Managing Business Performance: Analyzing Products and Costs

VerifiedAdded on 2023/04/11

|15

|3748

|102

Report

AI Summary

This report provides a comprehensive analysis of business performance within a university environment, focusing on the products offered, the associated direct and indirect costs, and the application of the Activity-Based Costing (ABC) approach. The report begins by analyzing the various educational courses and programs offered by a UK university, identifying cost pools and cost drivers relevant to these offerings. It then discusses the direct and indirect costs involved in delivering these products to students, providing examples and a comparative table. Furthermore, the report examines the usefulness, potential problems, and limitations of implementing the ABC approach within the university setting, considering aspects such as production costs for services. The analysis aims to provide insights into how universities can effectively manage their business performance by understanding and controlling costs and optimizing resource allocation.

STUDENT ID:

MODULE CODE:

ASSIGNMENT NAME: MANAGING BUSINESS

PERFORMANCE

1

MODULE CODE:

ASSIGNMENT NAME: MANAGING BUSINESS

PERFORMANCE

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction.................................................................................................................................................3

Task A.........................................................................................................................................................5

Analyzing the products offered by the university........................................................................................5

Task B.........................................................................................................................................................8

Discussing the direct and indirect costs of providing the products to the customer.....................................8

Task C.......................................................................................................................................................10

Analysis on the usefulness, potential problems, and limitations of the ABC approach within the university

environment...............................................................................................................................................10

(a) Production costs for services................................................................................................................11

Conclusion.................................................................................................................................................13

Reference List............................................................................................................................................14

2

Introduction.................................................................................................................................................3

Task A.........................................................................................................................................................5

Analyzing the products offered by the university........................................................................................5

Task B.........................................................................................................................................................8

Discussing the direct and indirect costs of providing the products to the customer.....................................8

Task C.......................................................................................................................................................10

Analysis on the usefulness, potential problems, and limitations of the ABC approach within the university

environment...............................................................................................................................................10

(a) Production costs for services................................................................................................................11

Conclusion.................................................................................................................................................13

Reference List............................................................................................................................................14

2

Introduction

Business performance refers to how the plans and approach by the business entities in the

struggle to achieve predefined business goals are applied on the market stage. Performance of the

business organization is of immense importance, which necessitates the speed of the business

approach for attaining the desired position (Hoerl and Snee, 2012, p.267). Businesses should

render performance of optimum level which requires critical monitoring and analysis. Business

performance management is a tool which encompasses the aspects of reviewing business

performance and determining better methods quick achievement of pre-requisite goals. It enables

the businesses to collect, analyze, recheck overhead business costs, resource allocation and

consumption, empirical data and make necessary recommendations. Through this, managers are

aware of the performance issues and company’s positions and thus can instantiate appropriate

decisions.

Management of business performance entails various frameworks. One of those

frameworks is Activity-Based Costing (ABC). As the name suggests, ABC is a framework which

measures the frequently adopted business, with diversity in design and use, providing insights

into what is providing value for to the customers. Activity-Based model was developed to

ascertain the overhead costs and their allocation to individual consumers and products. It

facilitates the allocation costs by organizations making adjustments to overhead costs that do not

model with the business propositions. ABC, being a strategic management tool, establishes direct

links between the performed activities and output generated (Hicks, 2012, p.257). The work flow

in ABC is a chain process, from the activities to products, services con consumers.

A costing system is typically designed for the purpose of monitoring the costs incurred by

the business entity. The system is comprised of different processes, controls and reports that are

designed to aggregate and report to management about revenues, costs and profitability. The

reports of a costing system are intended for internal use; hence it is not subjected to any

accounting framework.

The traditional method of cost accounting refers to the allocation of manufacturing

overhead costs to the manufactured products (Hopper and Major, 2007, p.84). The traditional

method is also known as the conventional method that assigns and allocated factory’s indirect

3

Business performance refers to how the plans and approach by the business entities in the

struggle to achieve predefined business goals are applied on the market stage. Performance of the

business organization is of immense importance, which necessitates the speed of the business

approach for attaining the desired position (Hoerl and Snee, 2012, p.267). Businesses should

render performance of optimum level which requires critical monitoring and analysis. Business

performance management is a tool which encompasses the aspects of reviewing business

performance and determining better methods quick achievement of pre-requisite goals. It enables

the businesses to collect, analyze, recheck overhead business costs, resource allocation and

consumption, empirical data and make necessary recommendations. Through this, managers are

aware of the performance issues and company’s positions and thus can instantiate appropriate

decisions.

Management of business performance entails various frameworks. One of those

frameworks is Activity-Based Costing (ABC). As the name suggests, ABC is a framework which

measures the frequently adopted business, with diversity in design and use, providing insights

into what is providing value for to the customers. Activity-Based model was developed to

ascertain the overhead costs and their allocation to individual consumers and products. It

facilitates the allocation costs by organizations making adjustments to overhead costs that do not

model with the business propositions. ABC, being a strategic management tool, establishes direct

links between the performed activities and output generated (Hicks, 2012, p.257). The work flow

in ABC is a chain process, from the activities to products, services con consumers.

A costing system is typically designed for the purpose of monitoring the costs incurred by

the business entity. The system is comprised of different processes, controls and reports that are

designed to aggregate and report to management about revenues, costs and profitability. The

reports of a costing system are intended for internal use; hence it is not subjected to any

accounting framework.

The traditional method of cost accounting refers to the allocation of manufacturing

overhead costs to the manufactured products (Hopper and Major, 2007, p.84). The traditional

method is also known as the conventional method that assigns and allocated factory’s indirect

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

costs to the items manufactured on the basis of volume, number of units manufactured and

additional costs of business.

Activity Based Costing is a methodology which aids in allocating overhead to those items

that are useful. The system is typically utilized for the targeted reduction of overhead costs.

There is a particular way of managing ABC process flow and that is being mentioned as under:

Identify costs

Load secondary cost pools

Load primary cost pools

Measure activity drivers

Allocate costs in secondary pools to primary pools

Charge cost to cost objects

Formulate reports

Act on the information

Hence, these are the steps that are involved in Activity Based Costing and that works for

the purpose of specifying the resource requirements of the business entity.

4

additional costs of business.

Activity Based Costing is a methodology which aids in allocating overhead to those items

that are useful. The system is typically utilized for the targeted reduction of overhead costs.

There is a particular way of managing ABC process flow and that is being mentioned as under:

Identify costs

Load secondary cost pools

Load primary cost pools

Measure activity drivers

Allocate costs in secondary pools to primary pools

Charge cost to cost objects

Formulate reports

Act on the information

Hence, these are the steps that are involved in Activity Based Costing and that works for

the purpose of specifying the resource requirements of the business entity.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task A

Analyzing the products offered by the university

UK lists among the top education destinations in the world. Students from various

corners of the world come in study in its university. It is home to some of the oldest and

renowned universities in the world and provides quality curricula of courses (Rausch et al. 20-

13, p.89). It has to accommodate large number of international students. They are engaged in

business with the students, they are considered as a business organization and the students are

their customers. Thus it becomes important for UK universities to maintain their brand and

quality for growth of their business.

The major products which are offered by the university are different types of educational

courses, training curriculum, post-graduation, diploma and professional degree courses. As per

the area of interest, students get involved in the same curriculum.

At undergraduate level, these courses are provided by UK University:

Undergraduate or bachelor’s degree such as Bachelor of Engineering (BEng), Bachelor of

Science (BSc), Bachelor of Arts (BA), etc.

Foundation degree which is equal to two years of honours degree, and can be studied full-

time or part-time

Diploma of higher education, full-time two years of DipHE is equivalent of two years of

degree and can entail in the third year of the degree course

Higher national diploma (HND), a two-year course when completed with high grades

equals three years of education.

At Post graduation level, these courses are available at UK University:

Master’ degree in the courses offered in the undergraduate level. It leads to masters in

engineering (MEng), master of science (MA), master of architecture (MArch), master in

philosophy (MPhil), master of fine arts (MFA), etc.

MBA courses or Master of Business Administration which is one of the top draws in UK

offered in universities. MBA candidates from UK universities are highly respected and

enjoy domination.

5

Analyzing the products offered by the university

UK lists among the top education destinations in the world. Students from various

corners of the world come in study in its university. It is home to some of the oldest and

renowned universities in the world and provides quality curricula of courses (Rausch et al. 20-

13, p.89). It has to accommodate large number of international students. They are engaged in

business with the students, they are considered as a business organization and the students are

their customers. Thus it becomes important for UK universities to maintain their brand and

quality for growth of their business.

The major products which are offered by the university are different types of educational

courses, training curriculum, post-graduation, diploma and professional degree courses. As per

the area of interest, students get involved in the same curriculum.

At undergraduate level, these courses are provided by UK University:

Undergraduate or bachelor’s degree such as Bachelor of Engineering (BEng), Bachelor of

Science (BSc), Bachelor of Arts (BA), etc.

Foundation degree which is equal to two years of honours degree, and can be studied full-

time or part-time

Diploma of higher education, full-time two years of DipHE is equivalent of two years of

degree and can entail in the third year of the degree course

Higher national diploma (HND), a two-year course when completed with high grades

equals three years of education.

At Post graduation level, these courses are available at UK University:

Master’ degree in the courses offered in the undergraduate level. It leads to masters in

engineering (MEng), master of science (MA), master of architecture (MArch), master in

philosophy (MPhil), master of fine arts (MFA), etc.

MBA courses or Master of Business Administration which is one of the top draws in UK

offered in universities. MBA candidates from UK universities are highly respected and

enjoy domination.

5

PhDs/Doctorates in various undergraduate courses related to science, arts, philosophy,

sports studies, etc. it is offered to students in UK who have at least managed a result of

2:1 at undergraduate.

Professional and vocational qualifications which is taken to improve skills and attributes

regarding a specific job.

Thus, it can be said that UK University is engaged in many activities and courses and

prior supplying the products to the users (students), it is essential for the university to make plan

each and every aspect. In order to supply appropriate services to the students, professors must

have to look upon the availability of services so that they can manage their schedule. The

University is also required to manage cost aspect so that organizational resources can be

prominently utilized. It has also been observed that UK University is concerned about the

standard of studies; hence for such prospects, specific qualifications are being determined while

taking the students.

Cost pools and cost drivers

Cost pools

Activity cost pool is the accumulated or total cost incurred for specific or similar

activities. It is a way of recording the cumulative costs for similar activities. Though cost pools

are similar to factory accounts, it consist both fixed and variable costs, where fixed cost include

equipment purchases and variable costs denotes the material purchases (Khataie and Bulgak,

2013, p.762). Once the costs of similar activities have been sorted and totaled together, an

overhead rate can be computed for activities and assigned to objects based on their activity

drivers.

Cost Drivers

Activity cost drivers is a factor that influences the level of expenses of the specific

business activities. In ABC, activity cost driver is drives the labor cost, maintenance and

purchase of goods (McLaughlin et al. 2014, p.E3). Cost drivers in essentially a branch of

managerial accounting in methods of ABC that helps managers relate the activities to the

variable costs at different activity levels.

Example of cost pools and drivers in the university

Cost pool is an accounting term that refers to groups of accounts that serves to express

the cost of goods and services which is allotted in a business and manufacturing organization. As

6

sports studies, etc. it is offered to students in UK who have at least managed a result of

2:1 at undergraduate.

Professional and vocational qualifications which is taken to improve skills and attributes

regarding a specific job.

Thus, it can be said that UK University is engaged in many activities and courses and

prior supplying the products to the users (students), it is essential for the university to make plan

each and every aspect. In order to supply appropriate services to the students, professors must

have to look upon the availability of services so that they can manage their schedule. The

University is also required to manage cost aspect so that organizational resources can be

prominently utilized. It has also been observed that UK University is concerned about the

standard of studies; hence for such prospects, specific qualifications are being determined while

taking the students.

Cost pools and cost drivers

Cost pools

Activity cost pool is the accumulated or total cost incurred for specific or similar

activities. It is a way of recording the cumulative costs for similar activities. Though cost pools

are similar to factory accounts, it consist both fixed and variable costs, where fixed cost include

equipment purchases and variable costs denotes the material purchases (Khataie and Bulgak,

2013, p.762). Once the costs of similar activities have been sorted and totaled together, an

overhead rate can be computed for activities and assigned to objects based on their activity

drivers.

Cost Drivers

Activity cost drivers is a factor that influences the level of expenses of the specific

business activities. In ABC, activity cost driver is drives the labor cost, maintenance and

purchase of goods (McLaughlin et al. 2014, p.E3). Cost drivers in essentially a branch of

managerial accounting in methods of ABC that helps managers relate the activities to the

variable costs at different activity levels.

Example of cost pools and drivers in the university

Cost pool is an accounting term that refers to groups of accounts that serves to express

the cost of goods and services which is allotted in a business and manufacturing organization. As

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

per the method of ABC costing, it is essential for the university to segregate the expenditure

accordingly and on that basis, different changes could be made to the overall spending. Since,

there are various expenditure which UK University needs to incur; therefore it is essential to

categorize such expenses in indirect and direct aspects. In ABC costing, cost pools and cost

drivers includes several elements so the basis of which resources are allocated to organizational

activities. Thus, it can be said that with the help of Activity Based Costing, adequate amount of

resources can be allocated to the organizational processes. This is also useful for the purpose of

minimizing the possibilities of constraints.

7

accordingly and on that basis, different changes could be made to the overall spending. Since,

there are various expenditure which UK University needs to incur; therefore it is essential to

categorize such expenses in indirect and direct aspects. In ABC costing, cost pools and cost

drivers includes several elements so the basis of which resources are allocated to organizational

activities. Thus, it can be said that with the help of Activity Based Costing, adequate amount of

resources can be allocated to the organizational processes. This is also useful for the purpose of

minimizing the possibilities of constraints.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task B

Discussing the direct and indirect costs of providing the products to the

customer

While determining the cost of products, it is necessary to keep account of the production

cost and that the production cost does not excels that of the product (Kaplan and Anderson, 2013,

p.28). Sometimes the production and services cost can go beyond the resources and materials

cost, barring the cost of the employee salary, the working space, marketing advertisements and

employee perks. These make up the direct and indirect costs when taken together.

Both direct and indirect cost enhances the expenditure of UK University. Direct costs are

associated with the production of products and services. Organizations can instantly recognize

the direct costs as the expenses on a specific object, which can be any item, product, services,

including raw materials, labor cost. These make up the costs incurred in procurement of

materials and equipments from planning stage to completion of product (Jean et al. 2014, p.109).

For example, the products here are the various courses offered by universities. Direct costs for

universities are planning and organizing the curriculum for the offered courses, inducting

professors and lecturers specialized in respective fields, making arrangements of lab facilities,

procuring equipments and materials for sports, science lab, etc.

Indirect Costs on the other hand go beyond the costs associated with the production and

delivery of products. It includes maintenance and servicing costs post completion of products. It

is often the overhead costs left over after computation of direct costs and generally accounts for

the real costs of doing business (Kumar and Mahto, 2013, p.173). These are generally allocated

to specific production runs for a time periods. The indirect includes:

1. Materials purchase orders cost, products are not ordered for single unit but for entire batches

2. Product packaging costs, multiple products packaged in single unit

3. Machine set up costs, machine set up not for single unit for entire product model

4. Maintenance and cleaning costs, maintaining the end products and keeping it clean.

For instance- indirect cost includes – insurance expenses, salaries to the employees,

expenses on computer system and other techniques and depreciation on machines. While

providing value to the expenses, it is crucial to segregate the practices on the basis of direct and

indirect cost factors. For example- if rent for electricity is required to be paid, then UK

8

Discussing the direct and indirect costs of providing the products to the

customer

While determining the cost of products, it is necessary to keep account of the production

cost and that the production cost does not excels that of the product (Kaplan and Anderson, 2013,

p.28). Sometimes the production and services cost can go beyond the resources and materials

cost, barring the cost of the employee salary, the working space, marketing advertisements and

employee perks. These make up the direct and indirect costs when taken together.

Both direct and indirect cost enhances the expenditure of UK University. Direct costs are

associated with the production of products and services. Organizations can instantly recognize

the direct costs as the expenses on a specific object, which can be any item, product, services,

including raw materials, labor cost. These make up the costs incurred in procurement of

materials and equipments from planning stage to completion of product (Jean et al. 2014, p.109).

For example, the products here are the various courses offered by universities. Direct costs for

universities are planning and organizing the curriculum for the offered courses, inducting

professors and lecturers specialized in respective fields, making arrangements of lab facilities,

procuring equipments and materials for sports, science lab, etc.

Indirect Costs on the other hand go beyond the costs associated with the production and

delivery of products. It includes maintenance and servicing costs post completion of products. It

is often the overhead costs left over after computation of direct costs and generally accounts for

the real costs of doing business (Kumar and Mahto, 2013, p.173). These are generally allocated

to specific production runs for a time periods. The indirect includes:

1. Materials purchase orders cost, products are not ordered for single unit but for entire batches

2. Product packaging costs, multiple products packaged in single unit

3. Machine set up costs, machine set up not for single unit for entire product model

4. Maintenance and cleaning costs, maintaining the end products and keeping it clean.

For instance- indirect cost includes – insurance expenses, salaries to the employees,

expenses on computer system and other techniques and depreciation on machines. While

providing value to the expenses, it is crucial to segregate the practices on the basis of direct and

indirect cost factors. For example- if rent for electricity is required to be paid, then UK

8

University must have to ensure that rent is paid for only those areas which is being utilized by

the university. At the same time, while calculating the price of machine, it is crucial for UK

University to deduct the amount of depreciation so that actual value of the product can be

ascertained. Further example is – in case of payment of rent, UK University has to pay rent for

only those area which is used by the university members. However, the university is not liable to

pay rent for the entire building.

Operational cost includes all the expenses which are being incurred on administration,

supervision and on other areas (Stouthuysen et al. 2010, p.87). Cost benefit relationship is

required to be developed between cost pool and allocation base so that all the activities can be

managed effectively. Another example can be taken for library expenses wherein expenses

should be allocated according to utility frequency. While calculating value for the expenses, UK

University must have to segregate both direct and indirect cost.

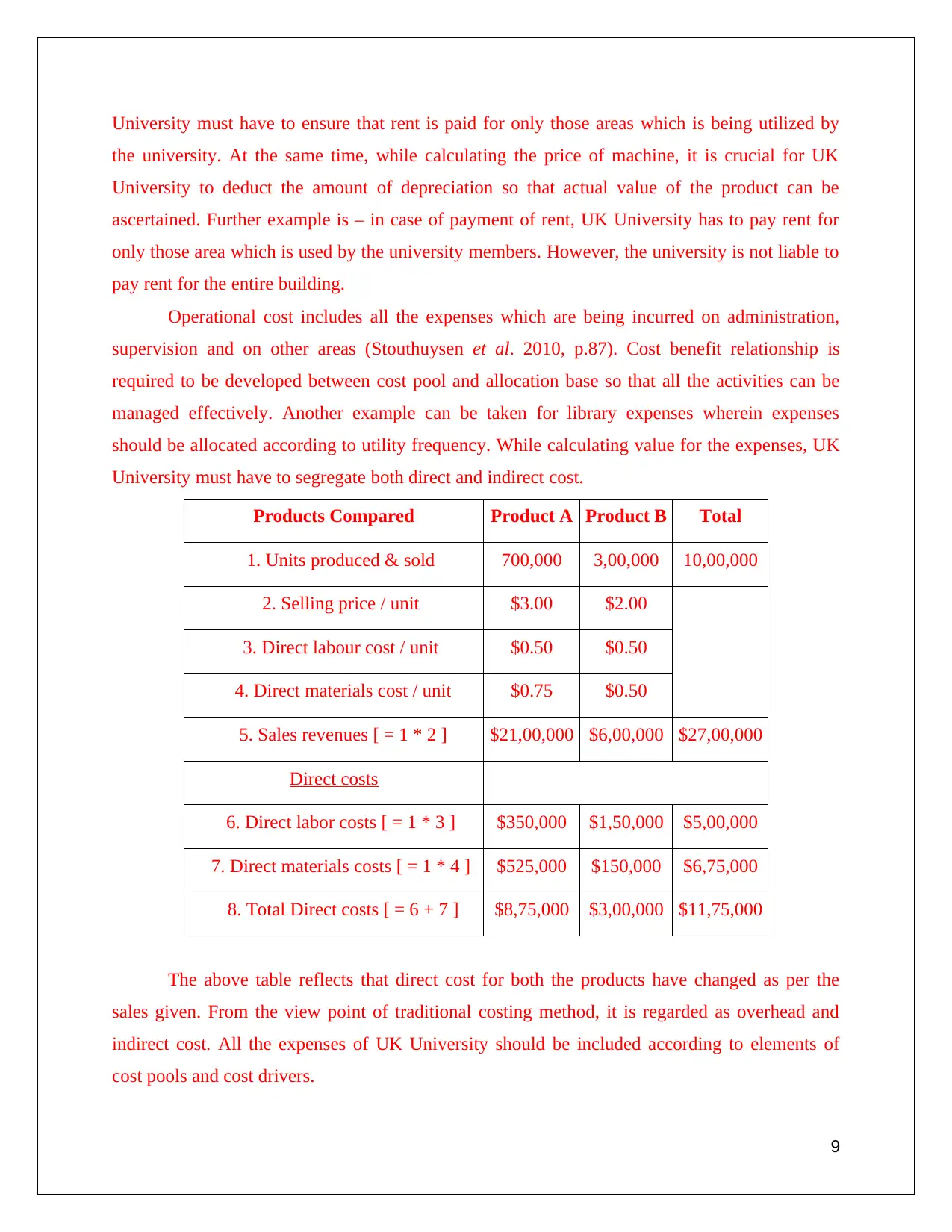

Products Compared Product A Product B Total

1. Units produced & sold 700,000 3,00,000 10,00,000

2. Selling price / unit $3.00 $2.00

3. Direct labour cost / unit $0.50 $0.50

4. Direct materials cost / unit $0.75 $0.50

5. Sales revenues [ = 1 * 2 ] $21,00,000 $6,00,000 $27,00,000

Direct costs

6. Direct labor costs [ = 1 * 3 ] $350,000 $1,50,000 $5,00,000

7. Direct materials costs [ = 1 * 4 ] $525,000 $150,000 $6,75,000

8. Total Direct costs [ = 6 + 7 ] $8,75,000 $3,00,000 $11,75,000

The above table reflects that direct cost for both the products have changed as per the

sales given. From the view point of traditional costing method, it is regarded as overhead and

indirect cost. All the expenses of UK University should be included according to elements of

cost pools and cost drivers.

9

the university. At the same time, while calculating the price of machine, it is crucial for UK

University to deduct the amount of depreciation so that actual value of the product can be

ascertained. Further example is – in case of payment of rent, UK University has to pay rent for

only those area which is used by the university members. However, the university is not liable to

pay rent for the entire building.

Operational cost includes all the expenses which are being incurred on administration,

supervision and on other areas (Stouthuysen et al. 2010, p.87). Cost benefit relationship is

required to be developed between cost pool and allocation base so that all the activities can be

managed effectively. Another example can be taken for library expenses wherein expenses

should be allocated according to utility frequency. While calculating value for the expenses, UK

University must have to segregate both direct and indirect cost.

Products Compared Product A Product B Total

1. Units produced & sold 700,000 3,00,000 10,00,000

2. Selling price / unit $3.00 $2.00

3. Direct labour cost / unit $0.50 $0.50

4. Direct materials cost / unit $0.75 $0.50

5. Sales revenues [ = 1 * 2 ] $21,00,000 $6,00,000 $27,00,000

Direct costs

6. Direct labor costs [ = 1 * 3 ] $350,000 $1,50,000 $5,00,000

7. Direct materials costs [ = 1 * 4 ] $525,000 $150,000 $6,75,000

8. Total Direct costs [ = 6 + 7 ] $8,75,000 $3,00,000 $11,75,000

The above table reflects that direct cost for both the products have changed as per the

sales given. From the view point of traditional costing method, it is regarded as overhead and

indirect cost. All the expenses of UK University should be included according to elements of

cost pools and cost drivers.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task C

Analysis on the usefulness, potential problems, and limitations of the ABC

approach within the university environment

Generally activity based costing (ABC) assigns manufacturing overhead costs to products

in a more logical manner than the traditional approach of simply allocating costs on the basis of

machine honours. Activity based costing first assigns costs to the activities that are the real cause

of the over head. It then assigns the cost of those activities only to the products that are actually

demanding the activities (Kaplan and Anderson, 2013, p.156).

The usefulness of the ABC approach lies in its objectivity. With ABC, a company can

soundly estimate the cost elements of the entire products, activities and services her in this case

the products and services offered by the university which helps in making decision for the

university. This lies in Identification and elimination of those products and services of the

university here that are unprofitable and lower the prices of those services are that are overpriced

and increase their affordability and demand. The process also helps in identification and

elimination of services and processes that are ineffective in allocation processes and concepts

that lead to very same product and services (Kaplan and Atkinson, 2015, p.109).

Further, ABC approach is also useful in terms of identifying the internal efficiency and

profitability per service line so that difficult services can be identified and results in overcoming

their efficiency so that best results can be attained. However, it is also crucial for UK University

to undertake such approach as it is significant for them to improve their internal efficiency and

thus enhance profitability aspect so that desired courses can be offered to students and enhance

their satisfaction. In contrast to UK University the internal efficiency and profitability of

organization has been affect by ABC approach in a positive manner. It means that through

implementing such approach it would benefit UK University to assess the costing of services as

well as minimizing the cost of different courses offered by University in relation to attain best

results (Drury, 2013, p.136). In evaluating the efficiency of the educational institution this could

be found that the outcomes of educational programs are long-term and the social and political

pressures can affect the institutions increasing the cost of their services provided and ABC can

play a role in internally resolving the issue.

10

Analysis on the usefulness, potential problems, and limitations of the ABC

approach within the university environment

Generally activity based costing (ABC) assigns manufacturing overhead costs to products

in a more logical manner than the traditional approach of simply allocating costs on the basis of

machine honours. Activity based costing first assigns costs to the activities that are the real cause

of the over head. It then assigns the cost of those activities only to the products that are actually

demanding the activities (Kaplan and Anderson, 2013, p.156).

The usefulness of the ABC approach lies in its objectivity. With ABC, a company can

soundly estimate the cost elements of the entire products, activities and services her in this case

the products and services offered by the university which helps in making decision for the

university. This lies in Identification and elimination of those products and services of the

university here that are unprofitable and lower the prices of those services are that are overpriced

and increase their affordability and demand. The process also helps in identification and

elimination of services and processes that are ineffective in allocation processes and concepts

that lead to very same product and services (Kaplan and Atkinson, 2015, p.109).

Further, ABC approach is also useful in terms of identifying the internal efficiency and

profitability per service line so that difficult services can be identified and results in overcoming

their efficiency so that best results can be attained. However, it is also crucial for UK University

to undertake such approach as it is significant for them to improve their internal efficiency and

thus enhance profitability aspect so that desired courses can be offered to students and enhance

their satisfaction. In contrast to UK University the internal efficiency and profitability of

organization has been affect by ABC approach in a positive manner. It means that through

implementing such approach it would benefit UK University to assess the costing of services as

well as minimizing the cost of different courses offered by University in relation to attain best

results (Drury, 2013, p.136). In evaluating the efficiency of the educational institution this could

be found that the outcomes of educational programs are long-term and the social and political

pressures can affect the institutions increasing the cost of their services provided and ABC can

play a role in internally resolving the issue.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

However, there are several issues as well as faced by the ABC approach in terms of

implementing the IT support system and thus enhance the cost of services provided by UK

University. Therefore, it is essential for UK University undertake effective ABC Costing method

so that it aids in enhancing the efficiency and profitability of firm in market. However, it would

result in providing best results so that appropriate courses can be offered to students (Mahal and

Hossain, 2015, p.64). Thus, it would benefit University to enhance their efficiency and thus

profitability could be raised. However, it can be articulated that ABC approach assesses the

issues in relation to identify the costing technique so that cost could be minimized and

profitability can be enhanced.

(a) Production costs for services

Strengths and Advantages of ABC costing

Activity Based costing is useful in determining product cost; hence it is termed as more

accurate and reliable because it typically emphasizes on cause and effect linkage of costs

and activities with regards to production of goods. It also aids in recognizing that it is the

activities which causes costs, not products as that consumes activities.

On the other hand, fixation of selling price for multiple products under ABC is

appropriate and correct since overheads are allocated on the basis of relevant cost

derivers.

Control of overheads comprises of fixed and variable expenses which sometimes can be

controlled and monitored. Thus, it can be said that connection between cost and activities

are clearly defined in ABC which also provides opportunities to control overhead costs

(Mahal and Hossain, 2015, p.64).

ABC is useful for UK University because it uses multiple cost drivers in which many are

transaction based. It is also concerned with the activities beyond which overheads of the

products can be recorded.

It is also useful because it traces costs to areas of managerial responsibility, processes,

customers and departments.

Further, it can assist UK University to improve the decision making capability through

using reliable product cost data (Anderson and Young, 1999, p.556).

Disadvantages of ABC process

11

implementing the IT support system and thus enhance the cost of services provided by UK

University. Therefore, it is essential for UK University undertake effective ABC Costing method

so that it aids in enhancing the efficiency and profitability of firm in market. However, it would

result in providing best results so that appropriate courses can be offered to students (Mahal and

Hossain, 2015, p.64). Thus, it would benefit University to enhance their efficiency and thus

profitability could be raised. However, it can be articulated that ABC approach assesses the

issues in relation to identify the costing technique so that cost could be minimized and

profitability can be enhanced.

(a) Production costs for services

Strengths and Advantages of ABC costing

Activity Based costing is useful in determining product cost; hence it is termed as more

accurate and reliable because it typically emphasizes on cause and effect linkage of costs

and activities with regards to production of goods. It also aids in recognizing that it is the

activities which causes costs, not products as that consumes activities.

On the other hand, fixation of selling price for multiple products under ABC is

appropriate and correct since overheads are allocated on the basis of relevant cost

derivers.

Control of overheads comprises of fixed and variable expenses which sometimes can be

controlled and monitored. Thus, it can be said that connection between cost and activities

are clearly defined in ABC which also provides opportunities to control overhead costs

(Mahal and Hossain, 2015, p.64).

ABC is useful for UK University because it uses multiple cost drivers in which many are

transaction based. It is also concerned with the activities beyond which overheads of the

products can be recorded.

It is also useful because it traces costs to areas of managerial responsibility, processes,

customers and departments.

Further, it can assist UK University to improve the decision making capability through

using reliable product cost data (Anderson and Young, 1999, p.556).

Disadvantages of ABC process

11

In ABC costing, reduction is not always possible if the overhead costs are higher because

of the reasons such as volume, limited benefits and repetition from activity based costing.

It does not look efficient when overhead cost of UK University depicts small portion of

the costs. ABC methods of costing may not be appropriate if the overhead waste is

perceived to be relatively low (Mitchell, 1996, p.54).

Hence, in this procedure, UK University is required to consider the costs associated in

different activities.

There is a long time period that is involved in using an activity based on costing method;

therefore all the business practices of UK University must be properly associated with

costs methods. ABC requires many different departments to collect and input data.

The production cost of services for a university lie in recruiting and hiring teachers for

the specified task, Resourcing study materials for students and teachers for different courses

which involves a cost, technological facilitation for both students and teachers, logistic

requirement needed to continue with the courses and provision of lodging and food for

residential students and teachers, provision of residential boarding is an essential service for nay

university. Basing on all these the production cost of services depends (Min and Yan, 2013,

p.71). ABC or the activity based cost technique play an important role in determining analysing

and implementing service costs for universities here in this case the University of Nottingham.

The process further helps in identification of activities and services which are not

profitable and can help in reducing cost of the service without affecting the educational slandered

and prestige of the institution. In the present world self funding and profit for organisations even

educational institutions like Nottingham University is essential. In the era of Globalisation

focusing only on internal students or students within the country is not an option. But in looking

for students abroad there are various concerns that needs to be taken into consideration and

ABC(Activity Based Costing) plays an important role in this regard (Cropper and Cook, 2000,

p.66). The first concern in this regard is the affordability of courses among the student

community, if the organisation is not able to formulate a policy keeping the desired rate for the

services among students across the world, the institution in the end will not be able to admit any

student for their academic sessions, and if students are not admitted the institution needs to suffer

a huge loss as the fixed cost are to be paid by the university like the salary and remunerations of

the employees and in maintaining the university infrastructure (Malmi, 1999, p.663)

12

of the reasons such as volume, limited benefits and repetition from activity based costing.

It does not look efficient when overhead cost of UK University depicts small portion of

the costs. ABC methods of costing may not be appropriate if the overhead waste is

perceived to be relatively low (Mitchell, 1996, p.54).

Hence, in this procedure, UK University is required to consider the costs associated in

different activities.

There is a long time period that is involved in using an activity based on costing method;

therefore all the business practices of UK University must be properly associated with

costs methods. ABC requires many different departments to collect and input data.

The production cost of services for a university lie in recruiting and hiring teachers for

the specified task, Resourcing study materials for students and teachers for different courses

which involves a cost, technological facilitation for both students and teachers, logistic

requirement needed to continue with the courses and provision of lodging and food for

residential students and teachers, provision of residential boarding is an essential service for nay

university. Basing on all these the production cost of services depends (Min and Yan, 2013,

p.71). ABC or the activity based cost technique play an important role in determining analysing

and implementing service costs for universities here in this case the University of Nottingham.

The process further helps in identification of activities and services which are not

profitable and can help in reducing cost of the service without affecting the educational slandered

and prestige of the institution. In the present world self funding and profit for organisations even

educational institutions like Nottingham University is essential. In the era of Globalisation

focusing only on internal students or students within the country is not an option. But in looking

for students abroad there are various concerns that needs to be taken into consideration and

ABC(Activity Based Costing) plays an important role in this regard (Cropper and Cook, 2000,

p.66). The first concern in this regard is the affordability of courses among the student

community, if the organisation is not able to formulate a policy keeping the desired rate for the

services among students across the world, the institution in the end will not be able to admit any

student for their academic sessions, and if students are not admitted the institution needs to suffer

a huge loss as the fixed cost are to be paid by the university like the salary and remunerations of

the employees and in maintaining the university infrastructure (Malmi, 1999, p.663)

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.