Financial Decision-Making in NHS Organizations

VerifiedAdded on 2019/12/28

|22

|5933

|161

Essay

AI Summary

The research highlights the limitations and drawbacks of the funding process for project expansion in NHS organizations. To make effective financial decisions, various information is required, including income, expenditures, financial statements, product quality, and service standards. The study concludes that benchmarks, criteria, and scoring systems are necessary to evaluate tenders effectively, ensuring the best choice for management.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGING FINANCE IN THE PUBLIC

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

SECTOR

Assignment by

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 In chosen nation explanation of the public sector............................................................1

1.2 Organisations funding and operating system...................................................................3

1.3 Information which are required to reporting in public sector company...........................8

TASK 2............................................................................................................................................9

2.1 Accountability of the firm with availability of financial information..............................9

2.2 Monitoring and controlling of financial resources in NHS organisation.......................11

2.3 Financial decision making process for NHS..................................................................12

TASK 3..........................................................................................................................................14

3.1 Tender documentation and tender process for NHS organisation..................................14

3.2 Criteria and scoring system for evaluation of tenders....................................................16

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

Assignment by

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 In chosen nation explanation of the public sector............................................................1

1.2 Organisations funding and operating system...................................................................3

1.3 Information which are required to reporting in public sector company...........................8

TASK 2............................................................................................................................................9

2.1 Accountability of the firm with availability of financial information..............................9

2.2 Monitoring and controlling of financial resources in NHS organisation.......................11

2.3 Financial decision making process for NHS..................................................................12

TASK 3..........................................................................................................................................14

3.1 Tender documentation and tender process for NHS organisation..................................14

3.2 Criteria and scoring system for evaluation of tenders....................................................16

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

INTRODUCTION

Finance plays a significant role in each and every business, without financial resources an

enterprise can not exist and survive in the market or industry. The main objective of managing

finance is to assure the best use of available funds. It further ensures optimum utilization of

funds at least cost. Thereafter, managing finance assure constant and appropriate supply of funds

to the business. The present report is based on the national heath services PLC (NHS) company

which is England based firm and operating in the healthcare sector. The company provides its

products and services across the world. The report describes informations which are needed for

increase the fund and require reporting to the authority body. Another part of the project shows

responsibility for financial informations and process for making financial decisions in the public

sector business. Apart from this last part of the report describes regarding to the tender and its

documentation as well as system of scoring for evaluating tenders.

TASK 1

1.1 In chosen nation explanation of the public sector

The public sector can be referred to as the state sector or the government sector, is a

portion of the state that deals with the manufacturing, control, sale, precondition, transportation

and allotment of goods and services by and for the government or its residents, whether national,

regional or local/municipal (Flynn, 2012). It is the income generating division which renders

administrative services to the public and community. The public sector differs from nation to

nation where it may involve, health care, education, roadways, railways, postal services, military

and police etc. In the public organisations there are all the control and monitoring is in

government's hand, it can be said that regulatory body of public company is government of the

country. Here the national health services company which is operating in the England country

where it needs to follow all the rules and regulations framed by respective country. Ownership of

the company is with government due to regulating the public organisations and all the policies

must be followed by the NHS. The England is in Europe continent where a union is established

by the countries for public sector and private sector companies as well. As per the European

union the public sector company has not to do any discrimination between employees, customers

and other stakeholders. Apart from this in the county the company can move or sell and buy

goods and services without any taxes and tariffs. In the England there is policy for the

government companies is that free movement of its products and services. Apart from this the

1

Finance plays a significant role in each and every business, without financial resources an

enterprise can not exist and survive in the market or industry. The main objective of managing

finance is to assure the best use of available funds. It further ensures optimum utilization of

funds at least cost. Thereafter, managing finance assure constant and appropriate supply of funds

to the business. The present report is based on the national heath services PLC (NHS) company

which is England based firm and operating in the healthcare sector. The company provides its

products and services across the world. The report describes informations which are needed for

increase the fund and require reporting to the authority body. Another part of the project shows

responsibility for financial informations and process for making financial decisions in the public

sector business. Apart from this last part of the report describes regarding to the tender and its

documentation as well as system of scoring for evaluating tenders.

TASK 1

1.1 In chosen nation explanation of the public sector

The public sector can be referred to as the state sector or the government sector, is a

portion of the state that deals with the manufacturing, control, sale, precondition, transportation

and allotment of goods and services by and for the government or its residents, whether national,

regional or local/municipal (Flynn, 2012). It is the income generating division which renders

administrative services to the public and community. The public sector differs from nation to

nation where it may involve, health care, education, roadways, railways, postal services, military

and police etc. In the public organisations there are all the control and monitoring is in

government's hand, it can be said that regulatory body of public company is government of the

country. Here the national health services company which is operating in the England country

where it needs to follow all the rules and regulations framed by respective country. Ownership of

the company is with government due to regulating the public organisations and all the policies

must be followed by the NHS. The England is in Europe continent where a union is established

by the countries for public sector and private sector companies as well. As per the European

union the public sector company has not to do any discrimination between employees, customers

and other stakeholders. Apart from this in the county the company can move or sell and buy

goods and services without any taxes and tariffs. In the England there is policy for the

government companies is that free movement of its products and services. Apart from this the

1

public sector business entities can freely provide its services across the world, in case of health

care companies there are no restrictions as well as obstacles in order to provide its services in the

world (Graham, 2014).

Furthermore, in the England country the public sector companies has freedom in order to

establish a new firm or expand existing business. There are all the rules, regulations and policies

as well procedures are better up to greater extent due to not facing any obstacles for establish and

operate in the country. As per the rules of England public sector companies are needs to follow

all the rules and regulation which are imposed by government for various functions such as

financial, operation, accounting and auditing, human resources, recruitment and selection process

etc. (NHS England. 2016). According to the present scenario government of the country is

contributing in the financial resources by which profitability ratios are high and business

performance is also better in comparison to another segment.

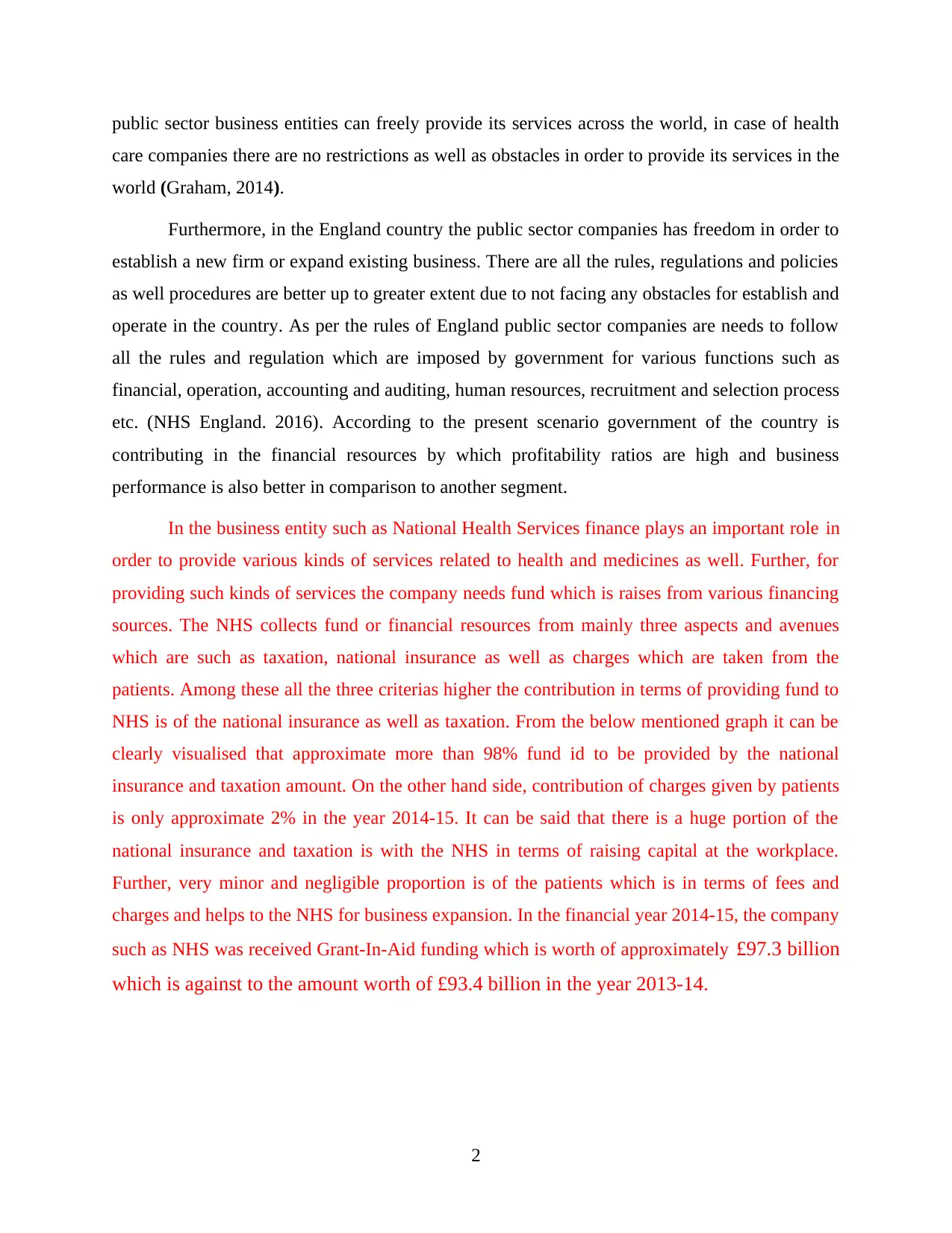

In the business entity such as National Health Services finance plays an important role in

order to provide various kinds of services related to health and medicines as well. Further, for

providing such kinds of services the company needs fund which is raises from various financing

sources. The NHS collects fund or financial resources from mainly three aspects and avenues

which are such as taxation, national insurance as well as charges which are taken from the

patients. Among these all the three criterias higher the contribution in terms of providing fund to

NHS is of the national insurance as well as taxation. From the below mentioned graph it can be

clearly visualised that approximate more than 98% fund id to be provided by the national

insurance and taxation amount. On the other hand side, contribution of charges given by patients

is only approximate 2% in the year 2014-15. It can be said that there is a huge portion of the

national insurance and taxation is with the NHS in terms of raising capital at the workplace.

Further, very minor and negligible proportion is of the patients which is in terms of fees and

charges and helps to the NHS for business expansion. In the financial year 2014-15, the company

such as NHS was received Grant-In-Aid funding which is worth of approximately £97.3 billion

which is against to the amount worth of £93.4 billion in the year 2013-14.

2

care companies there are no restrictions as well as obstacles in order to provide its services in the

world (Graham, 2014).

Furthermore, in the England country the public sector companies has freedom in order to

establish a new firm or expand existing business. There are all the rules, regulations and policies

as well procedures are better up to greater extent due to not facing any obstacles for establish and

operate in the country. As per the rules of England public sector companies are needs to follow

all the rules and regulation which are imposed by government for various functions such as

financial, operation, accounting and auditing, human resources, recruitment and selection process

etc. (NHS England. 2016). According to the present scenario government of the country is

contributing in the financial resources by which profitability ratios are high and business

performance is also better in comparison to another segment.

In the business entity such as National Health Services finance plays an important role in

order to provide various kinds of services related to health and medicines as well. Further, for

providing such kinds of services the company needs fund which is raises from various financing

sources. The NHS collects fund or financial resources from mainly three aspects and avenues

which are such as taxation, national insurance as well as charges which are taken from the

patients. Among these all the three criterias higher the contribution in terms of providing fund to

NHS is of the national insurance as well as taxation. From the below mentioned graph it can be

clearly visualised that approximate more than 98% fund id to be provided by the national

insurance and taxation amount. On the other hand side, contribution of charges given by patients

is only approximate 2% in the year 2014-15. It can be said that there is a huge portion of the

national insurance and taxation is with the NHS in terms of raising capital at the workplace.

Further, very minor and negligible proportion is of the patients which is in terms of fees and

charges and helps to the NHS for business expansion. In the financial year 2014-15, the company

such as NHS was received Grant-In-Aid funding which is worth of approximately £97.3 billion

which is against to the amount worth of £93.4 billion in the year 2013-14.

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1.2 Organisations funding and operating system

Every organisation whether it is public, private or non profit, all are needs finance or

capital in order to expand the business. For raise fund or capital in the firm there are different

sources available which provide financial services to the companies. National health services

organisation which is a public sector company also require finance for expand the services and

products as well as increase consumers. The government of the country is main sources of

finance for public sector enterprises and other several sources are also available. Another various

sources of finance are such as equity share, bank loan, venture capital, retained earnings,

merchant banking, leasing etc. When the NHS raise fund through various sources then it has to

pay cost of this in terms of different kinds and there are some limitation as well (Wang, 2015).

Drawbacks or limitations of the funding are enumerated below:

Most of the business entities prefer equity financing in order to enhance financial

resources in the company which helps to expand firm and product range as well. Very main

limitation of this funding is that, the company have to pay dividend amount year by year to the

stakeholders or investors. This factor impact to the financial performance of the firm adversely

because dividend is given to stakeholders from net profit of the enterprise. Apart from this

without listing or registering in stock market of respective country NHS cannot raise fund

through equity and unable to offer shares. As per the another funding option venture capital it

3

Every organisation whether it is public, private or non profit, all are needs finance or

capital in order to expand the business. For raise fund or capital in the firm there are different

sources available which provide financial services to the companies. National health services

organisation which is a public sector company also require finance for expand the services and

products as well as increase consumers. The government of the country is main sources of

finance for public sector enterprises and other several sources are also available. Another various

sources of finance are such as equity share, bank loan, venture capital, retained earnings,

merchant banking, leasing etc. When the NHS raise fund through various sources then it has to

pay cost of this in terms of different kinds and there are some limitation as well (Wang, 2015).

Drawbacks or limitations of the funding are enumerated below:

Most of the business entities prefer equity financing in order to enhance financial

resources in the company which helps to expand firm and product range as well. Very main

limitation of this funding is that, the company have to pay dividend amount year by year to the

stakeholders or investors. This factor impact to the financial performance of the firm adversely

because dividend is given to stakeholders from net profit of the enterprise. Apart from this

without listing or registering in stock market of respective country NHS cannot raise fund

through equity and unable to offer shares. As per the another funding option venture capital it

3

imposes cost on company in terms of stake of the firm. When the entity raise fund from venture

capital then it needs to give stake and dividend amount as well from margin earned by it.

Dividend is just like expense of the firm which lead to decrease level of profit by which financial

performance hampers in the industry (Shah, 2007). Hence, it can be said that funding is affects to

the firm in negative manner. Apart from this when NHS raise capital from bank loan then cost of

it is in terms of interest amount which is depended on the stock market. Interest amount is also

leads to reduce benefits or profit of the firm and impact on profitability in negative manner.

Drawback of bank loan is that when the firm is unable to pay loan amount then bank has power

to wound up whole business.

Government funding is another main source for the company in order to raise finance. In

the present case NHS raise fund from European regional development fund which a kind of

government funding. In this limitation is that, if government found any problem in respective

business then it can terminate contract and not provide fund. As per the sources all formalities

related to documentation must be appropriate, without this firm cannot raise capital in the

company (Starling, 2010). Hence, it can be analysed that with various advantages on other side

there are several drawbacks of the funding.

In the business various financial informations are available and analysed from different

financial statements like as Income statement, Balance sheet, Statement of cash flow, Statement

of shareholder's equity and gains etc. These all the statements and financial informations are

helpful for the NHS in order to meet accountability requirements as well as goals and objectives

of it. Further, the NHS has various trusts among then NHS foundation trust is to be chosen at

over here. The respective trust is a semi-autonomous unit of the NHS and take care department

of health by providing adequate fund to it. With the help of financial information available in

balance sheet the company able to meet various accountability requirements of

There are various kinds of accountability requirements are need to meet for the company

such as National Health Services foundation trusts in terms of statutory which helps to it in the

future in order to organise and raise fund. With the help of financial information available in

balance sheet the company able to meet various accountability requirements. Many kinds of

statutory accountability requirements for the entity like as NHS foundations trust with help of

balance sheet are stated as below:

4

capital then it needs to give stake and dividend amount as well from margin earned by it.

Dividend is just like expense of the firm which lead to decrease level of profit by which financial

performance hampers in the industry (Shah, 2007). Hence, it can be said that funding is affects to

the firm in negative manner. Apart from this when NHS raise capital from bank loan then cost of

it is in terms of interest amount which is depended on the stock market. Interest amount is also

leads to reduce benefits or profit of the firm and impact on profitability in negative manner.

Drawback of bank loan is that when the firm is unable to pay loan amount then bank has power

to wound up whole business.

Government funding is another main source for the company in order to raise finance. In

the present case NHS raise fund from European regional development fund which a kind of

government funding. In this limitation is that, if government found any problem in respective

business then it can terminate contract and not provide fund. As per the sources all formalities

related to documentation must be appropriate, without this firm cannot raise capital in the

company (Starling, 2010). Hence, it can be analysed that with various advantages on other side

there are several drawbacks of the funding.

In the business various financial informations are available and analysed from different

financial statements like as Income statement, Balance sheet, Statement of cash flow, Statement

of shareholder's equity and gains etc. These all the statements and financial informations are

helpful for the NHS in order to meet accountability requirements as well as goals and objectives

of it. Further, the NHS has various trusts among then NHS foundation trust is to be chosen at

over here. The respective trust is a semi-autonomous unit of the NHS and take care department

of health by providing adequate fund to it. With the help of financial information available in

balance sheet the company able to meet various accountability requirements of

There are various kinds of accountability requirements are need to meet for the company

such as National Health Services foundation trusts in terms of statutory which helps to it in the

future in order to organise and raise fund. With the help of financial information available in

balance sheet the company able to meet various accountability requirements. Many kinds of

statutory accountability requirements for the entity like as NHS foundations trust with help of

balance sheet are stated as below:

4

The respective statutory requirements are for keeping record of various financial

transactions as well as make the accounts effectively of NHS.

With this the management such as NHS is highly able to make different financial

accounts and statements for the end of every accounting year.

To comply various kinds of instructions, guidelines and directions which are

formulated and given by the respective authority and regulatory body of NHS

foundation trust.

To make accounting treatment and present annual report of NHS along with

financial statements in proper and structured format.

To present and show consolidated trust and information about different kinds of

consolidated financial accounts and informations of NHS.

Apart from this statutory requirements of the financial information and statement

are to publish in the industry or market at or before time period or deadline given

to the NHS.

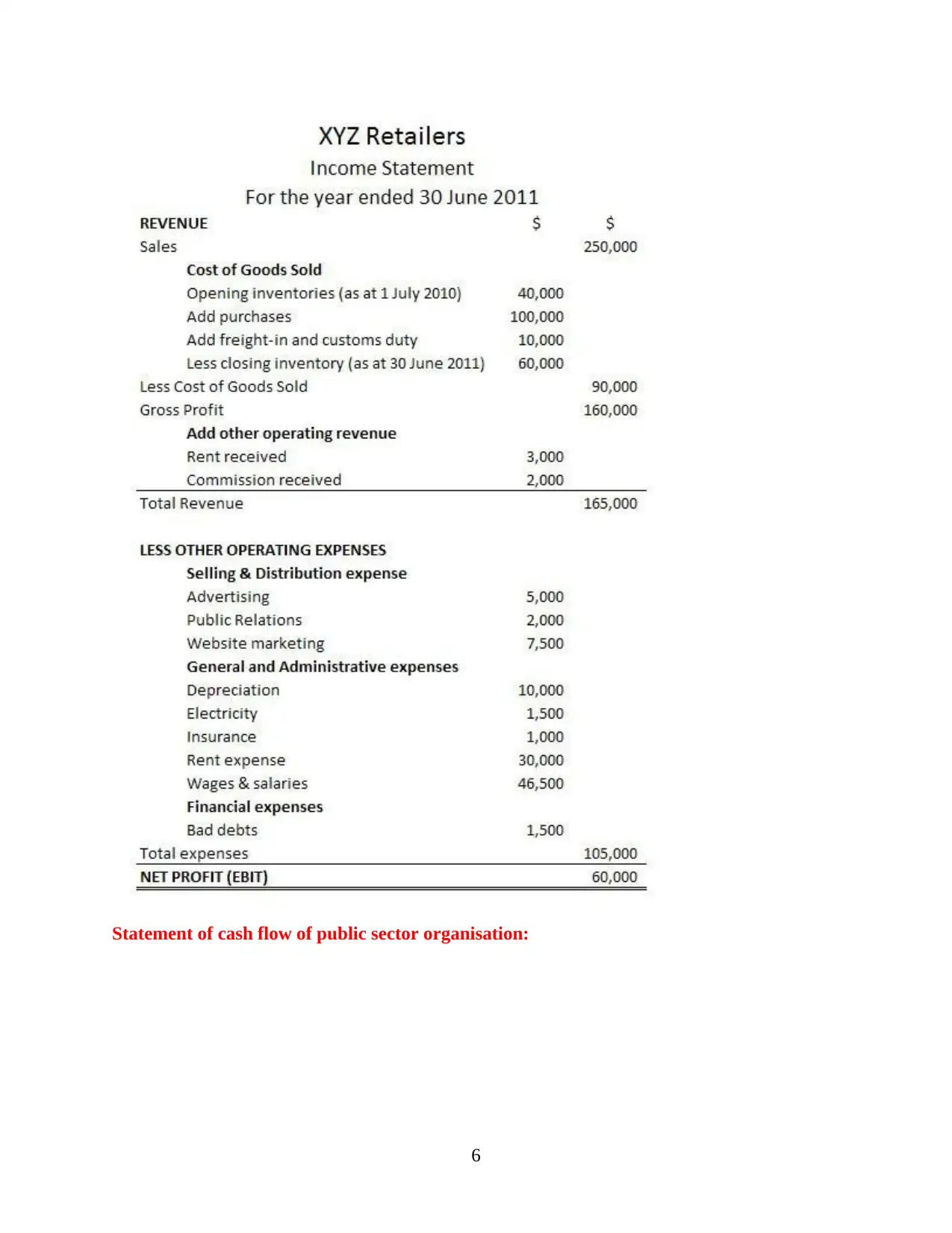

Statement of income of public sector organisation:

5

transactions as well as make the accounts effectively of NHS.

With this the management such as NHS is highly able to make different financial

accounts and statements for the end of every accounting year.

To comply various kinds of instructions, guidelines and directions which are

formulated and given by the respective authority and regulatory body of NHS

foundation trust.

To make accounting treatment and present annual report of NHS along with

financial statements in proper and structured format.

To present and show consolidated trust and information about different kinds of

consolidated financial accounts and informations of NHS.

Apart from this statutory requirements of the financial information and statement

are to publish in the industry or market at or before time period or deadline given

to the NHS.

Statement of income of public sector organisation:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

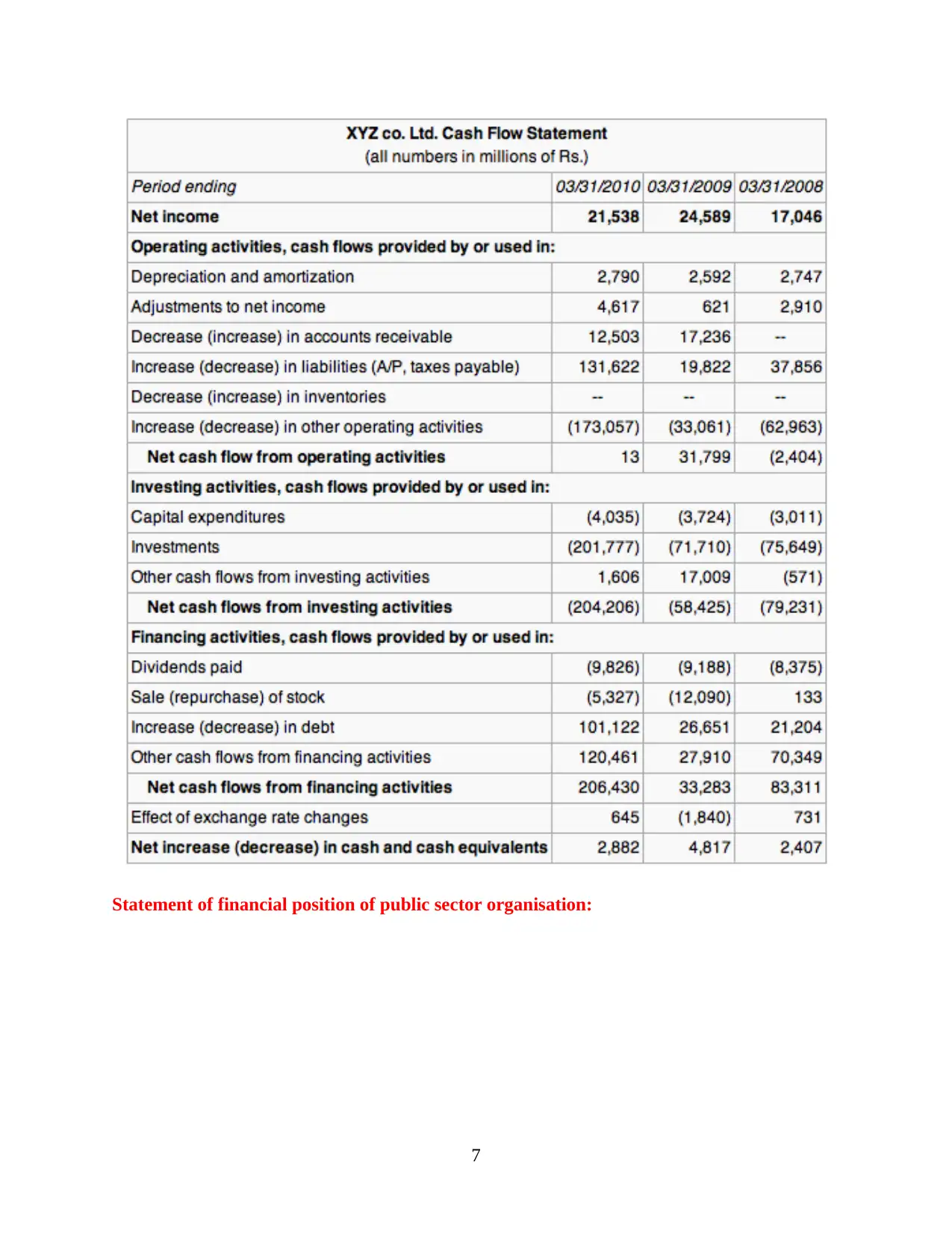

Statement of cash flow of public sector organisation:

6

6

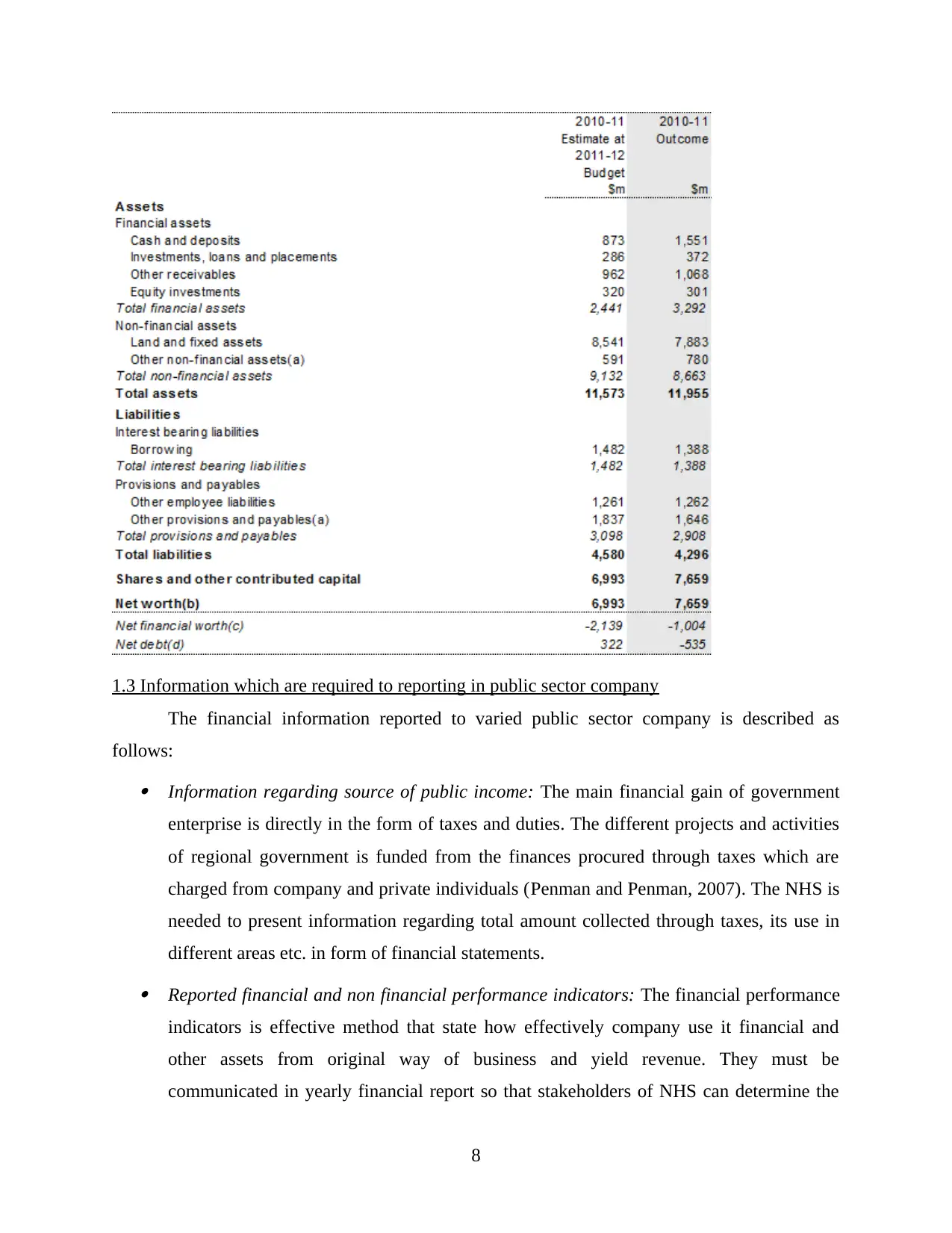

Statement of financial position of public sector organisation:

7

7

1.3 Information which are required to reporting in public sector company

The financial information reported to varied public sector company is described as

follows: Information regarding source of public income: The main financial gain of government

enterprise is directly in the form of taxes and duties. The different projects and activities

of regional government is funded from the finances procured through taxes which are

charged from company and private individuals (Penman and Penman, 2007). The NHS is

needed to present information regarding total amount collected through taxes, its use in

different areas etc. in form of financial statements. Reported financial and non financial performance indicators: The financial performance

indicators is effective method that state how effectively company use it financial and

other assets from original way of business and yield revenue. They must be

communicated in yearly financial report so that stakeholders of NHS can determine the

8

The financial information reported to varied public sector company is described as

follows: Information regarding source of public income: The main financial gain of government

enterprise is directly in the form of taxes and duties. The different projects and activities

of regional government is funded from the finances procured through taxes which are

charged from company and private individuals (Penman and Penman, 2007). The NHS is

needed to present information regarding total amount collected through taxes, its use in

different areas etc. in form of financial statements. Reported financial and non financial performance indicators: The financial performance

indicators is effective method that state how effectively company use it financial and

other assets from original way of business and yield revenue. They must be

communicated in yearly financial report so that stakeholders of NHS can determine the

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

financial position of the business (Revsine and et.al., 2005). The financial performance

can be shown through organization gain, sales, cash inflows and outflows, worth of

assets. The financial data must be communicated so that capitalist can make wise

judgement on whether to spend or not in NHS. While, non financial performance

indicators depends upon the satisfaction of employee, customers, service quality, market

share, and rate if creativity introduced in offering by entity (Schroeder, Clark and Cathey,

2011). The information regarding non financial and financial indicators is communicated

which assist in knowing the forthcoming fiscal performance of NHS. Published reports for varied entities: The public sector company is needed to prepare

annual report. It is broad report on the entity activities throughout preceding year. The

financial information along with the list of board of directors, key person of company are

detailed in annual report (Sueyoshi, 2005). Financial statements: It is the formal record of the financial activities and standing of

NHS. It further includes balance sheet, income statement, cash flow details etc. They

must be reliable as capitalist decision to make investment is depended upon the financial

statements.

Quality commission report: Being a health care organization, it is very much important

for NHS to provide the best quality services to its customers. The care quality report

specifies that company is maintaining the said quality standards or not (Wildeman and

Jogo, 2012).

TASK 2

2.1 Accountability of the firm with availability of financial information

Financial data are very necessary for the management which helps to determine financial

performance and accountability towards various stakeholders of the national health services

organisation. Analysis of the financial data which are helps to meet objectives of its stakeholders,

given as below:

Financial informations are derived from financial statements of the NHS company. There

are different financial statements are such as profit and loss statement, balance sheet or statement

of financial position, cash flow statement etc. From this all statement the company is able to

meet with goals of the various stakeholders (Bandy, 2014). Customers are key stakeholder of the

9

can be shown through organization gain, sales, cash inflows and outflows, worth of

assets. The financial data must be communicated so that capitalist can make wise

judgement on whether to spend or not in NHS. While, non financial performance

indicators depends upon the satisfaction of employee, customers, service quality, market

share, and rate if creativity introduced in offering by entity (Schroeder, Clark and Cathey,

2011). The information regarding non financial and financial indicators is communicated

which assist in knowing the forthcoming fiscal performance of NHS. Published reports for varied entities: The public sector company is needed to prepare

annual report. It is broad report on the entity activities throughout preceding year. The

financial information along with the list of board of directors, key person of company are

detailed in annual report (Sueyoshi, 2005). Financial statements: It is the formal record of the financial activities and standing of

NHS. It further includes balance sheet, income statement, cash flow details etc. They

must be reliable as capitalist decision to make investment is depended upon the financial

statements.

Quality commission report: Being a health care organization, it is very much important

for NHS to provide the best quality services to its customers. The care quality report

specifies that company is maintaining the said quality standards or not (Wildeman and

Jogo, 2012).

TASK 2

2.1 Accountability of the firm with availability of financial information

Financial data are very necessary for the management which helps to determine financial

performance and accountability towards various stakeholders of the national health services

organisation. Analysis of the financial data which are helps to meet objectives of its stakeholders,

given as below:

Financial informations are derived from financial statements of the NHS company. There

are different financial statements are such as profit and loss statement, balance sheet or statement

of financial position, cash flow statement etc. From this all statement the company is able to

meet with goals of the various stakeholders (Bandy, 2014). Customers are key stakeholder of the

9

company, without them a business can not run in the industry. They have objective towards the

firm that, it provides better products and services, when the firm has adequate finance then able

to fulfil their objectives. Financial information is profit which is most important, when investors

or shareholders make investment in the firm then analyse profitability. Hence, the firm generate

higher profit leads to attract more number of investors and increase shareholders. Apart from this

another financial informations are related to assets and liabilities of the firm which are shown in

balance sheet. Employees are another key element of the national service organisation, financial

data such as profit requires providing adequate and proper wages and salary by which it able to

meet their requirements. When NHS wants to raise fund then its responsibility that it has all the

informations properly or not (White, 2015). Furthermore, budget is also another concept which

provides financial information for the upcoming financial year. By this it able to fulfil objectives

and goals which are its stakeholders have. Every business entity have responsibilities that to

meet goals and objectives of several stakeholders such as consumer, investor, employee,

government etc.

In the firm there are various kinds of financial informations are available which are

derived from the financial statements such as balance sheet, incomes statement, cash flow

statement, total shareholder's equity and gains etc. With the help of these various financial

informations the company is able to monitor as well as control over the extra and miscellaneous

financial transactions. For example: when talking about income statement then it shows various

costs and revenue comes into existence at the workplace of NHS. Further, it able to know that

company has profit in which direction such as higher or lower. If it found that expenses are more

as compare to incomes then able to manager extra costs and monitor the activity where

expenditures incur at higher level. Furthermore, it able to formulate better strategies in order to

control over the extra expenses and fulfil objectives such as maximize profit.

Moreover, financial information in terms of liquid position is to be derived from balance

sheet of NHS. If the management found that ability of entity is not good and unable to meet with

short term debt then make various strategies to attract more number of customers and enhance

level of sales. Hence, it can be said that with the help of financial informations the NHS is highly

able to control and monitor over the firm and achieve financial goals and objectives of it.

10

firm that, it provides better products and services, when the firm has adequate finance then able

to fulfil their objectives. Financial information is profit which is most important, when investors

or shareholders make investment in the firm then analyse profitability. Hence, the firm generate

higher profit leads to attract more number of investors and increase shareholders. Apart from this

another financial informations are related to assets and liabilities of the firm which are shown in

balance sheet. Employees are another key element of the national service organisation, financial

data such as profit requires providing adequate and proper wages and salary by which it able to

meet their requirements. When NHS wants to raise fund then its responsibility that it has all the

informations properly or not (White, 2015). Furthermore, budget is also another concept which

provides financial information for the upcoming financial year. By this it able to fulfil objectives

and goals which are its stakeholders have. Every business entity have responsibilities that to

meet goals and objectives of several stakeholders such as consumer, investor, employee,

government etc.

In the firm there are various kinds of financial informations are available which are

derived from the financial statements such as balance sheet, incomes statement, cash flow

statement, total shareholder's equity and gains etc. With the help of these various financial

informations the company is able to monitor as well as control over the extra and miscellaneous

financial transactions. For example: when talking about income statement then it shows various

costs and revenue comes into existence at the workplace of NHS. Further, it able to know that

company has profit in which direction such as higher or lower. If it found that expenses are more

as compare to incomes then able to manager extra costs and monitor the activity where

expenditures incur at higher level. Furthermore, it able to formulate better strategies in order to

control over the extra expenses and fulfil objectives such as maximize profit.

Moreover, financial information in terms of liquid position is to be derived from balance

sheet of NHS. If the management found that ability of entity is not good and unable to meet with

short term debt then make various strategies to attract more number of customers and enhance

level of sales. Hence, it can be said that with the help of financial informations the NHS is highly

able to control and monitor over the firm and achieve financial goals and objectives of it.

10

2.2 Monitoring and controlling of financial resources in NHS organisation

There are wide range of decision that are taken by NHS Trust to assure proper

functioning of company. Since, it is inception that it is public sector company that can be

impacted by political parties and varied community. The decision are also influenced by different

factors. The example of major decision that are taken by NHS trust are investment into growth

and diversification activities etc. Thereafter, purchase of expensive machines, medical

equipments and technology are some decision that involve significant amount of funds (Chaston,

2011). The financial decisions are further supported by various techniques which are explained

as follows: Budgeting: It is a process where budget is prepared which leads to determine financial

data for the next accounting year. It is techniques in which budget is formulated on the

basis of past financial informations, where the management is able to forecast about

future cash flows such as inflow and outflow. For example various budgets such as cash,

sales, material, production etc. which provide information that how much revenue is to be

generate in next year. Furthermore, it gives informations to NHS related to production

units, raw material required etc. and incomes and expenditures as well (Wildeman and

Jogo, 2012). With this the management is able to control and monitor all financial

resources in effective manner and enhance profitability as well. Cost benefit analysis: It is method which is reasoned to ascertain the advantage of

pecuniary worth over cost. During financial decisions making, NHS Trust's use the cost

benefit analysis. In this technique, if the profit surpass the worth of cost, then the decision

is reasoned as executable and taken by the financial executive. It is assured that in no

case, profits must not be less than the cost. In this analysis there are various components

are used such as variable cost, direct cost, fixed cost, indirect cost etc (Metemadi, and

et.al.,2016. Capital Budgeting methods: Tool which helps to organiser in order to assess viability of

the project and provide appropriate decision, known as a capital budgeting method. It

helps to the NHS for undertake or choose and particular project among two or more

mutually exclusive projects. National heath service trust execute investment appraisal

techniques while planning to start other healthcare facility under the reputation of trust in

11

There are wide range of decision that are taken by NHS Trust to assure proper

functioning of company. Since, it is inception that it is public sector company that can be

impacted by political parties and varied community. The decision are also influenced by different

factors. The example of major decision that are taken by NHS trust are investment into growth

and diversification activities etc. Thereafter, purchase of expensive machines, medical

equipments and technology are some decision that involve significant amount of funds (Chaston,

2011). The financial decisions are further supported by various techniques which are explained

as follows: Budgeting: It is a process where budget is prepared which leads to determine financial

data for the next accounting year. It is techniques in which budget is formulated on the

basis of past financial informations, where the management is able to forecast about

future cash flows such as inflow and outflow. For example various budgets such as cash,

sales, material, production etc. which provide information that how much revenue is to be

generate in next year. Furthermore, it gives informations to NHS related to production

units, raw material required etc. and incomes and expenditures as well (Wildeman and

Jogo, 2012). With this the management is able to control and monitor all financial

resources in effective manner and enhance profitability as well. Cost benefit analysis: It is method which is reasoned to ascertain the advantage of

pecuniary worth over cost. During financial decisions making, NHS Trust's use the cost

benefit analysis. In this technique, if the profit surpass the worth of cost, then the decision

is reasoned as executable and taken by the financial executive. It is assured that in no

case, profits must not be less than the cost. In this analysis there are various components

are used such as variable cost, direct cost, fixed cost, indirect cost etc (Metemadi, and

et.al.,2016. Capital Budgeting methods: Tool which helps to organiser in order to assess viability of

the project and provide appropriate decision, known as a capital budgeting method. It

helps to the NHS for undertake or choose and particular project among two or more

mutually exclusive projects. National heath service trust execute investment appraisal

techniques while planning to start other healthcare facility under the reputation of trust in

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

other location and spread out their market share. The decision is taken only after

analysing that such expansion project are executable and gainful in coming time. For

example net present value, internal rate of return, profitability index, average rate of

return, payback period etc (Abraham, 2006). By this firm able to chose appropriate

project and able to manage its financial resources.

Ratio analysis: It is among the effective method that help in taking future financial

decisions. The analysis helps to the management in order to determine financial health

and performance of the firm in the healthcare industry. It is followed by NHS during

preparation of financial report to be bestowed to the stakeholders. With the help of this

method, various ratio are analysed to study the performance of organization. Examples

are such as profitability, liquidity, gearing or solvency, efficiency ratios etc. which

measures financial performance in the industry.

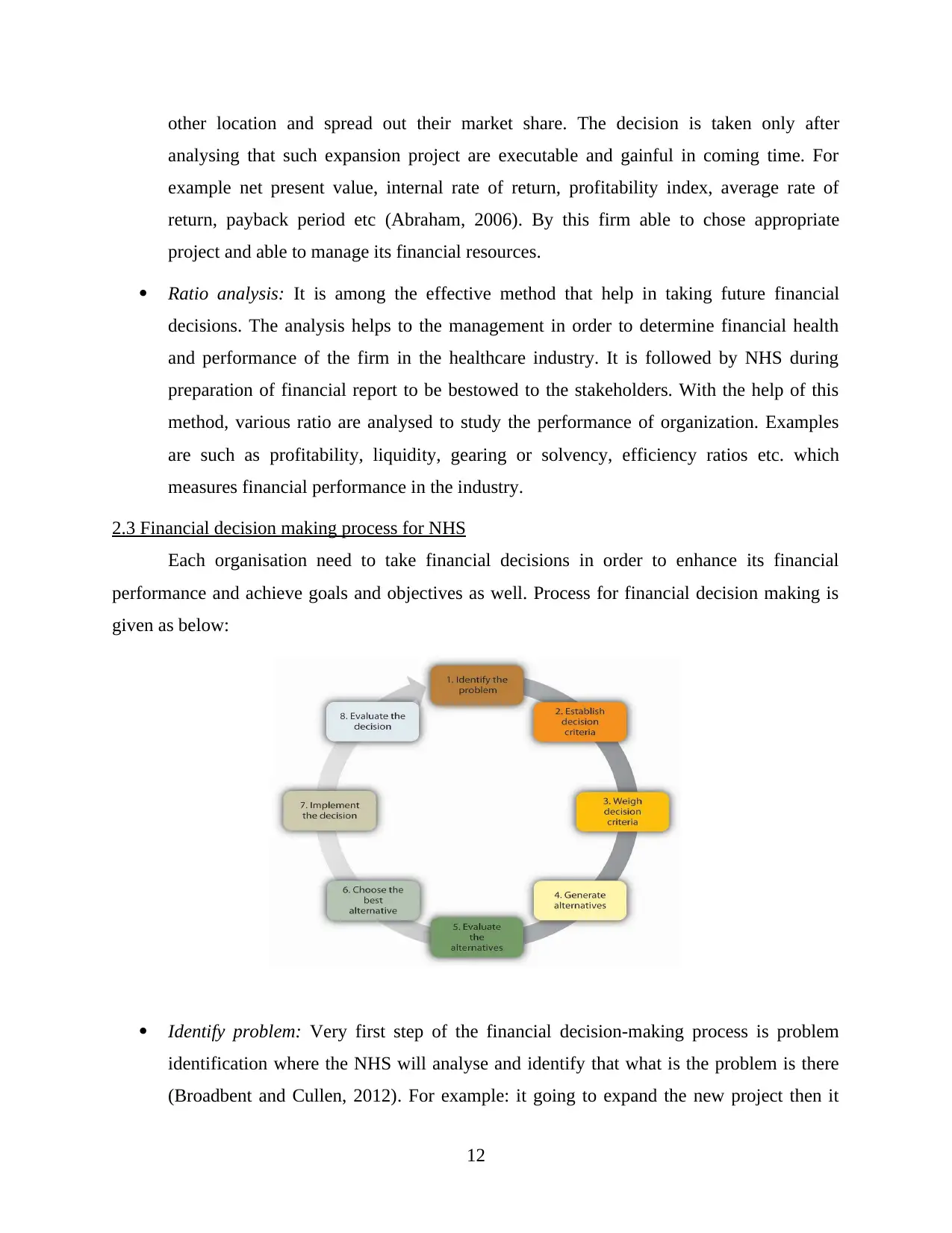

2.3 Financial decision making process for NHS

Each organisation need to take financial decisions in order to enhance its financial

performance and achieve goals and objectives as well. Process for financial decision making is

given as below:

Identify problem: Very first step of the financial decision-making process is problem

identification where the NHS will analyse and identify that what is the problem is there

(Broadbent and Cullen, 2012). For example: it going to expand the new project then it

12

analysing that such expansion project are executable and gainful in coming time. For

example net present value, internal rate of return, profitability index, average rate of

return, payback period etc (Abraham, 2006). By this firm able to chose appropriate

project and able to manage its financial resources.

Ratio analysis: It is among the effective method that help in taking future financial

decisions. The analysis helps to the management in order to determine financial health

and performance of the firm in the healthcare industry. It is followed by NHS during

preparation of financial report to be bestowed to the stakeholders. With the help of this

method, various ratio are analysed to study the performance of organization. Examples

are such as profitability, liquidity, gearing or solvency, efficiency ratios etc. which

measures financial performance in the industry.

2.3 Financial decision making process for NHS

Each organisation need to take financial decisions in order to enhance its financial

performance and achieve goals and objectives as well. Process for financial decision making is

given as below:

Identify problem: Very first step of the financial decision-making process is problem

identification where the NHS will analyse and identify that what is the problem is there

(Broadbent and Cullen, 2012). For example: it going to expand the new project then it

12

will find that due to which problem decision is to be taken. Further, when at the initial

phase the National Health Services will identify that due to which cause capital is to

invest and expand it at the broader level. Establish decision criteria: Furthermore, the criteria which is identified by NHS for make

decision i.e. expansion of new project will be established in the present step. Here the

NHS will establish a decision that by how above mentioned problem will be easily

resolve. Weigh decision criteria: In this firm will be analyse about that criteria and check that

whether it will be effective for the NHS or not. If effective and beneficial then move for

further step otherwise corrective action will be taken by the NHS (Metemadi, and

et.al.,2016). Generate alternatives: Here NHS will generate different alternatives for expand the

project. For example: various capital budgeting methods such as NPV, IRR, ARR,

payback etc. will be consider which are alternatives for taking decision in NHS. Evaluate the alternatives: In this step the management of NHS evaluate that which one

alternative or method will be appropriate for making decision. The company such as NHS

uses net present value which shows future value of initial investment. Choose the best alternative: Further, the method which gives higher return of initial

investment will be chosen and financial decision is to be taken by management of NHS.

Implement the decision: Second last step is implementation of the decisions which is

made in earlier step. Here the decision is applied or implement in the NHS for expansion

of the new project and invest capital.

Evaluate the decision: Last step is evaluation of the decision where the management of

NHS or controlling staff will be check and evaluate about the project. If NHS found any

problem and identify that the project is not working properly then corrective action is

taken in this step by management of NHS (Revsine and et.al., 2005).

Apart from the above mentioned financial decision making process the NHS going to

invest capital in the another criteria which helps to expand the entity at broader level up

to greater extent. NHS Trust Development Authority is taken by the company in order to

13

phase the National Health Services will identify that due to which cause capital is to

invest and expand it at the broader level. Establish decision criteria: Furthermore, the criteria which is identified by NHS for make

decision i.e. expansion of new project will be established in the present step. Here the

NHS will establish a decision that by how above mentioned problem will be easily

resolve. Weigh decision criteria: In this firm will be analyse about that criteria and check that

whether it will be effective for the NHS or not. If effective and beneficial then move for

further step otherwise corrective action will be taken by the NHS (Metemadi, and

et.al.,2016). Generate alternatives: Here NHS will generate different alternatives for expand the

project. For example: various capital budgeting methods such as NPV, IRR, ARR,

payback etc. will be consider which are alternatives for taking decision in NHS. Evaluate the alternatives: In this step the management of NHS evaluate that which one

alternative or method will be appropriate for making decision. The company such as NHS

uses net present value which shows future value of initial investment. Choose the best alternative: Further, the method which gives higher return of initial

investment will be chosen and financial decision is to be taken by management of NHS.

Implement the decision: Second last step is implementation of the decisions which is

made in earlier step. Here the decision is applied or implement in the NHS for expansion

of the new project and invest capital.

Evaluate the decision: Last step is evaluation of the decision where the management of

NHS or controlling staff will be check and evaluate about the project. If NHS found any

problem and identify that the project is not working properly then corrective action is

taken in this step by management of NHS (Revsine and et.al., 2005).

Apart from the above mentioned financial decision making process the NHS going to

invest capital in the another criteria which helps to expand the entity at broader level up

to greater extent. NHS Trust Development Authority is taken by the company in order to

13

take fund and invest. Moreover, financial decision making process is to be used at here

which has mainly three stages which are explained as below:1. Outline Analysis: In this step the NHS make and prepare outline or plan in order to

make capital investment. Here it formulates a plan that in which order capital will

be invested in particular sector and after analysing it go for further process.2. Detailed Evaluation and review: In the second phase of financial decision making

the NHS evaluate outline and plan which is prepared in the above stage. Further,

NHS analyses that in the future respective investment will be profitable or not.

After this, it reviews overall plan and then apply or implement at the workplace.

3. Decisions and Execution: At the last and third step National Health Services make

decisions to implement above evaluated outline of capital investment. After taking

decision to apply it executes or make investment in the avenue.

TASK 3

3.1 Tender documentation and tender process for NHS organisation

Tender can be defined as offer to perform a function which offering party is duty bound

to fulfil the promise to the party to which the offer is made. In this respect, the NHS Trust, issue

tender to the outside bodies regarding building of new hospital for the intention of enlargement.

It may consider supply of materials like, cement, construction equipments for building new

hospital. In addition to tender can be given for supply of medicinal drug, beds, stretchers or

medical devices which are needed by the NHS Trust (Schroeder, Clark and Cathey, 2011). In the

context of the public sector companies, tenders are issued to the public and the written agreement

is done with the suitable individual who meet the responsibility with supreme potency and

minimal cost. The requirements of tender are collected in terms of invitation. This invitation can

be provided through emails, post, by courier of by hand. The newspapers also contain

information about tender.

Documents required for the tender are given as below:

Certified copy of Document of registration of NHS, which show name of firm,

registration number, registration date, current directors and board members.

14

which has mainly three stages which are explained as below:1. Outline Analysis: In this step the NHS make and prepare outline or plan in order to

make capital investment. Here it formulates a plan that in which order capital will

be invested in particular sector and after analysing it go for further process.2. Detailed Evaluation and review: In the second phase of financial decision making

the NHS evaluate outline and plan which is prepared in the above stage. Further,

NHS analyses that in the future respective investment will be profitable or not.

After this, it reviews overall plan and then apply or implement at the workplace.

3. Decisions and Execution: At the last and third step National Health Services make

decisions to implement above evaluated outline of capital investment. After taking

decision to apply it executes or make investment in the avenue.

TASK 3

3.1 Tender documentation and tender process for NHS organisation

Tender can be defined as offer to perform a function which offering party is duty bound

to fulfil the promise to the party to which the offer is made. In this respect, the NHS Trust, issue

tender to the outside bodies regarding building of new hospital for the intention of enlargement.

It may consider supply of materials like, cement, construction equipments for building new

hospital. In addition to tender can be given for supply of medicinal drug, beds, stretchers or

medical devices which are needed by the NHS Trust (Schroeder, Clark and Cathey, 2011). In the

context of the public sector companies, tenders are issued to the public and the written agreement

is done with the suitable individual who meet the responsibility with supreme potency and

minimal cost. The requirements of tender are collected in terms of invitation. This invitation can

be provided through emails, post, by courier of by hand. The newspapers also contain

information about tender.

Documents required for the tender are given as below:

Certified copy of Document of registration of NHS, which show name of firm,

registration number, registration date, current directors and board members.

14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Certified copy of Directors and member's ID documents.

Certified copy of its shareholder's certificates.

Financial statements of last three years.

Annual report of NHS company.

Proof of membership of national contract association.

The tender process used by NHS Trust is described as follows: Identification of need: First of all, the requirement for issuance of tender is determined.

Therefore, tender is developed when company require reliable source of business. In case

there are too many suppliers and there is confusion regarding which must be selected by

entity tender can be used (Tenders & Contracts. 2014). Selecting supplier: Since its inception that tender is open invitation to the public. To

maintain the standards of NHS, entity only select the suppliers that provide the best

quality products at affordable price. Hence, competent suppliers that can take tender and

meet the requirement with maximum efficiency within the provided time frame can be

selected. Preparation of Documents: The required documents are prepared by management of

entity. In this the introduction, description of contract and submission of documentation

is required. Contract award: Just after the trust get tender application, they assess them and look

forward for the best supplier. The assessment for choice the best bidder is done through

different techniques and contract is granted to them (Wildeman and Jogo, 2012).

Monitoring and controlling: After providing the tender, constant observation and control

is done to guarantee top-quality outcome from the suppliers. It is performed by NHS

Trust to debar any destructive results that could cause failure of company efforts and

money. Further, use of poor quality input provided by the suppliers can destroy the image

of NHS and thus, it is important to supervise the work of suppliers.

15

Certified copy of its shareholder's certificates.

Financial statements of last three years.

Annual report of NHS company.

Proof of membership of national contract association.

The tender process used by NHS Trust is described as follows: Identification of need: First of all, the requirement for issuance of tender is determined.

Therefore, tender is developed when company require reliable source of business. In case

there are too many suppliers and there is confusion regarding which must be selected by

entity tender can be used (Tenders & Contracts. 2014). Selecting supplier: Since its inception that tender is open invitation to the public. To

maintain the standards of NHS, entity only select the suppliers that provide the best

quality products at affordable price. Hence, competent suppliers that can take tender and

meet the requirement with maximum efficiency within the provided time frame can be

selected. Preparation of Documents: The required documents are prepared by management of

entity. In this the introduction, description of contract and submission of documentation

is required. Contract award: Just after the trust get tender application, they assess them and look

forward for the best supplier. The assessment for choice the best bidder is done through

different techniques and contract is granted to them (Wildeman and Jogo, 2012).

Monitoring and controlling: After providing the tender, constant observation and control

is done to guarantee top-quality outcome from the suppliers. It is performed by NHS

Trust to debar any destructive results that could cause failure of company efforts and

money. Further, use of poor quality input provided by the suppliers can destroy the image

of NHS and thus, it is important to supervise the work of suppliers.

15

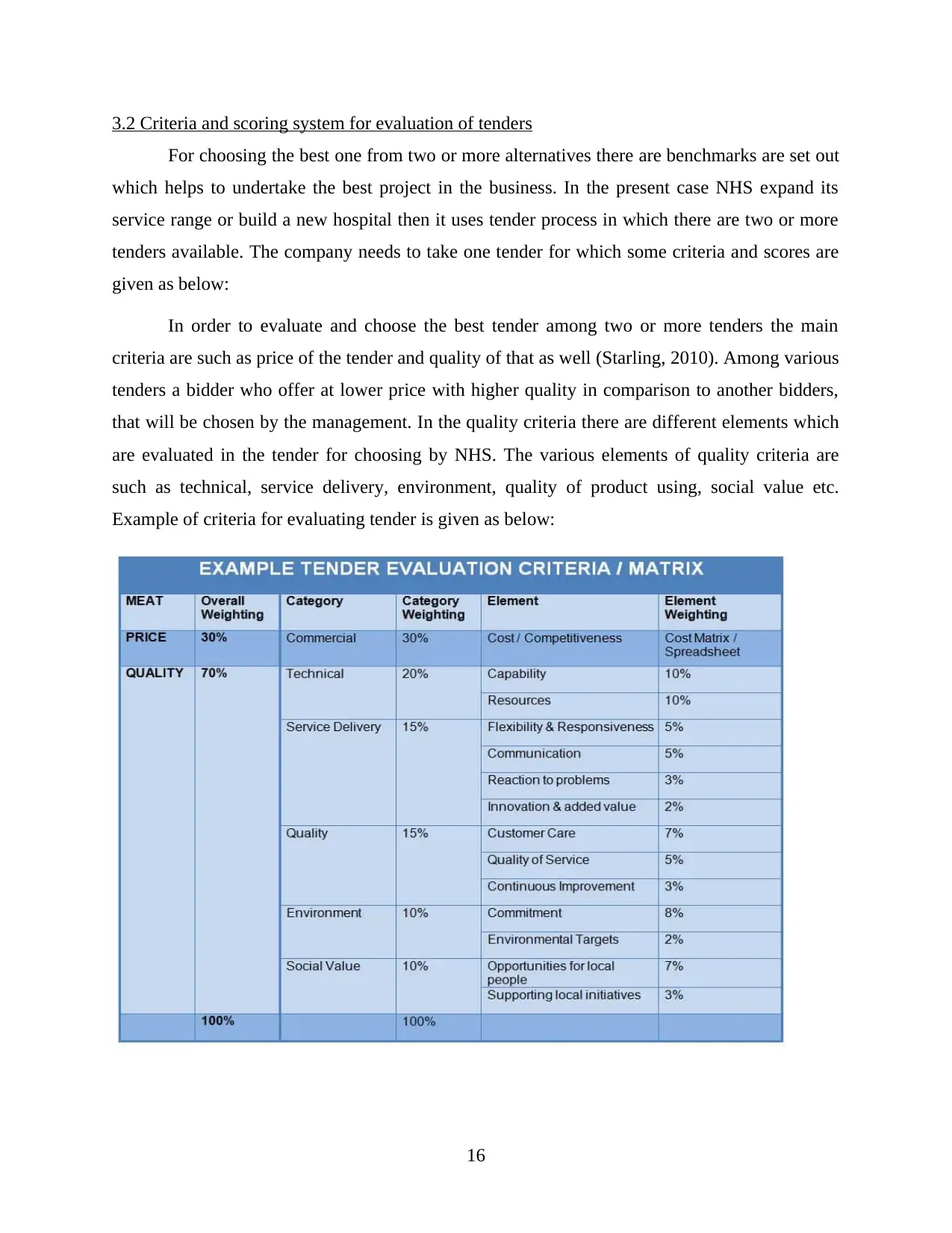

3.2 Criteria and scoring system for evaluation of tenders

For choosing the best one from two or more alternatives there are benchmarks are set out

which helps to undertake the best project in the business. In the present case NHS expand its

service range or build a new hospital then it uses tender process in which there are two or more

tenders available. The company needs to take one tender for which some criteria and scores are

given as below:

In order to evaluate and choose the best tender among two or more tenders the main

criteria are such as price of the tender and quality of that as well (Starling, 2010). Among various

tenders a bidder who offer at lower price with higher quality in comparison to another bidders,

that will be chosen by the management. In the quality criteria there are different elements which

are evaluated in the tender for choosing by NHS. The various elements of quality criteria are

such as technical, service delivery, environment, quality of product using, social value etc.

Example of criteria for evaluating tender is given as below:

16

For choosing the best one from two or more alternatives there are benchmarks are set out

which helps to undertake the best project in the business. In the present case NHS expand its

service range or build a new hospital then it uses tender process in which there are two or more

tenders available. The company needs to take one tender for which some criteria and scores are

given as below:

In order to evaluate and choose the best tender among two or more tenders the main

criteria are such as price of the tender and quality of that as well (Starling, 2010). Among various

tenders a bidder who offer at lower price with higher quality in comparison to another bidders,

that will be chosen by the management. In the quality criteria there are different elements which

are evaluated in the tender for choosing by NHS. The various elements of quality criteria are

such as technical, service delivery, environment, quality of product using, social value etc.

Example of criteria for evaluating tender is given as below:

16

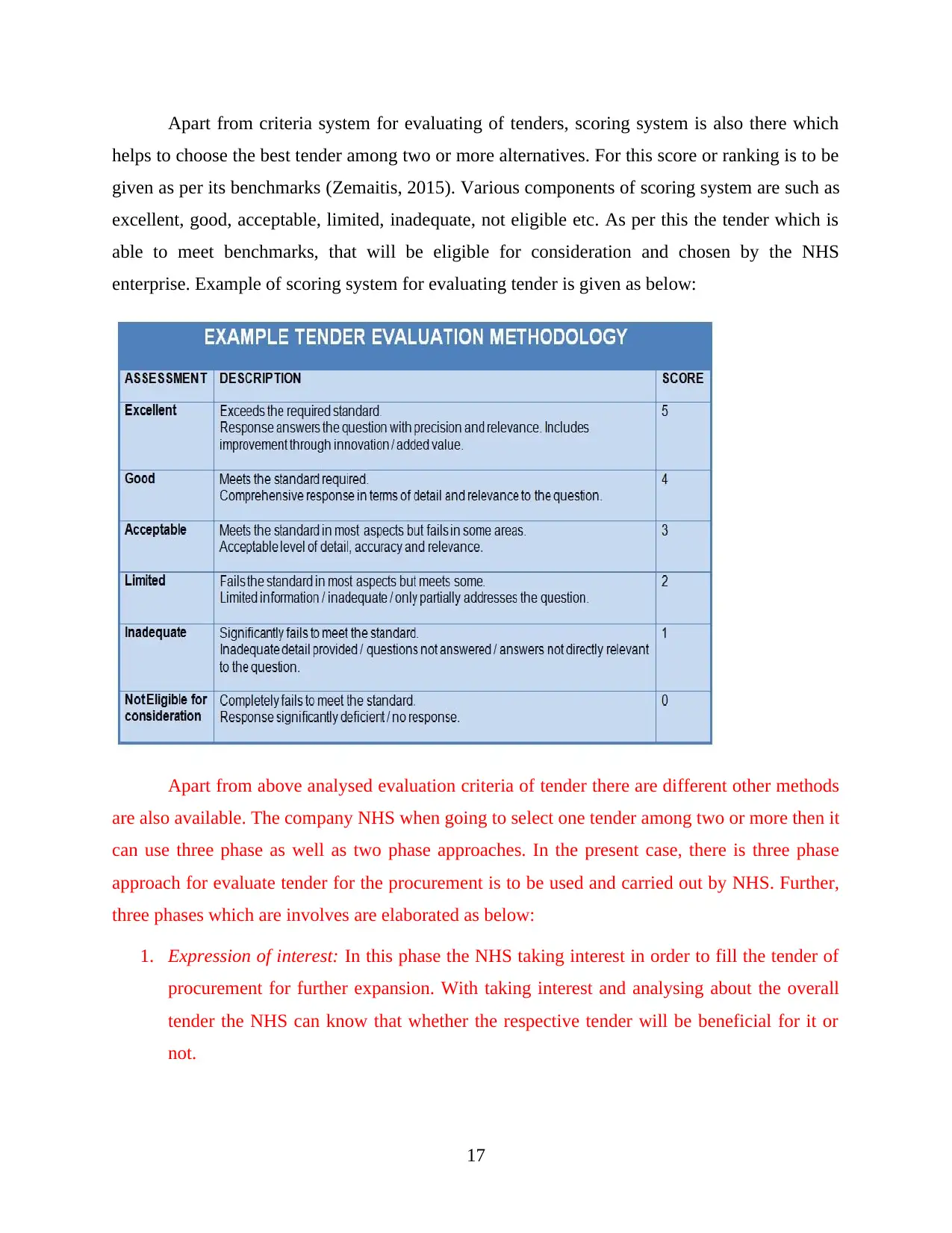

Apart from criteria system for evaluating of tenders, scoring system is also there which

helps to choose the best tender among two or more alternatives. For this score or ranking is to be

given as per its benchmarks (Zemaitis, 2015). Various components of scoring system are such as

excellent, good, acceptable, limited, inadequate, not eligible etc. As per this the tender which is

able to meet benchmarks, that will be eligible for consideration and chosen by the NHS

enterprise. Example of scoring system for evaluating tender is given as below:

Apart from above analysed evaluation criteria of tender there are different other methods

are also available. The company NHS when going to select one tender among two or more then it

can use three phase as well as two phase approaches. In the present case, there is three phase

approach for evaluate tender for the procurement is to be used and carried out by NHS. Further,

three phases which are involves are elaborated as below:

1. Expression of interest: In this phase the NHS taking interest in order to fill the tender of

procurement for further expansion. With taking interest and analysing about the overall

tender the NHS can know that whether the respective tender will be beneficial for it or

not.

17

helps to choose the best tender among two or more alternatives. For this score or ranking is to be

given as per its benchmarks (Zemaitis, 2015). Various components of scoring system are such as

excellent, good, acceptable, limited, inadequate, not eligible etc. As per this the tender which is

able to meet benchmarks, that will be eligible for consideration and chosen by the NHS

enterprise. Example of scoring system for evaluating tender is given as below:

Apart from above analysed evaluation criteria of tender there are different other methods

are also available. The company NHS when going to select one tender among two or more then it

can use three phase as well as two phase approaches. In the present case, there is three phase

approach for evaluate tender for the procurement is to be used and carried out by NHS. Further,

three phases which are involves are elaborated as below:

1. Expression of interest: In this phase the NHS taking interest in order to fill the tender of

procurement for further expansion. With taking interest and analysing about the overall

tender the NHS can know that whether the respective tender will be beneficial for it or

not.

17

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Technical bid evaluation: As per the second phase of tender evaluation the NHS evaluate

on the basis of different technical criteria. At such stage, the National Health Services

thinks technically and evaluate merits as well as demerits of the tender. On the basis of

this the NHS give rank or award to the tenders and then go for further step.

3. Commercial bid opening: At the last phase of tender evaluation the NHS select one

tender among two or more mutually exclusive tenders. Among all a particular tender

which provides higher return and beneficial then NHS will take and complete all the

commercial requirements.

CONCLUSION

From the above research it can be articulated that there are various drawbacks or

limitation of funding process for expansion of the project in NHS organization. Informations

which are required in order to reporting are such as income, expenditures, financial statements,

quality of products and services etc. It can be summarized that various financial informations

requires in order to complete responsibilities of fulfil objectives of its stakeholders. For taking

appropriate financial decision there is a process which helps to make effective decisions and

enhance profitability of the NHS. It can be concluded that for undertake one tender among two

or more tenders there are some benchmarks, criteria and scoring system set out which helps to

management for taking the best one tender.

18

on the basis of different technical criteria. At such stage, the National Health Services

thinks technically and evaluate merits as well as demerits of the tender. On the basis of

this the NHS give rank or award to the tenders and then go for further step.

3. Commercial bid opening: At the last phase of tender evaluation the NHS select one

tender among two or more mutually exclusive tenders. Among all a particular tender

which provides higher return and beneficial then NHS will take and complete all the

commercial requirements.

CONCLUSION

From the above research it can be articulated that there are various drawbacks or

limitation of funding process for expansion of the project in NHS organization. Informations

which are required in order to reporting are such as income, expenditures, financial statements,

quality of products and services etc. It can be summarized that various financial informations

requires in order to complete responsibilities of fulfil objectives of its stakeholders. For taking

appropriate financial decision there is a process which helps to make effective decisions and

enhance profitability of the NHS. It can be concluded that for undertake one tender among two

or more tenders there are some benchmarks, criteria and scoring system set out which helps to

management for taking the best one tender.

18

REFERENCES

Books and Journals

Abraham, A., 2006. Financial management in the nonprofit sector: A mission-based approach to

ratio analysis in membership organizations.

Bandy, G., 2014. Financial Management and Accounting in the Public Sector. Routledge.

Broadbent, M. and Cullen, J., 2012. Managing financial resources. Routledge.

Chaston, I., 2011. Public Sector Management: Mission Impossible?. Palgrave Macmillan.

Flynn, N., 2012. Public Sector Management. SAGE.

Graham, A., 2014. Canadian Public-Sector Financial Management, Second Edition. McGill-

Queen's Press – MQUP.

Metemadi, M. and et.al.,2016. Analysis of social functions in Iran’s public hospitals: pattern of

offering discounts to poor patients. International Journal of Human Rights in Healthcare.

Vol. 9(4). pp. -

Penman, S. H. and Penman, S. H., 2007. Financial statement analysis and security valuation (p.

476). New York: McGraw-Hill.

Revsine, L. and et.al., 2005. Financial reporting and analysis. New York, NY: Pearson/Prentice

Hall.

Schroeder, R. G., Clark, M. W. and Cathey, J. M., 2011. Financial accounting theory and

analysis: text and cases. John Wiley and Sons.

Shah, A., 2007. Local Public Financial Management. World Bank Publications.

Starling, G., 2010. Managing the Public Sector. Cengage Learning.

Sueyoshi, T., 2005. Financial ratio analysis of the electric power industry. Asia-Pacific Journal

of Operational Research. 22(03). pp. 349-376.

Wang, 2015. Financial Management in the Public Sector: Tools, Applications, and Cases. M.E.

Sharpe.

White, D. J., 2015. Managing Information in the Public Sector. Routledge.

Wildeman, R. and Jogo, W., 2012. Implementing the Public Finance Management Act in South

Africa: How Far are We?. African Books Collective.

Online

19

Books and Journals

Abraham, A., 2006. Financial management in the nonprofit sector: A mission-based approach to

ratio analysis in membership organizations.

Bandy, G., 2014. Financial Management and Accounting in the Public Sector. Routledge.

Broadbent, M. and Cullen, J., 2012. Managing financial resources. Routledge.

Chaston, I., 2011. Public Sector Management: Mission Impossible?. Palgrave Macmillan.

Flynn, N., 2012. Public Sector Management. SAGE.

Graham, A., 2014. Canadian Public-Sector Financial Management, Second Edition. McGill-

Queen's Press – MQUP.

Metemadi, M. and et.al.,2016. Analysis of social functions in Iran’s public hospitals: pattern of

offering discounts to poor patients. International Journal of Human Rights in Healthcare.

Vol. 9(4). pp. -

Penman, S. H. and Penman, S. H., 2007. Financial statement analysis and security valuation (p.

476). New York: McGraw-Hill.

Revsine, L. and et.al., 2005. Financial reporting and analysis. New York, NY: Pearson/Prentice

Hall.

Schroeder, R. G., Clark, M. W. and Cathey, J. M., 2011. Financial accounting theory and

analysis: text and cases. John Wiley and Sons.

Shah, A., 2007. Local Public Financial Management. World Bank Publications.

Starling, G., 2010. Managing the Public Sector. Cengage Learning.

Sueyoshi, T., 2005. Financial ratio analysis of the electric power industry. Asia-Pacific Journal

of Operational Research. 22(03). pp. 349-376.

Wang, 2015. Financial Management in the Public Sector: Tools, Applications, and Cases. M.E.

Sharpe.

White, D. J., 2015. Managing Information in the Public Sector. Routledge.

Wildeman, R. and Jogo, W., 2012. Implementing the Public Finance Management Act in South

Africa: How Far are We?. African Books Collective.

Online

19

NHS England. 2015. [online] England.nhs.uk. Available at: http://www.england.nhs.uk/about/

[Accessed on 14th January 2017].

Tenders & Contracts. 2014. [Online]. Available through:

<https://www.sutton.gov.uk/index.aspx?articleid=3410> [Accessed on 14th January

2017].

Zemaitis T., 2015. Understanding Tender Evaluation Criteria. [Online]. Available through:

<http://www.zemaitis-uk.com/tender-evaluation-criteria/> [Accessed on 14th January

2017].

20

[Accessed on 14th January 2017].

Tenders & Contracts. 2014. [Online]. Available through:

<https://www.sutton.gov.uk/index.aspx?articleid=3410> [Accessed on 14th January

2017].

Zemaitis T., 2015. Understanding Tender Evaluation Criteria. [Online]. Available through:

<http://www.zemaitis-uk.com/tender-evaluation-criteria/> [Accessed on 14th January

2017].

20

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.