Finance and HR for Sustainable Business Success: Sky Cafe Analysis

VerifiedAdded on 2023/01/17

|8

|2003

|26

Report

AI Summary

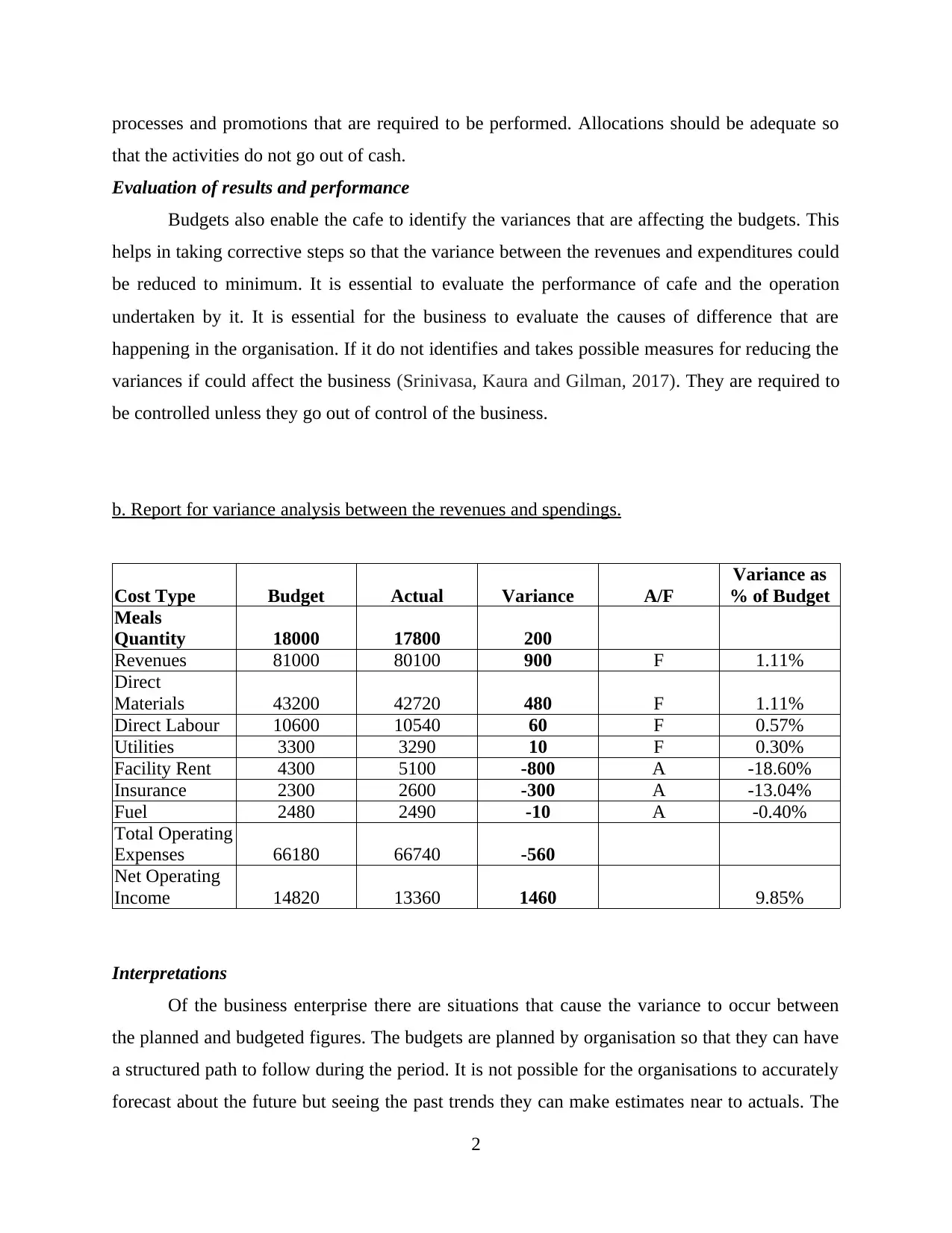

This report examines the financial performance of Sky Cafe, a coffee house, focusing on its budgeting and variance analysis. It outlines the objectives behind budget preparation, including planning, resource allocation, goal coordination, and performance evaluation. The report includes a variance analysis comparing budgeted and actual revenues and expenses, identifying variances in direct materials, labor, utilities, facility rent, and insurance. Key concerns for management are highlighted, such as the impact of increased rent and insurance premiums on profitability. The analysis also discusses strategies for cost control, including potential outsourcing and efficiency improvements. Finally, it underscores the importance of aligning financial planning with the company's objectives of profitability and customer satisfaction, suggesting measures to reduce variances and improve financial outcomes. The report references several academic sources to support its findings.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.