Analysis of Financial Resources: Costing, Budgeting & Forecasting

VerifiedAdded on 2023/06/15

|12

|2555

|488

Report

AI Summary

This report provides a detailed analysis of managing financial resources, covering essential aspects such as prime cost, production cost, sales and distribution cost, and total cost calculation. It explores budgeting and forecasting techniques, including variance analysis, flexible budgets, and static budgets. The report also delves into direct labor variances and key performance indicators for the hospitality industry, such as Average Daily Rate (ADR), Revenue per Available Room (RevPAR), Average Rate Index (ARI), and Market Penetration Index (MPI). Additionally, it discusses the importance of customer satisfaction and its measurement. This comprehensive analysis offers valuable insights into financial management practices and performance evaluation.

Managing Financial

Resources

Resources

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

MAIN BODY...................................................................................................................................3

SECTION A.....................................................................................................................................3

Question 1....................................................................................................................................3

SECTION B.....................................................................................................................................5

Question 4....................................................................................................................................5

Question 5....................................................................................................................................8

REFERENCES..............................................................................................................................11

MAIN BODY...................................................................................................................................3

SECTION A.....................................................................................................................................3

Question 1....................................................................................................................................3

SECTION B.....................................................................................................................................5

Question 4....................................................................................................................................5

Question 5....................................................................................................................................8

REFERENCES..............................................................................................................................11

MAIN BODY

SECTION A

Question 1

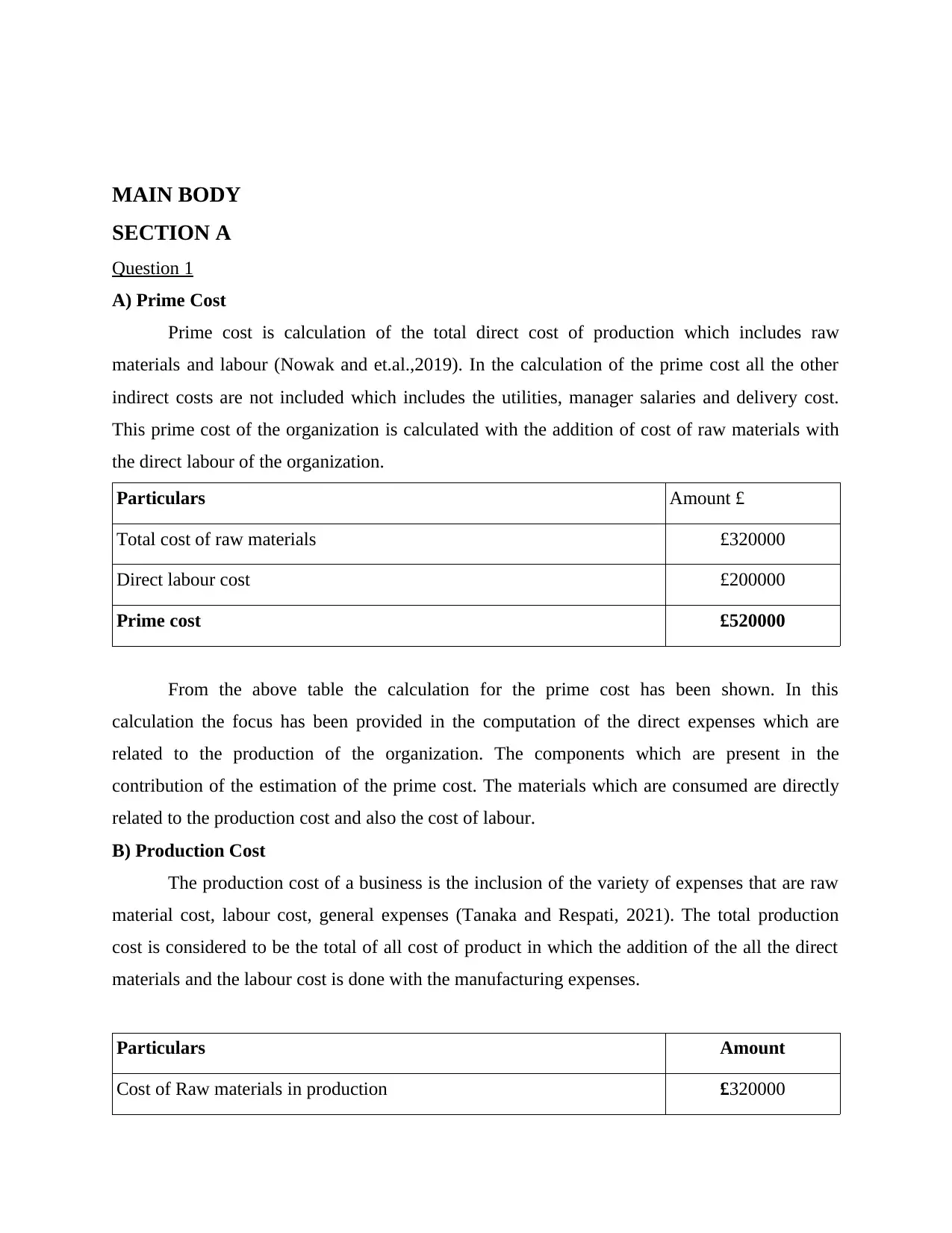

A) Prime Cost

Prime cost is calculation of the total direct cost of production which includes raw

materials and labour (Nowak and et.al.,2019). In the calculation of the prime cost all the other

indirect costs are not included which includes the utilities, manager salaries and delivery cost.

This prime cost of the organization is calculated with the addition of cost of raw materials with

the direct labour of the organization.

Particulars Amount £

Total cost of raw materials £320000

Direct labour cost £200000

Prime cost £520000

From the above table the calculation for the prime cost has been shown. In this

calculation the focus has been provided in the computation of the direct expenses which are

related to the production of the organization. The components which are present in the

contribution of the estimation of the prime cost. The materials which are consumed are directly

related to the production cost and also the cost of labour.

B) Production Cost

The production cost of a business is the inclusion of the variety of expenses that are raw

material cost, labour cost, general expenses (Tanaka and Respati, 2021). The total production

cost is considered to be the total of all cost of product in which the addition of the all the direct

materials and the labour cost is done with the manufacturing expenses.

Particulars Amount

Cost of Raw materials in production £320000

SECTION A

Question 1

A) Prime Cost

Prime cost is calculation of the total direct cost of production which includes raw

materials and labour (Nowak and et.al.,2019). In the calculation of the prime cost all the other

indirect costs are not included which includes the utilities, manager salaries and delivery cost.

This prime cost of the organization is calculated with the addition of cost of raw materials with

the direct labour of the organization.

Particulars Amount £

Total cost of raw materials £320000

Direct labour cost £200000

Prime cost £520000

From the above table the calculation for the prime cost has been shown. In this

calculation the focus has been provided in the computation of the direct expenses which are

related to the production of the organization. The components which are present in the

contribution of the estimation of the prime cost. The materials which are consumed are directly

related to the production cost and also the cost of labour.

B) Production Cost

The production cost of a business is the inclusion of the variety of expenses that are raw

material cost, labour cost, general expenses (Tanaka and Respati, 2021). The total production

cost is considered to be the total of all cost of product in which the addition of the all the direct

materials and the labour cost is done with the manufacturing expenses.

Particulars Amount

Cost of Raw materials in production £320000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

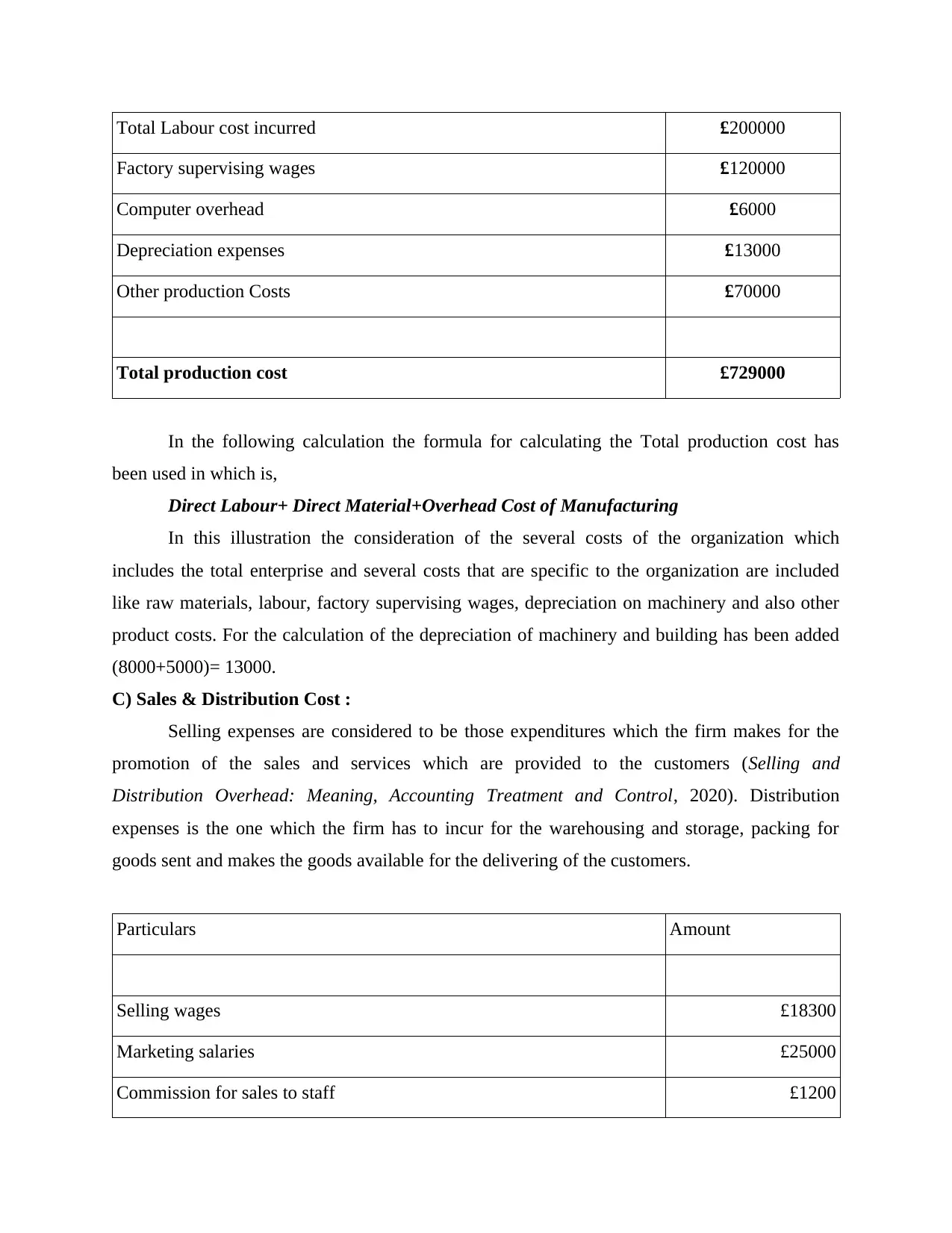

Total Labour cost incurred £200000

Factory supervising wages £120000

Computer overhead £6000

Depreciation expenses £13000

Other production Costs £70000

Total production cost £729000

In the following calculation the formula for calculating the Total production cost has

been used in which is,

Direct Labour+ Direct Material+Overhead Cost of Manufacturing

In this illustration the consideration of the several costs of the organization which

includes the total enterprise and several costs that are specific to the organization are included

like raw materials, labour, factory supervising wages, depreciation on machinery and also other

product costs. For the calculation of the depreciation of machinery and building has been added

(8000+5000)= 13000.

C) Sales & Distribution Cost :

Selling expenses are considered to be those expenditures which the firm makes for the

promotion of the sales and services which are provided to the customers (Selling and

Distribution Overhead: Meaning, Accounting Treatment and Control, 2020). Distribution

expenses is the one which the firm has to incur for the warehousing and storage, packing for

goods sent and makes the goods available for the delivering of the customers.

Particulars Amount

Selling wages £18300

Marketing salaries £25000

Commission for sales to staff £1200

Factory supervising wages £120000

Computer overhead £6000

Depreciation expenses £13000

Other production Costs £70000

Total production cost £729000

In the following calculation the formula for calculating the Total production cost has

been used in which is,

Direct Labour+ Direct Material+Overhead Cost of Manufacturing

In this illustration the consideration of the several costs of the organization which

includes the total enterprise and several costs that are specific to the organization are included

like raw materials, labour, factory supervising wages, depreciation on machinery and also other

product costs. For the calculation of the depreciation of machinery and building has been added

(8000+5000)= 13000.

C) Sales & Distribution Cost :

Selling expenses are considered to be those expenditures which the firm makes for the

promotion of the sales and services which are provided to the customers (Selling and

Distribution Overhead: Meaning, Accounting Treatment and Control, 2020). Distribution

expenses is the one which the firm has to incur for the warehousing and storage, packing for

goods sent and makes the goods available for the delivering of the customers.

Particulars Amount

Selling wages £18300

Marketing salaries £25000

Commission for sales to staff £1200

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

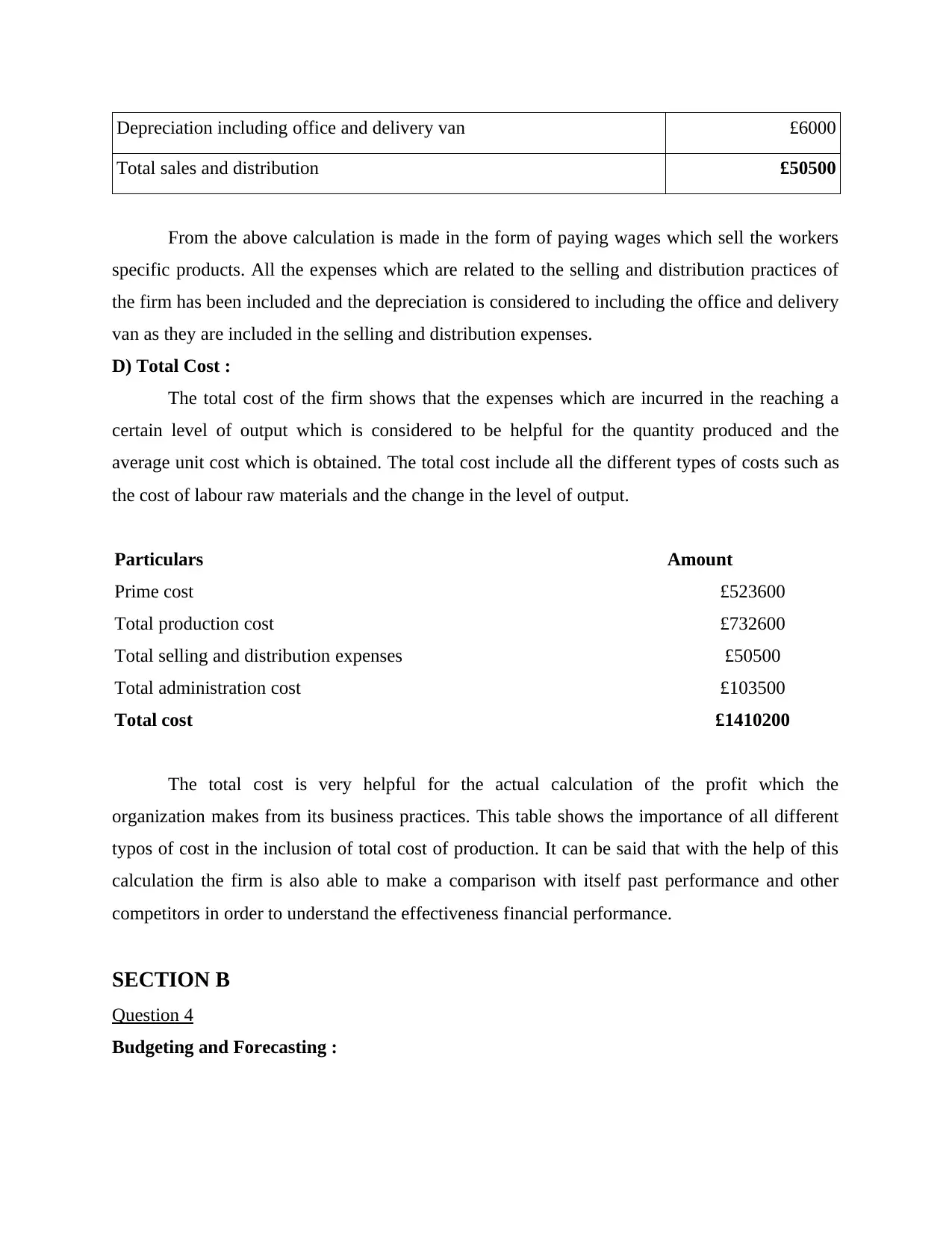

Depreciation including office and delivery van £6000

Total sales and distribution £50500

From the above calculation is made in the form of paying wages which sell the workers

specific products. All the expenses which are related to the selling and distribution practices of

the firm has been included and the depreciation is considered to including the office and delivery

van as they are included in the selling and distribution expenses.

D) Total Cost :

The total cost of the firm shows that the expenses which are incurred in the reaching a

certain level of output which is considered to be helpful for the quantity produced and the

average unit cost which is obtained. The total cost include all the different types of costs such as

the cost of labour raw materials and the change in the level of output.

Particulars Amount

Prime cost £523600

Total production cost £732600

Total selling and distribution expenses £50500

Total administration cost £103500

Total cost £1410200

The total cost is very helpful for the actual calculation of the profit which the

organization makes from its business practices. This table shows the importance of all different

typos of cost in the inclusion of total cost of production. It can be said that with the help of this

calculation the firm is also able to make a comparison with itself past performance and other

competitors in order to understand the effectiveness financial performance.

SECTION B

Question 4

Budgeting and Forecasting :

Total sales and distribution £50500

From the above calculation is made in the form of paying wages which sell the workers

specific products. All the expenses which are related to the selling and distribution practices of

the firm has been included and the depreciation is considered to including the office and delivery

van as they are included in the selling and distribution expenses.

D) Total Cost :

The total cost of the firm shows that the expenses which are incurred in the reaching a

certain level of output which is considered to be helpful for the quantity produced and the

average unit cost which is obtained. The total cost include all the different types of costs such as

the cost of labour raw materials and the change in the level of output.

Particulars Amount

Prime cost £523600

Total production cost £732600

Total selling and distribution expenses £50500

Total administration cost £103500

Total cost £1410200

The total cost is very helpful for the actual calculation of the profit which the

organization makes from its business practices. This table shows the importance of all different

typos of cost in the inclusion of total cost of production. It can be said that with the help of this

calculation the firm is also able to make a comparison with itself past performance and other

competitors in order to understand the effectiveness financial performance.

SECTION B

Question 4

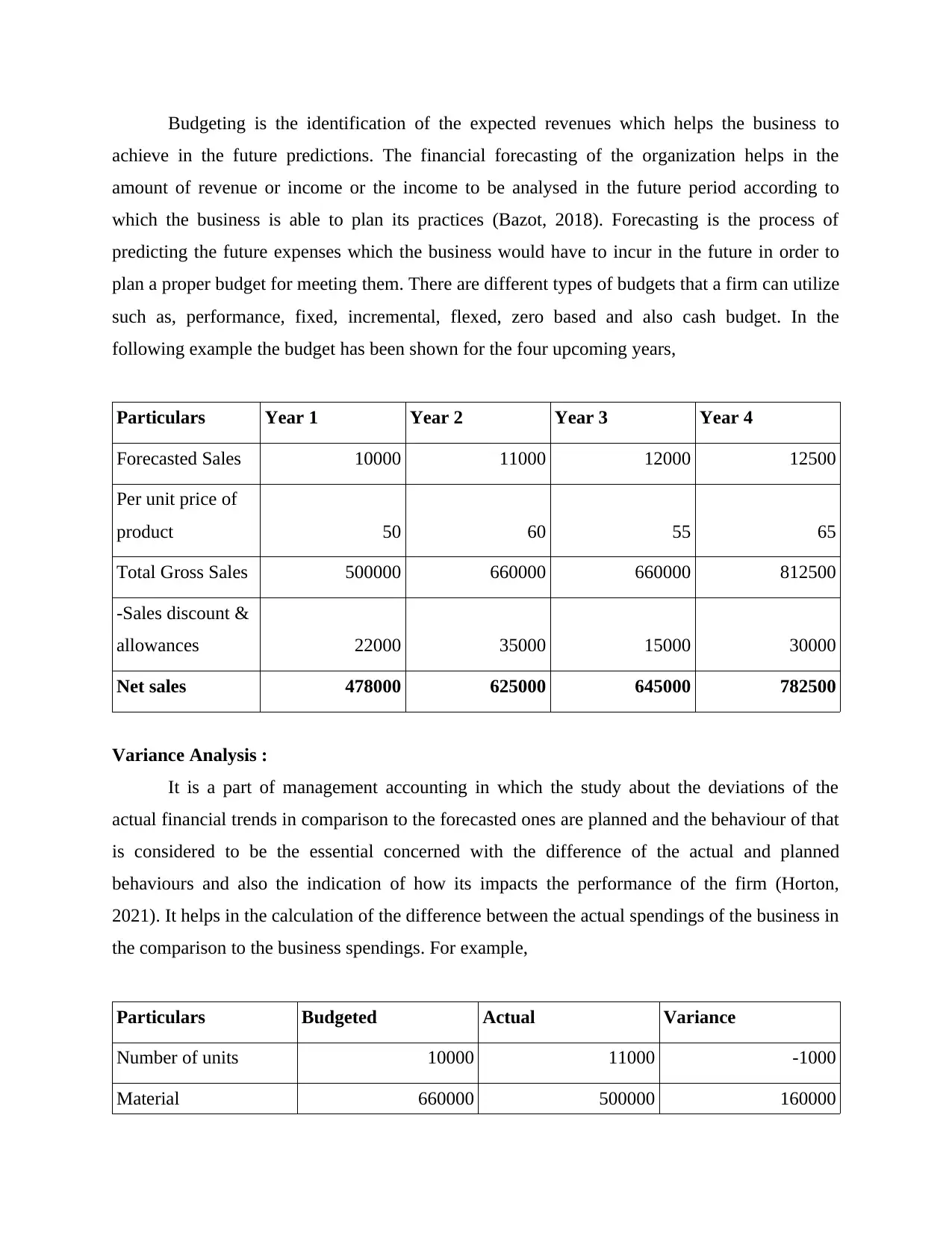

Budgeting and Forecasting :

Budgeting is the identification of the expected revenues which helps the business to

achieve in the future predictions. The financial forecasting of the organization helps in the

amount of revenue or income or the income to be analysed in the future period according to

which the business is able to plan its practices (Bazot, 2018). Forecasting is the process of

predicting the future expenses which the business would have to incur in the future in order to

plan a proper budget for meeting them. There are different types of budgets that a firm can utilize

such as, performance, fixed, incremental, flexed, zero based and also cash budget. In the

following example the budget has been shown for the four upcoming years,

Particulars Year 1 Year 2 Year 3 Year 4

Forecasted Sales 10000 11000 12000 12500

Per unit price of

product 50 60 55 65

Total Gross Sales 500000 660000 660000 812500

-Sales discount &

allowances 22000 35000 15000 30000

Net sales 478000 625000 645000 782500

Variance Analysis :

It is a part of management accounting in which the study about the deviations of the

actual financial trends in comparison to the forecasted ones are planned and the behaviour of that

is considered to be the essential concerned with the difference of the actual and planned

behaviours and also the indication of how its impacts the performance of the firm (Horton,

2021). It helps in the calculation of the difference between the actual spendings of the business in

the comparison to the business spendings. For example,

Particulars Budgeted Actual Variance

Number of units 10000 11000 -1000

Material 660000 500000 160000

achieve in the future predictions. The financial forecasting of the organization helps in the

amount of revenue or income or the income to be analysed in the future period according to

which the business is able to plan its practices (Bazot, 2018). Forecasting is the process of

predicting the future expenses which the business would have to incur in the future in order to

plan a proper budget for meeting them. There are different types of budgets that a firm can utilize

such as, performance, fixed, incremental, flexed, zero based and also cash budget. In the

following example the budget has been shown for the four upcoming years,

Particulars Year 1 Year 2 Year 3 Year 4

Forecasted Sales 10000 11000 12000 12500

Per unit price of

product 50 60 55 65

Total Gross Sales 500000 660000 660000 812500

-Sales discount &

allowances 22000 35000 15000 30000

Net sales 478000 625000 645000 782500

Variance Analysis :

It is a part of management accounting in which the study about the deviations of the

actual financial trends in comparison to the forecasted ones are planned and the behaviour of that

is considered to be the essential concerned with the difference of the actual and planned

behaviours and also the indication of how its impacts the performance of the firm (Horton,

2021). It helps in the calculation of the difference between the actual spendings of the business in

the comparison to the business spendings. For example,

Particulars Budgeted Actual Variance

Number of units 10000 11000 -1000

Material 660000 500000 160000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

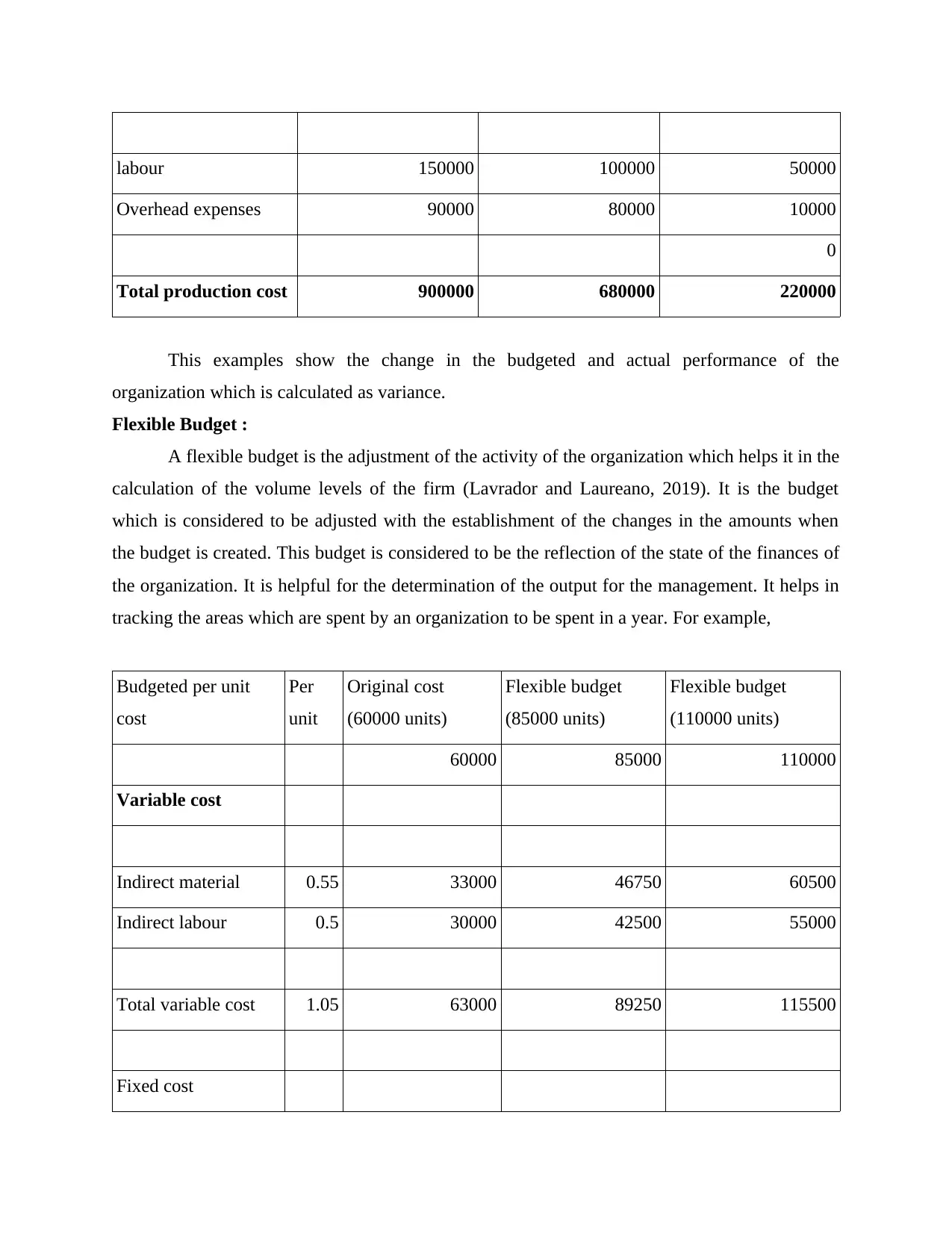

labour 150000 100000 50000

Overhead expenses 90000 80000 10000

0

Total production cost 900000 680000 220000

This examples show the change in the budgeted and actual performance of the

organization which is calculated as variance.

Flexible Budget :

A flexible budget is the adjustment of the activity of the organization which helps it in the

calculation of the volume levels of the firm (Lavrador and Laureano, 2019). It is the budget

which is considered to be adjusted with the establishment of the changes in the amounts when

the budget is created. This budget is considered to be the reflection of the state of the finances of

the organization. It is helpful for the determination of the output for the management. It helps in

tracking the areas which are spent by an organization to be spent in a year. For example,

Budgeted per unit

cost

Per

unit

Original cost

(60000 units)

Flexible budget

(85000 units)

Flexible budget

(110000 units)

60000 85000 110000

Variable cost

Indirect material 0.55 33000 46750 60500

Indirect labour 0.5 30000 42500 55000

Total variable cost 1.05 63000 89250 115500

Fixed cost

Overhead expenses 90000 80000 10000

0

Total production cost 900000 680000 220000

This examples show the change in the budgeted and actual performance of the

organization which is calculated as variance.

Flexible Budget :

A flexible budget is the adjustment of the activity of the organization which helps it in the

calculation of the volume levels of the firm (Lavrador and Laureano, 2019). It is the budget

which is considered to be adjusted with the establishment of the changes in the amounts when

the budget is created. This budget is considered to be the reflection of the state of the finances of

the organization. It is helpful for the determination of the output for the management. It helps in

tracking the areas which are spent by an organization to be spent in a year. For example,

Budgeted per unit

cost

Per

unit

Original cost

(60000 units)

Flexible budget

(85000 units)

Flexible budget

(110000 units)

60000 85000 110000

Variable cost

Indirect material 0.55 33000 46750 60500

Indirect labour 0.5 30000 42500 55000

Total variable cost 1.05 63000 89250 115500

Fixed cost

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

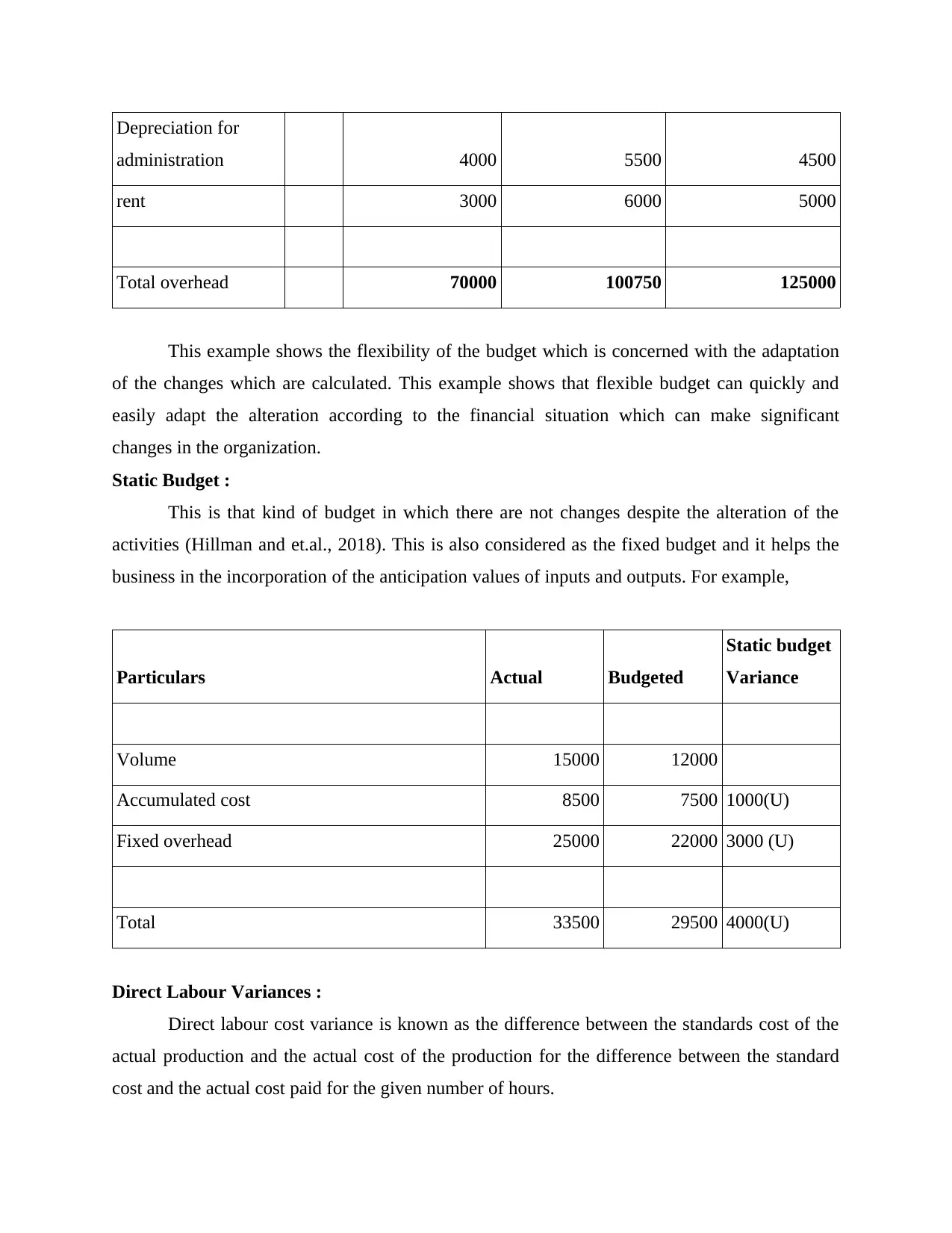

Depreciation for

administration 4000 5500 4500

rent 3000 6000 5000

Total overhead 70000 100750 125000

This example shows the flexibility of the budget which is concerned with the adaptation

of the changes which are calculated. This example shows that flexible budget can quickly and

easily adapt the alteration according to the financial situation which can make significant

changes in the organization.

Static Budget :

This is that kind of budget in which there are not changes despite the alteration of the

activities (Hillman and et.al., 2018). This is also considered as the fixed budget and it helps the

business in the incorporation of the anticipation values of inputs and outputs. For example,

Particulars Actual Budgeted

Static budget

Variance

Volume 15000 12000

Accumulated cost 8500 7500 1000(U)

Fixed overhead 25000 22000 3000 (U)

Total 33500 29500 4000(U)

Direct Labour Variances :

Direct labour cost variance is known as the difference between the standards cost of the

actual production and the actual cost of the production for the difference between the standard

cost and the actual cost paid for the given number of hours.

administration 4000 5500 4500

rent 3000 6000 5000

Total overhead 70000 100750 125000

This example shows the flexibility of the budget which is concerned with the adaptation

of the changes which are calculated. This example shows that flexible budget can quickly and

easily adapt the alteration according to the financial situation which can make significant

changes in the organization.

Static Budget :

This is that kind of budget in which there are not changes despite the alteration of the

activities (Hillman and et.al., 2018). This is also considered as the fixed budget and it helps the

business in the incorporation of the anticipation values of inputs and outputs. For example,

Particulars Actual Budgeted

Static budget

Variance

Volume 15000 12000

Accumulated cost 8500 7500 1000(U)

Fixed overhead 25000 22000 3000 (U)

Total 33500 29500 4000(U)

Direct Labour Variances :

Direct labour cost variance is known as the difference between the standards cost of the

actual production and the actual cost of the production for the difference between the standard

cost and the actual cost paid for the given number of hours.

The calculation of the direct labour time variance is done with the help of the following formula,

= Actual hour worked * Standard rate per hour - Standard hour* standard rate per hour

= 7*11 – 9*7

=77-63

= 14

Question 5

Average Daily Rate :

Average Daily Rate measures the average rental revenue earned for the occupation of the

room per day. This is considered to be the operations which impacts the performance of the hotel

in the lodging business which can be determined by the use of ADR, multiplication of ADR with

the occupancy rate is helpful for the calculation of the revenue per room. The formula for the

calculation of the Average Daily Rate is,

ADR = Rooms Revenue Earned/Number of Rooms Sold

For example there is a hotel with a room revenue of £80000 and the total of 500 rooms

sold is the total ADR for the Hospitality organization is 80000/500 = 160

Revenue per available room(RevPAR) :

This is the tool which is used by hospitality organization for the calculation of the

performance measurement in the hospitality industry (Xuyun, Yan and Xiaotian, 2020). The

calculation of the hotel's average is also known to be applicable in its occupancy rate. This is

considered to be calculated through the division of the total room revenue and also from the total

number of rooms which are available in the given time period. For example the total number of

rooms which are there in a hotel are, 250 for which the occupancy rate is give at 95%. Average

cost which is incurred by the hotel for a single room is £800 therefore this helps in the

calculation of RevPAR = per night cost multiplied by occupancy rate.

= (800*95%)

= £760.00

This calculation of the revenue of the per available room assumes that all the rooms have

same price.

Average Rate Index :

= Actual hour worked * Standard rate per hour - Standard hour* standard rate per hour

= 7*11 – 9*7

=77-63

= 14

Question 5

Average Daily Rate :

Average Daily Rate measures the average rental revenue earned for the occupation of the

room per day. This is considered to be the operations which impacts the performance of the hotel

in the lodging business which can be determined by the use of ADR, multiplication of ADR with

the occupancy rate is helpful for the calculation of the revenue per room. The formula for the

calculation of the Average Daily Rate is,

ADR = Rooms Revenue Earned/Number of Rooms Sold

For example there is a hotel with a room revenue of £80000 and the total of 500 rooms

sold is the total ADR for the Hospitality organization is 80000/500 = 160

Revenue per available room(RevPAR) :

This is the tool which is used by hospitality organization for the calculation of the

performance measurement in the hospitality industry (Xuyun, Yan and Xiaotian, 2020). The

calculation of the hotel's average is also known to be applicable in its occupancy rate. This is

considered to be calculated through the division of the total room revenue and also from the total

number of rooms which are available in the given time period. For example the total number of

rooms which are there in a hotel are, 250 for which the occupancy rate is give at 95%. Average

cost which is incurred by the hotel for a single room is £800 therefore this helps in the

calculation of RevPAR = per night cost multiplied by occupancy rate.

= (800*95%)

= £760.00

This calculation of the revenue of the per available room assumes that all the rooms have

same price.

Average Rate Index :

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Average Rate Index (ARI) is a index used in the hotel industry which shows the

comparison of the rates with the other hotels. It is considered to be very helpful in the

determination of the ways in which the firm can increase or decrease the rates. Formula of ARI

= Organizations ADR/ Competitors Average ADR

For example,

Given

Competitors ADR = 500

Room Revenue =£55000

Total Number of Rooms = 100

Organizations ADR = (55000/100)

=550

Therefore,

ARI = 550/500

=1.1

This rate shows greater than 1 which indicates that the hotel's average prices is higher

than that of its competitors.

Market Penetration Index :

This unit is considered to be the measurement of the hotel's occupancy which helps in the

comparison of the preselected set of competitors (Nyoman and et.al., 2019). This is considered to

be very helpful for showing the business and its relations with the competitors and in the market.

Formula for calculating this is MPI = Your occupancy rate / selected set of Competitors

occupancy rate,

For example, Occupancy rate is given at 95% and the set of competitors have the occupancy rate

of 90%.Therefore,

MPI= 95%/90%

= 1.055555556

Customer Satisfaction :

Customers satisfaction is considered to be the known as the measurement of the

happiness of the customers and its products, services and capabilities. It can be said that the

customer's satisfaction is known as the inclusion of surveys and ratings which helps the company

in the determination of the way of improving the hospitality services. The customer's satisfaction

comparison of the rates with the other hotels. It is considered to be very helpful in the

determination of the ways in which the firm can increase or decrease the rates. Formula of ARI

= Organizations ADR/ Competitors Average ADR

For example,

Given

Competitors ADR = 500

Room Revenue =£55000

Total Number of Rooms = 100

Organizations ADR = (55000/100)

=550

Therefore,

ARI = 550/500

=1.1

This rate shows greater than 1 which indicates that the hotel's average prices is higher

than that of its competitors.

Market Penetration Index :

This unit is considered to be the measurement of the hotel's occupancy which helps in the

comparison of the preselected set of competitors (Nyoman and et.al., 2019). This is considered to

be very helpful for showing the business and its relations with the competitors and in the market.

Formula for calculating this is MPI = Your occupancy rate / selected set of Competitors

occupancy rate,

For example, Occupancy rate is given at 95% and the set of competitors have the occupancy rate

of 90%.Therefore,

MPI= 95%/90%

= 1.055555556

Customer Satisfaction :

Customers satisfaction is considered to be the known as the measurement of the

happiness of the customers and its products, services and capabilities. It can be said that the

customer's satisfaction is known as the inclusion of surveys and ratings which helps the company

in the determination of the way of improving the hospitality services. The customer's satisfaction

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

cannot be measured in quantitate form however, Organizations are able to measure it through

analysing the customer they have retained. For example,

Formula for calculating Cs= (The total number of 4 of 5) / number of total respondents *100%

In the given case there are 72 out of 100 responses given, if the average response from

the customers rating is of 4 of 5 the its is at 80%, thus, it can be said that the majority of the

customers are satisfied.

analysing the customer they have retained. For example,

Formula for calculating Cs= (The total number of 4 of 5) / number of total respondents *100%

In the given case there are 72 out of 100 responses given, if the average response from

the customers rating is of 4 of 5 the its is at 80%, thus, it can be said that the majority of the

customers are satisfied.

REFERENCES

Books and Journals

Bazot, G., 2018. Financial consumption and the cost of finance: Measuring financial efficiency

in Europe (1950–2007). Journal of the European Economic Association. 16(1). pp.123-

160.

Hillman, D., and et.al., 2018. The economic cost of inadequate sleep. Sleep. 41(8). p.zsy083.

Horton, A., 2021. Liquid home? Financialisation of the built environment in the UK’s “hotel‐

style” care homes. Transactions of the Institute of British Geographers. 46(1). pp.179-

192.

Lavrador, A.M.S. and Laureano, R.M., 2019, June. Dashboard to monitor performance of an

hotel in the financial perspective. In 2019 14th Iberian Conference on Information

Systems and Technologies (CISTI) (pp. 206-211). IEEE.

Nowak, J., and et.al.,2019, September. Differences in the Cost Calculation for Construction

Work, Road Transport and Water Supply. In IOP Conference Series: Materials Science

and Engineering (Vol. 603, No. 3. p. 032086). IOP Publishing.

Nyoman, A.N., and et.al., 2019. DEVELOPING OF SALES ACCOUNTING MODEL HOTEL

SUPPLIER ON GROWTH OF BUSINESS REVENUE. International Journal of

Applied Sciences in Tourism and Events. 3(2). pp.122-130.

Tanaka, G.M.P. and Respati, H., 2021. Cost of Inventory Calculation Analysis Using The Fifo

and Lifo Methods. Economic Research. 5(4). pp.109-120.

Xuyun, B.A.I., Yan, G.U.O. and Xiaotian, W.A.N.G., 2020, December. Measurement of Hotel

Service Quality Based on Online Comment Sentiment Analysis. In 2020 Eighth

International Conference on Advanced Cloud and Big Data (CBD) (pp. 89-95). IEEE.

Online

Selling and Distribution Overhead: Meaning, Accounting Treatment and Control, 2020[Online].

Available through: <https://www.yourarticlelibrary.com/accounting/overheads/selling-

and-distribution-overhead-meaning-accounting-treatment-and-control/74477#:~:text=(d)

%20Percentage%20of%20Selling%20Price%3A&text=For%20example%2C%20if

%20fixed%20selling,00%2C000%20x%20100)%20on%20sales.>

Books and Journals

Bazot, G., 2018. Financial consumption and the cost of finance: Measuring financial efficiency

in Europe (1950–2007). Journal of the European Economic Association. 16(1). pp.123-

160.

Hillman, D., and et.al., 2018. The economic cost of inadequate sleep. Sleep. 41(8). p.zsy083.

Horton, A., 2021. Liquid home? Financialisation of the built environment in the UK’s “hotel‐

style” care homes. Transactions of the Institute of British Geographers. 46(1). pp.179-

192.

Lavrador, A.M.S. and Laureano, R.M., 2019, June. Dashboard to monitor performance of an

hotel in the financial perspective. In 2019 14th Iberian Conference on Information

Systems and Technologies (CISTI) (pp. 206-211). IEEE.

Nowak, J., and et.al.,2019, September. Differences in the Cost Calculation for Construction

Work, Road Transport and Water Supply. In IOP Conference Series: Materials Science

and Engineering (Vol. 603, No. 3. p. 032086). IOP Publishing.

Nyoman, A.N., and et.al., 2019. DEVELOPING OF SALES ACCOUNTING MODEL HOTEL

SUPPLIER ON GROWTH OF BUSINESS REVENUE. International Journal of

Applied Sciences in Tourism and Events. 3(2). pp.122-130.

Tanaka, G.M.P. and Respati, H., 2021. Cost of Inventory Calculation Analysis Using The Fifo

and Lifo Methods. Economic Research. 5(4). pp.109-120.

Xuyun, B.A.I., Yan, G.U.O. and Xiaotian, W.A.N.G., 2020, December. Measurement of Hotel

Service Quality Based on Online Comment Sentiment Analysis. In 2020 Eighth

International Conference on Advanced Cloud and Big Data (CBD) (pp. 89-95). IEEE.

Online

Selling and Distribution Overhead: Meaning, Accounting Treatment and Control, 2020[Online].

Available through: <https://www.yourarticlelibrary.com/accounting/overheads/selling-

and-distribution-overhead-meaning-accounting-treatment-and-control/74477#:~:text=(d)

%20Percentage%20of%20Selling%20Price%3A&text=For%20example%2C%20if

%20fixed%20selling,00%2C000%20x%20100)%20on%20sales.>

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.