Financial Analysis and Investment Recommendation Report (FINA6000)

VerifiedAdded on 2023/01/09

|10

|2016

|47

Report

AI Summary

This report analyzes the financial performance of two companies, Insurance Australia and DBS Group Holdings, focusing on profitability and investment ratios over a five-year period. It includes a comparative financial statement analysis, commentary on capital structure changes, and justifications for differences in capital structures. The report calculates the cost of equity, cost of debt, and weighted average cost of capital (WACC) for both companies. It also employs the Constant Growth Dividend Discount Valuation (DDM) model to value shares, discusses the appropriateness of this model, and ultimately recommends investment in DBS Group Holdings based on its superior performance in key financial metrics like earnings per share and return on equity, as well as its more stable capital structure. The conclusion emphasizes the importance of financial analysis in making sound investment decisions.

Managing finance

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

(a) Comparative financial statement analysis..............................................................................1

(b) Commentary on how the capital structure has changed over the 5 years..............................2

(c) Reasons justifying why there could be differences in the capital structures of the two

companies....................................................................................................................................3

(d) (i) Cost of equity....................................................................................................................3

(d) (ii) Cost of capital or debt......................................................................................................4

(e) Weighted average cost of capital...........................................................................................4

(f) Valuation of the shares using Constant Growth Dividend Discount Valuation model

(DDM).........................................................................................................................................5

(g) Discussing the appropriateness of using this model..............................................................5

(h) Recommendation for investments..........................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

(a) Comparative financial statement analysis..............................................................................1

(b) Commentary on how the capital structure has changed over the 5 years..............................2

(c) Reasons justifying why there could be differences in the capital structures of the two

companies....................................................................................................................................3

(d) (i) Cost of equity....................................................................................................................3

(d) (ii) Cost of capital or debt......................................................................................................4

(e) Weighted average cost of capital...........................................................................................4

(f) Valuation of the shares using Constant Growth Dividend Discount Valuation model

(DDM).........................................................................................................................................5

(g) Discussing the appropriateness of using this model..............................................................5

(h) Recommendation for investments..........................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

2

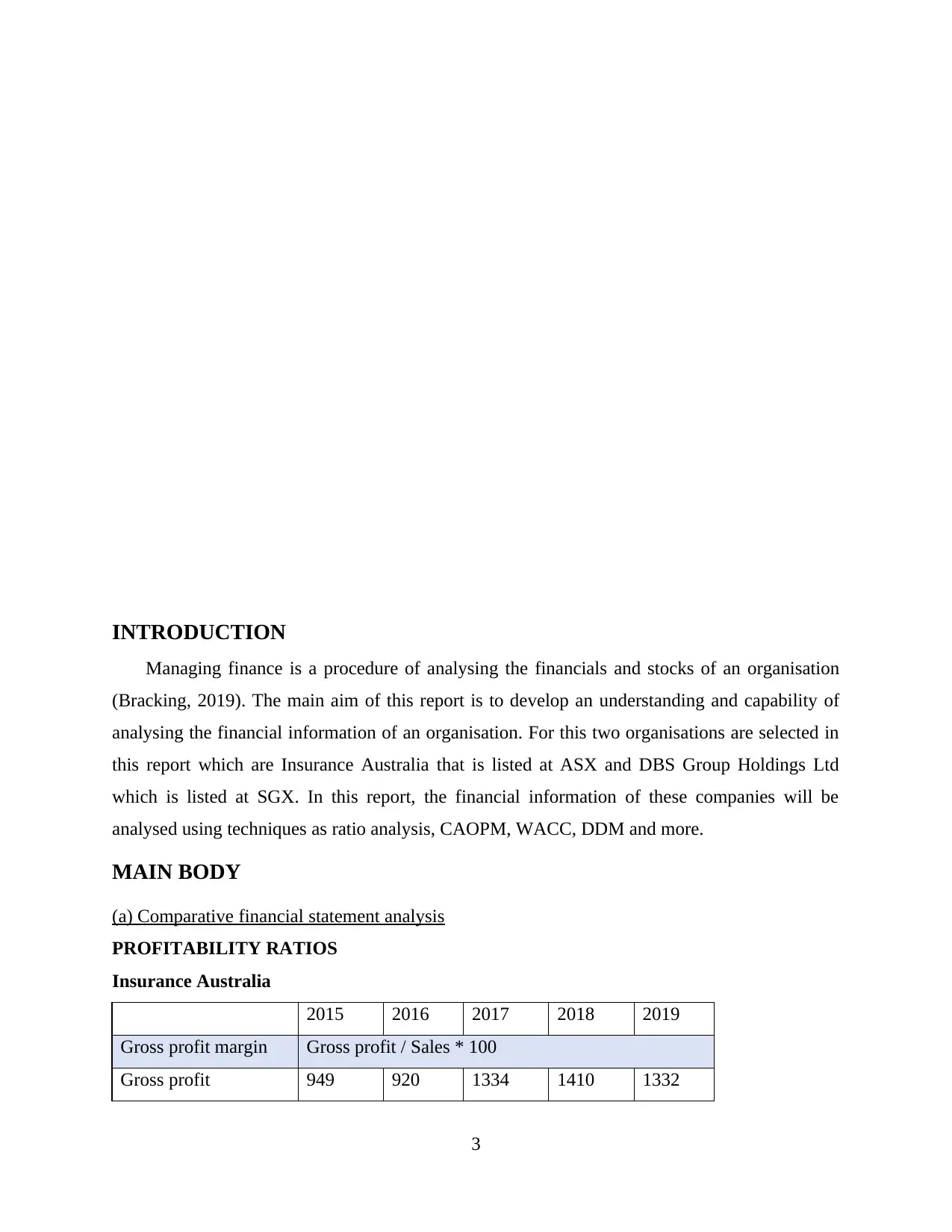

INTRODUCTION

Managing finance is a procedure of analysing the financials and stocks of an organisation

(Bracking, 2019). The main aim of this report is to develop an understanding and capability of

analysing the financial information of an organisation. For this two organisations are selected in

this report which are Insurance Australia that is listed at ASX and DBS Group Holdings Ltd

which is listed at SGX. In this report, the financial information of these companies will be

analysed using techniques as ratio analysis, CAOPM, WACC, DDM and more.

MAIN BODY

(a) Comparative financial statement analysis

PROFITABILITY RATIOS

Insurance Australia

2015 2016 2017 2018 2019

Gross profit margin Gross profit / Sales * 100

Gross profit 949 920 1334 1410 1332

3

Managing finance is a procedure of analysing the financials and stocks of an organisation

(Bracking, 2019). The main aim of this report is to develop an understanding and capability of

analysing the financial information of an organisation. For this two organisations are selected in

this report which are Insurance Australia that is listed at ASX and DBS Group Holdings Ltd

which is listed at SGX. In this report, the financial information of these companies will be

analysed using techniques as ratio analysis, CAOPM, WACC, DDM and more.

MAIN BODY

(a) Comparative financial statement analysis

PROFITABILITY RATIOS

Insurance Australia

2015 2016 2017 2018 2019

Gross profit margin Gross profit / Sales * 100

Gross profit 949 920 1334 1410 1332

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

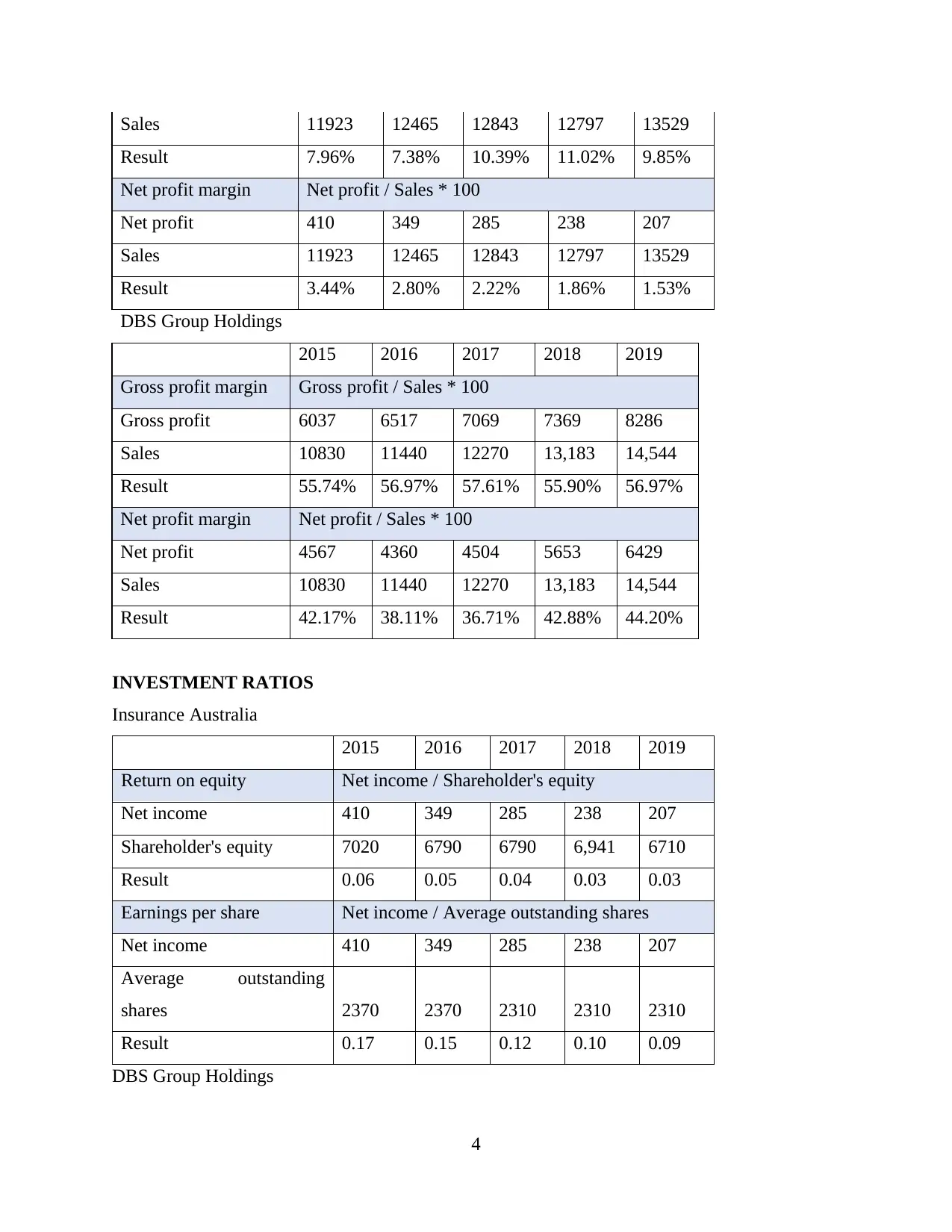

Sales 11923 12465 12843 12797 13529

Result 7.96% 7.38% 10.39% 11.02% 9.85%

Net profit margin Net profit / Sales * 100

Net profit 410 349 285 238 207

Sales 11923 12465 12843 12797 13529

Result 3.44% 2.80% 2.22% 1.86% 1.53%

DBS Group Holdings

2015 2016 2017 2018 2019

Gross profit margin Gross profit / Sales * 100

Gross profit 6037 6517 7069 7369 8286

Sales 10830 11440 12270 13,183 14,544

Result 55.74% 56.97% 57.61% 55.90% 56.97%

Net profit margin Net profit / Sales * 100

Net profit 4567 4360 4504 5653 6429

Sales 10830 11440 12270 13,183 14,544

Result 42.17% 38.11% 36.71% 42.88% 44.20%

INVESTMENT RATIOS

Insurance Australia

2015 2016 2017 2018 2019

Return on equity Net income / Shareholder's equity

Net income 410 349 285 238 207

Shareholder's equity 7020 6790 6790 6,941 6710

Result 0.06 0.05 0.04 0.03 0.03

Earnings per share Net income / Average outstanding shares

Net income 410 349 285 238 207

Average outstanding

shares 2370 2370 2310 2310 2310

Result 0.17 0.15 0.12 0.10 0.09

DBS Group Holdings

4

Result 7.96% 7.38% 10.39% 11.02% 9.85%

Net profit margin Net profit / Sales * 100

Net profit 410 349 285 238 207

Sales 11923 12465 12843 12797 13529

Result 3.44% 2.80% 2.22% 1.86% 1.53%

DBS Group Holdings

2015 2016 2017 2018 2019

Gross profit margin Gross profit / Sales * 100

Gross profit 6037 6517 7069 7369 8286

Sales 10830 11440 12270 13,183 14,544

Result 55.74% 56.97% 57.61% 55.90% 56.97%

Net profit margin Net profit / Sales * 100

Net profit 4567 4360 4504 5653 6429

Sales 10830 11440 12270 13,183 14,544

Result 42.17% 38.11% 36.71% 42.88% 44.20%

INVESTMENT RATIOS

Insurance Australia

2015 2016 2017 2018 2019

Return on equity Net income / Shareholder's equity

Net income 410 349 285 238 207

Shareholder's equity 7020 6790 6790 6,941 6710

Result 0.06 0.05 0.04 0.03 0.03

Earnings per share Net income / Average outstanding shares

Net income 410 349 285 238 207

Average outstanding

shares 2370 2370 2310 2310 2310

Result 0.17 0.15 0.12 0.10 0.09

DBS Group Holdings

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

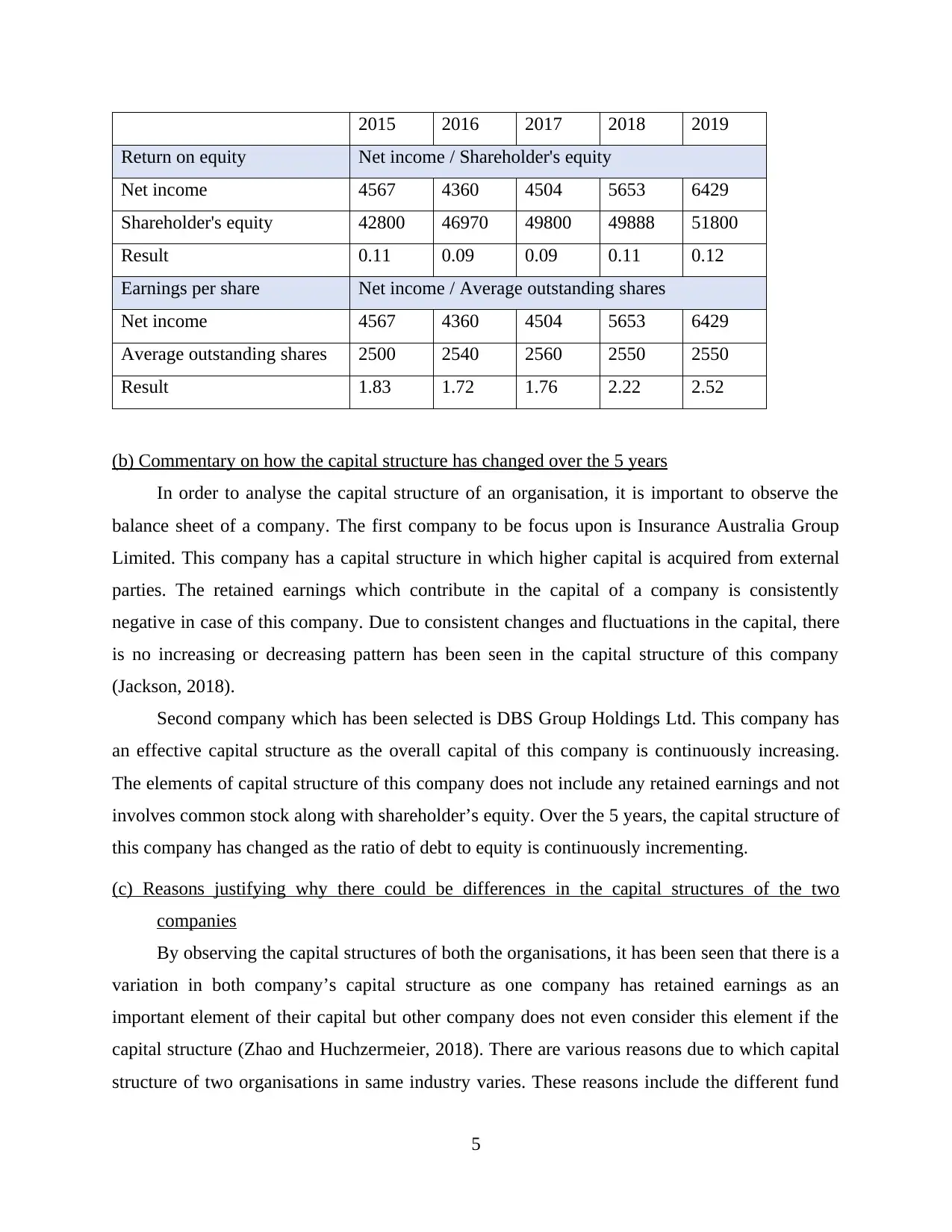

2015 2016 2017 2018 2019

Return on equity Net income / Shareholder's equity

Net income 4567 4360 4504 5653 6429

Shareholder's equity 42800 46970 49800 49888 51800

Result 0.11 0.09 0.09 0.11 0.12

Earnings per share Net income / Average outstanding shares

Net income 4567 4360 4504 5653 6429

Average outstanding shares 2500 2540 2560 2550 2550

Result 1.83 1.72 1.76 2.22 2.52

(b) Commentary on how the capital structure has changed over the 5 years

In order to analyse the capital structure of an organisation, it is important to observe the

balance sheet of a company. The first company to be focus upon is Insurance Australia Group

Limited. This company has a capital structure in which higher capital is acquired from external

parties. The retained earnings which contribute in the capital of a company is consistently

negative in case of this company. Due to consistent changes and fluctuations in the capital, there

is no increasing or decreasing pattern has been seen in the capital structure of this company

(Jackson, 2018).

Second company which has been selected is DBS Group Holdings Ltd. This company has

an effective capital structure as the overall capital of this company is continuously increasing.

The elements of capital structure of this company does not include any retained earnings and not

involves common stock along with shareholder’s equity. Over the 5 years, the capital structure of

this company has changed as the ratio of debt to equity is continuously incrementing.

(c) Reasons justifying why there could be differences in the capital structures of the two

companies

By observing the capital structures of both the organisations, it has been seen that there is a

variation in both company’s capital structure as one company has retained earnings as an

important element of their capital but other company does not even consider this element if the

capital structure (Zhao and Huchzermeier, 2018). There are various reasons due to which capital

structure of two organisations in same industry varies. These reasons include the different fund

5

Return on equity Net income / Shareholder's equity

Net income 4567 4360 4504 5653 6429

Shareholder's equity 42800 46970 49800 49888 51800

Result 0.11 0.09 0.09 0.11 0.12

Earnings per share Net income / Average outstanding shares

Net income 4567 4360 4504 5653 6429

Average outstanding shares 2500 2540 2560 2550 2550

Result 1.83 1.72 1.76 2.22 2.52

(b) Commentary on how the capital structure has changed over the 5 years

In order to analyse the capital structure of an organisation, it is important to observe the

balance sheet of a company. The first company to be focus upon is Insurance Australia Group

Limited. This company has a capital structure in which higher capital is acquired from external

parties. The retained earnings which contribute in the capital of a company is consistently

negative in case of this company. Due to consistent changes and fluctuations in the capital, there

is no increasing or decreasing pattern has been seen in the capital structure of this company

(Jackson, 2018).

Second company which has been selected is DBS Group Holdings Ltd. This company has

an effective capital structure as the overall capital of this company is continuously increasing.

The elements of capital structure of this company does not include any retained earnings and not

involves common stock along with shareholder’s equity. Over the 5 years, the capital structure of

this company has changed as the ratio of debt to equity is continuously incrementing.

(c) Reasons justifying why there could be differences in the capital structures of the two

companies

By observing the capital structures of both the organisations, it has been seen that there is a

variation in both company’s capital structure as one company has retained earnings as an

important element of their capital but other company does not even consider this element if the

capital structure (Zhao and Huchzermeier, 2018). There are various reasons due to which capital

structure of two organisations in same industry varies. These reasons include the different fund

5

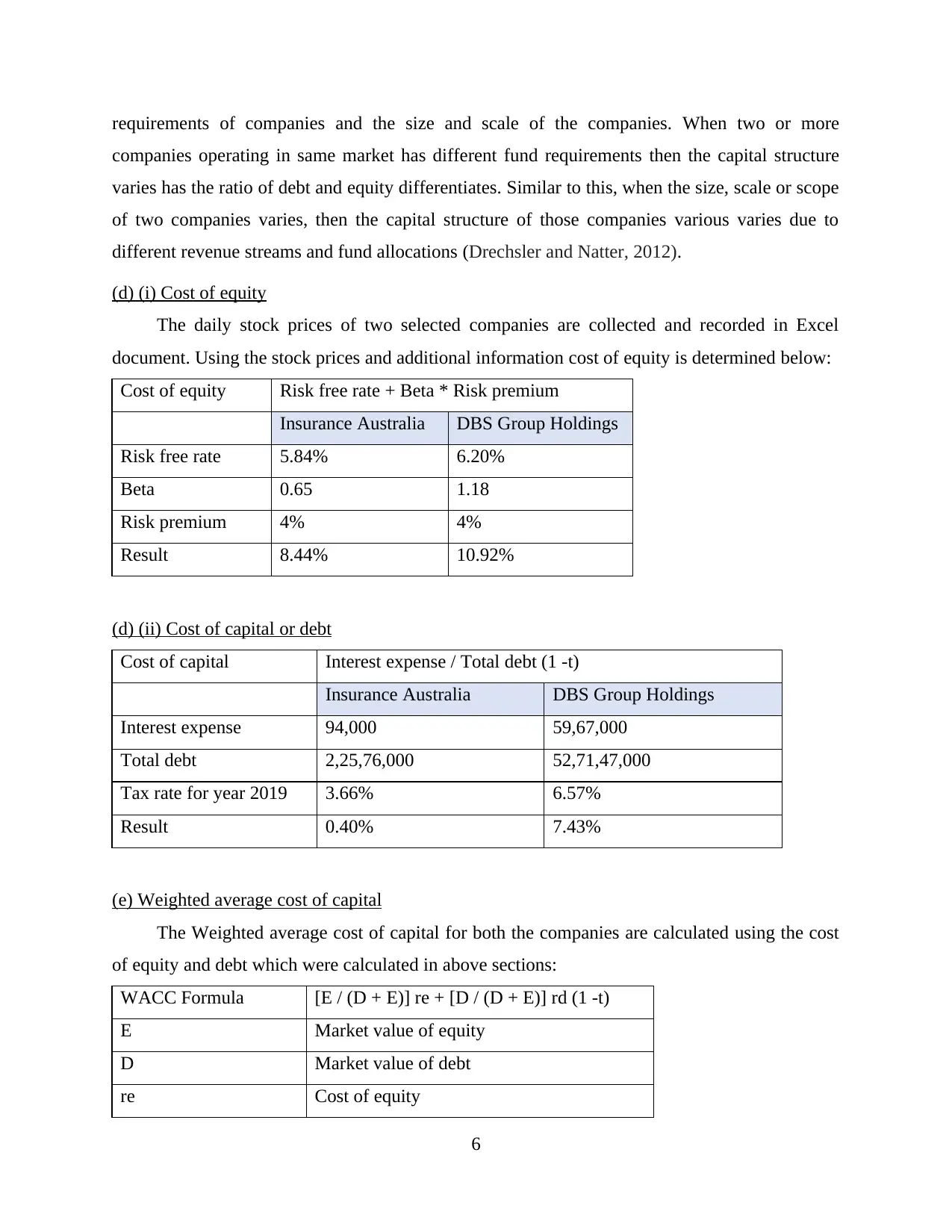

requirements of companies and the size and scale of the companies. When two or more

companies operating in same market has different fund requirements then the capital structure

varies has the ratio of debt and equity differentiates. Similar to this, when the size, scale or scope

of two companies varies, then the capital structure of those companies various varies due to

different revenue streams and fund allocations (Drechsler and Natter, 2012).

(d) (i) Cost of equity

The daily stock prices of two selected companies are collected and recorded in Excel

document. Using the stock prices and additional information cost of equity is determined below:

Cost of equity Risk free rate + Beta * Risk premium

Insurance Australia DBS Group Holdings

Risk free rate 5.84% 6.20%

Beta 0.65 1.18

Risk premium 4% 4%

Result 8.44% 10.92%

(d) (ii) Cost of capital or debt

Cost of capital Interest expense / Total debt (1 -t)

Insurance Australia DBS Group Holdings

Interest expense 94,000 59,67,000

Total debt 2,25,76,000 52,71,47,000

Tax rate for year 2019 3.66% 6.57%

Result 0.40% 7.43%

(e) Weighted average cost of capital

The Weighted average cost of capital for both the companies are calculated using the cost

of equity and debt which were calculated in above sections:

WACC Formula [E / (D + E)] re + [D / (D + E)] rd (1 -t)

E Market value of equity

D Market value of debt

re Cost of equity

6

companies operating in same market has different fund requirements then the capital structure

varies has the ratio of debt and equity differentiates. Similar to this, when the size, scale or scope

of two companies varies, then the capital structure of those companies various varies due to

different revenue streams and fund allocations (Drechsler and Natter, 2012).

(d) (i) Cost of equity

The daily stock prices of two selected companies are collected and recorded in Excel

document. Using the stock prices and additional information cost of equity is determined below:

Cost of equity Risk free rate + Beta * Risk premium

Insurance Australia DBS Group Holdings

Risk free rate 5.84% 6.20%

Beta 0.65 1.18

Risk premium 4% 4%

Result 8.44% 10.92%

(d) (ii) Cost of capital or debt

Cost of capital Interest expense / Total debt (1 -t)

Insurance Australia DBS Group Holdings

Interest expense 94,000 59,67,000

Total debt 2,25,76,000 52,71,47,000

Tax rate for year 2019 3.66% 6.57%

Result 0.40% 7.43%

(e) Weighted average cost of capital

The Weighted average cost of capital for both the companies are calculated using the cost

of equity and debt which were calculated in above sections:

WACC Formula [E / (D + E)] re + [D / (D + E)] rd (1 -t)

E Market value of equity

D Market value of debt

re Cost of equity

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

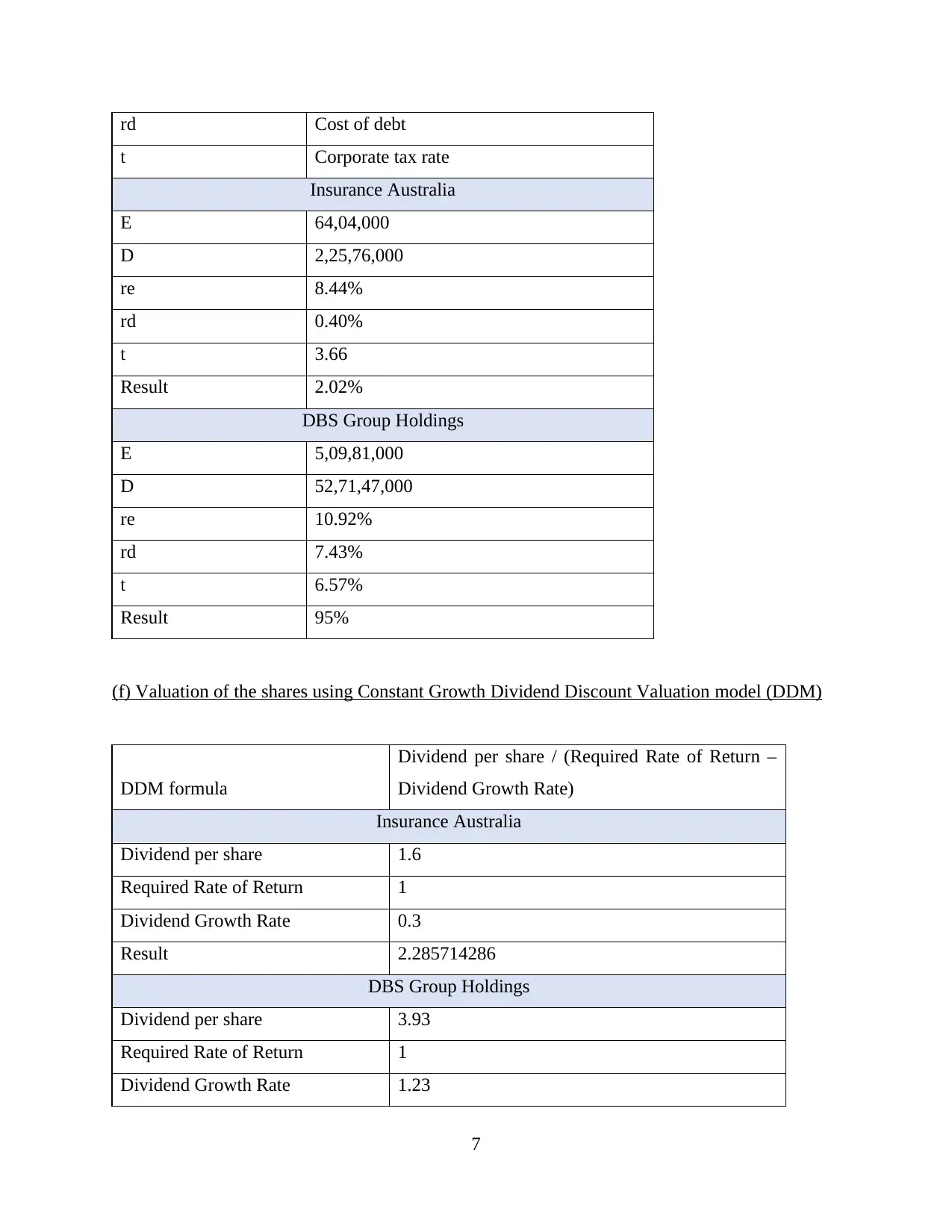

rd Cost of debt

t Corporate tax rate

Insurance Australia

E 64,04,000

D 2,25,76,000

re 8.44%

rd 0.40%

t 3.66

Result 2.02%

DBS Group Holdings

E 5,09,81,000

D 52,71,47,000

re 10.92%

rd 7.43%

t 6.57%

Result 95%

(f) Valuation of the shares using Constant Growth Dividend Discount Valuation model (DDM)

DDM formula

Dividend per share / (Required Rate of Return –

Dividend Growth Rate)

Insurance Australia

Dividend per share 1.6

Required Rate of Return 1

Dividend Growth Rate 0.3

Result 2.285714286

DBS Group Holdings

Dividend per share 3.93

Required Rate of Return 1

Dividend Growth Rate 1.23

7

t Corporate tax rate

Insurance Australia

E 64,04,000

D 2,25,76,000

re 8.44%

rd 0.40%

t 3.66

Result 2.02%

DBS Group Holdings

E 5,09,81,000

D 52,71,47,000

re 10.92%

rd 7.43%

t 6.57%

Result 95%

(f) Valuation of the shares using Constant Growth Dividend Discount Valuation model (DDM)

DDM formula

Dividend per share / (Required Rate of Return –

Dividend Growth Rate)

Insurance Australia

Dividend per share 1.6

Required Rate of Return 1

Dividend Growth Rate 0.3

Result 2.285714286

DBS Group Holdings

Dividend per share 3.93

Required Rate of Return 1

Dividend Growth Rate 1.23

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Result -17.08695652

(g) Discussing the appropriateness of using this model

Constant Growth Dividend Discount Valuation model is often considered as Dividend

discount model. This model is appropriate for the valuation of two selected companies as this

model is highly suitable for mature organisations which are stable in nature and are at the stage

where they can afford to pay dividend to their shareholders (Massingham, 2014). There are some

organisations which are difficult to value such as banks and financial institutions. This model of

dividend discount is appropriate for such organisation and as both the organisations selected are

a part of finance and insurance industry, it can be said that this model is appropriate for both the

companies.

Besides DDM, there are few others models as well that can be used by an organisation to

value their stocks; such models or methods include FCFE. This model of FCFE is considered as

appropriate for large business organisations which has a stable capital structure and as the capital

structure of both the organisations is already analysed in above sections, it can be said that DDM

is more effective model of valuation than FCFE for both the organisations as not only these

organisations pay dividend or operate in finance industry, both of these organisations experience

fluctuations and yearly variations in their capital structure (Maskell, Baggaley and Grasso,

2016).

(h) Recommendation for investments

All other above quantitative and qualitative analysis which are conducted above has helped

in developing a familiarity with both the organisations stock valuations (Malmström, Wincent

and Johansson, 2013). Considering all the observations, it is considered suitable to recommend to

invest in DBS Group Holdings. There are various reasons which can justify this

recommendation; these reasons are:

The investment amount of 15 million dollars is a large amount which must not be invested

by taking a huge risk due to which it is viable to invest in an organisation which is constantly

providing positive and generous return un per share.

Earnings per share and return on equity are two investment ratios which were calculated for

both the organisations. These ratios clearly reflect that the investment performance of DBS

Group Holdings is better than Insurance Australia Group.

8

(g) Discussing the appropriateness of using this model

Constant Growth Dividend Discount Valuation model is often considered as Dividend

discount model. This model is appropriate for the valuation of two selected companies as this

model is highly suitable for mature organisations which are stable in nature and are at the stage

where they can afford to pay dividend to their shareholders (Massingham, 2014). There are some

organisations which are difficult to value such as banks and financial institutions. This model of

dividend discount is appropriate for such organisation and as both the organisations selected are

a part of finance and insurance industry, it can be said that this model is appropriate for both the

companies.

Besides DDM, there are few others models as well that can be used by an organisation to

value their stocks; such models or methods include FCFE. This model of FCFE is considered as

appropriate for large business organisations which has a stable capital structure and as the capital

structure of both the organisations is already analysed in above sections, it can be said that DDM

is more effective model of valuation than FCFE for both the organisations as not only these

organisations pay dividend or operate in finance industry, both of these organisations experience

fluctuations and yearly variations in their capital structure (Maskell, Baggaley and Grasso,

2016).

(h) Recommendation for investments

All other above quantitative and qualitative analysis which are conducted above has helped

in developing a familiarity with both the organisations stock valuations (Malmström, Wincent

and Johansson, 2013). Considering all the observations, it is considered suitable to recommend to

invest in DBS Group Holdings. There are various reasons which can justify this

recommendation; these reasons are:

The investment amount of 15 million dollars is a large amount which must not be invested

by taking a huge risk due to which it is viable to invest in an organisation which is constantly

providing positive and generous return un per share.

Earnings per share and return on equity are two investment ratios which were calculated for

both the organisations. These ratios clearly reflect that the investment performance of DBS

Group Holdings is better than Insurance Australia Group.

8

Another reason that can justify the recommendation is the high beta value and risk premium

rate of DBS Group Holdings which implies that with increasing risk on the investment, the

chances of earning high earnings by the investors will also increase.

Another reason for justification is the capital structure of DBS Group Holdings. The capital

structure of this company is observed to be more stable than Insurance Australia Group as even

after having an increasing capital in every year, the capital is increasing with an enhancing and

stable rate.

CONCLUSION

From the above report, it has been concluded that the concept of managing finance does not

only helps in analysing the financial statements of an organisation but also helps in analysing the

stock process of an organisation in order to make an effective investment decision. It has also

concluded that DBS Group Holdings is a better choice for investment.

9

rate of DBS Group Holdings which implies that with increasing risk on the investment, the

chances of earning high earnings by the investors will also increase.

Another reason for justification is the capital structure of DBS Group Holdings. The capital

structure of this company is observed to be more stable than Insurance Australia Group as even

after having an increasing capital in every year, the capital is increasing with an enhancing and

stable rate.

CONCLUSION

From the above report, it has been concluded that the concept of managing finance does not

only helps in analysing the financial statements of an organisation but also helps in analysing the

stock process of an organisation in order to make an effective investment decision. It has also

concluded that DBS Group Holdings is a better choice for investment.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Bracking, S., 2019. Financialisation, climate finance, and the calculative challenges of managing

environmental change. Antipode, 51(3), pp.709-729.

Drechsler, W. and Natter, M., 2012. Understanding a firm's openness decisions in innovation.

Journal of business research. 65(3). pp.438-445.

Jackson, D., 2018. Accounting and finance graduate employment outcomes: Underemployment,

self‐employment and managing diversity. Australian Accounting Review.

Malmström, M., Wincent, J. and Johansson, J., 2013. Managing competence acquisition and

financial performance: An empirical study of how small firms use competence

acquisition strategies. Journal of engineering and technology management. 30(4).

pp.327-349.

Maskell, B. H., Baggaley, B. and Grasso, L., 2016. Practical lean accounting: a proven system

for measuring and managing the lean enterprise. Productivity Press.

Massingham, P., 2014. An evaluation of knowledge management tools: Part 1–managing

knowledge resources. Journal of Knowledge Management. 18(6). pp.1075-1100.

Zhao, L. and Huchzermeier, A., 2018. Managing Supplier Financial Risk with Pre-shipment

Finance Instruments. In Supply Chain Finance (pp. 121-142). Springer, Cham.

10

Books and Journals

Bracking, S., 2019. Financialisation, climate finance, and the calculative challenges of managing

environmental change. Antipode, 51(3), pp.709-729.

Drechsler, W. and Natter, M., 2012. Understanding a firm's openness decisions in innovation.

Journal of business research. 65(3). pp.438-445.

Jackson, D., 2018. Accounting and finance graduate employment outcomes: Underemployment,

self‐employment and managing diversity. Australian Accounting Review.

Malmström, M., Wincent, J. and Johansson, J., 2013. Managing competence acquisition and

financial performance: An empirical study of how small firms use competence

acquisition strategies. Journal of engineering and technology management. 30(4).

pp.327-349.

Maskell, B. H., Baggaley, B. and Grasso, L., 2016. Practical lean accounting: a proven system

for measuring and managing the lean enterprise. Productivity Press.

Massingham, P., 2014. An evaluation of knowledge management tools: Part 1–managing

knowledge resources. Journal of Knowledge Management. 18(6). pp.1075-1100.

Zhao, L. and Huchzermeier, A., 2018. Managing Supplier Financial Risk with Pre-shipment

Finance Instruments. In Supply Chain Finance (pp. 121-142). Springer, Cham.

10

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.