2020. An Analysis of College Education Cost Accounting under the New Government

Accounting System. Frontiers in Educational Research. 3(14).

Andarwati, M., Nirwanto, N. and Darsono, J. T., 2018. Analysis of factors affecting the

successof accounting information systems based on information technology on SME

managementsas accounting informationend user. EJEFAS Journal. (98). pp.97-102.

Bühler, A., Wallenburg, C. M. and Wieland, A., 2016. Accounting for external turbulence of

logistics organizations via performance measurement systems. Supply Chain

Management: An International Journal.

Glushchenko, A. V., Yarkova, I. V. and Kucherova, Y. P., 2017, December. The Role of the

Ecologically-Oriented Accounting Systems from the Perspective of Minimizing the

Strategic Risks in Terms of Ecologizing the Production. In Perspectives on the use of

New Information and Communication Technology (ICT) in the Modern Economy (pp.

741-747). Springer, Cham.

Horvat, T. and Mojzer, J., 2019. Influence of Company Size on Accounting Information for

Decision-Making of Management. Naše gospodarstvo/Our economy. 65(2). pp.11-20.

Kramer, S., Maas, V. S. and Van Rinsum, M., 2016. Relative performance information, rank

ordering and employee performance: A research note. Management Accounting

Research. 33. pp.16-24.

Nkundabayanga, S., Tauringana, V. and Muhwezi, M., 2018. Management accounting practices,

governing boards and competitive advantage of Ugandan secondary schools. The

International Journal of Management Education. 32(6). pp.958-974.

Shil, N. C., Hoque, M. and Akter, M., 2019. Revisiting Management Accounting Practice Gap:

A Proposed PERAPPGAP Model. Journal of Accounting and Finance. 19(1). pp.135-

155.

Sledgianowski, D., Gomaa, M. and Tan, C., 2017. Toward integration of Big Data, technology

and information systems competencies into the accounting curriculum. Journal of

Accounting Education. 38. pp.81-93.

Online

An overview of management accounting. 2021. [Online]. Available through:

<https://www.accounting.com/careers/management-accounting/>

Inventory management systems. 2021. [Online]. Available through:

<https://www.unleashedsoftware.com/inventory-management-guide/inventory-

management-systems>

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.